A reduction in early oranges harvest is expected in South America

The USDA expects a reduction in early oranges harvest in Brazil by 30% in the 2020/2021 season compared to the previous 2019/2020 season. The Brazilian agricultural agency Cepea agrees with this assessment. A low harvest is a result of the drought in Brazil in September-October 2019. Another positive factor for orange juice may be the decision of the US Senate to resume the allocation of funds to Florida to treat all tourists with orange juice free of charge as a part of the “VISIT FLORIDA” marketing program. The authorities of China’s Chongqing city assume that fresh fruits and oranges may alleviate the state of patients with coronavirus.This can stimulate demand.

Sector expert Michael Ballanger sees something “terrifying” in the charts for copper and long-term bonds.

One of the advantages of being a sexagenarian is that after forty years investing in stocks, bonds, commodities, and currencies you have a pretty good idea when something is not exactly “right.” If you have lived a good, normal life and you still have decent control of over your mental faculties and bodily functions, you remember moments in time that impacted your sensibilities, not unlike your first crush on a girl, or that final exam, or an authoritarian coach’s dressing-down.

However, given my chosen profession, nothing gets more indelibly etched into one’s psyche than a big price “move” in something one owns. Be it a loss or a win, one can recall all the inputs that created that “move” and, sometimes elatedly and sometimes sadly, one can recall all of the ramifications and repercussion from the “move.” You will, later in life, regale in the joy (or sorrow) of recounting the story of the “move” until people roll their eyes in angst upon being subjected to their ninth or tenth serving.

Of course, one of the disadvantages of being a sexagenarian is that over time, one forgets (or imbues) portions of the story, usually in favor of its historical significance or personal accolade. But, alas, that is an anecdote for another day. What I wish to discuss with you all today is that my geriatric power of recall and my olfactory rot-sensor are telling me that something is definitely not “right.”

This pervasive feeling of dread originates from this perversion known as “the stock market.” where our banker-politico alliance has conspired to distort its historical role as a barometer for the economy and instead use it as a tool for manipulating consumer (and voter) behavior.

The practice of using the Working Group on Capital Markets to alleviate concern in the minds of iPhone-buying citizens through the constant and criminal levitation of stock prices (as shown above in the “All is well!” chart), and the capping of gold prices, has now made the barometric role of natural price discovery a thing of the past, a distant memory, a figment of sexagenarian imagination. That young investors can boldly go where no man has gone before in terms of risk discounting (or risk ignorance) is a moral hazard of utmost consequence and danger.

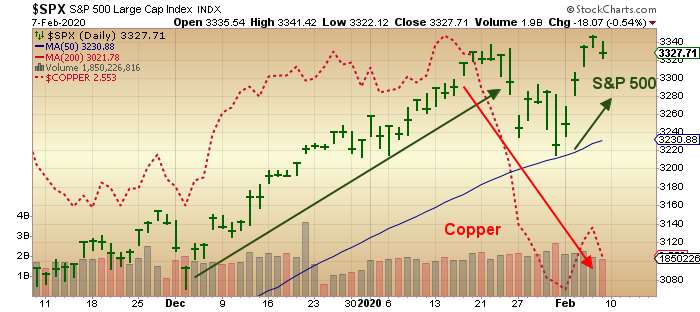

It is said that copper has a PhD in economics, and since it is such a gargantuan global market, it is essentially immune from the whims of the banker-politico lever-pullers. As such, it has been screaming “Danger!” for most of this very young 2020. This swoon in the world’s #1 industrial metal is comparable to the crashes in 2001 and 2008, and similar recessionary periods such as 198082 and 19731974, and warns of a rapidly slowing global trend.

Actually, copper has been moving straight south since mid-2018, but there hasn’t been as much as a peep from the hallowed halls of the Wall Street Journal or the sacred studios of CNBC, because to do so would oppose the national narrative. To wit, it is this national narrative that really gets on my wick because my training from the pre-2000 period of financial sanity has me constantly on the lookout for things that just aren’t “right.” To have young people diving into overinflated stock funds (and housing) because global growth is “healthy” is somewhat warped and totally bereft of logic.

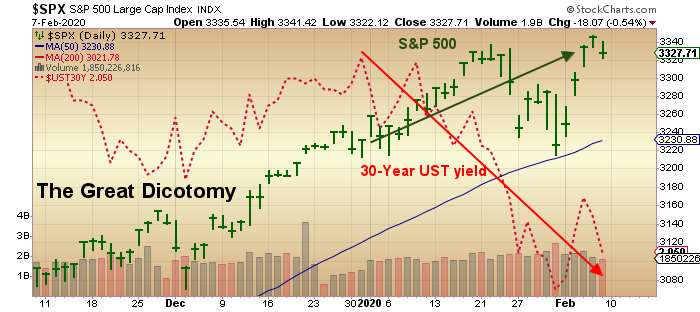

We can look at charts of the Fed balance sheet, or national debt, or China’s purchasing manager indexes (PMIs) and all arrive at various (bullish) conclusions of all shapes and sizes. But there is one chart in all of the financial universe that tells me what the smartest people in the world are doing with their “big wallets,” and that is the chart of long-term bond yields. If copper has a PhD in economics, then bond yields would be the academic masters that wrote the books copper studied en route to its degree.

Long-term yields are different than short-term yields because the former are demand-driven while the latter are policy-driven or “administered.” The Federal Reserve maestros can play Pac-Man with short-term interest rates, but they can’t with long-term yields because over the long term, yields will move to levels governed by fear. And it is fear and fear alone that drives the risk-free rate of return for holders of all the wealth in the world.

Accordingly, it is this next chart whose eardrum-splitting air raid siren is drowning out the blips and beeps of the copper chart or the ding-dong of the stock chart without a trace of indecision or reflection. Long-term yields are moving lower and they are moving lower fast. That, my friends, reeks of a sense of urgency verging on panic, and it began long before the coronavirus arrived.

The chart below is truly “The Great Dichotomy.”

It is this Great Dichotomy that terrifies me, and the one chart that should be required reading for everyone participating in the world of financial speculationand a rote memory prerequisite for the all serious investors.

To put this in perspective, you are afflicted with a certain medical condition and there are ten people in a room all telling you what medicine to take. You can heed the younger guy with the tattoos and the leather chains smoking a reefer, or you can listen to the older, quite hale gentleman in the white coat and glasses. One is telling you that you are fine while the other says you need some rest. One is telling you that “All is well!” while the other is telling you to go directly to the emergency ward. Failure to respect dichotomies such as this can lead one to disaster and financial ruin.

If it was only copper, or only elevated relative strength index (RSI) readings, or only a global pandemic, one could a write it off as “a buying opportunity,” and take the tack of patience and calm, moving forward into battle with a stiff upper lip and stoic resolve. This, however, is not a one-off “event-risk” situation that will eventually fade, leaving the dance floor wide open for above-average capital gains and central planner-entitled prosperity. Long-term yields do not lie. You can discount virtually everything else in the universe of chart-ology, but you dare not doubt that one simple dichotomy shown above.

Stocks are being priced for massage parlor perfection, but bond yields are being priced for a nuclear winterandthat is how I am proceeding. Caution over greed. . .

Now, last week was a the second-most blatant case of intervention by the banker-politico alliance, exceeded only by the 2008 bank bailout and stock levitation, and slightly ahead of the Christmas 2018 activation of Smilin’ Stevie Mnuchin’s Plunge Protection Team (PPT) campaign. With stocks breaking down on the eve of the impeachment vote and on the crest of the coronavirus wave, China set the table with trillions of USD-equivalent yuan liquidity jolts in order to prevent a microbe-triggered meltdown in its capital markets, matched majestically by similar actions from its U.S. counterparts. The result was a near-magical, one-week levitation of 2.46%, the biggest advance of this duration and amplitude in two-odd years. Praise the Lord!

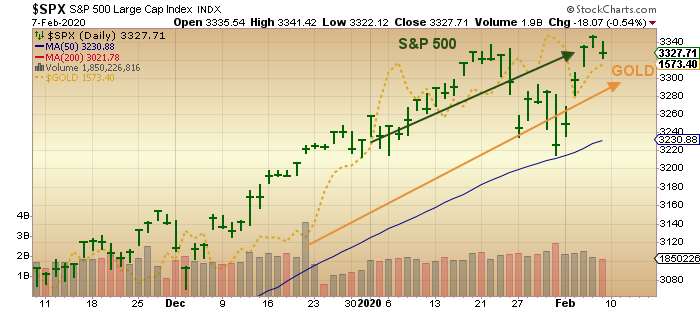

When I look at a chart such as this, I am inclined to default to a well-honed suspicion, and in order to decipher the true meaning of such an advance, I turn to gold and fully expect that these collusive cretins would have engineered a countertrend takedown of equal magnitude. But while gold lost some $20 on the week, it was a mere pittance given the extent of the rescue mission in stocks. No uptrend line was broken; few negative divergences came about; and the bull market emerged from yet another week of pandemonium intact, albeit on a late downtick.

