Last week, all the majors dropped against the US dollar. The biggest loser was the Kiwi dollar (-1.89%), followed by the Aussie (-1.84%), the Swiss franc (-1.18%), the pound (-0.94%), the yen (-0.87%), the euro (-0.85%), and finally the Canadian dollar (-0.81%).

In Friday’s US session, the EURUSD pair dropped to 1.1122 following the release of American GDP data for the second quarter, which at 2.1% YoY, was better than predicted. The preliminary figures show that the economic slowdown is not as bad as expected.

Markets were pleased by this data as we approach the FOMC meeting on the 31st of July. The Federal Reserve is expected to lower the Federal Funds Rate by 25 base points to a range of 2.00 – 2.25%. This rate slash has already been factored in by markets, so Friday’s reaction was based on the assumption that the key rate will be lowered by 25 base points, rather than 50.

At the time of writing, the euro is trading at 1.1125. I’m predicting the pair to drop to 1.1100. On the 25th of July, when we had an ECB meeting and a press conference with Mario Draghi, we got an intraday range of 1.1101 – 1.1188. I reckon that trading will remain within this range today. The 112th degree at 1.1056 is a reversal level.

Markets have already factored in a 25-base-point reduction to the Fed’s key rate. The ECB is preparing a stimulus package for the Eurozone’s economy. According to Draghi, this will include a rate slash by mid-2020. Because of this, the euro remains under pressure, but this won’t last for long. This is because last week, US President Donald Trump called a meeting during which measures were discussed for weakening the dollar. Trump is concerned about currency manipulation by other central banks. White House economic advisor Larry Kudlow, however, has ruled out intervening on currency markets.

The prognosis for online exchange operator eHealth Inc. looks positive as the company reported a 101% increase in Q2/19 revenues over the prior year period and raised full year 2019 revenue estimates by $50 million to $365385 million, compared with previous guidance of $315335 million for 2019.

Private online health insurance exchange operator eHealth Inc. (EHTH:NASDAQ) posted better than expected results in its second quarter earnings report for the period ending June 30, 2019. The markets are reacting favorably to the news with the stock up over 25% following the report.

For Q2/19, the company indicated that Total Revenue increased by 101% to $65.8 million, compared to $32.7 million in Q2/18. The firm further reported a lower GAAP net loss of $5.8 million in Q2/19 versus a net loss of $12.0 million for the same period last year, and Adjusted EBITDA improved to $0.8 million in Q2/19 compared to ($10.1) million in Q2/18.

Revenue from the company’s Medicare segment was $52.3 million in Q2/19, representing a 105% increase compared to $25.5 million for Q2/18. During the same quarterly period the company noted that applications submitted for all Medicare products grew by 67% to 56,488, with approvals increasing by 78% to 52,559.

The company’s CEO Scott Flanders commented, “We delivered another strong quarter once again exceeding our expectations and building momentum in our Medicare business that has continued to scale rapidly accompanied by EBITDA margin expansion…Approved Medicare members grew 78% year-over-year, driving a 105% increase in Medicare revenue year-over-year and a significant increase in Medicare segment profit.”

The company updated its outlook for the full year ending December 31, 2019, noting, “Total revenue is expected to be in the range of $365 million to $385 million, compared with previous guidance of $315 million to $335 million. Revenue from the Medicare segment is expected in the range of $318 million to $333 million, compared with previous guidance of $281 million to $333 million. Revenue from the Individual, Family and Small Business segment is expected to be in the range of $47 million to $52 million, compared with previous guidance of $34 million to $38 million…assuming the impact of the non-cash charge related to an increase in fair value of the earnout liability in connection with eHealth’s acquisition of GoMedigap remains at $0.82 per diluted share, GAAP net income per diluted share for 2019 is expected to be in the range of $0.62 to $0.82 per share, compared with previous guidance of $0.60 to $0.79 per share”.

The company describes its business as a leading private online health insurance exchange where individuals, families and small businesses can compare health insurance products from brand-name insurers side by side and purchase and enroll in coverage online or by phone. Through its subsidiaries, eHealth is licensed to sell health insurance in all 50 states and the District of Columbia. Additionally, the firm offers educational resources, telephone support and online and pharmacy-based tools to help Medicare beneficiaries navigate Medicare health insurance options, choose the right plan and enroll in select plans online or over the phone through Medicare.com, eHealthMedicare.com GoMedigap and PlanPrescriber.com.

EHTH shares opened higher today at $101.99 (+16.51, +19.31%) from the prior day’s close of $85.48. Shares reached an intraday 52-week high price in early trading on higher than average volume and have traded between $98.50 to $108.48 today. Presently, shares are trading at $108.44 (+$22.96, +26.86%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The week ahead will mark the start of August. As a result, this week’s economic calendar will see a pickup in activity towards the second half. The data from the United States will be of particular importance as it includes the Fed meeting, payrolls, and data from the ISM.

On the economic front, the data from the Eurozone will cover monthly manufacturing and services PMI. The report covers the month of July and will show whether the Eurozone’s economy has been able to recover from the slump in the first half of the year.

Australia will be reporting on its quarterly inflation data this week. Expectations show that consumer prices might have advanced 1.5% during the three months ending June.

This increase comes amid higher fuel prices. There were similar trends in inflation across many other economies as well. Following the inflation report, on Friday, Australia’s monthly retail sales report will be coming out. Retail sales are forecast to rise at a higher pace of 0.2% during the month, from 0.1% previously.

Finally, Canada will also be reporting on the monthly trade balance figures. The data will showcase how Canada’s GDP might have performed during the month of June. This will give key information as investors adjust their expectations for Canada’s second-quarter GDP.

Canada’s imports are forecast to dip moderately while exports are expected to remain much lower. This could lead to a possible narrowing of trade balance data. In May, Canada’s trade balance was at 0.76 billion. Forecasts show that the balance could fall 1.50 billion in June.

Here’s a quick recap of what’s to come in the currency markets this week:

FOMC, ISM Manufacturing, and Payrolls to Keep USD Busy

A busy week lies in wait for the US dollar. The week starts off with Wednesday’s Federal Reserve monetary policy meeting. The FOMC will be deciding on cutting interest rates at this week’s meeting. Following an aggressive rate hike cycle, this will be the first-rate cut. The Fed funds rates will be cut from 2.50% to 2.25%.

The Institute of Supply Management will be reporting on the monthly manufacturing PMI numbers on Thursday. The ISM’s manufacturing index forecast remains optimistic and could rise to 52.7 in July. This follows an uptick from 51.7 in the month before. Manufacturing activity, as seen from the various regional indicators suggest a modest rebound, although underlying factors remain weak.

On Friday, the US nonfarm payrolls report will be released. Forecasts for the payrolls show an increase of 160k in July. This follows a 220k figure reported in June. While this figure is due for revision, the rebound in June’s payroll report indicates a possible strength in the labor market.

The unemployment rate in the US is expected to fall to 3.6% from 3.7% previously. Meanwhile, the average earnings are forecast to rise at a steady pace of 0.2% on the month.

BoE to Remain on the Sidelines

The Bank of England will also be holding its monetary policy meeting this week. But the FOMC meeting due on Wednesday will still overshadow the BoE’s meeting. Still, the BoE is unlikely to make any changes to monetary policy.

The Bank of England’s meeting comes amid a change of leadership in the UK parliament. With Boris Johnson now at the helm, the prospect of a no-deal Brexit has increased. BoE’s Carney is likely to remain on the sidelines until there is more clarity on the UK’s Brexit deal with the EU.

Besides their meeting, economic data from the UK is relatively quiet for the most part of the week. The BoE will be considering the uptick in the average earnings and a rather stable rate of inflation. This could potentially keep the officials on the sidelines.

The US dollar was seen closing last week with some solid gains. This came during the week, where the greenback already posted strong gains. Friday’s GDP report showed that the US economy grew 2.1% in the three months ending June 2019. This was slightly higher than the forecasts for a 2.0% increase. But the second-quarter data was still lower comparing to the first quarter’s 3.1% increase. The slightly better than expected data held the view that the Fed will cut rates by a quarter basis points only at this week’s meeting.

Euro Sinks on Strong USD and ECB Forward Guidance

The euro currency was seen trading weaker on Friday. The losses came a day after the ECB hinted at restarting its QE purchases and also cutting interest rates even lower. The stronger greenback following the GDP report also helped to keep the pressure upon the euro currency. Meanwhile, ECB forecasts said that they expect inflation to be around 1.7% in the longer term while forecasting a 1.3% average inflation rate for 2019.

Will EURUSD be Able to Rebound off the Lows?

EURUSD price action is currently near the previously established lows of 1.1140. The common currency is supported by the trend line and the horizontal support area as well. This could potentially trigger a short term rebound. However, price could remain caught within the range of 1.1250 resistance area. To the downside, a close below 1.1140 could signal further declines, as the EURUSD could test 1.1100.

Sterling Falls as Risk of a No-Deal Brexit Rises

Following the election of Boris Johnson as Prime Minister of the United Kingdom, the sterling is seen posting losses. This came amid reports of most of the cabinet members in Johnson’s administration being euro-skeptics. While the new administration wanted to negotiate a new Brexit deal, EU officials ruled out further talks. The British PM, however, said that the UK was committed to leaving the EU on October 31st.

GBPUSD at Risk of Falling to 1.20

The currency pair has been extending strong losses with Brexit now dominating the headlines once again. With price breaking below the initial support at 1.2426, the sterling remains dovish. However, the scope of the declines could be limited given the upcoming Fed meeting this week as well as the Bank of England’s monetary policy meeting.

Gold Pares Gains Ahead of Fed Meeting

The strong gains witnessed in gold is seeing a shift as price turns rather flat. The precious metal has been trading weaker. This comes as investors are now discounting just a quarter basis point rate cut. However, a lot will depend on how dovish the Fed will be at this week’s meeting.

XAUUSD Likely to Maintain a Flat Range

The precious metal has been consolidating near the resistance area of the 1431–1428 region. Price is likely to remain at these levels into Wednesday’s FOMC meeting. As a result, there is a downside risk that XAUUSD could slip to the 1404 level where support has been initially established. In the near term, we expect gold to hold flat ahead of further market developments.

This week – July 29 through August 3 – central banks from 10 countries or jurisdictions are scheduled to decide on monetary policy: Japan, Armenia, Bangladesh, Moldova, United States, Bulgaria, Brazil, Dominican Republic, Czech Republic and United Kingdom.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

On Wednesday 31 July the Federal Reserve may cut interest rates for the first time in over a decade, marking a significant reversal in policy from the tightening cycle that was first pursued by former Fed Chair Janet Yellen. While a rate cut seems like a done deal, markets are still puzzled about the scale of the cut.

As of today, investors forecast a 79% probability of a 25 basis points cut and a 21% likelihood of a larger 50 basis points cut according to CME Fedwatch Tool. Several economic data releases have shown a weakening of the US economy, but there’s still no apparent sign of a recession. While the US economic growth slowed to 2.1% in the second quarter compared to 3.1% in the first quarter, consumer spending remained strong, showing that Americans are not yet concerned about the impact of trade tariffs and slowing global economic growth. However, businesses have been curtailing their investments and if this becomes a trend, consumer confidence will eventually decline, leading to less spending in the future.

Overall, it doesn’t seem like there’s an urgency for a 50-basis point rate cut at this stage. It may even send the wrong signal if the Federal Reserve cuts rates aggressively. A large rate cut may indicate the Fed knows something others don’t, which will likely have negative consequences on asset prices and the US Dollar. Our base case scenario is to see a 25-basis point rate cut on Wednesday with further easing if economic data deteriorates further.

The Fed is not the only central bank aiming to ease monetary policy. This week we’re likely to see a shift from the Bank of England and Bank of Japan towards the same direction.

Trade talks to resume

Trade talks are finally back on the table. US Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer will kick off a new round of negotiations with their Chinese counterparty Vice Premier Liu He on Tuesday. Both parties know they are running out of time to prevent a sharper slowdown in the global economy, however, given the past experiences, investor sentiment isn’t too high. While resolving their core issues seems far from reach at this stage especially when it comes to China’s subsidies and technology transfers, markets need at least a sign of goodwill to prevent a sharp volatile reaction in financial markets.

Earnings and Economic data

The S&P 500 and Nasdaq Composite closed at record highs last week in the wake of better-than-expected earnings from tech giant Alphabet. It seems that equity markets are still running on at a sweet spot pace, and that’s likely to continue if earnings do not disappoint this week. One-third of the S&P 500 companies are due to announce results this week and Apple is likely to attract most of the attention, especially when it comes to iPhone sales.

On the data front, US jobs report will be under the investors’ radar, but given that it will be released after the FOMC policy announcement, it will have less of an impact on equities and FX markets. However, data released this week will be a good indicator of future Fed policy.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stock market advance resumed on Friday led by technology shares. The S&P 500 rose 0.8% to record high 3025.86, rebounding 1.6% for the week. Dow Jones industrial gained 0.2% to 27192.45. The Nasdaq advanced 1.1% to 8330.21 buoyed by 12% rally in Alphabet after better than expected quarterly sales report. The dollar strengthening accelerated despite the Bureau of Economic Analysis report US gross domestic product slowed from April to June. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 97.99 and is higher currently. Stock index futures point to lower market openings today

FTSE 100 leads European indexes gains

European stocks ended higher on Friday after the European Central Bank signaled it could lower borrowing costs to counter a slowdown in the euro zone. EUR/USD joined GBP/USD’s slide with both pairs lower currently. The Stoxx Europe 600 Index gained 0.4% Friday. The DAX 30 added 0.5% to 12419.90. France’s CAC 40 advanced 0.6% and UK’s FTSE 100 rose 0.8% to 7549.06.

Hang Seng leads Asian indexes retreat

Asian stock indices are mostly falling today ahead of resumption of US-China trade talks in Beijing Tuesday. Nikkei fell 0.2% to 21616.80 as yen resumed its climb against the dollar. China’s markets are retreating with China officials saying they hope U.S. creates positive conditions for trade talks: the Shanghai Composite Index is down 0.1% and Hong Kong’s Hang Seng Index is 1.1% lower. Australia’s All Ordinaries Index however extended gains 0.5% with the Australian dollar slide against the greenback reversed.

Brent futures prices are edging lower today on easing of Middle East tensions after weekend talks between Iran and major powers ended on a positive note. Prices rose on Friday on oil field services firm Baker Hughes report the number of U.S. oil rigs fell by three last week to 776: Brent for October settlement ended 0.2% higher at $63.37 a barrel Friday, nevertheless closing 1.5% higher for the week.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Brian Ostroff, a partner at Windermere Capital, in this interview with Streetwise Reports, discusses three companies in his portfolio that he believes are poised to benefit from the rise in commodity prices.

Streetwise Reports: Brian, you are a partner in Windermere Capital. Would you give us a brief introduction to the firm?

Brian Ostroff: Windermere operates two funds that are involved in the mining space. We are different than most funds in that most of the people involved have a technical background. Our partners in the fund are the former ore and concentrate trading team from the Pechiney Group. When Alcan bought Pechiney, they did a management buyout. So it today is a global offtaking group of traders focused primarily on the base metals. Its team is made up of mining engineers, geologists, logistical experts and people who really understand the business.

Windermere is the financial overlay. My colleague Chris Wright and I are the financial overlay, where we look at particular opportunities and, between the technical expertise and the financial expertise, make some decisions. We operate more like private equity. We are not active traders. We get involved in situations, very few, but the ones we get involved in we are usually the largest shareholder. We’re there for successive rounds of financing and look to advance companies usually to some liquidity event. In a lot of cases, our positions are so large in these companies that, again, it’s not something that we can necessarily get out of in the open market, so we try and drive the companies to some type of liquidity event.

SR: How many companies do you tend to have positions in at any one time?

BO: Typically it’s not more than about a half-dozen. There are typically two or three real drivers in our portfolio. It’s very concentrated. It’s really the private equity model more than the traditional hedge fund model.

SR: The last half dozen weeks have seen a large movement upward in the gold markets, and, more recently, in silver. Generally, what do you see going on in the precious metals and in broader commodities?

BO: Yes, we are starting to see some life come into the precious metals, probably long overdue. But I think this is a move that is not a flash in the pan and there is going to be some substance to it.

My logic behind that is gold is an interesting commodity; it’s fairly emotional. If you ask people what is it about gold that attracts them, you get a variety of answers. It’s a hedge against inflation; it’s a hedge against uncertain times and geopolitical unrest. Myself, I’m in the camp that gold is a currency. You basically have a choice. You can buy U.S. dollars or sterling or yen, or you can buy gold.

As I look at the world today, I see a whole bunch of central banks looking to devalue their currency. Whether it’s the U.S. or Canada or Europe, you basically have a rush to zero when it comes to the currencies. Gold doesn’t have a central bank, and there’s no one who can control the value of gold. And so gold in essence cannot participate in this rush to zero. So today, as an investor, as I choose currencies, there’s really, in my mind, only one currency that makes sense, which is the one that can’t be devalued. And so I think that’s why we’re starting to see a greater interest in gold.

I’ll add one other thing. Those who have historically not been fond of gold, one of the arguments they use is they want a return on their investments, and the problem with gold is it does not provide a return. The big change in that argument is today roughly $13 trillion of debt trades at a negative yield. In other words, investors basically pay governments for the pleasure of buying their bonds. So although gold does not give a positive yield, relative to all these other instruments that give a negative yield, all of a sudden, gold is providing a yield. So it seems to me that the backdrop is extremely constructive when it comes to gold.

You mentioned silver; I am a big fan of silver. One of the things that has been curious to a lot of people has been the relative underperformance of silver. We commonly watch the silver-gold ratio, which got up as high as 93, meaning it would require 93 ounces of silver to purchase 1 ounce of gold. Historically speaking, that is extremely high. Numbers would typically be around 60. So there is an opportunity for silver to catch up. And over the last few days, I think that’s what we’re starting to see.

I’ll also add that silver tends to be more of a speculator’s commodity, a retail commodity, whereas gold tends to be a big institutional, central bank commodity. Gold tends to move first, which we’ve seen, and then ultimately silver starts to play catch up. It is more volatile, and it moves a lot more dramatically. I think we’re starting to see some catch up.

I think there was a lot of doubt around the early moves in gold that we’ve been seeing now for the last four to six weeks. Investors have been burned before. They’ve heard for a long time about why the precious metals should move. So all of a sudden, gold started to move, and it moved and it moved, but I don’t think the speculators were buying it right away. But now, it seems as though this move is for real, and that has maybe enticed the more speculative end of investors to come in. And they tend to do it more with silver than they do with gold.

SR: Are there any other commodities you would like to talk about?

BO: A lot of your readers probably don’t watch the agricultural commodities all that much. Quite honestly, over the last few years they probably haven’t missed much, but to me, that’s been an area that has been interesting. At the end of the day, food is really what matters. Whether gold is $1,200 an ounce or $2,000 an ounce really doesn’t change anything for everyday living. People need to eat and livestock needs to be fed, etc. So it usually goes under the radar. The last five or six years have not been a particularly good time for the ag sector in general.

But we are definitely starting to see some signs of life. Corn as recently as about a week ago traded at a 40-year high. There are some events going on meteorologically that affect agriculturea tremendous amount of flooding in the Midwest that has basically submerged farmland, drought in central Canada, swine flu in Asia. We’re starting to see that play out in the food chain through grain prices and some other agricultural commodities.

Ultimately, the beneficiary of this is going to be fertilizer. Without fertilizer, there’s no food. The fertilizer market went through a very tough time from 2012 through 2017. But in 2018 things started to get considerably better.

When it comes to fertilizer, I’m a big bull on phosphate. Phosphate is a necessary component of fertilizer but unlike potash and nitrogen, which are pretty abundant, phosphate is not as abundant. In fact, most of the world is in deficit. North America, South America, Western Europe and most of Asia all have to import phosphate, and that phosphate comes from the Middle East and North Africa. We know historically the Middle East is not necessarily the most stable place in the world and any type of supply disruptions could really be an issue.

I know people don’t think about fertilizer much. And, as I always say, gold is sexy and oil is sexy, but you can’t eat gold and you can’t drink oil. At the end of the day, this is what really matters. For five years, no one paid much attention to phosphate and there wasnt any growth in production. It just didn’t happen because prices weren’t there. But demand continued to grow every year regardless of price and, all of a sudden, that demand started to overwhelm the existing supply. In 2018, the price of phosphate went up 25%, and I’m pretty bullish going forward.

SR: Let’s talk companies that are on your radar.

BO: I was just talking about fertilizer, so let’s start there. Arianne Phosphate Inc. (DAN:TSX.V; DRRSF:OTCBB; JE9N:FSE) is near and dear to my heart. Windermere owns just under 20% of the company. A couple of years ago, aside from my role at Windermere, I also became CEO of Arianne.

We talked briefly about phosphate, and I think it’s extremely compelling. Arianne has been able to advance its project in what has been arguably a very difficult time. They say that the cure for a low commodity price is a low commodity price, and that could definitely be said about phosphate. As the price continued to decline, more and more projects were given up on and expansions didn’t happen. And again, today we’re sitting at a place where people are now starting to ask where are we going to get the phosphate from.

So, unlike most phosphate, which comes from the Middle East and North Africa, Arianne’s project is in Canada. It is today the world’s single largest greenfield phosphate deposit and makes a very high-purity and environmentally friendly phosphate. This type of phosphate continues to be in demand, particularly as people tend to look a lot more at some of the environmental factors. It also sells for much higher prices. This project, over that five-year downturn, continued to move forward. Today, it is fully permitted. It has a collaboration agreement with the First Nations, has signed a couple of offtake agreements and is moving forward on the financing of its project. Also, of significant interest, about a month ago Arianne signed a memorandum of understanding (MOU) with a large Chinese group.

When it comes to phosphate, China has been viewed as being in equilibrium. It is a large producer of phosphate, and, of course, it’s a large consumer of it. Industry analysts now believe that China is heading into a deficit. I think that this is a game changer for phosphate and phosphate pricing. Today, India is the world’s largest importer. It has 1.3 billion people. China now looks like it’s going into deficit. That’s also over a billion people. Just those two countries alone represent about 35% of the world’s population. With the Chinese now looking as though they’re heading into deficit, they, too, are going to be out there looking to secure phosphate supplies.

With Arianne being the world’s largest greenfield deposit, it is I think a natural place for the Chinese to look. This MOU has been executed, and we are working toward a final agreement that in exchange for offtake and participation in the project, the Chinese would provide a large degree, if not all, of the financing. We will see where that goes.

I am encouraged. Arianne is a best-of-breed project, shovel ready. Today, it trades with a market cap of only about CA$60 million. It’s funny because Arianne was basically orphaned. As the phosphate market, from 2012 to 2017, declined, Arianne continued to move its project forward, but no one was paying any attention. So today, even at that CA$60 million market cap, it’s a fraction of what it was many years ago. The market cap today is lower than it was before the company had a bankable feasibility study, before it had its collaboration agreement with the First Nations, before it received its permits, before it had its offtakes, before it did this MOU. So to me, that is just incredible. The company trades at 4% of its net present value for a fully permitted, shovel-ready, best-of-breed project. To me, that is just as cheap as it gets. The one thing that arguably held it back was the overall macro, as we talked about earlier, and I think that’s changing, and the company should get a lot of attention.

SR: Upon completion of financing, how long would it take Arianne to get into production?

BO: It is a two-year construction period, at which point the company will then be producing 3 million tons (3 Mt) a year of concentrate. That is an extremely large mine. At today’s pricing, that would represent close to $500 million a year in revenue. In fact, it is projected to be the only large-scale independent phosphate mine to come into production over the next few years. Most mines are actually owned by the companies that make fertilizers; it’s a very vertically integrated business. But Arianne is independent, which I think is of interest to companies that are short phosphate rock and are looking for access in.

SR: Let’s go on to other companies that you’re excited about that would benefit from a rise in commodity prices.

BO: I’d like to turn my attention to a couple of silver names. As I said, I definitely have a soft spot in my heart for silver. Although gold may be the big brother, I think the opportunities really are in silver. One of the reasons for that is it is hard, short of getting into physical silver itself or an ETF, to find a decent equity way to play silver. Over the last few years, during the downturn, what we’ve seen is a lot of the silver companies go out and do deals in gold assets, such that as investors now look at how they can get exposure to silver, it is more and more difficult.

So in that area, one of our names that I like very much is a company called Defiance Silver Corp. (DEF:TSX.V). Windermere has been involved in the name for quite some time. It owns the San Acacio project in Mexico in Zacatecas. San Acacio was a past-producing mine over its extended history. That mine had produced 100 million ounces (100 Moz) of silver. It sits on the Veta Grande vein, and that vein has produced 200 Moz of silver.

What interested us about the San Acacio mine was historically the mine had produced down to a depth of about 175 meters (175m). We know that the neighboring mine had produced down to 300m. So for us, there was a decent level of comfort that we had a lot more mine life to go if we went to depth. That was the original reason for us getting involved in the project.

But in addition, one of the things that was very exciting to us and that we believe provides a lot of upside is that with Defiance’s property, there is a lot of potential laterally. Historically, the company had mined over a footprint of about 1 kilometer (1 km), but Defiance owns roughly 5 km of what could be lateral extension. So for us, the safe bet was at depth with the excitement being the ability to extend laterally. We are continuing to do some work there. It is I think a pretty exciting project. It is a silver play in Mexico, where I think that there is a lot of opportunity and interest.

Just as an idea of how starved the overall equity markets are for decent silver plays, back in that period that I talked about, late 2015 to middle 2016, Defiance was a well-known name, and when activity came back to the sector, which it did, Defiance at that point had moved, over that six-month period of time, from about $0.07 trading up close to $0.70. The project has continued to advance over the last couple of years during the tough times.

But now with interest coming back to the sector and people starting to look for silver names, I think Defiance will grab its share of attention. In fact, just over the last few days, as the silver market has improved, some attention has come back to Defiance, and the stock has started to perform much better, as well it should. Again, I think any decent silver asset in this upcoming market is going to perform extremely well.

SR: Do you want to go on to another company?

BO: The third company I’d like to talk about is Megastar Development Corp. (MDV:TSX.V). Megastar is early stage, but it’s a very interesting situation. Your readers may be familiar with David Jones. He is a very accomplished geologist with many finds to his name in Mexico. He was responsible for the discovery of Los Filos, which is Mexico’s largest gold mine, and El Limon, Torex Gold Resources Inc.’s (TXG:TSX) producing mine. He was on the board and involved with Cayden Resources Inc. at the time that it was acquired by Agnico Eagle Mines Ltd. (AEM:TSX; AEM:NYSE), and he had done most of the work around Switchback, which is owned by Gold Resource Corp. (GORO:NYSE.MKT) in Oaxaca.

Jones had developed a geological theory of what was going on in Oaxaca and based on these theories and work he had done on Switchback, he had assembled three properties in Oaxaca. Jones and I have known each other for a very long time. He alerted me to what he believed was some of this potential in Oaxaca and these properties and a deal was done to vend them into Megastar Development. Megastar can earn 100% of these three properties by doing some work and issuing some shares.

Unlike typical transactions where assets get vended into a company and then the company raises additional funds, Megastar had cash. With that, the company did not suffer that initial dilution usually seen in transactions of this type, but also flew under the radar screen. It was only about six weeks ago that the company did raise some funds, a small amount, to allow Jones to do some further work.

So now, Megastar is starting to get a little attention and the company just started to put out some of the results from his early-stage work. Jones is extremely excited by these initial findings, and they very much seem representative of what Jones was looking for and consistent with what we see at the Switchback mine and also Fortuna Silver Mines Inc.’s (FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE) San Jose mine in that district as well. Jones believes this is all part of a trend that had come to be as a result of the same event that created similar geology and that the opportunity is very strong.

I should also say that Megastar recently announced Bob Archer, the co-founder and CEO of Great Panther Silver Corp., joined the board. Archer knows very much what it is to found and build a successful silver company. He and I know each other quite well, and I alerted him to some of the things that Jones was up to. They had spent some time together, and I think Archer got pretty excited by the potential here, Jones’ theories and certainly these initial findings.

It is very early stage, of course, but it’s also a very small market cap. Today, the company is probably trading under a $5 million market cap for something that looks pretty exciting, and with a great pedigree between Jones and Archer. And for investors who like that early stage, where it’s high risk but very high return, Megastar would definitely be on my shopping list.

SR: Any parting thoughts for our readers?

BO: I’d just say I understand investors’ skepticism. It’s been a very tough period of time. Certainly, a lot of speculative money has fled the sector, going into things like cannabis and cryptocurrency and has really kind of taken the luster, if you will, off of the small-cap mining space. I do believe that we are at the early stages of a trend change. I think that as this sector starts to perform better, a lot of money can come in, and because the sector is as small as it is, you can really see some outsized gains.

SR: Thanks for your insights, Brian.

Brian Ostroff is a managing director at Windermere Capital, where he focuses on the junior and mid-tier mining sectors. He also serves as CEO of Arianne Phosphate. He brings over 25 years of small-cap mining expertise to the table, having served at RBC Dominion Securities and as a managing partner at Goodrich Capital, an M&A advisory firm.

Disclosure: 1) Patrice Fusillo conducted this interview for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She owns, or members of her immediate household or family own, shares of the following companies mentioned in this article: None. She is, or members of her immediate household or family are, paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this interview are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Brian Ostroff: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Arianne Phosphate, Defiance Silver and Megastar Development. I, or members of my immediate household or family, are paid by the following companies mentioned in this article: Arianne Phosphate as a result of my employment as CEO. Windemere has holdings in the following companies mentioned in this interview: Arianne Phosphate, Defiance Silver and Megastar Development . I determined which companies would be included in this article based on my research and understanding of the sector. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. 4) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Orthodontic and GP Dental medical device maker Align Technology announced a 24.6% increase in sales volume of its Invisalign products in its Q2/19 earnings report, but investors are not smiling much over China growth concerns as the shares of the company have fallen more than 25%.

Orthodontic and GP dental medical device maker Align Technology Inc. (ALGN:NASDAQ) yesterday announced second quarter earnings ended June 30, 2019. The firm reported total revenues in Q2/19 were $600.7 million, up 22.5% year-over-year. Operating income in Q2/19 was $176.5 million, up 43.8% year-over-year, resulting in an operating margin of 29.4% and a net profit of $147.1 million in the quarter, or $1.83 per diluted earnings per share (EPS). The firm noted that Q2/19 operating expense included a $51 million benefit from the ClearCorrect settlement with Straumann, which increased Q2/19 operating margin by approximately 8 points and benefited EPS by $0.57.

Invisalign volume in Q2/19 was 377,000 cases, up 24.6% year-over-year, composed of 16% growth in the Americas and 36.7% in international regions. Invisalign volume for teenage patients in Q2/19 was 103,700 cases, up 32.2% year-over-year, and Q2/19 scanner and services revenues were $104.0 million, up 82.4% year-over-year.

Align Technology President and CEO Joe Hogan said, “Our Q2/19 revenues were at the high-end of our guidance, reflecting Invisalign volume growth primarily from international doctors, as well as very strong sales from iTero scanner and services with Q2/19 Invisalign volumes up 24.6% year-over-year. . .In Q2/19, total Invisalign case shipments were lower than expected, primarily due to a softness in China related to a tougher consumer environment and slower growth in young adult case in North America…given the uncertainty in China, our outlook for Q3/19 reflects a more cautious view for growth in the Asia Pacific region.”

The company further provided guidance for Q3/19 for Net revenues in the range of $585 million to $600 million, up approximately 16%-19% over Q3/18 and Diluted EPS in the range of $1.09 to $1.16. Align also stated in the outlook that it expects to repurchase at least $100 million of its stock (shares) in the open market in Q3/19.

Align Technology is a medical device company that designs, manufactures and markets the Invisalign system, which according to the company is the world’s leading invisible orthodontic product,and and the iTero Intraoral scanning systems and services. The Invisalign system and iTero Intraoral scanning system and OrthoCAD digital services are available to general practitioner dentists, orthodontists and other dental specialists, and the firm provides training, clinical education programs and the tools needed for dental industry adoption.

Align’s Clear Aligner segment consists of its Invisalign System, Express/Lite (Non-Comprehensive Products) and Vivera Retainers, along with its training and ancillary products for treating malocclusion (Non-Case). The firm’s Scanner and Services segment consists of intra-oral scanning systems and other services available with the intra-oral scanners that provide digital alternatives to the traditional cast models and includes its iTero scanner and OrthoCAD.

ALGN shares opened much lower today at $219.28 (-$55.88, -20.63%) from yesterday’s closing price of $275.16, and traded down more than 25%, closing at $200.90 (-$74.26, -26.99%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Bob Moriarty of 321Gold profiles a precious metals ETF that has “absolutely obliterated its main competition.”

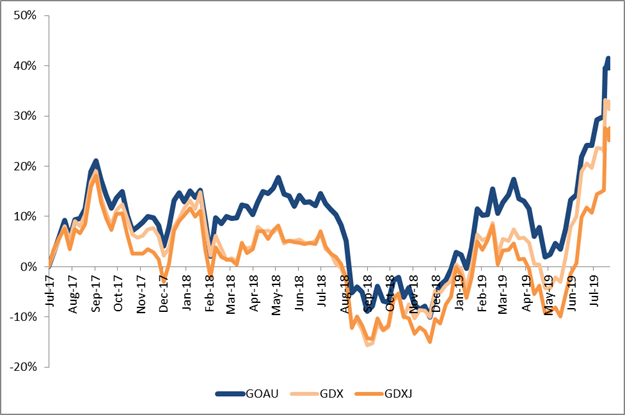

The U.S. Global GO GOLD and Precious Metal Miners ETF (NYSE: GOAU) just had its two-year anniversary at the end of June, and since inception, the fund has absolutely obliterated its main competition.

GOAU delivered a remarkable 41% since inception through July 24, crushing the hugely popular VanEck Vectors Gold Miners ETF (GDX) and VanEck Vectors Junior Gold Miners ETF (GDXJ), which were up 32.7% and 27.6% over the same period.

Some might call it beginner’s luck. I call it superior planning. Here’s why

Dummy Diversification

If you look at the construction of VanEck’s products, personally, I would describe them as dumb. The GDX and GDXJ are over diversified. GDX has close to 45 holdings while its junior counterpart has as many as 70.

In the senior ETF, Newmont Goldcorp is the number one holding at almost 12%, followed by Barrick at just over 10% and Newcrest at 6.5%.

The GDXJ is even more watered down. The top holding, Northern Star Resources, represents only 6% of the fund.

What it really comes down to is that both funds are market cap-weighted. That’s no way to build a gold fund, as I see it. No thought or analysis has gone into stock selection or weighting. Investors are getting little or no exposure to companies that are growing the fastest. The chart above makes that very clear.

Like I said: Dumb-as-bricks. VanEck takes you for a fool and is banking on you not having a clue. I hate to say it, but if you’re fine with this, you deserve what VanEck is selling.

An Emphasis on Royalty and Streaming Companies

GOAU just does things differently and, frankly, better. I like it a lot. Unlike the GDX and GDXJ, GOAU is a dynamic, rules-based gold ETF. As of my writing this, the ETF is concentrated in fewer than 30 names, all of them high-quality with strong balance sheets, and it’s rebalanced and reconstituted every quarter.

Obviously this is why it’s destroying its much larger competition. But there’s more to it.

GOAU is the first gold ETF that I know of that has such a large weighting in royalty and streaming companies. Approximately 30% of the fund is devoted to royalties.

If you don’t know what these are, I suggest you buy my latest book, Basic Investing in Resource Stocks: The Idiot’s Guide.I have an entire chapter on what makes royalty and streaming companies a solid bet in the gold industry. But in short, they help investors get exposure to gold and precious metals mining without taking on a lot of the risks that producers face.

Frank Holmes, CEO, U.S. Global Investors and a real “ground floor” investor, recognizes this better than most anyone else. As a young analyst in the early 1980s, he helped work on the IPO for Franco-Nevada (FNV), the very first such royalty company. He and his firm were also one of the seed investors in Wheaton Precious Metals (WPM)now the world’s largest precious metal streaming companywhen it debuted as Silver Wheaton in 2004.

He and his team back-tested five key success factors going back over 12 years to feel confident before launching GOAU. The back tests were very compelling in picking the best quality names every quarter.

Again, 30% of GOAU is spread between Franco, Wheaton and Royal Gold (RGLD), the leaders in the royalty industry.

The GDX’s exposure to royalty names, by contrast, is less than half that.

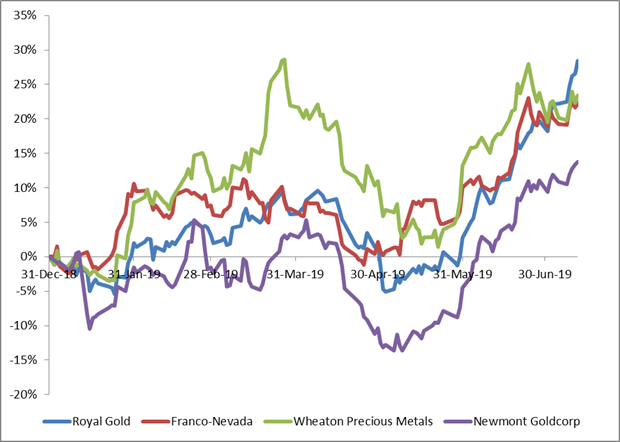

Check out Franco, Wheaton and Royal Gold’s year-to-date performance against that of Newmont Goldcorp, the largest holding in the GDX. That’s the difference GOAU provides.

If any of this sounds compelling to you which it should I highly recommend you learn more about the U.S. Global GO GOLD and Precious Metal Miners ETF (GOAU). You can do so by clicking here!

I have no financial interest in any of the GOLD ETFs but for a lot of investors they make sense. Do your own due diligence and again, feel free to read up on Gold ETFs in Basic Investing in Resource Stocks. We are solidly back into the gold bull and prices are going to go a lot higher.

Bob and Barb Moriarty brought 321gold.com to the Internet almost 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: Wheaton Precious Metals. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Newmont Goldcorp, Franco-Nevada and Royal Gold, companies mentioned in this article.

Current situation:

Current situation: