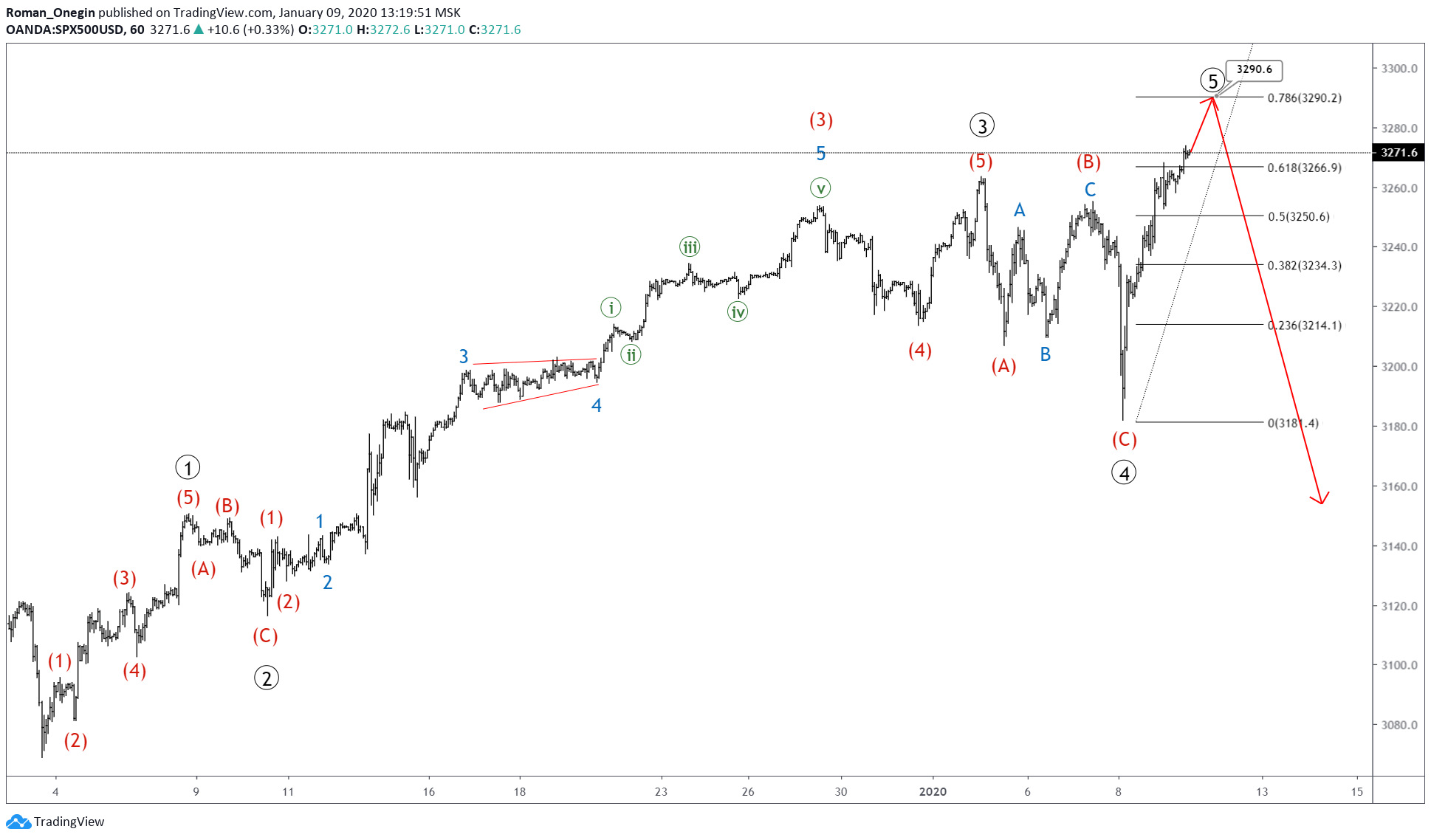

Most Asian stocks are seeing out the week on a positive note, after the S&P 500 notched a new record high. Despite the recent US and Iran airstrikes, risk appetite has been largely restored, with USDJPY advancing some 1.3 percent so far this week, while Gold has erased all of its gains this week to trade below the psychological $1550 level.

Investors have been emboldened by signs that both the US and Iran are backing away from the brink of an all-out war. The flare-up in the Middle East was the latest reminder for investors to remain vigilant over geopolitical risks. It remains to be seen whether this is merely a lull in what could be a protracted action-reaction cycle between the US and Iran; such a risk may have to be factored into investors’ respective asset allocation strategies.

Still, the diminished risks of a near-term escalation in the US-Iran conflict mean that market participants can refocus their attentions on the US-China “phase one” trade deal which is set to be signed in the week ahead. The key detail would be the timing of the expected rollback in tariffs. The lowering of these barriers to trade, sooner rather than later, should give the global economy more time to recover and provide cause for investors to add exposure to riskier assets, including those in emerging markets.

Positive surprise in US jobs data to spur Dollar on

The Dollar index (DXY) has now climbed one percent so far in 2020, trading back above 97.4 in the lead up to the December non-farm payrolls (NFP) release. Markets are currently pricing in an NFP print of 160,000, and such a figure would underscore the job market’s resilience as US consumers are being relied on to maintain the growth momentum in the world’s largest economy.

Positive surprises in the headline NFP, wage growth, or average hourly readings could see the Dollar index closing in on its 200-day moving average of 97.706 and stall its downward trend. However, considering that the DXY has been posting lower lows since October, the US Dollar is expected to moderate further, as long as risk-on sentiment remains uninterrupted and the Fed stands pat on US interest rates.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