Silver fared not as well. It suffered its fourth down week in five for the year, but remains in the uptrend that started last May. If that “slingshot effect” I wrote of earlier is to pass, silver needs to get the lead out of its jeans, and quickly. The gold:silver ratio (GSR) is hovering just under 90 (88.80), and please forgive the redundancy, but a rising GSR is not characteristic of a healthy bull market.

Similarly, the action in the gold miners early in the week gave me the opportunity to replace

50% of the GDX and GDXJ positions at or under their respective 50-day moving averages (dma) and then top up the rest on Friday. However, the HUI has also struggled since 2020 arrived and, like silver, suffered its fourth down week in five. More ominously, unlike gold and silver, the HUI has broken below the uptrend line drawn off the May 2019lows, and this is not good. We absolutely must reclaim that uptrend lineand hopefully this weekto avoid any further divergences and potential nonconfirmations.

Keep in proper perspective that considering the raging advance in the NASDAQ this week, led by the epic short squeeze in Tesla (and move to over $960), gold miners did relatively well despite a weak silver market and a near-300 point drop in the Dow.

More than a few subscribers and followers have been asking about the junior developer/explorer portion of the GGM Advisory portfolio, and while Aftermath Silver Ltd. (AAG:TSX.V) was the superstar in 2019, it has been in correction mode recently, with both Goldcliff Resource Corp. (GCN:TSX.V; GCFFF:OTCBB) (now drilling Nevada Rand) and Getchell Gold Corp. (GTCH:CSE) (preparing to drill Fondaway) outperforming. I put out a note to subscribers on Thursday on Aftermath that I am now happy to share, so e-mail me at [email protected]and I’ll be pleased to pass it along. I smell an upside advance on the immediate horizon and my note (hopefully) spells it out in large block letters.

Heed the Great Dichotomy. It is an insidious omen for all but those things “precious.”

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver, Goldcliff Resource, Getchell Gold. My company has a financial relationship with the following companies referred to in this article: Aftermath Silver, Goldcliff Resource, Getchell Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Goldcliff Resource. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Aftermath Silver. Please click here for more information. Within the last six months, an affiliate of Streetwise Reports has disseminated information about the private placement of the following companies mentioned in this article: Aftermath. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver, Goldcliff Resources, and Getchell Gold, companies mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Shares of Myriad Genetics traded 30% lower after the firm released Q2/20 earnings and announced the appointment of a new interim CEO.

After U.S. markets closed yesterday afternoon, global molecular diagnostics and precision medicine company Myriad Genetics Inc. (MYGN:NASDAQ),announced Q2/20 financial results for the period ending December 31, 2019. The firm additionally provided an update on recent operational highlights and reported revised Q3/20 and FY/20 financial guidance.

The company reported that in Q2/19 total revenues decreased by 10% to $195.1 million, compared to $216.8 million in Q2/18. The firm indicated that in Q2/19 it had diluted earnings per share (EPS) of ($0.11) and Adjusted EPS of $0.23, compared to diluted EPS of $0.03 and Adjusted EPS of $0.38 for Q2/18.

The company’s newly appointed President and Chief Executive Officer R. Bryan Riggsbee commented, “Revenue in the fiscal second quarter fell short of expectations largely due to the prenatal business. Prenatal cash collections were negatively impacted by issues in billing operations that occurred during the transition of the homegrown Counsyl billing system to an industry-standard system used by Myriad. We are in the process of implementing a number of initiatives focused on improving cash collections, have made several organizational changes to bolster growth and are evaluating additional initiatives…Despite recent payer related headwinds, we continue to see significant near-term prospects to drive increased revenue and I am highly focused on returning Myriad to a position of sustained long-term profitable growth.”

The firm discussed some of the recent business highlights including that it has signed a fixed-price payer portfolio contract with UnitedHealthcare and grew hereditary cancer diagnostic volumes at a mid-single digit rate on a year-over-year basis.

The company also provided Q3/20 and FY/20 forward guidance. For Q3/20 the company expects Revenue of $172 million with GAAP diluted EPS of ($0.30) per share and Adjusted EPS of $0.02 per share. For FY/20 the company expects Revenue of $735 million with GAAP diluted EPS of ($0.80) per share and Adjusted EPS of $0.45 per share.

On the same day the company also announced that effective immediately R. Bryan Riggsbee, Chief Financial Officer, has been appointed Interim President and Chief Executive Officer, but will also continue to serve as CFO. The firm advised that Mark C. Capone has resigned as CEO and President and as a member of the Myriad’s Board of Directors.

John T. Henderson, M.D., Chairman of the Board of Directors commented, “As we position Myriad for its next phase of growth and value creation, the Board and Mark have mutually agreed that now is the right time for a leadership transition…We are pleased to have a leader with Bryan’s experience to step into the additional role of Interim CEO and provide continuity as we execute on our search for a permanent CEO…We are confident in Bryan’s ability to drive the Company forward and will continue to support him and the entire executive team while we work to identify a permanent CEO…On behalf of the entire Board of Directors, I want to thank Mark for his leadership and contributions to Myriad over his more than 17-year tenure with the Company. We have had numerous scientific and medical advances during this time that have contributed significantly to the health and transformation of patients’ lives around the world.”

Myriad Genetics is headquartered in Salt Lake City , Utah and describes its business as “a leading molecular diagnostic and precision medicine company dedicated to being a trusted advisor transforming patient lives worldwide with pioneering molecular diagnostics. The company discovers and commercializes molecular diagnostic tests that: determine the risk of developing disease, accurately diagnose disease, assess the risk of disease progression, and guide treatment decisions across six major medical specialties where molecular diagnostics can significantly improve patient care and lower healthcare costs.”

Myriad Genetics began the day with a market capitalization of around $2.2 billion with approximately 74.39 million shares outstanding and a short interest of about 17.2%. MYGN shares opened nearly 30% lower today at $20.68 (-$8.61, -29.40%) compared to yesterday’s $29.29 closing price and fell to a new 52-week low price this morning of $19.08. The stock has traded today between $19.08 to $21.02 per share and is presently trading at $20.51 (-$8.78, -29.98%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

Brent crude made a new 13-month low on Monday around $53.11 on news that potentially deeper OPEC+ cuts may not occur soon. The spreads in the futures markets are signaling weaker demand, with the discount on spot prices widening further. This year, Brent crude has dropped by more than 18% and by 25% from its January peak of $71.75.

2020 was supposed to put an end to the global manufacturing slump after the US and China reached their “phase one” trade agreement. It was expected that Europe would begin to shine again due to renewed Chinese demand after the signing of the trade deal. But no one expected a coronavirus outbreak that would interrupt economic activity in China and spread globally.

Now it’s no longer a question of whether the coronavirus epidemic will lead to an economic slowdown, but how painful this slowdown will be. The scale of the impact can only be determined when the spread of the virus begins to slowdown and the outbreak gets under control, which is not the case at the moment.

Chinese companies were supposed to return to work on Monday, but many car plants and other manufacturers have remained closed following the new year holiday. State refiners such as PetroChina, Sinopec Corp and CNOOC have all announced cuts to their refinery runs totaling approximately 940,000 barrels per day. In fact, this number will be much bigger if you take into account independent refiners.

Given that China’s oil demand has fallen by more than three million barrels a day, the country may need to cut imports for several months to come. Until then, supertankers may need to store oil, which means inventories will begin to build-up excessively.

That’s why OPEC+ may need to make a quick decision very soon to prevent prices from slumping further. Russia seems to be the main obstacle against cutting production at this stage. But if the coronavirus continues to spread and we don’t see a response from the cartel, expect oil prices to remain in a freefall.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stock market rebounded on Monday as positive earnings reports buoyed investors optimism undermined by worries about the impact of coronavirus infection in China. The S&P 500 gained 0.7% to new record 3352.09. Dow Jones industrial added 0.6% to 29276.82. The Nasdaq rose 1.1% to fresh record 9628.39. The dollar strengthening continued at steady pace as Federal Reserve Governor Michelle Bowman said she was “comfortable with the current stance of our policy.” The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 98.85 and is higher currently. Fed Chair Powell is testifying today on the semiannual Monetary Policy Report before the House Financial Services Committee. Futures on stock indexes point to higher openings today.

FTSE 100 still top loser among European stock indexes

European stocks ended marginally higher on Monday despite weak data. The GBP/USD reversed its sliding yesterday while EUR/USD continued declining with both pairs dynamics unchanged currently. The Stoxx Europe 600 index added 0.1% despite both the Sentix investor confidence index for euro-zone and Italy’s industrial production coming lower than expected. The DAX 30 however slipped 0.15% to 13494.03. France’s CAC 40 slid 0.23% while UK’s FTSE 100 lost 0.3% to 7446.88.

