On Thursday the 18th of July, trading on the euro closed significantly up to completely recover the losses incurred earlier in the week. The 1.1280 mark was reached once again, revisiting the high set on Monday. In the Asian session, the pair reached 1.1241, while the euro tumbled to 1.1205 during trading in Europe. This was brought about by very strong retail sales data from the UK. Growth across the retail sector increased by a factor of 1.5 – 3, both in monthly and annual terms.

The euro’s decline was also helped along by the Bank of England’s credit conditions survey. It’s worth remembering, however, that the tensions in the UK surrounding the change in government and Brexit still reign supreme. In the US session, the single currency began its recovery. Jobs data and the Philadelphia Fed manufacturing survey weakened the dollar, allowing the euro to rise, while FOMC members Rafael Bostic and John Williams added to the downside pressure on the greenback later on.

Day’s news (GMT+3):

11:30 UK: public sector net borrowing (Jun).

15:30 Canada: retail sales (May).

18:05 US: Fed’s Bullard speech.

23:30 US: Fed’s Rosengren speech.

Current situation:

Yesterday’s range, in which the EURUSD pair continues to trade today, will most likely remain intact. The current situation is uncertain, however. We can’t rule out breakouts of both the upper (1.1287) and lower (1.1194) boundaries of this range. A breakout to either side will set the tone for the near future.

Asian stocks are taking their cues from their US counterparts to push higher, after Fed officials appeared to call for US monetary policy stimulus in the near-term. On Thursday, Federal Reserve Bank of New York President, John Williams, said that central banks must “take swift action when faced with adverse economic conditions”. Also, Federal Reserve Vice Chairman, Richard Clarida, said yesterday that policymakers “don’t need to wait until things get so bad” before cutting interest rates.

Safe haven assets have been boosted by risk appetite that is being curtailed by the thought of waning US economic growth. The Yen has strengthened below the 107.6 level against the US dollar, Gold prices briefly breached the $1450 handle, while the yields on 10-year US Treasuries aren’t straying far away from the two percent mark. Although central banks around the world have embarked on policy easing in a bid to support their respective economies, investors are left to ponder whether the stimulus will be enough to offset the effects from heightened US-China trade tensions which have already dragged global growth lower.

Dovish Fed makes for softer-Dollar environment for the rest of July

The dovish commentary by Fed officials underscored expectations that the US central bank will lower interest rates by a larger quantum at the FOMC meeting later this month. At the time of writing, markets now expect a 43.5 percent chance of a 50-basis point cut at the July 30-31 meeting, as seen in the Fed funds futures.

Despite the better-than-expected June non-farm payrolls, retail sales, and factory output data, the Fed is expected to press ahead with at least a 25-basis point interest rate cut this month. Given that US inflation remains muted while global uncertainties continue to prevail, lower US interest rates should help ensure that US economic growth momentum remains steadfast. However, ramped-up expectations over a bigger July Fed rate cut are undermining the Greenback, and are likely to contribute to a softer-Dollar environment for the rest of this month. The weaker Dollar is set to play into the hands of Gold and Yen bulls.

Oil tumbles as slowing global demand overshadows rising geopolitical tensions

Both WTI crude and Brent futures have each shed over seven percent so far this week, with the former briefly dipping below $55/bbl before recovering slightly, while the latter has dropped below $62/bbl at the time of writing. US inventories increased by over 9 million barrels last week, which added to market jitters that the growth in global demand is lagging severely behind the rise in output.

The slowdown in global growth has overshadowed market sentiment for Oil, as rising geopolitical tensions have failed to live up to their potential of sending prices higher. With US-China trade negotiations merely offering a pittance to risk appetite since the tariff truce was announced at the end of June, any further deterioration in the global demand outlook could open up further downside for Oil prices. Still, markets can take some comfort in the OPEC+ decision to extend its supply cuts through March 2020, which should help support Oil prices over the coming months.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Dollar weakening accelerated after Williams’ comments

US stock market rebounded on Thursday as New York Fed President John Williams said the most effective strategy for the Federal Reserve is to cut rates at the first sign of trouble with benchmark interest rate so close to zero. The S&P 500 gained 0.4% to 2995.11. The Dow Jones industrial average edged up 0.01% to 27222.97. Nasdaq composite index rose 0.3% to 8207.24. The dollar weakening accelerated as traders interpreted Williams’ comments as support for a half-point rate cut at the Fed’s next policy meeting on July 30-31: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, fell 0.5% to 96.70 but is higher currently. Stock index futures point to higher market openings today

DAX 30 leads European indexes slump

European stocks extended losses on Thursday led by 5.6% drop in SAP share after Europe’s most valuable tech company’s disappointing quarterly results. Both EUR/USD and GBP/USD accelerated their climb with both pairs lower currently. The Stoxx Europe 600 index ended 0.2% lower. Germany’s DAX 30 lost 0.9% to 12227.85. France’s CAC 40 fell 0.8% and UK’s FTSE 100 slid 0.6% to 7493.09 despite a report of unexpected 0.1% on month rise in UK retail sales for June.

Nikkei leads Asian indexes recovery

Asian stock indices rebounded today after a recovery on Wall Street overnight. Nikkei rose 2% to 21466.99 as yen resumed its slide against the dollar. Chinese shares are gaining despite reports trade negotiations between the U.S. and China had faltered over restrictions on Chinese telecommunications giant Huawei: the Shanghai Composite Index is up 0.8% and Hong Kong’s Hang Seng Index is 1.1% higher. Australia’s All Ordinaries Index turned 0.8% higher as Australian dollar resumed its slide against the greenback.

Brent futures prices are edging higher today after a U.S. Navy ship destroyed an Iranian drone in the Strait of Hormuz. Prices fell yesterday: September Brent crude lost 2.7% to $61.93 a barrel on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Sector expert Michael Ballanger is watching the gold market and banking on opportunities in silver.

“The desire for gold is the most universal and deeply rooted commercial instinct of the human race.”Gerald M. Loeb

One of the finest books ever written on investing was “The Battle for Investment Survival,” by Gerald M. Loeb, the provider of today’s quote and a true legend in the distant, long-forgotten world of free market capitalism. Also credited with “Put all of your eggs in one basket and watch the basket,” it was an obvious slap-in-the-face to those who eat, drink and breathe the diversification mantra.

Having avoided disaster in the 1929 market crash, Loeb was deeply affected by the devastating swath it cut through the economic field of vision and was one of the first of his era to debunk the “long-term investing” track record, choosing instead to trade positions rather than hold. I remember reading the book in 1974 and marveled at how, thirty-nine years after its initial publishing run, it still retained relevancy, a quality that many professional investors lack given the rapidly changed/changing universe of financial products available to generations of new investors around the globe. From time to time, I will take it down from the bookshelf in my study, pour a glass (or two) of fine wine and browse the many chapters in search of old, time-honoured lessons and rules that I deem still absolutely relevant here in the Year of our Lord 2019.

The fact that gold remains “the most universal and deeply rooted commercial instinct of the human race” defines the reason why the paper merchants (bankers, brokers) detest its very existence. Since 1977, when I joined the Canadian securities industry, I have watched with abject horror the concerted campaign of misinformation, disinformation, propaganda and fraud condoned, promoted and executed by the “destroyers” (as Ayn Rand called them) as a means of swaying the “desire” mentioned by Loeb from gold to”financial assets” (including stocks and bonds). Financial news networks, not to be found anywhere until the 1980s, served to deify stock ownership, and the proof of that is the rise in household ownership of stocks from 4% in 1974 to over 50% by the year 2000.

In light of the intensity of the message being broadcast by the elitist bankers and politicians, gold has been an unwanted house guest, rarely if ever to be invited to any of the celebrations such as the “all-time highs!” or “Dow 30,000” parties so common in this period of insane currency debasement operating under the alias of “easy money.” Today, there is a generational tendency that allows the “most universal and deeply rooted commercial instinct of the human race” to be the desire for paper wealth through stocks, a trait held by over 65% of all Millennials, who in a recent survey said that they preferred computer-generated “BUY” recommendations rather than those by highly educated, brilliantly trained carbon units.

The reason I write this missive is that being a gold or silver “expert” provides a function to an increasingly shrinking market, in the same sad manner in which buggy-whip manufacturers were forced from relevancy by the invention of the automobile. Being brilliantly trained by brilliant mentors in the importance of anchoring one’s wealth in solid, time-tested stores of value such as gold and silver carries little or no usefulness in a world managed, manipulated and molded by the paper merchants, as year upon year upon year the suppression of precious metals marches on.

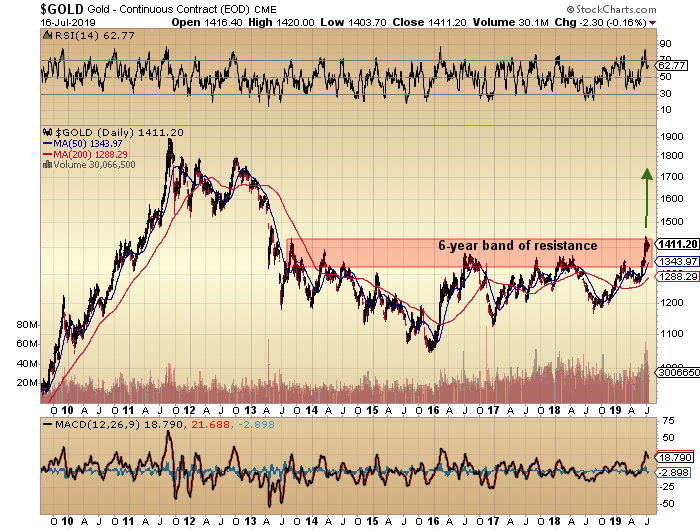

However, in June 2019, there was an event that broke the shackles of price management for gold with the near-magical surge to $1,442/ounce, finally vacating a six-year band of resistance despite heavy shorting by the Commercials and a seriously underperforming silver market. With the HUI now above 200 for the first time since January 2018, it needs to get above 225 to set up the assault on 280, the August 2016 high. Of major significance to the physical metals is this: The miners must lead the charge to the 2016 highs, assuming the leadership role and the gold-to-silver ratio (GTSR) must be in full descent as it happens.

This brings us right back to the term “relevancy,” and the debate over whether any real bull market in gold can sustain itself without participation by silver. You notice I use the term “participation” as opposed to”outperformance,” and that is noteworthy because integral to any sustainable and trustable advance in gold has historically been silver’s role as the superstar.

In 2009, I was long gold, and every morning I looked at the percentage gain in both metals and was delighted to see silver consistently outperforming gold on its advance post-GFC from under $9/ounce to nearly $50/ounce by 2011. The great debate going on with technical types, fundamentalists, CTAs, and historians (like me) is whether or not the silver price is today relevant to gold’s future performance. It is no longer a question of why silver has lagged so dreadfully; everyone points to JP Morgan or China or base metal byproduct supply as possible answers. But for me, anchored perhaps incorrectly in the biases of past bull markets, it is especially difficult to charge into a 50-car position in August gold with the GTSR over 90. For me, the silver price is absolutely relevant to the gold price, but more so to the gold price riskand for all of us so unmercifully bludgeoned by precious metals drawdowns over the years, no amount of megaphone-fueled, pom-pom waving, siss-boom-bah cheerleading will remove silver’s relevancy from my analytical cement mixer.

To wit, the one argument to which I am oh-so-slowly swinging is that gold can be a leader in the early stages of precious metals bulls, with silver being the late-cycle bloomer that at once captivates the retail hordes and signals the maturity of the bull move. Since 2015, I have been using a set of rules that blissfully allowed me to avoid the drawdowns that have sent so many gold/silver bulls to the emergency room with terminal injuries to net worth, from which recovery would be impossible. While the rules worked wonderfully, the June skew in their predictive value was an important omen for me, so I have no choice but to revert back to “full-on” bull market tactics, as opposed to “protect-principal” trading range tactics.

So, here is what I am driving at: The trade that I am slowly teeing up is in silver. Gold is in an unbridled, unassailable, accelerating bull market and one that will drag silver, irrespective of JPMorgan or China or base metals supply, to new recovery highs above the 2016 highs at $20.26. Gold is the fleeting leader that will forfeit its dominance to silver as the second major up-wave kicks into gear. Silver should be able to seize the mantle of dominance by the end of the summer, and the key will be its performance during the seasonally weak month of July. So far, it has been a distinct improvement over the May-June window.

The COT structure for silver is far friendlier than it is for gold; Commercials appear poised to let silver advance while they are markedly hostile to gold. As you can see from the red rectangles shown above, the alligator jaws depicting heavy Commercial shorting into heavy Large Spec buying in April 2017 and February 2019 are today muted and indicative of a price shock to the upside.

That is what I am predicting and that is why I am accumulating the iShares Silver Trust (SLV:US), as well as the August and December $15 calls. Now, the true silver aficionados would tell you that SLV has zero physical silver and therefore is devoid of purpose relative to our mission to protect against the debasement of purchasing power of currency. However, if in U.S. dollar-denominated terms SLV moves from $14.54 to 24.54, the trade will be satisfactory to the extent that the profits from the paper trade will allow me to exchange paper for physical silver, thus enabling the safe-haven utility while increasing the number of silver ounces sitting instructively idle in my safe.

The time to have been aggressive was in that first explosive shot to $1,375 off the December 2015 bottom at $1,045, and make no mistake, I was. I rode the wave until mid-May 2016 and then exited when the Commercials decided to lower the boom, which they certainly did by August. Four more times the cretins capped assaults to $1,3501,375 and all four times, I was flat all of the leveraged positions before they took them right back down.

Since the top in 2016 at 280 the HUI has tried to rally four times, and all four times, the HUI crashed right back down again. For this advance to be truly different, silver must take the reins of the beast and simply take off, and therein lies the speculative shot I am taking. Tactics from pre-June 2019 are to be discarded in favor of those from pre-August 2011. Dipsany and allare to be bought, with sales only into relative strength index (RSI) spikes into the 85-90 ranges.

Ladies and gentlemen, conditions have changed; the tone and texture of the market has changed; and I have changed in all aspects related to strategy as we move forward. The current consolidation for gold is more so a particularly compelling buying opportunity for silver, on the expectation that silver rejects the gold correction and instead leads the entire complex out of this pregnant pause and upward to new recovery highs, flipping the algobots and the Millennial traders to “bullish” while forcing tens of millions of social media sheep into the silver trade thanks to their undying loyalty to the “safety of crowd investing.”

With the Fed about to cleave another fifty beeps off the funds rate in an effort to drive down the U.S. dollar, aiding U.S. exports while attempting to steepen the yield curve, it is obvious to me that they are completely out of control as to policy, as to purpose, and as to implementation. The conclusion I draw is that it is not the hard assets investor that is rapidly becoming irrelevant; it is the Fed. Once recognized, it is important. Once acted upon, it is crucial.

I leave you with a memorable quote from Ayn Rand, with the suggestion that everywhere you see the word “gold,” simply insert “silver”:

“Whenever destroyers appear among men, they start by destroying money, for money is men’s protection and the base of a moral existence. Destroyers seize gold and leave to its owners a counterfeit pile of paper. This kills all objective standards and delivers men into the arbitrary power of an arbitrary setter of values. Gold was an objective value, an equivalent of wealth produced. Paper is a mortgage on wealth that does not exist, backed by a gun aimed at those who are expected to produce it. Paper is a check drawn by legal looters upon an account which is not theirs: upon the virtue of the victims. Watch for the day when it bounces, marked: ‘Account Overdrawn’.” Ayn Rand

Buy silver.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

The study results and their meaning are reviewed in an H.C. Wainwright & Co. report.

In a July 10, 2019 research note, H.C. Wainwright & Co. analyst Yi Chen reported that Check-Cap Ltd.’s (CHEK:NASDAQ) C-Scan showed “statistically better polyp-detecting sensitivity than the fecal immunochemical test (FIT).”

This superiority over the FIT, a commonly used screening test, was demonstrated in the recently completed study, initiated following CE mark approval in January 2018.

Chen reviewed how the study worked and the outcome. It was a multicenter, open-label trial involving 142 patients. Ninety of them were evaluable and either had or were at average risk for polyps. Each patient ingested a C-Scan capsule, took an FIT and underwent a colonoscopy, done by independent gastroenterologists, for comparison. Results of the C-Scan and FIT were compared to those of the colonoscopy. Only mild, no serious, events were noted during the study.

As for the findings, Chen relayed that in patients with polyps greater than or equal to 10 millimeters (10 mm) in size, C-Scan had a sensitivity, or ability to correctly identify persons with polyps, of 76% (p=0.0005), more than double that of the FIT at 29% (p=0.005). Regarding specificity, the ability to correctly identity persons without polyps, C-Scan’s rate was 82%; FIT’s was 96%.

Also, in patients with polyps greater than or equal to 40 mm in size, C-Scan detected all four patients who had them whereas the FIT detected only one patient. Chen highlighted that these results show C-Scan has clinical value when it comes to identifying patients with large polyps, those most likely to become malignant.

Of note, however, C-Scan also showed superior sensitivity to the FIT in patients with smaller polyps, Chen pointed out. C-Scan’s sensitivity among all of the study patients, even those having polyps smaller than 10 mm in size, was 66% (p=0.01) whereas the FIT’s was 23% (p<0.0001).

“C-Scan has the potential to meet the unmet medical need for a patient-friendly and preparation-free screening option for precancerous polyps,” the analyst added.

Chen noted that the U.S. pilot study of the C-Scan system is underway, at the New York University School of Medicine and the Mayo Clinic. The intent is to measure the number of device and procedure-related serious adverse events that occur and quantify both participant satisfaction and noncompliance. Results could be available in late 2019/early 2020.

“We believe [C-Scan] has the potential to increase the number of adults screened for colorectal cancer by eliminating common barriers and allowing for early detection of polyps without the use of colonoscopy,” added Chen.

H.C. Wainwright & Co. has a Buy rating and a $15 per share price target on Check-Cap. The stock is currently trading at around $2.20 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from H.C. Wainwright & Co., Check-Cap Ltd., Company Update, July 10, 2019

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Yi Chen, Ph.D. CFA and Raghuram Selvaraju, Ph.D., certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Check-Cap Ltd. (including, without limitation, any option, right, warrant, future, long or short position).

As of June 30 30, 2019 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Check-Cap Ltd.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The Firm or its affiliates did receive compensation from Check-Cap Ltd. for investment banking services within twelve months before, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

H.C. Wainwright & Co., LLC managed or co-managed a public offering of securities for Check-Cap Ltd. during the past 12 months.

The Firm does not make a market in Check-Cap Ltd. as of the date of this research report.

H.C. Wainwright & Co., LLC and its affiliates, officers, directors, and employees, excluding its analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research report.

Seattle Genetics announced a 28.3% increase in net sales for its second quarter 2019 powered by ADCETRIS sales along with a promising pipeline.

After the close of trading Tuesday, Seattle Genetics Inc. (SGEN:NASDAQ)reported financial results for Q2/19 and the H1/19. In the announcement, the company also highlighted ADCETRIS (brentuximab vedotin) commercialization and clinical development accomplishments and progress with its late-stage clinical programs for cancer.

The firm’s President and CEO Clay Siegall, Ph.D advised that “in the second quarter, we achieved record ADCETRIS net sales in the U.S. and Canada, reflecting growth in frontline CD30-expressing peripheral T-cell lymphomas as well as frontline advanced Hodgkin lymphoma.” Mr. Siegall added that “the biologics license application for enfortumab vedotin was submitted to the FDA for patients with locally advanced or metastatic urothelial cancer, taking us another step closer to becoming a multi-product oncology company, and we expect to report top-line data from the tucatinib pivotal trial, HER2CLIMB, in HER2-positive metastatic breast cancer later this year and from the tisotumab vedotin pivotal trial, innovaTV 204, in metastatic cervical cancer in the H1/20.”

The company stated that revenues in Q2/19 and H1/19 ending June 30, 2019, increased to $218.4 million and $413.6 million, respectively, compared to $170.2 million in Q2/18 and $310.8 million for H1/18.

Highlighted in the report was that ADCETRIS net sales for the U.S. and Canada in Q2/19 were $159.0 million, a 30% increase over the $122.4 million Q1/18. Royalty revenues in Q2/19 were up 16% to $23.3 million over $20.6 million in Q/18. Amounts earned under the company’s ADCETRIS and ADC collaborations increased as well to $36.1 million in the second quarter of 2019, compared to $27.2 million for the same period in 2018.

According to the company, Seattle Genetics flagship product is ADCETRIS (brentuximab vedotin), “which utilizes the company’s industry-leading antibody-drug conjugate (ADC) technology and is currently approved for the treatment of multiple CD30-expressing lymphomas.” “ADCETRIS is commercially available in 72 countries is approved in the U.S. for six indications including use as frontline therapy for Stage 3 and 4 Hodgkin lymphoma (HL) and CD30-expressing peripheral T-cell lymphomas (PTCL).”

The firm ‘s pipeline includes a potential second approved drug in the EV-201 pivotal trial of enfortumab vedotin in metastatic urothelial cancer, and plans to submit application for approval to the FDA in 2019. It also is working on other late-stage programs targeting solid tumors in HER2-positive metastatic breast cancer and metastatic cervical cancer.

The market appears to be quite pleased with the reported results as SGEN shares opened higher today at $69.89 (+$6.71, +10.62%) over Tuesday ‘s closing price of $63.18. The company’s shares have traded more than 18% higher today on higher than average volume between $6975.06/share and are presently trading at $74.85/share.

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

A description of the asset and its potential are provided in a Dawson James report.

In a July 11 research note, Dawson James Securities analyst Jason Kolbert reported that coverage of DelMar Pharmaceuticals Inc. (DMPI:NASDAQ) transferred to him and, subsequently, he issued a lower target price on the company, $3 versus $4 per share. In comparison, the Buy-rated biopharma is trading today at about $1.37 per share.

Kolbert described the firm’s lead drug candidate and its initial target indication. DelMar is developing VAL-083, a first-in-class small molecule chemotherapeutic for glioblastoma multiforme (GBM). The agent is a “bifunctional alkylating agent that causes DNA methylation of guanine at the N7 position,” he explained.

The analyst purported that VAL-083 is “a good asset and is supported by plenty of patient-based data.” Since it was introduced in the 1970s, it has been evaluated in more than 40 clinical trials and given to more than 1,000 patients, he relayed. Data from the National Institutes of Health have shown it to be efficacious against brain and lung tumors, melanomas and sarcomas as well as safe.

GBM is the most common type of brain tumor occurring in adults. Each year, 29,000 people in the U.S. and the European Union are diagnosed with it. It is frequently inoperable and associated with a poor prognosis.

Kolbert noted a key characteristic of VAL-083 that could make it superior to the current standard of care for GBM, Temodar (temozolomide). Temodar damages the DNA of cancer cells, and GBM cells respond by turning on multiple DNA repair pathways, including MGMT, to demethylate the DNA. As a result, patients can develop resistance to Temodar and, consequently, have a poor treatment outcome.

Unlike Temodar, MGMT does not repair VAL-083, Kolbert highlighted. In clinical trials, VAL-083 overcame MGMT-related resistance and was shown to be more potent against brain tumor cells than Temodar. “This suggests that VAL-083 has the potential to significantly benefit patients and create a higher, new standard of care for patients facing MGMT-unmethylated GBM,” Kolbert added.

Currently, VAL-083 is being evaluated as a treatment for GBM in Phase 2, open-label clinical trials with partner facilities to generate proof-of-concept data while managing operating costs, relayed Kolbert. With the MD Anderson Cancer Center, DelMar is pursuing a recurrent GBM study and a maintenance-stage GBM study. The trial in collaboration with the Sun Yat-sen University Cancer Center in China is on patients with newly diagnosed GBM.

“Based on the outcome of these two trials, VAL-083’s designated orphan and fast track status, we believe the company can raise the needed capital to run a pivotal program (by mid-2020),” commented Kolbert. Capital needed to advance VAL-083 is substantial. A recent raise generated $3.6 million, enough to support DelMar’s operations through year-end 2019.

About DelMar, Kolbert concluded, “We see little downside to the stock but recognize the challenges ahead for the company to raise capital.” DelMar’s valuation is “at a severely distressed level” with a market cap below $10 million.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures for Dawson James Securities, DelMar, July 11, 2019,

The Firm does not make a market in the securities of the subject company(s). The Firm has engaged in investment banking relationships with DMPI in the prior twelve months, as a manager or co-manager of a public offering and has NOT received compensation resulting from those relationships. The Firm may seek compensation for investment banking services in the future from the subject company(s). The Firm has NOT received any other compensation from the subject company(s) in the last 12 months for services unrelated to managing or co-managing of a public offering.

Neither the research analyst(s) whose name appears on this report nor any member of his (their) household is an officer, director or advisory board member of these companies. The Firm and/or its directors and employees may own securities of the company(s) in this report and may increase or decrease holdings in the future. As of June 30, 2019, the Firm as a whole did not beneficially own 1% or more of any class of common equity securities of the subject company(s) of this report. The Firm, its officers, directors, analysts or employees may affect transactions in and have long or short positions in the securities (or options or warrants related to those securities) of the company(s) subject to this report. The Firm may affect transactions as principal or agent in those securities.