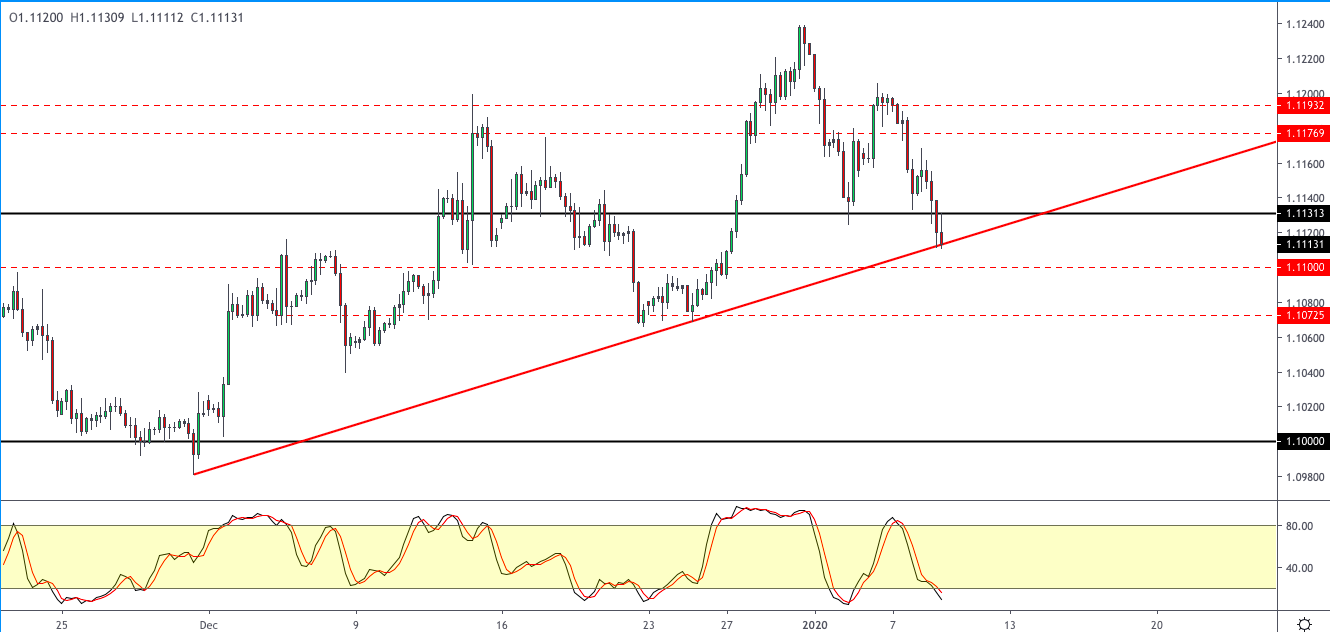

On Thursday, January 9, the euro was up one point at the close of trading. The price consolidated at 1.1105, in a narrow range. It was business as usual after President Trump’s speech on Wednesday, as the markets braced themselves ahead of the publication of the US Non-Farm Payrolls report, scheduled for later on today.

16:30 USA: Nonfarm Payrolls (Dec), Average Hourly Earnings (YoY) (Dec), Labor Force Participation Rate (Dec).

21:00 USA: Baker Hughes US Oil Rig Count.

Current situation:

The price did not recover to 1.1130, as predicted. In fact, it was in a horizontal range of 1.1100-1.1120. In six hours, we can expect the price will meet with the balance line. When this happens, the market will be ripe for sharp fluctuations to occur.

Today, the focus is on the US Non-Farm Payrolls report. It is predicted that employment increased by 164,000 in December, compared with an increase of 266,000 in November, while the unemployment rate stayed around 3.5%. The indicator for jobs is unpredictable, therefore, has a strong influence on the main pairs. On days like this, it is better to refrain from making forecasts. Although technically, the pair is ready to decline.

Trump tweeted that he would sign the trade agreement with China on January 15, the ceremony will take place at the White House with senior Chinese figures in attendance. Chinese Deputy Prime Minister Liu He, who leads the country’s negotiating delegation with the US, will be in Washington on January 13-15.

US stock market rally resumed on Thursday as US-China trade deal came into forefront anew. The S&P 500 gained 0.7% to new record 3274.70. The Dow Jones industrial average advanced 0.7% to fresh record 28956.90. Nasdaq composite index rallied 0.7% to record 9203.43. The dollar strengthening slowed as the number of people applying for first time jobless benefits slipped to 214,000 last week: live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.1% to 97.41 and is higher currently. Futures in stock indexes point to higher openings today.

DAX led European indexes rebound

European stocks extended gains on Thursday buoyed by strong German industrial data. The slide of both GBP/USD and EUR/USD continued yesterday with Pound turning higher currently while euro little changed. The Stoxx Europe 600 index ended 0.3% higher led by technology stocks. Germany’s DAX 30 rallied 1.3% to 13495.06 as data showed German industrial output rose above expected 1.1% over month in November after 0.1% decline the previous month. France’s CAC 40 added 0.2% and UK’s FTSE 100 rose 0.3% to 7598.12.

Australia’s All Ordinaries Index leads Asian indexes gains

Asian stock indices are mostly higher today. Nikkei ended up 0.5% at 23850.57 with yen slide against dollar slowing. Chinese stocks are mixed: the Shanghai Composite Index is down 0.08% while Hong Kong’s Hang Seng Index is 0.3% higher. Australia’s All Ordinaries Index extended gains 0.8% despite Australian dollar reversing its slide against the greenback.

Brent futures prices are extending losses today. Prices ended lower third session yesterday: March Brent crude slipped 0.1% to $65.37 a barrel on Thursday. Despite downward momentum in oil prices Saudi Aramco shares recovered most of losses incurred in previous three sessions Thursday: Aramco gained 2.34% to 35.50 riyals in Riyadh at Tadawul exchange.

Gold weakening dynamic while Dollar strengthens holds

Gold prices are edging lower after Wednesday’s loss. The price of an ounce of gold for February delivery fell 0.9% to $1,560.20 Wednesday as the dollar strengthening continued.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

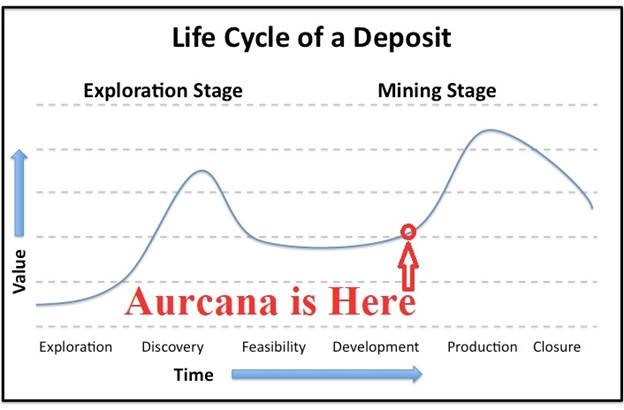

Bill Powers of Mining Stock Education sits down with Kevin Drover, CEO of Aurcana, to talk about the company’s production plans for its high-grade project in Colorado.

Aurcana Corporation (AUN:TSX.V; AUNFF:OTCQX) has 100% ownership of the world’s highest-grade silver mine (P&P): the Revenue-Virginius mine in Ouray, Colorado, USA. This fully permitted mine will also be one of the lowest-cost silver producers in the world at only US$8/oz Ag (AISC) after byproduct credits. Aurcana is currently (Q1 2020) securing the final capex needed to commence production, which it expects to accomplish in Q4 2020. In this interview, Aurcana CEO Kevin Drover provides an overview of the Revenue-Virginius mine and Aurcana’s investment value proposition.

Kevin Drover has over 40 years of both domestic and international experience. He was previously VP Worldwide Operations at Kinross Gold and possesses experience in all aspects of mining industry operations, process re-engineering, project development and corporate management.

Bill Powers: I would like to welcome Aurcana Corporation president and CEO, Kevin Drover. I’ve met Kevin at the last two Beaver Creek Precious Metals Summits and have been following the company and getting updates annually at the Precious Metals Summit. So, Kevin, it’s your first time on Mining Stock Education, welcome. Please begin provide an overview of this mine that I’ve referenced with the highest grade proven and probable silver reserves in the world?

Kevin Drover: Well, thank you, Bill. Yes, this mine, it’s located in Colorado in the San Juan Mountains near the town of Ouray, and it’s up at about 10,000 feet, in that range, and it is extremely high grade. Our Proven and Probable reserves are 21 million ounces at 37 ounces of silver equivalent per ton. And I don’t know of any other mine in the world, at least that I’m aware of, with a Proven and Probable reserve of that grade. And the exploration potential of this property is quite significant as well for the future.

Bill: And you own this project 100% outright?

Kevin: We own the project 100%. We own this one, and this mine is essentially fully built. It is fully permitted. There’s a feasibility study completed and it’s ready to go. Technically, there’s nothing left to do with this mine but to put it into production and we, of course, are seeking funding to do that now.

We also have a fully-permitted, fully-built mill in place, 1,500 ton a day mill, located at the Shafter Mine in Texas and that’s near the town of Marfa, Texas. It’s currently on care and maintenance, but at some point we will need to revisit that one as well. It needs some additional technical work and that’s not our focus right now. Our primary focus is to get the Revenue-Virginius mine back into production as soon as possible.

Bill: What are some of the highlights of the Revenue-Virginius mine? The feasibility study that you referenced?

Kevin: Well, first, maybe I can just step back a second and just talk about the resources and reserves. We have a Measured and Indicated resource of 30 million ounces at 30 ounces per ton. An Inferred resource, of course, which you cannot include in your feasibility study, but it’s still an Inferred resource of 13.2 million ounces at 40 ounces per ton and ,of course, our Proven and Probable reserves are 21 million ounces at 37 ounces per ton. Currently, it’s at six and a half year mine life, an average production rate of 3.1 million ounces per year. Our all-in sustaining cost of production after byproduct credits is $8 an ounce. If you look at byproducts and convert them to silver equivalent, our all-in sustaining cost is $10.71 per ounce, which is one of the lowest cost silver producers in the world by far.

Our pre-production capital needs are $37 million. We’ve recently raised approximately $7 million in August and September, so our needs are somewhat less than that $37 million on a go-forward basis. The NPV on this project at 5% using an $18.50/ounce silver price, which is not far from where we are today, is $75 million and the IRR is 71%. Time to production from full funding is seven months.

Bill: And of your total resource, what percentage of that is actually silver?

Kevin: Probably the best way to look at that would be from a revenue perspective and silver generates 71% of the revenue. Gold will produce 8% of the revenue, lead 15% and zinc 6%. There is some copper here, but it’s not a high enough grade to make sense for us to start up our copper circuit. We do have a copper circuit in the mill, but on some of the other veins that we have, we may look at producing a copper concentrate, but right now we won’t do that.

Bill: So you’re in Colorado, you have your permit, so there’s nothing on the environmental front or the permitting front that you have to worry about. The main hurdle here is just securing the funding in order to bring the mine into production?

Kevin: That’s correct. Yes. There’s no permits required whatsoever to go into production. Our environmental, social and government relations are excellent. Our guys down there have done a fantastic job with our environmental folks in that area and of course, we’re not far from Telluride, Colorado, and it’s a primary ski area, but the guys on the ground down there have done a fantastic job. We’ve had environmental groups to the site. We’ve had most of the senators, local county commissioners, mayor and such visit our site. We enjoy a good relationship with them.

We won the Colorado environmental stewardship award last year and we continue to pay a lot of attention to our health, safety, environmental, government and community relations. The community has been extremely supportive of us down there and so we continue to enjoy that and we want to make sure that that continues on into the future as we get up and running.

Bill: Kevin, is there anything more of pertinence regarding your treasury and how you might obtain this CAPEX money that you could share with investors?

Kevin: We’re looking for a debt facility at the moment and we’ve been somewhat successful. We’re going down the road on a couple of a different routes in terms of raising that. Gary Lindsey (Investor Relations) and I were recently through Europe and we have talked to a number of entities that appear to be interested in taking a deep look at this operation here.

So, we’re rather hopeful that we’re going to be able to find the funds, certainly within the next quarter, which is what we are targeting. And there will be a debt facility. We will do some more equity as well in the next little bit here, and between those two we think we’ll have sufficient funding to be able to fully restart the project.

Bill: What about expansion potential? Do you own the full strike length and are there other veins that you could potentially target to increase your resources?

Kevin: There are significant vein systems in this particular area. This is a very prolific area of the San Juan Mountains. Over the course of the last century and a half, there’s probably been thousands of mines in this region here. We are currently the only one with a mill that’s fully permitted and ready to go into operation.

The Virginius vein that we have is rather prolific. It’s the highest-grade vein, relatively cleanest and easiest to mine. It’s rather vertical. There was one area on the Virginius vein and basically one claim that we didn’t own that interrupted our ownership of the Virginius vein. We’ve recently acquired that vein and signed an agreement. The closing of that should be relatively soon, within the next month or thereabouts. And that is contiguous to our operation where we’re actually going to be first restarting the mining.

We intend this coming spring to do a drill program on that. This is one area up there that you can drill from surface, for the most part. There are no other areas that you can really drill from surface in this particular area. So, we’re pretty excited that we’ve been able to acquire that claim and that we will start a drill program. The goal of this drill program will be to add another couple of years of mine life to the operation along with the target that we already have as we develop the underground mine up toward the Monongahela, which is the area where we will be mining first.

Bill: And typically, with these underground mines in Colorado in the mountains, you kind of have that six to eight-year runway and then you keep that six to eight-year runway often, don’t you, as you just drill and expand?

Kevin: That’s absolutely correct. These narrow vein mines, I mean they’re narrow vein, but they’re very high grade of course and almost impossible to drill from surface and in order to drill them from underground, you actually have to do a significant amount of development in order to get yourself in a position where you can access the vein so you can point your drill in the right direction. And it’s very, very costly. Not just this mine, but any narrow vein mine in the world.

For instance, I used to work for Dome Mines in Timmins, Canada. And Dome Mines was a mine that ran for 120 years and it had only about two years of reserves for those 120 years. So, nobody spends that huge amount of money upfront to put all of these reserves out in front of you when you know all you’re going to do is you follow the vein. Right now we have six and a half years. We believe within the next year to year and a half, we’ll have closer to 10 years. We’ll add a couple of years from this Blue Grass claim. We think we will convert some of our Inferred that’s underground and if you look on page 17 of our presentation (see chart below), you’ll see there the green area that’s outlined by the red. We believe we’ll convert that into Measured and Indicated within the next year and that as well will add about two years of reserve. So, we’re looking at close to 10 years of reserves by the time we really get into operation and that’s quite a long time in the narrow vein environment.

Bill: Kevin, we’ve mentioned some of the unique factors and highlights of the Revenue-Virginius Mine, but are there any other market comparables that you could point out for investors?

Kevin: Yes. As a matter of fact, there are. If you were to go in our presentation to page 20 (see chart below), probably the best one to look at is the comparable valuations of enterprise value to M and I resource, silver equivalent ounces. And if you look there, you’ve got Excellon, Great Panther, Alexco, Endeavour and Aurcana. And if you look at that, we’re at 45 cents per enterprise value per silver equivalent ounce. You look at Endeavor, they’re at $1.17, Alexco, which probably is more comparable to us, they’re not operating at this stage of the game. I believe they’re still waiting on one permit and they’re at $1.34. I think what this chart tells you is that you can you buy a dollar stock here for about 30 cents as of today.

Bill: Are there any other monetization opportunities within the company? Assets that you could sell to self-fund?

Kevin: Yes, there are. And we have some options in that regard. As I said at the outset, the Shafter project is certainly not core to us. We’ve had some offers to purchase. We’ve had some offers to purchase just the milling facility itself. The mill is designed for 1,500 tons a day. We see Shafter more as a 500-600 ton a day operation in the future. So, the mill is probably not the right mill to start with and I certainly believe we could monetize the mill. We may or may not do that, but it is one of our options that we do have here.

Bill: Please share a little bit about your background and what makes you qualified to advance this project?

Kevin: I’ve been doing this for close to 45 years, I guess. At this stage, I’ve worked in most places around the world. My background is in operations. I work with Kinross as Vice President of Operations. Ran six of their mines in the Northern Hemisphere around the world for a number of years. Spent a lot of time in Russia. Built mines, restarted mines in countries like Nicaragua, Costa Rica, Peru, Russia, United States, Canada, and I’ve been doing this a very long time and I guess if there’s one claim to fame from my perspective, is that what I’ve typically done most of my life has gone into operations. I restarted them and get the production going, get the cost down, and those things are the focus that we have here, is we get ourselves funded, we will get this thing restarted, we will control our costs. We don’t have any control over the price of the metal that we sell. What we do have control over is how we operate and how we spend our money and we’re going to spend it very, very wisely going forward.

Bill Powers is the host of the Mining Stock Education podcast that interviews many of the top names in the natural resource sector and profiles quality mining investment opportunities. Powers is an avid resource investor with an entrepreneurial background in sales, management and small business development. His latest interviews can be found at MiningStockEducation.com.

Disclosure: 1) Bill Powers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Aurcana Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Aurcana Corp. is a Mining Stock Education advertiser. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The content produced by Bill Powers and Mining Stock Education LLC is for informational purposes only and is not to be considered personal, legal or investment advice or a recommendation to buy or sell securities or any other product. It is based on opinions, public filings, current events, press releases and interviews but is not infallible. It may contain errors and we offer no inferred or explicit warranty as to the accuracy of the information presented. If personal advice is needed, consult a qualified legal, tax or investment professional. Do not base any investment decision on the information contained on MiningStockEducation.com, our podcast or our videos. We usually hold equity positions in and are compensated by the companies we feature and are therefore biased and hold an obvious conflict of interest. MiningStockEducation.com may provide website addresses or links to websites and we disclaim any responsibility for the content of any such other websites. The information you find on MiningStockEducation.com is to be used at your own risk. By reading MiningStockEducation.com, you agree to hold MiningStockEducation.com, its owner, associates, sponsors, affiliates, and partners harmless and to completely release them from any and all liabilities due to any and all losses, damages, or injuries (financial or otherwise) that may be incurred.

Applied Therapeutics’ shares traded 25% higher today after the company reported positive topline results from its Pivotal Phase 2 ACTION Study of AT-007 for use in the treatment of galactosemia. The firm expects to file for regulatory approval of AT-007 in H2/20.

This morning, New York City-based clinical-stage biopharmaceutical company Applied Therapeutics Inc. (APLT:NASDAQ)announced “positive topline results from the Pivotal Phase 2 portion of the ACTION-Galactosemia study of AT-007, a central nervous system (CNS) penetrant Aldose Reductase inhibitor, in adult Galactosemia patients.”

The company explained in the report that “Galactosemia is a rare metabolic disease that affects how the body processes a simple sugar called galactose, and for which there is no known cure or approved treatment available.”

The firm stated that the ACTION study is a double-blind trial evaluating the effects of AT-007 in healthy adult Galactosemia patients, and noted that the “key biomarker outcome of the study was reduction in galactitol, an aberrant toxic metabolite of galactose, formed by Aldose Reductase in Galactosemia patients.”

According to the report, the data from the study showed that the AT-007 treatment resulted in a statistically significant and robust reduction in plasma galactitol versus placebo in adult Galactosemia patients and that reductions in galactitol were dose dependent. The company indicated that AT-007 was well tolerated, with no drug-related adverse events reported in the 72 healthy volunteers treated in the first part of the trial or in Galactosemia diagnosed patients. Applied Therapeutics believes that AT-007 represents a potentially compelling new therapeutic option for patients with Galactosemia and stated that it expects to file for regulatory approval for the drug in H2/20.

The company’s Chief Medical Officer Riccardo Perfetti, MD, PhD, commented, “We are thrilled with these results…Galactosemia is a devastating disease with no treatments currently available. We have long known that dietary restriction alone does not prevent chronic complications of disease. These results provide hope for patients and families that action through drug treatment with AT-007 can potentially change the course of the disease, transforming patients’ lives.”

Shoshana Shendelman, PhD, founder, CEO and chair of the Board of Applied Therapeutics, added, “The Galactosemia program is an example of our overall strategy to apply technological breakthroughs to areas of high unmet need…By employing new regulatory pathways and using biomarkers early in development, we are able to bring critical drugs to patients who desperately need them quickly and effectively. The ACTION-Galactosemia data presented today is our first pivotal study readout – but it’s just the beginning. We are continuing to advance our pipeline of novel drug candidates in other disease indications and look forward to sharing additional successful data readouts in the future.”

Applied Therapeutics is headquartered in New York, N.Y., and describes its business as “a clinical-stage biopharmaceutical company developing a pipeline of novel drug candidates against validated molecular targets in indications of high unmet medical need.” In addition to AT-007, the company is developing another lead drug candidate, AT-001, a novel aldose reductase inhibitor that is being developed for the treatment of Diabetic Cardiomyopathy, a fatal fibrosis of the heart.

Applied Therapeutics has a market cap of approximately $484 million with about 18.52 million outstanding shares. APLT shares opened more than 20% higher today at $31.75 (+$5.59, +21.37%) over yesterday’s closing price of $6.16 and the company’s stock achieved a new 52-week high price this morning of $40.141. The stock has traded today between $31.00 and $40.141 per share and is presently trading at $33.00 (+$6.84, +26.15%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

In this interview with Maurice Jackson of Proven and Probable, Exploration Insights’ Brent Cook discusses the value of site visits to determining the potential of a prospect, and offers insights into various metals markets.

Maurice Jackson: Joining us for conversation is Brent Cook. He’s the founder of the highly regarded Exploration Insights. Mr. Cook, you’re one of the most trusted, highly regarded names in the natural resource space, so it’s a real pleasure to be speaking with you today sir.

Today we will address the positives and negatives for the mining sector in 2020. Sir, from a macro perspective, please share with us what is your view on the current state of the mining sector?

Brent Cook: For my colleague Joe Mazumdar and me, the overriding issue that the mining sector faces is they’re just not finding enough economic metal deposits to replace what’s been mined. To put that into terms that might make sense, we are producing on a global scale, 90 million ounces a year, which is about what’s come out of the Carlin Trend in Nevada since 1980. We’re not finding 90 million ounces a year. Ditto for copper. We’re burning through one Bingham Canyon deposit just outside of Salt Lake a year. We’re not putting in production one of those a year. So that’s the real issue they face. It’s real positive for those of us in the exploration sector.

Maurice Jackson: Speaking of positives, are there any catalysts that you see that will enhance the value propositions of companies in 2020?

Brent Cook: Well, certainly metal prices. We expect gold to do well, platinum, palladium, nickelbut the lack of production we really see as the catalyst for the metal prices.

Maurice Jackson: And where do you see the best value propositions in 2020? Is it the precious metals or is it the base metals?

Brent Cook: We’re going with precious metals for a lot of reasons, from a shortage of deposits, to global geopolitical risks that keep increasing with every threat, to global debt. There’s just so much going on that I think gold is going to act as a safe haven more and more.

Maurice Jackson: And regarding base metals, which base metals have your attention and why?

Brent Cook: Copper for the future is certainly something that’s going to be in deficitthe demand for copper with the increase with electric vehicles, electrification, green energy, etc. So copper, further down the road. Right now, probably the one base metal we’re most interested in is nickel. Fortunately or unfortunately, there’re not many decent nickel plays out there, so nickel is a good one. Palladium, I think, is also going to do well again this year. So those are the base metals we’re sticking with. Zinc, lithium, lead; sort of so-so on those.

Maurice Jackson: I’d be remiss if I didn’t ask you about uranium.

Brent Cook: Not keen on the uranium price, per se. I started off the business in the uranium industry, working in the Colorado Plateau, and I’ve done work in Australia and Africa as well. There is no shortage of uranium out there. It’s just waiting on an increase in the price. So I don’t see uranium as a good investment.

Although, having said that, we recently purchased Energy Fuels (NYSE: UUUU), just based on the potential for the U.S. to start stockpiling uranium bought from U.S. uranium producers, which requires about a $5060 a pound price for them to even break even or make money. So there’s that play, but that’s not really a play on uranium. It’s more a play on a political event.

Maurice Jackson: Speaking of that political eventSection 232? Do you think it will pass?

Brent Cook: I honestly, give it a 50/50 chance. I think it’s a dumb idea. There’s no shortage of uranium in the world, and it doesn’t make sense for the U.S. government to subsidize industries like that. Having said that, anything could happen.

Maurice Jackson: Moving on to physical precious metals: You alluded to gold earlier, and palladium. What are your thoughts on platinum, and silver, and rhodium?

Brent Cook: Platinum is not used as much as palladium, so I don’t think it’s got that much of an upside to it. Rhodium is such a small market, we don’t even consider it. I think the price is great, but there’s no rhodium deposits. It all comes with the platinum group metal mining anyway. I mean, there’s no way to play, in my mind, rhodium.

Maurice Jackson: And if you don’t mind me asking, because readers like to follow your work. . .what are you buying at the moment, as far as physical precious metals? Or are you buying anything at all?

Brent Cook: I’ve got some physical goldcoins, basically, I store in a safe deposit box in two countries, just in case. And I don’t own a lot of precious metals, personally.

Maurice Jackson: Moving onto Exploration Insights. Sir, you run one of the most successful newsletters in the space. For someone not familiar with your work, please introduce us to Exploration Insights.

Brent Cook: Love to. I bought Exploration Insights from Paul Van Eaton back in early 2009, as everything was collapsing, and I switched over. His was more of a macro picture sort of thing. And I did the geology forum, so I rebranded it Exploration Insights. The letter’s basically about what. . .I was buying and selling and seeing in the metals exploration market.

Recently, I brought on Joe Mazumdar, who is an extremely smart economic geologist who worked and studied in Australia, Argentinabasically all over the world, including Canada and the U.S. It’s now his letter, and so he writes almost all of the letter. He and I communicate back and forth. I’m sort of a senior advisor there. The letter is about what he is buying, selling and seeing in the exploration industry.

We make no money from companies. Everything we make is based on subscriptions and how we do in terms of our purchases. And it’s pretty technical. That’s a positive and a negative, because sometimes we get pretty far in the weeds explaining what exactly is happening in terms of the geology, the metallurgy, the geopolitics, all that sort of thing. We get pretty heavy into the weeds, but it’s our money, so we don’t want to make any mistakes, or as few as possible.

Maurice Jackson: Prior to this interview, you shared with me that if you’re going to be in the space, the importance of attending site visits, specifically on early-stage exploration and development projects. Please share why access to site visits are paramount for speculators in the natural resource space.

Brent Cook: You go to the shows or you sit down with a company’s investor relations person, and you go through the, “It all looks great. Here’s the geology. This looks just like this deposit over here, which is a $1 billion company. We’ve got this project that looks the same, it just hasn’t been drilled. We’re going to drill it and we’re going to find a billion-dollar deposit,” or something like that. But the reality is only maybe 1 in 10,000 prospects turns into an economic mine.

It’s important to realize that an economic deposit is a unique geological event, and to go there and see it with knowledgeable eyes. I’ve been doing this for almost 35, 40 years, and Joe has been doing it for 30, all over the world. To go and look at these projects with your eyes and experience that you’ve gotten from previous work you’ve done, you see things that you might not see in those flip books.

For instance, I remember one project in Mexicogreat trench, I think it was like, 40 meters of six grams. Looked fantastic on paper. You get there and the things sits in the bottom of a canyon, and there’s no way it’ll ever be a mine.

I can think of a lot of examples like that, where you get there and go, “Wait a minute, this isn’t going to work.” We were in Colombia, another project; sounded really good. Got there, and there was this beautiful, little, white church sitting on top of the hill that they want to mine. Well, that isn’t going to happen.

On site visits you are able to see things like that. I’ll give you one more. I was in Peruagain, a high-sulphidation epithermal discovery. The theory was that a later, volcanic rock had covered up the deposit, and all what we were seeing was a small window into what was below. Sounded great. Went and looked at itactually, what happened was that they had misinterpreted, and the small window was in fact a small crack, and the rest of the rock was the same rock that hadn’t been altered. It’s about just those things you see on the ground that you don’t necessarily get on the website or out of the flipbook.

Maurice Jackson: On average, how many site visits do you attend?

Brent Cook: I think last year Joe and I visited 33 projects. So quite a few. We’re trying to slow down, but you know how it goes.

Maurice Jackson: So if I, as a speculator, don’t have access to site visits, I can gain access through Exploration Insights?

Brent Cook: Most definitely. I mean, again, I think if mining and exploration is not your expertise, it really is critical, especially in the early-stage exploration stuff, to have someone that you trust and can give you insights into the companies. Now, this could be a broker that you trust, or a relative who’s in the industry, that sort of thingor a newsletter. I personally think ours is one of the best in terms of technical detail and thatI mean, you’ve got two economic geologists writing it. So I really think it’s a big help to have expert advice if this isn’t your area of expertise.

But the rewards are huge. I mean, as you know, you can take a $0.20 stock to two bucks within a couple of weeks with a discovery, or vice versa. You can take a $2 stock to $0.20 if something goes wrong. And that’s the key. We spend a lot of time looking for that fatal flaw ahead of the market.

Maurice Jackson: And you have a proven pedigree of success. In closing, sir, what keeps you up at night that we don’t know about?

Brent Cook: Someone’s tweets (laughter).

Maurice Jackson: Someone, huh? No particular name there (laughter).

Brent Cook: It’s pretty crazy out there. And I guess in terms of the mineral industry and mining, that is it. I mean, one geopolitical event can just trash the marketthe larger markets or the smaller marketsor make them go up. I mean, just this week we’ve seen gold jump $5060 bucks? And who would’ve thought that was going to happen last week?

