Shares of Achillion Pharmaceuticals are trading much higher today after the firm reported that it has agreed to be acquired by Alexion Pharmaceuticals for $930 million, or $6.30 per share in cash, along with the potential for an additional $2 per share if certain other specific clinical trial and regulatory milestones are met.

This morning prior to the market open, Achillion Pharmaceuticals Inc. (ACHN:NASDAQ) and Alexion Pharmaceuticals Inc. (ALXN:NASDAQ)announced that they have entered into a definitive agreement for Alexion to acquire Achillion, a clinical-stage biopharmaceutical company “focused on the development of oral small molecule Factor D inhibitors to treat people with complement alternative pathway-mediated rare diseases, such as paroxysmal nocturnal hemoglobinuria (PNH) and C3 glomerulopathy (C3G).” The release indicates that Achillion currently has two clinical-stage medicines in development, danicopan (ACH-4471) in Phase 2 and (ACH-5228) in Phase 1.

Under the terms of the transaction, Achillion shareholders will initially receive $6.30 cash per share of Achillion common stock, for a total price of approximately $930 million. The report further indicates that the transaction includes the potential for additional consideration in the form of non-tradeable contingent value rights (CVRs), which will be paid to Achillion shareholders if certain clinical and regulatory milestones are achieved within specified periods. These CVRs include $1.00 per share for the FDA approval of danicopan and $1.00 per share for ACH-5228 Phase 3 initiation.

The report notes that the acquisition is subject to the approval of Achillion shareholders and satisfaction of customary closing conditions and approval from relevant regulatory agencies, including clearance under the Hart-Scott Rodino Antitrust Improvements Act, and is expected to close in the first half of 2020.

For Alexion, the benefit of the deal is that it adds a clinical-stage portfolio of oral small molecule Factor D inhibitors to its pipeline. “Factor D is an essential serine protease and critical control point in the alternative pathway (AP) of the complement system, a part of the innate immune system.” The release further states that deal provides the opportunity to “enhance treatment for Paroxysmal Nocturnal Hemoglobinuria (PNH) patients experiencing extravascular hemolysis (EVH) with a potential first-in-class C3 Glomerulopathy (C3G) therapy and promising development platform for Factor D inhibition in additional alternative pathway complement-mediated rare diseases.” C3G is an ultra-rare kidney disease for which there is no approved treatment.

Achillion ‘s President and CEO Joe Truitt commented, “We have established great momentumdiscovering and advancing several small molecules into clinical development that have the potential to treat immune-related diseases associated with the alternative pathway of the complement system. . .Having already demonstrated proof-of-concept and proof-of-mechanism with our lead candidate, danicopan (ACH-4471), in PNH and C3G, respectively, we believe there is significant opportunity for Factor D inhibition in the treatment of other diseases as well. Alexion is an established leader in developing medicines for complement-mediated diseases, and we look forward to working together to accelerate our objective of bringing novel therapies to patients as quickly as possible and ensuring that the broad promise of this approach is fully realized.”

Ludwig Hantson, Ph.D., CEO of Alexion, stated, “Alexion has demonstrated the transformative impact that inhibiting C5 can have on multiple rare and devastating diseases. However, we believe this is just the beginning of what’s possible with complement inhibition…Targeting a different part of the complement systemthe alternative pathwayby inhibiting Factor D production addresses uncontrolled complement activation further upstream in the complement cascade, and importantly, leaves the rest of the complement system intact, which is critical in maintaining the body’s ability to fight infection. We believe this approach has the opportunity to help patients with diseases not currently addressed through C5 inhibition. We look forward to applying our nearly three decades of complement and development expertise to unlock the potential of oral Factor D inhibitors and bring these benefits to patients.”

Alexion Pharmaceuticals is headquartered in Boston, Mass., and has offices around the world serving patients in more than 50 countries. It describes itself as a global biopharmaceutical company “focused on serving patients and families affected by rare diseases through the discovery, development and commercialization of life-changing therapies,” and focuses its research efforts on the core therapeutic areas of hematology, nephrology, neurology and metabolic disorders. Alexion trades under the symbol ALXN on the NASDAQ and has a market capitalization of about $23.5 billion.

Achillion Pharmaceuticals is a “clinical-stage biopharmaceutical company focused on advancing its oral small molecule complement inhibitors into late-stage development and commercialization” in the therapeutic areas of nephrology, hematology, ophthalmology and neurology. The firm notes that the potential indications being evaluated for its compounds include paroxysmal nocturnal hemoglobinuria (PNH), C3 glomerulopathy (C3G), and immune complex membranoproliferative glomerulonephritis (IC-MPGN). The company reports that it received Breakthrough Therapy designation for danicopan for treatment in combination with a C5 monoclonal antibody for patients with paroxysmal nocturnal hemoglobinuria (PNH) who are sub-optimal responders to a C5 inhibitor alone.

Achillion Pharmaceuticals began the day with a market capitalization of about $509.9 million and approximately 139.7 million outstanding shares. ACHN shares opened nearly 75% higher on the news today at $6.38 (+$3.65, +74.79%) compared to the prior day’s $2.73 closing price. The stock has traded today on very high volume between $6.10 and $6.44/share and at present is trading at $6.23 (+$2.58, +70.68%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Jordan Trimble, CEO of Skyharbour Resources, sits down with Maurice Jackson of Proven and Probable to discuss his company’s exploration plans in Canada’s uranium-rich Athabasca Basin.

Maurice Jackson: Joining us for a conversation is Jordan Trimble, the president, director and CEO of Skyharbour Resources.

Glad to have you on the program to discuss Skyharbour Resources Ltd. (SYH:TSX.V; SYHBF:OTCQB) is a preeminent uranium explorer in Canada’s Athabasca Basin. Readers should note that we recently conducted a very thorough comprehensive interview regarding the value proposition of Skyharbour Resources. We encourage you to visit that interview to fully appreciate today’s interview. Mr. Trimble, please introduce us to Skyharbour Resources and the opportunity the company presents to the market.

Jordan Trimble: We are a high-grade uranium exploration and early-stage development company with projects in the Athabasca Basin in northern Saskatchewan, which is known for the highest-grade depository of uranium in the world. We have six projects scattered throughout the Basin on the west side near recent notable discoveries made by NexGen and Fission, as well as projects over on the east side where you have infrastructure and the largest and richest uranium mines in the world being at McArthur River and Cigar Lake. We’ve done a good job over the last five or six years of acquiring projects at attractive valuations in a depressed uranium market.

Our flagship project is a project called Moore Lake. Moore Lake is a project we acquired about three years ago from our largest shareholder and strategic partner, Denison Mines. We’ve been actively exploring and advancing that project, making some recent notable discoveries. We are now preparing for a winter drill program. That’s a big upcoming catalyst for the company, and then in addition to our offering that high-grade discovery potential, really looking to emulate the recent again successes at the Nexgens, Fissions, Hathors of the world. We also act as a prospect generator. We look to bring in partner companies to advance our other projects.

Notably, we’ve done two deals in the last several years, one of which is with France’s largest uranium mining company known as Orano, previously called AREVA, where it can spend upwards of $8 million to earn up to 70% of our Preston Project. We conducted a similar deal with Azincourt a few years back under similar terms where it spent $3.5 million, to earn up to 70% of our East Preston Project. A good complement to what we’re doing at our flagship. These partner companies fund the work. We get some cash payments from them, and we also benefit from news flow.

That’s the company in a nutshell, run by myself, my team here in Vancouver, and my head geologist and a director of the company, Rick Kusmirski, and our geological team in Saskatoon. Some notables on the Board and Advisory Board, David Cates, who is the president and CEO of Denison Mines, which is our strategic partner and our largest shareholder. Another gentleman, Paul Matysek, a strategic advisor to the company. Skyharbour Resources has a good technical team and management team and a strong shareholder base as well.

Maurice Jackson: To gain some better context and appreciation for Skyharbour’s most recent press release, Mr. Trimble, where in the Athabasca is the flagship Moore Lake Project located? How many hectares does it contain?

Jordan Trimble: The Moore Lake Project is a big property. It’s about 36,000 hectares. It’s located on the east side of the Athabasca Basin, south of McArthur River, and approximately 13 kilometers east of Denison’s flagship Wheeler Project. The road that goes up to McArthur River is actually in between Denison’s project and our project. Logistically for us, especially in the winter, it’s very easy to get in and out. The main Maverick corridor where most of the drilling is focused is very easy to work on. The infrastructure allows our drill costs to come down quite a bit as we are ideally located or situated on the east side where the infrastructure is, power, roads, existing mines and mills. That’s an important part of the story here for us at our flagship project.

Maurice Jackson: Jordan, take us to your flagship Moore Lake Project, which is known for its rich, high-grade uranium, and let’s discuss the details of the company’s latest press release regarding airborne geophysical surveying and the exciting plans for the upcoming drill program.

Jordan Trimble: We announced about a week ago results from a UAV drone MAG survey flown by Pioneer Aerial Surveys, and so this is a new technique that we’re using to refine and identify new and existing targets at our flagship project, Moore Lake Project. At the project, there’s a 4-kilometer-long structural mineralized corridor called the Maverick corridor. This is where most of the historical exploration and the drilling we’ve carried out over the last several years has been focused. There’s high-grade uranium mineralization there, upwards of 21% U308. There are several high-grade pods along strike on this 4-kilometer-long corridor, but really only 2 kilometers of it has been systematically drill tested, so there’s room to expand alongside strike, make additional discoveries.

What’s intriguing right now and what’s significant for this upcoming drill program is that we are now looking a little bit deeper in drill testing, a little bit deeper into the basement rocks. Worth noting, these recent discoveries that were referenced with NexGen, Fission, the Gryphon deposit that Denison discovered several years back, these are all basement-hosted deposits below the sandstone sediments and the unconformity being the contact.

Finding these feeder zones in the basement rock, that’s where you can really find your biggest and highest-grade deposits in the Athabasca Basin and what’s exciting about this project right now is that using these new techniques, these MAG surveys flown by drones, we’re able to get a more refined geophysical signature, get a better picture of what is happening beneath, and properly with pinpoint accuracy target these potential feeder zones. We really believe that we’re going after some of our best targets.

It’s worth noting in the last drill program, which was earlier in the year, one of our last drill holes intersected some of the highest-grade mineralization that we found in the basement rock on this project to date. Again, relatively untested. We really think we’ve just scratched the surface and we believe we’re on to finding something much larger in these basement rocks.

The results from the MAG survey identified cross-cutting structures, features that basically come and break up that main structural corridor and allow the fluids, uranium to come up. We’ve identified a couple of top priority targets, one of which is at what’s called the East Maverick Zone. This was a new discovery we made a few years ago where we discovered high-grade mineralization along strike from the main Maverick Zone and we had grades there upwards of 9% over a meter and a half.

In this last drill program, on one of these last holes drilled we successfully hit high-grade in the basement rock, but we haven’t been able to follow up on it yet. Sure enough, we flew the drone survey. We see a target a little bit deeper down and we’re going to be drill testing that in this program coming up. We also have another zone about a kilometer and a half along strike up to the northeast called the Viper Zone.

We’ll be drill testing the Viper Zone, and then from a regional perspective, it’s a big property, we’re going to be going back into an area that’s had limited historical drilling called the Otter Zone, and this was a zone about 9 kilometers away actually from that main Maverick corridor that we drilled a couple of holes earlier this year. It had anomalous uranium mineralization, but definitely warrants follow-up work, so we’ll be doing a little bit of exploratory work and drilling there as well.

Maurice Jackson: Let’s discuss the forthcoming drill program.

Jordan Trimble: It’s going to be winter drill program. We’re waiting for freeze-up, so that’ll be later this year and early in the new year. We have planned and budgeted for 2,500 meters of drilling. We’ll have details out on this drill program over the next month or two here, so look out for additional news flow on that. We’re just going through the final plan right now, and we have those highlighted for readers in our news release. Most of the drilling focused at the Maverick Zone, in particular the Maverick East Zone and then the Viper Zone, and then a regional target at the Otter Grid.

Maurice Jackson: What are some of the potential catalysts on the horizon for shareholders?

Jordan Trimble: The big one needless to say is this upcoming drill program. One hole can change the fortunes for the company and can really be a game changer. I think given the current valuation and market cap, one big hole we can see a significant price increase on that. Again, we’re out there looking to make that next big high-grade discovery, continuing to advance our flagship project. That’s a big one, but we also, as I mentioned earlier, acting as a prospect generator, have partner companies that are planning upcoming work programs, specifically Orano at our Preston Project, which is adjacent to NexGen’s ground and Fission as well on the west side of the Athabasca Basin. Orano completed previous drill programs and exploration programs at Preston and it is now planning for an upcoming winter program as well. We’ll have details on that program when we get the final plan from them.

In addition, last month we shared our partners at Azincourt announcing plans for a 2500-meter drill program at our East Preston Project. These are partner-funded programs. Collectively, the partners spending upwards of $11.5 million to earning up to 70% of our Preston East and Preston Project. Both of these programs will provide news flow for Skyharbour. We do get some cash payments as per the option earning agreements with the partners and it’s a great complement to our value proposition. These are added catalysts that we have at our flagship project, Moore.

Another note I’ll just make is we are talking with other companies right now regarding interest that we are receiving from other groups on additional noteworthy projects that we have as a prospect generator. We’re always looking to bring in strategic, value-add partners to come in and advance our secondary projects, and we have three other projects on the east side of the Athabasca Basin in Falcon Point, Mann Lake, and Yurchison, all three which are a 100% owned. Falcon Point is worth noting that there’s a small resource there, NI 43-101 compliant inferred resource, and a very high-grade surface showing on the north end of the property at 68% U308. A project that we would like to get back to work to or find a partner company to come in and fund that exploration, as we think there’s a lot more to be found there.

Maurice Jackson: Switching gears. Mr. Trimble, please share the current capital structure for Skyharbour Resources.

Jordan Trimble: Skyharbour Resources has 64 million shares issued and outstanding. I’d say just under half of that is in the hands of several groups, including management and insiders. As I mentioned, Denison Mines is our largest strategic shareholder. We have a few funds and institutional investors that have come in over the last several years.

Maurice Jackson: When was the last time you purchased shares? At what price?

Jordan Trimble: That was actually today. I’ve been buying more shares in the market over the last several weeks. In the last couple of months here, just a note on the market post-Section 232, we have seen a sell-off across the board with uranium companies. There was a lot of money or some money that came into the sector about a year ago that drove higher prices, and some of that money that came in came in on a trade on this 232. It was event-driven funds and money that came in that bid these companies up.

We also saw that in the backdrop of a rising uranium price, but we’ve now seen some of those funds have to exit the sector and we’ve seen a sell-off as a result of that, so it’s, I think, really just a short-term unfortunate sell-off that we’re going through, again, across the board. It’s, I believe, an incredible buying opportunity and value proposition, given that we’ve continued to advance our projects. I think there’s going to be also a move in the uranium price here between now and year end that will help drive higher prices. I think the value proposition right now is really better than ever given the upcoming catalysts we have and, again, this uranium market recovery.

Maurice Jackson: Mr. Trimble, last question. What did I forget to ask?

Jordan Trimble: I would like to touch on the uranium market. It’s obviously a big part of our story and there’s a lot to update on since we last spoke. We have seen the uranium price settle in. It’s pulled back a little bit earlier in the year, but it has settled in the mid-20s. We’re still trading near historical lows and in inflation-adjusted terms, we’re trading well below that average global cost of production. We need to see a much higher uranium price for new mines to come on-line, for existing mines that have been idle to come back on-line, most notably McArthur River. There’s a good case, a compelling case, for much higher uranium prices given the supply-demand. We’re now seeing a major supply deficit forming.

I was just at the World Nuclear Association Symposium in London, which is one of the marquee conferences for the nuclear industry and uranium mining industry held annually in London and was quite interesting. The association came out with its bi-annual fuel report and this was, I think, one of the key takeaways from the conference is seeing that fuel report really I think opened a lot of people’s eyes to what’s happening in the uranium mining sector right now. You’ve had major supply curtailments, almost 30% of global primary mine supply that’s been either shut down or curtailed, including as I mentioned McArthur River in the Athabasca Basin. You’ve seen major supply cuts in response to a low commodity price environment. We’re now producing about 135 million pounds from primary mine supply and that’s in the backdrop of well over 190 million pounds of annual demand in reactor requirements. I think something has got to give. That’s obviously coming from secondary supplies.

