Asian stocks are climbing, carrying over the momentum from the late surge in US equities. The lull in the US-China trade conflict has prompted safe haven assets to unwind recent gains: Gold is now trading below the $1490 level, the Japanese Yen has weakened above 107.5 against the US Dollar, while yields on 10-year US Treasuries have surged past 1.70 percent.

Still, South Korea’s decision to file a WTO complaint against Japan today is reminding investors that global trade tensions remain an ongoing concern. Although market sentiment may occasionally peek out from behind the risk-off curtain, the overall mood still speaks to a broader apprehension towards riskier assets, barring a meaningful de-escalation in the US-China trade conflict.

EURUSD steady around 1.10 level ahead of ECB’s expected rate cut

The Euro has remained subdued around the 1.10 level against the US Dollar so far this week, in the lead up to the European Central Bank’s policy decision on Thursday. Markets are expecting the ECB to push interest rates further into negative territory by 10 basis points, with potentially more stimulus to be unleased onto the ailing Eurozone economy.

It remains to be seen whether the incoming policy stimulus by the ECB will be enough to offset the headwinds faced by the bloc, even as policymakers prepare for a leadership transition at the ECB on November 1. Should the ECB not live up to markets’ dovish expectations this week, that may allow the Euro to post some immediate gains, although the broader outlook for the bloc’s currency is expected to remain lackluster. The ECB’s policy decision and conveyed outlook may also prompt immediate moves in the Dollar, considering that the Euro accounts for more than half of the Dollar Index (DXY).

US inflation, retail sales data in focus as markets countdown to next Fed meeting

The 98.1 support level has proven effective for the Dollar Index (DXY), despite last Friday’s lower-than-expected US non-farm payrolls print. Dollar bulls have taken the softer US jobs market in stride, propping up DXY this week. Most Asian currencies are currently weaker against the Greenback, while G10 currencies are seeing mixed fortunes against the Dollar.

Looking at the Fed Funds Futures at the time of writing, markets are expecting the Fed to lower US interest rates next week and again in October, before pausing in December, only to incur one more rate cut in January. The upcoming US inflation and retail sales data releases for August are set to shape market expectations over the Federal Reserve’s rates path in the lead up to next week’s policy decision. Should the incoming economic indicators prompt the Fed to pivot towards a more dovish stance, that could send the Dollar Index below the psychological-98 level, on a path towards the 97.55 support level.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

By CentralBankNews.info Armenia’s central bank lowered its refinancing rate by 25 basis points to 5.50 percent, reiterating that it expects to maintain a stimulative monetary policy stance in the medium term to achieve its inflation target due to the deflationary impact from the external sector, where economic growth and inflation is slowing. The Central Bank of Armenia (CBA), which has now cut its rate twice this year following a cut in January for a total decline of 50 basis points, also said it expects inflation to remain below its target of 4.0 percent, plus/minus 1.5 percentage points, in coming months before stabilizing around the target in the medium term. Armenia’s inflation rate slumped to 0.6 percent in August from 1.7 percent in July, partly due to a seasonal decline in agricultural prices that is also reflecting international commodity markets. Economic activity in Armenia remained high in the third quarter, largely driven by growth in processing industries and private consumption while fiscal policy is acting as a brake on demand. Armenia’s dram rose steadily from March through August and has remained stable this month, trading at 476.6 to the U.S. dollar today, up 1.5 percent this year. Aided by a pickup in private investment and private remittances, Armenia’s economy grew 5.2 percent last year and 6.5 percent year-on-year in the second quarter of this year. In late May the International Monetary Fund forecast growth of a more sustainable 4.6 percent this year and stabilize around 4.5 percent in the medium term, with fiscal consolidation remaining on track to bring government debt below 50 percent of gross domestic product in the medium term.

Technical analyst Clive Maund discusses the factors he sees pulling gold down.

Although a major precious metals sector bull market has certainly started, various fundamental and technical factors came together last week to suggest that a significant correction to the recent strong run-up has now started.

The main fundamental development was the announcement that there will be a Trade War summit between China and the U.S. early next month, with hopes being expressed that this may lead to compromise or some kind of truce. Whilst the chances of improvement may be slim, the market has got what it wants for now which is hope, and this hope should continue at least until this meeting, which provides the excuse for the markets to go “risk on” until then, which is why the stock market broke higher last week, delaying but not eliminating our crash scenario.

A return to “risk on” is clearly not good for the precious metals, which, until last week, had been benefiting from a flight to safety as had the dollar, creating the unusual situation where the dollar and gold were rising at the same time. Now, in a risk on environment they are suddenly out of favor again.

In addition to this fundamental argument we have a range of technical indicators pointing to a correction in the precious metals sector that we will now look at. They include its overbought status, overly bullish sentiment readings and COTs showing extreme readings.

Starting with gold’s 6-month chart, we can see that it doesnt look too badyet, but if we look more closely we can see that it is on the point of breaking down from the rather steep uptrend in force from late May, with it having dropped back on quite high volume the past two trading days, and it is noteworthy that Thursday’s drop was the biggest 1-day drop for a long time, making it more likely that it signals a reversal. In addition, the MACD indicator shows that momentum is starting to flag.

So, how far could gold react back? It happens more often than not that after a price breaks clear out of a giant base pattern, as gold did from its giant complex Head-and-Shoulders bottom or Saucer base shown on our 10-year chart, that it then returns to test support at the upper boundary of the base pattern before turning higher again. That could happen again and it would throw a lot of investors in the sector who are now of the view that we are “off to the races.” So, if it does react back that far don’t be dismayedon the contrary it would throw up one last great buying opportunity.

We have had a rather unusual situation in the recent past where the dollar and the precious metals have been strengthening together. This is because, in a risk-off environment both have been considered safe havens. In a risk-on environment this logic works in the other direction so that the dollar and the precious metals may both react back together. On the 3-year chart for the dollar index we can see that it is at a good point to turn lower, despite its still bullishly aligned moving averages, as its persistent gentle uptrend has brought it up to the significant resistance level shown.

While precious metal stocks continued to push higher in recent weeks, the decline was losing momentum, as revealed by the downtrending MACD indicator on the 6-month GDX chart below, which led to its breaking down on high volume on Thursday and Friday, and it won’t have to drop much lower to break below its 50-day moving average, that has opened up a rather large gap with the 200-day, a development that is likely to happen soon.

So how about COTs and sentiment? We will now proceed to look at them. We had been wary of calling a top too soon based on the increasingly lopsided COTs, having called a top too soon during the run-up early in 2016, but now, given the other factors that we have considered, in particular the negative developments last week, the latest gold COT, which shows high Large Spec long positions and heavy Commercial short positions, certainly makes a reaction back by gold now or soon a lot more likely

Click on chart to pop-up a larger, clearer version.

The COT is backed up by the latest Hedger’s chart, that goes back to 2010, which shows that positions match the extreme reached in the summer of 2016, and as we know this was followed by a brutal correction for the rest of the year. While a correction certainly looks likely it shouldn’t be so deep, because there is a big difference this time round, which is that gold has broken out into a major new bull marketit was still in a basing phase in 2016.

Click on chart to popup a larger, clearer version.

Chart courtesy of sentimentrader.com

Lastly, the Gold Miners Bullish % Index is still at 87%, and while we were waiting to see if it would hit 100% as it did in 2016, it doesn’t have to, of course, before a reversal occurs, and 87% certainly shows that enough people are bullish to warrant a trip to the fleecing shed.

Investors in the precious metals sector should therefore take measures to protect themselves, which include stepping aside for a while, or if staying long, hedging with inverse ETFs such as DUST, or options (options are much more cost effective), GLD Puts being very suitable as they are highly liquid with narrow spreads, and then we watch for the expected correction to unfold, aware that when it has run its course, we will be presented with a MAJOR BUYING OPPORTUNITY.

Originally published on CliveMaund.com on September 9, 2019

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

US stock market edged up on Tuesday while tech stocks weighed after the attorneys general of 50 US states announced an investigation into Google’s ‘potential monopolistic behavior’. The S&P 500 added 0.03% to 2979.39. Dow Jones industrial rose 0.3% to 26909.43, extending winning streak to fifth session. The Nasdaq however retreated 0.04% to 8084.15. The dollar strengthening resumed as the Labor Department reported Americans quit their jobs hit an all-time high in July, suggesting that workers are confident in the strength of the job market. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.01% to 98.32 and is higher currently. Stock index futures point to higher openings today.

CAC 40 leads European indexes gains

European stocks resumed advancing on Tuesday as investors anticipate a stimulus package at European Central Bank policy meeting on Thursday. The EUR/USD halted its advance while GBP/USD continued gaining yesterday with both pairs lower currently. The Stoxx Europe 600 ended 0.1% higher. The German DAX 30 added 0.4% to 12268.71. France’s CAC 40 rose 0.8%. UK’s FTSE 100 gained 0.4% to 7267.95 as lawmakers rejected prime minister Johnson’s second bid to hold a snap general election.

Hang Seng leads Asian indexes gains

Asian stock indices are mostly rising today. Nikkei gained 1.0% to 21597.76 with yen slide against the dollar intact. Chinese stocks are mixed: the Shanghai Composite Index is down 0.4% while Hong Kong’s Hang Seng index jumped 1.6%. Australia’s All Ordinaries Index recovered 0.4% despite Australian dollar’s move higher against the greenback.

Brent futures prices are extending losses today. Prices fell yesterday after news US National Security Adviser John Bolton resigned, spurring hopes tensions with Iran may ease: November Brent lost 0.3% to $63.28 a barrel on Tuesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of ACADIA Pharmaceuticals opened up 75% higher today after the company announced that its Phase 3 Study of pimavanserin for the treatment of dementia-related psychosis met its primary endpoint.

San Diego, Calif.-based biopharmaceutical company ACADIA Pharmaceuticals Inc. (ACAD:NASDAQ) today announced that its Phase 3 HARMONY study evaluating pimavanserin for the treatment of dementia-related psychosis met its primary endpoint, demonstrating a highly statistically significant longer time to relapse of psychosis with pimavanserin compared to placebo in a planned interim efficacy analysis. The firm further reported that upon the recommendation of the study’s independent data monitoring committee, which met to review the data from the planned interim efficacy analysis, the study will now be stopped early based on pre-specified stopping criteria requiring a one-sided p-value less than 0.0033 on the study’s primary endpoint.

The company plans to meet with the U.S. Food and Drug Administration (FDA) regarding a supplemental New Drug Application (NDA) submission in 2020, and the results from the HARMONY study will be submitted for presentation at upcoming medical meetings. The FDA previously granted Breakthrough Therapy Designation for pimavanserin for the treatment of dementia-related psychosis. No drug is approved by the FDA for the treatment of dementia-related psychosis.

Jeffrey Cummings, M.D., Sc.D., Director Emeritus of Cleveland Clinic Lou Ruvo Center for Brain Health in Las Vegas, commented, “Psychosis adds dramatically to the marked burden that dementia patients already carry and is one of the most challenging-to-manage aspects of the disease for caregivers…With no approved treatment options available today for dementia-related psychosis, the pimavanserin study results represent a meaningful advance that will potentially bring us a much needed therapy for this debilitating disease.”

ACADIA’s President Serge Stankovic, M.D., M.S.P.H., stated, “We are very excited that today’s results bring us one step closer to the potential of offering patients with dementia-related psychosis a critically needed treatment option…We look forward to speaking with the FDA about a supplemental new drug application (NDA) to support pimavanserin for the treatment of dementia-related psychosis. I want to thank all of the patients, their families, and the investigators for their participation in this important study.”

The firm indicates that pimavanserin is a selective serotonin inverse agonist and antagonist preferentially targeting 5-HT2A receptors. These receptors are thought to play an important role in psychosis, schizophrenia, depression and other neuropsychiatric disorders.

The HARMONY Study is a Phase 3 study double-blind, placebo-controlled relapse prevention trial designed to evaluate the efficacy and safety of pimavanserin for the treatment of delusions and hallucinations associated with dementia-related psychosis across a broad population of patients with the most common subtypes of dementia including: Alzheimer’s disease, dementia with Lewy bodies, Parkinson’s disease dementia, vascular dementia, and frontotemporal dementia spectrum disorders. The study included a 12-week open-label stabilization period during which patients with dementia-related psychosis were treated with pimavanserin 34 mg once daily. Dose reduction to 20 mg once daily was allowed if clinically justified within the first four weeks.

The company advised in the release that around 8 million people in the United States are living with dementia and studies suggest that approximately 30% of dementia patients, or 2.4 million people, have psychosis, commonly consisting of delusions and hallucinations. Serious consequences have been associated with severe or persistent psychosis in patients with dementia such as repeated hospital admissions, increased likelihood of nursing home placement, progression of dementia, and increased risk of morbidity and mortality.

ACADIA Pharmaceuticals states that its vision is to become the leading pharmaceutical company dedicated to the advancement of innovative medicines that improve the lives of patients with central nervous system (CNS) disorders. The company received FDA approval for NUPLAZID (pimavanserin) in April 2016, the first and only medicine approved for the treatment of hallucinations and delusions associated with Parkinson’s disease psychosis. The firm also has ongoing clinical development efforts in additional areas with significant unmet need, including dementia-related psychosis, schizophrenia, major depressive disorder, and Rett syndrome.

ACADIA shares opened much higher today at $41.79 (+$17.99, +75.59%), compared to Friday’s $23.80 closing price. The stock has traded today between $36.62 and $43.98/share and at present is trading at $39.21 (+$15.41, +64.75%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professional for medical advice.

Tim Johnson, CEO of Granite Creek Copper, speaks with Maurice Jackson of Proven and Probable about his company’s exploration activities in the Yukon.

Maurice Jackson: Joining us for conversation is Tim Johnson, the president and CEO of Granite Creek Copper Ltd. (GCX:TSX.V). Pleasure to be speaking with you today regarding the value proposition before us in Granite Creek Copper. Before we delve into project specifics, Mr. Johnson, please introduce us to Granite Creek Copper and what is the opportunity you present to the market?

Tim Johnson: Granite Creek Copper is a member of the Metallic Group of Companies; that’s a group that identifies what we see as undervalued opportunities. In Granite Creek Copper’s case we’ve acquired a large brownfields land position in the Minto Copper Belt in Yukon, Canada. It’s a type of thing that you can acquire at the low part of the market, which we think we are for copper, and we only see upside from here. We have assembled a team of professionals who can advance a project and we’ve acquired a significant land position.

Maurice Jackson: Take us to the Minto Copper Belt and provide us with some historical context on the region.

Tim Johnson: Well, it’s an interesting region. At one time it was held by a single junior mining company, United Keno Hill Mines. It did quite a bit of exploration in the belt. It was part of the discovery of the two major deposits in the belt, which one of them is now in operation, the Minto Mine, that was recently purchased by Pembridge. And the other one is the Carmacks Copper Project that is held by Copper North.

Granite Creek Copper sits right between them. Our ground, even though was held by this group, hasn’t seen any significant exploration since the early 1980s. So we were able to acquire a really unique property that wouldn’t normally have been available.

Maurice Jackson: To really appreciate the opportunity before us in the Stu Copper Project, which is your flagship project, share with us some of the resources and reserves from the Minto mines and the Carmacks deposit.

Tim Johnson: The most important number, in our context regarding the Minto Mine, is 3.9 million tonnes Proven and Probable. And the significance of that is that provides them roughly a four-year mine life with their current reserves. They do have some resources that they could probably convert, but we see them potentially running out of ore fairly shortly.

And then to the south of us, right adjacent to us, is the Carmacks Project and, again, they have a small deposit. They’ve got about a seven-year mine life as contemplated by a 2016 PEA. We don’t see that as being big enough. So we are strategically positioned very well to potentially provide mill feed for two mines, one to the north of us and one to the south. The one north of us is within about 25 kilometers, and the one to the south of us is right adjacent to our claim boundary. So any success that we have, we have potential partners to look at things. So we view both scenarios favorably.

Maurice Jackson: The Yukon is attracting a lot of investment. Who is investing there and why?

Tim Johnson: The majors in the past few years have taken another look at the Yukon. Newmont Goldcorp is in there in some of the gold spaces, Coeur Mining is in there and I think what you’re going to see over the coming years is more interest in the Yukon. I mean one of the reasons for that, it’s a great jurisdiction to work, theyre very forward thinking, they’re inviting investment. The Yukon government is one of the promoters of the mining industry itself, and they spend a lot of time and resources to try attract investment in into the region.

Maurice Jackson: There are some strategic advantages that Granite Creek Copper has over its peers that are exploring for copper with regards to brownfields exploration. They’re very important to know for our audience here, please share them with us.

Tim Johnson: We feel, and this is the philosophy of the Metallic Group itself, that we’ve acquired a land position that if a major was where we are in the copper space, they would have acquired it. So, if a major held the Minto Mine, for instance, we have the ground that they would be looking to acquire to expand their resource. That’s not the case here. In fact, there are three different juniors, one that’s got an operating mine, and one in near-term production and ourselves within a space that you would really see a major consolidate at some point.

And we think that one of our major advantages is that as we develop resources and our neighbors to the north and south, we think at some point there’s going to be a critical pound in the ground number that’s going to attract the big companies, the big copper companies, that are going to have to take a look at the belt.

Maurice Jackson: Mr. Johnson, introduces to your flagship, Stu Copper Project, and share some of the project highlights with us.

Tim Johnson: After we acquired the Stu Copper Project, we also acquired a historical database that was developed by the previous company, United Keno Hill Mines that I mentioned before. We’ve done some compilation work on that database and we’ve also signed datasharing agreements with our neighbor to the south. And by consolidating that data we’re starting to get some new, interesting ideas about our project. We recently completed a soil compilation that identified four significant multi-kilometer targets, and that was without putting any boots on the ground.

That was just taking the old data, getting it into modern GIS software and reviewing what we had. We’ve acquired over 5,000 soil samples, historical, most of them copper. So a lot of the work that we’re doing now is having to look at that, going back in, doing multi-element sampling just to see if the gold and the silver that we know is in the system can be advanced along with copper. Historically, there are some significant high-grade drill intercepts in the order of 2% to 2.5% copper, as high as 3% copper over 13, 14 meter intercepts. So not long, but significant grade.

Maurice Jackson: Granite Creek Copper has a database of historical data including drilling, trenching, geophysics and geochemical sampling. From those results, what makes Granite Creek Copper confident that they have the next major copper discovery in the Yukon?

Tim Johnson: Our compilation work has shown some significant multi-element targets. We are currently doing geophysics work to focus those targets and identify high priority drill targets. We know, based on the work of other operators in the belt, that a certain type of geophysics, induced polarity, that we’re using works quite well. We’re using known technology and we’re compiling known data and developing new targets. So, we think we’ve got a really good chance of developing significant resources, either for our neighbors to the south, or our neighbors to the north, or even a standalone operation should we develop enough.

Maurice Jackson: What can you share with us regarding soil anomalies?

Tim Johnson: Our recent compilation effort showed four large regional targets. One of them was new to us; it was in the data, but not obvious because different operators had held it in different broken up land ownerships over the years. Once we started to compile the data and realize where the data was in reference to the claim boundaries, we were able to actually develop a significant new target, our northeast target, as well as ones that are close to our southern claim boundary with Copper North.

Maurice Jackson: Now you somewhat addressed my next question, which was a two-fold question, which is have you identified drill targets and are you actively drilling there now?

Tim Johnson: We’re not actually drilling now, and when we acquired the property there were actually some pretty good drill targets from previous operators. However, we felt that a compilation effort, a review of the data and really wrapping our heads around what we had, before we rushed to drill, was the best approach. I think a lot of juniors, they rushed to drill to try and show what they’ve got, and I think that can be very dangerous. We’re comfortable with the compilation that we’re doing and the ground work that we’re doing this year to develop drill targets to be drilled as soon as we can next season.

Maurice Jackson: Let’s discuss some important topics germane to the project, beginning with reversionary interest. Are there any on the project?

Tim Johnson: There is a net smelter return on the project, other than the NSR we hold a 100% interest. It was acquired for stock. When we did the acquisition, Granite Creek had been a shell and we cleaned it up, put new management in place, and acquired this project. So other than the NSR, we have no obligations other than maintaining the claims in good standing by doing sufficient work on them on an annual basis.

Maurice Jackson: We’re going to get into some numbers later in this discussion, but from a capital expenditure standpoint, what is your largest expense, and at what cost?

Tim Johnson: Well, our largest expense will be drilling. You know, we envision a $1.5 to $2 million drill program next season. Our current exploration is in the $200k to $300k range and we expect that to develop significant targets for us for next season’s drilling program.

Maurice Jackson: Are you fully permitted?

Tim Johnson: We are fully permitted on about half the claim block, the southern half of the claim block. The northern half permits are underway. They’re with the Yukon government now. We don’t see a lot of problems getting the permit to the stage that we need for exploration. And then, as we move towards development, there’s another permitting process to go through.

Maurice Jackson: We’ve discussed the good, let’s address the bad. What can go wrong and what is your action plan to mitigate that wrong?

Tim Johnson: I think the biggest risk for us and our shareholders this time is the near-term price of copper. We see a little bit of weakness right now, but we don’t think that’s long term. We think in a 6 to 12 month timeframe that’s going to turn around. We see significant shortfalls in the copper market moving forward. So, we think that’s the biggest risk.

A possible mitigation would be look to another project, but we’re quite happy with the one we have; this is going to continue to be our flagship project. If the copper prices continue to stay soft, we will look at reducing our expenditures to preserve capital, but, long term this is where we want to be.

Maurice Jackson: Switching gears, let’s discuss the people responsible for increasing shareholder value. Mr. Johnson, please introduce us to your board of directors.

Tim Johnson: As president and CEO and director of the company, my background is logistics and project management. I’ve been in the public company space for almost 10 years now. Prior to that I ran a service company that had large projects in northern British Columbia, so I’m good at keeping things on track and on budget. Mike Rowley is also a director. He is president, CEO of Group Ten Metals and part of the Metallic Group. He’s been in a public space for about the same time, 10 to 12 years. He’s focused on his company, but also provides critical advice.

Another director of ours is John Cumming. John is a securities lawyer who’s been practicing in Vancouver for a very long time. And the last director is Francois Lalonde. Francois is an investor and businessman, an engineer. He lives in Montreal and provides us access to some of our potential investors there. So we’ve got a pretty well-rounded board.

In addition to that, because we are part of the Metallic Group of Companies, we access personnel such as Greg Johnson, who has a track record of taking resources and expanding and developing them. He is ex Novagold, and the CEO of Metallic Minerals, and we have access to some of his compatriots who were involved in that operation and many others. And, because of our association with the Metallic Group, we share geologists and geophysicists and professionals that we don’t have to pay their full salary because they’re spread amongst the group. So, the group is an opportunity for us to cost save and to access some of the personnel that we normally wouldn’t be able to, with a company our size.

Maurice Jackson: Well, good stewards of capital. Always good to hear. Who is on your management team and what skill sets do they bring to Granite Creek Copper?

Tim Johnson: Our management team includes individuals who were formally part of Metallic Minerals and when we formed the Metallic Group, we accessed them. So our geologist, Debbie James, does a lot of work for us. Scott Petsel does a lot of work for us. Again, these are individuals who have experience developing resources, taking small, underdeveloped resources and expanding them. We also have personnel with Debbie, including Lauren Blackburn, who have extensive experience in the Yukon, understand the Yukon geology and the ways of working with the Yukon government and local First Nations as, well.

Maurice Jackson: Let’s get into some numbers. Please share the capital structure for Granite Creek Copper.

Tim Johnson: We’ve got 35.7 million shares issued and outstanding, fully diluted 68 million. Roughly 37% to 38% of that is held by insiders and other people close to the company. So, we’re fairly tightly held, and with a significant holding of the insiders.

Maurice Jackson: How much debt do you have?

Tim Johnson: We have no debt. We’re currently about $700,000 cash positive.

Maurice Jackson: What is your burn rate?

Tim Johnson: Our burn rate is about $20,000 a month.

Maurice Jackson: Are there any redundant assets on the books that we should know about?

Tim Johnson: No, there are not.

Maurice Jackson: Are there any change of control fees and if yes, what is the compensation?

Tim Johnson: The change of control fees to the CEO is six months’ salary.

Maurice Jackson: Is management charging a consulting fee for any services?

Tim Johnson: Other than the CEO, I draw a salary, there’s no other management charges to the company.

Maurice Jackson: In closing, multi-layer question, what is the next unanswered question for Granite Creek Copper? When can we expect the response? And what determines success?

Tim Johnson: Big question is when do we drill? That is going to depend on the current ground programs going on, geophysics and soils, and of course the weather. We will likely have to do another raise in order to fund that drill program. But that’s the next question that we’re looking at.

Maurice Jackson: What keeps you up at night that we don’t know about?

Tim Johnson: I think the markets, really. Where copper is going, how long we’re going to see these slightly depressed prices and when we’re going to see a turnaround. We rely heavily on where copper price is going and the perception of the market.

Maurice Jackson: Mr. Johnson, last question. What did I forget to ask?

Tim Johnson: Well, I don’t know that you’ve got to ask it more like I forgot to mention it. What I forgot to mention is the nature of the two projects to the south and to the north of us. To the south of us, the Carmacks Project is an oxide copper project. To the north of us, the Minto Mine is a sulphide mine. The significance of this is that one mill can’t process the other’s material. We know that there’s some limited oxide at Minto and we know that there is some limited sulfide at Carmax, and we have both.

So, we could potentially see a scenario where trucks were shipping both ways. It would be picking up sulphide material from us delivering it to the mine to the north. Picking up oxide material from them, maybe some more from us, and delivering it to the mind to the south. So, the belt is really a significant consolidation potential with an oxide mill in the south, potentially, and a sulfide mill to the north and us in the middle. We think that’s a great scenario.

Maurice Jackson: And how does grade fit into the narrative?

Tim Johnson: This is some of the highest-grade copper in Western Canada, at Minto and potentially on our ground, and even the oxide resource to the south. So even though the tonnages are quite a bit smaller here than you would see, say, for a big porphyry system, the grade makes up the difference.

Maurice Jackson: Mr. Johnson, for someone listening that wants to get more information about Granite Creek Copper, please share the website address.

Maurice Jackson: For direct inquiries, call (604) 235-1982 or you may email [email protected]. Granite Creek Copper trades on the (TSX.V: GCX).

Before you make your next bouillon purchase, make sure you call me. I’m a licensed representative for Miles Franklin, precious metals investments, where we provided a number of options to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs, and private blockchain distributed ledger technology. Call me directly at (855) 505-1900 or you may email [email protected].

Finally, please subscribe to provenandprobable.com for Mining Insights and Bullion Sales.

Tim Johnson of Granite Creek Copper, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Granite Creek Copper. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Granite Creek Copper is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Metallic Group of Companies, Group Ten Metals, Metallic Minerals and Granite Creek Copper. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Metallic Group of Companies, Group Ten Metals, Metallic Minerals and Granite Creek Copper. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Group Ten Metals, Metallic Minerals, Granite Creek Copper, Coeur Mining and Newmont Goldcorp, companies mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Sector expert Michael Ballanger offers his observations of recent activity in the gold and silver markets.

“The permabulls will tell you that the bullion banks and their treasury department conspirators have lost all power in this ‘new paradigm’ and we should relax and refrain from worry. I tend to disagree because wounded animals are the singular most dangerous of all creatures on this debt-ravaged planet, and with gold at $1,552, these cartel cretins are now wounded, angry and very desperate animals.”

Michael Ballanger, Sept. 2, 2019; silver at $19.00 one day before the top

OK, so now that there is zero doubt surrounding the recent demise of the bullion banks, I was reminded yesterday (amidst the gnarling and gnashing of many a silver bulls’ incisors) of a famous Mark Twain quote surrounding rumors of his passing: “The reports of my death are greatly exaggerated.”

That is exactly the reply of the criminal cartel last week as bullion bank shenanigans took a page out of the Carpe Diem playbook and absolutely pounded the precious metals with such feral ferocity that they quite predictably set off a retail panic of the highest order. One very prominent gold and silver bull tweeted out, “It should be noted that Crimex silver is still up on the week!”, to which I quickly and cynically replied, “Tell that to my margin clerk.”

Tweets defending the tape action were furious all day Friday after noticeable calm on Thursday, and the fact that every single tweet was of the “BTFD!” or “buying opportunity” vintage, I would have felt a great deal better had there been a few “Get me the $#$% out!” tweets implying the arrival of panic, and not of the “buying” kind we saw on Wednesday. It would seem that the Millennials and GenX-ers suddenly discovered the precious metals over the Labor Day weekend and were abruptly punished for their tardiness. Empty vodka bottles and used vaping dispensers were everywhere. . .

The daily charts for gold and silver have recorded but a mere blip on the long-term radar screen and remain in beautifully choreographed uptrends. But there is one chart that has me a tad rattled and it is the weekly silver chart, where the arrival of the dreaded and most-foul “gravestone doji” marks a powerful reversal signal to a market that has been trending higher in orderly fashion since my July 2 bullish call at $15.00 silver at $14.20 SLV. The gravestone doji is one of the most reliable reversal indicators and is always found at the tail end of a bull move. When accompanied by the big volume spike we had last week in silver, it suggests that my re-entry into the silver market is going to be farther away and possibly a bit lower than I initially expected.

Going into Thursday, the number of tweets from newly minted gold “experts” (most of whom you know) that were the literary equivalent of a NASCAR victory lap, complete with buxomy girls and flowing champagne, were voluminous to the point where I actually tweeted this during the final orgasmic spike in silver on Wednesday: “Not ONErepeatNOT ONE bearish tweet on the PM sector in the past two sessionseveryone now long and strong with bows taken and egos fully erect.”

Whenever highly emotional extremes of either greed or fear enter the marketany marketI have learned over the years to be prepared to take the opposite side of the trade. Certainly there was an extreme last July when people were revolted by the prospect of owning silver, with more than a few of the “enlightened ones” calling for a 100 GSR (gold-silver ratio), which was the equivalent of capitulation.

I took the other side of that trade and remain short the GSR from 92.40 (currently 82.68). Similarly, I counted somewhere in the order of 75 bullish articles on silver and over 200 on gold by Wednesday of last week, and answered over 50 e-mail queries asking whether they should add to Aftermath Silver Ltd. (AAG:TSX.V) at $0.30 per share (up from $0.10 60 days prior).

The abject terror of early July was replaced with unwavering avarice last week, so naturally, seeing, feeling and smelling the odious presence of greed slithering its way into the gold and silver trading pits compelled me to take the other side of that trade as well. And I offer this not as a self-laudatory handwave but more as an educational lesson in human behavior.

What has annoyed me to no end in the past few weeks has been the presence of hubris in the collective psyches of many precious metals bulls, and it is not surprising that an attitude of “There! Take that, ya bastards!” was prevalent with regard to the bullion banks after year-after-year of intervention, interference and criminal collusion. I, too, was delighted in July when the $1,375 cap for gold was blown to smithereens by the combination of physical demand and rising mistrust. Notwithstanding the many thousands of dollars I left on the table by exercising the same prudence that saved my sexagenarian ass in past campaigns, the move into the $1,500s has been at once both vindication and celebration for a gold “opinionator” known to launch quote monitors from ninth-floor windows in search of banker craniums with alarming regularity.

However, the camaraderie among we gold bulls turned ugly when I started to read about a “new paradigm,” to the point where I wanted to take the term and install it in my lavatory. Just as pride cometh before a fall, tweaking the bulbous, red-veined noses of the bullion bank sloths is analogous to shuffling deck chairs on the Titanic; it invites a negative outcome.

That is why I started this week’s missive with a quote not from Ayn Rand or John Maynard Keynes but from last week’s missive. By last Wednesday, the bullion bank traders weren’t just irritated canines; they were bruised and bloodied wolverines, backed into a corner of the underground garage with nary a path for escape save launching a final desperate attackand attack they did, sending the gold and silver bulls reeling into urgent and intensified retreat after weeks of complacency and control.

If there is one thing I have learned over the years, you do not tempt fate. In the minds of those who control governments and their military-industrial complexes, gold is the enemy. Rising gold prices are the financial equivalent of nuclear missiles being shipped to and installed in Cuba. Neither will be tolerated (for very long) by those wielding the baton of power and if we, for one millisecond, forget that, we are doomed to margin call miasma and deflated dreams.

Wall Street symbolizes the American Way of Life and all that is good that separates them from the heathens in Afghanistan or Venezuela. When rising gold prices hijack the financial news headlines, you had better prepare yourselves (and your margin clerk) for a change of venue. The most dangerous phrase in all of trading is “It’s different this time.” It is never, ever, “different”. . .

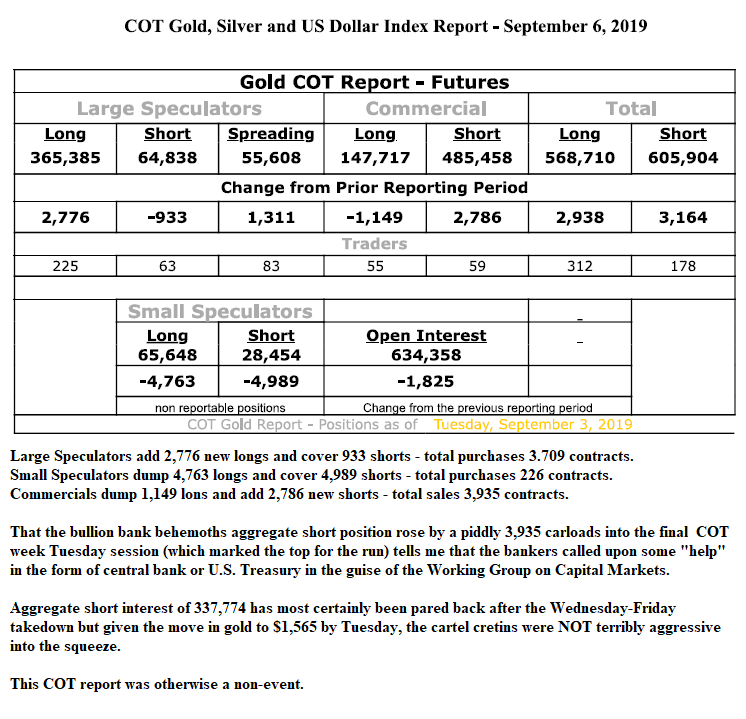

Cot Report

The September 2 COT had only one notable item: The bullion banks were afraid of adding more than 4,000 new shorts to their positions despite a massive price surge on Tuesday. That is informative. (See below.)

To summarize what I deem as a “watershed week,” I go into Monday morning with a 53.7% cash position my unleveraged trading account and 85% cash in the leveraged account. The GGMA portfolio is essentially my unleveraged account and is now up 163% year to date. But what is important for me is being able to resist the temptation of buying back all positions that I put on in the first half of the year too early.

In an election year, the incumbent president (and particularly DJT) will be acutely aware of the S&P 500 and of gold prices. I do not trust these insidious serial manipulators because the most mind-numbing and alluring narcotic of all is power, and with the addictive personalities sported by all politicians, there is little if anything they will not do to lose their grasp of it.

Therein lies the danger in assuming that physical demand alone will give way to unimpeded advances in gold and silver; the central banking global cabal has many tools at its disposal, and to underestimate its willingness to use them to advance its own agenda would be abject folly. What we witnessed late last week was most certainly a healthy and well-deserved spate of gold ol’ all-American profit-taking in the metals but the manner in which it closed out the week, and particularly the post-Crimex Access market, reeked of the all-too-familiar odor of interference.

While natural forces may have initiated the pullback, a malevolent and purposeful force exacerbated it and that was clearly evident in the final hours on Friday. While the bullion bank behemoths were blatantly timid earlier in the week, someone or something gave them great confidence in pressing their bearish bets late Friday, and I think readers of this publication have a pretty good idea who or what that presence might be.

Wounded animals, indeed.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Aftermath. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver, a company mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

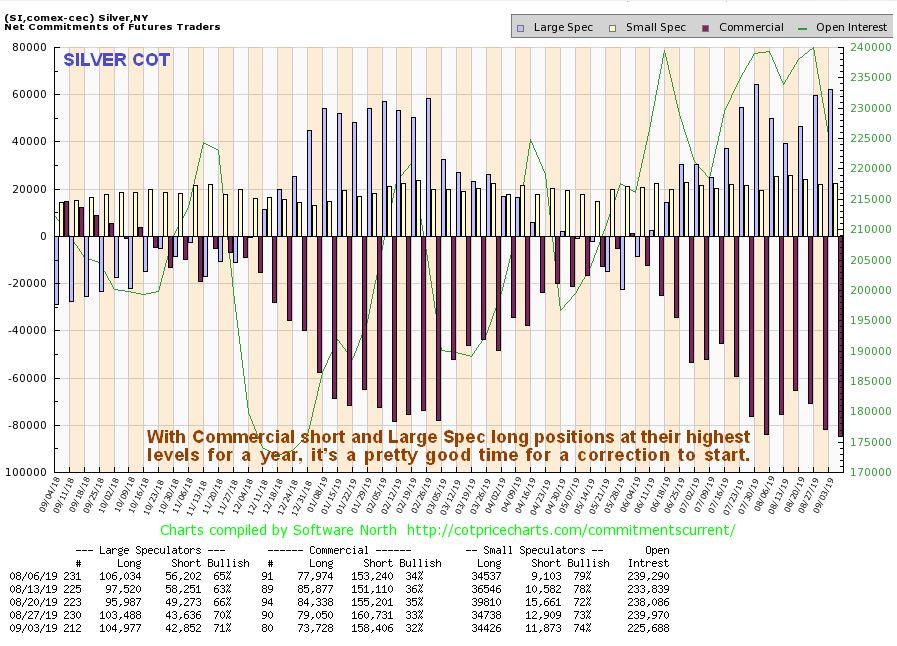

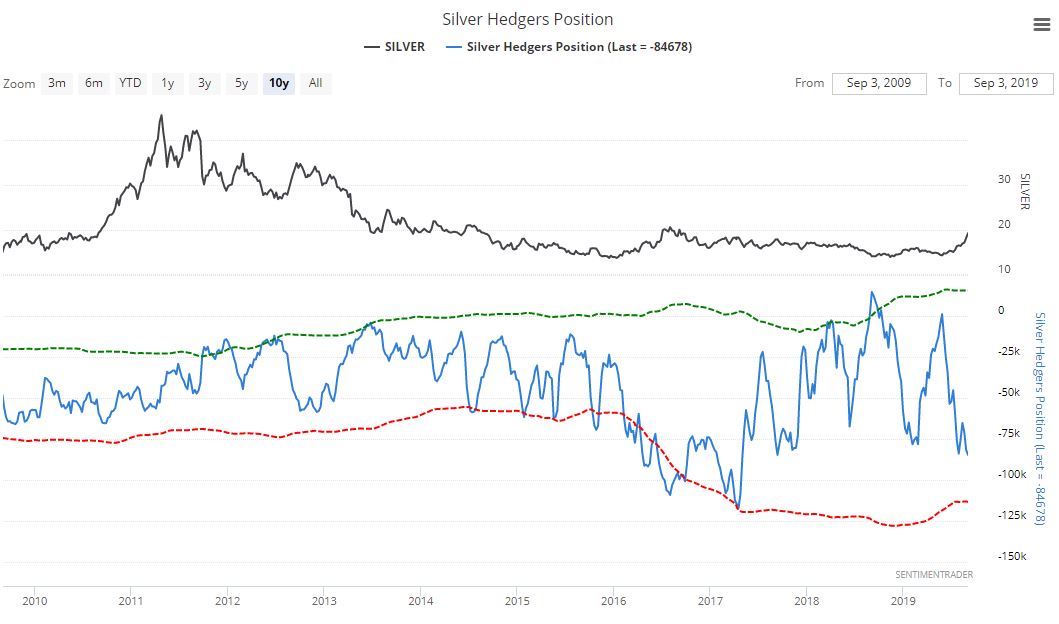

Technical analyst Clive Maund charts silver and explains why he believes it hasn’t hit a final top.

Silver reacted back sharply on Thursday and Friday after a parabolic blowoff top. This was not a final top, but it does indicate that silver needs to take a rest and consolidate/react back, probably for at least several weeks.

The latest silver COT is also showing a 1-year record extreme for positions, giving grounds for caution

Click on chart to pop-up a larger, clearer version.

Although the longer-term Hedgers chart for silver is not at the extremes that it reached in 2016 and 2017, readings are also at levels that give grounds for caution, especially considering that silver just did a parabolic slingshot move.

Click on chart to pop-up a larger, clearer version.

Chart courtesy of sentimentrader.com

The conclusion is that silver has started a corrective phase, and, given the nature of the beast, it could be quite scary for the unprepared once it breaches the parabolic uptrend, but with gold especially having signaled the start of a major bull market any such corrective action will be viewed as presenting a rare opportunity to buy silver investments at very good prices ahead of the major uptrend that is expected to follow.

Originally published on CliveMaund.com on September 9, 2019

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

The Japanese Yen is entangled in losing battle against every single G10 currency today as risk appetite improves on trade optimism and hopes of global economic stimulus.

Attraction towards the Yen is set to weaken further if the European Central Bank (ECB) satisfies market expectations by unleashing a fresh wave of monetary stimulus to boost the Eurozone economy. The USDJPY already trading at levels not seen in 5 weeks above 107.30 as of writing. In regards to the technical setup, the currency is bullish on the daily charts as there have been consistently higher highs and higher lows. A solid daily close above 107.50 should trigger a rally towards 108.00 and 108.30, respectively.

Euro on standby ahead of ECB meeting

Where the Euro concludes this week will be heavily influenced by what the ECB does on Thursday.

The central bank is widely expected to cut deposit rates by 10 basis points and restart quantitative easing (QE) from October. While this may be good news for the Eurozone economy, it is certainly negative for the Euro which remains near a 2-year low against the Dollar.

Euro bears still remain in firm control on the weekly charts thanks to fundamental and technical themes weighing heavily on the currency. A solid weekly close below 1.10 should inspire a decline towards 1.09.

AUDUSD punches above 0.6830

Concerns over the health of Australia’s economy and speculation around the Reserve Bank of Australia (RBA) coming to the rescue by easing monetary policy will weigh on the Australian Dollar. Buying sentiment towards the currency is set to remain muted following reports that the economy grew at its slowest pace since the global financial crisis in the last quarter (Q2).

Although the AUDUSD staged a rebound yesterday, the currency remains firmly bearish on the daily charts. A breakdown below 0.6830 should inspire a selloff towards 0.6700. Should 0.6830 prove to be a reliable support, prices could end up trading back towards 0.6920 and 0.7000 before bears reclaim control of the driving seat.

Commodity spotlight – WTI Oil

Oil prices pushed higher on Tuesday thanks to optimism over OPEC + extending production cuts in bid to stabilize markets and support prices.

The upside is was complemented by optimism over US-China trade talks and easing concerns over slowing global growth. WTI Crude certainly has scope to push higher in the near term and this continues to be reflected in price action.

Focusing on the technical picture, the upside momentum should open doors towards $63.00. A breakout above this resistance level could trigger a move to $65.00.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

U.S. Rep. Alex X. Mooney, R-West Virginia, is continuing his efforts to get answers from the U.S. Treasury Department, Federal Reserve, and Commodity Futures Trading Commission about surreptitious interventions by the U.S. government in the financial and commodity markets and particularly the gold and silver markets.

Mooney’s efforts began with letters sent to the Federal Reserve chairman and treasury secretary in April 2018:

In July 2018 the Fed and Treasury responded to Mooney but only incompletely, the Fed denying that it was trading in gold but refusing to say whether it is trading in other markets, the Treasury giving a partial denial of gold trading but failing to answer about the government’s policy toward gold:

In February this year Mooney asked the CFTC, as GATA already had done, if it has jurisdiction over manipulative trading undertaken by the U.S. government or brokers acting for the U.S. government, or if such manipulative trading is authorized by federal law:

The CFTC has never responded to GATA or to Mooney.

Summarizing the major questions that remain unanswered:

1) What is U.S. government policy toward gold? Is the policy still to drive gold out of the world financial system in favor of the U.S. dollar, as State Department records show the policy was in the 1970s?

2) Is the Treasury Department’s Exchange Stabilization Fund transacting in gold?

3) What markets are the Fed and Treasury trading in, through what mechanisms, and for what purposes?

4) Does the CFTC have jurisdiction over manipulative trading by the U.S. government or its agents?

5) Has the U.S. gold reserve ever been audited for any encumbrances? If so, what were the findings?

Mooney’s latest letter to Treasury Secretary Steven Mnuchin, sent last month, is here:

Of course the refusal of the Fed, Treasury, and CFTC to answer the congressman’s questions promptly and fully is strong evidence that the U.S. government is deeply and comprehensively involved in market manipulation.

If only mainstream financial news organizations and financial market analysts had the courage and integrity to pose Mooney’s questions on their own behalf. Then the world might enjoy some actual financial journalism — and the market rigging and the imperialism the rigging represents might be defeated and free and transparent markets restored along with limited and accountable government.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.