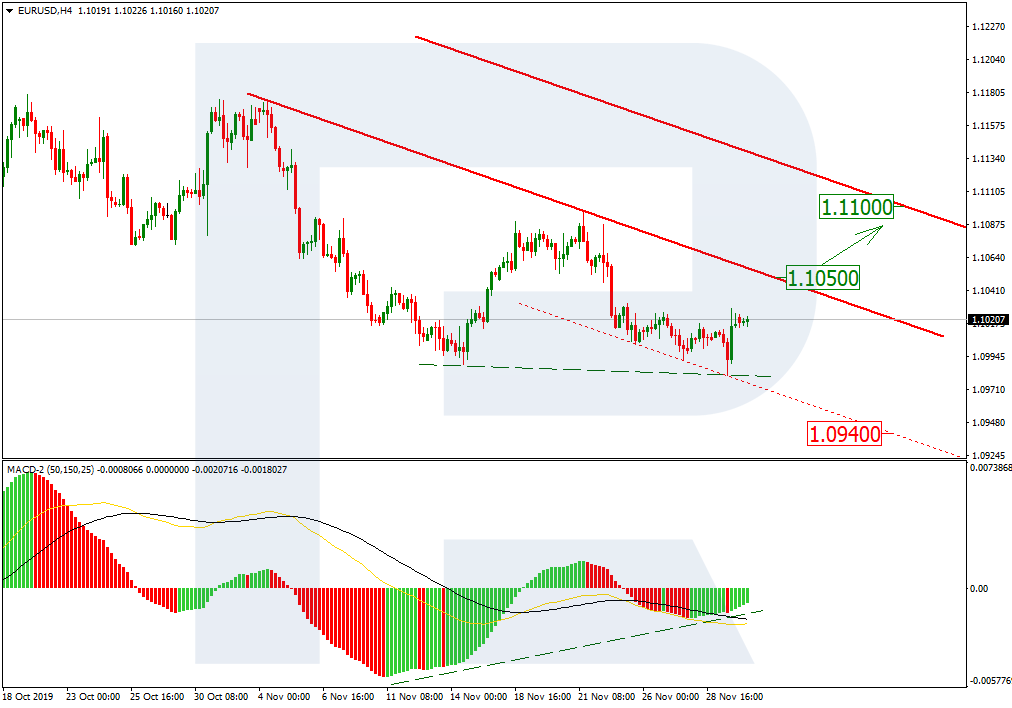

Early in December, the major currency pair is trading calmly – everything is getting back to normal after a pause on the occasion of Thanksgiving Day in the USA. On Monday, December 2nd, EUR/USD is mainly trading around 1.1020.

Investors are still focused on the US-China trade talks, a pause in which may last for a long time. it is already known that Beijing hasn’t taken any countermeasures in response to the “Hong Kong Human Rights and Democracy Act” passed by the USA earlier. It means that China decided not to exacerbate relations with its trade partner and was very serious about continuing negotiations through diplomatic channels.

However, November has gone by and now it’s already December, but there is still no new information about this. There is a possibility that the trade agreement or at least its first phase won’t be signed this year. This, in its turn, may later increase the market volatility and count against the Euro.

On the last Friday of November, EUR/USD managed to update its previous low, but then the news made the pair start a pretty strong rising correction. In the H4 chart, there is a divergence on MACD, which may indicate a new tendency to the upside. However, to confirm the tendency reverse from descending to ascending, the price must break the resistance line of the current trend at 1.1050. If it happens, the pair may continue growing towards 1.1100. Still, an opposite scenario is also possible: the instrument may rebound from the resistance line and fall to reach the support level at 1.0940.

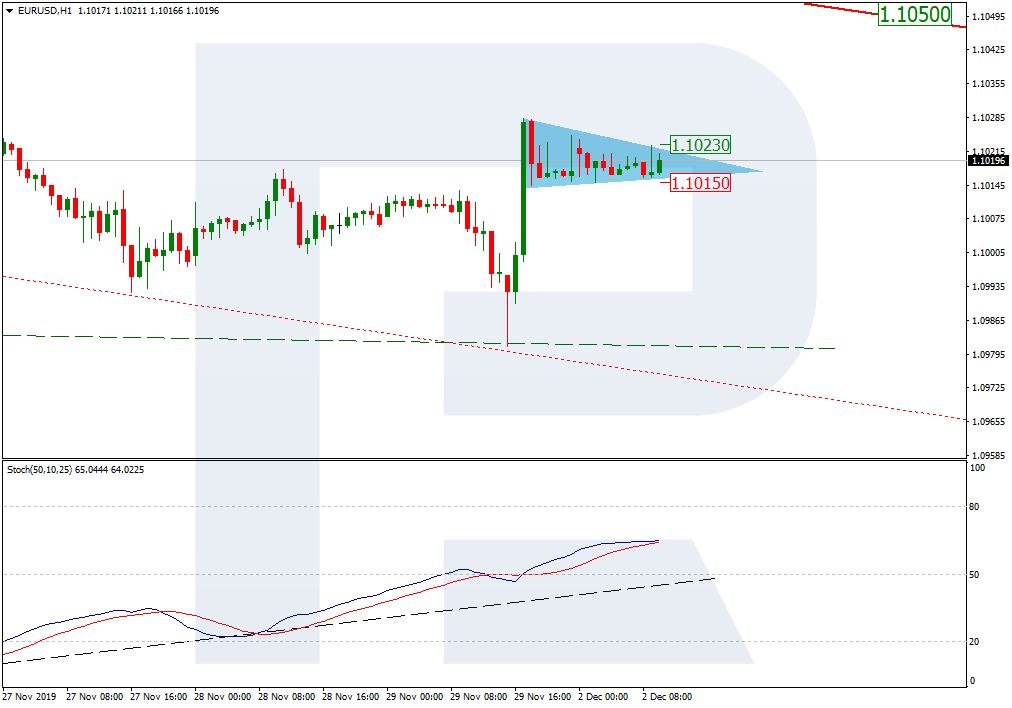

As we can see in the H1 chart, after finishing the rising impulse, EUR/USD is forming a correction in the form of Triangle. In this case, the resistance line is at 1.1023. If the price breaks this level, it may continue growing towards the next resistance level. A convergence on the Stochastic Oscillator confirms the new-rising-tendency scenario.

Disclaimer

Any predictions contained herein are based on the authors’ particular opinion. This analysis shall not be treated as trading advice. RoboForex shall not be held liable for the results of the trades arising from relying upon trading recommendations and reviews contained herein.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

Investors kicked off the last month of the year in a positive mood. Stocks across Asian markets traded in the green on Monday with 10-year US Treasury bonds back above 1.8% and the Yen retreating slightly against the US Dollar.

The risk-on mood was driven by better than expected economic figures out of China. The Caixin/Markit manufacturing Purchasing Manager’s Index rose to 51.8 in November, marking the fastest expansion in activity since December 2016. Meanwhile, the official manufacturing PMI released over the weekend returned to growth for the first time in seven months and crucially above the 50 threshold. Monetary stimulus and declining trade tensions have been major factors in improving the figures, but whether the economy has hit a bottom really still depends on the outcome of US-China trade negotiations. That said, China PMIs lead global PMI by a few months and China drives one-third of global GDP growth so there seems to be some light on the horizon.

US Jobs report

After three interest rate cuts implemented since July in 2019, the Fed signaled it would be on hold. Unless we see further deterioration in economic data, there isn’t a reason to justify another easing move in the near term. Friday’s jobs report is expected to show nonfarm payrolls increased by 180,000 as seasonal hiring picks up and 45,000 GM workers return to their jobs following a long strike. Average earnings are expected to have improved slightly in November and unemployment to remain steady at 3.6%. Barring any surprises, the figures may justify Fed Chair Jerome Powell’s assessment that the economy still has room to continue its current expansion.

Investors will also keep a close eye on ISM data which should receive a lift from optimism around US-China trade deal expectations. Jobs and ISM figures are going to be key components for a December rally in stocks.

UK Election

Sterling has been stuck in a range of 1.28 – 1.30 as traders struggle to forecast the result of the December 12 election. Traders seem reluctant to make big bets despite the latest YouGov poll showing that the Conservative party is expected to win its biggest majority since 1987. The opposition Labour party is trying to sway voters by driving fears about the future of the National Health Service if the UK strike a trade agreement with the US.

The latest poll from BMG Research showed the Conservative’s lead slipping 2% to 39%, while the Labour party gained 5% to narrow the gap to just a 6-point lead. The mixed poll results are making it difficult to predict the election outcome. However, any signs of the gap narrowing further will be bad news for Sterling bulls.

Central Bank Meetings

The Bank of Canada and the Reserve Bank of Australia are set to announce rate decisions this week. Both are expected to keep interest rates unchanged, but we shouldn’t completely rule out the chances of a rate cut.

Canada has seen its economic growth weakening significantly in the third quarter as global demand has fallen. More surprisingly, jobs unexpectedly declined in October losing 1,800 jobs against expectations of a rise of 15,900. Australia shares a similar story with a weakening labour market and inflation below target. If we don’t see a rate cut this week expect the two central banks to be on the more dovish side.

OPEC meeting

Oil traders will finally get some questions answered on OPEC policy. Whether we’ll see an extension or deepening of production cuts for 2020 will be known this week. The deal of 1.2 million barrels per day of supply cuts will expire by the end of March 2020. However, global inventories are still expected to rise in the first half of next year due to weak demand and more supply from countries outside of OPEC, in particular, from the US. For prices to move above the recent range of $55 – $65, we will need to see OPEC+ take bolder action, such as further cutting production targets. However, given that the compliance rate is low from some key players such as Russia, it seems getting deeper production cuts will be a difficult task.

Expect oil price volatility to increase this week with risks tilted to the downside. Any outcome, other than stricter compliance or deeper production cuts, is likely to increase selling pressure.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stocks closed lower on Friday after reopening for a shortened session following Thanksgiving holiday. The S&P 500 slid 0.4% to 3140.98, rebounding 1% for the week. Dow Jones industrial slipped 0.4% to 28051.41. The Nasdaq fell 0.5% to 8665.47. The dollar weakening accelerated despite reports online sales on Thanksgiving were up 20% from a year ago. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, slipped 0.1% to 98.25 but is higher currently. Futures on three main US stock indices indicate higher openings today.

FTSE 100 led European indexes losses

European stock indexes extended losses on Friday. GBP/USD joined EUR/USD’s climb on Friday as data showed the eurozone’s annual rate of inflation rebounded in November after two straight months of decline. Both pairs are gaining currently. The Stoxx Europe 600 Index lost 0.4% . The DAX 30 slipped 0.1% Friday to 13236.38 as Germany retail sales fell more than expected in October. France’s CAC 40 slid 0.1% and UK’s FTSE 100 fell 0.9% to 7346.53.

Nikkei leads Asian Indexes gains

Asian stock indices are mostly rising today following an unexpected rise in China’s manufacturing activity in November. Nikkei ended 1% higher at 23529.50 as yen resumed its slide against the dollar. China’s markets are rising s China’s official manufacturing purchasing managers index topped 50 the first time since April: the Shanghai Composite Index is 0.1% higher and Hong Kong’s Hang Seng Index is up 0.2%. Australia’s All Ordinaries Index recovered 0.2% despite Australian dollar’s resumed climb against the greenback.

Brent futures prices are recovering today. Prices fell on Friday after reports casting doubt on possible production-cut extension at this week’s OPEC meeting: Brent for January settlement lost 2.3% to $62.43 a barrel Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The perceived pros and cons of the transaction are provided in a CIBC report.

In a Nov. 25 research note, analyst Cosmos Chiu reported that CIBC downgraded its rating to Neutral and lowered its target price to CA$60 per share from CA$73 (current share price CA$55.79) on Kirkland Lake Gold Inc. (KL:TSX; KL:NYSE) due to the increased risk associated with the miner’s agreement to acquire Detour Gold Corp. (DGC:TSX). The transaction is expected to close in Q1/20.

Chiu pointed out that another potential downside to the deal is that it could cause a slowdown in Kirkland Lake’s current efforts to optimize its operations, the Fosterville and Macassa projects, and hamper progress with its Macassa mine.

The major benefit of the transaction, Chiu noted, however, is it will expand Kirkland Lake’s project portfolio. “Long term, we see the merits of this acquisition, by adding a third cornerstone [open-pit] mine to the asset base and potentially creating a Canadian champion,” he added.

With the acquisition, Kirkland Lake’s reserve base will jump to 21 million ounces (20 Moz) from 5.75 Moz. Its production will increase in 2020 to 1.621 Moz from 1 Moz. However, the all-in sustaining cost will rise in tandem, to CA$773 per ounce from CA$564 per ounce.

Merging the two companies is estimated to result in about CA$75100 million of pre-tax synergies per year.

The analyst reviewed the terms of the acquisition agreement. All outstanding Detour Gold shares will be exchanged for Kirkland Lake shares at a ratio of 0.4343 Kirkland share to 1 Detour share. Accordingly, when the deal closes, existing Kirkland Lake shareholders will own about 73% of the company, and Detour Gold shareholders will own about 27%.

Chiu concluded that “while the proposed acquisition of Detour Lake is a change from Kirkland Lake’s previous focus on high-grade underground operations, it adds a long-life Canadian producing asset that should help the company deliver continued free cash flow growth in the future.”

Next, Kirkland Lake will announce results from its exploratory drilling at Fosterville. Those are expected by year-end 2019.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from CIBC, Kirkland Lake Gold Ltd., Ratings Change, November 25, 2019

Analyst Certification: Each CIBC World Markets Corp./Inc. research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein accurately reflect such research analyst’s personal views about the company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Analysts employed outside the U.S. are not registered as research analysts with FINRA. These analysts may not be associated persons of CIBC World Markets Corp. and therefore may not be subject to FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets Corp./Inc. are compensated from revenues generated by various CIBC World Markets Corp./Inc. businesses, including the CIBC World Markets Investment Banking Department. Research analysts do not receive compensation based upon revenues from specific investment banking transactions. CIBC World Markets Corp./Inc. generally prohibits any research analyst and any member of his or her household from executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World Markets Corp./Inc. generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report, CIBC World Markets Corp./Inc. may have a long position of less than 1% or a short position or deal as principal in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Kirkland Lake Gold Ltd. (KL)

2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services from these companies in the next 3 months: Kirkland Lake Gold Ltd.

7 CIBC World Markets Corp., CIBC World Markets Inc., and their affiliates, in the aggregate, beneficially own 1% or more of a class of equity securities issued by these companies: Kirkland Lake Gold Ltd.

For important disclosure footnotes for companies mentioned in this report that are covered by CIBC World Markets Inc., click here: Disclaimers & Disclosures.

“The sale is a positive for the company as it improves its balance sheet and allows the company to refocus on its Mexico asset,” highlighted Reagor. Also, the transaction should “remove some holding costs and general and administrative expenses from future expenses.” The resulting cash infusion should help improve Avino’s overall valuation.

According to the agreement, Reagor relayed, the total consideration for the asset will include about $6.6 million in cash, 9.9% of Talisker’s outstanding shares following an announced financing, a 50% warrant coverage and a $2.5 million cash payment if and when Talisker starts commercial production at Bralorne. Reagor noted that the deal terms appear fair and in line with the value ROTH assigned the project.

ROTH has a Buy rating and a $1.25 per share price target on Avino. The stock is now trading at around $0.71 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Avino Silver & Gold Mines Ltd., Company Note, November 22, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Avino Silver & Gold Mines Ltd. and as such, buys and sells from customers on a principal basis.

Shares of Avino Silver & Gold Mines Ltd. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

Within the last twelve months, ROTH has received compensation for non-investment banking securities-related services from Avino Silver & Gold Mines Ltd.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

The thesis for investing in this company is provided in a Raymond James report.

In a Nov. 21 research note, analyst Pavel Molchanov reported that Raymond James initiated coverage on Ameresco Inc. (AMRC:NYSE) with a Strong Buy rating and a $20 per share target price. The stock’s current share price is around $16.35.

Molchanov reviewed the key aspects of this large U.S.-based energy service company with a footprint in all 50 states. One is that Ameresco is a “one stop shop for energy efficiency” and the only pure play in the space, affording “investors unique leverage to the efficiency theme.”

Two, Ameresco’s business lines are diverse as are its customers, which are commercial entities and public and nonprofit institutions, Molchanov highlighted. One service the company provides is implementation of energy efficiency solutions, for which it receives revenue upfront. Other recurring revenue comes from operations and maintenance.

The fact that buildings are projected to be a major component of the energy efficiency trend in the future is significant, Molchanov purported. An estimated 45% of U.S. construction companies plan to have 60%-plus “green building” projects by 2021, up from 32% in 2018. Part of this is cities and states mandating energy efficiency in buildings.

A third revenue source for Ameresco is its expanding portfolio of solar power and landfill gas assets, an area of current growth focus for it. “This in-house capacity buildout requires more capital deployment, but the result is a more predictable and higher-margin revenue mix,” Molchanov noted.

Ameresco’s future revenue growth and EBITDA look good, with growth expected to be mainly organic with a small portion resulting from mergers and acquisitions. In 2020 and 2021, the company should achieve attain an EBITDA increase of 10% and organic revenue growth of 7%, according to Raymond James. Both metrics increased since 2014 at a compound annual growth rate of 8% and 19%, respectively.

Molchanov concluded, “While Ameresco’s strategy heightens the level of capital intensity, the story’s appealing and differentiated aspects lead us to initiate coverage.”

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Raymond James, Ameresco Inc., November 21, 2019

ANALYST INFORMATION

Analysts Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination, including quality and performance of research product, the analyst’s success in rating stocks versus an industry index, and support effectiveness to trading and the retail and institutional sales forces. Other factors may include but are not limited to: overall ratings from internal (other than investment banking) or external parties and the general productivity and revenue generated in covered stocks.

The analyst Pavel Molchanov, primarily responsible for the preparation of this research report, attests to the following: (1) that the views and opinions rendered in this research report reflect his or her personal views about the subject companies or issuers and (2) that no part of the research analyst’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views in this research report. In addition, said analyst(s) has not received compensation from any subject company in the last 12 months.

RAYMOND JAMES RELATIONSHIP DISCLOSURES Certain affiliates of the RJ Group expect to receive or intend to seek compensation for investment banking services from all companies under research coverage within the next three months.

Additional Risk and Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available here.

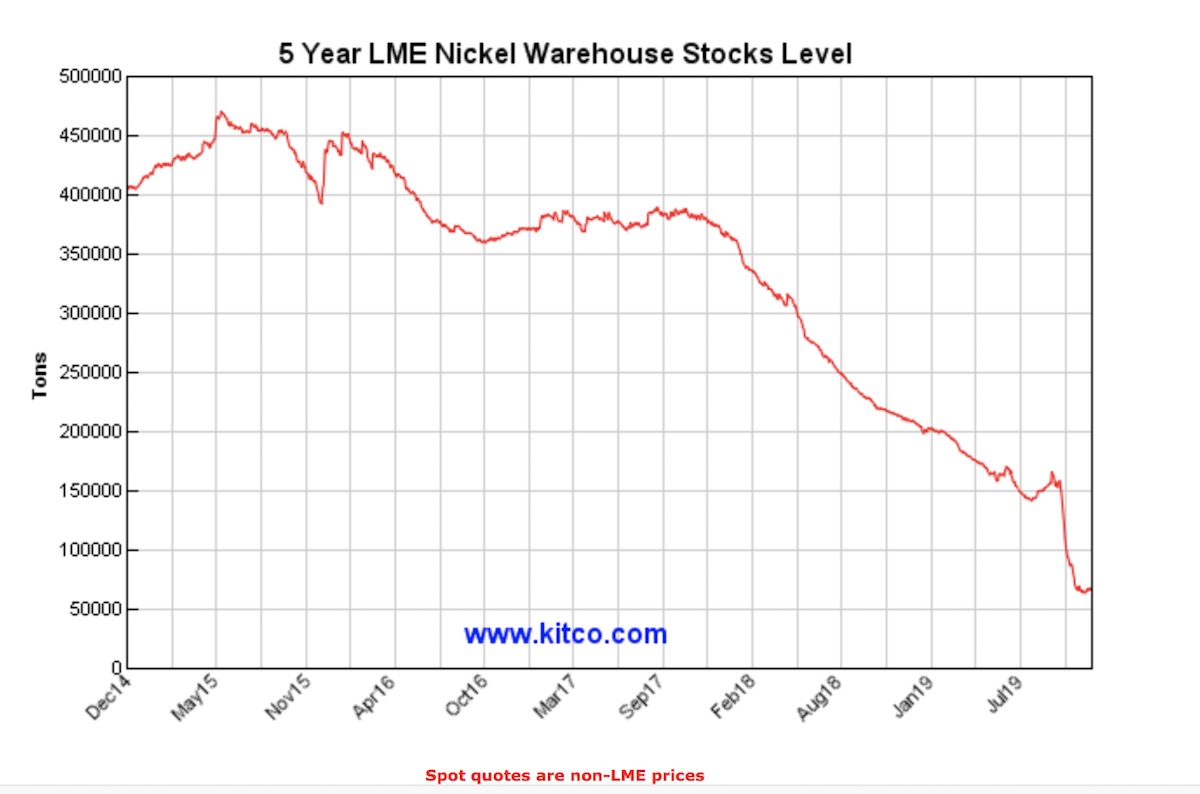

Bob Moriarty of 321gold discusses the Indonesian government’s actions in the nickel market and how they might affect a company with a project in Norway.

As the world’s largest producer of nickel, the actions of the Indonesian government not only affect those companies working in Indonesia but also half way around the world.

In 2014 the country restricted the export of nickel concentrate in an effort to force producers to construct smelting plants in the country. As a result production dropped from 400,000 tons a year to 100,000. In 2017, Indonesia relaxed the export regulations on the export of low-grade nickel in an effort to stimulate their flagging economy.

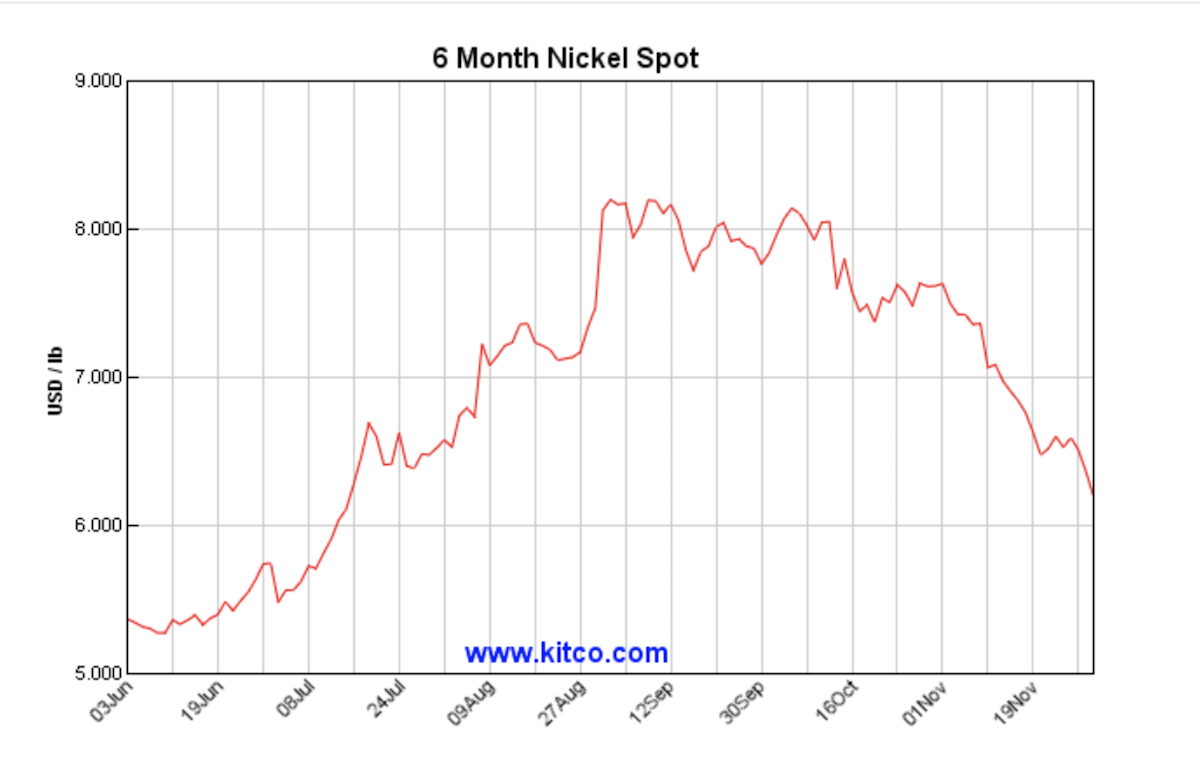

The actions of Indonesia regarding permission to export nickel concentrate have caused great confusion in the nickel market with warehouse stocks of nickel dropping almost 90% and the price of the metal bouncing up and down.

No one is certain what the Indonesian government will do next but their convoluted behavior has opened new opportunities along with new danger in the nickel market.

Playfair Mining Ltd (PLY:TSX.V) is a micro-junior with aspirations to advance three base metals projects in Norway. The company announced an option on March 1st of 2019 to pick up 100% of three contiguous nickel/copper/cobalt properties in an historic mining district in south central Norway. The terms are a little convoluted but basically say that Playfair will issue over time 9.9% of their shares and spend a certain amount of money in exploration to own 100% of the projects subject to a 3% NSR.

What Playfair calls their RKV target included two past producing copper VMS mines and a nickel/copper deposit with an historic, non-43-101 resource of 400,000 tons of nickel and copper. The gross metal value in the non-43-101 resource produced by Falconbridge based on 109 drill holes would total about $64 million. So it is an indication of potential.

VMS deposits tend to occur in clusters so finding a group of them in an area is an indication that there easily could be more. And their nickel target already had a significant resource albeit historic but from one of the giants in the industry, Falconbridge.

Playfair has done what they said all along they would do. Their next step is to conduct a scout drill program where drill results will dictate what happens next. With a $3.2 million market cap, there just isn’t much of a risk to the stock. It either goes to zero or up a lot.

Playfair is an advertiser. I have participated in the last PP and I look forward to the upcoming drill program. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Playfair Mining. Playfair Mining is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

By CentralBankNews.info The Central Bank of the Dominican Republic (BCRD) left its monetary policy rate steady at 4.50 percent for the third month, saying domestic demand is continuing to react favorably to the expansive monetary policy measures it has taken since June and energized private credit, which has risen 11 percent so far this year and 12 percent in the last 12 months. BCRD cut its policy rate three times in a row by a total of 100 basis points in June, July and August and released more than 34 billion Dominican peso in legal reserves to productive sectors. Economic activity has improved with growth of 5.2 percent year-on-year in October following 5.1 percent growth in September for average growth in the first 10 moths of 4.8 percent. “The dynamism that economic activity has registered in recent months will contribute to economic growth of around its 5.0 percent potential by the end of the year, ” BCRD said, confirming its forecast from September after a monetary policy meeting on Nov. 29. Inflation in the Dominican Republic rose to 2.48 percent in October from 2.02 percent in September but remains below BCRD’s lower limit of its target range of 4.0 percent, plus/minus 1 percentage point. The Dominican peso fell fast between mid-September and mid-October but since then it has firmed slightly. Today it was trading at 52.9 to the U.S. dollar, down 4.7 percent this year. The central bank said the exchange rate had been relatively stable, depreciating less than the average Latin American currency and emerging economies due to the strength of macroeconomic fundamentals and the credibility of economic policies.

This week – December 1 through December 7 – central banks from 7 countries or jurisdictions are scheduled to decide on monetary policy: Australia, Namibia, Poland, Canada, Chile, India and Botswana.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

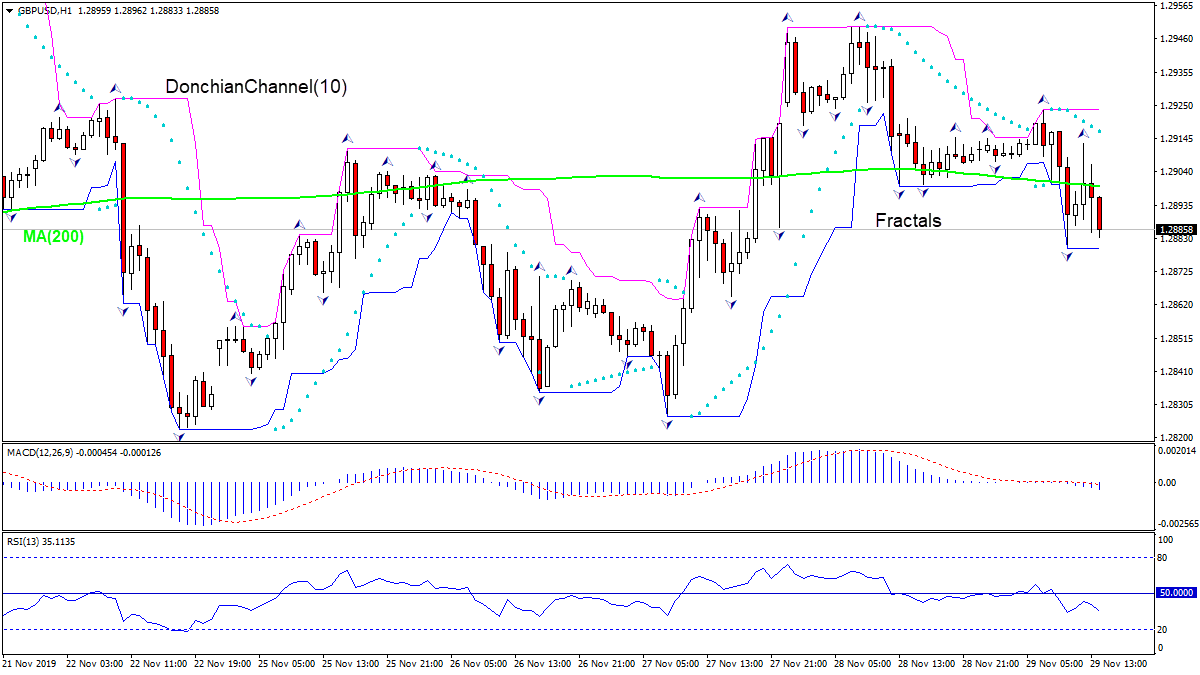

Britain’s M4 money supply (currency in circulation plus money in bank accounts) was unchanged in October after 0.2% increase over month in September. Will the GBPUSD rise?

The price chart on 1-hour timeframe shows GBPUSD: H1 is trading sideways. The price is testing the 200-period moving average MA(200) which is falling. And the RSI oscillator is below 50 level and has not reached the oversold zone. There is no trend yet formed, traders have to decide when it would be a best time to enter the market.