Hang Seng leads Asian indexes rebound

Asian stock indices are rebounding today with Nikkei closed for holiday while yen slide against the dollar continuing. Markets in China are rising despite reports of more than 100 dead in a single day: the Shanghai Composite Index is up 0.4 % and Hong Kong’s Hang Seng Index is 1.4% higher. Australia’s All Ordinaries Index recovered 0.6% despite accelerating Australian dollar climb against the greenback.

Brent futures prices are recovering today. Prices ended sharply lower yesterday on supply glut concerns as it remained unclear if the Organization of the Petroleum Exporting Countries and its allies, including Russia, will move to further cut production beyond an existing agreement on output curbs: April Brent crude closed 2.2% lower at $53.27 a barrel on Monday, the lowest settlement since December 28, 2018.

Gold slides as Dollar strengthening continues

Gold prices are pulling back today. April gold rose $6.1 ending at $1579.50 an ounce on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

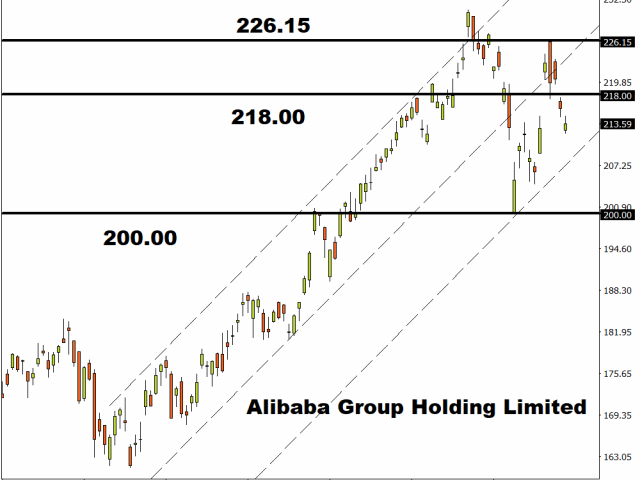

One of the world’s largest e-commerce players is scheduled to release third quarter earnings before US markets open on Thursday.

There is a strong sense of optimism over the business outlook for Alibaba Group Holding Limited amid strong mobile growth, a firmer foothold in the digital and entertainment industry coupled with rising revenues from the cloud segment. However, the company’s domestics and international growth were probably impacted by US-China trade tensions during the third quarter of 2019, something that may hit profits. Nevertheless, Alibaba’s earnings could still surprise to the upside – especially when factoring how the e-commerce giant has a history of surpassing both earnings per shares and revenue estimates.

Alibaba is expected to report earnings of $2.25 per share on $22.68 billion in revenues. A positive earnings report could boost appetite for the company’s shares with prices rebounding towards 218.00 and potentially 226.15. Alternatively, if earnings disappoint this could drag shares back towards 200.00.

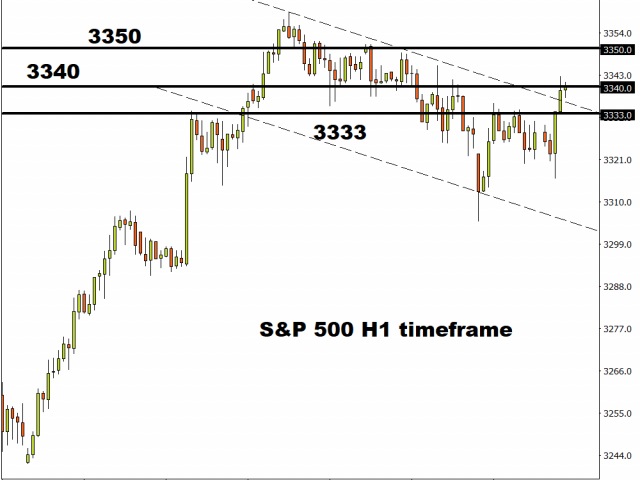

S&P 500 U turns despite virus concerns

The S&P 500 has entered the week on positive note, gaining roughly 0.3% as of writing despite coronavirus fears fuelling market uncertainty and risk aversion.

The Index is trading around 3340 and could push higher towards 3350 on speculation around central banks easing monetary policy in the face of slowing global growth. Focusing on the technical picture, bulls need to break above 3340 to open a path towards 3345 and 3350. Alternatively, sustained weakness below this level should encourage a decline towards 3333 and potentially lower.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

By TheTechnicalTraders – The first part of this article highlighted what we believe is the start of a broad market sector rotation setup in the US and global markets. This second part will highlight what we believe are excellent examples of sector trade setups for our friends and followers.

As China continues to pour capital into their markets to stabilize the outflow and fall of asset prices, a number of interesting components of broader sector rotation are setting up. First, the US stock market has rolled lower in what we are calling a “first-tier” of the “waterfall event”.

Additionally, Mid-Caps, Transportation, Energy, and Financials have all started to roll-over of already begun to rotate lower. We believe the contraction in economic activity and global market engagement as a result of the Wuhan virus will result in a much bigger and broader downside price move than many are expecting in the coming weeks.

The death toll for the Coronavirus outbreak reached 910, surpassing the number that died in the 2003 SARS episode. This is causing huge issues with global supply chains and shipping companies as I talked about last week in my HoweStreet Interview.

We believe traders need to be aware of the continued capital shift that has been taking place over the past 4+ years. As foreign markets struggle and the US Dollar continues to strengthen, capital has been moving into the US stock market as a protective measure. We believe this will continue throughout the virus event, yet we believe the US stock market will contract, move lower, as a result of this virus event as well.

Many US companies are still exposed to foreign markets through overseas engagement and retail locations, Automakers, consumer products, manufacturing, heavy equipment and dozens of other sectors derive 5% to 25%+ of their revenues from China and other overseas markets. MacDonalds, Starbucks, Caterpillar and dozens of other US companies have broad exposure in China and Asia. We believe this virus event could last well into July and possibly much longer. Because of this, we believe a broader market sector rotation will take place and that volatility will continue to increase over the next 6 to 12+ months.

Here are the three sectors we believe have a strong potential for setting up a fantastic trade. Follow our research to learn more about what we do and how we can help you find incredible trade setups.

Russell 2000 (IWM) – Weekly Chart

The Russell 2000 (IWM) has already started to move a bit lower over the last few weeks. Even though the US stock market was plowing higher throughout most of December and January, the Russell 2000 is actually showing signs of a rounded top formation with a very clear downside “first leg” (waterfall) type of price decline. We believe broader market contraction and sector rotation could push IWM below $144 in an attempt to target historical support near $126.

TECS Technology Sector ETF – Weekly Chart

The Technology sector may see a broader market decline over the next 30 to 60 days that could push TECS from recent lows, below $6, to levels above $12 to $16 on a reactionary move in this 3x ETF. TECS has experienced very low volatility over the past 3+ months while the US stock market has continued to rally in Q3 and Q4. Any breakdown in the global technology sector could push TECS well above recent peak levels near $18.

XLF Financial Sector ETF – Weekly Chart

The Financial Sector is very likely to experience a 3% to 10% decrease in consumer activity related to the lack of travel, outside entertainment, shopping and food services activities and could see extended risk to loans, debts, and other services as a result of a global economic market contraction. We believe a downside risk exists in XLF where the price will likely break below $30 and target the $25 to $26 level over the next 30 to 60+ days. Ultimately, XLF must hold above the December 2018 lows near $22 if the current downside rotation ends within recent price ranges. A move below $22 would indicate we have entered a new stage of a Bear trend.

The reality of the situation for most of us is that we are not at immediate risk of catching anything except a common cold or flu. As skilled traders, we must identify an opportunity where it presents itself and we must attempt to learn to capitalize on that opportunity. We believe these sectors, and many others, are about to present very real trading opportunities for skilled traders.

The virus is expected to double in scope every 6.5 days based on modeling data. Obviously China and Asia are the biggest risks right now. Our biggest concern is that the virus spreads into India and Africa. We believe a spread into these regions could add hundreds of thousands or millions of infected people to the lists. At this point, it is far too early to tell how extended this virus event will become – yet we feel we are just starting this rotation and the true scope of it won’t be known for many weeks or months.

Join us in our quest to create incredible profits from these bigger trends today. As a technical analyst and trader since 1997 I have been through a few bull/bear market cycles, I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

Join my Swing Trading ETF Wealth Building Newsletter if you like what you read here and ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own.

NOTICE: Our free research does not constitute a trade recommendation or solicitation for our readers to take any action regarding this research. It is provided for educational purposes only. Our research team produces these research articles to share information with our followers/readers in an effort to try to keep you well informed. Visit our web site (www.thetechnicaltraders.com) to learn how to take advantage of our members-only research and trading signals.

The events in that trio are presented in a ROTH Capital Partners report.

In a Feb. 3 research note, ROTH Capital Partners analyst Yasmeen Rahimi reported that Albireo Pharma Inc. (ALBO:NASDAQ) plans to launch three clinical trials this year in the same number of pediatric liver indications, thus making its 2020 “pivotal” and “catalyst rich.”

ROTH’s target price on Albireo is $75 per share, and the share price is about $23.47.

Rahimi went on to note what the U.S.-based biopharma’s imminent three studies are and when they are likely to start.

Albireo’s clinical program with the most imminent readout, expected in mid-2020, is its PEDFIC 1 Phase 3 trial of odevixibat at a low dose and a high dose (40 and 120 micrograms per kilogram per day, respectively) in pediatric patients with progressive familial intrahepatic cholestasis (PFIC) 1 and 2. Only one more patient is needed for enrollment to be completed. Accordingly, “potential approval and launch of odevixibat are within sight, which are anticipated in in H2/21,” noted Rahimi.

Another data readout expected in mid-2020 is from the Phase 2 study of a different therapeutic, elobixibat, in nonalcoholic steatohepatitis, or NASH, in adults.

Two, now with U.S. Food and Drug Administration (FDA) approval, Albireo is about to launch a pivotal trial in biliary atresia, a rare pediatric liver disease, in H1/20. The study will be double blind and placebo controlled and enroll 200 patients at 70 locations around the world. Patients will be required to have undergone the Kasai surgical procedure and, thus, be newborns under 90 days old. They will be administered 120 micrograms per kilogram of odevixibat once daily. The trial’s primary endpoint will be survival with native liver after two years of odevixibat therapy. Albireo has the funding necessary to conduct this trial that will cost an estimated tens of millions of dollars.

Three, Albireo aims to commence a pivotal trial in Alagille syndrome by year-end 2020. The next step is meeting with the FDA in Q1/20 to finalize the study design.

“Albireo has made it loud and clear that 2020 is the year of execution and advancing all of its assets forward in the clinic,” wrote Rahimi.

ROTH has a Buy rating on the biopharmaceutical company.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from ROTH Capital Partners, Albireo Pharma Inc., Company Note, February 3, 2020

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Albireo Pharma, Inc. and as such, buys and sells from customers on a principal basis.

Shares of Albireo Pharma, Inc. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

The new numbers and potential for further growth are discussed in an Echelon Wealth Partners report.

In a Feb. 3 research note, Echelon Wealth Partners analyst Gabriel Gonzalez reported that Revival Gold Inc.’s (RVG:TSX.V) updated mineral resource estimate for Beartrack-Arnett Creek hit its target of 3 million ounces of gold (3 Moz), up from 2 Moz, and further upside remains.

“We believe that Revival has the potential to demonstrate additional resource growth potential to drive further project value,” Gonzalez commented.

Both the mill resource and heap-leach resource were updated. The new total mill resource, including Indicated and Inferred ounces, is 2.4 Moz gold at a grade of 1.47 grams per ton (1.47 g/t). This reflects a 46% growth in ounces and a 3% increase in grade over those in the previous estimate.

The new total heap-leach resource is 580,000 (580 Koz) gold at a grade of 0.56 g/t. These updated amounts changed from the previous ones by +76% and -23%, respectively, “with the decrease due to the exclusion of historical RC drill holes from the estimate, and a conservative 75% assumed metallurgical recovery (compared to >90% in preliminary bottle roll tests).”

Gonzalez pointed out that further heap-leach resource potential exists. For Beartrack specifically, the total resource now stands at 384 Koz, up 16%, at a grade of 0.55 g/t, down 24%. The differences in those numbers are due to use of a 15% lower mining cost of $2.25 per ton and a lower cutoff grade of 0.17 g/t (versus 0.26 g/t).

Regarding Arnett Creek, its total resources are now 196 Koz gold, down 48%, at a grade of 0.58 g/t, down 34%. The changes are due to the exclusion of historical reverse circulation drill hole results from the estimate along with a conservative assumed metallurgical recovery of 75%. “There is substantial opportunity for a pickup in ounces and grade as work on Arnett Creek is advanced,” wrote Gonzalez.

Additional heap-leach resource potential exists through possible expansions to the main Haidee target and other Arnett Creek areas. At Beartrack, growth potential exists on the delineated 5 kilometers (5 km) of strike and at depth of it as well as to the south, where Revival identified another 56 km structure.

Gonzalez purported that “mill resource growth will drive longer-term project upside.” The mill could produce more than 250 Koz per year in addition to the projected 50 Koz per year of heap-leach production. This could move the project to a production level of interest to intermediate and senior gold producers.

The analyst concluded, “We continue to be positive on Revival Gold given the large resource demonstrated at Beartrack-Arnett Creek and further potential upside as well as the project’s location in Idaho (a favorable mining jurisdiction) and highly experienced management team and board of directors.”

Echelon has a Speculative Buy rating and a CA$1.80 per share target price on Revival Gold. The company’s stock is trading at around CA$0.78 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Revival Gold, a company mentioned in this article.

Disclosures from Echelon Wealth Partners, Revival Gold Inc., February 3, 2020

Echelon Wealth Partners compensates its Research Analysts from a variety of sources. The Research Department is a cost centre and is funded by the business activities of Echelon Wealth Partners including, Institutional Equity Sales and Trading, Retail Sales and Corporate and Investment Banking.

I, Garbriel Gonzalez, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that I have not, am not, and will not receive, directly or indirectly, compensation in exchange for expressing the specific recommendations or views in this report.

Important Disclosures: Is this an issuer related or industry related publication? Issuer.

Does the Analyst or any member of the Analyst’s household have a financial interest in the securities of the subject issuer? No

The name of any partner, director, officer, employee or agent of the Dealer Member who is an officer, director or employee of the issuer, or who serves in any advisory capacity to the issuer.? No

Does Echelon Wealth Partners Inc. or the Analyst have any actual material conflicts of interest with the issuer? No

Does Echelon Wealth Partners Inc. and/or one or more entities affiliated with Echelon Wealth Partners Inc. beneficially own common shares (or any other class of common equity securities) of this issuer which constitutes more than 1% of the presently issued and outstanding shares of the issuer? No

During the last 12 months, has Echelon Wealth Partners Inc. provided financial advice to and/or, either on its own or as a syndicate member, participated in a public offering, or private placement of securities of this issuer? Yes

During the last 12 months, has Echelon Wealth Partners Inc. received compensation for having provided investment banking or related services to this Issuer? Yes

Has the Analyst had an onsite visit with the Issuer within the last 12 months? No

Has the Analyst or any Partner, Director or Officer been compensated for travel expenses incurred as a result of an onsite visit with the Issuer within the last 12 months? No

Has the Analyst received any compensation from the subject company in the past 12 months? No

Is Echelon Wealth Partners Inc. a market maker in the issuers securities at the date of this report? No

The U.S. Department of Justice investigation of criminal activity in the precious metals markets has taken an interesting new turn.

According to Bloomberg, prosecutors are targeting the bank itself and not just the individual traders involved in rigging prices. If convicted, the bank as an institution could be held accountable for years of structured and pervasive cheating.

The DOJ investigation of JPMorgan’s metals trading desk began more than two years ago. It came on the heels of a guilty plea by Deutsche Bank.

Deutsche Bank copped to spoofing prices and agreed to turn state’s evidence. DB then handed over hundreds of thousands of pages of documents, along with chat logs and voice recordings which featured traders gleefully conspiring with one another to cheat clients and other market participants.

Officials used that trove of information and other evidence to charge six JPMorgan traders with crimes. Some already pleaded guilty and made their own agreements to cooperate with the larger investigation.

But last week’s revelations from Bloomberg are the first confirmation that the mega bank is itself in the crosshairs.

Bank of America followed Deutsche Bank’s lead and moved to settle charges. The company paid fines and promised internal reforms. Many expect the extraordinarily well-connected JPMorgan Chase & Co will be granted similar leniency.

There is one interesting distinction in the DOJ’s handling of the bank, however. Officials have charged JPMorgan traders using RICO laws.

The implication is that the bank itself is to be treated as a criminal enterprise. Perhaps this time company executives will not be able to convince investigators the bank is an honest institution with the simple misfortune of having rogue criminal traders among its ranks.

JPMorgan deserves to get more than a slap on the wrist.

For many involved in the metals markets, it has been obvious for years that JPMorgan is at the center of a program to rig gold and silver prices. These cries were long dismissed as conspiracy theory. Today few can dispute there has been pervasive, well-orchestrated cheating over nearly a decade, if not much longer.

We now know at least some officials inside the Department of Justice agree. They view the bank’s activities as organized crime, like the mafia.

It remains to be seen whether actual charges will be brought against the bank. So far, only individuals have been charged. Given the bank’s power and influence there is no certainty justice will prevail, even if the evidence is overwhelming.

Finally, there is no certainty as to whether any penalties will be commensurate with the crime. Individual criminals on Wall Street may have been banned from trading and bankrupted by fines. However, it would be unprecedented for a bank the size of JPMorgan to receive a trading ban or fines large enough to meaningfully impact the bank’s operations.

The road to full accountability for JPMorgan remains long and full of obstacles. But it is certainly nice to see prosecutors treating the bank without the usual kid gloves.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.