So it’s those sorts of things. . .It’s the unforeseeables, the black swans that hit you that you really can’t know. And I think the best way to avoid thatwhat we try and dois if we’re into a project or a company that has a legitimate play, a legitimate deposit that we think will make money, at least we’ve got some founding, some basis for owning it, as opposed to just betting on the metal price or betting on what’s the greater fool theory. We prefer to sell to someone smarter than us than someone dumber than us. I guess that’s our game plan, which means we try and get into projects that a major mining company will buy.

Maurice Jackson: Last question, sir. What did I forget to ask?

One more thing, Maurice. Joe just finished our year-in New Year review, and he’s putting together an article, I guess, if you will, that would be free to any of the readers. Just go to our website, www.explorationinsights.com, and contact us and we’ll send that along for free.

Maurice Jackson: Before you make your next bullion purchase, make sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs, and private blockchain-distributed ledger technology. Call me directly at (855) 505-1900, or you may e-mail [email protected]. Last but not least, please subscribe to www.provenandprobable.com for mining insights and bullion sales.

Brent Cook of Exploration Insights, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Statements and opinions expressed are the opinions of Maurice Jackson and not of Streetwise Reports or its officers. Maurice Jackson is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Maurice Jackson was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Israel’s central bank left its key interest rate steady at 0.25 percent, as expected, and confirmed its guidance that it “will be necessary to leave the interest rate at its current level for a prolonged period or to reduce it” to ensure inflation stabilizes around its the midpoint of its target range.

The Bank of Israel (BOI), which has maintained its rate since raising it in November 2018 for the first time since 2011, added its monetary policy committee “is taking additional steps as necessary to make monetary policy more accommodative,” a reference to its intervention in foreign exchange markets to weaken the strong shekel.

Israel’s shekel rose in 2019, prompting expectations last year the central bank would cut rates to stem further gains.

Instead, BOI in November opted to intervene in the foreign exchange markets to weaken the shekel and boost inflation and has bought more than $3.5 billion of foreign currency since Nov. 25, 2019.

In response to today’s policy decision, the shekel weakened 0.3 percent to 3.47 to the U.S. dollar after rising 8.3 percent in terms of an effective exchange rate in 2019, “a development that continues to make it difficult to return inflation to the target range,” BOI said.

Underlining the BOI’s dovish policy stance, its research staff lowered its forecasts for economic growth and inflation in 2020, and forecast the key interest rate would be between 0.25 percent and 0.1 percent in the coming year before gradually rising toward the end of 2021.

Israel’s inflation rate dropped to a lower-than-expected 0.3 percent in November from 0.4 percent in October and BOI lowered its forecast for inflation to be 1.0 percent in 2020, down from its previous forecast of 1.2 percent but up from 0.4 percent in 2019.

BOI targets inflation of 1.0 to 3.0 percent.

Economic activity in Israel last year was better than BOI had expected, with gross domestic product up an estimated 3.3 percent, on strong public and private consumption.

BOI lowered its forecast for 2020 growth to 2.9 percent from October’s forecast of 3.0 percent, and forecast 3.2 percent growth in 2021.

BOI said the government’s interim budget is expected to have a “markedly contractionary effect” in the first half of this year and there is continuing uncertainty about budgets after that.

“Global economic activity continues to slow, but its seems that the risks of a significant deterioration have declined in view of progress in the trade negotiations between the US and China and the results of the UK elections,” BOI said, adding additional monetary easing by major central banks “has reached its limits at this stage.”

The Bank of Israel issued the following press release:

“The Monetary Committee decides on January 9, 2020 to keep the interest rate unchanged at 0.25 percent

The inflation environment remains low. The November CPI was lower than expected, and inflation over the past 12 months is 0.3 percent. Inflation excluding energy and fruits and vegetables indicates a lower basic inflation rate than in previous months. In the coming months, inflation is expected to stay low, but most one-year expectations and forecasts remained near the lower bound of the target range.

Since the previous interest rate decision, the shekel has been relatively stable against the dollar, while most other currencies strengthened against the dollar. However, during 2019, the shekel strengthened by 8.3 percent in terms of the nominal effective exchange rate, a development that continues to make it difficult to return inflation to the target range.

Most indicators of economic activity point to continued solid growth in the fourth quarter, and the labor market remains tight. However, the interim budget is expected to have a markedly contractionary effect in the first half of 2020, and there is continuing uncertainty regarding budgetary policy thereafter. According to the Research Department’s staff forecast, growth is expected to slow somewhat in 2020.

Global economic activity continues to slow, but it seems that the risks of a significant deterioration have declined in view of progress in the trade negotiations between the US and China and the results of the UK elections. Inflation remains low, but it appears that the process of enhanced monetary accommodation by the major central banks has reached its limit at this stage.

The Monetary Committee’s assessment is that in view of the inflation environment in Israel, the monetary policies of major central banks, developments in the global economy and the risks to the domestic economy, and the development of the exchange rate, it will be necessary to leave the interest rate at its current level for a prolonged period or to reduce it in order to support a process at the end of which inflation will stabilize around the midpoint of the target range, and so that the economy will continue to grow strongly. Furthermore, the Committee is taking additional steps as necessary to make monetary policy more accommodative. The Bank of Israel continues to monitor developments in inflation, the real economy, fiscal policy, the financial markets, and the global economy, and will act to attain the monetary policy targets in accordance with such developments.

The inflation environment remains low. The CPI reading for November declined by 0.4 percent, a greater decline than expected, so that year over year inflation remained below the target range. In the past 12 months, inflation was 0.3 percent (Figure 1 in the attached file of figures), and inflation excluding energy and fruit and vegetables stabilized at a low level, which may indicate a lower basic inflation rate than in previous months (Figure 2). Inflation of nontradable goods prices remained moderate, in view of the slowdown in the increase of the housing component, and inflation in the prices of tradable goods remained negative, in view of the decline in energy prices and the appreciation of the shekel. Inflation is expected to remain low in the coming months, but most one-year forecasts and expectations remain around the lower bound of the target range (Figure 4). The Research Department’s staff forecast indicates that inflation in 2020 is expected to be 1 percent, 0.2 percent lower than in the previous forecast. Expectations derived from CPI financial contracts appear to have declined moderately in recent months. Medium-and long-term forward inflation expectations derived from the bond market remained largely stable since the previous interest rate decision, and have increased slightly in recent days (Figure 5). Since the previous interest rate decision, the shekel was relatively stable against the dollar, while most currencies strengthened against the dollar. However, over the course of 2019, the shekel strengthened by 8.3 percent in terms of the nominal effective exchange rate (Figure 6), which continues to make it difficult to return inflation to the target range.

Most indicators of economic activity show that in the fourth quarter, the economy continued to grow solidly. This is substantiated by the Business Tendency Survey for December and the Companies Survey for the fourth quarter (Figure 13), the Composite State of the Economy Index for November (Figure 14), and the Purchasing Managers Index. Goods exports were flat in October and November, while services exports continued to grow rapidly in October (Figure 15). In contrast, the Consumer Confidence Index declined in October and in November. The labor market remains tight: The unemployment rate remained low, while the employment and participation rates increased (Figure 17), and wage increases continue despite a moderate decline in the job vacancy rate and a halt in the increase in employee posts. The interim budget is expected to have a markedly contractionary effect in the first half of 2020, even in view of the path of government debt repayment, and uncertainty remains regarding budgetary policy thereafter and its implications for economic activity and inflation. According to the Research Department’s staff forecast, growth is expected to slow somewhat in 2020 as a result of the continued slowdown in world trade and the budgetary contraction. GDP is expected to grow by 2.9 percent, of which about 0.3 percentage points is due to the one-off effect of the start of natural gas production from the Leviathan field. In 2021, GDP is expected to grow by 3.2 percent.

Equity indices in Israel were relatively stable since the previous interest rate decision, despite equity market increases abroad. Long-term government bond yields declined since the previous interest rate decision, in contrast with the continued increase in yields in Europe and the US (Figure 8).

Home prices continued to increase moderately, and in the past year they have increased by 2.6 percent. The number of home purchases increased, led by first-home purchasers. Mortgage volume continued to expand, and mortgage interest rates continued to decline.

The global economy continues to slow, but several indicators point to a possible moderate improvement in the coming months. Forecasts by investment houses were stable regarding global growth in 2020 and 2021, following a long period of downward revisions in growth forecasts (Figure 20). With the exception of the United States, most fourth quarter country statistics indicated a continued slowdown in the growth rate, with the main weakness focused on manufacturing. The slowdown in world trade continues (Figure 21), but the risk of a significant worsening has declined in view of progress in trade negotiations between the US and China and the results of the UK election. Inflation remained lower than the central banks’ guiding targets (Figure 23), but it appears that the process of enhanced monetary accommodation by the major central banks has reached its limit at this stage. In the financial markets, the price increases in equity indices have continued (Figure 26). In the US, the Federal Reserve kept the federal funds rate unchanged, and signaled that the rate is expected to remain at its current level unless there is a significant change in the state of the economy. Growth surprised to the upside in the fourth quarter as well, and the trade agreement that is taking shape with China may contribute to a recovery in manufacturing. In Europe, growth remains moderate, mainly in Germany and Italy, and the manufacturing sector continues to weigh on activity. The ECB left its interest rate unchanged, and is expected to leave its policy in place for a long time. In Japan, leading indicators point to a slowing of growth in the fourth quarter, after the increase in VAT. Data on activity in China were positive, but the long-term trend of moderation continues. Oil prices increased in view of a reduction of supply and an expected increase in demand (Figure 24).

Equity markets resumed the rally following Iran’s response to the US attacks.

Investors remain hopeful that the tensions will not escalate too far.

This has resulted in the precious metal retreating amid a surge in risk appetite. Investors are also looking forward to this week’s payroll report.

Germany Factory Orders Slip in November

The latest factory orders in Germany saw a decline. Industrial orders fell 1.3% on the month beating forecasts of a 0.2% increase and a decline from 0.2% previously.

Trade balance figures from France were also weaker.

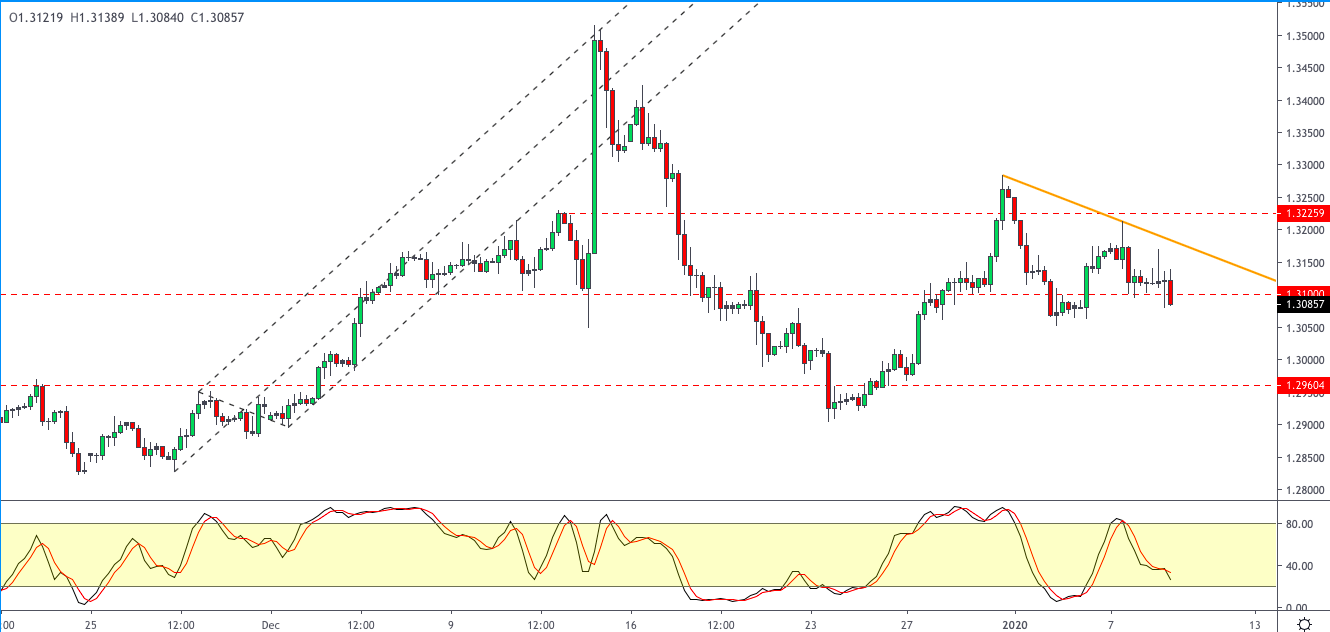

EURUSD Testing the Rising Trend Line

The common currency is currently testing the rising trend line. After the break down below the support level of 1.1131, this will be the next dynamic support. In the event of a break down below this trend line, the lower support at 1.1100 will be open for a retest. This potentially confirms the downside below 1.1131.

Sterling Under Pressure on Rising Dollar Strength

The pound is trading weaker amid a broader strength in the US dollar. The USD is rising for the second consecutive day. Economic data from the UK remains sparse in the meantime. Still, Brexit continues to remain the biggest risk for investors.

GBPUSD Forming into a Descending Triangle

The GBPUSD currency pair is currently threatening the 1.3100 level of support. If support breaks, we expect accelerated declines further. The minimum downside is at 1.2960. Alternately, to the upside, price action will need to break the minor falling trend line for any hopes of an upside bounce.

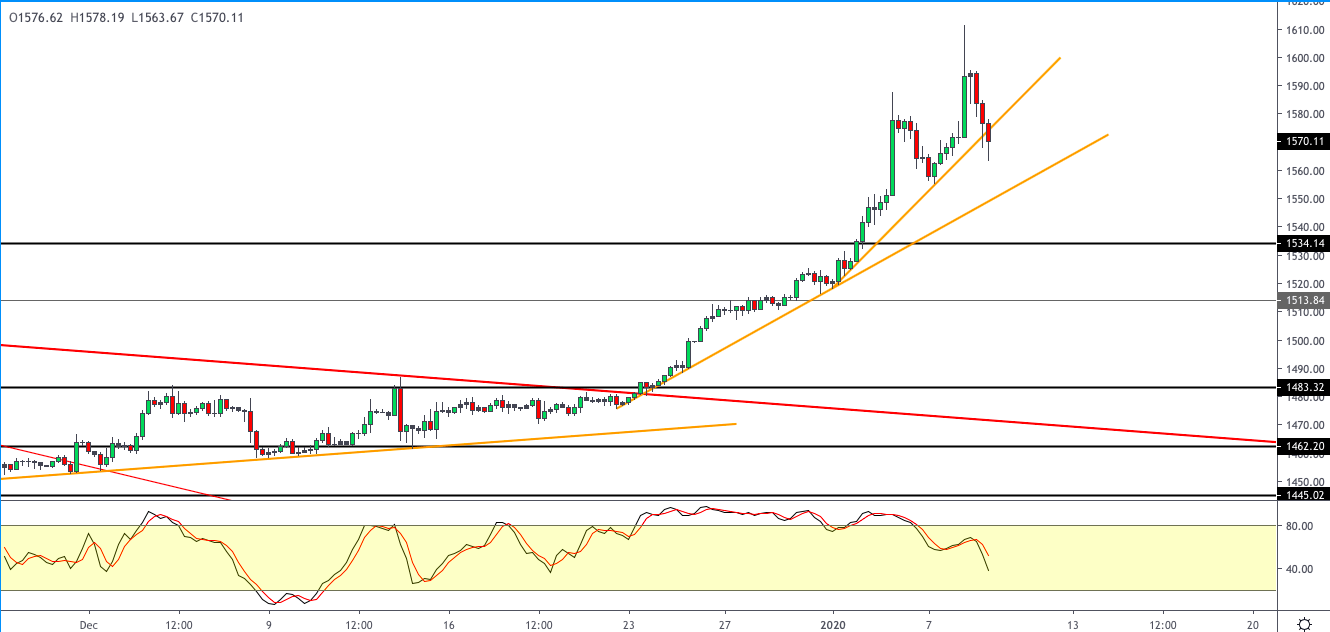

Gold Prices Fall as Risk Appetite Improves

The precious metal is retreating after a strong rally in the commodity. Falling tensions have made the safe haven less appealing. This would potentially mark a decline in gold prices. However, given the fact that there is potential for the middle east tensions to rise, it is possible that gold prices could snap back.

XAUUSD Could Post Declines in the Near Term

XAUUSD is posting declines and this is likely to see a retest of the previous lows near 1557.76. If this support breaks then prices could slip further. The next main support is at 1534.10. The upside bias remains as long as prices are supported above this level.

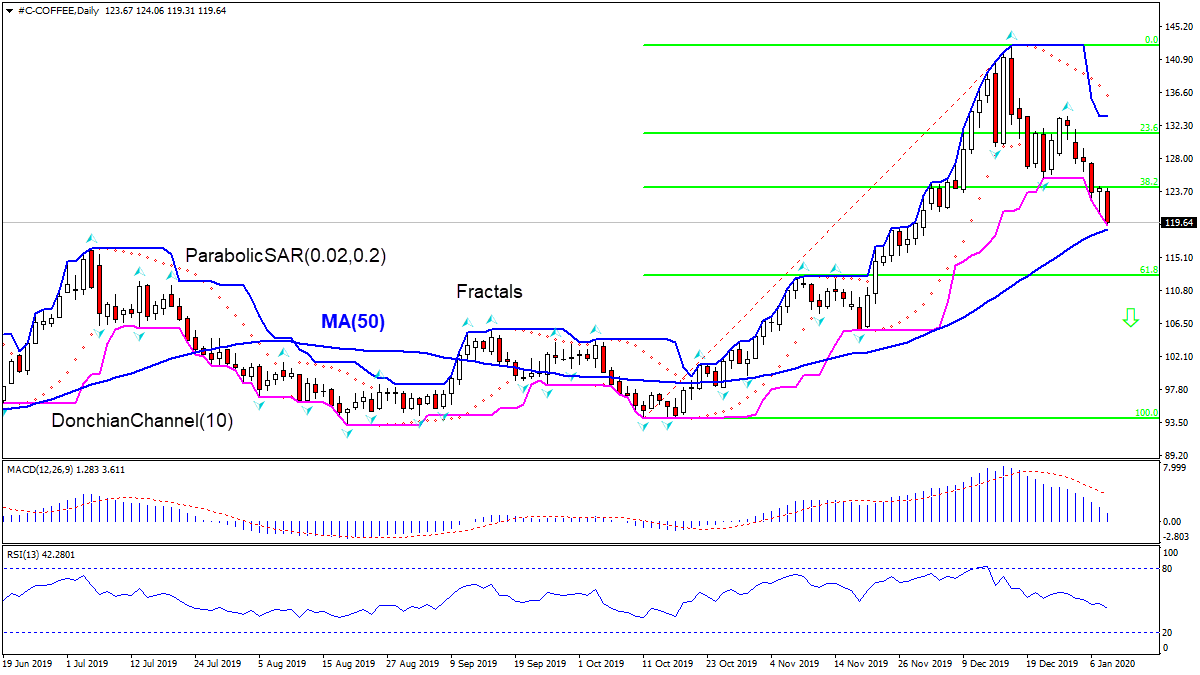

By IFCMarkets – Rising Brazil output bearish for coffee price

Coffee production in Brazil is forecast to rise this year. Will the coffee prices continue falling?

Brazilian farmers are expected to produce a record coffee crop in 2020. Brazil, world’s largest producer of coffee, produced a record 62.6 million bags in 2018, followed by 57.6 million bags in 2019. Analysts forecast increasing Brazil production for 2020. Thus, the Dutch bank Rabobank forecast a 2020 output at 66.7 million 60-kg bags a month ago, and the research arm of the University of São Paulo – Cepea, forecast “slightly” more than 60 mln bags a few days ago. Expectations of higher output by world’s top coffee producer is bearish for coffee. However International Coffee Organization forecast last month that world coffee production in 2019-20 marketing year will decline, resulting in a shortage of around 502,000 bags of coffee. Yesterday the ICO report stated global coffee output is estimated at 168.71 million bags in 2019/20, 0.9% lower than last year. A 4.1% decline in arabica production was stated as the main reason. Expectations of lower global production are an upward risk for coffee price.

On the daily timeframe the COFFEE: D1 is about to test the 50-day moving average MA(50) which is rising. Price has breached below Fibonacci 38.2 support level.

The Parabolic indicator gives a sell signal.

The Donchian channel indicates downtrend: it is widening down.

The MACD indicator gives a bearish signal: it is above the signal line and the gap is narrowing.

The RSI oscillator is falling but has not reached the oversold zone.

We believe the bearish momentum will continue as the price breaches below the lower Donchian boundary at 119.31. A pending order to sell can be placed below that level. The stop loss can be placed above the upper Donchian boundary at 133.50. After placing the order, the stop loss is to be moved every day to the next fractal high, following Parabolic signals. Thus, we are changing the expected profit/loss ratio to the breakeven point. If the price meets the stop loss level (133.50) without reaching the order (119.31), we recommend cancelling the order: the market has undergone internal changes which were not taken into account.