Risk-off mode continues to cast a cloud over Asian assets, as media reports pour cold water on hopes that a US-China trade deal can be sealed by the end of the year. Asian stocks are retreating, while the Japanese Yen is the only Asian currency that’s gaining against the US Dollar at the time of writing, with USDJPY inching closer to the 108.0 mark. Other safe haven assets such as Gold are also advancing, with Bullion consolidating its place above the $1470 psychological level.

Safe haven assets have been held back from runaway gains by investors’ collective hopes that a US-China trade deal remains possible, albeit delayed. Chinese Vice Premier, Liu He, said he is “cautiously optimistic” about reaching the highly-anticipated phase one deal with the US, although he reportedly was left confused by some of the demands out of Washington. Expect market participants to continue chasing the US-China trade theme, potentially triggering erratic market movements along the way.

Dollar index steadies below 98.0 psychological mark

The Dollar index (DXY) is keeping within the upper-97 range, after the minutes from the October FOMC meeting were released. According to the minutes, Fed officials still noted that downside risks to the US economy remained “significant” and “prominent” in justifying their third 25-basis point cut to US interest rates for the year.

Still, the Fed believes that US interest rates are “well calibrated” at current levels, which supports market expectations that the Fed will stand pat over the coming months, hence the muted reaction in the DXY. Should the incoming domestic economic data or global economic conditions show a marked deterioration, that is likely to prompt the Fed into reassesing its US economic outlook and potentially move US interest rates again.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Shares of Myovant Sciences opened 120% higher today after the firm reported a 97% response rate in its Phase 3 HERO Study of oral Relugolix in men with advanced prostate cancer. In the study, Relugolix achieved all six key secondary endpoints and the firm expects to submit a New Drug Application in Q2/20.

This morning before the U.S. markets opened, healthcare company Myovant Sciences Ltd. (MYOV:NYSE), which is focused on developing innovative treatments for women’s health and prostate cancer, announced positive results for its Phase 3 HERO study for oral relugolix. The firm indicated that in the study once-daily, oral relugolix (120 mg) met its primary efficacy endpoint and all six key secondary endpoints in men with advanced prostate cancer and that “these results support a New Drug Application (NDA) submission to the U.S. Food and Drug Administration (FDA) in Q2/20 and future regulatory submissions in Europe and Japan.”

The Phase 3 HERO program plans include the enrollment of approximately 1,100 patients. It is a multinational clinical study designed to evaluate the safety and efficacy of relugolix in men with androgen-sensitive advanced prostate cancer who required at least one year of continuous androgen deprivation therapy. The firm states that the trial includes 138 Chinese patients residing in China and Taiwan in order to support future registration in China.

According to Neal Shore, M.D., medical director of the Carolina Urologic Research Center and HERO Program Steering Committee Member, “An oral gonadotropin-releasing hormone, or GnRH, antagonist for advanced prostate cancer has been an aspiration for many years…If approved, relugolix would become the first-of-its-kind oral option for men with advanced prostate cancer.”

Lynn Seely, M.D., president and CEO of Myovant Sciences commented, “With the exciting results from the HERO study demonstrating the potential of relugolix to provide unique benefits compared to leuprolide, we look forward to submitting an NDA to the FDA…We are now closer to our goal of bringing a precision oral medicine to the broad spectrum of men with advanced prostate cancer.”

The company advises that “prostate cancer is the second most prevalent form of cancer in men and the second leading cause of death due to cancer in men in the U.S. Approximately three million men in the U.S. are currently living with prostate cancer, and approximately 170,000 men are estimated to be newly diagnosed in 2019. Advanced prostate cancer is prostate cancer that has spread or come back after treatment.”

The firm explains that Relugolix is a once-daily, oral gonadotropin-releasing hormone (GnRH) receptor antagonist that reduces testicular testosterone production, the hormone primarily responsible for stimulating prostate cancer, and ovarian estradiol production, a hormone known to stimulate the growth of uterine fibroids and endometriosis.

Myovant Sciences is a clinical-stage biopharmaceutical company focused on developing and commercializing therapies for the treatment of women’s health, prostate cancer and endocrine diseases. The company’s lead product candidate is relugolix, a once-daily, oral GnRH receptor antagonist that binds to and inhibits receptors in the anterior pituitary gland. The company has three late-stage clinical programs for relugolix in uterine fibroids, endometriosis, and prostate cancer.

Myovant Sciences began the day with a market capitalization of approximately $543.1 million with about 89.62 million shares outstanding, along with a 4.50% short interest. MYOV shares opened 120% higher today at $13.37 (+$7.31, +120.63%) over yesterday’s $6.06 closing price. The stock has traded today between $10.37 to $17.17 per share and closed at $12.92 (+$6.86, +113.20%) on very high volume.

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Over the past 20 years, this company’s shares have outperformed gold by more than five to one.

Seabridge Gold Inc. (SEA:TSX; SA:NYSE.MKT), throughout its 20-year history, has focused on buying assets with exploration upside in low-risk jurisdictions during down times and selling noncore assets during good times, using the proceeds to fund exploration at its larger and more advanced projects, thereby minimizing equity dilution. This strategy has paid off; its flagship KSM project located in the center of British Columbia’s Golden Triangle boasts a Proven and Probable reserve of 38.8 million ounces of gold plus 10.2 billion pounds of copper, and a 50-year mine life. The Courageous Lake project, in Canada’s Northwest Territories, holds a reserve of 6.5 million ounces of gold. The company has a tight share structure, with 66 million shares outstanding fully diluted.

“We came away impressed with the potential at KSM and believe the growing resource base provides optionality to an incoming JV partner.” – Joe Reagor, ROTH Capital Partners

Rudi Fronk, CEO of Seabridge Gold, explains the strategy, “When we took over the shell in 1999, there were 17 million shares outstanding. We increased that to 27 million over three years to buy assets, so by the end of that period, we had roughly half an ounce of gold per share, 15 million ounces gold and 27 million shares. As the gold price then started to move higher, we realized that finding accretive acquisitions was going to be difficult, so we turned to the drill bit, first at Courageous Lake and then at KSM, and we were able to deliver significant growth in mineral resources. We also sold some assets at the top of the market. One property that we purchased for around $4 million and put $1 million into it, we sold a year later for over $35 million in cash.”

That cash Seabridge deployed into Courageous Lake and KSM thereby minimizing its need to issue new shares. The company’s rule of thumb is to grow ounces of gold in the ground faster than shares outstanding.

KSM is Seabridge’s flagship; the company has spent about $250 million over the past 13 years defining “the largest undeveloped gold project as measured by gold reserves,” Fronk stated. It is shovel ready and has completed its preliminary feasibility study and has its environmental approvals in hand. When Seabridge bought the property in 2000, there was little infrastructure. There is now a major highway just east of KSM, and governments of Canada and British Columbia have spent $700 million extending the power grid. Seabridge has preliminary agreements in place with BC Hydro to buy 250 megawatts of power from this line for about 5 cents a kW hour. And at the town of Stewart, two new port facilities make it possible to transport supplies year round, Fronk stressed.

The tailings capacity at KSM has been approved for about 2.3 billion tons of material; the company is playing around with mine plans to maximize the financial returns with that capacity. The Deep Kerr and a new zone under Iron Cap are higher-grade than the average reserve grades, and changing some open-pit mining to underground also saves on waste rock. An alternative mine plan Seabridge released in 2016 still captures around 40 million ounces of gold, but increases copper from 10 billion pounds to 17 billion pounds, and drops the cost per ounce of gold from $671/ounce to $359/ounce. The company expects to release a new mine plan next year and anticipates a further reduction in costs as higher grade zones are integrated into it.

The huge size of the project is daunting for a small company. “We admitted very early on that KSM is beyond our capabilities, so we have been searching for a partner. There are maybe only seven companies in the world today that have the technical, the financial and the social license to build a mine the size of KSM. We continue to speak with potential joint venture partners for both the gold and the copper side, and we have turned down several proposals over the past five years. Our view is we only get to do this once and it’s got to be with the right partner with the right terms,” Fronk explained.

“This is a project that up and running at today’s metal prices will generate about $1.5 billion of cash flow a year for the first ten years of mine life,” Fronk stated.

ROTH Capital Partners covers Seabridge. In July, analyst Joe Reagor, after visiting KSM, wrote, “We came away impressed with the potential at KSM and believe the growing resource base provides optionality to an incoming JV partner. . .Our most significant takeaway from the KSM tour was that as the resource base has grown the project has gained optionality as to the timing and method of development. . . we came away with renewed confidence that SA will attract a JV partner for KSM in the coming quarters.”

Seabridge also has the Snowstorm project in Nevada, which sits at the intersection of three prolific gold belts, the Getchell Trend, the Carlin Trend and the Northern Nevada Rift Trend. South of the project lie a number of producing mines, including Twin Creeks and Getchell, two of the mines that form the basis of the recent joint venture between Barrick Gold and Newmont Goldcorp. “We believe that the potential at Snowstorm is similar to what the potential was at Getchell when Placer Dome bought that outfit in the 1990s,” Fronk stated.

The aim of this year’s drill program at Snowstorm has been to confirm the geologic model. “I can say that what we’ve seen so far has confirmed the model and we look forward to what comes next. We’ll have subsequent programs over the next several years,” Front stated.

ROTH analyst Joe Reagor, after visiting Snowstorm in October, wrote, “We believe there is potential for the company to make a significant discovery on the project. . . While we believe the project is well located and that SA has a significantly better handle on the geology than the prior operators, we also believe it would be unreasonable to expect a discovery in the near-term. . . we believe it is in the company’s best interest to take a slow and steady approach to drilling the project.”

On the macro side, Fronk firmly believes that gold is going higher. “Many people believe that gold is doing a nice bottoming process right now from its recent highs and is poised to go substantially higher,” Fronk stated. He points to global debt of about $260 trillion, compared to a world economy that only generates GDP of about $80 trillion. “That’s more than 300% debt to GDP, which is at record levels on any measure throughout history. In addition, global equities are now about $80 trillion, and a lot of the high debt and equity values in our opinion have been driven by central bank policy of easy money over the past decade or so.”

“Our belief is that the coming recession will pop the credit bubble, generating defaults, corporate and potentially sovereign, creating unemployment, then huge government deficits, and central banks will try and prevent this collapse by aggressive monetization. As a result of that, we foresee currencies falling really hard and gold will soar.”

Seabridge shares have outperformed gold by more than five to one. While gold has risen 433% from 2000 through October 2019, Seabridge’s shares have increased 2,324% during that period.

ROTH analyst Joe Reagor wrote in September, “We believe a rising gold and silver market should benefit the company and could help the company attract a JV partner. . . Additionally, we believe the company could take advantage of rising precious metals prices and divest of non-core assets.”

ROTH has a 12-month target price of US$17 on Seabridge. The company’s shares are currently trading at around US$12.42. Insiders own over 30% of common shares, while institutional investors, including National Bank, Century Management, Van Eck, Weiss, TD Bank, Sprott, Fidelity and Paulson & Co., own about 25% of common shares. Seabridge has no debt and more than $20 million in working capital.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Seabridge Gold. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Torchlight Energy, a company mentioned in this article.

Disclosures from ROTH Capital Partners, Seabridge Gold Inc., Company Note, October 16, 2019 and July 15, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Seabridge Gold Inc. and as such, buys and sells from customers on a principal basis.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

The company continues to prove up its holdings as it searches for a partner.

Torchlight Energy Resources Inc. (TRCH:NASDAQ) is actively looking for a suitor for its large134,000 net acresOrogrande Basin project in Texas and is further exploring it to gain more scientific data.

ROTH Capital Partners has Torchlight under coverage with a Buy rating and a target price of $1.56. The stock is currently trading at around $0.82.

Torchlight holds a 72.5% interest in the Orogrande project. The company has re-entered a well bore the previous owners of the lease originated and, with the Cactus A35 1H well, has now drilled horizontally into the Penn formation.

“Our last producing well there was actually a 1,000 foot horizontal well that produced a lot of gas, but should also produce oil if we frack it hard enough,” Torchlight CEO John Brda told Streetwise Reports. “It’s all looking very good. It’s drilled and cased and ready for fracking, which we will do at the end of the month.”

The Penn formation has a dual porosity system, which means it has both gas and oil pores. “The gas is the easiest to get out of the rock, but we have to frack it hard enough to get the oil out of the rock,” Brda explained.

“The Cactus A35 #1H well targeted one of several prospective target zones within the Pennsylvanian Section, a different and deeper zone than the zone which was productive in the Founders A25 #1H,” explained Torchlight’s Geoscience Team lead, Mike Zebrowski. “The Cactus A35 # 1H was landed horizontally in the sweet spot and then geo-steered to stay within an optimal position for testing one of the oil zones to hydraulically fracture.”

In addition, Torchlight has identified about 20,000 acres of structure in addition to the unconventional acreage, and is now drilling the Founders A25 #2 wellit currently has drilled about one-third of the total 8,000 feetand will test about six or seven conventional zones, along with the Barnett and Woodford unconventional zones.

“The Orogrande is a unique system much like the Midland Basin and the Delaware Basin in that there are multiple benches of pay and it’s our job to determine which ones are going to be best and which ones are going to be economic. We obviously are going to focus on the most economic pay zones, but we have to do the science to determine that,” Brda said.

“The Founders A25 #2 well will provide the opportunity to test deeper zones below the Penn Section which offer both Conventional and Unconventional opportunities,” Zebrowski explained. “Many wells east of the Torchlight acreage targeted the Helms and Barnett/Woodford sections and achieved hydrocarbon production using only small vertical fracs. These zones are proven for horizontal unconventional production in the Delaware Basin, Midland Basin, Ft. Worth Basin, and in Oklahoma. The Founders A25 #2 will allow Torchlight to evaluate these deeper unconventional zones within the Torchlight Acreage and offer considerable upside.”

The company expects to release information on that drilling by the end of November.

Torchlight has several other properties. At its Hazel property located in the Midland Basin, the company conducted a full core on the Flying B Ranch #4 well and had that analyzed by Schlumberger. “It looks really, really good through the Wolfcamp section, Brda stated. “We are contemplating how we are going to go horizontal in that section, whether we will drill it ourselves or find a partner. We will determine that in the next few months.”

The company also recently drilled a shallow well to maintain the lease; it needs to drill one well every six months.

In additional, Torchlight holds a 12.5% interest in the Winkler property in the Delaware Basin, which is held by production. The project is producing 200300 barrels a day gross.

“We continue to have meaningful discussions with several large oil and gas peers regarding the potential of the Orogrande Project,” said Brda. “Feedback from technical teams has been overwhelmingly positive and complimentary regarding our operational accomplishments to date including the associated scientific data our team has assembled. The Merger, Acquisition and Divestiture market has been somewhat constricted this year precipitated by changes in commodity price, but we continue to pursue strong indications of interest and look forward to eventually moving the discussions from scientific to financial in nature. In the meantime, we will continue meeting drilling requirements and improving our asset profile. We will provide additional updates as developments are made both corporately and operationally.”

Torchlight has about 74 million shares outstanding.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Torchlight Energy. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Torchlight Energy. Please click here for more information. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Torchlight Energy, a company mentioned in this article.

By CentralBankNews.info Zambia’s central bank raised its policy rate for the second time this year to counter rising inflationary pressures and warned it may “further adjust the policy rate upward, if inflation persistently remains above the target range.” The Bank of Zambia (BOZ) raised its policy rate by 125 basis points to 11.50 percent and has now raised it 175 points this year following an earlier hike in May. Today’s rate hike follows BOZ’s warning in August that it could raise the rate if inflation didn’t revert to its target range. Since then, Zambia’s inflation has continued to accelerate, rising to 10.7 percent in October, the highest rate since October 2016, from 10.5 percent in September as food prices have continued to rise following drought and the kwacha depreciates further. The kwacha has fallen sharply since mid-October and was trading at 14.05 to the U.S. dollar today, down almost 15 percent this year.

In August BOZ expected inflation to remain above the upper bound of its target range for much of the forecast horizon but today it revised this forecast higher, saying inflation is now expected to remain above the upper bound of its 6-8 percent target range over the entire forecast horizon.

“The decision to raise the policy rate is therefore intended to counter inflationary pressures that include exchange rate pass-through effects and bring inflation back to the target range in the medium-term and hence support macroeconomic stability,” BOZ said. Looking ahead, BOZ said policy decisions would continue to be guided by inflation forecasts and outcomes, and progress in the execution of fiscal consolidation measures, BOZ said, adding monetary policy can’t solve the economic challenges alone and fiscal authorities and policy makers have to implement tight spending controls and improve the collection of revenue to tackle high fiscal deficits, debt and debt service while dismantling domestic arrears. Zambia’s economy is seen slowing further in the third quarter of this year as mining output, electricity generation, cement production and output of some manufactured products has declined, BOZ said, forecasting gross domestic product growth this year falling to 2.0 percent from 4.0 percent in 2018. In July the International Monetary Fund also forecast 2.0 percent growth this year on lower mining output and the impact of drought on hydro power generation.

The US Federal Reserve Bank will be releasing their meeting minutes today. The minutes cover the central bank’s monetary policy meeting held on October 30th this year.

The minutes will be interesting as they cover the meeting where the Fed cut rates, yet indicated that it would be pausing its rate cut cycle.

Interest rates were cut for the third time this year, bringing the Fed funds rate to 1.5% – 1.75%. The central bank cited various risks including the global developments to justify its rate cuts. It hopes that the rate cuts will help the US economy to stave off a recession.

Fed Funds Rate, October 2019

There has been an increase in concerns over the recession in the US economy. The US economy is currently enjoying the longest stretch of economic expansion to date. Therefore, economists are rightfully concerned about the implications.

The business cycle, at some point, is naturally expected to head into contraction.

US economic growth has seen that trend this year. This is evident from the latest GDP reports. The third-quarter GDP report covering the three months ending September 2019 showed a 2.0% expansion.

This marks one of the slowest patches of expansion in recent history. Therefore, it was a no-brainer for the Fed to cut rates. That being said, the cuts were not unanimous.

There were two dissenting voters who voted in favor of leaving rates unchanged. The dissenting votes came from Boston Fed President Eric Rosengren and the Kansas City Fed President, Esther George. Both these FOMC voters dissented across all the previous rate cuts as well.

Will the Fed minutes Spring a Surprise?

For the minutes to have any impact on the markets, they need to include a surprise. Given that officials already indicated their intention to pause further rate cuts, it is unlikely.

However, there is still a chance that a number of other Fed members might have felt that a rate cut was unnecessary. In the past week, a number of Fed members took to the stage.

Most importantly, Fed Chair, Jerome Powell gave his two-day testimony to US lawmakers. In his prepared remarks, Powell said that the current interest rates were sufficient for the economy.

He was hopeful that the lower rates would help the economy rebound. The slump in the third quarter was brushed aside. According to Powell, the declines in growth were largely due to the auto workers’ strike.

But besides growth, inflation also remains a concern for the Fed. Headline CPI has been stubbornly low. It is currently averaging around 1.7%. While this is close to the Fed’s 2% inflation target rate, there has been no evidence of price pressures.

As a result, the central bank is willing to wait for inflation to overshoot the Fed’s 2% inflation target rate. It hopes that this will help make up for years of low inflation. But, the evidence so far proves otherwise.

At the previous meeting, the markets were expecting the Fed to cut rates once more this year. But with the Fed coming out clear that it was done with rate hikes, the markets have been realigning themselves.

Will Trade Talks Have the Answer?

It would be prudent to expect the Fed to begin raising rates once again next year. It is quite likely that interest rates will remain near the current levels for the foreseeable future.

The biggest outlier is, of course, the US-China trade talks. The trade talks have been dragging on with no clear outcome in sight. The markets continue to trade mixed to mere rumors on progress.

The latest GDP data also showed that among all the components, trade was a drag with exports rising just 0.7% while imports grew 1.2% during the period.

Shares of Karuna Therapeutics, which completed an IPO in July 2019, soared more than 375% higher today after the firm reported that its KarXT met primary endpoint in a phase 2 clinical trial of acute psychosis in patients with schizophrenia.

This morning clinical-stage biopharmaceutical company Karuna Therapeutics Inc. (KRTX:NASDAQ), which focuses on developing novel therapies for people with disabling and potentially fatal neuropsychiatric disorders and pain, announced results from its Phase 2 clinical trial of KarXT for the treatment of acute psychosis in patients with schizophrenia.

According to the company, “KarXT is an oral coformulation of xanomeline (a novel muscarinic receptor agonist) and trospium (a muscarinic receptor antagonist) designed to treat psychosis and related symptoms through preferential stimulation of muscarinic receptors in the central nervous system (CNS).”

The firm noted that in the Phase 2 trial, KarXT demonstrated statistically significant and clinically meaningful improvement in total PANSS score at all time points over five weeks and was well-tolerated compared to placebo. The firm further stated that the data from the study supports advancing KarXT to Phase 3 and continued development in other CNS disorders.

Jeffrey Lieberman, M.D., professor and chairman of the Department of Psychiatry, Columbia University, College of Physicians and Surgeons and a member of Karuna’s scientific advisory board, commented, “The results of the Phase 2 trial are impressive and encouraging because they indicate that KarXT, if approved, could represent a game-changing therapeutic advance in the treatment of patients with schizophrenia…The effectiveness of antipsychotics has been limited by the frequent and serious side effects of first- and second-generation drugs which are difficult for many patients to tolerate, are potentially harmful, and lead to high rates of discontinuation and relapse. In addition to its novel mechanism of action, KarXT could be a new therapeutic option that has the potential to offer robust efficacy devoid of weight gain, metabolic effects and extrapyramidal side effects.”

Steve Paul, M.D., CEO, president, and chairman of Karuna, added, “The schizophrenia treatment landscape has remained rather stagnant for decades with therapeutic options relying on discoveries dating back to the 1950s…KarXT and its novel muscarinic receptor mechanism of action represent the potential to become a true advancement in how schizophrenia is treated, allowing patients relief from their debilitating psychotic symptoms without experiencing some of the very troubling side effects associated with current treatments.”

The company’s Chief Medical Officer Stephen Brannan, M.D., stated, “We are extremely pleased with these results, as the 11.6-point PANSS score separation from placebo far exceeded the five-point minimum improvement that has historically supported approval of current antipsychotics…With this information, and following our anticipated end-of-Phase 2 meeting with the FDA in the second quarter of 2020, we will work to initiate a Phase 3 clinical trial of KarXT in patients with schizophrenia by the end of 2020.”

The company elaborated in the report that the KarXT study was a Phase 2, randomized, double-blind, placebo-controlled, inpatient trial enrolled 182 adult patients, age 18 to 60, who had been diagnosed with DSM-5 schizophrenia and were experiencing acute psychosis.

The firm explained that “schizophrenia is a chronic, disabling disorder typically diagnosed in late teenage years or early adulthood. Characterized by recurring episodes of psychosis requiring long-term treatment with antipsychotic drugs in most patients, it affects more than 21 million people worldwide and 2.7 million Americans.”

Karuna Therapeutics is headquartered in Boston, Mass., and is a clinical-stage biopharmaceutical company focused on developing and delivering first-in-class therapies for people with central nervous system (CNS) disorders. CNS disorders remain among some of the most disabling and potentially fatal disorders worldwide. The firm states that “galvanized by the understanding that today’s neuropsychiatric and pain management patients deserve better, the company’s mission is to harness the untapped potential of the brain’s complex biology in pursuit of novel therapeutic pathways that will advance the standard of care”. The firm’s lead product candidate is KarXT, an oral modulator of muscarinic receptors that are located both in the CNS and various peripheral tissues. It is initially developing KarXT, for the treatment of acute psychosis in patients with schizophrenia.

Karuna started off the day with a market cap of approximately $413.9 million with about 23.41 million shares outstanding. The company completed its initial public offering (IPO) of its shares less than six months ago on July 2, 2019. KRTX shares opened nearly 84% higher today at $32.50 (+$14.82, +83.82%) over Friday’s $17.68 closing price. Since the open, the stock has soared much higher hitting a new 52-week high price of $86.00/share. The shares have traded today on high volume between $32.47 and $86.00 per share and are currently trading at $85.00 (+67.32, +380.77%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Sector expert Jason Hamlin explores the potential of the current gold bull market by charting the courses of past bull markets.

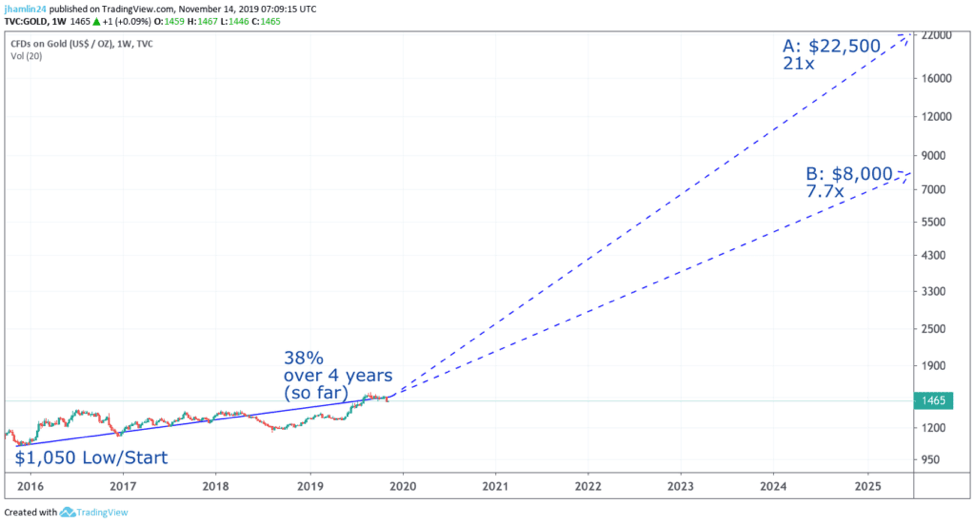

The gold price bottomed in late 2015 around $1,050 per ounce. It has since advanced to a high of $1,555 in early September, followed by a pullback to the current price of $1,470. Gold is in a well-defined uptrend channel with higher lows and recently higher highs. The breakout above $1,360 this summer was significant and we have seen follow-through buying. The $420 move in the price of gold from the bottom in late 2015 represents a gain of 40% in just under four years.

While this is a respectable gain, it only scratches the surface of the potential move ahead. To understand why, let’s take a look at the last two major bull markets in gold.

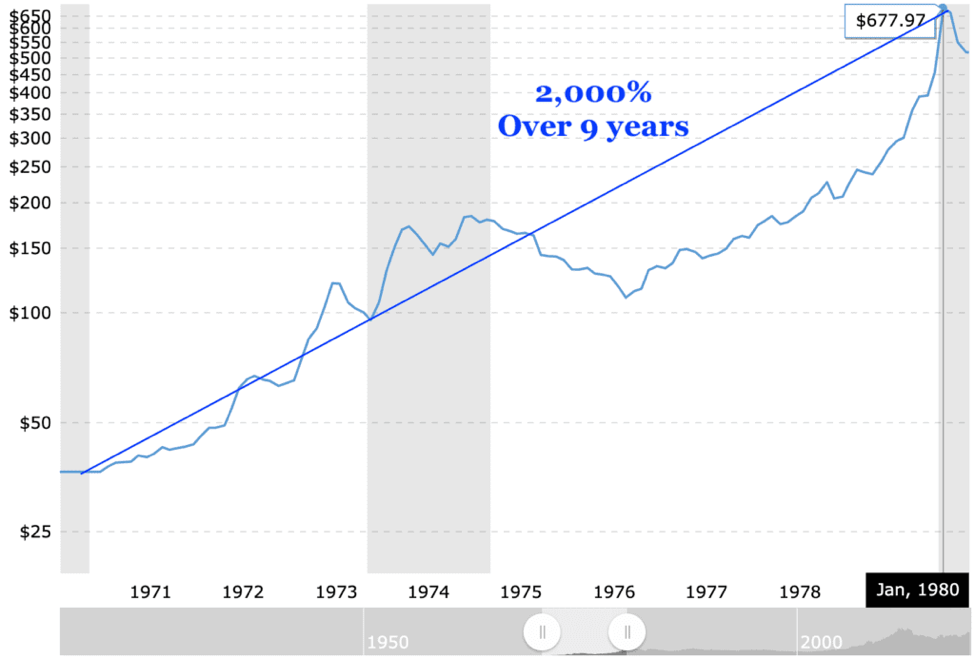

From 1971 to 1980, the gold price rocketed from a low of $35 to briefly peak at a high of around $850 ($678 high on the weekly chart) for a gain of just over 2,000%. It was closer to 850% in inflation-adjusted terms.

Of course, this massive move was driven by the abandonment of the gold standard window by Nixon, a stampede into gold as a safe haven from double-digit inflation, oil price shocks, a weak dollar, and political instability that made investors fearful and nervous.

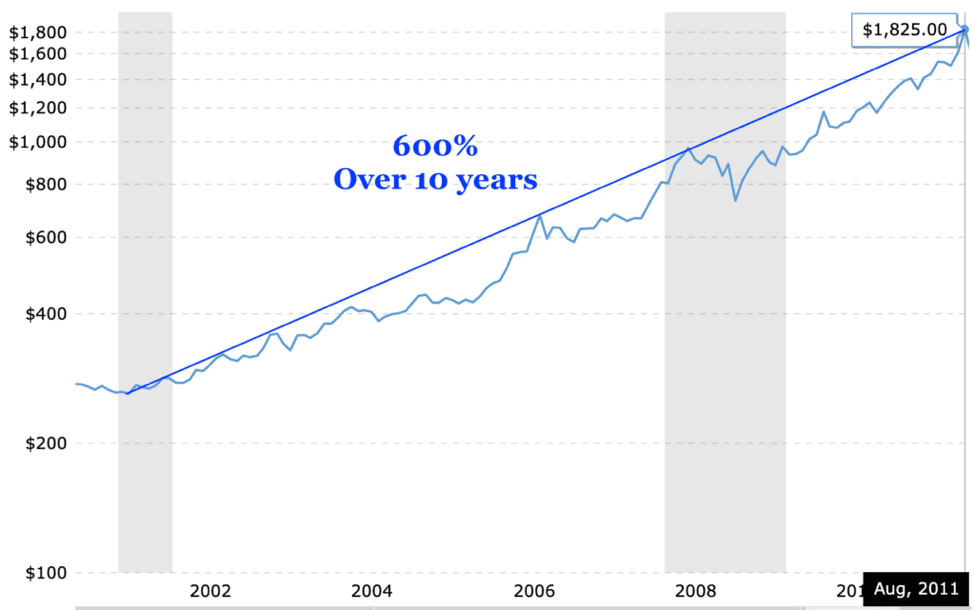

Fast-forward to 2001 and we can see that gold made another impressive move from $250 to a weekly high of $1,825 ($1,920 daily) over the course of roughly the same time period. This represents a gain of around 600% in that decade, or 450% in inflation-adjusted terms.

The current bull market cycle in gold is nearly four years old but hasn’t broken out of the gates yet. The 40% move higher since the start of 2016 is a modest advance relative to the last two bull markets. The gold price is moving higher today, so the chart below shows a 38% gain since the bottom.

The price would still need to go up roughly 15x (1,400%) to match the 1970s bull market, which would take the price to over $22,000! Or it would need to go up another 5.5x (450%) to $8,000 to match the magnitude of gains from the 20012011 bull market.

Put simply, the gold price has an explosive move ahead if the current bull cycle is to come anywhere close to the magnitude of the past two bull cycles.

While we don’t have runaway inflation (yet) and we aren’t facing a closing of the gold convertibility window as Nixon did in 1971, we do have quite a few factors that should be supportive of the gold price going forward.

These include record debt and deficits, a record-high debt-to-GDP ratio, interest rates dropping toward zero, the Federal Reserve expanding its balance sheet at twice the pace it was during QE3 (just don’t call it quantitative easing!), the Fed intervening in various markets to provide emergency liquidity, a crisis in confidence in governments and political unrest worldwide, the potential for the impeachment of the United States president, elevated geopolitical tensions between world powers, a global de-dollarization movement that is accelerating, slowing economic growth, historically overvalued equity markets, a record low commodity-to-equities ratio and record-high total stock market cap to GDP ratio.

If anything, the underlying conditions that caused the gold price to spike 20x in the 1970s could be viewed as even worse today. We have a massive derivatives issue and corporate debt problem that many view as ticking time bombs. This grand experiment with fractional reserve fiat paper money being used as a world reserve currency is likely coming to an end.

As it does, people will move toward forms of money with a limited supply that are not controlled by centralized authorities. Whether this is gold-backed money, digital currency from a tech giant or increased usage of Bitcoin for reserves and international exchange, the legacy financial system is on the way out.

Assuming another ten-year bull cycle for gold, there are just over six years left in the current move and upside of 5x to 15x the current price. In this environment, cash flows for quality mining stocks will absolutely explode and provide investors with leveraged returns. At a modest projection of just 2x leverage, there exists the potential for 10x to 30x returns in gold mining stocks over the next 5 to 6 years!

This is precisely the type of asymmetric trade that we look for at Nicoya Research. If you would like to receive our top gold stock picks, real-time portfolio, monthly newsletter, and trade alerts, you can sign up for the top-rated Gold Stock Bull subscription here. Read the original article here.

Jason Hamlin is the founder of Nicoya Research and goldstockbull.com and has published investment research for over a decade. He previously worked in data analytics for Nielsen, the world’s largest market research firm, where he consulted to Fortune 500 companies including Nestlé, Johnson & Johnson and Del Monte. Hamlin’s investment philosophy takes into account political, historical and socio-economic factors to determine macroeconomic trends and isolate the sectors that stand to benefit. He then applies fundamental and technical analysis, as well as proprietary models, to find companies that are undervalued within those sectors. Hamlin is a contrarian, cycles investor and student of Austrian economics.

Disclosure: 1) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. The author was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

Nicoya Research is not an investment advisory service, nor a registered investment advisor or broker-dealer and does not purport to tell or suggest which securities or currencies customers should buy or sell for themselves. All ideas, opinions, and/or forecasts, expressed or implied herein, are for informational purposes only and should not be construed as a recommendation to invest, trade, and/or speculate in the markets. Any investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied herein, are committed at your own risk, financial or otherwise. The information on this site has been prepared without regard to any particular investors investment objectives, financial situation, and needs. Accordingly, investors should not act on any information on this site without obtaining specific advice from their financial advisor. Past performance is no guarantee of future results. View the full disclaimer and privacy policy.

China’s central bank lowered its one-year Loan Prime Rate (LPR) by another 5 basis points to 4.15 percent, the third cut since it was designated as the new benchmark lending rate in August.

The People’s Bank of China (PBOC) also lowered the five-year LPR by 5 basis points to 4.80 percent, the first cut in this tenor since August.

The rate cut was widely anticipated as it comes on the heels of cuts to two other lending rates earlier this month and confirms PBOC’s concerted effort to lower the cost of financing throughout the banking system and boost economic activity.

On Aug. 17 PBOC reformed its mechanism for calculating LPR to improve the transmission of its policy decisions to the economy and on Aug. 20 it announced LPR for the first time under this new framework, setting it at 4.25 percent.

This was 6 basis points below the old LPR, which had been unchanged since October 2013, and 10 basis points below the previous benchmark lending rate.

Under the new policy, LPR will be announced on the 20th of each month and on Sept. 20 LPR was cut by another 5 basis points to 4.20 percent while on Oct. 20 it was unchanged.

LPR has now been cut by 16 basis points since it was designated the new benchmark lending rate, with today’s cut following a 5-basis-point cut in the 7-day reverse repo rate to 2.50 percent on Nov. 18 and a 5-basis-point cut to 3.25 percent for the medium-term lending facility (MLF) on Nov. 5.

Today PBOC said it didn’t conduct any reverse repurchase operations on Nov. 20 “due to reasonably adequate liquidity” in the banking system.

China’s economy has been slowing for the last six quarters, with annual growth in gross domestic product slowing to 6.0 percent in the third quarter from 6.2 percent in the second quarter and 6.4 percent in the first quarter of this year.

Growth in the third quarter was the weakest since the first quarter of 1992 but PBOC has been steadily loosening its monetary policy stance this year by lowering reserve requirements three times and cutting interest rates to ensure economic activity doesn’t contract further.

Most recently, PBOC Governor Yi Gang on Nov. 19 said credit support to the economy would be stepped up and lending rates would be pushed lower.

In his meeting with representatives from commercial banks, Yi also urged them to refer to LPR when issuing new loans. Meanwhile, inflation jumped to a 2019-high of 3.8 percent in October, the highest since January 2012, from 3.0 percent in September due to a surge in pork prices from an outbreak of swine fever.

Like many questions about trading profitability, the answer is far from cut and dried. There are certainly people and businesses making substantial profits with automated trading. But it also has its pitfalls and there are a lot of scams and dubious claims out there.

There are various forms of automated trading.

Starting from the most simple, for instance, is a system of triggers that informs an FX trader to buy or sell automatically. From there it goes all the way up to a fully automated trading robot that is practically hands-off.

The larger players in the marketplace have very sophisticated algorithms that make thousands of trades per minute. However, we don’t have to go that far to get into automatization. And, if you can access high-frequency trading algorithms, you’re probably not going to be reading this.

AT and EA, What’s the Difference?

Automated Trading (AT) is a broader concept that comprises most activities around the use of algorithms and automated systems in forex trading.

On the MetaTrader 4 platform, the most popular among forex traders, there are customizable programs that assist with and can do automated FX trading. These are called Expert Advisors, or EAs.

EAs have become something of a short-hand among forex traders when referring to automated trading programs. Some people use “algo” and “EA” interchangeably, even though, technically, they are not the same.

Some FX traders also use “bots” when talking about automated trading systems. But, with social trading, there’s the potential for “bots” to be confused with the social media automated accounts. So, the use of “bots” in FX trading is falling out of fashion.

What AT Can Do For You

Your forex trading platform probably has a major limitation: it only follows your instructions.

If you aren’t there, because you are human and need to do human things like eat and sleep, you might be missing out on trading opportunities.

Most trading platforms allow you to add on an additional program that will place trades for you. The program can execute your instructions far faster than you can and analyze data and respond quicker, more precisely, and less emotionally than a human.

However, the actions are only taken based on the rules and instructions programmed into it by the designer.

A savvy FX trader can use a well-implemented robotic system to facilitate their own trading procedures. This way, they benefit from both their own skills, as well as the speed and consistency provided by a computer program. Sometimes, this is called an “app” or an “algo.”

How good that program will be at squeezing a profit out of the forex market will depend almost entirely on the strategy that it is programmed to use. The mere fact that it is a robot doesn’t change the profitability of the strategy; they are not artificial intelligence.

Although some machine learning is available to major trading houses and banks, those programs are usually way beyond the means of your average FX trader. When we are talking about automated trading, we are referring generally to programs that follow preset instructions.

So, the question of profitability depends on who programmed the robot. But there are some other upsides that are worth considering, too.

Trading Programs Have Some Advantages

Forex robots or EAs can help lighten the emotional and psychological burden of trading.

A program will follow the formula regardless of an emotional state that might cause hesitation or recklessness in a human trader. This lightning-fast consistent response helps turn a favorable trade signal into a profitable outcome.

Note that it says “helps”, not guarantees. There is no way to predict the future for sure when it comes to the markets.

Computer programs also have the ability to monitor more markets and signals than a person and turn that information into action. This allows for developing more sophisticated trades, including currency triangulation and other more advanced trading strategies and techniques that are harder for a human to process quickly.

Finally, one of the biggest attractions of forex robots is the idea of setting it and leaving it to work while you don’t have to be glued to the screen. Though it should be pointed out that this is only somewhat true. You still need to keep a very close eye on your program and correct and update it regularly.

Pitfalls of Automating

If you just buy a prepackaged EA or forex robot then you are at the mercy of the system that was designed by someone else. You won’t know when to correct it or intervene.

When market conditions change, it will require updating. And, you might not even know that it’s no longer working properly until your account balance has shrunk significantly!

On the other hand, if you create and maintain the system yourself, it requires a lot of work to set up, test and keep up to date with the changing marketplace. Also, you can’t code a successful forex trading strategy without first developing a tried and tested successful strategy. (Well, technically you can, but who wants a trading robot that doesn’t make money?)

Buyer Beware

There are a lot of people out there selling trading systems or forex robots. Most of them won’t turn a profit if bought by someone with little knowledge or experience in FX trading themselves.

This is unfortunate since one of the appeals of a trading robot is getting to use more advanced systems that other traders have, without having to spend a lot of time learning.

Even the ones that do initially prove profitable in the short term will become obsolete rather quickly. Obsolete systems mean losing money. So, it’s a good idea to beware of sales pitches that sound too good to be true. Particularly when they promise a large reward for very little effort.

The Bottom Line

Automation works best when you use it as a tool to assist your forex trading strategy. It has a hard time replacing you as a trader, but it can help you achieve greater consistency in your execution.

On the other end, it can also multiply the results of a winning strategy that you are already using. Small advantages make a big difference in your profitability at the end of the day when it comes to forex.