Despite trade wars and geopolitics, Chinese economic growth shows resilience. So why is there a deep gap between the third-quarter data and gloomy international headlines?

After the release of third-quarter data, The Wall Street Journal headline sounded a warning: “China’s economic growth slowest in decades.” CNN seconded: “China’s economic growth drops to lowest level since 1992.” Reuters extended the timeline: “China’s GDP growth grinds to near 30-year low as tariffs hit production.”

The fallacy in these headlines is that they mistake business cycles for secular trends and vice versa. When countries industrialize, they enjoy relatively high growth. After industrialization, growth rates decelerate. China is no exception.

In reality, much of recent quarterly data in China and other major economies has been penalized for the same reason – the US-launched trade wars and geopolitics, which foster diminished global economic prospects.

Only 0.1% behind quarterly expectations

In secular terms, China’s economic growth has been gradually decelerating since the early 2010s, as it should after years of high-growth industrialization. Yet, per capita incomes will almost double in the ongoing decade. In other words, economic growth is decelerating, but living standards continue to rise.

That’s very different from major advanced economies in which economic prospects continue to stagnate, in both secular and cyclical terms.

In the United States, the living standards of middle-class and working people have lingered since the 1980s contributing to steep income polarization. In the eurozone, polarization is not as bad yet, but it is deepening. In contrast, China’s middle-income groups continue to expand.

In terms of cyclical data, China’s economic growth slowed to 6.0 percent from 6.2 percent in the second quarter. But seriously, how much did the actual result differ from the expected one? Analysts polled by Reuters had forecast GDP to grow 6.1 percent in the July-September quarter from a year earlier. So the difference was a mere 0.1 percent.

So why the hullabaloo? Such a slight deviation does not warrant panicky headlines. Nor do such reports provide appropriate guidance to US investors.

Unlike the media, institutional investors see economic resilience in China, even amid trade wars and geopolitical pressures. That’s why almost half of fixed income institutional investors outside China plan to increase their exposure to China-issued debt in the coming year, according to FinanceAsia.

Cyclical resilience, secular potential

On the Chinese mainland, positive signs include growth in industrial production, which picked up in September, despite reduced export growth. And while months of trade wars have made consumers more cost-conscious, retail sales climbed to 7.8 percent, thanks to state council’s slate of policy supports. The latter are warranted because wage growth remains restrained.

Property prices have stayed relatively strong, which has left a substantial burden on households’ shoulders. Since household debt to disposable income climbed to nearly 140 percent in 2018, household spending will be more cautious, as evidenced by lingering car sales. Yet, the big picture is more nuanced. For instance, education and medical expenditures remain solid.

Indeed, China’s secular potential remains strong. The growth rate is still three-to-four times faster than in major advanced economies. The rebalancing of the Chinese economy toward innovation and consumption remains on track. And while the contribution of investment rose to 19.8 percent of the GDP, that of consumption climbed to 60.5 percent.

The International Monetary Fund has projected China’s GDP growth to slow to 5.8 percent by 2020. That scenario presumes weakened consumption, coupled with cautious private investment and shrinking exports. But the final figure may be more likely to hover around 5.8-6.2 percent in 2020, depending on the severity of the headwinds in trade – which will result in further fiscal and monetary accommodation and thus slower deleveraging.

It is not the policy the Chinese authorities would normally prefer, but we do not live in normal times.

Policy mistakes and global uncertainty

When the Trump administration adopted a protectionist trade policy some two years ago, it not only committed the worst US policy mistake in the postwar era but also undermined the nascent global recovery.

Before the US launched the trade war against China, its annual GDP growth rate peaked at 3.2 percent in mid-2018. Now it has almost halved to 1.8 percent. As for the eurozone, after a peak at 3 percent in January 2018, its growth has tumbled to about 1 percent; even before Germany’s economic uncertainties over Brexit. In Japan, too, growth has plunged to below 1 percent after climbing to 2.4 percent in early 2018.

In 2017, global economic growth was as high as 3.8 percent. Given the right policies, it might have exceeded 4 percent in 2018 and this year. Instead, thanks to US trade protectionism and geopolitical friction, global integration has stalled. World trade is at pre-2008 levels, and the same goes for world investment. As migration flows have plunged, the number of globally displaced exceeds 71 million;15 million more than at the end of World War II.

If misguided policies are permitted to prevail, these adverse trends are likely to further intensify, compounded by potential impeachment divisions in the US, recessionary landscape in the eurozone and stagnation in Japan.

Guided by US policy mistakes, the global economy is now amid a “synchronized slowdown,” as the IMF has warned. But there is much worse ahead, if these mistakes are permitted to prevail.

About the Author:

Dr. Dan Steinbock is the founder of Difference Group and has served at the India, China and America Institute (US), Shanghai Institute for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

The original version was released by China Daily, China’s leading English-language daily, on October 25, 2019

Asian stocks are taking their cues from the mixed close in US stocks, with the S&P 500 just 16 points or 0.5 percent away from a new all-time record close. The ongoing earnings season has given equities another leg up , even as global uncertainties persist. Despite some bellwether companies missing estimates, many of the reported results show US companies faring better than expected amidst global trade tensions and the downward pressures on the world’s economy. However, noting that the downside risks are still on the table, markets may not be fully comfortable with diving head first into riskier assets, until there is greater certainty surrounding the US-China trade conflict and Brexit.

UK election adds to political risks surrounding Sterling

GBPUSD dipped below 1.28 before paring losses but is still currently weaker against most G10 and Asian currencies. Although the October 31 deadline is set to be a mere footnote in this longstanding Brexit saga, the Pound will remain sensitive to any political developments either out of Westminster or Brussels.

Given calls for a UK election, this adds another layer of political risk to Sterling’s outlook. Since surging about 6.5 percent to breach the 1.30 level, GBPUSD has moderated as markets question the justification for keeping the Pound elevated. Still, at least investors can draw relief from the diminished chances of a no-deal Brexit, which puts a sturdier floor below the Pound.

Policy continuity, economic pressures muddy Euro outlook

EURUSD is hovering just above the 1.11 psychological level, after the European Central Bank decided to keep its policy settings unchanged at Mario Draghi’s final meeting at the helm. With new President Lagarde taking up the reigns next Friday, policy continuity is set to frame investors’ outlook at the central bank, with the Eurozone economy still contending with subdued economic growth.

Germany’s manufacturing slump, as evidenced further by yesterday’s IHS Markit manufacturing PMI, continues to be a drag on the EU economy. Unless policymakers step in with substantial fiscal stimulus measures, barring a rapid dissipation of external headwinds, the outlook for the economy and the bloc’s currency remains tilted to the downside.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stocks ended mixed on Thursday as corporate reports and data painted mixed picture of the health of US economy. The S&P 500 gained 0.2% to 3010.29. The Dow Jones industrial average however slipped 0.1% to 26805.53 dragged by 4.1% drop in 3M as it cut its full year guidance. Nasdaq composite index rose 0.8% to 8185.80. The dollar weakening reversed as data showed initial jobless claims fell while both new home construction and durable goods orders fell in September. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 97.65 but is lower currently. Stock index futures point to mixed openings today.

FTSE 100 still ahead of European indexes

European stock market gains broadened on Thursday as the European Central Bank didn’t change interest rates in the last meeting with Mario Draghi as president. Both GBP/USD and EUR/USD turned lower yesterday and are little changed currently. The Stoxx Europe 600 index ended 0.6% higher led by auto shares. Germany’s DAX 30 gained 0.58% to 12872.10 despite the services PMI falling to a 37-month low. France’s CAC 40 added 0.55% and UK’s FTSE 100 rose 0.9% to 7328.25 as Prime Minister Boris Johnson said he would seek a general election in December to break the Brexit impasse.

Australia’s All Ordinaries Index leads Asian indexes gains

Asian stock indices are mixed today. Nikkei rose 0.2% to 22799.81 as yen resumed its slide against the dollar. Chinese stocks are mixed: the Shanghai Composite Index is up 0.5% and Hong Kong’s Hang Seng Index is 0.3% lower. Australia’s All Ordinaries Index doubled gains to 0.6% despite resumed Australian dollar climb against the greenback.

Brent futures prices are edging higher today. Prices gained yesterday on reports Iraq and Nigeria, two of the most non-compliant OPEC producers, have reduced their production. December Brent crude added 0.8% to $61.67 a barrel on Thursday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The results and commercial potential of the therapeutic are discussed in an H.C. Wainwright & Co. report.

In an Oct. 22 research note, H.C. Wainwright & Co. analyst Andrew Fein reported that the “remarkable HER2CLIMB topline positions Seattle Genetics Inc. (SGEN:NASDAQ) as a strong player in the breast cancer space.” Accordingly, the investment bank increased its target price on the biotech to $140 per share. In comparison, the current share price is about $100.89.

HER2CLIMB is a Phase 3 study evaluating tucatinib plus trastuzumab plus capecitabine against trastuzumab plus capecitabine in thirdline HER2-positive breast cancer patients.

Regarding the recently released topline results, Fein commented, “We are impressed by the remarkable survival benefits in the overall patient population, with a 46% risk reduction of disease progression or death (p<0.00001), as well as a 34% risk reduction of death (p=0.0048).” The results were even greater among patients with brain metastasis; 52% showed reduction of risk for disease progression or passed away (p<0.00001).

Fein pointed out that “the differentiating value of tucatinib suggests a strong commercial outlook in the competitive HER2+ breast cancer landscape,” particularly in the subpopulation of patients with brain metastasis, where the need is the greatest. Unlike antibody-based treatments, tucatinib penetrates the brain, making it ideal for use as a complement to those therapies rather than a direct competitor. Also, tucatinib does not bind to the EGFR receptor and as such, has as better safety profile.

With respect to another tucatinib clinical trial, HER2CLIMB-2, for which the dosing of patients began earlier in October, H.C. Wainwright believes topline data from it will also be a “win,” noted Fein.

This Phase 3 study is evaluating tucatinib plus ado-trastuzumab emtansine, or T-DM1, in HER2-positive breast cancer patients. “We point that tucatinib may be used in an off-label setting for brain metastasis patients ahead of the study readout, due to highly unmet medical need and the superior activity of tucatinib in this patient population,” the analyst added.

H.C. Wainwright has a Buy rating on Seattle Genetics.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from H.C. Wainwright & Co., Seattle Genetics Inc., Initiating Coverage, October 22, 2019

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Andrew S. Fein, Alicia Yin, Ph.D., and Matthew Caufield, certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analyst’s household has a financial interest in the securities of Blueprint Medicines Corporation, Deciphera Pharmaceuticals, Inc. and Turning Point Therapeutics, Inc. (including, without limitation, any option, right, warrant, future, long or short position).

As of September 30, 2019 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of Seattle Genetics Inc.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The Firm or its affiliates did not receive compensation from Seattle Genetics Inc. for investment banking services within twelve months before, but will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

The Firm does not make a market in Seattle Genetics Inc. as of the date of this research report.

H.C. Wainwright & Co., LLC and its affiliates, officers, directors, and employees, excluding its analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research report.

This morning shares of Boston Scientific traded 6% higher after the firm reported a 13.1% increase in revenue for Q3/19. The firm also raised its revenue guidance for both Q4/19 and FY/19.

Early this morning medical device maker Boston Scientific Corp. (BSX:NYSE)announced third quarter earnings results for the period ending September 30, 2019. In the report the company indicated that it achieved sales of $2.707 billion during Q3/19 which represents growth of 13.1% on a reported basis when compared to Q3/18. The company further reported GAAP earnings of $126 million or $0.09 per share in Q3/19, compared to GAAP earnings of $432 million or $0.31 per share in Q3/18 with adjusted earnings per share of $0.39 in Q3/19 compared to $0.35 in Q3/18. The firm advised that Q3/19 GAAP earnings of $0.09 per share compared to its previous guidance range of $0.23 to $0.25 per share was due to acquisition related charges in Q3/19 primarily associated with the acquisition of BTG plc.

Boston Scientific’s Chairman and CEO Mike Mahoney commented, “Our third quarter results reflect accelerated growth fueled by several key product launches, excellent regional performance and the broad strength of our core portfolio, and we continue to invest in building a robust pipeline…I am proud of our global teams across Boston Scientific who continue to bring forward new clinical solutions that advance science and help improve patient lives.”

The company indicated that in Q3/19 it achieved revenue growth in all segments compared to Q3/18. Specifically, the MedSurg segment increased 13.2%, Rhythm and Neuro was up 5.4%, and Cardiovascular increased 11.3%. By region, sales in the U.S. increased by 10.6%, Europe, Middle East and Africa was up 6.3%, Asia-Pacific increased 13.8% and Emerging Markets were up 16.1% in the same corresponding period.

The company pointed out that in the quarter it “commenced launch of the WATCHMAN Left Atrial Appendage Closure Device in Japan upon securing positive local reimbursement; surpassed 100,000 patient implants worldwide…the WATCHMAN device is an affordable stroke risk reduction strategy for Medicare and Medicare beneficiaries compared to warfarin.”

In the report the company also adjusted its forward guidance for Q4/19 and FY/19. The company now “estimates revenue growth for Q4/19, versus Q4/18, to be in a range of approximately 13-15% on a reported basis and a growth range of approximately 8-9% on an organic basis. The company estimates earnings on a GAAP basis in a range of $0.22-0.25/share and adjusted earnings, excluding certain charges (credits), in a range of $0.42-0.45/share…The firm estimates revenue growth for the FY/19, versus FY/18, to be in a range of approximately 9-9.5% on a reported basis (compared to prior guidance of 7-8%), and to be approximately 7.5% on an organic basis (compared to prior guidance of 7-8%). The company now estimates income on a GAAP basis in a range of $0.72-0.75/share (compared to prior guidance of $0.94-0.98/share) and estimates adjusted earnings, excluding certain charges (credits), in a range of $1.55-1.58/share (compared to prior guidance of $1.54-1.58/share).”

Boston Scientific is based in Marlborough, Mass., and is a developer, manufacturer and marketer of medical devices used in a range of interventional medical specialties. The firm offers products used in the areas of Interventional Cardiology, Cardiac Rhythm Management, Endoscopy, Peripheral Interventions, Urology and Pelvic Health, Neuromodulation, and Electrophysiology.

Boston Scientific has a market cap of about $53.2 billion with approximately 1.393 billion shares outstanding. BSX shares opened higher today at $40.75 (+2.57, +6.73%) over yesterday $38.18 closing price. The stock has traded between $39.77 to $41.24 per share today and currently is trading at $40.62 (+$2.44, +6.39%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

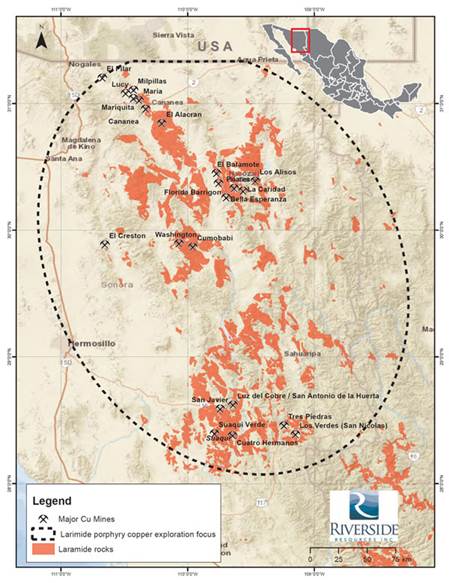

John-Mark Staude, president and CEO of Riverside Resources, speaks with Maurice Jackson of Proven and Probable about his company’s strategic funding agreement with BHP to explore the Laramide copper belt of Sonora.

John-Mark S.: It’s excellent. For Riverside, it provides at least two years and maybe more of full funding by BHP of over $1 million a year to generate new projects. Then, as we generate new projects, every additional project we do gets a half-a-million-dollar technical work program as well. On top of that, it’s over $5 million of spending by BHP for them to earn into a 70% interest. So what we’re doing is we’re allowing for BHP to earn into projects, but what’s really great for Riverside is we have that funding to go forward and explore in Sonora, Mexico. It’s a real win-win type of strategic program we’re doing with BHP.

Maurice Jackson: Sticking with BHP, are there any updates that you can provide for shareholders since the signing of this agreement?

John-Mark S.: The Strategic Funding Agreement is focused in Sonora, Mexico. The area of focus is in orange on the map above, called the Laramide. The Laramide rocks are the right age rocks for copper. These are some of the centralized areas that have copper mining, big mines, and copper operations. What we’ve been doing in the last six months is developing our own projects along the following belts: the Cananea, Caridal Suaqui Verde, Suaqui Grande, other areas. We’ve now been able to update the shareholders that Riverside has been able to get targets going forward. We’re excited to be working in these mineralized areas and finding new targets that we will be able to, in the next six months, have news flow from the acquisition, and then further follow up towards drilling of these different targets for copper. We really like this region and we’re very excited to have BHP funding our program here.

Maurice Jackson: Looking forward, John-Mark, what is the next unanswered question that Riverside Resources will be answering for the market regarding its work with BHP? And you alluded to six months is the next time we should hear a response, but what will determine success?

John-Mark S.: So first off, we will hear, even before six months, the new acquisition of properties. News releases about that are pending. Secondly, high-value work programs. Those are those $500,000 additional funding programs that we’re doing with BHP. In the next three months, we expect to have a couple of those coming forward. So that’s good.

What will be success? First, is BHP funding it, and secondly, will be the results coming out of that. We know this is a prolific belt. In particular in the region near Arizona, there are over 17 major copper mines. Yet, in Mexico, there are only six. We think this shows a great potential for finding of more. So what will be successful will be us acquiring properties, us moving those forward, and eventually with us drilling. Drill discoveries, we’ve heard about them just up here in the north with big transactions and big deals out of Tucson, Arizona, which just to the north of us, really leaves us feeling that there’s a great potential here in Sonora, Mexico. So we’re delighted now to be moving forward with those different target areas with BHP.

Maurice Jackson: Moving on to the remaining project portfolio, the property bank has expanded quite considerably this year. Please provide an overview of the property acquisitions for this year.

John-Mark S.: Riverside has been quite active this year. We have expanded our property bank in Mexico and Canada. Beginning with Mexico is the Cecilia Project; we also added have Los Cuarentas. And what we have in these projects in this area of Sonora is gold near the surface, very good. One of the things we’ve had in news flow at Los Cuarentas was the fact that we’d had the work next to us, Santa Gertrudis Mine, Premier Gold Mines, Santa Elena, the development of that by First Majestic, and even the Silver Crest. So right in the middle of the map is where Riverside’s been able to go and is diversifying our portfolio, so we’re very excited by that. Surrounded by other projects as well. Makes the Sonora State great for Riverside.

Maurice Jackson: John-Mark, take us to Canada and share with us the project portfolio expansion there.

John-Mark S.: Riverside during this year has been expanding into Canada. We’ve been working in the province of Ontario because it’s one of the major gold-producing provinces in the country of Canada. Ontario produces over 43% of all the gold in Canada. The gold deposits come from a belt, which is sheer-zone gold, as we have at our Oakes Project and further to the west at our Longrose Project. Both of these are part of the Geraldton Beardmore gold belt.

This is a prolific gold belt with over 8 million ounces of resources and past production. And we see good potential at Oakes. We’ll have news flow coming in the next three months from Oakes, from the sampling and field work, and also with Longrose, where we have shear-zone gold near to the old Beardmore mine. Beardmore mine produced over a million ounces at one ounce per ton, a nice high-grade operation at Beardmore. So we like these high-grade near-surface gold projects; they are excellent additions for Riverside’s portfolio.

Maurice Jackson: Dr. Staude, when can shareholders expect to hear the next press release regarding one or more of the aforementioned projects?

John-Mark S.: In the next four weeks, we’ll actually have news. We’re working on getting the final results put together, and we’ll look forward to keeping the updating of the shareholders. Very excited about us moving into November. It’ll be a really good time with news flow from Riverside.

Maurice Jackson: Switching gears, John-Mark, please share the current capital structure of Riverside Resources.

John-Mark S.: Riverside continues to have a tight share structure with 63 million shares out, a good cash position of over $2.5 million cash, and no debt. Additionally, our $1 million a year coming in from BHP helps us to keep that burn rate low as we continue to grow the portfolio and work with joint venture partners.

Maurice Jackson: Sir, when was the last time you purchased shares, and at what price?

John-Mark S.: Actually, I’m purchasing shares right now at 15 cents. It’s a low price for us, and so I’m delighted to be able to pick up shares here. It’s a wonderful time. And with the news out, I can do that now. We’ve been in a bit of a hold period with this news, wanted to get it out. And now we can buy more shares of Riverside.

Maurice Jackson: In closing, sir, what keeps you up at night that we don’t know about?

John-Mark S.: Really the speed. Riverside wants to get news out there and we’re pushing hard. Also, the access to capital for partners. It’s just really difficult right now for other people. Riverside’s in a good position with cash, good position with no debt, but other companies. Those are the two things that we’re working very hard at ourselves, to get partners funding and move things ahead quickly. We really want to make a great discovery for Riverside shareholders.

Maurice Jackson: Finally, what did I forget to ask?

John-Mark S.: Besides the news flow, what also is next is continuing to grow in Canada. We like Canada. We want to expand in Canada. So we’re excited to do that diversification beyond Mexico, where we’re very strong, but Canada’s wide open for us as well.

Maurice Jackson: Dr. Staude, for someone listening that wants to get more information on Riverside Resources, please share the contact details.

John-Mark S.: Please call us at 778-327-6671, or come to the website at rivres.com.

Maurice Jackson: And as a reminder, Riverside Resources trades on the TSX.V: RRI |OTCQB: RVSDF. Before you make your next bullion purchase, be sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs, and private blockchain-distributed ledger technology. Call me directly at 855-505-1900 or you may email [email protected].

Finally, we invite you to visit provenandprobable.com, where we provide Mining Insights and Bullion Sales. Riverside Resources is a sponsor of Proven and Probable, and we are proud shareholders of Riverside Resources for the virtues conveyed in today’s message.

Dr. John-Mark Staude, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Riverside Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Riverside Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Riverside Resources, a company mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Sweden’s central bank maintained its benchmark interest rate and while it confirmed it still expects to raise the rate in December, it said the outlook for economic growth and inflation in coming years is “very uncertain” and pushed back any further rate hikes to 2022.

As widely expected, Sveriges Riksbank left its benchmark repo rate steady at minus 0.25 percent and confirmed it “will most probably” raise the rate in December to zero percent, only the second time it will have tightened its policy since July 2011.

In December 2018 the Riksbank raised its rate for the first time in 7-1/2 years on solid economic growth and rising inflation, but then pushed back another rate hike to late this year as global economic growth weakened, curbing inflationary pressures.

Although economic growth in Sweden is now slowing, inflation remains close to the Riksbank’s 2.0 percent target and is forecast to remain steady at 1.8 percent this year and 1.9 percent next year, setting up the conditions for the rate hike in December.

But economic activity is now slowing faster than expected, but expansionary monetary policy in many countries is expected to support growth and the Riksbank doesn’t expect a recession and inflation is expected to tick up by 2022.

“However, the development of economic activity and inflation abroad and in Sweden in the coming years is very uncertain, and it is therefor difficult to say, at present, when it will be appropriate to raise the repo rate next time,” the Riksbank said, adding it expects interest rates to be unchanged “for a prolonged period after the expected rise in December.”

Underscoring this uncertainty, the Riksbank said improved economic prospects would justify a higher interest rate but if the economy were to develop less favourably, it “could cut the repo rate or make monetary policy more expansionary in some other way.”

The Riksbank confirmed its decision from April that it is purchasing government bonds worth 45 billion Swedish crown from July this year to December 2020.

In an update to its forecasts, the Riksbank sees the repo rate averaging 0.0 percent in 2020 and 2021, down from 0.2 percent forecast in September, and then rising to 0.1 percent in 2022.

Economic growth is expected to slow to only 1.3 percent this year, down from its earlier forecast of 1.5 percent, and 2.3 percent in 2018. Sveriges Riksbank issued the following statement:

“After several years of strong economic activity and inflation close to the target of 2 per cent, the Swedish economy is slowing down and the economic conditions are becoming more normal. In recent months, inflation has indeed fallen back, but this was expected and overall, the inflation prospects for the next year are unchanged. In line with the forecast from September, the Executive Board has therefore decided to leave the repo rate unchanged at –0.25 per cent. As before, the forecast indicates that the interest rate will most probably be raised in December to zero percent. Uncertainty over the development of economic activity and inflation abroad and in Sweden is considerable, however. The forecast for the repo rate has therefore been revised downwards and indicates that the interest rate will be unchanged for a prolonged period after the expected rise in December.

Slowdown in global growth

International GDP growth has slowed in recent years towards more normal levels. At the same time, unemployment is low in many countries. Compared with the assessment in September, the economic outlook for the euro area has deteriorated somewhat. However, expansionary monetary policy in many countries is helping to provide support to the economy. Inflation is therefore expected to rise from low levels. At the same time, the trade conflict between the United States and China and the unclear situation around the United Kingdom’s withdrawal from the EU continue to create uncertainty over growth prospects.

Faster slowdown towards more normal economic conditions

Similar to economies abroad, the Swedish economy has entered a phase of lower growth. The information received since the monetary policy decision in September indicates that economic activity is slowing down slightly faster than expected. However, the slowdown implies a normalisation of an economic situation that has been strong for many years with high growth and favourable development on the labour market.

Probable that the repo rate will be raised in December

Even though the forecasts have been revised downwards, they are not giving a picture of a recession – either abroad or in Sweden. Since the start of 2017, inflation has been close to the inflation target. It has indeed fallen back over recent months but this was expected and overall, the inflation prospects for the next year are unchanged from September. In line with the forecast from September, the Executive Board has therefore decided to leave the repo rate unchanged at –0.25 per cent. As before, the forecast indicates that the interest rate will most probably be raised in December to zero percent.

However, the development of economic activity and inflation abroad and in Sweden in the coming years is very uncertain, and it is therefore difficult to say, at present, when it will be appropriate to raise the repo rate next time. The forecast for the repo rate has been revised downwards and indicates that the interest rate will be unchanged for a prolonged period after the expected rise in December. In accordance with the decision from April 2019, the Riksbank is purchasing government bonds for a nominal total amount of SEK 45 billion, with effect from July 2019 to December 2020. The low level of interest rates will continue to give support to the economic outlook and inflation.

Uncertainty over economic developments

If the prospects were to change, monetary policy may need to be adjusted going forward. Improved prospects would justify a higher interest rate. If the economy were instead to develop less favourably, the Executive Board could cut the repo rate or make monetary policy more expansionary in some other way.

Important to have measures to mitigate the risks associated with household indebtedness

Swedish households are heavily indebted and thereby sensitive to changes in economic conditions. In order to reduce the risks linked to household indebtedness and address the structural problems on the Swedish housing market, measures within housing and tax policy and appropriate macroprudential policy are required.

Forecast for Swedish inflation, GDP, unemployment and the repo rate*

2018

2019

2020

2021

2022

CPI

2.0 (2.0)

1.8 (1.8)

1.9 (1.9)

1.8 (2.1)

2.1

CPIF

2.1 (2.1)

1.7 (1.7)

1.8 (1.7)

1.8 (1.8)

2.0

GDP

2.3 (2.4)

1.3 (1.5)

1.2 (1.5)

1.6 (1.9)

1.8

Unemployment, per cent

[6.3 (6.3)]

[6.8 (6.6)]

6.9 (6.7)

7.0 (6.8)

7.1

Repo rate, per cent

–0.5 (–0.5)

–0.3 (–0.3)

0.0 (0.0)

0.0 (0.2)

0.1

*Annual percentage change, annual average Note. The assessment in the September 2019 Monetary Policy Report is shown in brackets. Statistics Sweden has identified quality flaws in the LFS which mean that the statistics for unemployment in 2018 Q2–2019 Q3 are misleading. The figures directly affected by this are italicised and enclosed in square brackets. Sources: Statistics Sweden and the Riksbank

Forecast for the repo rate*

2019 Q3

2019 Q4

2020 Q1

2020 Q4

2021 Q4

2022 Q4

Repo rate

–0.25 (–0.25)

–0.25 (–0.23)

–0.05 (–0.05)

0.00 (0.08)

0.00 (0.24)

0.13

*Per cent, quarterly mean values Note. The assessment in the September 2019 Monetary Policy Report is shown in brackets. Source: The Riksbank

The decision on the repo rate will apply from 30 October 2019. The minutes from the Executive Board’s monetary policy meeting will be published on 5 November. A press conference with Governor Stefan Ingves and Jesper Hansson, Head of the Monetary Policy Department, will be held today at 11.00 at the Riksbank. Press cards must be shown. The press conference will be broadcast live on www.riksbank.se.”

Sterling fell out of favour with investors on Thursday after U.K Prime Minister Boris Johnson called for a general election on December 12 to break the Brexit deadlock.

The British Pound tumbled close to 1% against the Dollar to $1.2790, its lowest level since October 17, before later rebounding back towards $1.2850 as of writing. By Law, Johnson will need the backing of two-thirds of parliament to hold an early election. Given how his calls for a general election have already been rejected twice, history could repeat itself for the third time.

This development will most likely compound to the growing drama and uncertainty revolving around Brexit with the Pound in the direct firing line. While speculation over the European Union approving a three-month Brexit extension could cushion downside losses, this is simply kicking the can further down the road.

Until proper clarity and direction are offered on Brexit, the GBPUSD is positioned to trend lower. In regards to the technical picture, sustained weakness below 1.3000 should open a path towards 1.2790 and 1.2700, respectively.

Commodity spotlight – Gold

Gold bulls made a late apperance on Thursday as prices punched above the $1500 level. Price action suggests that investors are still waiting for a fresh market-moving event or report that will impact global sentiment. Market players remain cautious over the Brexit developments while some are optimistic over the US-China “phase-one” trade deal. Until something fresh is brought into the picture, Gold is poised to remain range bound.

Looking at the technicals, the breakout above $1500 should iopen the doors towards $1515 and $1525, respectively.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

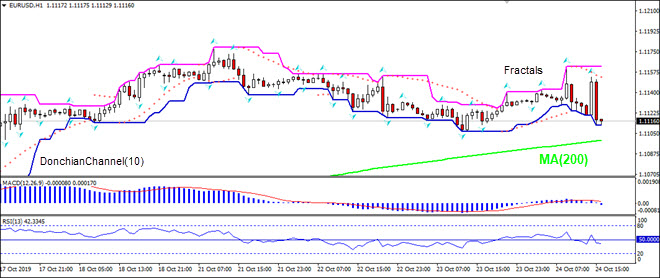

Weaker than expected euro area PMIs bearish for EURUSD

Euro-zone’s flash readings of manufacturing and services sectors’ PMIs for October were weaker than expected. Will the EURUSD decline?

The price chart on 1-hour timeframe shows EURUSD: H1 is trading sideways. The price is falling toward the 200-period moving average MA(200) which is rising. And the RSI oscillator is below 50 level but has not reached the oversold zone. There is no trend yet formed, traders have to decide when it would be a best time to enter the market.

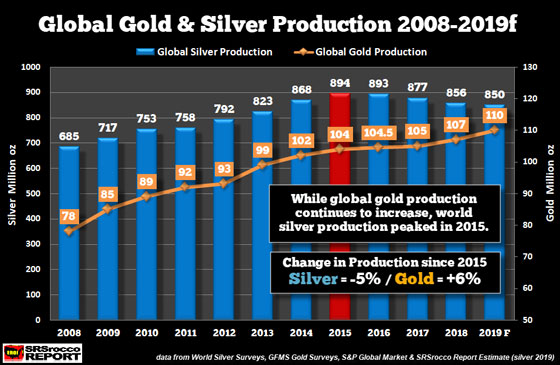

Three of the largest silver producers in the world saw their combined mine supply continue to weaken in the first seven months of 2019. While Mexico and Chile experienced declines in their silver production, Peru was by far the biggest loser. Peru, which is the second-largest silver producer in the world, suffered an 11% decline in the country’s domestic mine supply Jan-Jul 2019.

Even though the decline of silver mine supply at these leading producers isn’t impacting the current silver market price currently, it will likely do so as the Fed and central banks lose control of their QE money printing and asset purchase policy. In less than two weeks, the total U.S. debt has increased by another COOL $85 billion. With total U.S. public debt now at $22.92 trillion, it’s only a matter of time, maybe just a few weeks before we reach another record of $23 trillion.

With the global silver mine supply this year to reach an estimated 850 million oz of production, the total value based on the Kitco $16 average for the year would only be $13.6 billion. Thus, the U.S. Government has increased the public debt in the past two weeks by more than SIX TIMES the value of the Global silver production this year.

Yes, I do realize that comparing the value of silver to the increase in U.S. debt hasn’t mattered to the markets, but it will. What will happen with silver (and gold) will be very similar to the investor reaction to ENRON when the market realized that the company was a fraud. And, let’s not forget that several top Wall Street analysts, in their glorious (Let’s continue to bamboozle investors) fashion, continued to put out BUY recommendations days before ENRON collapsed.

So, the market will continue to be BAMBOOZLED by Wall Street and central banks right up until the time that the GIG IS OVER. This means the time to acquire Gold & Silver physical insurance is likely much wiser to purchase BEFORE than the day AFTER the GIG is up.

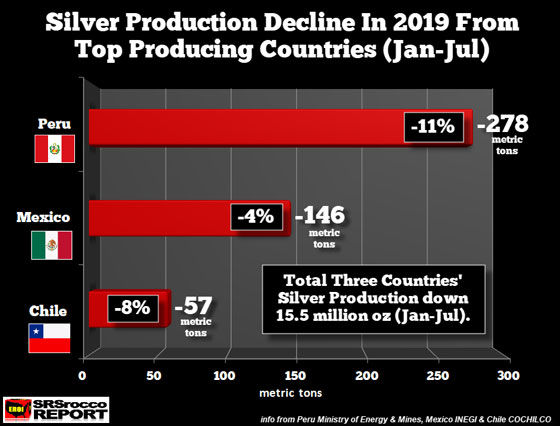

Okay, let’s look at the Top silver producers decline in silver mine supply Jan-Jul 2019:

In the first seven months of the year, Peru’s domestic mine supply is down a whopping 278 metric tons (11%), while Mexico is down 146 metric tons (4%), followed by Chile down 57 metric tons (8%). The total decline in silver production from these three countries is 481 metric tons (mt) or 15.5 million oz.

Furthermore, Polymetal International, Russia’s largest silver producer, which accounted for 58% of the country’s total mine supply last year, is down 14% in the first half of 2019. Russia is the fourth largest silver producer in the world, followed by Chile. So, four of the top five silver producers in the world are showing considerable declines in mine supply.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.