By IFCMarkets

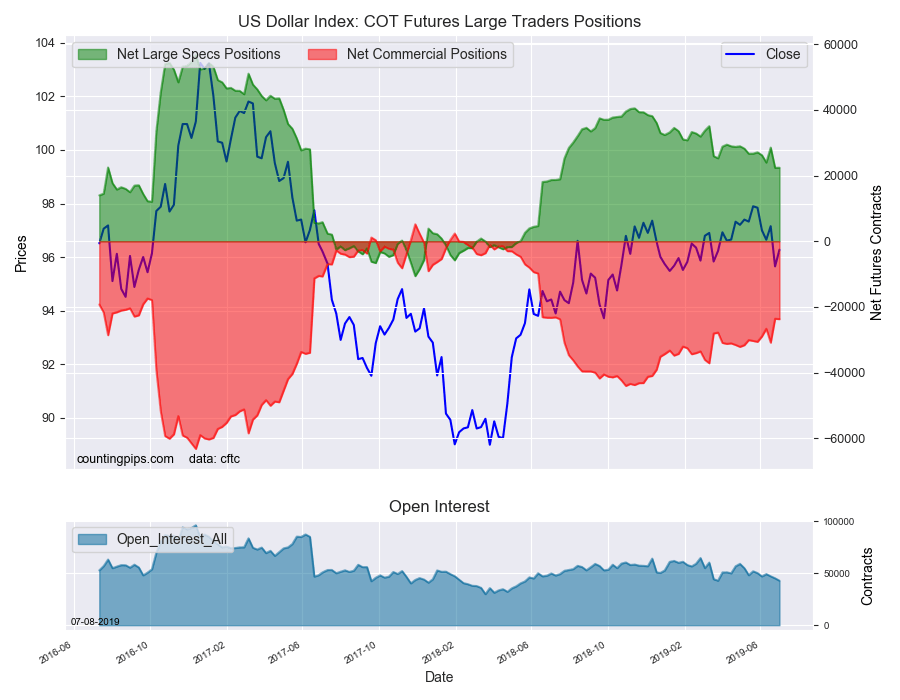

Dollar strengthening intact

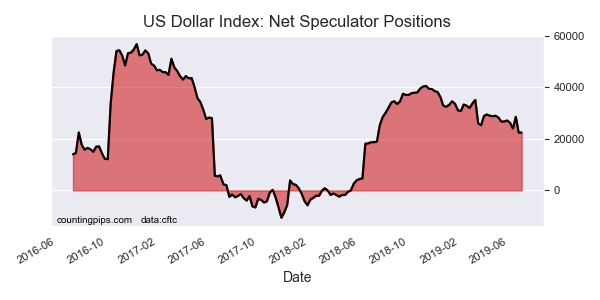

US stock market continued their retreat on Monday led by communication services and materials shares. The S&P 500 lost 0.5% to 2975.95. Dow Jones industrial slid 0.4% to 26806.14. The Nasdaq composite fell 0.8% to 8098.38. The dollar strengthening continued : The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.1% to 97.36 and is higher currently. Stock index futures point to lower market openings today

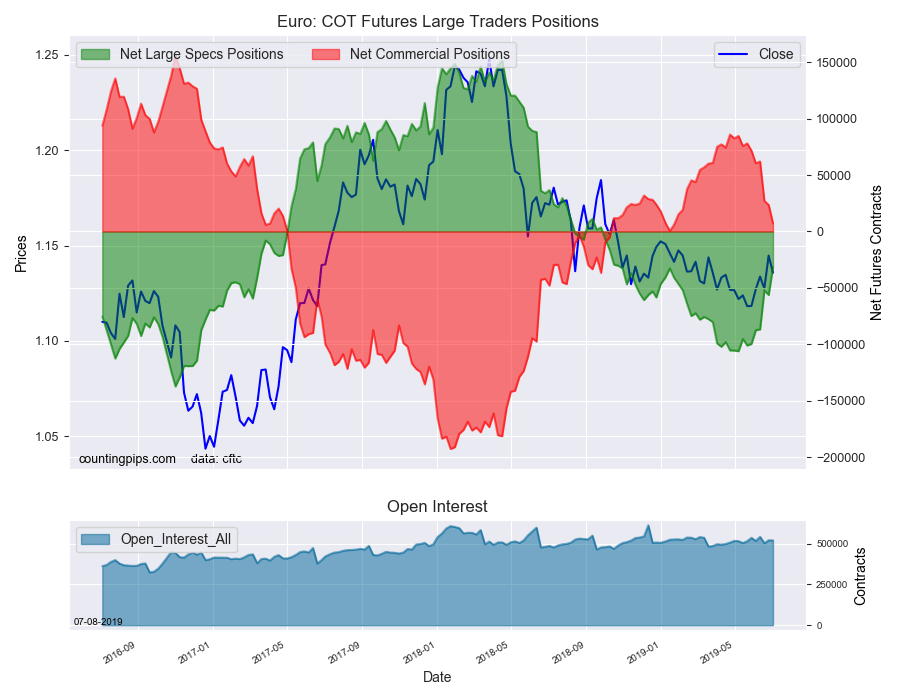

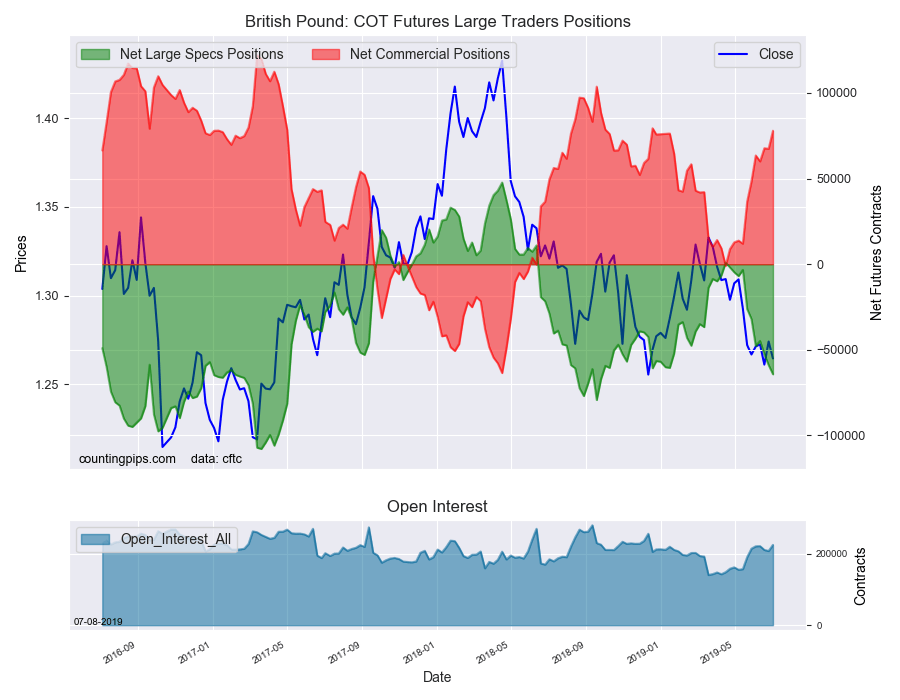

DAX 30 leads European indexes losses

European stocks extended losses on Monday led by banking shares. Both GBP/USD and EUR/USD continued falling and are lower currently. The Stoxx Europe 600 index slid 0.05%. The DAX 30 lost 0.7% to 12543.51 weighed by 5% drop in Deutsche Bank after news it would pull out of its global equities sales and trading operations. France’s CAC 40 slid 0.08% and UK’s FTSE 100 slipped 0.05% to 7549.27.

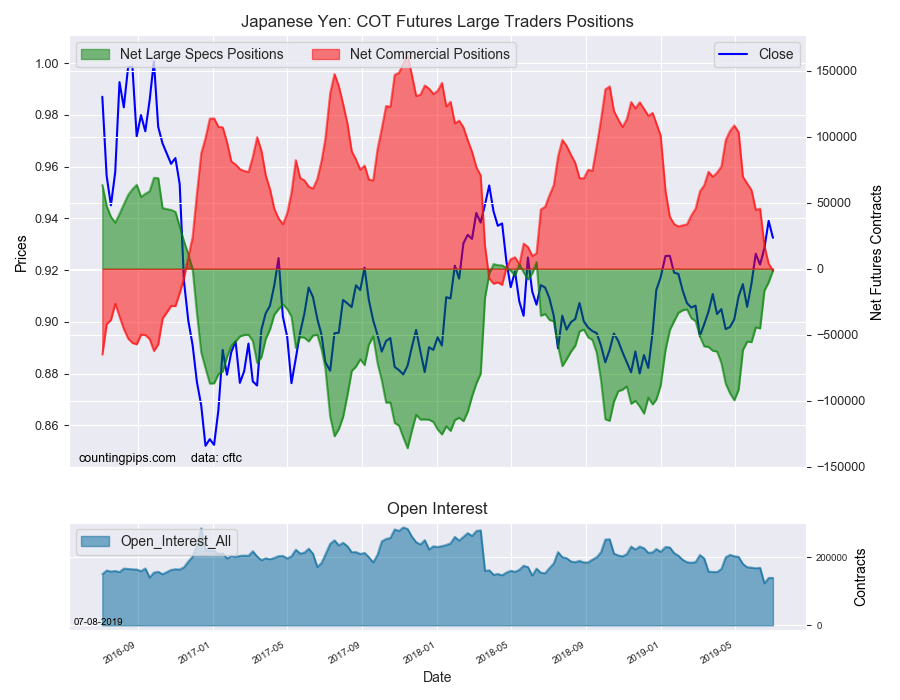

Hang Seng leads Asian indexes losses

Asian stock indices are mostly falling today. Nikkei however closed 0.1% higher at 21565.15 with yen slide against the dollar intact. Markets in China are retreating: the Shanghai Composite Index is down 0.2% and Hong Kong’s Hang Seng Index is 0.8% lower. Australia’s All Ordinaries Index extended losses 0.1% despite Australian dollar’s accelerating slide against the greenback.

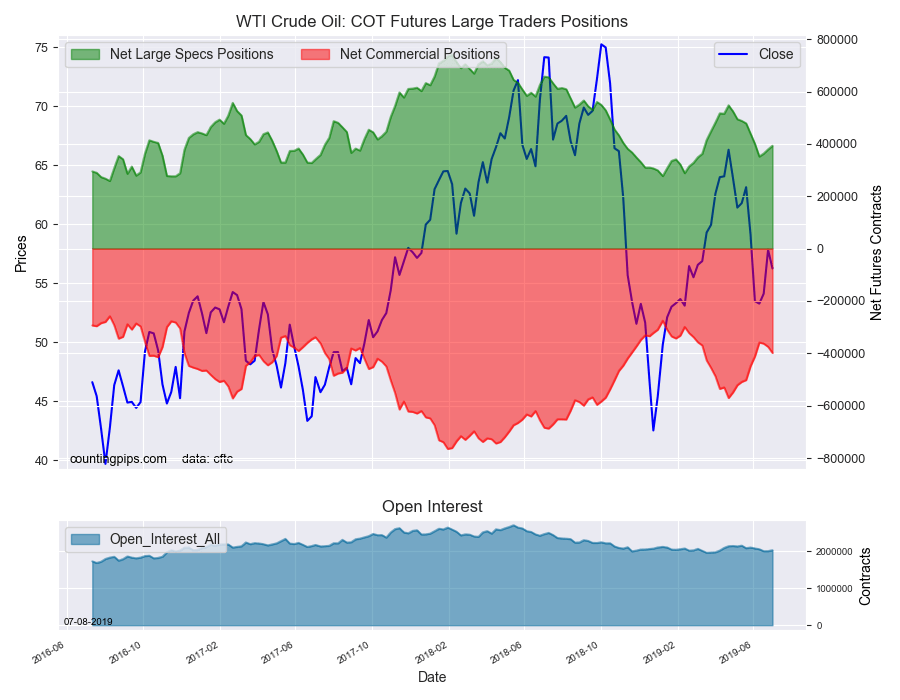

Brent up

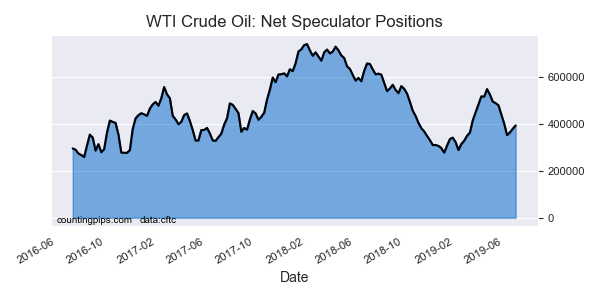

Brent futures prices are edging higher today supported by Middle East tensions as Iran claimed it was enriching uranium above the 3% level agreed in the 2015 nuclear deal, and threatened retaliation for the UK seizure of Iranian oil tanker last week. Prices fell yesterday: September Brent crude lost 0.2% to $64.11 a barrel on Monday.

Market Analysis provided by IFCMarkets

Note:

This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.