by JustForex

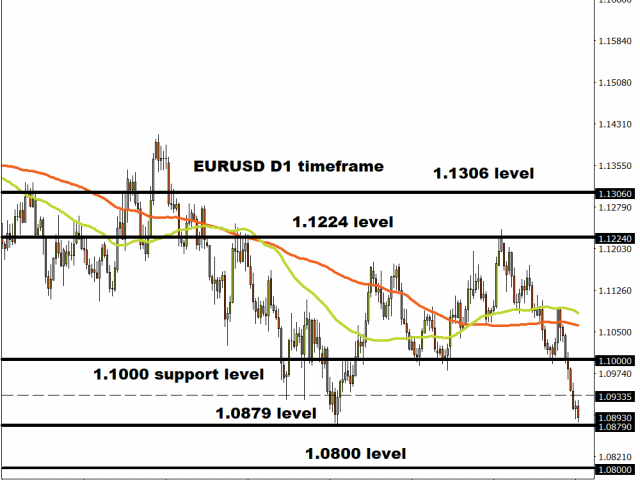

The EUR/USD currency pair

- Prev Open: 1.09152

- Open: 1.08738

- % chg. over the last day: -0.37

- Day’s range: 1.08653 – 1.08765

- 52 wk range: 1.0879 – 1.1572

The single currency keeps losing positions against USD. Yesterday the drop in quotations exceeded 40 points. At the moment the trading instrument is consolidating near the local support at 1.08650. The round level 1.09000 is already a mirror resistance. In the nearest future the technical correction after the prolonged fall is not ruled out. Today investors will evaluate economic reports from the USA. We recommend opening positions from key levels.

The Economic News Feed for 13.02.2020:

- – US inflation data (US) – 15:30 (GMT+2:00);

- – Initial Jobless Claims (US) – 15:30 (GMT+2:00);

The indicators signal the sellers’ strength: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone, which indicates a bearish sentiment.

The Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which gives a signal to buy EUR/USD.

- Support levels: 1.08650, 1.08300

- Resistance levels: 1.09000, 1.09400, 1.09700

If the price fixes below 1.08650, expect the quotes to descend toward 1.08300-1.08100.

Alternatively, the quotes could grow toward 1.09300-1.09500.

The GBP/USD currency pair

- Prev Open: 1.29518

- Open: 1.29597

- % chg. over the last day: +0.04

- Day’s range: 1.29441 – 1.29647

- 52 wk range: 1.1959 – 1.3516

The technical picture on the GBP/USD currency pair is ambiguous. At the moment the sterling is consolidating. Financial markets participants are waiting for additional drivers. The local support and resistance levels are 1.29400 and 1.29800, respectively. The trading instrument has potential for recovery. We recommend to pay attention to the US economic news background. Positions should be opened from key levels.

Publication of important economic reports from the UK is not planned.

Indicators do not give accurate signals: 50 MA crossed 100 MA.

MACD histogram is near the 0 mark.

The Stochastic Oscillator is located in the neutral zone, the %K line is above the %D line, which indicates a bullish mood. .

- Support levels: 1.29400, 1.28750

- Resistance levels: 1.29800, 1.30100, 1.30450

If the price fixes above 1.29800, expect the quotes to rise toward 1.30200-1.30500.

Alternatively, the quotes could descend toward 1.29000-1.28800.

The USD/CAD currency pair

- Prev Open: 1.32870

- Open: 1.32516

- % chg. over the last day: -0.23

- Day’s range: 1.32406 – 1.32646

- 52 wk range: 1.2949 – 1.3566

Bearish sentiment prevails on the USD/CAD currency pair. The trading instrument has set new local lows. At the moment the CAD is consolidating. The key range is 1.32400-1.32700. The technical pattern signals further correction of USD/CAD quotes. Additional support for the Canadian dollar is provided by the oil price recovery. Positions should be opened from key levels.

The Economic News Feed for 13.02.2020:

Indicators point to the strength of sellers: the price has fixed below 50 MA and 100 MA.

Histogram of MACD is in the negative zone, which indicates a bearish sentiment.

The Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which gives a signal to buy USD/CAD.

- Support levels: 1.32400, 1.32200, 1.31900

- Resistance levels: 1.32700, 1.33000, 1.33250

If the price fixes below 1.32400, expect further movement toward 1.32000.

Alternatively, the quotes could grow toward 1.32900-1.33100.

The USD/JPY currency pair

- Prev Open: 109.783

- Open: 110.071

- % chg. over the last day: +0.13

- Day’s range: 109.748 – 110.090

- 52 wk range: 104.45 – 113.53

The USD/JPY currency pair is consolidating near the two-month highs. The technical picture is ambiguous. At the moment local support and resistance levels are at 109.700 and 110.150, respectively. Technical correction is not ruled out in the nearest future. Today we recommend to pay attention to the economic releases, as well as the dynamics of the US government securities yield. Positions should be opened from key levels.

The news background on Japanese economy is calm.

Indicators do not give an accurate signal: 50 MA crossed 100 MA.

MACD histogram is near the 0 mark. No signals at the moment.

The Stochastic Oscillator is located in the oversold area, the %K line has crossed the %D line. There are no signals at the moment.

- Support levels: 109.700, 109.550, 109.300

- Resistance levels: 110.150, 110.400

If the price fixes above 110.150, consider buying USD/JPY. The movement will tend toward 110.400-110.600.

Alternatively, the quotes could correct toward 109.400-109.200.

by JustForex