I think we’ll see secondary supplies continue to dwindle here and we’re seeing that spot market tightening up. One of the big talking points going forward here in the near term, and potentially one of the biggest catalysts for any uranium company, is the fact that Cameco, because it has shut down its largest mine at McArthur River, it has to buy or shore up supply of uranium either in the spot market or from other secondary sources to meet to delivery into the contracts that it has with utility companies. We now know that it has to buy quite a bit between now and year-end, potentially upwards of 10 million pounds, and then next year over 20 million pounds. That’s a lot of material that it has to get either from secondary supplies or what appears will happen, it will have to buy some of that, if not all of that, in the spot market over a very short period of time.

Just to give some perspective on that, a year ago when a lot of these uranium companies including us were hitting 52-week highs, that was driven by a uranium price increase from the low $20s to about $29 a pound in about a five-month period. A big part of that was Cameco buying in the spot market and it bought about 8 million pounds. Here we are today and Cameco has to buy about 10 million pounds between now and early in the new year, and so this could be one of the single-largest catalysts for the spot price over the coming months. I think if we see that spot price break $30 a pound, we’ve seen this resistance in the high 20s, but I think if we see it break $30 a pound, I think that is what is going to spur utility buying contracting to pick up.

In our previous interview, we’ve discussed Cameco’s participation is going to be one of the more important catalysts coming up over the next few years, but I think it’s waiting to see that price tick up through $30, and as we’ve seen in the past. It’s important to note, that the combined market capitalization of all publicly traded uranium companies is less than $10 billion. That means that money that comes into the space works its way down to the junior companies like Skyharbour quite quickly, so we see that uranium move as we have seen a few times in the past several years. We benefit from that quite quickly. Money flows down quickly from the large caps to the small caps in the sector.

Maurice Jackson: Mr. Trimble, for someone listening that wants to get more information about Skyharbour Resources, please share the website address.

Jordan Trimble: Absolutely, so it’s skyharbourltd.com. More than welcome to get in touch with me directly my office, or you can email me at [email protected].

Maurice Jackson: Skyharbour Resources trades on the (TSX.V: SHY| OTCQB: SYHBF). Skyharbour Resources is a sponsor of Proven and Probable. As a reminder, I’m a Licensed Representative for Miles Franklin Precious Metals Investments. We offer a number of opportunities to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs, and private blockchain-distributed ledger technology. Call me directly at 855-505-1900 or you may email [email protected]. Finally, please subscribe to provenandprobable.com. We provide Mining Insights and Bullion Sales.

Jordan Trimble of Skyharbour Resources, thank you for joining us today on Proven and Probable.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Skyharbour Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Skyharbour Resources. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Skyharbour Resources, a company mentioned in this article.

Images provided by the author.

Proven and Probable Disclosures: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Getting your head around how margin works, and the different subdivisions it has in forex can be an exercise even for those gifted in math.

To complicate matters further, there are a lot of margin calculations which aren’t used in your day-to-day forex trading. And it’s not practical to worry too much about them!

So, let’s figure out what’s need-to-know information about margins, and how to use it to improve your forex trading results.

If you’ve already opened your FX trading account, you know what margin is. But the purpose of this article isn’t to repeat theory, but rather to have a look at the practical concepts that you can incorporate into your daily forex trading.

Margin Isn’t Just a One-Off Decision

So, when you open your account, you decide on how much leverage you want.

After that, you typically don’t change your margin. This can lead some FX traders to forget about it. But it has a direct impact on how much you can trade.

There are other articles that get into the mechanics of leverage and margins, but the practical effect is that your account leverage shows how much you borrow from your forex broker each time you open a trade.

For example, if your leverage is 1:100, that means for each $1 that you put up for trade, your broker will “loan” you $99 so you can trade $100.

This is important because a 1% move with $100 is very different than with just $1. Leverage is how you can make (and lose) a lot more in the forex markets by putting relatively small amounts of money in your account.

Margin Calls

The thing with this “loan” that your forex broker gives you when you trade, is that, if the trade goes in your favor, everything is fine.

When you close the trade, you pay back the “loan” and take the profit. But, if the trade goes against you, then you start losing money.

The forex broker knows you can pay the amount that you’ve put up for the trade, and in order to make sure you don’t lose more than that, typically will close your trade in order to recover the “loaned” money.

This is known as a “margin call”. So, the amount of money you put up for a trade is how much “margin” you have for market moves against you. Using our 1:100 leverage example, if you put up $1 to trade, you can take a $100 position.

If the market goes down by 0.5%, that means you’ve lost $0.50. It’s still within your “margin” of $1; but if the market goes down by 1%, then you’ve “lost” $1, and your broker will call the trade off, so you don’t start going into negative.

The Whole Account is in Play

Generally, forex brokers try to give you a little extra leeway with your trades by doing the complement of that principle. So, when you enter a trade, the FX broker “locks” in that amount and the rest of your account acts as margin.

Practically speaking, let’s say you have $50 in your account, and take a $2 position. At 1:100 leverage, it means you can buy $200 in the market. That $2 gets “locked” by your broker to cover your current trade, and the remaining $48 is called your “free margin”. That’s how much is still available in your account to put up to trade.

If the market goes in your favor, your portfolio equity increases, and you have more margin available. That is, you have more free margin. And if the market goes against you, then you have less equity available, and therefore less free margin.

Keep an Eye on the Gas Tank

If an analogy helps understand this, let’s turn to cars. Leverage would be like the size of your engine: the bigger it is, the faster you go, but the more gas you need.

Your gas tank would be like your free margin. If you go fast (open a lot of trades) you use up more margin. If you have a smaller engine (lower leverage) then you use less gas. And, of course, if you run out of gas, then your car stops – just like your forex trading stops when you run out of margin!

Veteran investor and newsletter writer Chen Lin explains the upside he sees with this energy company.

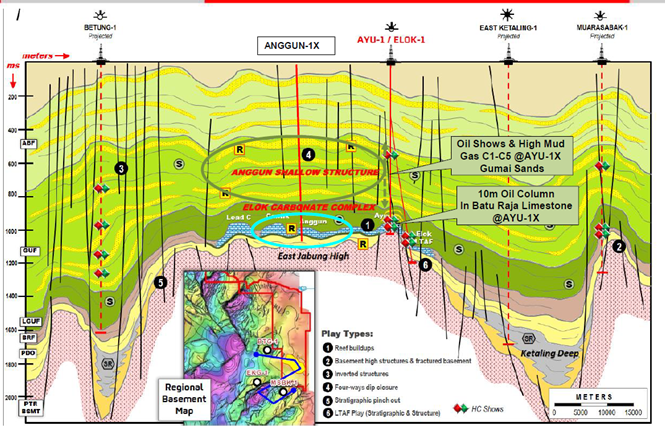

In late 2008, when the world was in the middle of the great recession, a young energy company was looking to take advantage of the circumstances by bargain hunting. Led by CEO Jeff Chisholm, a well-known goldbug, Pan Orient Energy Corp. (POE:TSX.V) has always maintained a strong balance sheet. When the market crashed and everyone, including the largest energy companies in the world, was looking for cover, POE was able to take advantage of it. One of POE’s key acquisitions was East Jabung PSC. POE was the sole bidder in that bid round. (Where were Exxon, Repsol and PetroChina?)

In the years prior to the tender of the East Jabung PSC, the surface area covering the majority of the Anggun prospect was re-classified from restricted forest (where only seismic is allowed) to production forest (where both seismic and drilling are allowed). Jabung PSC is in the region of the most prolific oil and gas fields in South Sumatra, Indonesia. It hosts the largest gas discovery in the past 18 years in Indonesia. That news was announced earlier this year by Repsol. POE had acquired the acreage next to it for a song!

As the sole bidder, POE became 100% owner of the concession. This was a huge concession and POE decided to partner with Talisman (now part of Repsol) for down payment, part of Repsol exploration concessions and to carry the cost of the first two wells. Repsol drilled one well at the edge of the structure two years ago and had a very promising find of oil and gas. Now they are moving the rig to the center of the structure. We expect the rig to be spud in late October and TD in 3040 days.

Repsol had high hopes for the East Jabung target. A permanent road was constructed so they can use it in the long run to drill more wells, should they have a major discovery in the area. The permanent road probably delayed the drilling for about one year and add a lot to the cost. However, it will be a good move if they hit the next high impact well.

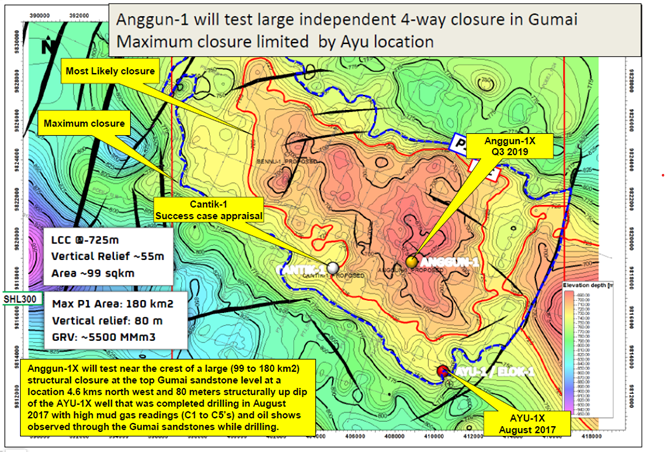

Now the long wait is over and the stage is set for the next high impact well, Anggun-1X, in East Jabung. We are hoping it will be one of the largest discoveries in Indonesia and potentially one of the largest onshore conventional discoveries in the world. We should have the results in late Q4. If it is successful, Repsol will pay for this well. Repsol will continue to drill out the area in 2020 and beyond and POE will need to fund 49% of the cost. With POE’s current strong balance sheet and a strong cash flow from Thailand, POE should be able to fund the continuing exploration without the need of raising money from the market. In the past decades, very seldom we see junior companies involved in the major discoveries in the world. Usually majors, well connected and well capitalized companies, took all the best prospects. We have a unique opportunity to participate in this potentially huge discovery without any major dilution. After years of waiting, the key drilling is about to happen.

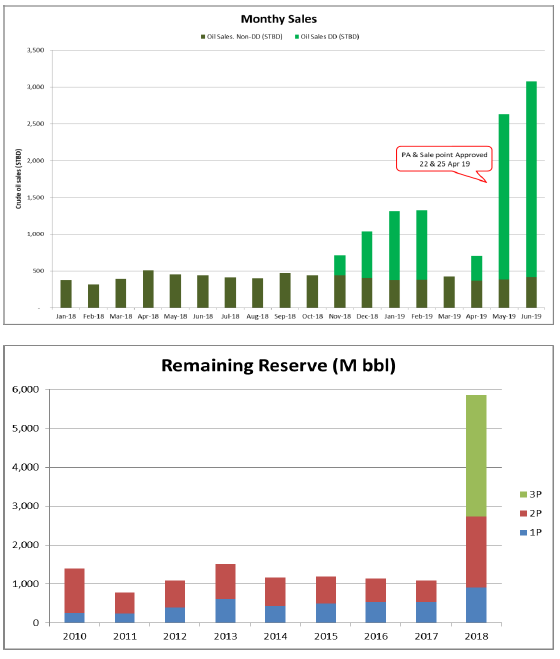

In addition, POE already has made a new discovery in Thailand in the past year. So far almost every well they drilled in the past year was a hit. The drilling cost is low, less than $1 million. The payback time is 12 months. Oil is trucked to a nearby refinery, which is eager to take domestic oil as Thailand is an oil importer. Cost is below $10 and free cash flow is strong. POE used some of the cash generated to buy back the shares from the open market.

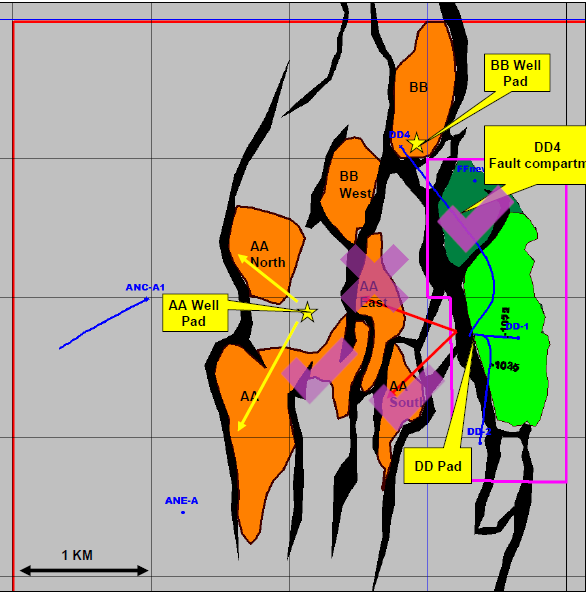

As you can see, POE experienced a dramatic rise of oil production and reserves lately. This is only the beginning. The reserve report at the end of 2018 shows it is primary composed of DD1, bright green on the map below. POE already hit DD4 dark green, AA south and AA successfully. They are planning to explore more AA, AA north and BB high-impact targets in the next two months. You can see clearly that upon successes of 2019 as well as 2020 exploration, POE can easily expand their oil reserve by many-fold and its net asset value can be worth many more times than its current share price. No wonder insiders have been busy buying shares in the past years.

In addition, POE has about 50c cash per share as of last quarter, no debt and strong free cash flow. It can potentially own 49% of one of the world’s largest discoveries in the next few months. The time has come for this potentially huge return we have been waiting for for a long time.

My family has accumulated a large position of POE stock in the past years and we are one of the largest POE shareholders, for full disclosure.

Chen Lin is a full time manager of his family assets. He started to write the stock newsletter What Is Chen Buying? What Is Chen Selling? in 2009 he after successfully navigated his family portfolio during the 2008 financial crisis. For more information on Lin, visit his website at chenpicks.com.

Disclosure: 1) Chen Lin: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Pan Orient Energy. My family accumulated a large position of POE stock in the past years and we are one of the largest POE shareholders. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Pan Orient Energy. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Pan Orient Energy, companies mentioned in this article.

Manufacturing sales rose 0.8% in August in Canada, after two consecutive monthly declines. Will the USDCAD decline?

The price chart on 1-hour timeframe shows USDCAD: H1 is in uptrend. The price is rising toward the 200-period moving average MA(200) which is falling. The RSI oscillator is falling but has not reached the oversold zone.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up Bill Holter of JSMineset.com joins me for an explosive conversation on why he is convinced there will eventually be a failure to deliver in the futures markets which will trigger a run on gold and silver… and if that happens, inventory would completely dry up and become unavailable. Holter also describes the scary amount of credit that exists in all facets of the economy and the credit crisis that could ensue due to a monetary hiccup. So be sure to stick around for my conversation with Bill Holter, coming up after this week’s market update.

Precious metals are catching some mild buying interest this week as the U.S. dollar slumps. On Thursday, the Dollar Index fell to a two-month low.

Global equity markets didn’t seem bothered. They are posting gains this week, which is limiting the appeal of gold and other safe-haven assets.

Gold prices currently come in at $1,492 per ounce, up a fraction of a percent since last Friday’s close. Silver, meanwhile, is posting a slight 0.2% decline on the week to trade at $17.60 an ounce. Silver prices have ranged around the $17.60 level for the past few weeks. A heavy commercial short position in the futures market appears to be keeping a lid on rally attempts for the time being.

Turning to platinum, prices are down 1.1% this week and currently check in at $889. And finally, high-flying palladium is up 2.9% on the week to trade at a lofty $1,756 per ounce.

Metals investors are positioning themselves for rapidly developing political and geopolitical events, as well as a rapidly expanding Federal Reserve balance sheet. What started out as a limited intervention to provide temporary liquidity to overnight lending markets has morphed into a massive $60-billion-per-month Treasury-buying campaign. By some measures, it’s even bigger than the last Quantitative Easing program.

The Fed has yet to fully explain why this is all necessary given the lack of an immediate crisis in the real economy. Last week, Fed chair Jerome Powell took great pains to insist that their expanded repo market operations are “not QE” – only to announce a massive new Treasury bill buying program on Friday.

Is there some emergency going on behind the scenes that Fed officials don’t want us to know about? It could well be that they are engineering another bailout of “too big to fail” banks on a scale they aren’t admitting.

Naturally, they don’t want to spook the markets or trigger a public backlash against an unpopular bailout program. But Powell’s QE denials are only adding to growing suspicions that the Fed is trying to fix something much bigger than a plumbing issue in the repo market.

More than a decade after the Fed initiated secret bailouts of U.S. and foreign financial institutions, we still don’t know where all that money went. Or on whose authority winners and losers were determined.

All we do know is that since 2008, trillions of dollars have been pumped directly into the banking system. And the Fed is showing no signs of stopping.

If the Federal Reserve ever became truly transparent, the public would likely be shocked at the cronyism, corruption, and outright parasitism involved in the banks’ relationship to the Fed. It would be a far bigger scandal than the corrupt crony capitalism practiced by Hunter Biden, that’s for sure.

Unfortunately, the Fed has its own lobbying arm in Congress that always finds a way to shoot down the “Audit the Fed” bill in the Senate even though it has previously passed with broad bipartisan support in the House.

President Donald Trump has called for greater transparency at the Fed and repeatedly jabbed Chairman Powell. This week, the President clashed with the foreign policy establishment over his controversial decision to withdraw military forces in northern Syria. Trump called out the “military-industrial complex” for pushing never-ending wars and occupations overseas.

Trump’s words echoed those of Dwight Eisenhower. In his farewell address, President Eisenhower, himself a military man, warned Americans of the dangers of a self-serving military-industrial complex.

President Eisenhower: In the councils of government, we must guard against the acquisition of unwarranted influence, whether sought or unsought by the military industrial complex. The potential for the disastrous rise of misplaced power exists and will persist. We must never let the weight of this combination in danger our liberties or democratic processes.

A similar warning could have been issued about the dangers of a self-serving and wholly unaccountable central banking cartel. The Fed has strayed far beyond its dual mission of pursuing stable prices and full employment. It has effectuated a massive wealth transfer into the hands of those who are first in line to receive its monetary emissions. It has artificially extended and amplified bull markets on Wall Street while diminishing the purchasing power of cash savings.

There will one day likely be another great wealth transfer – from artificially overvalued financial assets to undervalued hard assets such as gold and silver. If the Fed continues to damage its own credibility by saying one thing and doing another – growing its balance sheet QE style while insisting it’s not QE – investors may begin preferring the unassailable credibility of physical precious metals.

Well now, without further delay, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome in Bill Holter of JSMineset and the Holter-Sinclair Collaboration. Since leaving Wall Street more than a decade ago, Bill has made a name for himself as an astute and highly respected market commentator, writer and has teamed up with Jim Sinclair to help others discover the inherent dangers of our debt based economy and how to protect yourself against it.

Bill, it’s great to have you back and I very much appreciate the time today. Welcome.

Bill Holter: Thanks for having me, Mike.

Mike Gleason: Well Bill, let’s talk for a minute about what the Fed has been up to. They announced some intervention in the repo markets late last month. The program was initially sold as something very short term, there was absolutely nothing to worry about. Now that program has been extended through at least January and the Fed is seeing daily demand for short-term loans of $50 to $80 billion. Again, that’s per day. We know lying is part of the job description at the Fed. It sure seems like something serious is going on when banks start charging one another huge interest rates, or stopped doing this short term, fully collateralized lending altogether. Something is definitely rotten, but the markets aren’t really reacting. There isn’t that much talk about it in the financial press. What is your best guess about why the Fed has had to step in there with hundreds of billions of dollars? Are they bailing out Deutsche bank, another bank? What’s happening here?

Bill Holter: Well, we don’t know for sure what bank it is. Basically something has broken in the plumbing system or the background, whatever you want to call it. And the result is banks don’t trust each other. There’s demand from a bank or a group of banks that need capital overnight. The reason banks need capital overnight is because they carry positions, if you want to call it the carry trade. They carry positions overnight. They have to finance it. And what’s happened is from bank to bank, there’s a lack of confidence and banks are balking at lending to each other and there you have the rate going higher.

Mike Gleason: On top of the hundreds of billions being pumped into the repo markets, the Fed just announced another 60 billion per month in treasury notes. They haven’t come up with a clever name for this quote new program yet, but we definitely aren’t supposed to call it QE.

Bill Holter: Right, it’s not QE.

Mike Gleason: We’re told this is also just a routine preventative measure, nothing to see here. Well they can say what they want, but one thing should be clear our markets are hopelessly addicted to Fed stimulus. We’ve definitely learned that over the last several years. Quantitative tightening has failed and the Fed isn’t going to be able to normalize interest rates. The question is how goofy things will get now. They printed a few trillion dollars last time and didn’t get all that much economic growth. What will it be this time, do you think? $10 trillion in bond purchases? Will they finally resort to dropping money from helicopters as Ben Bernanke once suggested? What do you think?

Bill Holter: I have no idea what the number is going to be, but what this basically means is the real economy is not generating enough cashflow to support the financial economy and the Fed by doing QE, by shoving liquidity into the system is trying to make up for the gap that is not being created by the real economy. It shows you, I think the best way to look at it is the financial system is a patient on life support and the central banks, the Fed, the ECB, Bank of Japan, they’re all acting as life support for the financial markets, which without the central banks, the financial markets would basically just, the tents would fold up.

Mike Gleason: Has it surprised you how little response there’s been in the markets in terms of investors showing signs of worry? It’s really quite amazing to us that we haven’t seen this become a bigger story. Did you see it the same way?

Bill Holter: Yeah, I agree wholeheartedly. It’s amazing. I mean the very first day I heard that they had to do overnight repos. It raised eyebrows and then it was day after day and now it’s we’re weeks into it. It tells me something is broken and it’s shocking that nobody cares.

Mike Gleason: Thus far metals markets haven’t responded to the Feds new measures either and the prospects for even more rate cuts. We’re well below the highest put in over the summer. In fact, most of the markets that seem to have met the news of extraordinary measures with a collective shrug, as we just talked about. Stocks have moved a bit higher, 10 year bond yields are actually moving higher as well. The dollar hasn’t done much. What do you make of the market’s response? Talk about metals specifically, you would think that they would maybe be getting a little bit more of a safe haven bid. You almost have to wonder at this point what it will take to rattle investors. Are these markets so tightly controlled now that fundamentals have stopped mattering all together?

Bill Holter: I think that’s right. I think fundamentals they matter less today than at any point in the past. Yes, we should have seen a movement higher in the metals, but rallies have been met with paper. If you look at the big up days, the open interest explodes on up days and that’s not so much from the buy side. That’s the short side meeting the demand with paper as opposed to meeting it with metal.

Mike Gleason: Obviously, the metals investors have been frustrated for a long time. You see this, so you think you’re going to get some kind of a market reaction. You certainly think gold and silver should be getting more of a pop. What does that say to you in terms of the fundamentals? Obviously fundamentals may not have the impact that they once had. Eventually, will they? I mean how does the story end and how does somebody who sees all of these black swans and has so much concern about what’s going on in the financial system and their angling and positioning themselves for all of that risk, how do they benefit in the long run or do they?

Bill Holter: Well, you asked how it ends it. I’m convinced that it ends in a failure to deliver, whether it be out of COMAX or LBMA or wherever. There’s going to be a failure to deliver because there’s more demand than there is global production and the demand for years and years has been met from already mined and hoarded gold that’s leaked into the market as a salve if you will for the price. It seems to me… we’re here in North America, the little guy is burned out. The little guy for really the last year or so in North America has been a seller. There’s not been big demand and that tells me that the average retail person has just thrown up their hands and is surrendering and liquidating… everyone else is making money in the market, so I might as well put my money in the market, which is a huge mistake.

Because once the unwind really begins, it’ll be like a light switch. At some point in time I’m convinced that you’re not going to be able to source gold or silver for fiat. Now you’ll be able to trade gold for silver or silver for gold or gold and silver for something real, but I think metal is going to go into hiding and you’re not going to be able to buy it anywhere near current levels and there will be a point in time I think that you won’t be able to buy metals or source metals at all for fiat until the smoke clears.

Mike Gleason: Yeah. That’s one thing we’ve always said in the metals markets. I mean when you really look at the overall participation among the buying public throughout the world, it is such a small percentage and if we just go from say 1% ownership, whatever it is, it’s a very small fraction.

Bill Holter: I think that’s high to begin with. I think 1% is high, I think it’s under 1%.

Mike Gleason: Yeah. If we just see like a doubling of that or a tripling even in a black swan type of scenario, there’s just not that much metal out there, Bill.

Bill Holter: Right. It’s a supply and demand equation and you know, often people say, “Oh, well you can’t go to a gold standard because there’s not enough gold.” Well, that’s true at current prices, but you markup gold to $10,000, $25,000, pick a number at some number there’s enough gold and that’s where we’re headed is to wherever that clearing number is.

Mike Gleason: Certainly presidential politics are going to be a big story in the year ahead. We’ve got quite the slate of socialists running for the Democratic nomination. In normal times, you would think that the nomination of someone like Elizabeth Warren would mean limit down in the stock markets the next day, but these are hardly normal times. The only thing we can be pretty sure about is that the battle to defeat Trump is going to shift into even higher gear, if that’s even possible. Talk about some of the implications you see for the markets based on the political theater over the next 12 months?

Bill Holter: Well, obviously the next 12 months is going to be a circus. From the left, it’s nothing but impeachment and I actually watched about 10 minutes of the debate last night. It was the first one I watched and I just turned it off. I mean, you’re talking about blatant socialism, communism, whatever you want to call it, which is an abject failure. If one of the 12 that… well, let’s leave Tulsi Gabbard out of it… but if one of the remaining 11 does become president, it’s pretty much over because you’re looking at income redistribution as opposed to capital formation. We’ll go through a phase of total capital destruction as opposed to what capitalism is which is capital formation.

Mike Gleason: Do you see any real possibility that that could happen? Obviously these are fringe candidates for the most part. Usually when you get to the general election, they’ll come back to center and try to get those moderate voters to swing their way. But is it really just going to come down to the economy? People will vote with their wallets. If the economy is going to remain in a kind of similar spot that it’s in now, 12 months from now, then Trump’s probably fine, but if we go off the proverbial cliff, then he’s in trouble. Is that kind of how you’re viewing it?

Bill Holter: When President Trump back in 2017 started taking ownership of the stock market, I wrote and had done interviews saying that that was very, very dangerous. He should not take ownership of the stock market simply because within the four years I didn’t see even a possibility that it could be held together. So here we are, not quite three years, we’ve got another year to go. Yeah, I do see that as a danger. I’m also on record as saying that none of the current candidates from the left will be the eventual nominee. I think someone else is going to come in. If I had to guess, it might be Michelle Obama. That’s just a wild dart right there, but I don’t think that any of the current candidates will be the nominee.

Mike Gleason: Yeah, interesting theory. I’ve seen that elsewhere. Michael Bloomberg I know is as a name that some people have thrown around too. But yeah, it’ll be a very interesting theater for sure.

Well, Bill, before we go, I want to ask you to comment on any of the other stories you think investors need to be watching here and then also comment if you would, on whether any of the recent market reaction to everything we’ve just been talking about here today, perhaps has made you rethink your belief about the importance of owning precious metals or has it given you more conviction about that? Give us your thoughts about any or all of that as we wrap up today, if you would.

Bill Holter: Market action, well, you’re always rethinking. I mean you come to a conclusion and then you try to break your conclusion. You come at it from a hundred different angles and I’ve done that over years and years and mathematically, pure logic says that if they’re printing paper for free, it doesn’t have any value. And if they’re digging gold and silver up out of the ground and it takes capital, labor and equipment to do that, it has value. My premise for years now has been this is a credit problem. It’s a credit bubble that has been created over, well literally over my lifetime since 1960 say. The world runs on credit and I actually started writing a short article, What if Everyone’s Credit is Ruined. And that’s what I think is going to happen.

I think you’re going to see a credit event where credit basically ceases because you have distrust from counterparty to counterparty and you get a disruption in credit and then our everyday life is disrupted. I’ve said this probably, gosh, I don’t know, 50 or a hundred times in interviews and articles that if there’s an interruption in credit, you’re going to go to Walmart and find that if it is open, there’s nothing on the shelves because there’s not little elves in the back room that make loaves of bread or shoes or whatever. For a loaf of bread, there’s like seven or eight uses of credit from the wheat field to the shelf. And if any of those instances of credit get shut off, the loaf of bread doesn’t make it to the store. So, I think that’s the most significant thing that people just don’t think about it because your everyday life, “Oh, well I need this, or I need that. I’ll go down to my store or go online and order it, whatever.” But shipping, trucking, distribution, all of that, will stop with a credit implosion and that’s where mathematically we’re headed.

Mike Gleason: Yeah. And at the end of the day, if you look at precious metals, it is like a form of insurance more so than it is an investment per se.

Bill Holter: Well, they’re not credit, gold and silver are no one’s liability. They’re not a promise. Everything else is a promise. Gold and silver are merely proof that capital, labor and equipment have already been expended, so they’re pure assets. They’re pure money.

Mike Gleason: Yeah, that’s a great way of summarizing that, very, very well stated. Well Bill thanks so much for your time, enjoyed visiting with you and I certainly hope we can do it again before much longer, great insights as usual from you and we appreciate the time. Thanks for coming on and all the best to you.

Bill Holter: Appreciate it. Thanks Mike.

Mike Gleason: Well, that will do it for this week. Thanks again to Bill Holter. The site is JSmineset.com, be sure to check out all the great commentary that Bill and Jim put out there on a regular basis. Again, JSmineset.com.

And check back next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange. thanks for listening and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

After three and a half years of chronic uncertainty, drama and constant toeing and froing, the Brexit saga is reaching a critical turning point.

In a positive development, Boris Johnson has agreed on a Brexit deal with the European Union. However, it is far too early for any celebrations given how the deal will need to be approved by the House of Commons on Saturday. While the revised agreement has many similarities with the one agreed by Theresa May, the major difference lies in the proposal on Northern Island. The new Brexit deal simply replaces the Irish backstop plan with a new arrangement where the North will continue to follow EU regulations on goods after Brexit.

With Northern Ireland’s DUP already refusing to support Boris Johnson’s deal, investors should brace for another showdown in Westminster on Saturday. Although EU leaders have left the doors open for a Brexit extension beyond October 31st if Johnson’s plan is rejected by the commons, this is simply kicking the can further down the road.

If Boris Johnson’s deal is given the thumbs up by the House of Parliament this weekend, it will be a major relief for the British pound as fears of a no-deal Brexit completely fade. This welcome development should push the GBPUSD well above 1.30 towards 1.318. Alternatively, if Johnson’s deal fails to pass through parliament, the Pound is seen sinking back towards 1.27 as uncertainty makes an unwelcome return.

Will the Brexit saga come to end on Saturday? Or will this be the start of another drama-filled season? This is the question on the mind of many investors.

Whatever the outcome of ‘Super Saturday’s’ Brexit showdown, it will certainly have a profound impact on Sterling.

Gold waits for fresh catalyst

Gold is finding comfort within a $20 trading range as investors remain cautiously optimistic over the United States and China finalizing a “phase one” trade agreement.

Given how high-level trade talks between both sides will resume next week, Gold is positioned to remain range-bound until a fresh directional catalyst is brought into the picture. A sense of optimism surrounding the current Brexit developments is also impacting appetite for the safe-haven metal with prices trading around $1491 as of writing. Although a softer Dollar could provide Gold bulls with some support, the real action may not be seen until next week following the outcome of ‘Super Saturdays’ showdown and trade talks.

Focusing on the technical picture, Gold remains range-bound with support around $1480 and resistance at $1500. A breakout above $1500 should encourage a move higher towards $1515. Should prices secure a weekly close below $1480, Gold is likely to sink towards $1465.

Commodity spotlight – WTI Oil

Oil prices are pushing higher despite China’s economic growth slowing to 6% during the third quarter of 2019.

Given how China is the world’s largest energy consumer, signs of slowing economic growth from the nation could ignite fears of a drop in demand for crude oil. Regardless of recent gains, Oil markets remain heavily influenced by demand side factors revolving around trade uncertainty and global growth fears. If the United States and China officially sign a “phase one” trade agreement, Oil prices have scope to push higher as trade tensions ease.

Focusing on the technical picture, WTI Oil is trading above $54 on the daily charts. A weekly close above this level should encourage an incline towards $55.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

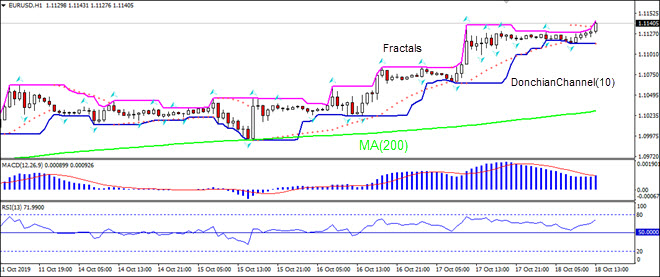

Euro-zone current account surplus rise bullish for EURUSD

Euro-zone current account surplus rose to €27 billion from €22 billion in July. Will the EURUSD rise?

The price chart on 1-hour timeframe shows EURUSD: H1 is trading sideways. The price is above the 200-period moving average MA(200) which is rising. And the RSI is above 50 level and has not reached the overbought zone. There is no trend yet formed, traders have to decide when it would be a best time to enter the market.

Our research team believes the US Treasuries and the US Dollar will continue to strengthen over the next 2 to 6+ weeks as foreign market and emerging market credit and debt concerns outweigh any concerns originating from the US economy or political theater. Overall, the major global economies will likely continue to see strength related to their currencies and debt instruments simply because the foreign market and emerging markets are dramatically more fragile than the more mature major global economies.

We believe the US Treasuries may surprise investors by rallying from current levels, near price resistance, to levels above $151 on the TLT chart.

Our belief is that further economic concerns related to trade, foreign economic metrics and data and the forward perspective of many emerging and foreign markets will continue to weaken much more dramatically than the US or other major global economies. Thus, we believe capital will continue to pour into the US and more mature major global economic markets (Canada, Japan, Great Britain, Swiss) as a move to safety just as capital is moving into the precious metals markets.

When fear enters the global markets, capital seeks out the safest and most secure environments for investment. If the rest of the world’s economies are becoming weaker and more fragile as trade and economic factors continue to hit the news wires, the more mature major economic countries are naturally going to benefit from their more robust and secure economic power and strength. The flight to safety will result in capital moving away from risk and into the safety of these more mature economies simply because they provide a level of security and risk aversion that can’t be found elsewhere. Make sure to opt-in to our free market trend signals newsletter.

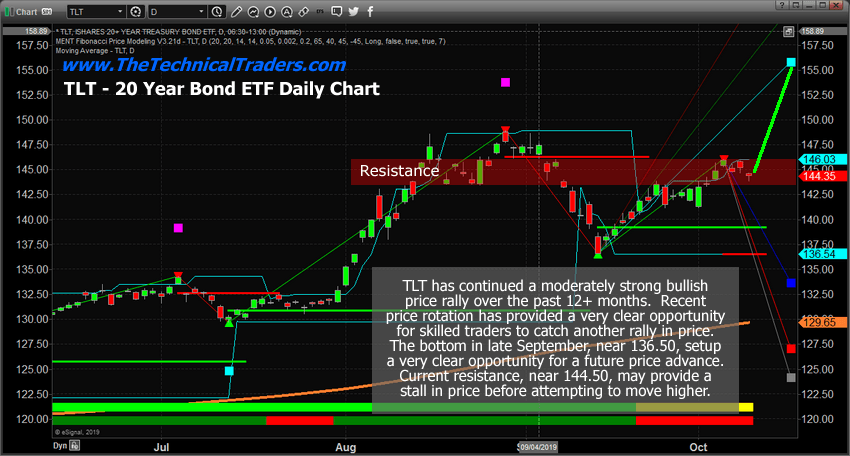

Daily TLT Chart

This Daily TLT chart highlights the resistance level that we believe is current constricting the current price advance from breaking higher. We believe this resistance channel is causing the TLT price to pause below $147 and will continue to keep prices within this channel until some economic news event or positive US economic news item pushes the price higher. The US and global markets are waiting for some type of news event before attempting to make another move. We believe the future news will result in an upside technical breakout and a new rally towards the $152 to $155 level in TLT.

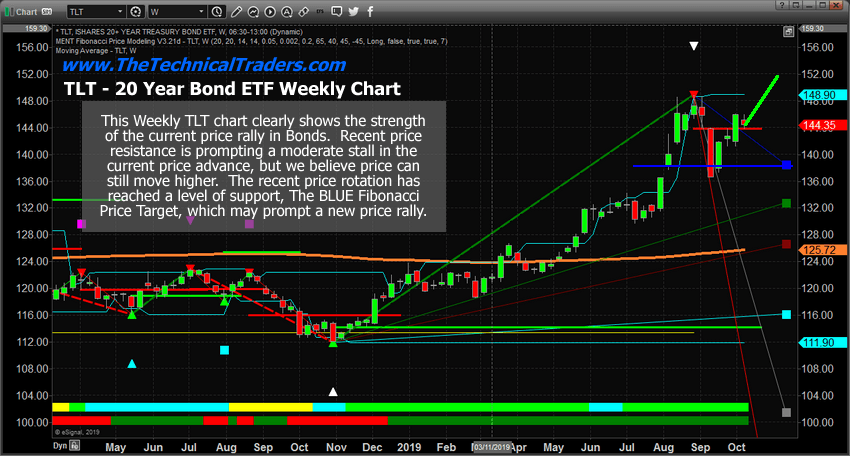

Weekly TLT Chart

This Weekly TLT chart highlights the extended bullish price rally that started back in late October 2018. This upside price move has already rallied more than 40%, but we don’t believe it is over yet. Our Fibonacci price modeling system is suggesting $154 to $155 is the next upside price target. To be a bit more conservative, we’ve targeted the $152 level for skilled traders to work with. Once price achieves the $152 target level, look to cover any open long trades you may have.

If you are an active trader of gold, gold stocks, bonds, or the SP500 and would like to hear a trading style that reduces the amount of trades you take while making the same or better returns listen to this conversion with Adam Johnson who is an x-Bloomberg anchor, and now active trader.

Understanding how pricing and global market dynamics work throughout the stock market and the global market can be confusing at times. How can one attempt to understand what will move in a certain direction, why it will move that way and how one can profit from these opportunities and be difficult for many people to grasp. We do our best to try to help you by highlighting trade setups, explaining our thinking and research, sharing some of the charts with our proprietary trading tools and to help you identify strong opportunities for success.

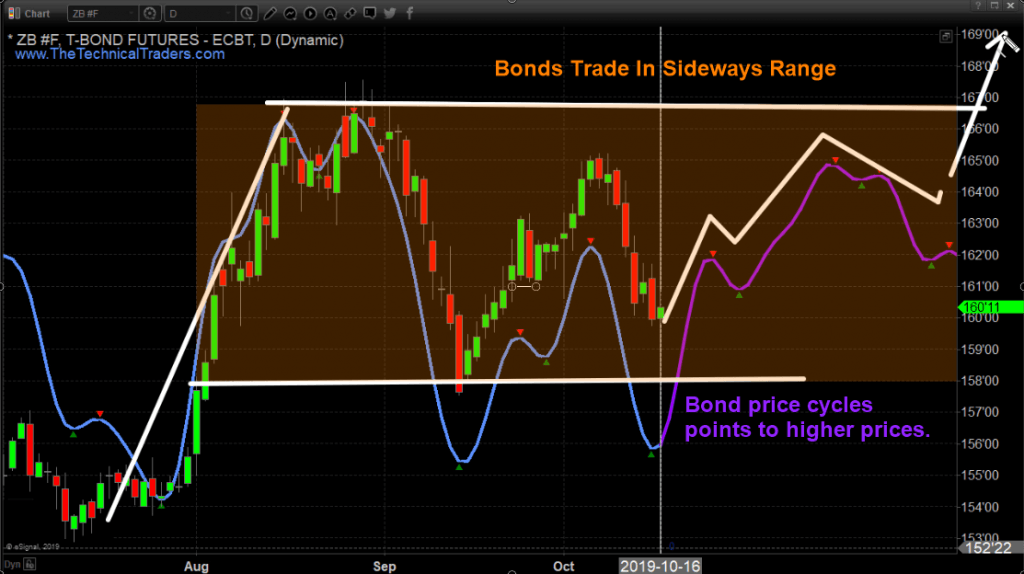

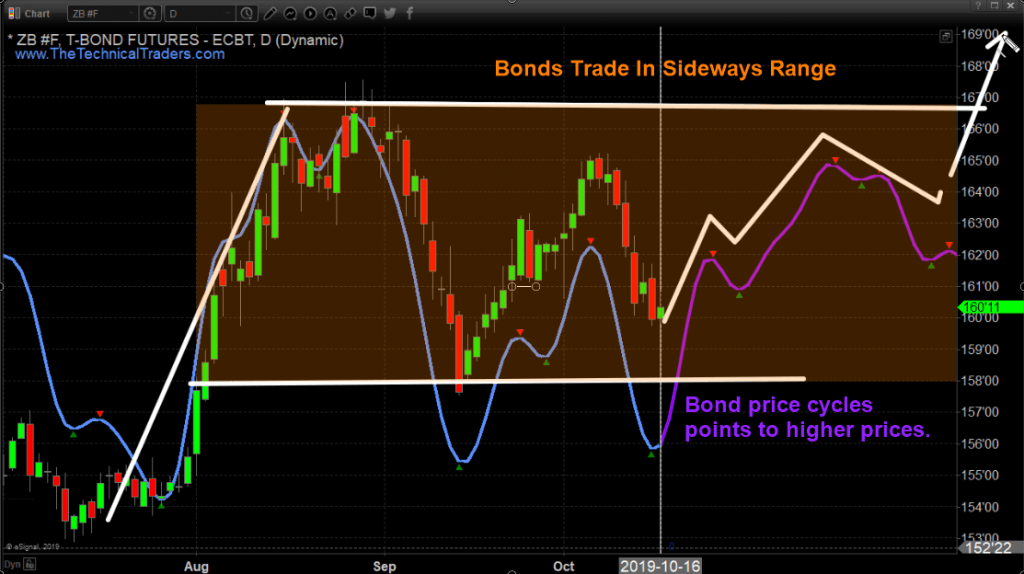

Bonds are likely to continue to trade in a sideways price range before breaking higher near the end of 2019. This aligns with our expectations that foreign markets may come under intense economic pressure while the US economy continues to provide safety for investors for the long term. The support level above 157 is critical going forward.

Daily Price Cycle Predicted Price Trend

While cycle analysis helps us paint a clear picture of what to expect looking forward up to 45 days I still rely on my market trend charts to know when I should be buying or selling positions.

The Technical Traders Concluding Thoughts:

Right now, we believe the markets are waiting for some news events to make their next move. This is the time to take very measured positions when trading. This is NOT the time to go “all-in” on some trade. Be prepared for a spike in volatility and a new price trend to establish within the next 3 to 10 trading days.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

I urge you visit my ETF Wealth Building Newsletter and if you like what I offer, join me with the 1-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next financial crisis. Join Today to Get a Free 1oz Silver Bar with a subscription – Offer Ends This Week!

Today I want to talk to you about the SP500 because it’s on the verge of making a very significant move. We could experience a 15% rally or a 15% decline and it could be just around the corner.

Let me recap on both the short-term top this month, and then a look at the bigger picture of what happened last October through December and if we are going to see that happen again. There is the possibility we get a massive rally if the market breaks to new highs. The market is loaded and ready for action. Whichever way it breaks will have a strong impact on precious metals and bonds. Make sure to opt-in to our free market trend signals newsletter.

21 Days Then A Breakdown?

Let’s look at the SP500 for the last 6 months in the chart below. If we were to just draw support trendlines across the lows and a resistance trend line across the highs, you can see we still have some room for the SP500 to work itself higher and still be within the pattern.

Do you see the blue line that is on the chart? You will notice it follows price very closely and you’ll notice the purple line on the hard-right edge as well. This purple line is the forecasted projected cycle price that we are anticipating for the SP500 over the next 45 days.

I should note that as the market evolves and moves this price cycle forecast will change, but it gives us a good idea of current cycles in the market and where the price should go next.

Overall, we’re all you’re looking for SP500 to struggle to move higher because it acts as resistance. If resistance holds then it is likely the market breaks down and tests the August or September Low.

S&P 500 October – December Market Crash to Repeat?

Let’s step back and look at last year’s price action. You can see that the cycle analysis is pointing to potentially another market crash down to those December low. If that is the case then it could be the start of something very significant like a new bear market.

So that’s where we’re at in terms of the SP500 and at this point, we’ve got another 21 days or so before the SP500 should start breaking below our white trendline support level.

While cycle analysis helps us paint a clear picture of what to expect looking forward up to 45 days I still rely on my market trend charts to know when I should be buying or selling positions.

Bonds – The Natural Investor Safe Haven

The first safe haven investors flock to when they become scared are bonds. By looking at the chart we can see they should start to find a bottom based on our cycles. Bond prices are stuck within a large sideways channel and should hold their ground until the SP500 starts collapse. If the SP500 breaks down then we’re going to see bonds move higher and should eventually break out and make new highs.

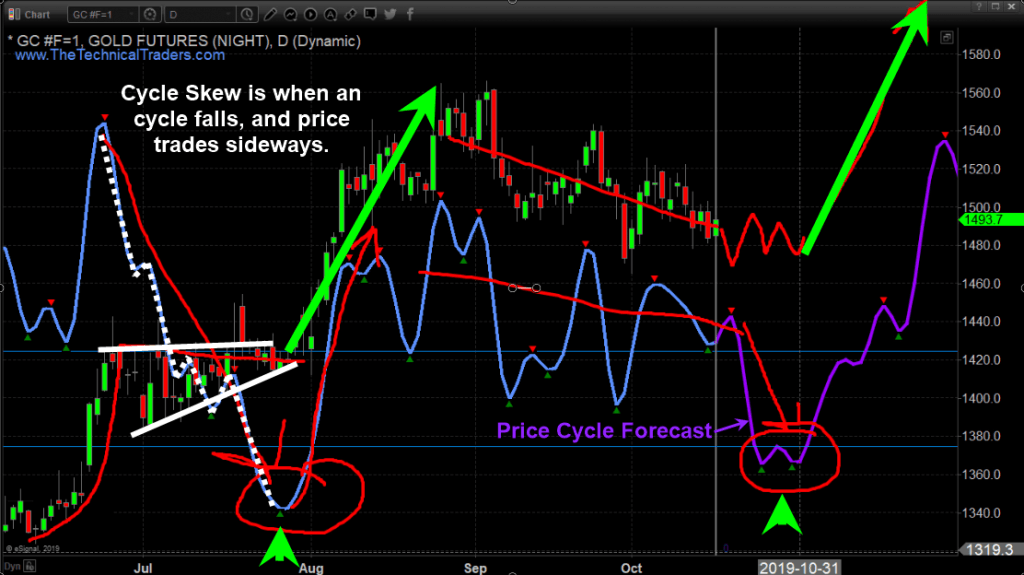

Gold – The Safest of Safe Havens

The true safe Haven is gold when it comes to a global store of value for all countries and individuals.

Take a look at the price of gold, as you can see it rallied in June and again in August when the cycles bottomed and started an uptrend. Right now the price is in a much larger consolidation (bull flag pattern) which is a positive sign. In fact, this multi-month pause makes gold even more bullish in my opinion. The longer a commodity trades sideway the more powerful the next move will be.

You can see based on our cycles analysis and forecasted price gold still has some potential weakness for a couple of weeks.

Understanding cycles and how to trade with them is much harder than most people think. If you do not understand cycle skew then you will struggle to turn a profit. I have been trading with cycles since 2001 and still, I find them very deceiving at times.

In laymen terms, cycle skew is when a cycle moves against the direction of the underlying asset’s trend. The chart below shows this clearly with the white lines. In short, gold is in an uptrend, and when the cycle moves down against the assets trend price will in most cases trade sideways. Do not try to short cycle tops when the trend is up, no matter how tempting it may be.

The key is to wait for cycles to bottom, then get back into position for the next upward move in the cycle and price.

I had a fantastic chat with Adam Johnson from BullsEyeBrief today and if you are interested in more juicy details on the SP500, Gold, and how I trades be sure to listen to the most recent podcast we did together at the top of his website https://bullseyebrief.com/podcast/

The Technical Traders Thoughts:

In short, the stock market continues to keep the bull market alive, but investors have started to move into gold as a safe haven. The fear of a market downturn is growing which is why gold has rallied and started a new bull market. The money flow into gold is very strong and is warning us that US equities could enter a bear market in the next few months and that possibly something much larger globally could be at play as well.

Gold continues to just hold up well even with the current cycle forecast trending lower. Overall, we’re looking at about 20 days or so and we could see metals and equity prices make some incredible moves.

Keep reading our research because our proprietary tools have been nailing all of these price targets and move many months in advance. The next bottom in metals should set up when our cycle bottoms – then the next upside leg will begin. This time Gold should target $1800 and Silver should target $21 to $24. This will be an incredible move higher if it plays out as we suspect.