Economic data on the day saw the Conference Board’s consumer confidence index coming below forecasts. The index fell to 125.9 following a revision for the previous month to 126.3.

Euro Trades Mildly Bullish

The lack of economic data from the eurozone and sparse data from the United States saw the euro lacking direction.

Trading was largely subdued with most of the flows coming out of the US data. A line of big-ticket events today will likely change that.

EURUSD Holds on to Support – Will it Bounce Higher?

The currency pair was seen retesting the support area of 1.1075 – 1.1062. This marks the correction to the downside after price rallied to highs of 1.1177 – 1.1193.

Following this retest of support, we expect the bias to be to the upside. Price action will likely struggle as it approaches the resistance area. All in all, the EURUSD should be confined to the range.

UK Likely to Head for a General Election

The United Kingdom is likely to head for a general election after the opposition Labor party cleared the way. Leading UK indices fell on the news while the sterling did not budge.

The vote, which could take place as early as December, will be pivotal for the country. PM Johnson called for the elections after lawmakers vetoed his Brexit bill to enable the October 31st deadline.

GBPUSD Likely Forming the Upside

The currency pair has been in a holding pattern following the gains. The currency pair rose to highs near 1.2960. The current consolidation shows that there is the potential for a breakout above this level.

This would validate the bullish flag pattern with the GBPUSD likely to break past 1.30 threshold. To the downside, the lower support at 1.2582 will be key.

Gold Prices Recover After Losses

The precious metal was weaker on Tuesday, but the declines were smaller. This comes a day after gold prices fell sharply boosting risky assets.

The current consolidation is expected as investors wait for today’s Fed meeting. But the bias looks to be to the downside for the moment.

XAUUSD Could Test Support at 1462

The precious metal has been quite erratic in the recent few sessions. This comes after price failed to break past the resistance area of 1511.50. The retest of this level promptly sent gold prices lower. The breakdown of the rising trend line now likely opens the way for declines to 1462.20.

Asian stocks are mixed after US stocks came off record highs, as investors await the Federal Reserve’s latest policy decision and forward guidance. Safe haven assets have also been trading sideways mostly, with Gold not straying too far from the $1500 psychological level, while the Japanese Yen remains below 109 against the US Dollar.

The Dollar index (DXY) is currently steady around the mid-97 levels, as markets await Fed chair Jerome Powell’s forward guidance, sandwiched between the release of US Q3 GDP data and the October non-farm payrolls report. With Fed funds futures already forecasting a 95 percent chance of a third consecutive 25-basis point cut to US interest rates, Powell’s remarks are set to have a bigger influence over the markets rather than the FOMC decision itself.

Should Powell signal a “hawkish cut”, whereby the Fed deems the US economy as having sufficient “insurance” after this month’s 25-basis point adjustment, that could propel DXY back above the 98 psychological level. However, if the door is left wide open for more US rate cuts going into next year, that would disappoint investors who are currently betting that the Fed will leave its policy settings unchanged for the December FOMC meeting.

The upcoming Q3 GDP and jobs report could also further garnish the Dollar’s moves this week, as investors ascertain whether the economic data will either raise or lower the bar for more Fed rate cuts.

Pound in political paralysis as investors digest snap election prospects

News of the upcoming UK elections didn’t offer markets enough reason to break GBPUSD out of the 1.28-1.29 range for now. Over the next six weeks, Sterling could still reflect the political nuances out of the UK as investors try and pre-empt the outcome of the December 12 polls.

Ultimately, investors will be filtering the elections through the Brexit prism, hoping that the world can gain conclusive clarity to this saga that has dragged on since 2016. It remains to be seen how the various political parties position themselves during the campaigning period, who has the better chances of winning and potentially having the final say on Brexit. However, with a no-deal Brexit now seemingly off the table, that suggests that Sterling’s downside is limited, barring any sustained rally in the US Dollar.

Post-Fed Dollar moves to feed into Oil’s near-term performance

Brent futures have climbed more than 3.5 percent so far this month and made their way above the 100-day moving average, taking advantage of the softer Dollar. Oil prices have been buoyed by expectations that OPEC+ will have to enact deeper supply cuts in December, as well as optimism surrounding a US-China trade deal. Should any of these hopes prove unfounded, Brent is likely to give up recent gains as investors refocus on further signs of waning global demand and rising US stockpiles. In the event that the Fed signals a “hawkish cut”, subsequently prompting a bout of Dollar strength, that could add to the downward pressure on Oil prices.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stocks pulled back on Tuesday on mixed earnings reports. The S&P 500 slipped 0.1% to 3036.89. The Dow Jones industrial average slid 0.1% to 27071.42 weighed by 2.1% drop in Google’s parent Alphabet on earnings miss. Nasdaq fell 0.6% to 8276.85. The dollar weakening was intact despite better than expected pending homes sales in September. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, slipped 0.1% to 97.68 but is higher currently. Federal Reserve is expected to cut rates a third time today. Futures on US stock indices point to lower openings.

CAC 40 rises while other European indexes slip

European stock market snapped four-session winning streak on Tuesday. The EUR/USD joined GBP/USD’ climb with both pairs higher currently. The Stoxx Europe 600 ended 0.2% lower led by telecom stocks. The German DAX 30 slipped 0.02% to 12939.62. France’s CAC 40 however advanced 0.2%. UK’s FTSE 100 slid 0.3% to 7306.26 ahead of UK House of Commons vote authorizing an election on December 12.

Nikkei leads Asian indexes losses

Asian stock indices are falling today after reports a “phase one” deal might not be ready to be signed at the Asia-Pacific Economic Cooperation summit in Chile next month. Nikkei fell 0.6% to 22843.12 despite yen continued slide against the dollar. Chinese stocks are falling as China accused the US of “bullying” over a proposed ban on Chinese telecom equipment in US networks: the Shanghai Composite Index is down 0.5% and Hong Kong’s Hang Seng index is 0.5% lower. Australia’s All Ordinaries Index turned 0.8% lower as Australian dollar continued climbing against the greenback.

Brent futures prices are edging lower today. Prices edged up yesterday: December Brent rose 0.03% to $61.59 a barrel on Tuesday. Trade group the American Petroleum Institute late Tuesday report indicated US crude supplies fell by 1.7 million barrels last week. Today at 16:30 CET the Energy Information Administration will release US Crude Oil Inventories.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

How the transaction benefits the London-based oil and gas firm is outlined in a Pareto Securities report.

In an Oct. 21 research note, Pareto Securities analyst Tom Erik Kristiansen reported that Panoro Energy ASA (PEN:OSE; 1PZ:FRA) agreed to sell its noncore stake (a 12.2% economic interest) in the Aje field in offshore Nigeria to PetroNor for US$10 million in shares plus long-term upside. “We believe the transaction could unlock significant value and view it as positive for both companies.”

For Panoro, Kristiansen indicated, the timing and structure around divesting the Aje stake were ideal.

He noted the positive effects the transaction will have on Panoro. Financially, the valuation impact on the United Kingdom company of the US$10 million in shares is about NOK1.5 per share, according to Pareto’s estimate. However, if the natural gas resources at Aje are developed, Panoro could receive up to US$25 million in royalty payments. “Panoro intends to dividend out the shares in PetroNor, which we view as shareholder friendly,” wrote Kristiansen.

Finally, for Panoro, the transaction will “free up additional resources that now can focus on Panoro’s core assets and potential future mergers and acquisitions transactions, which in our opinion is a significant positive,” Kristiansen highlighted.

Pareto has a Buy recommendation on and expects to increase its current NOK23 target price on Panoro Energy.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Pareto Securities AS, Panoro Energy, October 21, 2019

This publication or report has been prepared solely by Pareto Securities Research.

Opinions or suggestions from Pareto Securities Research may deviate from recommendations or opinions presented by other departments or companies in the Pareto Securities Group. The reason may typically be the result of differing time horizons, methodologies, contexts or other factors.

Analysts Certification The research analyst(s) whose name(s) appear on research reports prepared by Pareto Securities Research certify that: (i) all of the views expressed in the research report accurately reflect their personal views about the subject security or issuer, and (ii) no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analysts in research reports that are prepared by Pareto Securities Research.

The research analysts whose names appears on research reports prepared by Pareto Securities Research received compensation that is based upon various factors including Pareto Securities total revenues, a portion of which are generated by Pareto Securities investment banking activities.

Conflicts of interest

Companies in the Pareto Securities Group, affiliates or staff of companies in the Pareto Securities Group, may perform services for, solicit business from, make a market in, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned in the publication or report.

In addition Pareto Securities Group, or affiliates, may from time to time have a broking, advisory or other relationship with a company which is the subject of or referred to in the relevant Research, including acting as that companys official or sponsoring broker and providing corporate finance or other financial services. It is the policy of Pareto to seek to act as corporate adviser or broker to some of the companies which are covered by Pareto Securities Research. Accordingly companies covered in any Research may be the subject of marketing initiatives by the Corporate Finance Department.

To limit possible conflicts of interest and counter the abuse of inside knowledge, the analysts of Pareto Securities Research are subject to internal rules on sound ethical conduct, the management of inside information, handling of unpublished research material, contact with other units of the Group Companies and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. The object of the internal rules is for example to ensure that no analyst will abuse or cause others to abuse confidential information. It is the policy of Pareto Securities Research that no link exists between revenues from capital markets activities and individual analyst remuneration. The Group Companies are members of national stockbrokers associations in each of the countries in which the Group Companies have their head offices. Internal rules have been developed in accordance with recommendations issued by the stockbrokers associations.

This material has been prepared following the Pareto Securities Conflict of Interest Policy. The guidelines in the policy include rules and measures aimed at achieving a sufficient degree of independence between various departments, business areas and sub-business areas within the Pareto Securities Group in order to, as far as possible, avoid conflicts of interest from arising between such departments, business areas and sub-business areas as well as their customers. One purpose of such measures is to restrict the flow of information between certain business areas and sub-business areas within the Pareto Securities Group, where conflicts of interest may arise and to safeguard the impartialness of the employees. For example, the Corporate Finance departments and certain other departments included in the Pareto Securities Group are surrounded by arrangements, so-called Chinese Walls, to restrict the flows of sensitive information from such departments. The internal guidelines also include, without limitation, rules aimed at securing the impartialness of, e.g., analysts working in the Pareto Securities Research departments, restrictions with regard to the remuneration paid to such analysts, requirements with respect to the independence of analysts from other departments within the Pareto Securities Group rules concerning contacts with covered companies and rules concerning personal account trading carried out by analysts.

Pareto Securities AS may hold financial instruments in companies where a recommendation has been produced or distributed by Pareto Securities AS in connection with rendering investment services, including Market Making.

Overview over issuers of financial instruments where Pareto Securities AS have prepared or distributed investment recommendation, where Pareto Securities AS have been lead manager/co-lead manager or have rendered publicly known not immaterial investment banking services over the previous 12 months: Panoro.

Shares of IVERIC bio opened nearly 100% higher today after reporting that it successfully met its primary endpoint in its Phase 2b age-related macular degeneration study for Zimura.

Early this morning, gene therapy focused biopharmaceutical company IVERIC bio Inc. (ISEE:NASDAQ), which focuses on the discovery and development of novel treatment options for orphan inherited retinal diseases, announced initial topline data confirming that “Zimura (avacincaptad pegol), the firm’s complement factor C5 inhibitor, met its prespecified primary endpoint in reducing the rate of geographic atrophy (GA) growth in patients with dry age-related macular degeneration (AMD) in a randomized, controlled Phase 2b clinical trial.”

The study enrolled 286 patients in order to assess the safety and efficacy of various doses of Zimura in patients with GA secondary to dry AMD. The company reported a reduction in the mean rate of GA growth over 12 months and noted that the overall data suggest a dose response relationship across all treatment groups. The company further advised that Zimura was generally well tolerated after 12 months of administration with no Zimura-related inflammation, nor were there any ocular serious adverse events and no cases of endophthalmitis reported in the study eye in this ongoing clinical trial.

Marco A. Zarbin, M.D., Ph.D., FACS, Professor and Chair, Institute of Ophthalmology and Visual Science, Rutgers-New Jersey Medical School, Newark, NJ stated, “IVERIC bio’s unwavering commitment to science has resulted in compelling Phase 2b data in GA secondary to dry AMD, a major public health problem that has devastating effects on our patients…As a retina specialist, Zimura’s impressive efficacy results and favorable safety profile observed to date in this trial indicate its potential as a future treatment for this growing patient population, which represents an urgent unmet medical need.”

IVERIC bio’s CEO and President Glenn P. Sblendorio commented, “This is a major milestone for IVERIC bio and a potentially significant advancement for patients with GA secondary to dry AMD who currently have no treatment options…Based on these data, we intend to explore all options for the future development of Zimura, including the possibility for collaboration opportunities, licensing and / or potentially further internal development.”

IVERIC bio’s Chief Medical Officer Kourous A. Rezaei, M.D., added, “Zimura’s efficacy data in this clinical trial supports the potential role of C5 inhibition in GA secondary to dry AMD…C5 activation may lead to retinal cell degeneration and ultimately cell death. We believe that the combination of statistically significant efficacy results for both Zimura 2 mg and 4 mg groups compared to their respective sham controls, with the lack of Zimura induced inflammation, zero rate of endophthalmitis and observed CNV conversion rate as compared to sham in this trial may potentially differentiate Zimura. We are encouraged by these exciting results, which we look forward to presenting in more detail at upcoming medical meetings in the near future.”

The company explains that “dry AMD is where thinning of the retinal pigment epithelial cells in the central portion of the retina, or the macula, develops, along with other age-related changes to the adjacent retinal and choroidal tissue layers…it is a significant cause of moderate and severe loss of central vision in older adults, affecting both eyes in the majority of patients…Geographic atrophy, the advanced stage of dry AMD, is a disease characterized by degeneration of retinal tissue leading to further loss of vision.” IVERVIC points out that presently there are no U.S. FDA or European Medicines Agency approved therapies to treat dry AMD.

IVERIC bio is headquartered in New York, NY and is a gene therapy focused biopharmaceutical company focused on the discovery and development of novel treatment options for orphan inherited retinal diseases with significant unmet medical needs. The firm proclaims that “Vision is Our Mission”.

IVERIC started off today with a market capitalization of about $38.7 million with approximately 41.56 million shares outstanding. ISEE shares opened nearly 100% higher today on the news at $1.85 (+$0.92, +98.92%) compared to Friday’s $0.93 closing price. The stock typically trades 75,000 to 150,000 shares per day, but today has already traded more than 22 million shares between $1.58 to $1.99 per share and is presently trading at $1.87 (+$0.94, +101.08%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Observations from a recent site visit there are provided in a BMO Capital Markets report.

In an Oct. 22 research note, BMO Capital Markets analyst Andrew Mikitchook reported the main takeaways from a site visit to Premier Gold Mines Ltd.’s (PG:TSX) South Arturo joint venture project with Nevada Gold Mines.

The primary highlight, Mikitchook indicated, is that the El Niño mine at South Arturo in Nevada is now in commercial production, which began in September. Further, mine output could reach 30,000 ounces in 2019, which would surpass the previous expectation of 21,000 ounces.

Of note as well, the analyst wrote, is that “El Niño has extra capacity to mine existing reserves faster or to extend the mine plan to depth toward additional resources and new exploration intercepts.” In addition, the potential exists via exploration to expand the mineralization not only at El Niño but also at Phase 3 and East Dee.

As for work in progress at the South Arturo property, noted Mikitchook, testing by five autonomous trucks at Phase 1’s prestrip is scheduled to be completed by year-end 2019.

Also, the joint venture is constructing and evaluating an oxide heap leach at Phase 1 as a standalone development at South Arturo or for processing at the North Area.

Further, geological and metallurgical studies are being conducted on Phase 3 to inform the decision on whether or not to add the Phase 3 pit to the reserves and mine plan.

BMO has an Outperform rating and a CA$4.75 per share target price on Premier Gold. The stock is currently trading at around CA$1.95 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from BMO Capital Markets, Premier Gold, October 22, 2019

IMPORTANT DISCLOSURES

Analyst’s Certification I, Andrew Mikitchook, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Analysts who prepared this report are compensated based upon (among other factors) the overall profitability of BMO Capital Markets and their affiliates, which includes the overall profitability of investment banking services. Compensation for research is based on effectiveness in generating new ideas and in communication of ideas to clients, performance of recommendations, accuracy of earnings estimates, and service to clients.

Disclosure 16: A research analyst has extensively viewed the material operations of Premier Gold. Disclosure 17: Premier Gold has paid or reimbursed some or all of the research analyst’s travel expenses.

For Important Disclosures on the stocks discussed in this report, please click here.

The test results and next steps are provided in a Mackie Research Capital Corp. report.

In an Oct. 21 research note, Mackie Research Capital Corp. analyst Bill Newman reported that Valeura Energy Inc. (VLE:TSX; PNWRF:OTCMKTS) completed the final test of the Inanli-1 appraisal well in Turkey, which, like the first three, showed stable natural gas production.

Of the four tests of Inanli-1, the first, or deepest, zone had the “most encouraging” results, noted Newman. It had the highest average flow rate and a low, decreasing water rate. The other three tests flowed gas but more slowly than the first. The final test achieved a maximum sustained flow rate of 643,000 cubic feet per day at its deepest point.

“Valeura remains optimistic that certain zones within the Inanli-1 well hold the potential for exploitation through horizontal drilling and potentially through comingled vertical completions,” relayed Newman.

Valeura will begin testing the Devepinar-1 appraisal well, located 20 kilometers to the west of Inanli-1. The aim is to “better understand the lateral and vertical reservoir characteristic and hydrocarbon composition of its potential massive basin-centered natural gas accumulation (BCGA),” explained Newman.

The analyst added that whereas the potential size of the BCGA is “massive,” further drilling and testing are needed to derisk the play and advance the project to the development phase. Accordingly, Mackie has a Speculative Buy rating and a CA$3.50 per share target price on Valeura, recently down from CA$5.75 per share and versus the CA$0.82 current share price.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Mackie Research, Valeura Energy, Update, October 21, 2019

RELEVANT DISCLOSURES APPLICABLE TO COMPANIES UNDER COVERAGE Relevant disclosures required under Rule 3400 applicable to companies under coverage discussed in this research report are available on our web site at www.mackieresearch.com.

ANALYST CERTIFICATION Each analyst of Mackie Research Capital Corporation whose name appears in this report hereby certifies that (i) the recommendations and opinions expressed in this research report accurately reflect the analyst’s personal views and (ii) no part of the research analyst’s compensation was or will be directly or indirectly related to the specific conclusions or recommendations expressed in this research report.

Mackie Research Capital Corporation, its directors, officers and other employees may, from time to time, have positions in the securities mentioned herein.

RELEVANT DISCLOSURES APPLICABLE TO: VALEURA ENERGY INC. 1. Relevant disclosures required under IIROC Rule 3400 applicable to companies under coverage discussed in this research report are available on our web site at www.mackieresearch.com. 2. None Applicable for this Issuer

A case can be made that silver’s current price “stability” – believed by many to be well below where it “should” be – is the result of at least three interlocking factors.

There are certainly other considerations, but the following seem especially relevant today…

Our chosen metaphor is the three-legged stool. Take one leg away, and the stool topples. In the case of silver, the outcome is likely to be a violent price rise of epic proportions.

1. Draining the Silver Trading Swamp

In recent months, a series of criminal charges and admissions among banks, trading houses and their employees have begun to expose unfair and/or illegal trading practices. They have detrimentally influenced metals markets for many years, according to critics which include Ted Butler and the Gold Anti-Trust Action Committee (GATA).

Their illicit activities include “spoofing,” i.e. placing, then withdrawing large orders to cause investors to panic/offset a position, or risk a margin call; creating almost unlimited sell orders in the futures markets to break a bull rally’s back; writing derivatives to create/lease out more “paper metal” than is physically produced each year; and perhaps even collusion with government agencies to manipulate gold and silver prices as a tool of foreign policy.

Manipulation has become so widespread and blatant that the government is now leveling racketeering charges. How it all shakes out is anyone’s guess, but this can’t help but bring increased transparency in restoring supply/demand balance to markets sorely in need of it.

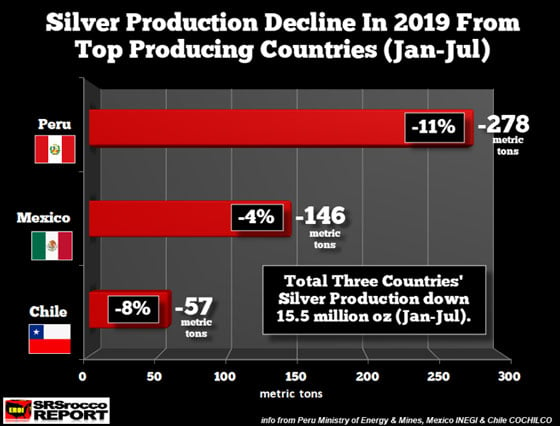

2. Mined Supply Constricting

Virtually all the precious metals, some base metals, and the PGMs (platinum and palladium) are currently mired in a series of systemic factors calling into question the ability of producers to reliably meet marketplace demands through the end of the next decade.

Declining production grades (in grams, ounces, or pounds/ton) plus a lack of major new discoveries to replace what’s mined leads to lower economically recoverable reserves.

Longer discovery-to production-timelines – often by many years, due to environmental concerns and country risk – add more complexity and unpredictability to the mix.

Large, already-producing mines in some of the most mineral-rich countries on the globe – Peru, Mexico, Argentina and Chile – face water access, community-relations and country taxation issues. They call into question if a given project is worth risking additional millions (sometimes billions) of operational capital just to keep it going.

These issues, affecting mining around the globe, have for the last decade weighed on annual metals’ production – even as imports to Asian countries continue at a blistering pace.

3. The Global Debt Trap

The most difficult to quantify, contain, and solve hydra-headed factor of all… is the global debt overhang/negative interest rate/cash-destruction trap.

This new “river of no returns” is becoming a systemic threat. It will at some point drive people across the board to one of the few options left: the historic utility and safety of gold and silver.

Global debt now exceeds a mind-boggling $250 trillion. As it rises, waves of money and credit chasing yields have driven rates to historic lows.

Banks penalize saving and responsible business decision-making, via negative interest rates (with 19 European countries now doing so) – and make the individual’s ability to offset inflation impossible.

At some point in the near future, the overburden of mispriced assets will inevitably decline in value. Negative interest rate victims, be they in savings accounts or underfunded pension plans, will be trapped.

Add to this an outbreak of inflation as massive amounts of money chases a limited supply of negatively-correlated assets – e.g. gold and silver – and a “run for the gold” lasting multiple years is almost a certainty.

Issues #1 and 2 above can possibly be contained. But printing money to infinity in support of never-to-be-repaid debts threatens a contagion imploding the entire financial house of cards.

European central banks have already sold over €15 trillion in negative interest bonds! Now the proverbial chicken – being penalized at the retail level for trying to save – is coming home to roost.

A government-backed digital currency is the likely next step. Sweden is looking at rolling out its own version called the “e-krona.” And, of course, China has an e-currency modeled on the renminbi.

Implications for consumers of moving from positive interest rates and physical cash to a “new normal” of negative rates and digital currencies are profound – and mostly negative. You will be penalized for what you do not spend; and will have virtually no privacy, since every item purchased with “digital cash” gets recorded.

The core function of interest rates – signaling the viability in making business and personal expenditure decisions, will have been completely silenced.

A recent Money Metals Exchange interview referenced the Federal Reserve’s ongoing fiat creation, now literally taking place day and night (repo market lending)…

Perhaps the biggest takeaway from these events is that Fed stimulus is a one-way train… (It) is better understood as an addictive drug. The Fed can never withdraw it without crippling or killing the markets. Plus, there’s always the risk of an overdose.

This kind of increasingly clueless monetary behavior weakens the leg of fiscal management that provides an artificial “lid” holding down silver bullion prices.

Ongoing investigation (finally) by regulatory agencies tasked with protecting the public, and keeping banks and trading houses honest, continues to uncover dirt as traders higher up the food chain are indicted for illegal trading practices, weakening supportive leg number two.

The Spark

When, not if, the “Iskra” – meaning “spark” in Croatian, is lit by high volume European and North American retail buying, you can expect supply – the third and final leg keeping silver prices reasonably stable – to be pulled out from under the market.

As the metaphorical stool tips over, we’ll see higher price points more quickly than most observers now believe possible.

Start protecting your assets by acquiring the insurance benefits and profit potential that physical gold and silver now provide.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Early tomorrow, or late tonight depending on where you live, we get the most important data of the week for the AUD.

Inflation data not only moves the currency on its own, but could be instrumental in determining whether the RBA cuts the reference rate again this year.

Despite moving higher so far this month, AUDUSD hasn’t managed to break out of the year-long downward channel it has been stuck in.

It might be optimistic to think it bottomed out in late September. But, if any data were to be able to nudge it higher, it would be CPI.

What We Are Expecting

There a host of different CPI measurements, all of which are important. But the one that the market tracks because it’s the one that the RBA uses for setting policy is the RBA Trimmed Mean CPI.

On a quarterly basis, expectations are for it to remain steady at 0.4% compared to the second quarter. But that would imply a slight lowering of the annual rate to 1.5% compared to 1.6% prior.

A quarterly CPI change of 0.4% would be bang in line with the average it has been maintaining for almost the last four years. Despite the inflation rate remaining relatively stable, it has been below the RBA’s target.

We can, therefore, expect that the central bank won’t be happy to see their favorite measure of inflation not budge after an unprecedented easing cycle.

The Other Measures

Expectations are for third-quarter CPI to come in identical to the prior quarter as well, at 0.6%.

On an annualized basis, however, this would show an increase to 1.8% from 1.6%, bringing it in closer to the RBA’s target. This would put it in a striking range of the projections made by the OECD and IMF, which supports the view that inflation in Australia will be higher next year.

Analysts have pointed to the droughts in Australia as having put upward pressure on food prices and would explain the discrepancy between the trimmed mean and CPI measurements.

With the currency basically leveling off during the last three months, rising import costs are not likely to have contributed to inflation.

What About Interest Rates?

There is a pretty strong consensus that the RBA won’t cut rates for the rest of the year, and it would take a substantial miss in expectations to shake that confidence.

For that matter, there are other indications that might give the bank reason to pause the rate cut. And it’s not just increasing pressure from MPs: retail consumption is not increasing significantly. Neither are home loans, the leading use of borrowed money among Australians.

Despite record-low mortgage rates, few Australians are seeking to refinance loans. Rather than increasing spending, Australians appear to be opting to pay down their existing debt.

The lack of spending isn’t going to help inflation numbers

But, Does the RBA Care?

The RBA has been rather emphatic that they are interested in bringing the unemployment rate down, which has been slowly moving above the structural level.

The standard macroeconomic thinking is that lower unemployment means higher wages mean higher inflation, but salaries in Australia have been rising apace without much change in inflation.

For the currency markets, the practical effect of this might be that we don’t get much of a reaction to inflation data this time around. That is unless the figures come in way outside expectations.

UK’s broad monetary aggregate M4 rose 0.7% on month in September from 0.4% in August. Will the GBPUSD decline?

The price chart on 1-hour timeframe shows GBPUSD: H1 is trading sideways. The price is rising toward the 200-period moving average MA(200) which is level. And the RSI oscillator is above 50 level but has not reached the overbought zone. There is no trend yet formed, traders have to decide when it would be a best time to enter the market.