We have just released our latest of our MT4 Indicators. This is an indicator that shows the Percent Change of price. It uses a separate indicator window and can add up to 3 lines.

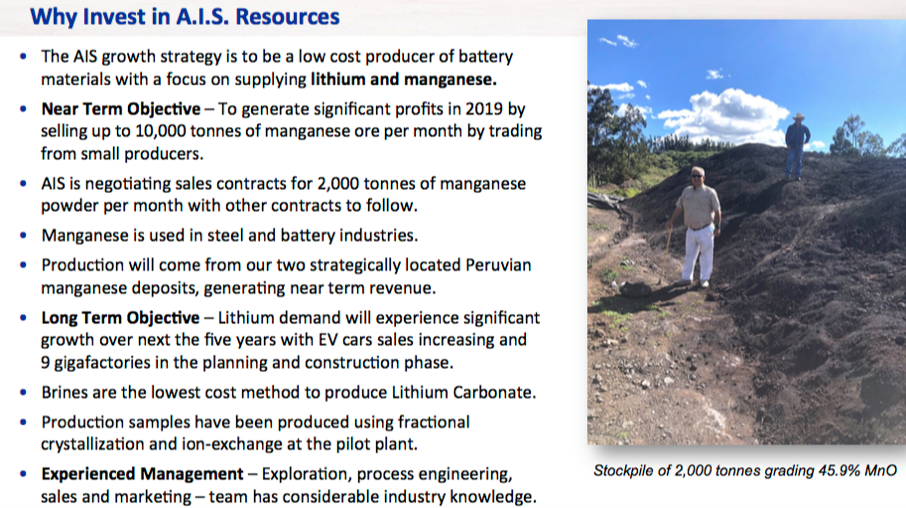

In this interview, CEO Philip Thomas of A.I.S. Resources discusses his company’s prospects in the lithium and manganese sectors with Peter Epstein of Epstein Research.

A.I.S. Resources Ltd. (AIS:TSX.V) is a lithium brine exploration and development company with projects in Argentina, and is setting up a potentially lucrative manganese (Mn) trading operation in Peru that could generate positive cash flow this quarter and well beyond. The market seems to like the near-term cash flow aspect; the share price took off on very heavy volume on July 23 based on this press release.

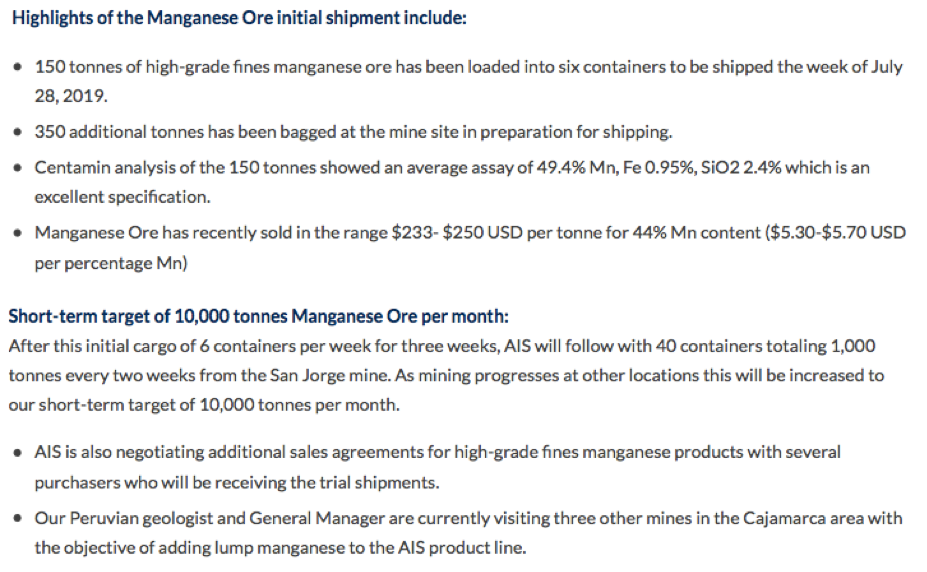

What on earth was in that release to cause a doubling in the share price to CA$0.13 per share (it has since pulled back to CA$0.09)!?! The prospects for near-term cash flow, possibly significant amounts relative to A.I.S.’ market cap, that’s what. Although just 150 tonnes of high-grade (49%) Mn fines ore has been loaded into six containers to be shipped the week of July 28, the press release discusses plans for 10,000 tonnes/month within about six to nine months.

Based on current Mn pricing and expected costs, A.I.S. should be able to make approximately US$100/tonne operating profit, or US$1 million per month (if /when selling 10,000 tonnes/month). In a sense, that’s all readers need to know. If the company can generate US$1 million per month, the current market cap of CA$7.3 million will prove to be way too cheap.

However, of course, there’s a lot of risk between a single shipment of 150 tonnes that has not even hit the water yet, and consistent delivery of 10,000 tonnes/month! For an update on the company’s lithium (Li) segment, and more on manganese trading, I spoke with CEO Philip Thomas. The following interview was conducted by phone and e-mail over an eight-day period ended July 24.

ER: Please give readers the latest update on your lithium project(s) in Argentina.

PT: We have two active locations in and around the Guayatayoc and Vilama Salars in northern Argentina, an area known as the Puna region. We sampled Vilama and obtained good surface results (145200 parts per million [ppm] Li), but we have yet to complete geophysics or drilling.

Guayatayoc has two concessions, Guayatayoc Mina and Guayatayoc III. We received a drill permit for Guayatayoc Mina (Mina) and drilled to a depth of 407 meters (407m). A number of small aquifers were encountered and lithium at low concentrations. The magnesium and potassium ratios were in a favorable range for future production.

Four more drill holes are planned (approximately 1 kilometer apart), which should allow us to deliver a maiden resource estimate in 1H 2020. If the drill program is successful, we will redrill the holes to turn them into 25-centimeter diameter production wells, and start a feasibility report.

In addition, we are examining other salars in Salta and Catamarca provinces that might be suitable for exploration.

ER: Can you explain further why you believe the A.I.S. project is more advanced than many lithium brine projects in Argentina?

PT: The A.I.S. team has many years of experience and is one of the few that have built large pilot plants and operated them. In 2004-8, when I was CEO of Admiralty Resources we gained a lot of experience in exploration and production, building ponds and lithium production chemistry. This extensive knowledge was advanced with work in a private capacity in the Pozuelos, Salinas Grandes, Pocitos, Hombre Muerto and Incahuasi salars.

At Guayatayoc we have processed enough brine in a pilot plant to produce 99.2% ithium carbonate at 77-82% yields, which has proven difficult for most other players. We have a complete capex and opex budget for a 10,000 tonne/year plant. Now we need to prove a lithium flow rate of 700 liters per minute and an average lithium grade of 250 ppm or higher.

ER: When is your final US$2.25 million payment due? How do you plan on paying that considerable amount?

PT: We are currently negotiating with Ekeko SA for an extension of the option on Mina and Guayatayoc III until February 2020. Between now and then, we are hopeful that our manganese business will accelerate so that we can generate cash flow to fund the $2.25 million payment and exploration to feasibility stage.

ER: Turning to manganese, why manganese and why Mn trading?

PT: Ninety-three percent of Mn is used in steel applications, but that number is slowly declining as lithium-ion batteries use more and more manganese. Mn is cheaper than cobalt and due to its multiple oxide states, it offers superior performance. Mn is prolific in Peru, where there is the ideal volcanic and sedimentary environment to host high-grade deposits.

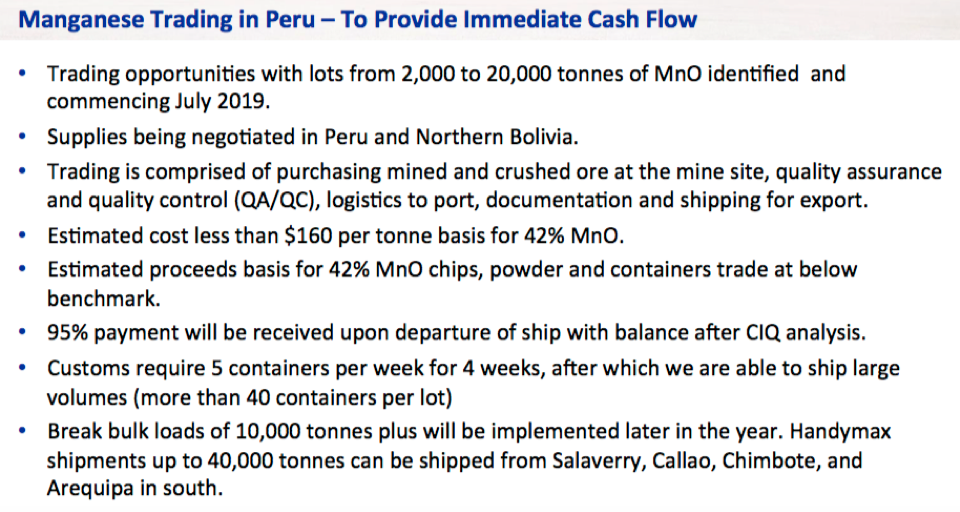

In Peru, we are looking for Mn miners of a reasonable size and we are assisting them with mine engineering, sales, documentation (which is exceptionally complex in Peru) and logistics support.

ER: Can you discuss at a high level what approximate tonnage you might be able to move and the potential economics of the operation?

PT: The main drivers of profitability are:

(1) Grade of manganesethe global benchmarks are 37% and 44%, as measured by Platts (2) Lumps, chips or fines (3) Transportvessels (break bulk 10,000+ tonnes) or containers (4) Impurities (less than 5% iron (Fe); 10% SiO2; carbonates)

Our latest press release reported that we delivered 49% Mn. At the San Jorge mine in Peru our contract miner now has two open pits with the objective of opening six. Production is ~500 tonnes/week, per pit. We are also reviewing additional properties under contract mining, joint venture (JV), or operating ourselves scenarios in the Cajamarca region. The aim is to take monthly lump production up to 5,000 tonnes per month, transported in break bulk vessels, and then 10,000 tonnes per month within about six to nine months.

The economics are simpleit costs US$140160 a tonne to buy the ore, transport it to Lima, and ship it to Tianjin or Qinzhou in China. The Platts benchmark for 44% Mnlumps in break bulk, CFR Tianjin, is US$5.90 per 1%. For fines in containers and bags it’s US$5.35 per 1%. So, at a 49% Mn grade, we receive $262 per tonne, less costs of say $160/tonne = ~$100/tonne operating profit. The larger the tonnage exported, the lower the cost/tonne as wages get spread over a larger production base.

ER: Is manganese trading a relatively short-term opportunity, or potentially a medium- to longer-term play?

PT: Good question. It’s a longer-term play. Initially we will be focused on the steel industry, but we will be ready to move to the battery industry as the opportunity arises. We have the chemical expertise to build electrolyte and cathode Mn materials, or contribution materials such as Mn sulphate used in cathode manufacture. Although only 10% of the global Mn market by volume, high-purity Mn makes up about 40% of global market value. It’s used in batteries, series 200 stainless steel, specialty alloys, fertilizers and trace nutrients.

ER: You are operating in a country (Peru) that many readers may not be familiar with. What can you tell us about working in Peru?

PT: Peru is probably the most advanced mining country in Latin America. Unlike Argentina, it has a single mine concession approval system and a well-documented system for dealing with approvals for water, roads etc. Peruvian people are very work-orientated and want to get things done rather than mañana (Ill get to it tomorrow).

ER: You have described to me how important it is, both morally and ethically, and for sound business reasons, to hire local laborers and managers. Can you talk about that?

PT: Poverty is common in rural areas. In the Cajamarca region (population 200,000), while the town is flourishing, workers in surrounding towns are subsistence farmers. Therefore, if the men can secure work in the mines, it significantly supplements their family’s otherwise small income.

By maximizing local employment, we minimize local issues such as water, dust, noise, etc., because everybody buys into the project. We have seen investors from Asian countries who didn’t understand the cultural significance get banned from mines, kicked out of the country.

ER: What are the biggest risks to achieving the meaningful cash flow from manganese trading that A.I.S. is expecting?

PT: Having spent 17 years working in Latin America, and having first worked in Peru in 2012, I have a good understanding of the risks.

We have analyzed our main risks as follows:

Product pricing: we have a production contract for fines and soon will have extended the product range to include lump. This will improve the price we receive and allow us to target new customers. The Mn ore 44% lump bulk product was as high as US$10 per 1% of grade in April 2018 and as low as US$7 this month. Oversupply is something we need to keep an eye on. However, we have the ability to change production volumes on a week to week basis, so we can react quickly with no penalties. Product Supply: we have one contract miner and several other negotiations and due diligence programs running to ensure that we meet our production target of 10,000 tonnes a month within six to nine months. Then, in 2H 2020/2021, a significant increase above 10,000 tonnes. Product Sales: Theres significant interest from new suppliers in the market. We may have to discount our product until we prove our ability to deliver, but the discount will be modest. We are having discussions with Chinese, Korean and other buyers.

ER: Why should investors consider buying shares of A.I.S. Resources?

PT: The company has adopted a low capital investment approach to mining and is focused on growing its retained earnings. As you are aware, we expended a lot of capital in Guayatayoc to build an asset, yet fell afoul of the administrative approval system in Jujuy province, leading to a delay in getting our drilling approved.

The board has supported my approach to being innovative in terms of trading and having a focus on cash flow. As we grow our cash flow from Mn trading we can redeploy it in Peru or, if sentiment in the lithium market improves, we can get busy again in Argentina. Mn trading gives us a lot of flexibility and will hopefully enable us to make that final $2.25 million payment.

If readers believe my maththat A.I.S. Resources can potentially generate about $100/tonne of Mn tradedthen it all comes down to volume, logistics and timing. If we can ramp up to 5,000 tonnes/month next quarter, on our way to 10,000 tonnes, then our current valuation is very attractive. (July corporate presentation. Latest press releases).

ER: Thank you Philip, very interesting update. Good luck with your new Mn venture. I will follow up with you and your team next month.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about A.I.S. Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of A.I.S. Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned no shares of A.I.S. Resources and the Company was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes hes diligent in screening out companies that, for any reasons, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts, financial calculations, etc., or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Asian stocks are taking their cues from the selloff on Wall Street, as the Federal Reserve confused investors with its policy outlook despite fulfilling market expectations by lowering US interest rates by 25 basis points. Fed chair Jerome Powell’s statement to the markets was interpreted as less-dovish-than-expected, prompting equity markets to unwind recent gains, with US benchmark indices shedding over one percent. As Asian markets came online, the Dollar index (DXY) saw a steep climb of 0.8 percent to breach the 98.8 mark and reach its highest level since May 2017.

The Fed Chair said he does not envision a “long series of rate cuts”, while indicating the recent rate cut may not be a one-and-done scenario. Market participants who had been hoping that the Fed would use this end-July meeting to embark on an aggressive easing cycle were left disappointed. Instead of receiving clear guidance from the world’s most influential central bank, the Fed has fudged its policy outlook, leaving investors to guess what’s next on the central bank’s policy agenda.

Where’s the justification for this “mid-cycle adjustment”?

Powell struggled to present the case for the first US rate cut in a decade, coming at a time when the outlook for the US economy remains “favourable”. Amid the feeble economic justifications for the recent rate cut, market attention has already turned to the next FOMC decision due September, with the incoming economic data between now and then set to be closely scrutinised in testing the Fed’s data-dependant stance. Should US economic growth momentum prove resilient over the coming months, any further rate cuts this year could undermine the Fed’s credibility.

At the time of writing, the Fed Funds Futures point to a 60 percent chance of another 25-basis point rate cut in September.

Could September be a hot bed for rate cuts?

Central bank action is now heavily concentrated in the mid-September period, as the Federal Reserve, European Central Bank, and the Bank of Japan are all due to make policy decisions. With the Fed leading the way by already lowering its benchmark interest rates, the ECB could push rates further into negative territory from minus 0.4 percent at present, while the BOJ has said it’s open to lowering interest rates from its current setting of minus 0.1 percent. Shifting market expectations over potential policy adjustments by major central banks are set to feed into the respective currencies performances in the interim.

Less-dovish Fed bolsters Dollar’s resilience, weigh on Asian currencies, Gold, and Oil

As markets continue to digest the Fed’s latest signals, as confusing as they were, a less-dovish Fed moving forward suggests that the stronger-Dollar is set to stick around for a while. The Greenback’s resilience in turn should continue exerting downward pressure on most Asian currencies.

The Dollar’s climb is also expected to make future gains for Gold and Oil harder to come by. Still, broader concerns over deteriorating global economic conditions should ensure that Gold remains supported, with US-China trade tensions still largely intact. Oil bulls can still find solace from the OPEC+ supply cuts that will be in place through the first quarter of 2020, even as demand-side uncertainties continue to hover over market sentiment.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

There are winners and losers from the Fed’s rate cut, the first in more than a decade – and U.S. and global investors now need to revise their portfolios, warns one of the world’s largest independent financial advisory organizations.

The warning from deVere Group’s International Investment Strategist, Tom Elliott comes as America’s central bank cut interest rates by 25 basis points Wednesday.

Mr Elliott comments: “The Fed’s first rate in more than a decade had been widely expected, yet divides the markets’ opinion.

“U.S stocks have taken heart from a recent upturn in domestic economic data and from the prospect of the Fed and other central banks easing monetary policy over the coming months.

“This, it is argued, will help the current cycle of U.S. and global economic growth.

“However, the U.S Treasury market, is indicating that a recession is around the corner. The inverted Treasury yield curve is cited as ‘exhibit number one’ for this thesis.”

“Today’s decision by the Fed to cut rates suggests that while the policymakers believe the economy is looking in good shape, there are also some growth headwinds on the horizon and inflation is low, so a rate cut will act as a buffer.

He continues: “Where does this leave for U.S. and international investors?

“Investors can incorporate both opinions into a portfolio by owning growth-sensitive stocks and misery-loving government bonds. This multi-asset approach is standard amongst long-term investors.

“Specifically, the rate cut will put further downward pressure on the U.S. dollar, with the Yen, Swiss franc and Euro likely to rise against the greenback.

“Emerging stock markets should gain the most from lower Fed rates and a weaker dollar, since the massive U.S. dollar debt many emerging market companies took on in the early years of this decade becomes cheaper to service and repay in local currency terms.

“U.S. exporters should also benefit, plus the battered British Pound may get some near-term relief from a Fed rate cut, particularly as the Bank of England seems unlikely to be cutting its own benchmark rates any time soon.”

Mr Elliott concludes: “U.S. and global investors now need to revise their portfolios to ensure that they are best-positioned to take advantage of opportunities and mitigate the risks as we enter what is likely to be a new era of rate cutting for the Federal Reserve.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

History was made today after the Federal Reserve cut interest rates for the first time since the 2008 financial crisis.

Unfavourable global conditions, persistent US-China trade tensions and muted inflation pressures have forced the Fed to cut interest rates by 25 basis points, taking the federal fund’s target range to 2-2.25%. The central bank also decided to conclude its balance sheet reduction in August – two months earlier than previously announced.

Although the monetary easing was justified by “uncertainties” stemming from weakness in the global economy, the committee expressed optimism over the US economy by calling growth “moderate” and the labour market “strong”. Overall, the Fed statement was not as dovish as markets priced for and this sentiment is being reflected in the Dollar Index which is blasting above 98.50 as of writing.

While the Fed also left the door open to future cuts, saying it will “act as appropriate to sustain the expansion”, this will be contingent on incoming data and US-China trade developments.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The Bank of England is the last of the major central banks to have their monetary policy meeting.

Despite being the most important event on the British economic calendar this week, we aren’t expecting a major change in terms of monetary policy.

Now that the Tory leadership spill is over and the Boris Johnson is settling in at 10 Downing Street, Britain is turning to a relatively quieter spell.

Brexit still looms on the horizon. However, Parliament is off for a month of vacation in August. Therefore, major votes or moves on that front are unlikely.

The Outlook

BOE Governor Carney has, in the past, repeated that the interest rate path forward depends chiefly on the result of Brexit. Without much moving on that front, we’re in a bit of a wait-and-see pattern with interest rates in Britain.

The economic indicators from the UK are different from both the continent and from many of the other major economies. UK inflation is comfortable, and while economic growth is less than ideal, it’s not something that is causing overt concern for the central bank.

Some analysts have argued that were it not for the potential currency effects of a no-deal Brexit, the BOE would have hiked rates already.

The Odd One Out

The consensus is that the BOE will simply hold its current policy with, at most, a modest tweak in forward guidance. While other banks are looking to ease policy, the BOE’s chief economist Haldane recently said he saw policy as already relatively accommodative. He added that there was no reason to follow the other banks.

Not only that, but there is a pretty solid consensus that the BOE will reiterate its view that a gradual and limited rise in rate over an extended period could be necessary. If anything were to change, it’s likely to the wording of this statement. And that’s what could drive markets following the meeting!

Being Ready

The increased chances of a hard Brexit in October have also given the bank more reason to keep their powder dry ahead of what might be a turbulent period. The uncertainty leading up to such an event, and immediately after it, would make markets quite unhappy. And the central bank would want to have as many tools available to deal with it.

The market, however, has been pricing in rate cuts. Yet, in the speech scheduled after the policy meeting, we could expect Carney to push back on that notion. However, this is a standard position for the bank, so we won’t expect it to move the markets all that much.

The Events

On Monday Sterling hit a multi-year low. And there seems to be an impetus downward despite the insistence of regulators. A weaker currency might benefit exporters, but also contribute to inflation. This further supports the argument for rate hikes in the future.

But then there is always the black swan! With everyone focusing on Brexit, an escalation in tensions in the Middle East might catch people off guard. PM Johnson ordered the Royal Navy to escort UK-flagged vessels through the Strait of Hormuz after Iran seized a British tanker, in what was seen as a tit-for-tat move.

The Critical Investor looks beyond the headlines to analyze the factors behind the company’s sale of its JV share to its partner.

Golden Arrow Resources Corp. (GRG:TSX.V; GARWF:OTCQB; G6A:FSE) surprised the markets with its sale of its 25% interest in Puna Operations to majority JV partner SSR Mining Inc. (SSRM:NASDAQ), right at a time where precious metals seemed to have left a bear market behind them. The Puna operation just ramped up to full production a quarter ago, and it seemed only a matter of time for high opex to come down, as a new mine always has to fine tune things. When costs would have been normalized, Puna could finally start to bring in cash for Golden Arrow, to finance its exploration efforts. It never got that far, unfortunately.

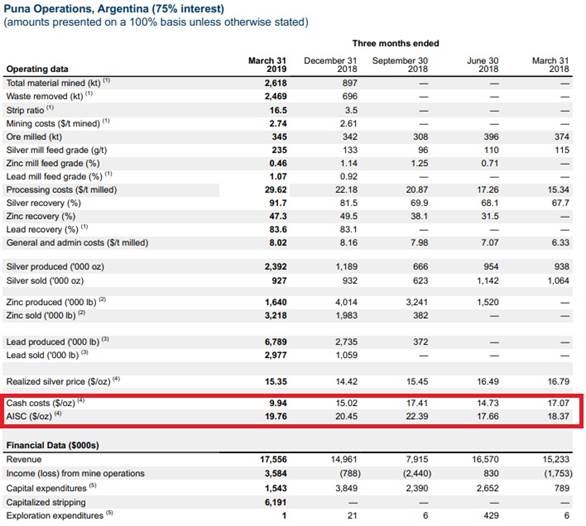

Instead of the pre-feasibility study (PFS) opex of US$9.75/oz Ag, cash costs were hovering around the price of silver itself for a long time (US$1417/oz Ag), and last quarter (first quarter of commercial production) the All-In Sustaining Costs (AISC) even went beyond that (US$19.76/oz Ag) despite cash cost coming down to US$9.94/oz Ag. These high costs led to an operation making losses, and SSR Mining didn’t hesitate to make cash calls to Golden Arrow, to pay up for its share of losses. This was something I didn’t anticipate, more on this later. First of all, let’s have a look at the deal. These are the highlights per the news release of July 22:

“C$3.0 million in cash consideration

C$25.9 million in common shares of SSR Mining

Approximately C$14.5 million in cash, which amount shall be used to repay in full at closing the outstanding principal and accrued interest owing by Golden Arrow under the credit agreement entered into in July 2018 with SSR Mining

C$1.0 million through the return for cancellation, for no consideration, of 4,285,714 Golden Arrow common shares currently owned by SSR Mining, which represents approximately 3.4% of Golden Arrow’s issued and outstanding common shares on the date hereof

Payment by SSR Mining of Golden Arrow’s portion of all cash contributions required to be made to Puna Operations under the Shareholders Agreement from July 22, 2019 until the closing date.”

In the end it means that Golden Arrow receives C$3 million in cash and C$25.9 million in common shares of SSR Mining, in total C$28.9 million. Golden Arrow management seemed quite pleased by it:

“The sale of our equity position in Puna Operations is a landmark achievement for the Company. The Transaction allows Golden Arrow to maintain diversified low-risk exposure to the continued success of SSR Mining at Puna Operations in Argentina and across their gold-focused producing portfolio in North America,” stated Joseph Grosso, executive chairman, president and CEO of Golden Arrow. “The Transaction provides Golden Arrow with a strengthened financial position to focus on delivering shareholder returns through the exploration and development of our exciting exploration portfolio in South America.”

Of course, this transaction removes a heavy burden of repayment terms for Golden Arrow, gets a decent package of SSR Mining shares with a lot of exposure to gold; it won’t have to go to the markets anytime soon now, and will be able to focus on its exploration assets now. All good. But there are more sides to this story, and not at least the factors that sent the share price crashing pretty hard after the news came out on July 22, more on this later:

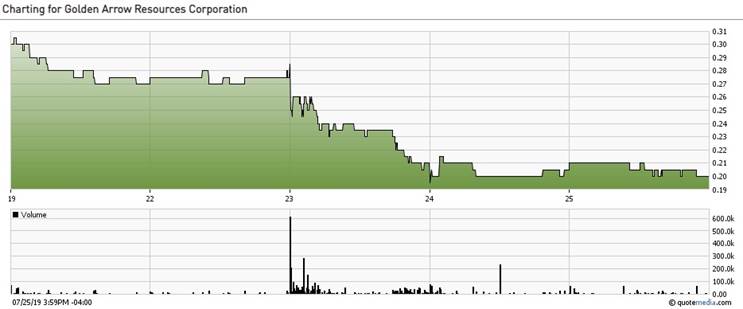

Besides this, just as remarkable was the sudden run-up from July 16 (C$0.205) to July 18 (C$0.30) on large volume, which doesn’t really indicate a tight ship as they say. However, whoever bought these shares, they did so on unrealistic expectations as the news of the transaction was apparently used to host a massive liquidity event.

There were some more transaction details:

“SSR Mining has agreed to loan (the “Contribution Loan”) to Golden Arrow the amount required to fund Golden Arrow’s portion of any cash calls under the shareholders agreement for Puna Operations made as of May 31, 2017 between SSR Mining and Golden Arrow, as amended by an amendment to the shareholders agreement made effective as of April 1, 2019 (as amended, the “Shareholders Agreement”) for the period from July 22, 2019 to the earlier of (i) the closing date of the Transaction and (ii) the termination of Agreement. Upon closing of the Transaction SSR Mining will provide Golden Arrow with an amount of cash sufficient for Golden Arrow to repay the Contribution Loans in full.

“However, if the Agreement is terminated prior to closing, such Contribution Loans shall be due and payable by Golden Arrow within twenty five (25) calendar days of such termination. The Contribution Loans are secured by a pledge of Golden Arrow’s shareholding interest in Puna Operations. The Agreement may be terminated for, among other things, (i) a material breach by Golden Arrow of its representations and covenants under the Agreement; or (ii) if the Transaction is not completed by October 15, 2019, or (iii) if Golden Arrow accepts a superior proposal.”

It sure is in the best interest of Golden Arrow to close this agreement, as in any other event it needs to repay the loans within 25 days, and these loans are secured by the 25% holding position of Golden Arrow in the Puna operation. As the company tried very hard to arrange a refinancing of the $10 million credit facility but failed, this effectively and most likely will mean that Golden Arrow just has to hand over their interest to SSR, unless a suitor pays off SSR.

“The Transaction is subject to the approval of two third of the votes cast in person or by proxy at a special meeting of the Golden Arrow shareholders and Golden Arrow shareholders shall be entitled to statutory dissent rights in respect of such vote. The Transaction also requires approval of Golden Arrow shareholders under the policies of the TSXV, as the Transaction represents the sale of more than 50% of Golden Arrow’s assets. Each director and officer of Golden Arrow and their associates and affiliates have each entered into voting agreements with SSR Mining pursuant to which they have agreed, among other things, to vote their respective shares in Golden Arrow in favour of the Transaction at the Golden Arrow shareholder meeting.

“Approximately 10.6% of Golden Arrow’s common shares are subject to these voting agreements. In addition, SSR Mining has indicated that it will vote the Golden Arrow common shares it holds in favour of the Transaction, representing an additional 3.4% of the issued and outstanding Golden Arrow common shares. It is expected that Golden Arrow will prepare and mail a meeting circular to its shareholders within 30 days, and that the special meeting of shareholders will be held by mid-September. The Transaction is subject to a number of customary conditions including the approval of Golden Arrow shareholders and the approval of the TSX Venture Exchange.”

So mid-September will be the moment of truth. Keep in mind that a lot of current shareholders weren’t too happy with proceedings and sold, so it wouldn’t surprise me if there are still a significant number of unhappy shareholders. And of course, their hired financial advisor PI Financial thinks this transaction is “fair,” otherwise they would miss their fees:

“The board of directors of Golden Arrow has determined that the Transaction is fair to the shareholders of Golden Arrow and in the best interests of Golden Arrow. The board of directors of Golden Arrow have received a fairness opinion from its financial advisor, PI Financial Corp., as to the fairness of the Transaction from a financial point of view to the shareholders of Golden Arrow, other than SSR Mining, which opinion was based on and subject to the assumptions made, matters considered and limitations and qualifications on the review undertaken.

“The Agreement provides for among other things, a non-solicitation covenant on the part of Golden Arrow (subject to customary fiduciary out provisions). The Agreement also provides SSR Mining with a right to match any competing offer which constitutes a superior proposal. A termination payment of US$1.36 million will be payable to SSR Mining in certain circumstances.”

This reminds me, I didn’t see a break fee for SSR Mining mentioned anywhere, which would be about 1015% of the transaction fee of $44.4 million. But buying the remaining 25% makes a lot of sense for SSR Mining (I always wondered why it didn’t do it in the beginning) so I guess that would be the reason. As SSR Mining is more and more gearing toward being a gold producer (it calls it precious metals producer), I don’t rule out the possibility that it would like to sell Chinchillas/Puna now it has consolidated it to 100% ownership.

A thing I found pretty remarkable here were the cash calls of SSR Mining to its minority nanocap junior JV partner, knowing this company didn’t have an exactly full treasury. As a result, Golden Arrow Resources surprised the market with another raise in June, as consensus was that the earlier C$4.74 million financing would be enough to carry the company through most of 2019. C$1.2 million was raised at 20 cents with a full 3 year warrant (exercise price 30 cents), oversubscribed (from C$750,000), and closed at June 20, 2019.

As I was curious why management decided to do so, I contacted them at the time to find out. It appeared that the JV with SSR Mining was organized in such a way that Golden Arrow Resources had to participate in the losses as well, and since the Q1 AISC came in again at US$19.76/oz Ag when silver was selling around US$15/oz Ag, it was beginning to dawn on me where the cash call from SSR came from (table from the Q1 MD&A of SSR Mining):

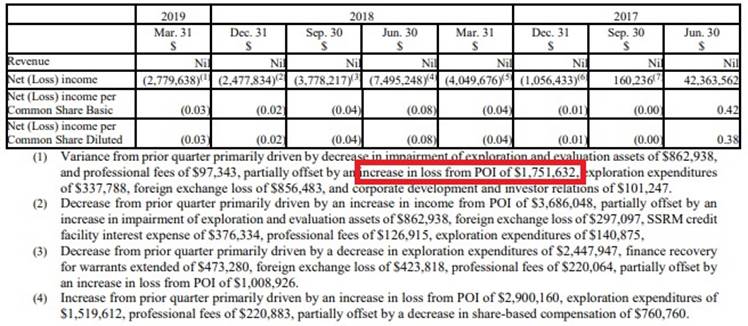

The Q1 financials (p. 12) describe this in a summarized way (POI means Puna Operations Inc.), and key here was of course “capital expenditures and working capital purposes”:

“On March 31, 2017, SSRM exercised its option on the Chinchillas project and on May 31, 2017, SSRM and the Company formed POI for the development of the property. The jointly owned company, holding the Pirquitas and Chinchillas properties is owned 75% by SSRM and 25% by the Company with SSRM as the operator. The Company is liable for contribution of 25% of the required funding for capital expenditures and working capital purposes of POI when requested by POI.”

My earlier understanding was that capital expenditures in this agreement only meant initial capex, to build the mine, and not sustaining capital expenditures or losses on the operation.

According to the MD&A (Management Discussions and Analysis), these were the highlights of Q1, taken from the financials of SSR Mining:

“Highlights of Puna’s first quarter 2019 production and financial results as reported by SSRM included:

Produced 2.4 million ounces of silver, double the silver production in the fourth quarter of 2018, with lead and zinc production of 6.8 million pounds and 1.6 million pounds, respectively.

Processed ore in the first quarter of 2019 contained an average silver grade of 235 g/t.

Silver recoveries quoted at 91.7%

Ramp up at the Chinchillas mine was substantially completed during the quarter.

Doubled silver production with lower costs at Puna Operations.”

These are, of course, the highlights, so I looked at the reporting of SSR Mining itself to get the whole picture.

And there it is, the unintended loss at commercial production.

Back to the MD&A of Golden Arrow:

“The Company’s continued operations, as intended, are dependent upon its ability to raise additional funding to meet its obligations and commitments and to attain profitable operations. Management’s plan in this regard is to raise equity financing as required to further fund its share of planned capital expenditures for its investment in POI and working capital. Management’s plan in this regard is to raise additional funding as required.”

These cash calls came at the end of each quarter, to the tune of $1-2 million. Of course this is an unsustainable situation for a small junior like Golden Arrow.

What I found even more strange were the high opex numbers produced by SSR Mining as the operator, and one with a very good reputation to go with that as well. These numbers deviated from the PFS numbers by 50100%, way higher than the usual margin of error in a PFS (although 35% as used is pretty high for a PFS, usually it is 25%, and 35% is more for a PEA). Therefore I contacted management again, for some answers on this topic.

According to them, SSR thought this situation of high costs would last well into 2020, meaning Golden Arrow had to raise C$12 million each quarter. This was the primary reason for Golden Arrow to sell its 25% interest, as the needed cap raises were almost undoable, also with the repayment of the US$10 million credit facility coming up in a year. The company tried very hard to refinance this facility, and looked at all other options, but with no luck being a minority JV partner, very dependent on SSR Mining as the operator who came up with a year of high opex from now.

These opex overruns revolved primarily around the stripping costs, where SSR Mining had to strip much more than planned. There were also heavy rains and severe lightning, causing problems for hauling ore to Pirquitas. Especially the stripping issue got my attention, and more specifically the extent of the resulting higher opex because of it. For answers on this issue, I got redirected to a director of Golden Arrow Resources, Alf Hills, who also sits on the BoD of Puna Operations Inc. for Golden Arrow. We had an interesting conversation.

Alf pointed out that the main difference in costs appeared to be in Processing, as reported in the SSR Mining Q1 news release, since these almost doubled compared to the PFS figures for Q1, stripping, however, wasn’t out of the ordinary as it was planned to be (very) high the first commercial quarters in the PFS.

It all seems to revolve around the AISC here. Point is the PFS isn’t providing AISC figures per production year, just a LOM average, so it is hard for me to reverse engineer this number. When looking at PFS table 16.3, the stripping for Y2Q1 (Y2 is 2019) and Y2Q2 is indeed very high (16.51 and 14.42) but also as planned, but coming down fast in Y2Q3 and further (5.90, 4.32, 3.75, 5.7).

When looking at silver production (as mentioned AISC is net of byproducts no need to use AgEq figures here) for the first year (2019) and more specifically the quarters, I get for Y2Q1 a silver production of 478 Koz, Y2Q2 of 436 Koz, Y2Q3 of 1.22 Moz, Y2Q4 of 1.8 Moz.

When I look at table 21.1, sustaining capital seems to be geared mostly toward mining equipment, mining support equipment, freight, contingency, and just $5.25 million (LOM) is reserved for Other sustaining capital cost. Note 3 states that sustaining capital is exclusive of capitalized stripping, so I don’t see how stripping costs could attribute to the AISC as much as management thought it does. Table 22.4 shows Sustaining capex of $15 million over Y2 (or 1 in this particular table), this means $15 million / 3.93 Moz Ag = $3.8/oz Ag sustaining cost on average for Y2, but I have no clue what the sustaining costs per quarter in Y2 would be, or even better the AISC per quarter.

More importantly, I don’t see how the stripping deviates from the PFS, and Alf agrees on this.

It seems all planned and clear to me from the start, so it seems GRG and SSR must have been aware when commercial production started at these low silver prices, they were already at increased risk of these cash calls, as without the processing cost increase, basically nothing could go wrong just to break even.

Of course, the silver price is significantly lower than what was assumed in the PFS. However, when the AISC goes over the assumed PFS silver price anyway, it doesn’t matter anymore, you lose money. According to the PFS, stripping costs should come down a lot. However, it is hard to draw conclusions on AISC as there is no info on this, just bits and reverse engineered pieces, and even more important, why does SSR say the AISC would remain high for another year? Will the processing problems (I would like to call double processing costs a problem) not be solved in a year?

Alf couldn’t elaborate on these high processing costs: “As I mentioned I don’t have visibility on the high processing cost reported by SSR Mining in its Q1 News Release, and suspect it has some legacy components to it. To my knowledge the mill did not have any material operating issues in Q1.”

As a result, on-going cash calls from the operation, the maturity date of the SSRM loan (this was July 2020 but with no payback schedule), low silver price compared to the PFS base case, and on-going challenging funding environment for junior companies were all substantial considerations for the company to sell its 25% interest, according to him.

To me it all seemed like a risky operation, to start production at this lower silver price. Everything had to go right as the margins weren’t substantial to begin with at US$19.50/oz Ag base case. Alf had the following comment: “I think it is fair to say the project was committed on the basis of the results of the Technical reportthe low silver price environment means the margins are squeezed even more. 2019 was seen and reported by SSRM as a transition year from project to routine operation and that is generally in line with what was planned in the PFS.”

Another detail Alf found is the fact that SSR produced more ounces in Q1 than it sold. He finds the reason for the high AISC/oz largely due to the use of ounces sold rather than produced, and this is a decision SSR Mining as the operator and majority owner has made.Over time, SSR will sell these stockpiled ounces for sure, and figures will even out. But I can’t imagine this being a reason for GRG to sell, as it is just a temporary thing.

According to management, they had a much more simple motivation to all this: “The main reason to sell now is because we have a buyer now.”

But this doesn’t tell the whole story of course.

So whatever the reason and the trajectory was, it appeared that Golden Arrow was with its back against the wall, and simply had to accept the offer of SSR Mining, at a time precious metals sentiment was turning unfortunately. Who would have thought this a few years ago, certainly not me. In my mind I still find it remarkable to see a non cash flowing junior being partly responsible for potential losses of a ramping up operation, operated by a majority JV partner. An important thing to consider is the fact there are no bonuses to be paid to Golden Arrow management this time, contrary to the sale of the first 75%.

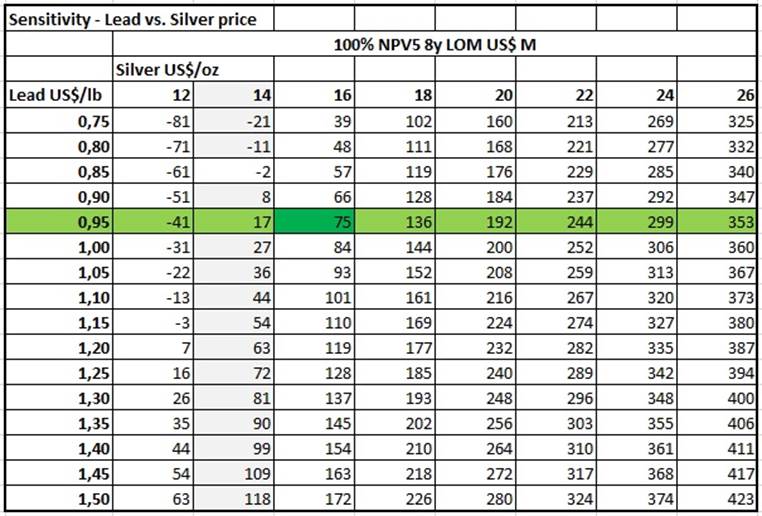

If C$44.4 million is a good price for Chinchillas/25% of Puna Operations is a good question. With silver at US$16.42, and lead at US$0.94, the sensitivity I calculated in my first article comes up with an estimated 100% NPV5 of about US$89 million:

When divided by 4, the 25% ownership of Golden Arrow attributes to US$22.25 millin, which is C$29 million. The 25% ownership of the Pirquitas plant break up value could be estimated at C$11.5 million midpoint based on the estimate I did in my first article. Usually this value is included in the NPV5, but since the NPV5 is so low because of metal prices being very low, I view it as fair to assign separate value to it. This brings the total value of the 25% interest in Puna Operations at a globally estimated C$40.5 million, which isn’t too far off from the C$44.4 million transaction fee. I can live with it, but remember SSR Mining buys it right at the time silver prices are cautiously following gold in its footsteps. There is no question in my mind SSR Mining hardly pays any premium for potential upside here, whether it is a longer mine life or a rising silver price or both.

Golden Arrow management is very pleased with the transaction, as it was their only way out of upcoming financial obligations, and sees the significant package of SSR shares as solid exposure to gold, which is doing well nowadays. Silver is still lagging, but has got a pulse. I have a slightly different view, to me this means the end of Golden Arrow as one of the best leveraged plays on silver in the entire industry. The beauty was it was a one producing asset pure play on silver, supported and operated by a very good operator, and hovering a long time around break even or small losses. Ideal for a leveraged play as the effect of a rising silver price would be optimal. And even better, with incoming cash flow it could self-fund its exploration ventures without having to go back to the markets, and get the upside here as a wild card. Unfortunately, all this was not to be. It appears many investors were invested in Golden Arrow for the same reason, as the share price lost 24% in one day on big volume (about 20 times normal volume) after announcing the transaction.

If the transaction gets approved, which could mean a challenge if the silver price rises substantially before the upcoming special AGM in September, Golden Arrow is no longer a producer, but a pure explorer again. It will have substantial current assets, to the tune of C$29 million (current market cap is C$25 million) with a lot of exposure to a very solid producer with lots of gold exposure, a few exploration assets, and is actively looking for new assets at the moment. Management indicated to me there will be significant news coming in a few weeks’ time, so my guess is they found something interesting in this regard, which will undoubtedly help them by creating a new direction.

Conclusion

Considering the financial hardship Golden Arrow was in, the selling of its 25% was the only realistic option after management did everything they could to avoid this, but I didn’t know the situation was this dire, and would be relatively long lasting, intensifying financial risks. Lessons learned in analyzing JV structures, and minority partners are not to be envied, this much is clear again from this development. It will be interesting to see which new asset(s) Golden Arrow will find in order to cement its soon to be newfound role as a pure-play explorer. Chances are the company will focus on quality gold assets this time around, as gold seems to be a better market proposition. I am curious to find out, with the kind of compensation it will get from SSR, the company should potentially be able to buy very good assets, possibly with significant historical, potentially economically viable deposits. But I am totally speculating now, of course. Let’s wait and see, to be continued.

<p

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The Critical Investor Disclaimer:

The author is not a registered investment advisor, currently has a long position in this stock, and Golden Arrow Resources is a sponsoring company. All facts are to be checked by the reader. For more information go to www.goldenarrowresources.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure: 1) The Critical Investor’s disclosures are listed above. 2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Golden Arrow Resources, a company mentioned in this article.

After waiting for seven years since the silver price traded above $30, precious metals investors are wondering if 2019 will be the year that shiny metal finally enters into a new bull market. However, for silver to enter into a new bull market, certain signs and indicators need to take place. I discuss this in detail in my latest video.

Interestingly we have seen several precious metals analysts suggest that something quite interesting is taking place in the silver market. For example, Alasdair Macleod wrote an article; A Whale Is Accumulating Silver Futures, implying that the Chinese government may indeed be acquiring a significant long position in the silver market. Macleod believes China may be going long silver, via the futures market, to protect its supply by hedging as the price heads higher in the future.

So, how can we tell if silver is entering into a new bull market? Well, the biggest indicator tends to be the price. While physical supply and demand factors impact price, we have seen years in which demand fell during rising prices, but also surged during extreme selloffs. Thus, it’s important to look for key price levels that will signal that silver has begun a new bull market.

The silver price has been impacted by fundamental and technical analysis. As I have mentioned in recent articles, I dismissed technical analysis for years as I thought it was nothing more than reading tea leaves or goat entrails, as a commenter stated. However, after I spent the past year watching and studying the day trading markets, I realized that stocks were bouncing off moving averages, technical levels, and formations… DAY IN AND DAY OUT.

When I went back and looked at the long-term gold and silver charts, I saw that the large price BREAKOUTS occurred at certain key levels. Why was this the case? Well, it seems that when the gold or silver price broke above a key level, it came on the RADAR of traders, hedge funds, investors, and institutions. Thus, breaking above or below these key levels brings on a great deal more interest and trading volume.

Basically, when the gold or silver price finally pushes above a long-term resistance level, EVERYONE WANTS IN. And, it’s not just in gold and silver. The market pays attention to these key levels IN ALL STOCKS & COMMODITIES.

So it’s essential to understand that while the fundamentals are the underlying drivers of price, the key technical levels provide the BIG PUNCH or huge increase in BUYING or SELLING depending on the technical setup. I ignored this information for years, but will no longer.

Does that mean that I am no longer interested in fundamentals? Hell no. Actually, I am interested in the fundamentals more than ever. However, technical analysis will provide us some with clues to how silver will BREAKOUT to new highs in the future. Furthermore, when the U.S. and world experience peak oil, the impact on most assets will be quite negative. BUT… this will be shown in the charts as Stocks, Bonds and Real Estate lose value while gold and silver move up in the opposite direction.

The key technical levels are important to keep an eye on because the PAPER BUYER or SELLER drive the majority of the silver market price. This shouldn’t be a surprise because only 1% or less, of investors, purchase physical gold and silver.

One of the charts I discuss in the video is the long-term silver chart with two crucial moving averages and the important lower trend line:

In the 20-year monthly chart of silver, the price has been bouncing off the lower rising trend line (blue dashed line) since 2004. Not only is this an important technical level for silver, but it also shows a BOTTOM for the price as $15 is now the average cost to produce an ounce of silver by the primary mining industry. If we go back to 2004, the primary silver mining industry was producing silver at about $5 an ounce. Thus, the cost to produce silver has tripled in 15 years… AND THE TECHNICAL LEVELS SHOW IT.

Lastly, I explain why the silver price must push above these two moving averages to be in a new bullish trend. However, for silver to be in a NEW BULL MARKET, I believe there is a certain key price level that it needs to rise above.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Today is the day for the US Fed to announce their rate decision and we believe the 25 basis point rate cut is the only option they have at the moment that will attempt to settle foreign market fears and allow for a suitable “unwinding” of the credit/debt “setup” we highlighted in Part I of this research post.

We believe out August 19 expectation of a global market PEAK and the beginning of a price reversion move is related to multiple aspects of the timing of this Fed move and the current global economic outlook. The unwinding of this debt/credit bubble will likely take many more years to unravel. Yet, right now the US Fed is trapped in a scenario they never expected to find themselves in. Either continue to run policy that supports the US economy (where rates would likely stay between 1.75 to 2.75) over the next 5+ years or yield to the global market and attempt to address a proper exit capability for this debt/credit “setup”.

We believe global investors are expecting a massive collapse in the US stock market as a reaction to this move by the Fed and because of the expectation that another bubble has set up in the US. But we believe the actual bubble is set up in the foreign markets and not so much in the US. Yes, the US markets have extended to near all-time highs and the US consumer is running somewhat lean. It would be natural for the US economy to revert to lower price levels and for the US economy to rotate as “price exploration” attempts to find true market support. Yet, our fear is that the foreign markets are much more fragile than anyone understands at the moment and that a reversion in the US markets will prompt a potential collapse in certain foreign markets.

Weekly SPY chart

This Weekly SPY chart highlights what we expect to transpire over the next 6 to 8+ months. We believe the August 19 peak date that we predicted months ago will likely start a process that will be tied to the US election cycle event (2020) and the US Fed in combination with global market events. We believe a reversion price process is about to unfold that could be prompted into action over the next 2+ weeks by the US Fed, trade issues and global central banks.

If the US Fed drops the FFR by 25pb, the fragility of the foreign market debt/credit issues is not really abated or resolved. It just allows for a bit of breathing room that may allow these foreign debtors enough room to wiggle out of some of their problems. The US Fed would have to decrease rates by at least 75 basis point before any real relief will materialize for these foreign debtors.

Asian Currency Custom Index

This Asian Currency Custom Index used by our research team highlights the weakness in the foreign markets. The recovery in 2018 is related to the Chinese/Asian currency market recovery that initiated in Feb/Mar 2018. The recent weakness in this custom index is related to strengthening major market currencies (USD, CAD, JPY, CHF) in relation to weakening Asian currencies. Notice how the price channels have set up to warn us that any further downside move will initiate a new “price exploration” phase that could see a -20% to -25% decrease in currency valuations – possibly much deeper.

We believe this is the real reason the US Fed is opting to decrease the FFR rate now and is not taking a more stern position related to US economic performance. We believe the US Fed is, again, donning the “Superman cape” and attempting to Save The World from their own debt/credit mess.

We are holding to our original predictions and expectations. We believe the US stock market indexes will enter a reversion price phase over the next few weeks that will prompt a downside price reversion toward recent lows (2018 levels or deeper). We believe this process will end in early 2020 and that the lows established by this move will represent incredible opportunities for skilled technical traders.

Weekly Dow Jones chart

This Weekly Dow Jones chart highlights our expectations. We believe a mild price rotation will start this move over the next 2~4 weeks before the August 19, 2019 date prompts a breakdown move. After that date, we believe an extended downside price leg will continue to reach a price bottom near the end of 2019 or in early 2020.

This Weekly Dow Jones chart highlights our expectations. We believe a mild price rotation will start this move over the next 2~4 weeks before the August 19, 2019 date prompts a breakdown move. After that date, we believe an extended downside price leg will continue to reach a price bottom near the end of 2019 or in early 2020.

Skilled traders understand how the global markets are setting up for incredible opportunities and how to identify where and when these opportunities are ripe for profits and this is where we can help you!

CRUCIAL WARNING SIGNS ABOUT GOLD, SILVER, MINERS, AND S&P 500

In early June I posted a detailed video explaining in showing the bottoming formation and gold and where to spot the breakout level, I also talked about crude oil reaching it upside target after a double bottom, and I called short term top in the SP 500 index. This was one of my premarket videos for members it gives you a good taste of what you can expect each and every morning before the Opening Bell. Watch Video Here.

I then posted a detailed report talking about where the next bull and bear markets are and how to identify them. This report focused mainly on the SP 500 index and the gold miners index. My charts compared the 2008 market top and bear market along with the 2019 market prices today. See Comparison Charts Here.

On June 26th I posted that silver was likely to pause for a week or two before it took another run up on June 26. This played out perfectly as well and silver is now head up to our first key price target of $17. See Silver Price Cycle and Analysis.

More recently on July 16th, I warned that the next financial crisis (bear market) was scary close, possibly just a couple weeks away. The charts I posted will make you really start to worry. See Scary Bear Market Setup Charts.

CONCLUDING THOUGHTS:

In short, you should be starting to get a feel of where each commodity and asset class is headed for the next 8+ months. The next step is knowing when and what to buy and sell as these turning points take place, and this is the hard part. If you want someone to guide you through the next 12-24 months complete with detailed market analysis and trade alerts (entry, targets and exit price levels) join my ETF Trading Newsletter.

Be prepared for these incredible price swings before they happen and learn how you can identify and trade these fantastic trading opportunities in 2019, 2020, and beyond with our Wealth Building & Global Financial Reset Newsletter. You won’t want to miss this big move, folks. As you can see from our research, everything has been setting up for this move for many months.

Join me with a 1 or 2-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next financial crisis.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities starting to present themselves will be life-changing if handled properly.

FREE GOLD OR SILVER WITH MEMBERSHIP!

Kill two birds with one stone and subscribe for two years to get yourFREE PRECIOUS METAL and get enough trades to profit through the next metalsbull market and financial crisis!