Yesterday, the US dollar sharply weakened against a basket of world currencies. Quotes rose by more than 70 points and updated the local maximums. The demand for USD declined after comments by Fed Chairman Jerome Powell. The official pointed to the willingness to reduce interest rates due to the growing risks in the global economy. The regulator plans to “act properly” so that the largest economy in the world can sustain a decade of growth. At the moment, the currency pair is testing a key resistance of 1.12800. 1.12350 is already a “mirror” support. Trading instrument can grow further. Open positions from key levels.

The Economic News Feed for 11.07.2019:

– CBE Minutes (EU) – 14:30 (GMT+3:00);

– Inflation Report (US) – 00:00 (GMT+3:00);

The price has fixed above 100 MA, which indicates the strength of buyers.

The MACD histogram is located in the positive zone and above the signal line, which gives a strong signal to buy EUR/USD.

The Stochastic Oscillator is in the neutral zone, the %K line crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.12350, 1.11950, 1.11600

Resistance levels: 1.12800, 1.13100, 1.13500

If the price consolidates above the resistance level of 1.12800, the quotes can grow to 1.13100-1.13400.

Alternatively, quotes can drop to a round level of 1.12000.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.24577

Open: 1.24974

% chg. over the last day: +0.31

Day’s range: 1.24974 – 1.25384

52 wk range: 1.2438 – 1.3631

GBP/USD began to recover and updated local maximums. The USD remains under pressure after the comments of the Fed. At the moment, the GBP is testing the offer zone 1.25350-1.25600. 1.24900 is already a “mirror” support. GBP/USD quotes have can grow further. Participants in financial markets continue to monitor the situation around Brexit. Positions must be opened from key levels.

The Economic News Feed for 11.07.2019 is calm.

The price has fixed above 100 MA, which indicates the strength of the sellers.

The MACD histogram is in the positive zone and above the signal line, which gives a strong signal to buy GBP/USD.

The Stochastic Oscillator is in the overbought zone, the %K line crossed the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.24900, 1.24400, 1.24000

Resistance levels: 1.25350, 1.25600, 1.26000

If the price consolidates above 1.25350, the quotes can grow to 1.25700-1.26000.

Alternatively, the quotes can descend to 1.24700-1.24500.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.31232

Open: 1.30806

% chg. over the last day: -0.40

Day’s range: 1.30486 – 1.30809

52 wk range: 1.2727 – 1.3664

Yesterday, high trading activity and volatility were observed on the USD/CAD. The The Bank of Canada, as expected, kept the key interest rate unchanged at 1.75%. The regulator plans to adhere to the current monetary policy. The USD/CAD quotes ended the trading session in the negative zone and reached key minimums. At the moment, CAD is consolidating in the range of 1.30500-1.30750. The Canadian dollar is supported by the positive dynamics of oil prices. We do not exclude a further decrease in the trading instrument. Positions must be opened from key levels.

The Economic News Feed for 11.07.2019 is calm.

The price has fixed below 50 MA and 100 MA, which indicates the strength of the sellers.

The MACD histogram is in the negative zone and continues to decline, which gives a strong signal to sell USD/CAD.

Stochastic Oscillator started to go out of the oversold zone, the %K line is above the %D line, which indicates the growth of the USD/CAD quotes.

Trading recommendations

Support levels: 1.30500, 1.30400, 1.30000

Resistance levels: 1.30750, 1.31150, 1.31400

If the price consolidates below 1.30500, the quotes can decline to 1.30200-1.30000.

Alternatively, the quotes can grow to 1.31000.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 108.856

Open: 108.423

% chg. over the last day: -0.48

Day’s range: 107.860 – 108.442

52 wk range: 104.97 – 114.56

There are aggressive sales on the USD/JPY currency pair. During yesterday’s and today’s trading, the quotes descended by 90 pips. The trading instrument has established new local minimums. At the moment, the safe-haven currency is consolidating in the range of 107.900-108.150. The demand for the US dollar has weakened significantly. We do not exclude a further descend in USD/JPY quotes. Pay attention to the dynamics of US Treasury bonds’ yield. Positions must be opened from key levels.

The Economic News Feed for 11.07.2019 is calm.

The price has fixed below 50 MA and 100 MA, which indicates the strength of the sellers.

The MACD histogram is in the negative zone and below the signal line, which gives a strong signal to sell USD/JPY.

Stochastic Oscillator started to go out of the oversold zone, the %K line is above the %D line, which indicates the growth of the USD/JPY quotes.

Trading recommendations

Support levels: 107.900, 107.700, 107.550

Resistance levels: 108.150, 108.300, 108.500

If the price consolidates below 107.900, the quotes can descend toward 107.600-107.400.

Alternatively, the quotes can grow toward 108.400-108.600.

Oil prices surged higher yesterday in response to the latest report reflecting a further drawdown in US crude stores.

Oil prices initially began to move higher on Tuesday in response to the weekly report from the API. The API report showed a large 8.1 million barrel crude inventories drawdown. On Wednesday, prices then shot up higher as the weekly report from the EIA confirmed the data.

Crude Inventories Fall Again

The report from the Energy Information Administration, covering the week ending July 5th, showed that US crude stores had fallen by 9.5 million barrels.

This decrease was well above the 3.1 million barrel decrease the market was looking for. It also marks the fourth consecutive week of drawdown in US crude stores.

Gasoline & Distillates Down

Elsewhere, the report showed that US gasoline stocks had also fallen by 1.5 million barrels. This was, again, more than the 1.3 million barrel drop forecast.

Refinery crude runs jumped by 148k barrels per day. They hit 17.4 million barrels per day, marking their highest levels since January. Distillate inventories, which include diesel and heating oil, jumped by 3.7 million barrels, far outstripping expectations for a 739k barrel increase.

Refinery Utilization Rates Increase

Refinery utilization rates rose by 0.5% to hit 94.7%, their highest level since January. This increase came despite a reduction in refinery operation capacity on the East Coast in the wake of the Philadelphia Energy Solutions Complex shutdown.

Oil prices have also been boosted by an incoming cyclone in the Gulf of Mexico. The cyclone has caused major oil producers in the area to close drilling facilities and evacuate staff.

Net us crude imports were down over the week, falling 341k barrels. Meanwhile, US crude production was actually seen ticking up by 100k barrels per day, to 12.3 million barrels per day. This is just off the all-time highs of 12.4 million.

OPEC Production Cut Extension Feeding Through

The uptick in oil this week might also be attributed to the market having digested OPEC’s announcement last week that it is extending the current production cuts by a further nine months.

Oil prices fell initially, likely in response to concerns over the demand outlook. However, in the wake of continued declines in US crude inventories, reflecting solid demand, the extended cuts now seem to be helping keep the market supported.

Last week, the UK seized an Iranian oil tanker. Iran responded by warning the UK. Consequently, a British oil tanker in the region has been sheltering off the coast of Saudi Arabia for fear of being seized by Iran.

This morning, the market was rocked by the news that Iranian military ships attempted totake over a UK oil tanker in the strait of Hormuz, forcing a UK navy warship which was accompanying the naker to train its guns on the Iranian ships and warn them off. With over a third of oil seaborne oil moving through the channel, the situation is causing concerns over supply disruptions.

Technical Perspective

The rally in crude has seen prices breaking back above the recent 60.07 resistance level which capped the last advance. This rally has also seen price breaking back above the bearish trend line running from year-to-date highs. Focus is now firmly fixed on a further push higher for oil, with the 64.02 level the next key target for bulls. Above this, the 2019 highs of 66.56 will be the main test. To the downside, any retest of the broken trend line should provide support, with the 57.98 level coming in just below.

Fed chair Jerome Powell’s latest dovish comments have removed market doubts over a US interest rate cut in July. Such signals have translated into the Dollar index (DXY) falling to around the 97 psychological level at the time of writing, allowing Asian currencies to climb higher against the Greenback. Asian stocks are also opened in the green, taking their cues from gains in US stocks, with the S&P 500 breaching the 3000 level for the first time ever before moderating.

Despite the June non-farm payrolls data still pointing to a robust jobs market, Powell said that the case for lower US interest rates has strengthened, citing “crosscurrents” pertaining to trade tensions and global growth, while the muted US inflation no longer appears transitory.

How deep will the Fed cut interest rates?

Powell’s speech on Wednesday essentially frames the July FOMC policy meeting as a decision between a 25- or 50-basis point rate cut. Whether FOMC officials will opt for the ‘kitchen knife’ or the ‘machete’ when cutting US interest rates can have a broader effect on global sentiment.

Should US monetary policy settings be eased by a wider-than-expected margin later this month, investors may question the strength of US economic growth momentum. Such concerns would encourage a softer-Dollar environment, presenting Asian assets with more potential upside, while safe havens such as Gold and the Japanese Yen could also advance further.

US-China trade impasse remains a key uncertainty for global growth

Still, potential gains in Asian assets remain capped by the lingering uncertainties surrounding US-China trade tensions. Risk appetite will likely be reined in, until both countries break the impasse and reach a deal that alleviates the global growth outlook. Market sentiment surrounding the strength of the global economy could be further influenced by China’s economic data releases due over the coming days, including external trade, industrial production, and Q2 GDP, as the world’s second largest economy continues to find its path towards a more sustainable path amid heightened external headwinds.

Oil on course for summer of gains

The moderating Dollar has also given Oil prices another reason to climb higher, with New York crude and Brent futures gaining over three percent respectively on Wednesday, to reach their highest levels since May. Oil’s climb was triggered by constrained US supplies, with production in the Gulf of Mexico being reduced by about a third given the possibility of an incoming hurricane, along with the steep decline reported in US crude inventories.

Oil bulls will be encouraged by the transpiring tailwinds, including rising geopolitical tensions, a potential US interest rate cut, and rising summertime demand, while the OPEC+ supply cuts extension effectively places a sturdier floor under Oil prices. Yet it remains to be seen whether Oil can prolong its upward climb, given the persisting uncertainties surrounding global demand for the year.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The US dollar fell against a basket of major currencies after the speech by Fed Chairman, Jerome Powell. The official said that concerns about trade policy and the weakness of the economy continued to put pressure on the forecasts for the US economy, and the Fed was ready to do everything necessary to support economic growth. Powell believes that the rate of economic growth has become moderate, but weak inflation may last a little longer than it was supposed. The US dollar index (#DX) closed in the negative zone (-0.40%) yesterday.

Investors took the statements by the head of the US Central Bank as a signal that the Fed was ready for a more aggressive interest rate reduction. According to the CME FedWatch Tool, more than 50% of financial market participants believe that the regulator may reduce the range of key interest rate to 1.75%-2.00% at a meeting in September.

Among other things. Yesterday, ambiguous economic statistics were published in the UK. GDP (m/m) increased by 0.3%, as experts expected. Manufacturing production grew by only 1.4% in May instead of 2.2%. Also, the Bank of Canada decided on a key interest rate yesterday. As expected, the regulator left the indicator unchanged at 1.75%.

The “black gold” prices are growing. At the moment, futures for the WTI crude oil are testing the mark of $60.75 per barrel.

Market Indicators

Yesterday, the bullish sentiment was observed in the US stock markets: #SPY (+0.48%), #DIA (+0.31%), #QQQ (+1.00%).

The 10-year US government bonds yield has become stable. Currently, the indicator is at the level of 2.04-2.05%.

The News Feed on 2019.07.11:

– Publication of the ECB account of monetary policy meeting at 14:30 (GMT+3:00); – Data on inflation in the US at 15:30 (GMT+3:00).

We also recommend paying attention to the speeches by the FOMC representatives.

The US dollar continued to decline over the early European session on Thursday as the sell-off in response to yesterday’s FOMC minutes develops further. The minutes were decidedly dovish, noting that

“Many judged additional monetary policy accommodation would be warranted in the near term should these recent developments prove to be sustained and continue to weigh on the economic outlook.”

USD index trades 96.55 last as the rejection from the 97.10 level deepens. Looking ahead to today’s US session, the market is waiting for US CPI data which is expected to have ticked lower last month. This would weigh on USD further if confirmed.

EUR Down Despite USD Weakness

EURUSD has weakened today, despite the sell-off in USD. Concerns around the health of the eurozone economy, as well as expectations of forthcoming ECB easing, are keeping the pressure on EUR. Price trades 1.1268 last. This is well above the 1.1217 level.

GBP Rallies Following Better GDP Data

GBPUSD is fighting to stay above the 1.2439 lows. Price is currently printing a second consecutive bullish day on the back of USD weakness. Yesterday’s better than expected GDP print is continuing to provide upside impetus. However, in the face of growing Brexit uncertainty, any rally seems likely to be short-lived, keeping focus on further downside in the near term.

Risk Sentiment Boosted B Dovish FOMC Minutes

Risk assets have been well supported this week, with US equities receiving a mid-week boost from the set of dovish FOMC meeting minutes released last night. The market is now pricing in a .25% July rate cut. This has pushed the SPX500 back up to 3001.13 last, sitting just below all-time highs. The lingering prospect of fresh efforts to achieve a US/China trade deal is also helping to keep risk sentiment buoyant despite rising tensions in the Middle East.

Gold Rallies, JPY Drops

Safe havens have had a mixed day today. Gold prices have risen against the US dollar in the face of increased Fed easing expectations. On the other hand, JPY has weakened, as equity prices have climbed higher again. Price action over recent weeks suggests that gold is being traded less as a safe haven in terms of equities prices and more as a reflection of US interest rate expectations. XAUUSD trades 1423.30 last as price begins the climb back to recent multi-year highs. USDJPY trades 108.15 last as the bounce of 107.90 support continues.

Oil Supported by Bullish EIA Report & Middle East Tensions

Oil prices have been higher again today. Yesterday, the EIA reported a fourth consecutive weekly drawdown in US crude stores, which has alleviated concerns about the demand outlook. Tensions in the Middle East are also keeping oil supported as the UK and Iran clash following the seizure of an Iranian oil tanker by the UK last week and the attempted seizure of a British oil tanker by Iran yesterday. Crude trades 60.80 last, with price having broken back above the 60.07 level.

Commodity Currencies Rally

USDCAD has turned lower once again, crumbling under the pressure of a weakened US dollar and stronger oil prices. The Canadian currency is now trading back below the 1.3068 support and is challenging recent lows at the 1.3037 level.

AUDUSD has turned higher today, with AUD taking advantage of a lower USD and higher gold prices.For now, price remains below the .70 level but is quickly advancing and looks set to test the level yet again over the coming sessions.

The monthly inflation report from the United States will be released today. Forecasts show that headline inflation will remain tame on an annualized basis. The data comes amid the markets speculating a Fed rate cut.

Headline inflation for June is forecast to remain flat on a month over month basis. This marks an unchanged print following a 0.1% increase in May. On a yearly basis, the inflation rate is expected to slow from 1.8% in May to 1.5% in June. This would mark another month of declines in the annualized CPI.

U.S. CPI Change, May 2019

Core CPI, which excludes the volatile food and energy prices are forecast to remain unchanged at 2.0% on the year. On a monthly basis, core CPI is expected to tick a notch higher to 0.2%, up from 0.1% previously.

Inflation in the US has remained tame for the most part this year.

However, the Fed maintains that inflation weakness remains transitory. But the prolonged weaker pace of increase in inflation has sparked speculation of a rate cut, alongside the expected lower GDP growth in the world’s largest economy.

Inflation Stays Broadly Muted in May

Headline inflation barely increased in May with the data pointing to inflation staying tame for another month. Combining this with the slower pace of growth in the economy, the data for May built up weight for the Fed to cut rates.

Data from the US Labor Department showed that there were small pockets where inflationary pressures were felt. These included rents and healthcare costs which rose sharply during the month. The data showed conflicting reports, which could lead to the Fed to use a wait and watch mode for its monetary policy guidance.

Data for May saw consumer prices rising just 0.1% on a month over month period. Price increase in food was offset by cheaper gasoline prices. The pace of increase in inflation in May was slower compared to the 0.3% increase in April.

Gasoline prices fell 0.5% after rising 5.7% in the previous month. Food prices rebounded 0.3% during the month, recovering from a 0.1% decline in April. The price of used motor vehicles and trucks fell 1.4%. This was the biggest drop since September 2018 and it was also a fourth consecutive monthly decline.

On a year over year basis, US inflation rose 1.8%.This was a modest slowdown from the 1.9% yearly increase seen in April. Economists polled forecast that inflation would rise 1.9% on the year.

The core inflation rate which excludes the volatile food and energy prices edged 0.1% higher on the month. This was the fourth consecutive monthly gain in the core inflation rate. Still, the pace of increase was modest.

The core CPI was pinned down by a decline in prices of used automobiles. On a yearly basis, core inflation rate ticked up 2.0%, slightly slower compared to the 2.1% increase in May.

Will Consumer Prices Report Beat Estimates?

Given the conservative estimates of no change during the month, there are prospects that consumer price data could beat estimates. This comes largely due to the higher energy prices seen during the month of June.

International crude oil prices were seen trading back near the $60 handle in the run-up to the OPEC meeting in early July this month. However, given that most of the gains in inflation during the previous month came from other sectors, there is scope that we could see this trend.

Last week, the markets reacted strongly following the June jobs report which came out stronger than expected. Likewise, a stronger than expected inflation report could potentially see this view being taken by the markets.

The core inflation data will also be something to be watched. This could potentially underline the inflationary pressures in the market. The impact of today’s CPI will be felt across all asset classes. This comes as investors are looking for further evidence of a slowdown in the US economy that could prompt the Fed to cut rates.

On Wednesday the 10th of July, trading on the EURUSD pair closed up by 60 pips. There was a surge in volatility in the US session during Fed Chair Jerome Powell’s testimony to the US House of Representatives. He hinted that the Fed could lower interest rates at the end of July due risks to the global economy. His remarks were taken to mean that the Fed is prepared to lower rates at the end of the month. After Powell’s testimony, US 10-year bond yields dropped by 3.3% to 2.04%. This means that markets are bracing themselves for a rate slash, which is good for more volatile assets.

Yesterday didn’t turn out as expected. During the Fed’s chair’s testimony, the bull army triggered the stop levels above 1.1235. The pair recovered to 1.1260, and the dollar’s decline continued to 1.1281 in today’s Asian session.

At the time of writing, the euro is trading at 1.1269. Since the upwards movement stopped at the 67th degree, and a bearish divergence has formed between the rate and the AO, today I’m expecting to see a downwards correction to 1.1240. I’ve drawn a channel with dashed lines on the chart, from which I’m expecting a downwards breakout. The 45th degree is at 1.1230.

Sometimes you get moments of inactivity among bears on the market, and the rate keeps climbing on the back of fundamentals, which under the current scenario would form a third higher high within the channel. This shouldn’t be ruled out as a possibility.

US stock market extended gains on Wednesday after Powell testimony confirmed Federal Reserve plans a rate cut in July. The S&P 500 rose 0.5% to 2993.07. The Dow Jones industrial average gained 0.3% to 26860.20. Nasdaq composite index advanced 0.8% to record 8202.53. The dollar strengthening reversed as Powell comments emphasized rising risks to the US economy from trade policy and slowing global growth, as well as falling price inflation. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, fell 0.4% to 97.10 and is lower currently. Stock index futures point to higher market openings today

FTSE 100 slips despite above expected GDP growth

European stocks continued retreating on Wednesday. Both EUR/USD and GBP/USD turned higher with both pairs rising currently. The Stoxx Europe 600 lost 0.2% led by telecom shares. Germany’s DAX 30 fell 0.5% to 12373.41. France’s CAC 40 slid 0.1% and UK’s FTSE 100 slipped 0.1% to 7530.69 despite data showing UK economy expanded by above expected 0.3% in May after contracting 0.4% in April.

Hang Seng leads Asian indexes rebound

Asian stock indices are rising today. Nikkei rebounded 0.5% to 21643.53 with yen continuing its climb against the dollar. Chinese stocks are gaining: the Shanghai Composite Index is up 0.1% and Hong Kong’s Hang Seng Index is 0.8% higher. Australia’s All Ordinaries Index extended gains 0.4% despite Australian dollar’s continuing climb against the greenback.

Brent futures prices jumped today as a storm built in the Gulf of Mexico. Prices rebounded yesterday after the Energy Information Administration report US crude inventories dropped by bigger than expected 9.5 million barrels last week while gasoline inventories declined by 1.5 million. September Brent crude jumped 4.4% to $67.01 a barrel on Wednesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The much-anticipated testimony from Fed Chair Jerome Powell happened on Wednesday. As widely speculated, Powell made the case for a rate cut.

This sets the stage for the July Fed meeting where interest rates could be lowered. Following Powell’s comments, the FOMC meeting minutes also hinted that the case for an accommodative monetary policy was more appropriate. The S&P500 pushed higher to test the 3000-mark by Wednesday’s close.

Euro Rebounds on a Weaker USD

The common currency posted strong gains on Wednesday as the USD fell. On the economic front, French industrial production jumped 2.1% in May, marking the biggest increase since May 2016. Similar gains were seen in Italy’s industrial production figures as well, which grew 0.9% on the month. The European Commission released its economic forecasts where it lowered eurozone growth to 1.2% for 2019.

Will the EURUSD Maintain the Bullish Gains?

The currency pair reversed just a few pips off the 1.1188 level of support. The reversal pushed prices higher as the EURUSD closed above 1.1250. If the bullish momentum is maintained, we could expect the euro to rise toward 1.1400 level of resistance. However, in near term, dips to 1.1250 will see support being formed.

WTI Crude Oil Jumps on EIA Report

Crude oil prices closed above $60 a barrel on Wednesday. The gains came after the Energy Information Administration released the weekly inventory report. Data showed that US crude oil stockpiles fell 10 million barrels per day. The drawdown was larger than expected. It also reflected the API’s inventory report released earlier in the week. Meanwhile, a developing weather disturbance near the Gulf of Mexico is also seen adding to the price gains.

Can Crude Oil Rise Further?

The current gains in oil prices came after price had initially declined. Following a period of consolidation near the support area of 57.50, oil prices have reversed direction. The strong gains off the 50.57 support level have led to oil testing the upper end of the range. A breakout above the $61.00 handle will further confirm the upside bias in oil.

Gold edges Higher on Powell Comments

The precious metal posted gains on Wednesday after the Fed Chair Powell hinted that the Fed was readyto cut rates. He cited the economic uncertainty but said that the federal deficit could potentially push interest rates higher.

Will XAUUSD Maintain the Gains?

The gains came after the precious metal was hovering close to the 1384 handle, following the break of the rising trend line. But the comments from the Fed Chair saw the precious metal reversing direction. After breaking past the resistance level of 1404, gold prices could be on track for further gains. The next upside target is seen at the previous highs at 1432.

Sector expert Michael Ballanger explores the analogies between fishing and investing.

As many of you know, I love to spend the summers exploring the thousands upon thousands of bays and inlets and coves that represent the Georgian Bay landscape. With the exception of a few boyhood jaunts around the Parry Sound area, I was not able to fully appreciate the grandeur of the Canadian Shield as it escapes its marine blanket while leaving behind thousand of large and small islands in its wake. Sightseers like the famous Group of Seven, whose artwork is almost exclusively the Georgian Bay vistas, would refer to them as islands or fresh water atolls but boaters young and old refer to them simply as “rocks,” and they are both feared and revered by anyone that has run aground, as propeller shafts and stern drives do not get mangled by islands or fresh water atolls.

Part of the majesty of the region lies in the perpetual presence of danger whenever one departs the well-marked channels and heads out into “the big water.” Summer weather on the Great Lakes and particularly northern Georgian Bay is fickle and it is immediate, in that a bright blue sky with calm seas during breakfast hours can become a roaring tempest by early afternoon, with winds that seem to know instinctively in which direction to blow your vessel. . .and know this: It is never away from rocks.

However, most seasoned mariners are well aware of weather conditions and are usually happily ensconced in a cove or bay, carefully free of any real or imagined threats from Mother Nature by the time storms arrive, not unlike seasoned portfolio managers, who are ever aware of changing economic or financial conditions that may produce a hurricane force impact upon their holdings.

Now, an integral part of the Georgian Bay boating experience lies in the remoteness of the anchorages to human interference and the uncanny ability of Mother Nature to ignore human expectation. One boater we know was in a tidy little cove hundreds of miles from the nearest highway. When they returning from a dinghy ride, they found a black bear rummaging the cockpit fridge (incensed that all he could find was beer). After they had shoo-ed the bear away and were exiting the cove, they noticed another boat attempting to take their spot. They quickly warned the others of the impending dangers via VHF radio, but just as boaters discount weather info at their own peril, this couple suffered the same fate as the former couple, and Yogi wound up with a double, taking much more than beer as its reward.

What makes northern Georgian Bay incomparable for me, though, is the fishing. In case you didn’t know, fishing is the #1 global recreational past-time, outranking international football (soccer), American football (football), golf, tennis, baseball and hockey. The reason is that the most populated country on the planet has a gene in the DNA of their citizens that forces them to drop a fishing line into any pond or lake or pool that exceeds one foot in depth. China has exported natural-born gamblers to Macau and Vegas (and to their central bank to manage exchange rates) but they have exported fifty times as many citizens to North America, whose major obsession is fishing. They line the busiest bridges and the most treacherous roads, crammed together elbow to elbow with lunch boxes at their feet, desperately trying to outcast and outmaneuver their counterparts so they can reel in a four-inch sunfish or a ten-pound carp.

However, before landing on the Chinese immigrants for their obvious love a sport, let it be known that I share their passion for angling. It is sport I have enjoyed, with my greatest conquest to date being in Lake Ontario (a 36.7 lb. chinook salmon in 1987), where the fish landed eleventh in the annual Lake Ontario Fishing Derby. (The tenth-place fish won its acquirer a $20,000 fishing boat, motor and trailer; my eleventh-place sammy got me a year’s supply of “Worm-Up,” worth $500.)

Fishing is a sport that attracts all types of people spanning all demographic and econographic strata. You find billionaires hunting tuna off the Great Barrier Reef, maniacally driven by the same endorphin that sent Huck Finn to the fishin’ hole instead of the schoolhouse. The thrill of catching a fish is on a par with hitting blackjack at the card table or having the winning card at your mother’s Wednesday night Bingo game. Fishing carries the same narcotic as horse racing, lotteries, Bingo, and, of course and without further adieu, investing.

As an example, my partner and I were circumnavigating Bone Island on the weekend, trolling the shoals and islets for bass, pike or, if very fortunate, pickerel (known as walleye to our American friends), and given that early afternoon in high heat and blazing sun is not always the most ideal angling time, we were proceeding with limited expectations, such that even a strike would be a success, let alone a landed fish. As we circled a small rock protruding from the water like an indignant waiter, I felt a tremor in the 10-pound test I was using and sure enough, it was “fish on.” The adrenalin surge of engagement had my mate feverishly reeling in her line as I battled was surely an eight-pound largemouth.

It is not unlike the rush of anticipatory excitement one feels when a junior mining stock, of which you are holding far too much, announces a 27-meter interval of economic-grade “anything,” after which you presume that it is surely the arrival of the next Voisey’s Bay or Olympic Dam or Hemlo. As tends to occur in the landing of a fish or the establishment of an economic ore body, the fish that had determined to chomp down on the flashy $20 Mepps was, alas, not the eight-pound leviathan for which I prayed, but rather a (perhaps) one-pound smallmouth with eyes obviously much larger than its stomach.

Furthermore, in the same manner than a PEA (preliminary economic assessment) can disappoint investors with an unexpected outcome, as my brave little fish approached the net of doom, it suddenly breached the surface and as if making a statement, spat the lure directly into the boat and disappeared beneath the wavesbut not before flipping me the middle fin in a gesture of “nice try, moron.” Four times that day we hooked a fish and four times they decided to elude the net and the boat, the result of which was an 0-4 record for the day.

We had all of the right tools and made all of the moves that, in the past, had worked, but at the end of the afternoon, we were frustrated, frazzled and fishless. Exactly as happens in the investment world, you can experience all of the excitement and satisfaction of proper research, funding and execution, but if the investment community decides to spit out the hook or break the line, you are doomed. The charm of fishing is like the charm of investing; you are in pursuit of what is elusive but attainable, a perpetual series of occasions for hope.

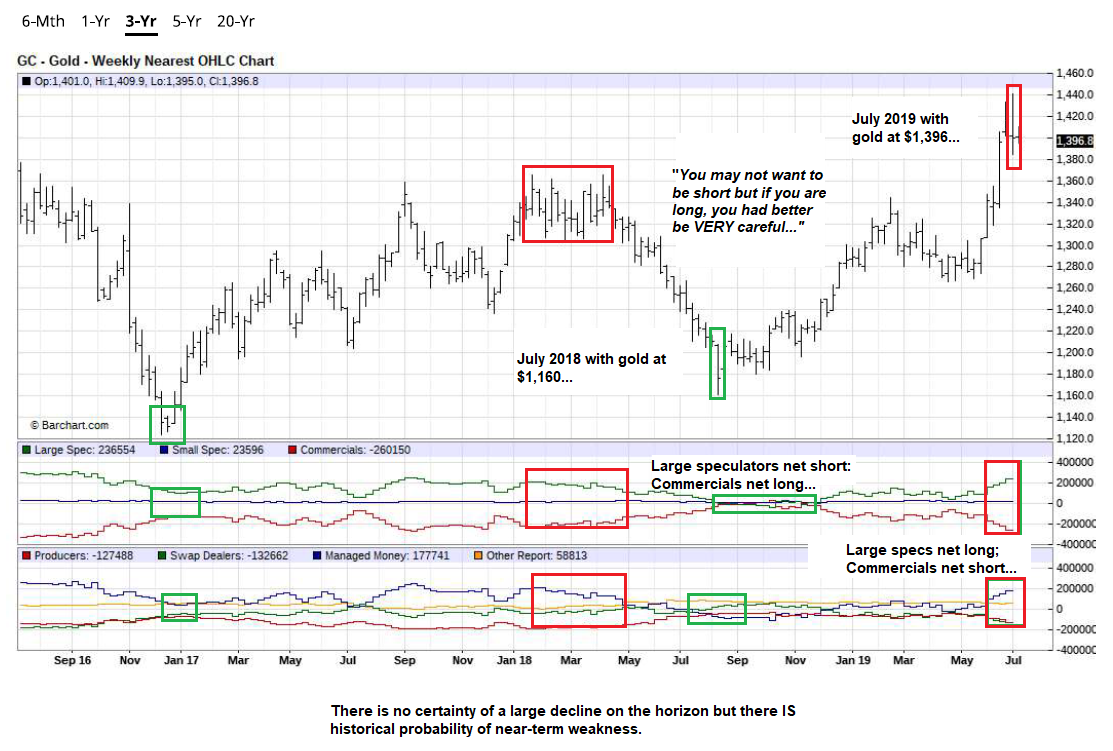

I post for comparison purposes two charts of gold futures continuous contract; the first was put up a week ago and the second is as of the close of business on Monday, July 8. You will note that the RSI (relative strength index), which traded up to nearly 90 in late June as gold touched $1,442, has now exited the overbought plus-70 zone from which every tradable correction since 2016 has occurred ( with the operative adjective being “tradable”).

While it is subject to conflicting interpretations from technicians far wiser than I, RSI in full retracement mode compels me to the sidelines, having jettisoned all leveraged ETFs and call options and 50% of the formerly untouchable GDX and GDXJ holdings. I was painfully early in the exit of the leveraged ETFs and call options, but near perfect in the sale of GDX and GDXJ and now enjoy the enviable task of buying them all back at lower levels.

It is only a week between the two charts but also notice that in addition to the continued drop in RSI from 68.48 to 61.27, the negative (bearish) MACD (moving average convergence-divergence) crossover is now complete, while volumes have become less robust than in the period immediately following the “breakout.”

Also, notice the red band at $1,350-1,375, which was three-year resistance and which is now the “absolutely critical band of support,” a close below which lies the dreaded “failed breakout.” These events, mastered beautifully in both planning and execution, are exceeded only by the illegality of their implementation. For years upon years, I have whined, screamed, pleaded and beseeched readers to avoid drinking the Kool-Aid of gold and silver market technical “breakouts,”and that only in the precious metals (PMs) do you sell breakouts and buy breakdowns. . .all for one simple reason: Both markets are rigged.

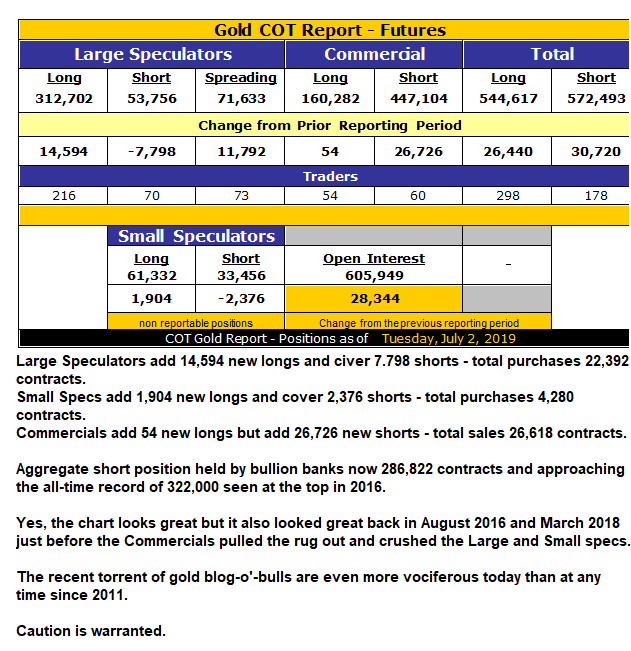

Further adding to the parade of red flags is, of course, the COT structure, where Commercials added yet another 26,616 net shorts, representing 2,616,000 ounces of undeliverable, phony, paper gold. This results in an aggregate short position of 286,822 contracts representing 28,682,200 ounces of that same fictitious metal, never the focus of a margin call and never, ever to be found in any vault or warehouse anywhere.

Now, the COT has rarely, if ever, been a useful timing tool but it has been an important barometer of trend changes looming on the horizon. The record net short was around 322,000 contracts, so that we are heading in that direction is concerning. Without the worry of capital constraints, the bullion banks are free to continue to pile on their aggregate short pile until demand by Large and Small Speculators (also referred to as “prey” by the Commercial trading desks) is exhausted. This creates a bid-stack vacuum into which the cretins simply nudge price for the express purpose of sending prices lower, which they cover and then make obscene profits with nary the report of as much as one trading day of losses in the past ten years.

The next chart carries the graphic images of how bottoms occur when the Large Spec positions converge with those of the Commercials, and vice-versa at tops. Those alligator jaws, so wide open as of Monday’s COT report, are destined to snap shut, but only after serious price declines. Now, there is the possibility of the signal failure in which the Commercials are forced to cover into rising prices, but my interpretation is that since we saw little if any capitulation from the shorts into the gap to $1,442, I see little evidence of a squeeze near term with prices now back below $1,400.

I would urge you all to view these charts and graphs in the context of assessing not just direction but, more importantly, probability of same. This is all in the interest of avoiding those $50-100/ounce drawdowns, the recovery of which are nigh on impossible in the course of a trading year. The data that currently presents itself demands cautionnot panic nor abandonment nor mass liquidation, but simple prudence in terms of position sizes and risk.

Just as in the world of successful investing, it is the charm of successful fishing that has kept me in the hunt for a return to free markets and fiscal sanity, both of which are absent from the 2019 landscape. Not that every time one has a fish on the line it should automatically result in a family of four being fed, but the fight should be a fair one. It is difficult enough to navigate free markets, but it is virtually impossible to survive the interference and interventions of, shall we say, “managed” markets, where all departments of government are openly hostile to gold and silver ownership and sponsorship.

Imagine battling an especially large fish in an epic angling affair lasting forty-five minutes, wherein the beast is inches from the net only to have an unknown entity suddenly emerge from the depths, severing your line. This is exactly what happens when the Commercials fill Large Spec demand with those phony, “paper” contracts, created magically out of thin air for the sole purpose of managing price. Buyers of the “paper” contracts have intent to acquire the physical by taking delivery which is a far cry apart from the intent of the bullion banks. They never deliver any physical metal and they almost always cover. They leap up and cut the lines of the Large and Small Specs with nary a tear being shed.

In the end, the rules of engagement in trading all markets should be the same irrespective of asset class; favoritism across asset classes destroys markets and creates unimaginable moral hazard. The last point of correlation I make is this: The singular most important attribute carried by the successful angler is patience. The ability to believe in your preparation and execution in both fishing and investing is matched only by your ability to wait diligently for the moment of opportunity. That requires patience, sometimes little, often much more, but never, ever without.

It is also a virtue the likes of which may be particularly valuable in the coming weeks and months; I pray it is not needed but fear that it may.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.