Analysts receive no direct compensation in connection with the Firm’s investment banking business. All Firm employees, including the analyst(s) responsible for preparing this report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of the Firm and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

Analyst Certification: The analyst(s) whose name appears on this research report certifies that 1) all of the views expressed in this report accurately reflect his (their) personal views about any and all of the subject securities or issuers discussed; and 2) no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analyst in this research report; and 3) all Dawson James employees, including the analyst(s) responsible for preparing this research report, may be eligible to receive non-product or service specific monetary bonus compensation that is based upon various factors, including total revenues of Dawson James and its affiliates as well as a portion of the proceeds from a broad pool of investment vehicles consisting of components of the compensation generated by investment banking activities, including but not limited to shares of stock and/or warrants, which may or may not include the securities referenced in this report.

Chile’s central bank left its monetary policy rate steady at 2.50 percent but said it may be necessary to “extend the current monetary stimulus” if the current trend of low inflation continues, with the magnitude of any easing to be assessed in the next quarterly monetary policy report. The Central Bank of Chile, which surprised economists by cutting its rate by 50 basis points in June, said information since its last policy report reflected “increased risks associated with the timely convergence of inflation to the target,” in particular inflation for services, and the “risks surrounding the future evolution of activity and demand, in a context of high external uncertainty.” At today’s board meeting a majority of its members voted to maintain the rate but board member Pablo Garcia voted to lower the rate by 25 basis points. The central bank publishes a monetary policy report every quarter and in the June report the forecasts for economic growth, investment and domestic demand for this year were lowered. Economic growth this year was seen between 2.75 percent and 3.5 percent, down from a range of 3.0 percent to 4.0 percent in the March report, and 2018’s 4.0 percent. In the first quarter of this year Chile’s gross domestic product stagnated from the previous quarter and on an annual basis GDP growth eased to 1.6 percent from 3.6 percent in the fourth quarter of last year. Data for the second quarter point to “less than expected dynamism,” the central bank said, due to a poor performance by the mining sector and additional downside risks may be expected in coming months. Exports had also contracted more than expected due to weakness in its trading partners, with growth expectations in the EES survey being lowered for this year and next year. Chile’s inflation rate was steady at 2.3 percent in June and May, below the bank’s 3.0 percent target, and inflation expectations for the end of this year and in 12 months have declined. Chile’s peso has risen slightly this year and was trading at 683 to the U.S. dollar today, up 1.6 percent since the start of the year.

The Central Bank of Chile released the following statement:

“In its Monetary Policy Meeting, the Board of the Central Bank of Chile decided to hold the monetary policy interest rate at 2.5%. The decision was adopted by the majority of its members, with the votes of Governor Mario Marcel, Vice-Governor Joaquín Vial, and Board members Rosanna Costa and Alberto Naudon. Board member Pablo García voted for lowering the policy rate by 25 basis points, to 2.25%. On the external front, the expectations of a more expansionary monetary policy stance have been consolidating in various economies, both developed and emerging, some of which have already taken action in that direction. This has occurred in a context in which inflation remains well contained in the developed world and there is ongoing general concern over the performance of the global economy. Incoming data from manufacturing, investment and foreign trade have brought a negative surprise in several economies, contrasting with information about employment, consumption and services, which shows no major changes in the main economies. In this scenario, long- term interest rates posted new declines, the stock markets increased and risk premiums tightened, while capital flows into emerging economies increased at the margin and the dollar tended to weaken against other currencies. Commodities have seen limited price increases since the last Meeting, copper and oil included. The evolution of the domestic financial market has been dominated by more expansionary monetary policy in Chile and by external developments. Peso- denominated long-term interest rates have dropped, stock returns have risen and risk indicators have declined. The exchange rate, with some volatility, is lower than it was at the last Meeting. In the credit market, housing loans dynamism is similar to the one of the past few months, while commercial and consumer loans have slowed down slightly. Meanwhile, interest rates on commercial and mortgage loans have diminished further, so they continue around record lows. The Bank Lending Survey of the second quarter reflects fairly stable supply conditions, while demand appears to be somewhat weaker in large companies and with moderate upswings in the segments of construction firms and housing financing. Regarding activity and demand, the information at hand for the second quarter points to somewhat less than expected dynamism, partly due to poor performance of mining and some specific factors. Some qualitative background indicators suggest that additional downside risks may be expected for the coming months. About consumption, imports of consumer goods have slowed down and consumers’expectations have deteriorated significantly (IPEC). The labor market shows no significant changes, the unemployment rate remains around 7% and various indicators point to increasing job creation. On the investment side, the favorable evolution of some elements related to business services contrasts with the moderation of sales of construction materials and business expectations (IMCE), which are still slightly below their neutral levels. On the other hand, exports contracted beyond expectations, partly reflecting the weakness of some trading partners. In this context, the growth expectations contained in the Economic Expectations Survey (EES) decreased for both this year and next.

The annual CPI variation remained at 2.3% in June, while core inflation (CPIEFE) continued to hover around 2% annually. Among core inflation components, it is worth noting the widespread drop in the prices of services, more closely linked to capacity gaps and labor costs. On the contrary, the goods component of the CPIEFE posted unexpected growth, although largely driven by tourist packages. As for inflation expectations, there is a decrease for both the end of 2019 and one year ahead. For two years ahead, while the EES median remained at 3%, the median of the Financial Brokers Survey dropped to 2.8%. The Board considers that information accumulated since the publication of the last Monetary Policy Report reflects increased risks associated with the timely convergence of inflation to the target over the policy horizon. In particular, due to lower services inflation figures, whose persistence is high relative to other CPI components and the risks surrounding the future evolution of activity and demand, in a context of high external uncertainty. In case these tendencies persist, the Board estimates that it will be necessary to extend the current monetary stimulus, in a magnitude to be assessed in the next Monetary Policy Report. Accordingly, it reiterates its will to conduct monetary policy with flexibility, so that projected inflation stands at 3% in the two- year horizon. The minutes of this Monetary Policy Meeting will be published at 8:30 hours Friday 2 August 2019. The next Monetary Policy Meeting will take place on 3 September and the statement thereof will be published at 18 hours the same day.” www.CentralBankNews.info

In this interview with Maurice Jackson of Proven and Probable, the president and CEO of a project generator working in the Goodpaster District of Alaska explains the rationale behind putting the company’s stock on sale.

Gregory Beischer: Hi Maurice, always good to be here.

Maurice Jackson: Always a pleasure to have you on the program, sir. As a reminder for our audience, in our last interview, we addressed claim staking Millrock Resources was conducting in the Goodpaster District of Alaska, which is becoming one of the most highly contested mining districts in the world.

Mr. Beischer, before we delve into today’s interview, please introduce us to Millrock Resources, a premiere project generator, and share the investment opportunity that the company presents to the market.

Gregory B.: We are a project generator/exploration company, so we develop early-stage exploration projects, but always, always find partners to share the natural risk that’s in early-stage exploration. That way we’re able to operate multiple projects at one time, and increase our chances of successfully finding an ore body that will greatly benefit Millrock shareholders.

The latest project that we’ve come up with is called the Goodpaster Project.

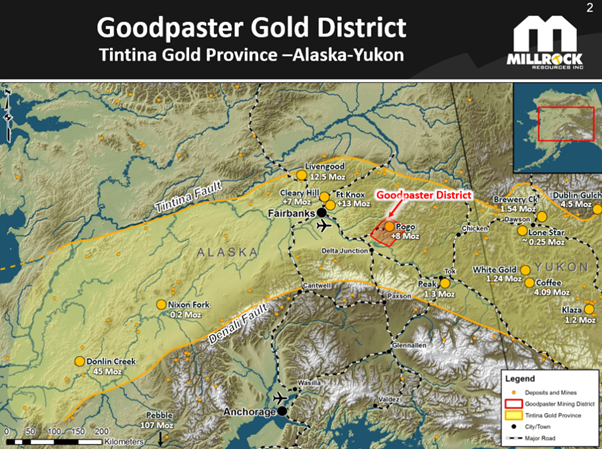

Maurice Jackson: We referenced the Goodpaster District of Alaska. Please provide us with some background on the district, and share with us where Millrock has been strategically positioning itself in the district.

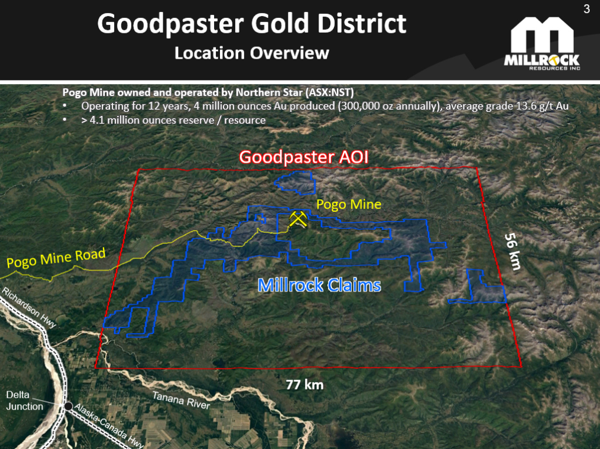

Gregory B.: Maurice, you and I have had several conversations about the Goodpaster District of Alaska. Right now, the best known and single mine in the Goodpaster District is the Pogo Gold Mine, and it’s a great mine. It produces several hundred thousand ounces of gold every year, and the concentration, or the grade of gold, is excellent. It’s close to half an ounce of gold for every ton that’s been mined, and the same going forward.

There’s a new owner, Northern Star Resources Ltd. (NST:ASX), an Australian company that seems to be making great changes to improve the profitability of the mine and, most importantly from our standpoint, made new exploration discoveries, one of which seems to be very, very close to the mutual claim boundary between Northern Star and Millrock.

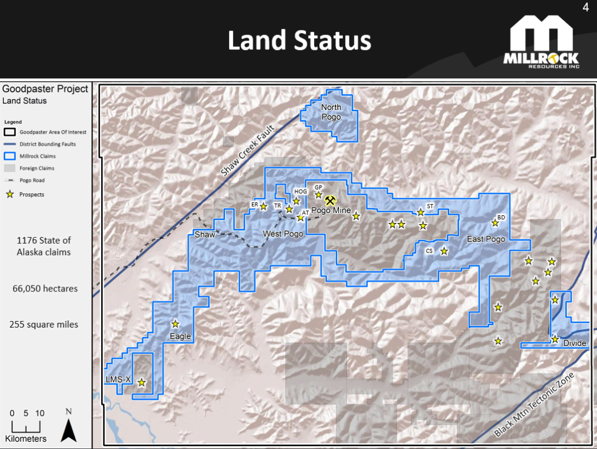

But we’ve staked a gigantic tract of claims, covering in excess of 660 square kilometers, over 255 square miles. So it’s a major piece of land that we’ve acquired. I’ll tell you, it’s not just moose pasture. We have a great database of information that we purchased with some claimed blocks years ago, and that’s paying off in spades, now.

Maurice Jackson: What are the latest developments from Millrock in the Goodpaster District?

Gregory B.: Well, we’ve been advancing the project and talking to potential partners that would fund exploration. But at the same time, we’re so keen on the West Pogo portion of this overall claim blockthe part that’s immediately to the west of the Pogo minethat we believe we should advance that project, or that block of claimsthat prospecta little bit further before we make an agreement with another company. It could be that there’s an ore body coming from the Northern Star ground right onto our claim block. We don’t want to give this one away prematurely, or too early, or too low on price. So, to improve the value, we’re going to put a little bit more of our own treasury in it. The thing is, we’re going to have to raise money to do that work.

Maurice Jackson: Mr. Beischer, when the thesis makes sense and the price is low, that’s called a sale. What would you like to tell shareholders regarding the opportunity that is before us right now?

Gregory B.: Well, Millrock stock is on sale. I mean, it’s painful to sell stock at this price when I know the company should be worth more. But I kind of feel like it’s the way things were back in early 2009. There was a really sharp downturn in 2008, and the Millrock share price got all the way down to $0.05$0.07. There were people that invested at that time, that believed in us. Within 12 to 14 months, our shares were trading at $0.80 or $0.90. Of course, the market was very helpful. The price of gold was going up, everything was suddenly great again in 2009. Those folks that invested in our company in early 2009, if they had sold in 2010 or 2011, made some really good profits. I think our share price exceeded $1, at one point. So those that had invested at a nickel did pretty darn well.

It’s sort of a similar, parallel situation now, except that I think Millrock is a much, much stronger company. We’ve got more experience. We’ve got a great team of people and we’ve got just a fantastic portfolio of gold projects.

Maurice Jackson: Millrock just announced that it will be raising capital through financing (press release). Please share the terms with us.

Gregory B.: The units will be sold at $0.075 each. A unit consists of one full share of Millrock and a warrant to purchase stock in Millrock in the future, at a certain specified price. That price will be $0.14 for the remainder of this year, $0.17 for the next year and $0.20 cents for the year after that. So it’s a pretty darn good deal for the investors. That warrant entices the capital to come to the company. That’s why we offer that, but I think it’s a great deal.

Maurice Jackson: Speaking of a deal, let’s compare that with what just occurred in April with EMX Royalty Corp. (EMX:TSX.V; EMX:NYSE.American). Back in April, Millrock Resources formed a strategic alliance with some prudent capital, and that would be EMX Royalty, as they’ve demonstrated confidence in Millrock’s potential in the Goodpaster District. Please share the terms with us.

Gregory B.: Sure. I know that you know EMX Royalty pretty well, Maurice, and so do we. We admire that team and the great success that they’ve had, and we hope to emulate that success. They’re a pretty darn good technical team and smart business people. I know you’re actually a shareholder of EMX, as am I, personally.

EMX invested in Millrock. They made a strategic investment. We came to them with the idea for the Goodpaster Project, but we needed capital to execute on the staking of the giant claim block. They provided that capital. In fact, they provided that capital at a premium to the market price of Millrock, at $0.14 a share. But there was a catch, and that was that we had to grant to EMX a modest royalty. It’s not a big one, but it’s enough that it enticed them to pay the extra price for Millrock.

It was, I believe, a win-win for our two companies. If there’s an ore body on the claims that we’ve staked, EMX and its shareholders will benefit, in addition to the great benefits that Millrock shareholders would get.

Maurice Jackson: For the record, we participated in the last two financings with Millrock Resources, and we’re going to make it a third, as we will be participating in full confidence in this round of financing with Millrock.

Before we close, on a personal note, Mr. Beischer, a number of shareholders have been inquiring about Melanie Henderson, a valued member of the Millrock team who’s been undergoing some health concerns. Can you provide us with an update, sir?

Gregory B.: Well, yes. Melanie did have surgery several weeks ago now. It was quite serious surgery, but I heard from her yesterday that she’s getting stronger and stronger every day, and it looks like she’s going to have one of the best possible outcomes that could be hoped for. So, it might still be a little while before she’s back in action, but we’re all cheering for her, and we’re all looking forward to seeing her bright, smiling face again.

Maurice, let me say, I personally really appreciate your continued confidence in Millrock, that you’ll be investing yet again. I know that some of your followers might also like to participate in such a financing. If they’re an accredited investor, we would be glad to allocate a certain part of the financing to your followers. You’re welcome to pass on my e-mail information, so that they can contact me, if you like.

Maurice Jackson: We will certainly do that, sir. For our audience members, the e-mail address is [email protected]. In the subject line, simply put in Millrock Resources.

And I just want to go back to Ms. HendersonMelanie, that was some welcome news that Mr. Beischer just shared with us, and on behalf of all of us, we wish you a speedy recovery and you’re in our hearts and prayers.

Mr. Beischer, for someone listening that wants to get more information on Millrock Resources, please share the contact details.

Maurice Jackson: Millrock Resources is a sponsor of Proven and Probable, and we are proud shareholders for the virtues conveyed in today’s message.

As a reminder, I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio from physical delivery, offshore depositories, precious metal IRAs, and private blockchain distributed ledger technology. Call me directly at (855) 505-1900 or you may email [email protected].

Finally, we invite you to visit provenandprobable.com, where we provide mining insights, and bullion sales. Gregory Beischer of Millrock Resources, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Millrock Resources and EMX Royalty. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Millrock Resources and EMX Royalty. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Millrock Resources and EMX Royalty, companies mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

By CentralBankNews.info South Africa’s central bank lowered its benchmark repurchase rate by 25 basis points to 6.50 percent amid an economic slowdown and said future policy decision will continue to be highly dependent and sensitive to the risks to the outlook and seek to anchor inflation expectations near the midpoint of its target “in this persistently uncertain environment.” It is the first rate cut by the South African Reserve Bank (SARB) since March 2018 and follows a rate hike in November 2018. While SARB Governor Lesetja Kganyago said the risks to growth and inflation were balanced in the near term, he is clearly concerned about the possible negative impact of any escalation of trade tensions and the absence of structural reforms – that are beyond the scope of monetary policy – that are limiting investment prospects. The rate cut was widely expected by investors and economists after the economy shrank by 3.2 percent quarter-on-quarter in the first quarter, inflation is steady and inflation expectations have declined, and the exchange rate of the rand has risen. SARB’s quarterly projection model shows one cut to the repo rate by the end of the fourth quarter. South Africa’s inflation rate has remained around the midpoint of its target range of 3.0 to 6.0 percent with the latest forecast lowered slightly to an average 4.4 percent for this year, down from 4.5 percent seen in April. For 2020 and 2021 the inflation forecast is unchanged at 5.1 percent and 4.6 percent, respectively, with inflation seen peaking at 5.4 percent in the first quarter of 2020. In May South Africa’s headline inflation rate rose to 4.5 percent from 4.4 percent in April. “The MPC welcomes the continued downward trend in recent inflation outcomes and the moderation in inflation expectations of about one percentage point since 2016,” said Kganyago, who this month was appointed for a second 5-year term after a bruising row within the governing African National Congress party (ANC) over SARB’s mandate and role in the economy. After shrinking in the first quarter, mainly due to electricity shortages and labour strikes, SARB expects a rebound in the second quarter though low business confidence remains a concern. SARB lowered its outlook for growth this year to an average 0.6 percent from May’s forecast of 1.0 percent, with the outlook for 2020 and 2021 unchanged at 1.8 percent and 2.0 percent, respectively. Since the monetary policy committee’s last meeting in May, South Africa’s rand has risen 3.3 percent against the U.S. dollar but on improved sentiment towards riskier assets, SARB still considers it slightly undervalued, with domestic growth and fiscal risks high on investors’ list of concerns. The rand rose in response to SARB’s rate cut to trade at 13.89 to the U.S. dollar, up 3.9 percent this year. The South African Reserve Bank issued the following statement from its monetary policy committee and its governor, Lesetja Kganyago:

Since the May meeting of the Monetary Policy Committee (MPC), near-term indicators point to weaker-than-anticipated global economic activity. Global financial conditions have eased, as central banks in advanced economies signaled a move towards monetary accommodation. However, downside risks remain and are dominated by escalating trade and geo-political tensions.

In the domestic economy, GDP contracted in the first quarter due to a combination of supply-side and demand-side factors. Monthly inflation outcomes have stayed around the mid-point of the inflation target range, as food and services price inflation remain subdued. The medium-term inflation outlook is unchanged.

The year-on-year inflation rate, as measured by the consumer price index (CPI) for all urban areas, was 4.5% in May (up from 4.4% in April). Goods price inflation was 4.2%, while services price inflation was 4.6%. The Bank’s measure of core inflation, which excludes food, fuel and electricity, was 4.1%. Producer price inflation for final manufactured goods decreased to 6.4% (compared to 6.5% in April).

The inflation forecast generated by the SARB’s Quarterly Projection Model (QPM) is for headline inflation to average 4.4% in 2019 (down from 4.5%). The projections for 2020 and 2021 remain unchanged at 5.1% and 4.6%, respectively. Headline CPI inflation is expected to peak at 5.4% in the first quarter of 2020 and settle at 4.5% in the last two quarters of 2021. The forecast for core inflation is lower at 4.4% in 2019 (down from 4.5%), 4.7% in 2020 (down from 4.8%) and is unchanged at 4.5% in 2021.

Electricity, food and fuel price inflation have shaped the trend in headline inflation. The assumptions for Brent crude oil in the QPM have been revised down from US$69.50 to US$67 for 2019. The assumptions for 2020 and 2021 are unchanged at US$68. Fuel price inflation is expected to average 3.2% in 2019 and to peak at 13.1% in the first quarter of 2020. Although food price inflation has continued to surprise on the downside, it is expected to start rising from the end of 2019 and to peak at 5.6% in the second and third quarters of 2020.

Inflation expectations have continued to moderate. According to the Bureau for Economic Research (BER) second quarter survey, expectations are for headline inflation of 4.8% in 2019. Inflation expectations for 2020 and 2021 eased to 5.0% and 5.2%, respectively. Five-year-ahead inflation expectations remain unchanged at a historic low of 5.1%.

The inflation expectations of market analysts in the July 2019 Reuters Econometer survey have been revised lower to 4.5% (from 4.7%) in 2019 and 5.0% (from 5.2%) in 2020 and remain unchanged at 5.0% in 2021.

Market-based expectations implicit in the break-even inflation rates (i.e. the yield differential between conventional and inflation-linked government bonds) have declined significantly since our last meeting, reflecting a firmer exchange rate and subdued domestic and global inflation pressures. Five-year break-even rates decreased to 4.5% and ten-year break-even rates decreased to 5.3%, the lowest level since January 2015.

Global GDP is expected to average 3.3% in 2019 and stabilise around 3.5% from 2020. While global growth remains relatively healthy overall, recent indicators on trade and manufacturing have deteriorated sharply and a range of downside risks to growth remain. Growth in world trade volumes contracted for the fifth consecutive month, declining by 2.1% in April 2019. Trade tensions remain heightened, weighing on market confidence and lowering investment. Other downside risks include geo-political developments and high levels of corporate and sovereign debt. Across most countries, there is limited policy space to respond to shocks.

Inflation outcomes and inflation expectations in most advanced economies remain below targeted levels. Recent communication by the Federal Reserve Bank and the European Central Bank indicate that in the absence of significant shocks, monetary policy will remain accommodative over the medium term. However, market expectations of the extent of future central bank actions appear high, creating the risk of significant market volatility should these not materialise.

Emerging market currencies are firmer, reflecting a combination of US dollar weakness and shifting market sentiment. However, country specific factors remain important, with currencies of countries with stronger macroeconomic fundamentals having fared better.

Since the May MPC, the rand has appreciated by 3.3% against the US dollar, by 2.4% against the euro, and by 2.3% on a trade-weighted basis. The implied starting point for the rand is R14.30 against the US dollar, compared with R14.40 at the time of the previous meeting. At these levels, the QPM assesses the rand to remain slightly undervalued. While the rand has benefited from improved sentiment towards riskier assets, it underperformed its emerging market peers due to idiosyncratic factors. Domestic growth prospects and fiscal risks rate high among investor concerns.

GDP contracted by 3.2% in the first quarter, reflecting weakness in most sectors of the economy. The sharp quarterly decline was primarily caused by electricity shortages and strikes that fed into broader weakness in investment, household consumption and employment growth. Based on recent short term indicators for the mining and manufacturing sectors, a rebound in GDP is expected in the second quarter of 2019.

Continued low business confidence remains a concern for the MPC. The Absa Purchasing Managers’ Index averaged 46.3 points in the second quarter, remaining below the neutral level. The RMB/BER Business Confidence Index remains unchanged at 28 points. The SARB’s composite leading business cycle indicator continued to trend lower.

The SARB now expects GDP growth for 2019 to average 0.6% (down from 1.0% in May). The forecast for 2020 and 2021 is unchanged at 1.8% and 2.0% respectively.

The MPC assesses the risks to the growth forecast to be balanced in the near term but remains concerned about longer term risks. Investment prospects will continue to be limited in the absence of structural reforms. The escalation of trade tensions could have further negative impacts.

While some cyclical factors constrained recent GDP growth outcomes, the Committee remains of the view that current challenges facing the economy are primarily structural in nature and cannot be resolved by monetary policy alone. Implementation of prudent macroeconomic policies together with structural reforms that raise potential growth and lower the cost structure of the economy remains urgent.

The MPC welcomes the continued downward trend in recent inflation outcomes and the moderation in inflation expectations of about one percentage point since 2016. The Committee would like to see inflation remain close to the mid-point of the inflation target range on a more sustained basis, with inflation expectations also anchored around these levels.

The overall risks to the inflation outlook are assessed to be largely balanced. Demand side pressures are subdued, wages and rental prices are expected to increase at moderate rates and global inflation should remain low. In the absence of shocks, relative exchange rate stability is expected to continue.

However, the impact of upside risks to the inflation outlook could be significant. Global financial conditions can abruptly tighten due to small shifts in inflation outlooks in advanced economies and changing market sentiment. Domestically, the financing needs of State-Owned Enterprises (SOE) could place further upward pressure on the currency and long-term market interest rates for all borrowers. Food, electricity and water prices also remain important risks to the inflation outlook.

Against this backdrop, the MPC unanimously decided to reduce the repurchase rate by 25 basis points to 6.5% per annum with effect from 19 July 2019.

Monetary policy actions will continue to focus on anchoring inflation expectations near the mid-point of the inflation target range in the interest of balanced and sustainable growth. In this persistently uncertain environment, future policy decisions will continue to be highly data dependent, sensitive to the assessment of the balance of risks to the outlook, and will seek to look-through temporary price shocks.

The implied path of policy rates generated by the Quarterly Projection Model was for one cut of 25 basis points to the repo rate by the end of fourth quarter of 2019. The endogenous interest rate path is built into the growth and inflation forecast. The implied path remains a broad policy guide which could change in either direction from meeting to meeting in response to new developments and changing risks.”

Current situation:

Current situation: