By CentralBankNews.info Georgia’s central bank left its benchmark refinancing rate steady for the first time since after four consecutive rate hikes after the exchange rate of the lari strengthened but said it would maintain a tight monetary policy stance inflation expectations decline to its 3.0 percent target. The National Bank of Georgia (NBG) raised its rate four times from September to December last year by a total of 250 basis points to curb inflation from the fall in the lari, which depreciated 10 percent from the start of 2019 until late November. But in early December the lari began to strengthen, taking some of the pressure off inflation, but NBG said the “nominal effective exchange rate remains undervalued.” After rising 4 percent between Dec. 8 and Dec. 14, the lari eased again and was trading around 2.90 to the U.S. dollar today, down 1.4 percent since the start of this year. “In recent periods, economic growth accelerated and lending is robust,” NBG said, adding “if these dynamics create additional inflationary pressure, the tight monetary policy stance may be maintained for more extended period.” Georgia’s inflation rate was steady at 7.0 percent in December and November but is still the highest rate since June 2016. The central bank expects inflation to decline at the start of 2020 but first begin to approach its 3.0 percent inflation target by the end of the year, a decline it said “will be ensured by the monetary policy which will remain tight until the medium term inflation expectations decline to the three percent target.” In December the International Monetary Fund (IMF) approved another $41.4 million loan to Georgia, its sixth under a 3-year program of just under $300 million, saying this should help authorities maintain policy discipline and help advance structural reforms. The IMF said the recent rise in inflation reflected both temporary factors and the impact of the lari’s depreciations, and said the NBG’s tightening was appropriate as it addressed inflationary pressures. But IMF also said exchange rate flexibility remains “vital as a shock absorber” for Georgia’s economy and interventions should be limited to addressing excessive volatility or building reserves. The IMF forecasts average inflation this year of 4.5 percent, down from 4.9 percent in 2019, and economic growth of 4.3 percent in 2020, down from 4.6 percent in 2019.

The National Bank of Georgia issued the following statement:

“The Monetary Policy Committee (MPC) of the National Bank of Georgia (NBG) met on January 29, 2020, and decided to keep the refinancing rate unchanged at 9.0 percent.

In December, annual inflation equalled 7.0 percent. In addition to the one-off factors from early 2019, the nominal effective exchange rate depreciation had a significant impact on inflation. In response, to neutralize inflationary pressures stemming from the exchange rate depreciation, from September 2019, the NBG began tightening its monetary policy stance. In December, the nominal effective exchange rate strengthened slightly, which reduced the pressure on inflation. However, the nominal effective exchange rate remains undervalued. In recent periods, economic growth accelerated and lending is robust. If these dynamics create additional inflationary pressure, the tight monetary policy stance may be maintained for more extended period.

According to the NBG forecast, other things being equal, the inflation will start to decline from the beginning of the year and approach the target by the end of the year. This will be ensured by the monetary policy which will remain tight until the medium term inflation expectations decline to three percent target.

Meanwhile, the exports and remittances revealed moderate growth, and, despite the decline in summer, the annual change in tourism revenues became positive since October 2019. It is noteworthy that in 2019, similar to 2018, the current account improved significantly.

The NBG will continue to monitor the developments in the economy and financial markets and will use all means and instruments at its disposal to ensure price stability.

The next meeting of the Monetary Policy Committee is scheduled on March 18, 2020.”

The US dollar has been helped higher once again this week, ahead of the FOMC later today. Yesterday, the conference board consumer confidence index printed a robust 131.6 reading against the prior and expected figure of 128.2. This latest reading, which is the best since August 2019, is not too far off the cycle higher of 137.9 (October 2018). This has seen the USD index well bid over the last 2 sessions.

The breakdown of the data shows the reading was driven by solid gains in both the present situation component as well as the expectations component. The Conference Board said that the gain was:

“driven primarily by a more positive assessment of the current job market and increased optimism about future job prospects”.

Labour Market Driving Confidence Gains

The explanation from the Conference Board once again puts emphasis on the strength in the US labor market. Unemployment is currently sitting at its lowest levels since the 1960s. This, combined with record highs in both home and equity prices and much-lower gasoline prices, is creating an encouraging environment for consumers.

Wage Growth Receding

Despite the strength in the labor market, however, one area where strength is not being seen is wage growth. The latest reading showed wage growth fell back to 2.9% year on year. This is despite having nearly been as high as 4% last year. The takeaway here is that, if the US economy is going to see the type of increase in consumer spending which is typical for this level of consumer confidence, households will have to start mobilizing their savings, as wages are not growing.

Corona-Virus Impact Not Accounted For

It is also worth noting that the cut off period for this latest CB consumer confidence reading was January 15th. This means that the survey period does not account for the period covering the corona-virus outbreak. In terms of impact so far, we have seen equities moving lower as risk sentiment weakens.

However, this correction could deepen as the outbreak spreads and could present a major headwind to the US economy in the early part of this year. It will certainly be interesting to see how the Fed addresses the outbreak at the FOMC later today given that it is presenting an opposing force to the positive pressure from the signing of the US/China trade deal.

Technical Perspective

The US dollar index has now broken out above both the 97.42 resistance level and the bearish channel top. While above here, the focus is on a further push higher to the 98.25 level next. This is a key resistance level for the USD and is the last main level ahead of the 2019 highs around 99.33. To the downside, any break lower will likely find support into the 97.42 level with a heavy reversal needed to put any focus back on the 96.37 level.

The Federal Reserve Bank will be concluding its two-day monetary policy meeting today. Heading into the interest rate decision, the consensus is loud and clear that the Fed will not tinker with the Fed funds rate, leaving them steady at 1.50%-1.75%.

This comes as policymakers have a lot to think about, including some recent developments that will compel them to remain on the sidelines.

Most importantly, the Phase One trade deal with China gives officials some breathing room. Further trade negotiations will continue only after the US elections, meaning that trade tensions will ease. This should potentially give enough time for the US economy to pick up momentum over the course of time.

Investors will be more interested to hear about the Fed funds rate path. The Fed signaled at the December meeting that interest rates will remain steady this year.

But this could change, subject to the incoming data. Investors, on the other hand, remain cautious. There is a slight consensus that the Fed is more likely to cut rates than keep them on hold this year.

GDP growth for the fourth quarter remains anchored on average to a two percent growth rate. While this is a full percentage point lower compared to the previous quarters this year, the pace of growth is still acceptable.

However, what remains to be seen is whether other factors such as inflation and wage growth will pick up.

Economic Risks Remain Unbalanced

One of the most important factors for the Fed is the imbalance in the markets. Equities have been charting to new highs. Yet, when it comes to growth, it is a different story. The US labor market remains one of the bright spots for the Fed.

But wage growth is sluggish, rising at an annual pace of around 2.9%-3.0%. For the moment, with inflation staying sluggish, wages are outperforming inflation. But with no upside risks, this could begin to be a cause for concern among Fed officials.

Another lesser-known fact is the Fed’s open market operations. Besides injecting liquidity into the overnight markets, the central bank is also buying the US T-Bills.

Recently, Larry Kudlow, the economic adviser to President Trump made claims that the Fed purchase of T-Bills amount to nothing short than QE.

The Fed is purchasing close to 60 billion in Treasury bills every month. While policymakers maintain that this is merely a technical measure to support the monetary policy, others have a different view. The fact that the Fed’s balance sheet is also growing is another indication.

In the near term, today’s Fed meeting will be just another placeholder meeting. But things could change into the coming quarters. Investors will be keen to see if the dissipating trade tensions will revive growth.

The International Monetary Fund maintains a pessimistic view of the global economy. Furthermore, with Brexit now a very likely thing, trade with the UK and the rest of the world will also play a big role. The US has already started talks with UK counterparts.

Impact of the Fed Rate Decision

The impact of the Fed meeting is not likely to be much from a trader’s perspective. It is quite likely that the Fed will maintain a cautious tone at today’s meeting. This could potentially give rise to a flight to safety.

Gold prices are already discounting this fact, given that price hasn’t budged off the current highs. Secondly, investor concerns now focus on the impact of the Coronavirus outbreak as well. Overall, today’s Fed meeting will perhaps give a clue into where the Fed stands on the monetary policy path.

Improving German consumer sentiment bullish for EURUSD

On 1-hour timeframe EURUSDJPY: H1 is in downtrend after retracing higher following a fall to 30-month low. The price is below the 200-period moving average MA(200) which is falling itself.

We believe the bearish momentum will resume after the price breaches below the lower bound of the Donchian channel at 1.0994. A level below this can be used as an entry point for placing a pending order to sell. The stop loss can be placed above 1.1009. After placing the order, the stop loss is to be moved to the next fractal high, following Parabolic signals. Thus, we are changing the expected profit/loss ratio to the breakeven point. If the price meets the stop loss level without reaching the order, we recommend cancelling the order: the market has undergone internal changes which were not taken into account.

GfK consumer confidence index improved in Germany in January. Will the EURUSD start rising?

The US dollar has been a little firmer again over the European morning on Wednesday. The main event focus today is the FOMC meeting later in today’s US session. While the Fed is not expected to move on rates, traders will be keen to see if the Fed’s outlook has shifted at all. The recent corona-virus outbreak poses downside risks. Although, resilience in the labor market and private consumption data should keep the outlook fairly balanced. USD index trades 97.88 last.

EUR Holding at Support

EURUSD continues lower today with price testing the 1.10 level again. The level held as support yesterday though looks vulnerable to a break today if the Fed refrains from any dovishness in its outlook. It’s been a quiet week for Eurozone data with the CPI flash on Friday the only key release to note.

GBP Muted Ahead of BOE

GBPUSD continues to hug the local rising trend line ahead of tomorrow’s BOE meeting. The market is divided over whether the bank will ease, in light of recent dovish commentary and weak data. Now, with the outbreak of corona-virus, it looks like rate cut risks have increased, which could see GBPUSD move sharply below the 1.2978 support.

SPX500 Recovery Pauses

Risk assets continue to recover off the initial lows posted on the week in response to news of the growing severity of the corona-virus outbreak. Following a gap lower at the open on Sunday, which took price below the 3261.46 level, the SPX500 has since recovered to 3285.93 last. Any dovishness from the Fed today could help propel the recovery further.

JPY & Gold Higher

Safe havens have been higher again today with both the Japanese yen and gold trading higher against USD in light of the broader risk-off tone across markets. USDJPY trades 109.00 last, having found resistance as it closed the weekly gap. XAUUSD trades 1571.11 last, with price rebounding off yesterday’s lows.

API Reports Inventories Draw

Oil prices have softened a little this morning though have been higher over the last 24 hours in response to the API reporting an unexpected 4 million barrel draw. If this inventory decline is confirmed by the EIA today, that could help crude further recover off the 52.73 level. Market sits at 53.97 last, having found resistance yesterday at the weekly gap close.

CAD Helped by Crude Recovery

USDCAD has been higher today, though is down from yesterday’s highs which were capped by the 1.3207 resistance level. The rebound in crude prices has helped CAD recover somewhat and any dovishness from the Fed tonight could see the recovery gain further traction.

AUD CPI Better than Expected

AUDUSD has been a little weaker again today though the recent sell-off has stalled for now. Overnight QoQ CPI came in better than expected at 0.7% vs 0.5% expected. However, the market is still looking for an RBA rate cut in February which should keep sentiment skewed to the downside in the near term.

The US dollar index is building upon the strong patch of economic data. The index is currently seen extending gains for four consecutive sessions so far.

But the momentum could stall ahead of the FOMC meeting due later in the week. The uncertainty over the impact of the coronavirus is also keeping the USD slightly supported for now.

Euro Slips on Dollar Strength

The Euro is extending declines amid a strong economic report from the United States. The CB Consumer confidence report rose to 131.6 in January, beating estimates of a headline print of 128.2. The data for the previous month was revised higher to 128.2.

Elsewhere, the Richmond manufacturing index was also higher at 20, beating estimates of -3 and up from -5 previously.

EURUSD Likely to Bounce Off Support

The currency pair’s declines have pushed price action to the support area of the 1.1000 region. We expect prices to consolidate around this level in the near term. Following which, as long as there is no further declines, the EURUSD could be looking to correct in the near term.

The correction could be limited to 1.1051 or possibly back to the breached support level of 1.1072.

Sterling Continues to Remain Weak

The pound sterling remains biased to the downside as the bearish momentum is strong. Economic data from the UK remains sparse ahead of the BoE meeting later in the week.

The currency pair lost over 0.50% intraday basis. Following the January 31st deadline, the UK and the EU will enter an 11-month transition period to chalk out the finer details.

GBPUSD Could Retest the Support at 1.2960

The current bearish momentum in GBPUSD indicates that the currency pair could slip to the support area of 1.2960. If we see a rebound in prices, then the GBPUSD could likely be forming a head and shoulders pattern.

This could turn out to be quite bearish for the pound sterling. For now, the retracement off 1.2960 support will be important.

Gold Prices Retreat on Strong US Data

The precious metal was giving up the gains made earlier in the week. The declines were set off by economic data from the US which also saw a strong durable goods orders report. Headline durable goods orders rose 2.4% on the month despite a 0.1% decline on the core.

XAUUSD Declines Could be Limited in Scope

Despite the retracement in the XAUUSD, price action could be limited to the price level of 1562. If support can be formed here, we expect prices to rebound once again.

But a lot will depend if the XAUUSD will be able to progress higher. To the upside, the resistance level of 1594 remains in place.

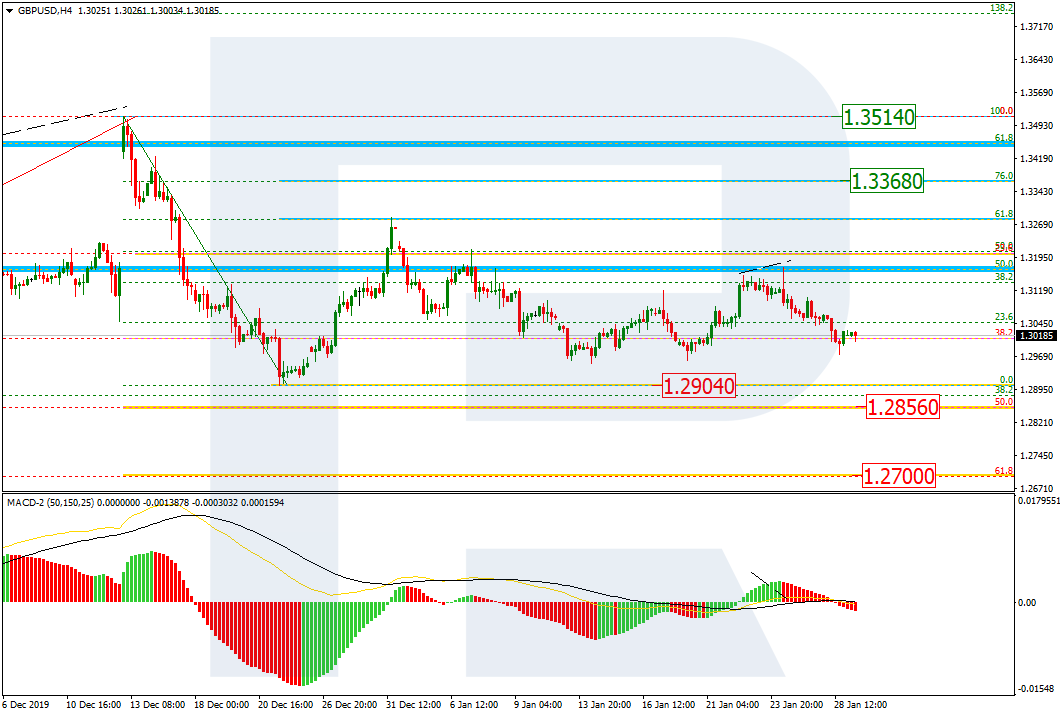

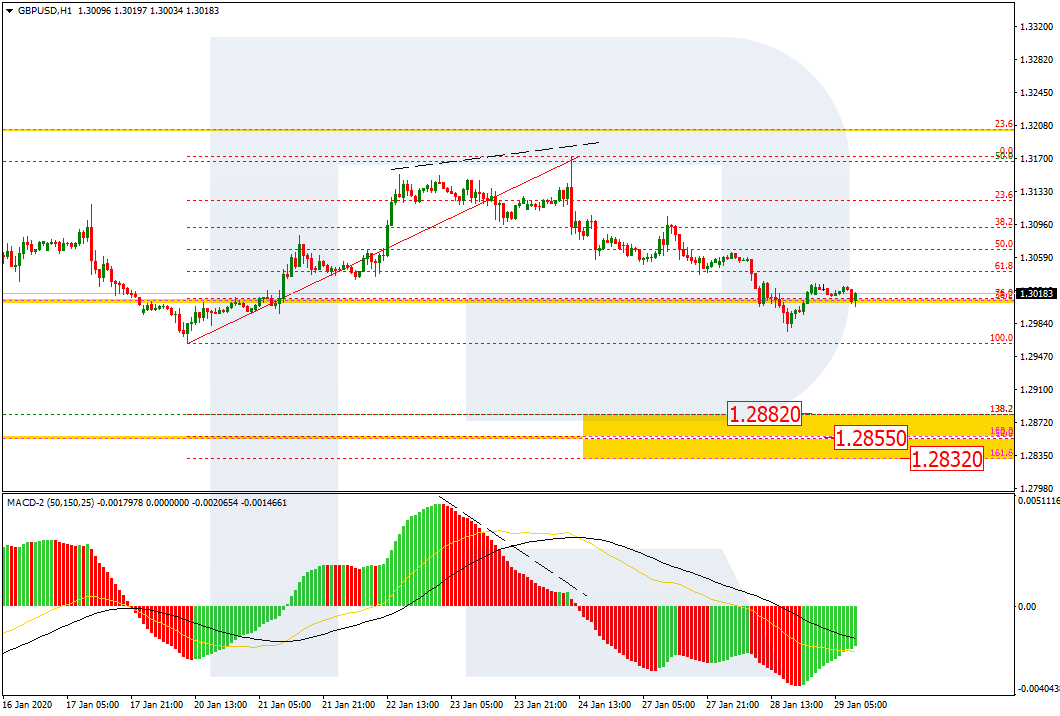

As we can see in the H4 chart, GBPUSD is still correcting and forming Triangle pattern. After attempting to break the resistance, the pair is returning to 38.2% fibo at 1.2883. The downside target is the low at 1.2904. If the price breaks this level, the instrument may continue falling towards 50.0% and 61.8% fibo at 1.2856 and 1.2700 respectively.

The H1 chart shows a new descending wave after the divergence on MACD. The price is moving towards mid-term 50.0% fibo (1.2855), which is inside the post-correctional extension area between 138.2 and 161.8% fibo at 1.2882 and 1.2832 respectively.

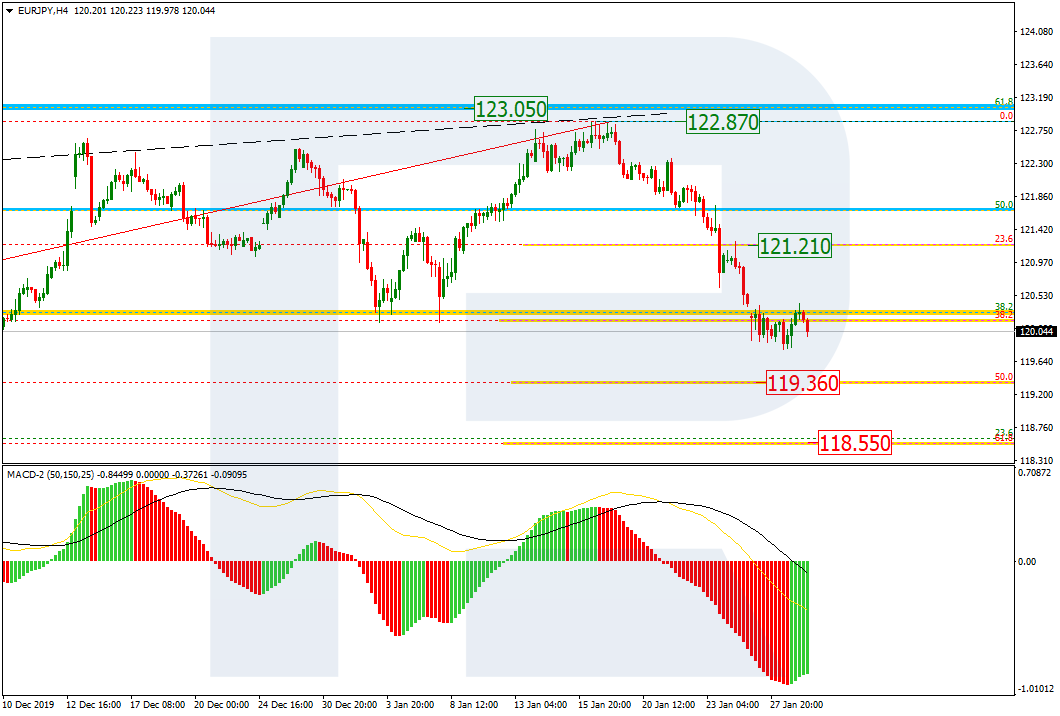

EURJPY, “Euro vs. Japanese Yen”

As we can see in the H4 chart, the correctional downtrend has stopped at 38.2% fibo. After testing and breaking this level, the decline may continue towards 50.0% and 61.8% fibo at 119.36 and 118.55 respectively. The resistance is at 121.21.

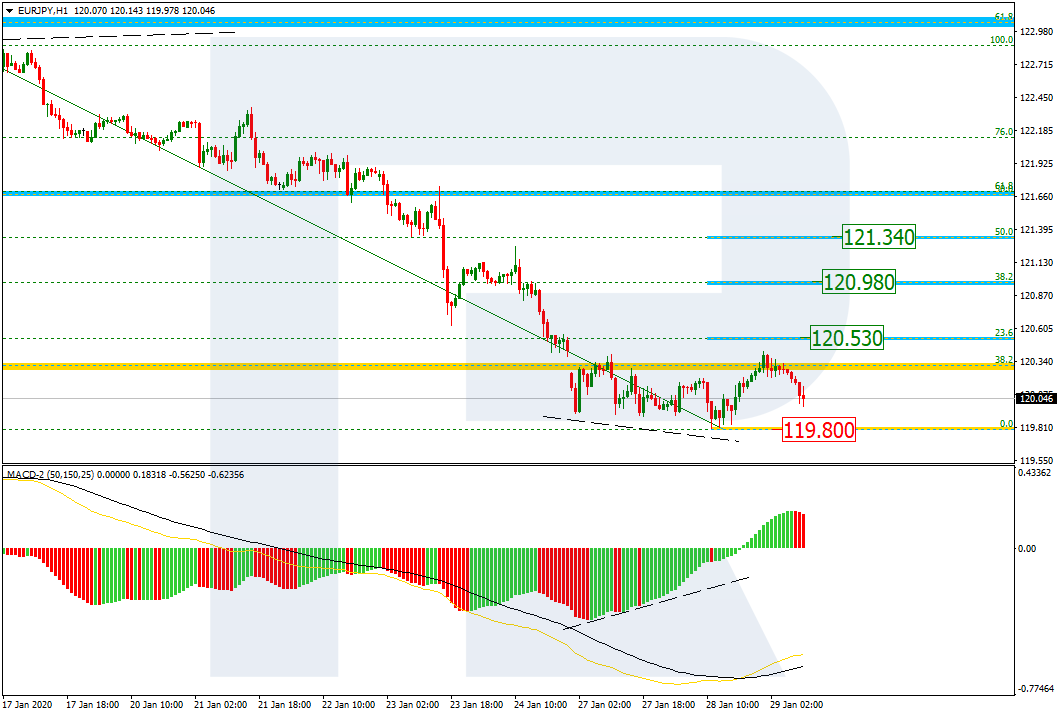

The H1 chart shows a new pullback after the convergence on MACD. The targets are 23.6%, 38.2%, and 50.0% fibo at 120.53, 120.98, and 121.34 respectively. The support is the low at 119.80.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Bob Moriarty of 321gold reflects on how government actions in the financial and public health spheres will pop market bubbles.

The “Everything Bubble” just burst. Here’s why.

I was in Vietnam from July 1968 until March 1970. From November 1968 until July 1969 I was flying the O-1 Birddog as a forward air controller (FAC). Back then I used to believe all the bull our government puts out. Now, when Trump says the Iranians fired missiles at a US base in Iraq and none of our troops were injured, I know at once he was lying. And sure enough, two weeks later we find that 34 soldiers were injured.

Governments lie about everything and as a result we are about to pay a terrible price. All of them lie.

As a FAC I controlled hundreds of air strikes and artillery missions in the belief I was helping protect the lives of the Marines and soldiers below. Compared with weapons systems of today what we did was primitive. We had to have the fixed-wing ordinance-carrying aircraft find us. We had to identify them and they had to identify us. Then we had to talk them into where they were to attack. It was vital to use exactly the correct terminology. It was easy to confuse the high-speed fixed-wing aircraft if you didn’t use words as they should be used.

Does the word “right” mean direction or does it mean “correct?” In the fog of battle you might tell an aircraft to attack on a heading of 355 and to pull off left to avoid high terrain covered in cloud.

If he responded, “Pull off left?” because he didn’t fully understand your instructions, and you respond, “Right,” don’t be real surprised if he makes a right hand pullout and hits the mountain because you used the wrong word. If you had said “correct,” he would not have been confused.

All of last year I was calling for a major correction. My belief that the bubble would burst in October was based on everything I saw. October came and went without a correction and certainly not a crash. I may have been “left,” but for certain I wasn’t “wrong.” Wrong and left both being the opposite of right.

I’ve called market turns in the past correctly. In January of 2008 I forecast a market crash in the fall. It happened just as I forecast. I called the top in silver to the day in 2011 and just a year ago called a stock market rally to the day at Christmas. Lots of other writers would love to throw rocks at me who have never managed to call anything correctly. I’ve made a lot of accurate calls. But actions of the Fed postponed the October crash.

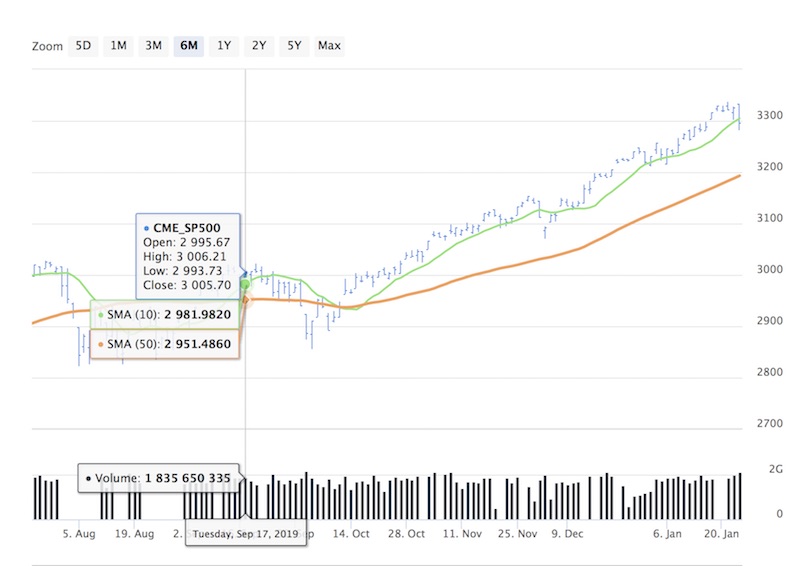

On the 17th of September the Fed panicked and began Not-QE, pumping billions of dollars into the Repo market. Clearly the money had to go somewhere. It found a home in the major markets just as the Fed wanted. If you look at the chart above, the market started a massive climb without a correction about the first of October, continuing until a few days ago.

That pile of cash postponed the “Everything Bubble Crash,” but for certain did not eliminate it.

The Fed began its journey down the rabbit hole in 2008. That was the last opportunity to allow the system to heal itself. Banks that caused the problem should have been allowed to die a merciful death, as they so justly deserved. But due to political pressures, losses were socialized and profits privatized. We have been in something right out of Kafka and Lewis Carroll ever since.

A simple concept exists in physics that everyone who wants to understand how the world works needs to understand. That concept is of entropy. Everything in the universe moves from order to disorder. Including financial systems.

Since 2008 the world’s financial system has been pushed, prodded and manipulated by all of the central banks to the point it is simply out of control. The system is so unstable that even a tiny straw would be sufficient to break the back of the system. That’s what I saw a year ago and predicted would burst the “Everything Bubble” at last. I may have been left but I wasn’t wrong. The Fed managed to push the system into even more disorder, which is now visible to everyone and anyone with a room temperature IQ or a lick of financial sense.

The coronavirus coming out of Wuhan is going to pop the “Everything Bubble.” It would be wrong to think of it as a minor pinprick. With somewhere between 35 and 50 million people in China already under quarantine in a dozen cities, it would be a lot more like a thermonuclear blast that will flatten every bubble in sight. In all of recorded history no nation has ever managed an effective quarantine on so many people. With transportation screeching to a halt, the lives of millions of those people are at risk due to a simple lack of food or warm shelter.

Every form of sickness that can be passed on has a reproductive number. If a cold or flu in one person is passed on to only one other person, it has an R0 of 1. Below 1 the flu or cold will eventually disappear. Above 1 the sickness will be passed on to more and more people. A typical seasonal flu comes in at an R0 of 1.28; the 2009 flu pandemic came in at 1.48 and the deadly Spanish flu of 1918 measured 1.80. Lancet believes this coronavirus is between 3.6 and 4.0. And it’s deadly.

This has the potential for being the biggest mass casualty event in world history. At the very least it will take down the financial system as the world economy grinds to a halt with efforts to contain the virus.

Now would be a great time to be prepared for a disaster bigger than any in history. On Jan. 1, 2020, I posted a piece warning of a stock market crash. It’s here and it’s now.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Statements and opinions expressed are the opinions of Bob Moriarty and not of Streetwise Reports or its officers. Bob Moriarty is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Bob Moriarty was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

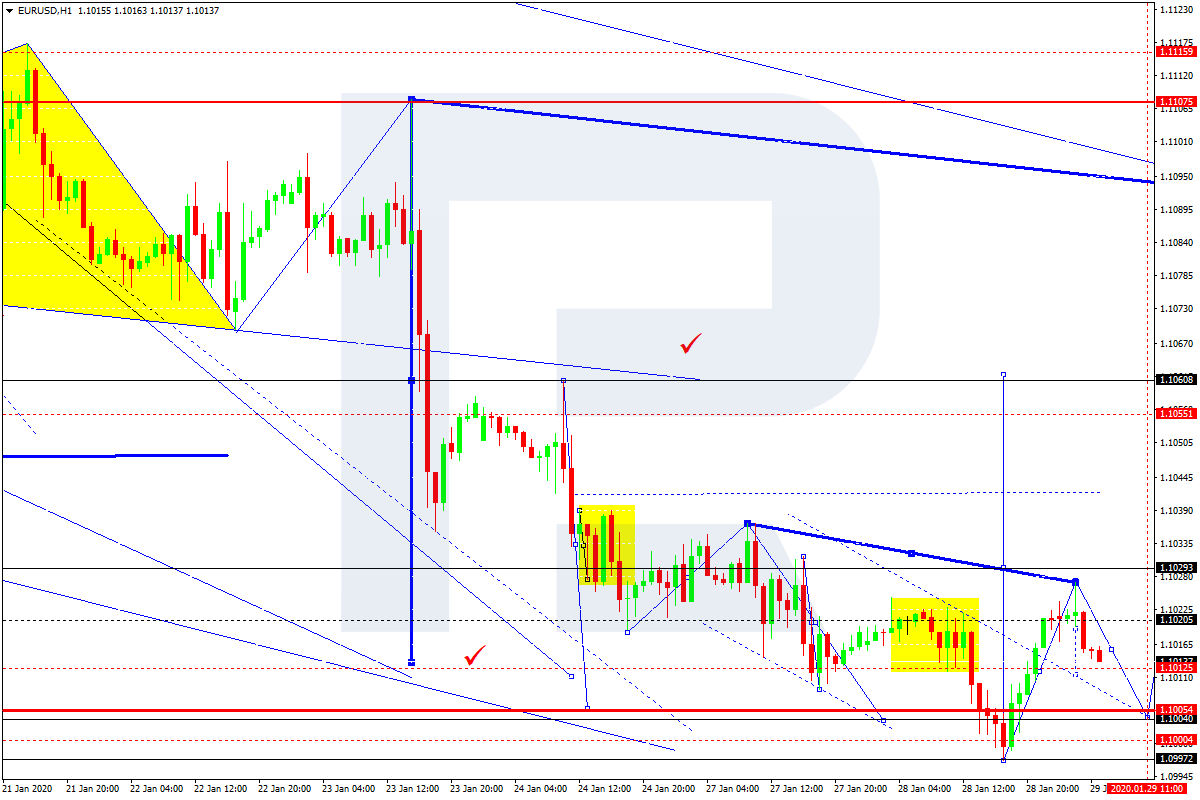

EURUSD has completed the ascending impulse; right now, it is correcting. Possibly, the pair may fall to reach 1.1012 or even 1.1004. Later, the market may resume trading upwards to break 1.1026 and then continue growing with the short-term target at 1.1053.

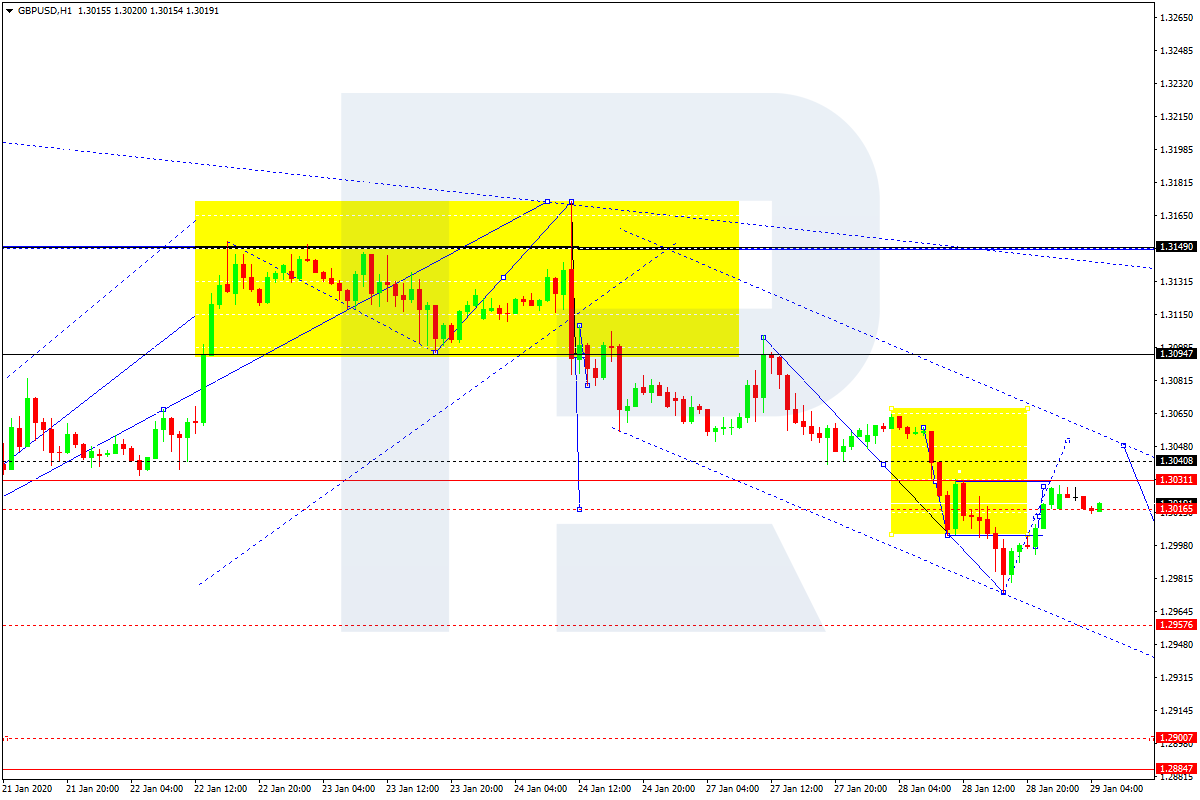

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD has finished another descending structure towards 1.2975; right now, it is correcting. Today, the pair may reach 1.3040 and then resume falling with the target at 1.2957.

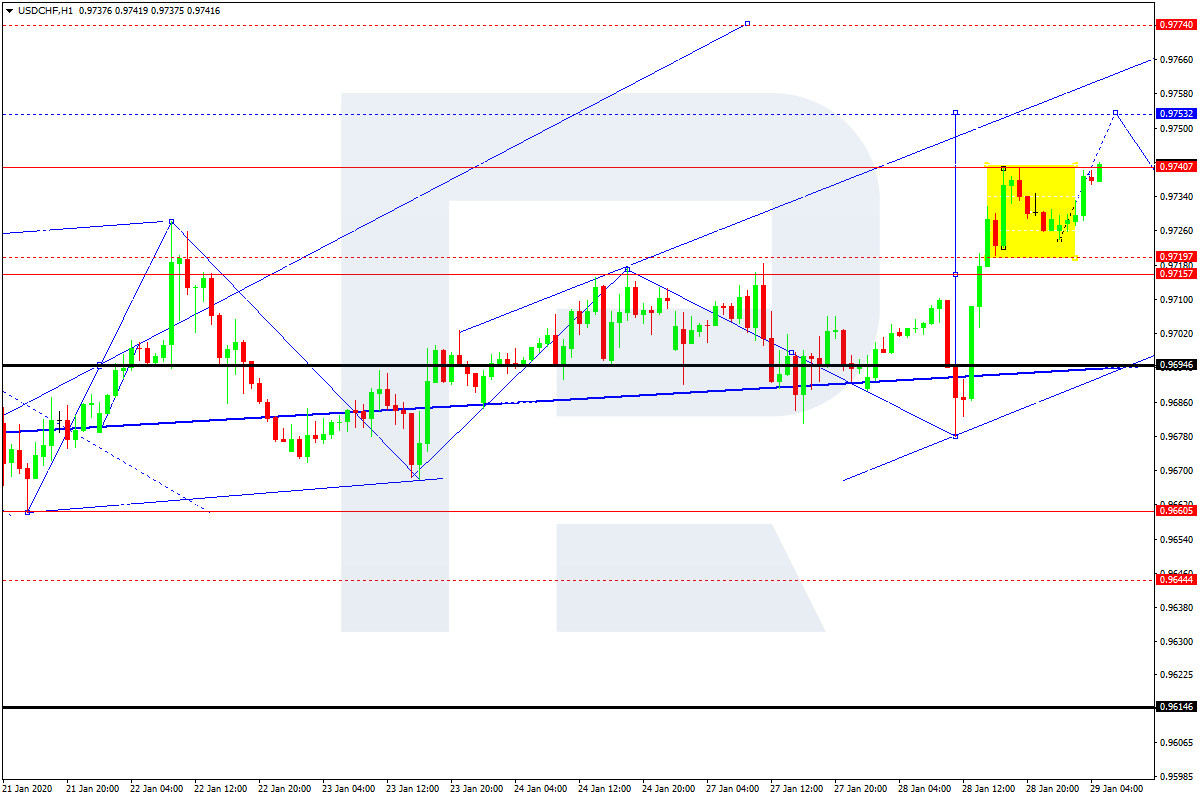

USDCHF, “US Dollar vs Swiss Franc”

USDCHF has completed the ascending wave towards 0.9735; right now, it is consolidating above 0.9715. If later the price breaks this range to the upside, the market may form one more ascending structure to reach 0.9753; if to the downside – start a new correction with the target at 0.9695.

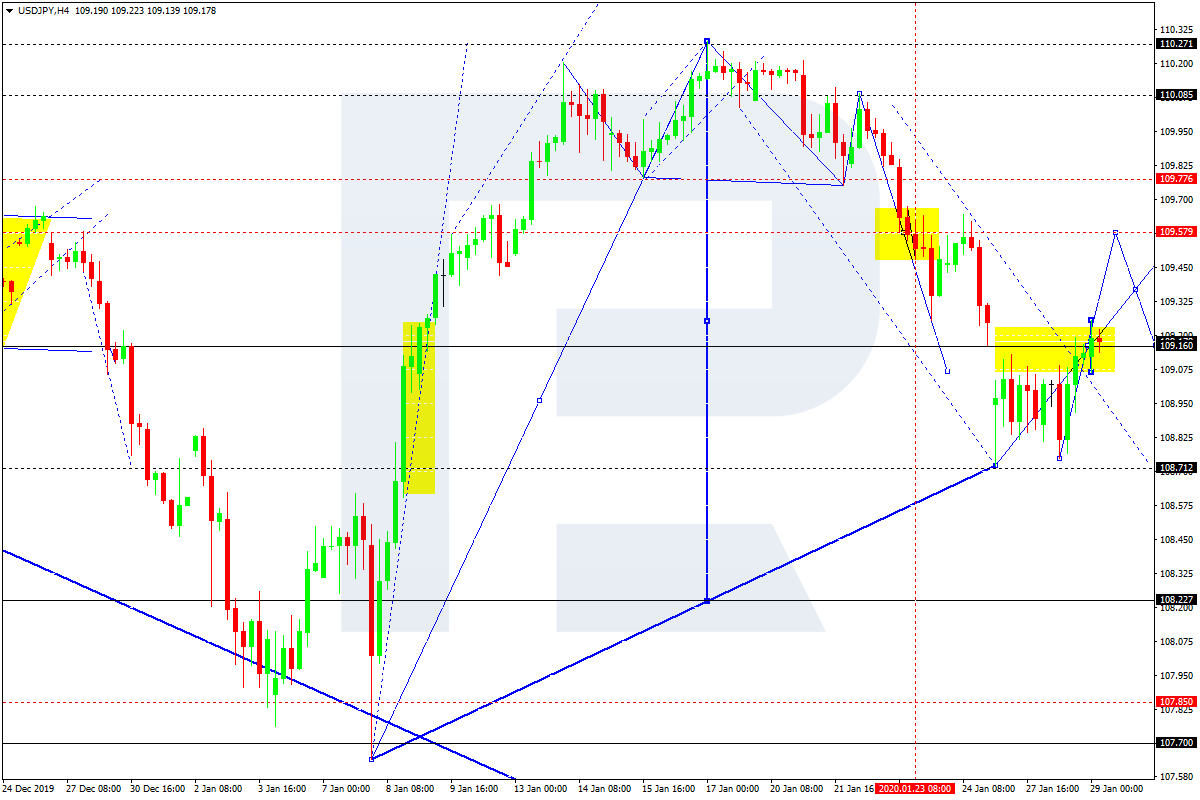

USDJPY, “US Dollar vs Japanese Yen”

USDJPY is growing to break 109.16. Possibly, today the pair may continue this correction towards 109.57 and then form a new descending structure to return to 109.16. After that, the instrument may grow to reach 109.60 and then resume trading inside the downtrend with the short-term target at 108.22.

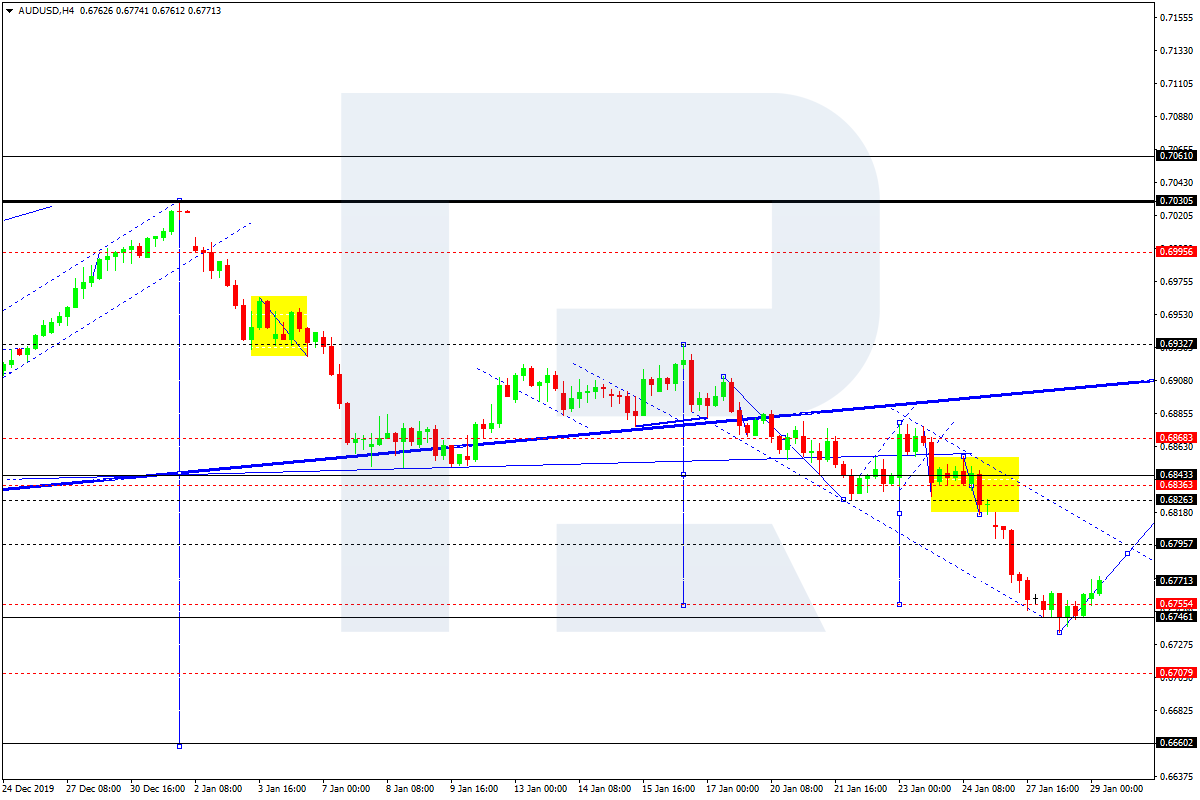

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is correcting upwards to reach 0.6844. Today, the pair may form the first structure of this correction with the target at 0.6790.

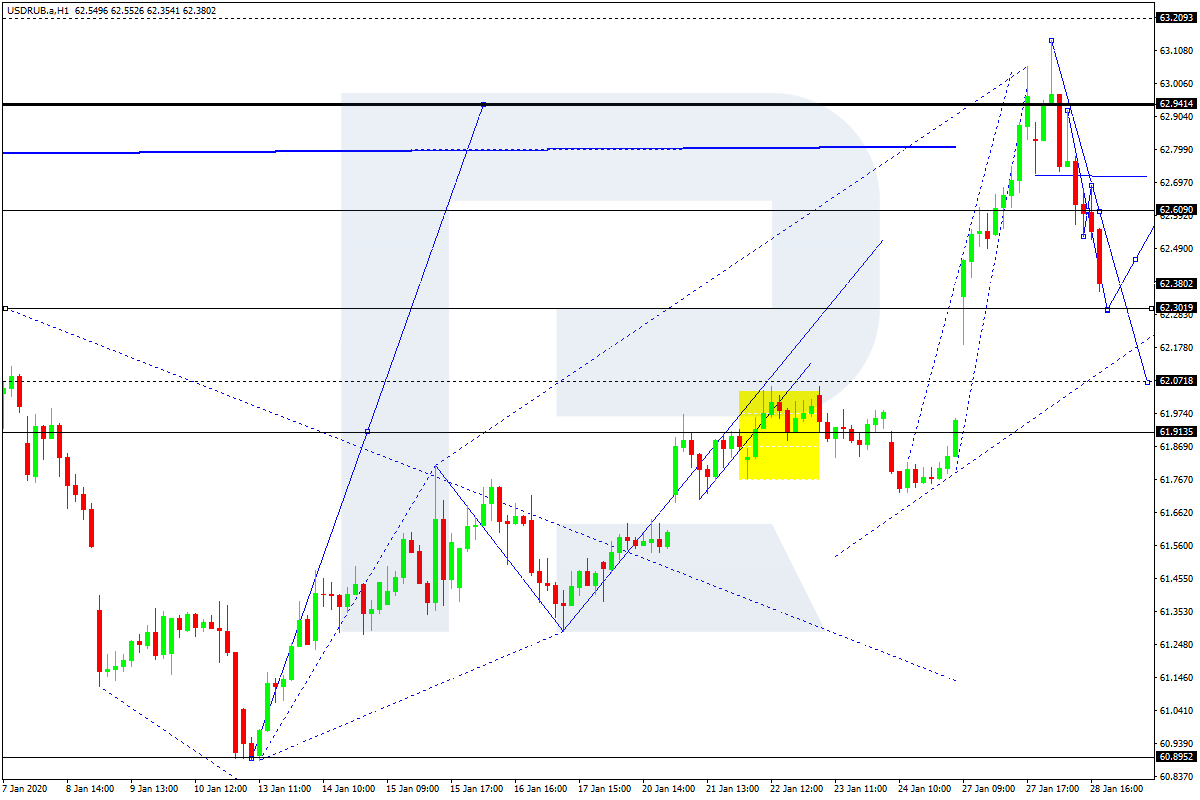

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is forming the first descending wave with the target at 62.08. According to the main scenario, the price is expected to reach it and then start a new correction towards 62.60.

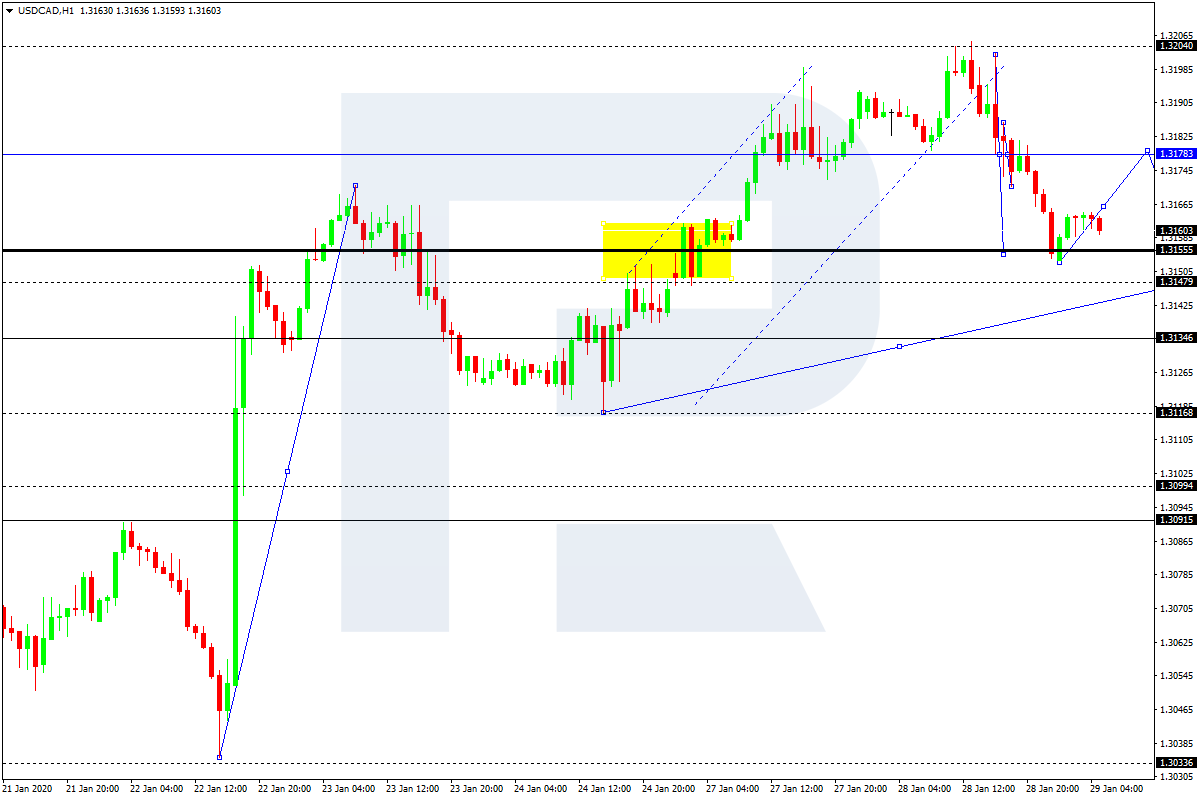

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is forming the first descending wave with the target at 1.3148. Possibly, the pair may reach this level and then start another correction towards 1.3178.

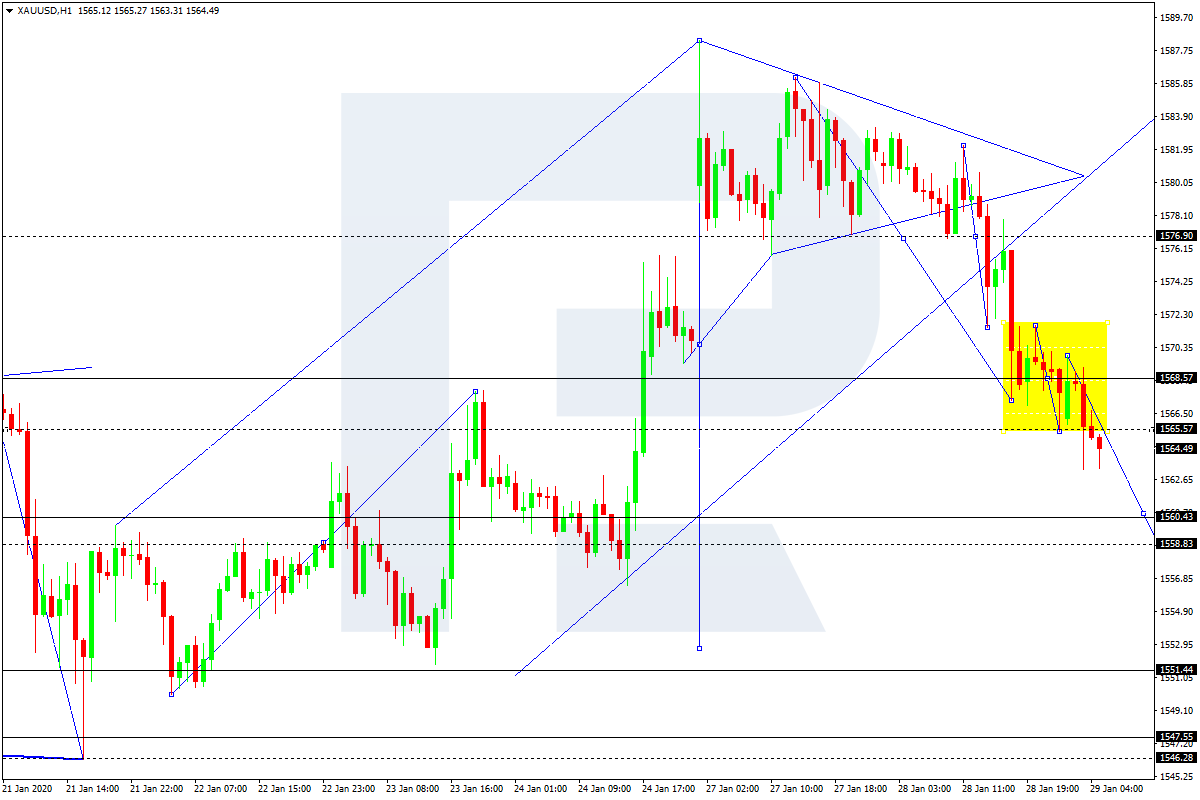

XAUUSD, “Gold vs US Dollar”

After reaching 1565.55 and then forming another consolidation range around 1568.87, Gold has broken it to the downside. Possibly, the pair may continue falling with the target at 1560.43. However, if the price breaks the range to the upside, the market may start a new correction to reach 1576.9 and then resume trading downwards with the above-mentioned target.

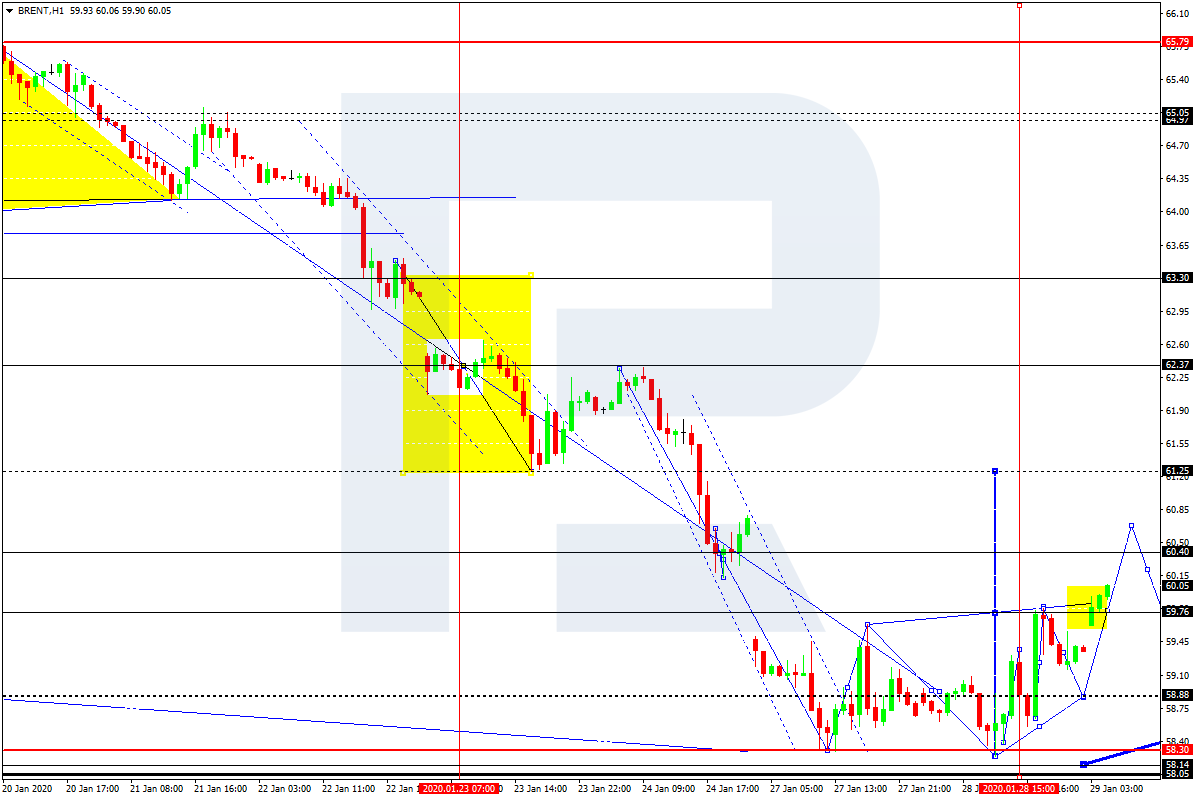

BRENT

After finishing the ascending impulse towards 59.76, Brent is trying to break its top. Possibly, the pair may continue growing to reach 60.80. An alternative scenario implies that the price may break 59.60 and start a new correction towards 58.88. After that, the instrument may form one more ascending structure with the target at 61.25.

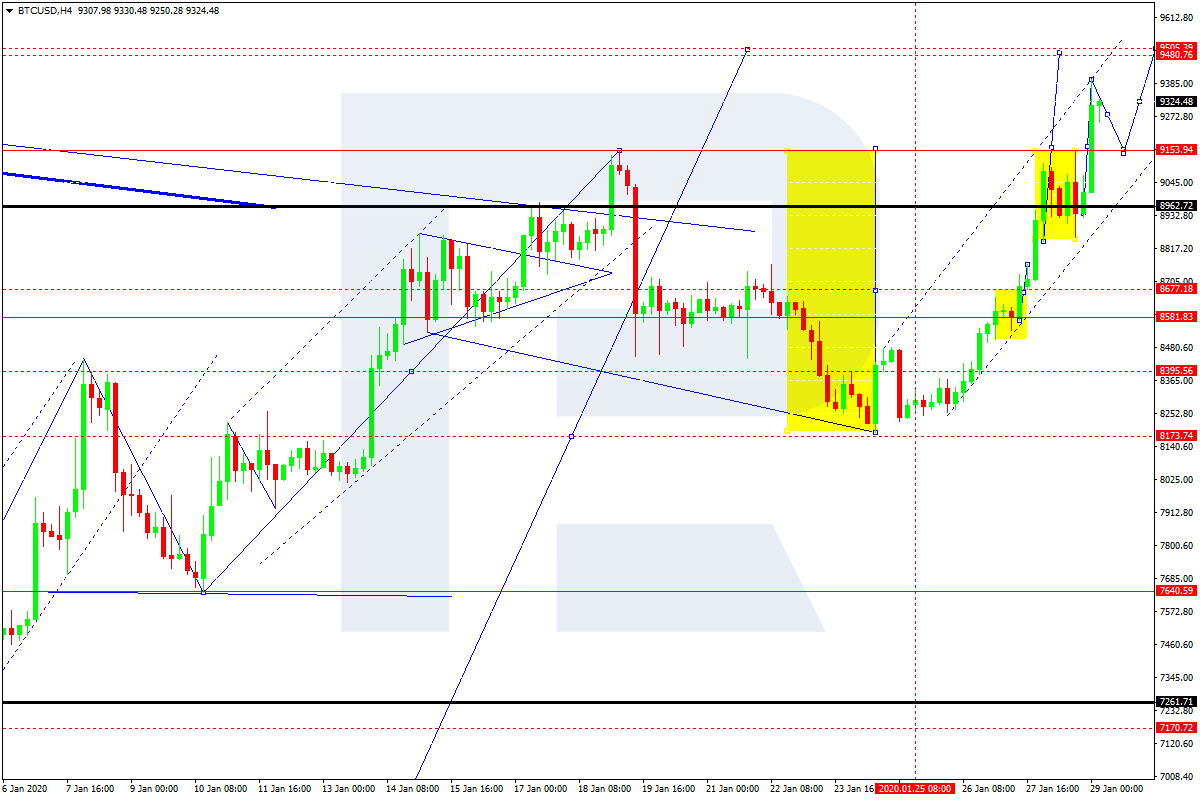

BTCUSD, “Bitcoin vs US Dollar”

After forming the consolidation range below 9153.00, BTCUSD has broken it to the upside. The main scenario implies that the pair may reach 9350.00 and then resume falling to test 9153.00 from above. After that, the instrument may start a new growth with the target at 9500.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Calling witnesses – including former national security adviser John Bolton – to President Trump’s impeachment trial is likely to cause short-term volatility in financial markets.

This is the warning from Tom Elliott, International Investment Strategist at deVere Group, one of the world’s largest independent financial advisory and services organizations.

It comes as the impeachment trial reaches a critical stage, with seemingly growing support to have witnesses called to the Senate.

Mr Elliott comments: “It was assumed that Trump’s impeachment trial would be done and dusted this week.

“However, in light of revelations from former national security adviser John Bolton’s draft book manuscript that Trump confirmed to him U.S. security support to Ukraine was based on the condition of investigations into political opponents, the conclusion and timings are now less certain due to the increasing calls for witnesses.

“At least two Republican senators are indicating that they are in favor of wanting to hear from witnesses, including Bolton.”

He continues: “Financial markets don’t want a drawn-out impeachment trial. They want certainty, especially as investors are already nervous because of the Coronavirus outbreak.

“Some sectors are more at risk of a longer impeachment trial – and damage to President Trump – than others.

“Sectors that would suffer from regulation by Democrats, notably pharma, energy and banks want him to win again.”

Mr Elliott concludes: “Four Republican senators need to agree to call Bolton.

“If they do, they are likely to demand the Bidens – both father and son – appear also. This will make the impeachment trial much longer. The longer the process, the more volatility will occur in global financial markets.

“Expect banks, pharma and energy to lead this market volatility if Bolton is called by the Senate.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement