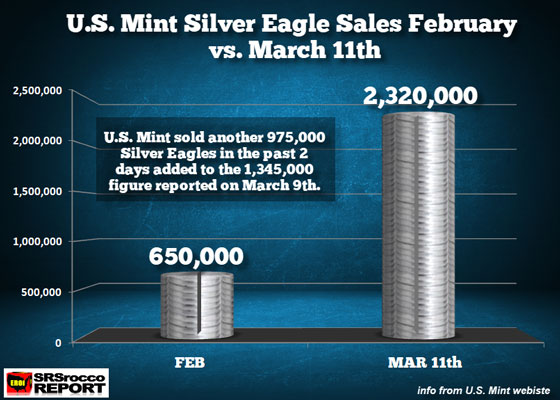

With the spread of the Global Contagion, the demand for physical precious metals has increased significantly. According to the U.S. Mint’s newest update, another million Silver Eagles were sold over the past two days. This brings to total Silver Eagle sales in March at 2.3 million, more than three times the previous month.

On my last update, the U.S. Mint sold a total of 1,345,000 Silver Eagles as of March 9th. Over the next two days, another 975,000 Silver Eagles were sold for a total of 2,320,000.

We haven’t seen this type of buying for quite some time. The U.S. Mint doesn’t sell Silver Eagles directly to the public, but rather to Authorized Purchasers who sell to the public. So, these sales figures represent purchases by the Authorized Dealers. Regardless, if the Authorized Dealers are buying a great deal more Silver Eagles in March, they are doing so because they are experiencing much higher demand from the public.

However, there may be a problem shortly for the Authorized Dealers if the U.S. Mint runs out of stocks of Silver Eagles. Why? Because, the U.S. Mint has cut back on monthly production runs of Silver Eagles due to the decreased demand for the past few years. I doubt the U.S. Mint will be able to supply another 1-2 million Silver Eagles in a short period of time. Thus, we may see the U.S. Mint suspend sales of Silver Eagles shortly until they can increase stocks.

If you do not own any physical precious metals, it may be a good idea to start DIVERSIFYING some assets into Gold and Silver. With the continued spread of the Global Contagion and coming disruptions in the Just-In-Time Inventory Supply Chain, it’s highly likely that demand for precious metals will only increase going forward. With rising demand and constrained supply, we may start to see much higher prices for gold and silver.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

By CentralBankNews.info The Federal Reserve Bank of New York, which implements U.S. monetary policy, is injecting massive amounts of liquidity into financial markets to ensure they continue to function smoothly and address “highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak.” Following instructions from Federal Reserve Chair Jerome Powell, the Open Market Trading Desk of the New York Fed said in a statement it was changing the maturity composition of its planned purchases to support the functioning of the market for Treasury securities, and also adding term repo operations “in large size” to enhance the functioning of dollar funding markets. The New York Fed, which already boosted its supply of liquidity by raising the amount of overnight repo operations and 2-week repos on March 9 and March 11, today offered $500 billion in a 3-month repo operation and will offer the same amount in a 3-month repo operation on March 13. In addition, the New York Fed will offer $500 billion in a one-month operation on March 13, and said 3-month and one-month repo operations of $500 billion will be conducted on a weekly basis for the rest of this month. The trading desk added that it would continue to offer at least $175 billion in daily overnight repo operations and at least $45 billion in 2-week term repo operations twice a week during the same period. As part of the Fed’s scheduled $60 billion reserve management purchases for the month beginning March 13 and through April 13, the trading desk will purchase securities across a range of maturities to roughly match the maturity compositions of Treasury securities outstanding, specifically across 11 sectors, including bills, Treasury Inflation-Protected Securities, and floating rate notes. Reserve management purchases into the second quarter will continue to be conducted with this maturity allocation, the Fed said, with the terms adjusted as needed to foster smooth market functioning and effective policy implementation.

As the coronavirus spreads fear, sickness, and death, a specter haunts investors – the specter of deflation.

Despite central bankers’ attempts to push inflation rates higher, equity and commodity markets are collapsing. Inflation expectations as reflected in tanking U.S. Treasury yields, meanwhile, appear headed toward zero – and perhaps even below.

“I think that we have a real danger of deflation in the economy right now,” former Trump economic advisor Stephen Moore told Fox Business’ Maria Bartiromo last weekend.

Clearly, symptoms of deflation and leading indicators of economic contraction are now manifesting in dramatic ways:

Wall Street is being hit with the most severe selling wave since 2008.

Junk bonds are also selling off hard as investors fear a wave of corporate defaults to come.

Crude oil has suffered its worst plunge in decades.

Economic growth in Asian and European countries is turning negative.

The odds of a recession hitting the U.S. this year are now 50%, according to Moody’s Analytics.

But before investors jump on the deflation bandwagon, they should carefully consider the monetary and political forces that could be deployed to reverse a whiff of deflation.

Stephen Moore – who was once floated by President Donald Trump as a nominee to the Federal Reserve Board – is now urging the Fed to reinflate the economy. “I think the Fed should be proactive. I want more dollar liquidity in the economy,” he told Bartiromo.

More rate cuts are coming – markets are currently pricing in a further 75 basis-point reduction in the Fed funds rate – and possibly some unconventional liquidity injections as well.

Meanwhile, President Trump is pitching a payroll tax cut and other fiscal stimulus measures intended to supply consumers with more cash to spend into the economy.

Once the threat of deflation becomes a top concern of central bankers and politicians, it is likely to have already run its course… or have little room left to run. Deflation scares tend to be sudden and severe but ultimately short-lived.

As an investment thesis, deflation lacks a long-term driver.

The reality is that deflation will never persist for very long while our inflationary fiat monetary system remains in place.

Obviously, there are no signs the Fed is going to close up shop anytime soon. Both Democrats and Republicans depend on it to fuel their spending and borrowing priorities. And both parties favor easy-money policies.

The old adage, “Don’t fight the Fed” is worth heeding.

The last deflation scare in 2008 led to Zero Interest Rate Policy, Quantitative Easing, and unprecedented Fed balance sheet expansion. A generational buying opportunity emerged in U.S. stocks. While most on Wall Street expected a bear market rally, few predicted a massive bull market that would last for over a decade.

Initially, all asset classes rose out of their 2008-2009 bottoms. Commodities and precious metals, which had delivered standout gains in the years leading up to the 2008 financial crises, resumed leadership into 2011.

As gold and silver topped out in 2011, the U.S. stock market became the prime beneficiary of monetary expansionism in succeeding years.

Today investors seem convinced that once the Wuhan virus crisis abates, the S&P 500 will bounce back and become the place to be for years more to come.

More likely, the current turmoil in markets – and the central bank response – will effect markets in ways that stock market bulls aren’t expecting.

One surprising development currently taking place is that instead of serving as a traditional safe haven, the U.S. dollar is actually dropping precipitously verses foreign currencies. Consequently, foreign developed and emerging markets are often falling less drastically in dollar terms during big down days than U.S. stocks are.

Meanwhile, the strongest currency in 2020 has been gold – up better than 10% for the year. One of gold’s most under-appreciated functions is that of a deflation hedge. When risk assets are being liquidated, an ensuing flight to quality includes gold and Treasuries.

U.S. government bonds have performed spectacularly in 2020. In fact, bonds have been in a super-cycle bull market for nearly 40 years!

In recent years, many bond skeptics have prematurely called a top. But with rates across the entire yield curve plunging below 1% this week, we are now getting close to the point where it will become mathematically impossible to milk bonds for the kind of returns they have delivered in the past.

There is asymmetric downside risk to bondholders given the possibility that inflation fears reemerge. The real losses on 30-year bonds bought with a yield 0.9% would be staggering if inflation merely averages the Fed’s target rate of 2% over that period.

With the bond bubble having little room left to expand and potentially nearing a prick that will burst it… and with a stock market bubble potentially having just burst, where will investors find the next great bull market?

Perhaps in asset classes that have been depressed for many years. No asset class has been more beaten up for longer than commodities. Narrowing down to the precious metals space, it’s hard to find any market more undervalued than silver.

The white metal is now historically cheap versus gold – selling recently at its largest discount to gold (1/98th the gold price) since 1991. This in part reflects how lopsided the deflation trade has become. Unlike gold, silver is more of a pure play on inflation.

When the powers that be finally succeed in staving off the deflation threat with inflationary injections of fiat currency into markets and pocketbooks, new investment trends will take hold. The coming inflation will lift hard assets in general – and could launch silver explosively higher in particular.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

With COVID-19 as the leading issue affecting the markets, we want to keep a close eye on consumer sentiment.

This time around we are focusing on the world’s largest economy. But the reasons for caring about consumers apply to pretty much most of the world now that the WHO has declared COVID-19 a pandemic.

The initial concern, which drove the first drop in global capital markets, was the potential impact on supply chains for businesses. The closure of production facilities in the world’s manufacturing area – China – meant that businesses might have increased difficulty in sourcing materials.

For retailers, it meant potentially running out of products. And, for manufacturers, it meant potential production stoppages. However, shortages did not materialize, and over the last couple of weeks, most major companies in the US and Europe have issued updates on their supplies and inventory.

Business Situation vs Consumer Situation

Most businesses issued profit warnings due to foreseen writedowns they’d make during Q1 from COVID-19-related effects. But all clarified that their supply issues were in hand and they had sufficient inventory.

While it might cause some additional stress on some companies’ financials, none said they were experiencing serious difficulties.

If a company has to delay production slightly due to supply issues, it generally isn’t a major concern. After all, you still make the sale, you just make it a little later!

But if consumer sentiment deteriorates, this implies a bigger problem. This is because it means people are less willing to buy. Supply issues can be addressed with alternate sourcing or other internal measures. However, a drop in buying will have a lasting, negative impact on the business sector and the economy as a whole.

Panic into a Recession

With COVID-19 spreading through the US, many worry America will implement economic measures to fight the disease that other countries have already done. That means restricting shopping and entertainment.

This is likely to massively impact consumer sentiment, especially if it leads to panic shopping as it has in Australia, Germany, Italy among others.

People buy what they believe are emergency supplies with what little money they have, leaving aside major purchases. Once they’ve “stocked up” they don’t have any need to buy more. And with consumption failing, businesses have to reduce production.

This scenario is already being considered in the financial sector. We’re seeing mortgage rates going up despite the Fed slashing rates and bond yields falling. This is because lenders are factoring an increased risk of defaults during an upcoming economically stressful period.

What We Are Looking For

Most of the upcoming Michigan Consumer Sentiment survey was carried out ahead of the sudden drop in the stock market. Therefore, we might not see that fully reflected yet.

Current expectations are for it to remain just slightly in expansion territory at 101.2 compared to 101.0 prior. That will probably be the last increase in the upward trend since September of last year.

Projections indicate that Michigan Consumer Expectations may decrease to 89.0 from 92.1. This reflects a negative outlook for the US economy as COVID-19 was already blanketing the news at this point.

The market is likely expecting this figure to underperform, given the recent events.

By CentralBankNews.info Ukraine’s central bank lowered its policy rate for the 7th time to boost the economy further as inflationary pressures are declining faster than expected as it continues with its plan to lower the rate to 7.0 percent by the end of this year. The National Bank of Ukraine (NBU) cut its rate by another 100 basis points to 10.0 percent and has now cut it by 800 points since it began the easing cycle in April 2019. In deciding on the pace of cutting its rate to 7.0 percent, NBU said it was closely monitoring the spread of the coronavirus and its impact on the domestic and global economy, the response of other governments and central banks, and progress in talks with the International Monetary Fund on a new aid agreement. “If there are favorable developments, and if the new Ukrainian government speeds up reform, the NBU will be able to ease its monetary policy more quickly” but conversely if “above risks materialize, the NBU will respond quickly by deploying the monetary tools if has at its disposal,” the central bank said. Although the spread of the coronavirus has had a “limited or neutral” impact on the country’s economy despite increased nervousness in financial markets, the central bank noted the global spread could, if realized, drive the global economy into recession and cause a significant slowdown in Ukraine’s economy by hitting trade and making it more difficult for its to obtain financing. But so far, NBU said its exports were continuing to rise while import prices, especially for energy, were falling faster than export prices, and overall effect of lower energy prices on Ukraine’s economy and inflation will be mixed, adding to uncertainty. Ukraine’s inflation rate fell to 2.4 percent in February, below the central bank’s target of 5.0 percent, plus/minus 1 percentage point. Ukraine’s parliament has not yet passed legislation dealing with land and banking reforms that are needed for final approval of a new $5.5 billion, 3-year loan package that was preliminarily agreed with the IMF.

The National Bank of Ukraine issued the following statement:

“The Board of the National Bank of Ukraine has decided to cut the key policy rate to 10% per annum effective 13 March 2020. The NBU continues its monetary policy easing, as predicted, in order to bring inflation back to its target range of 5% +/- 1 pp and to support economic growth in Ukraine amid a cooling global economy.

The first months of the year show that inflationary pressures are waning faster than the NBU expected

In January–February, consumer inflation declined faster than foreseen in the forecast trajectory (reaching 3.2% yoy in January and 2.4% in February), remaining below the target range of 5% +/- 1 pp. Core inflation was also lower than forecast during this period.

The faster disinflation was driven by the sustained effects of the last year’s hryvnia appreciation on prices of goods, large supplies of the majority of raw foods, and lower energy prices. These factors offset the effect of robust consumer demand, which was bolstered by the continued growth in real household income.

In January the NBU forecast inflation at 4.8% as of the end of 2020, but this forecast may be reviewed in April depending on further developments

So far, the global spread of the novel coronavirus has had a limited or neutral impact on the economy of Ukraine. Ukraine’s exports continue to rise. Further increases in physical volumes of exports have more than offset certain declines in prices for some of the goods the country exports. At the same time, import prices (especially energy prices) are declining even faster than export prices.

Uncertainty over the spread of the novel coronavirus, and stronger turbulence on financial and commodity markets saw the Ukrainian FX market respond with deteriorated sentiment and increased nervousness.

However, the following consequences of the spread of the coronavirus have not yet impacted the economic activity and inflation in Ukraine:

the downward pressure on prices and cooling of the global economy

monetary policy easing by central banks of the leading economies and Ukraine’s trading partners in response to these processes

measures taken by governments to prevent the spread of COVID-19.

Apart from the drop in global prices caused by the coronavirus, disinflation in Ukraine will be driven by the recent rise in competition between crude oil producers. This will keep energy prices at record lows, which will also impact prices for Ukrainian exports.

Overall, the effect of all these factors on economic growth and inflation in Ukraine will be mixed, adding to the uncertainty.

The NBU Board relied on the key assumption that cooperation with the IMF continues

Signing a new agreement with the IMF will make the Ukrainian economy less vulnerable in a time of turbulent global markets and during a period of heavy public debt repayments. Investors’ perception of Ukraine will also depend on Ukrainian court rulings on the responsibility and liabilities to the state of the former owners of insolvent banks.

The risk arising from the global spread of the novel coronavirus could, if realized, drive the global economy into a recession and cause a significant slowdown in the Ukrainian economy. A dramatic decline in global demand and investors’ revaluation of risks related to developing economies could negatively affect Ukraine’s external trade and make it more difficult for Ukraine to obtain financing.

There are other significant risks. They include:

an escalation of the military conflict in eastern Ukraine and new trade restrictions being introduced by Russia

a drop in the harvest of grain, fruit and vegetable crops in Ukraine in the wake of unfavorable weather

the higher volatility of global food prices, driven by global climate change

Therefore, the NBU Board made its key policy rate decision when inflationary pressures were decreasing faster than expected, and the economy needed further support.

In view of the above, the NBU Board continued its monetary policy easing cycle by cutting the key policy rate by 1 pp, to 10%, as envisaged by the central bank’s January forecast. This will give the required impetus to the economy.

As before, the NBU plans to decrease its key policy rate to 7% by the end of the current year

In deciding on the pace of key policy rate cuts to that level, the NBU will closely monitor:

the spread of the coronavirus around the world and in Ukraine, and its impact on the domestic and global economy

the response of governments and central banks to these developments

any progress achieved in negotiating a new aid agreement with the IMF, which will shape the expectations of financial market participants, and determine the prices of Ukrainian assets.

If there are favorable developments, and if the new Ukrainian government speeds up reform, the NBU will be able to ease its monetary policy more quickly.

Conversely, if the above risks materialize, the NBU will respond quickly by deploying the monetary policy tools it has at its disposal.

The decision to cut the key policy rate to 10% was approved by NBU Board Decision No.172-D On the Key Policy Rate,dated 12 March 2020.

A summary of the discussion by Monetary Policy Committee members that preceded this decision will be published on 23 March 2020.

The next meeting of the NBU Board on monetary policy issues will be held on 23 April 2020 as scheduled.”

By CentralBankNews.info The European Central Bank (ECB) surprised financial markets by maintaining its key interest rates, which are essentially already at the zero lower bound, but boosted its purchases of assets by 120 billion euros and will launch a new round of targeted longer-term refinancing operations (TLTROs) to “support bank lending to those affected most by the spread of the coronavirus, in particular small and medium-sized enterprises.” The ECB, the central bank for the 19 countries that share the euro currency, has maintained its benchmark refinancing rate at 0.0 percent and the lending rate key at 0.25 percent since March 2016, but lowered its deposit rate in September 2019 to the current level of minus 0.50 percent. “Although the Governing Council does not see material signs of strains in money markets or liquidity shortages in the banking system, these operations will provide an effective backstop in case of need,” the ECB said, referring to additional longer-term financing operations. The ECB confirmed its earlier guidance that it expect key rates to “remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below 2% within its projection horizon…” A new round of targeted longer-term financing operations (TLROs) will begin in June and run until June 2021 but to bridge this gap, the ECB said it would conduct additional longer-term financing operations (LTROs) at fixed rate tenders will full allotment at a rate that is equal to the average rate on the deposit facility to “provide immediate liquidity support to the euro area financial system.” TLTROs became part of the ECB’s non-standard monetary policy tools in 2014 and a second one, known as TLTRO-II, was launched in March 2016. Banks that participated in those programs were able to borrow up to 30 percent of their outstanding loans to businesses and consumers, boosting the amount that banks can lend to the real economy at lower interest rates than the ECB normally offers. Loans under TLTRO-III will be on more favorable terms, the ECB said, to support lending to business most affected by the spread of the coronavirus, known as Covid-19, with interest rates as low as 25 basis points below the average interest rate on the main refinancing operations. For banks that maintain their levels of credit provision, the rate applied on these operations will be as low as 25 basis points below the average deposit facility over the period ending in June 2021. In addition, the maximum amount that banks can borrow under TLTRO-III is raised to 50 percent of their outstanding loans, and the ECB will look into collateral easing measures. In September last year the ECB restarted an earlier asset purchase program – known as quantitative easing (QE) – and began to purchase assets worth 20 billion euros from Nov. 1, 2019. The earlier asset purchase program was completed at the end of 2018 after the ECB had accumulated some 2.6 trillion euros of bonds. Today, the ECB said “a temporary envelope” of additional net asset purchases of 120 billion will be added until the end of the year and in combination with the existing asset purchase program (APP) will “support favorable financing conditions for the real economy in times of heightened uncertainty.” The ECB confirmed its earlier guidance that it expects these asset purchases to “run for as long as necessary to reinforce this accommodative impact on its policy rates, and to end shortly before it starts raising the key ECB interest rates.” Reinvestments from its maturing securities purchased under APP will also continue “for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favorable liquidity conditions and an ample degree of monetary accommodation.”

The European Central Bank released the following monetary policy statement and a statement regarding banking supervision:

“At today’s meeting the Governing Council decided on a comprehensive package of monetary policy measures:

(1) Additional longer-term refinancing operations (LTROs) will be conducted, temporarily, to provide immediate liquidity support to the euro area financial system. Although the Governing Council does not see material signs of strains in money markets or liquidity shortages in the banking system, these operations will provide an effective backstop in case of need. They will be carried out through a fixed rate tender procedure with full allotment, with an interest rate that is equal to the average rate on the deposit facility. The LTROs will provide liquidity at favourable terms to bridge the period until the TLTRO III operation in June 2020.

(2) In TLTRO III, considerably more favourable terms will be applied during the period from June 2020 to June 2021 to all TLTRO III operations outstanding during that same time. These operations will support bank lending to those affected most by the spread of the coronavirus, in particular small and medium-sized enterprises. Throughout this period, the interest rate on these TLTRO III operations will be 25 basis points below the average rate applied in the Eurosystem’s main refinancing operations. For counterparties that maintain their levels of credit provision, the rate applied in these operations will be lower, and, over the period ending in June 2021, can be as low as 25 basis points below the average interest rate on the deposit facility. Moreover, the maximum total amount that counterparties will henceforth be entitled to borrow in TLTRO III operations is raised to 50% of their stock of eligible loans as at 28 February 2019. In this context, the Governing Council will mandate the Eurosystem committees to investigate collateral easing measures to ensure that counterparties continue to be able to make full use of the funding support.

(3) A temporary envelope of additional net asset purchases of €120 billion will be added until the end of the year, ensuring a strong contribution from the private sector purchase programmes. In combination with the existing asset purchase programme (APP), this will support favourable financing conditions for the real economy in times of heightened uncertainty.

The Governing Council continues to expect net asset purchases to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates.

(4) The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.50% respectively. The Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

(5) Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Further details on the precise terms of the new operations will be published in dedicated press releases this afternoon at 15:30 CET.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:30 CET today”

——

“ECB Banking Supervision provides temporary capital and operational relief in reaction to coronavirus

12 March 2020

Banks can fully use capital and liquidity buffers, including Pillar 2 Guidance

Banks will benefit from relief in the composition of capital for Pillar 2 Requirements

ECB to consider operational flexibility in the implementation of bank-specific supervisory measures

The European Central Bank (ECB) today announced a number of measures to ensure that its directly supervised banks can continue to fulfil their role in funding the real economy as the economic effects of the coronavirus (COVID-19) become apparent.

“The coronavirus is proving to be a significant shock to our economies. Banks need to be in a position to continue financing households and corporates experiencing temporary difficulties. The supervisory measures agreed today aim to support banks in serving the economy and addressing operational challenges, including the pressure on their staff,” said Andrea Enria, Chair of the ECB Supervisory Board.

Capital and liquidity buffers have been designed with a view to allowing banks to withstand stressed situations like the current one. The European banking sector has built up a significant amount of these buffers. The ECB will allow banks to operate temporarily below the level of capital defined by the Pillar 2 Guidance (P2G), the capital conservation buffer (CCB) and the liquidity coverage ratio (LCR). The ECB considers that these temporary measures will be enhanced by the appropriate relaxation of the countercyclical capital buffer (CCyB) by the national macroprudential authorities.

Banks will also be allowed to partially use capital instruments that do not qualify as Common Equity Tier 1 (CET1) capital, for example Additional Tier 1 or Tier 2 instruments, to meet the Pillar 2 Requirements (P2R). This brings forward a measure that was initially scheduled to come into effect in January 2021, as part of the latest revision of the Capital Requirements Directive (CRD V).

The above measures provide significant capital relief to banks in support of the economy. Banks are expected to use the positive effects coming from these measures to support the economy and not to increase dividend distributions or variable remuneration.

In addition, the ECB is discussing with banks individual measures, such as adjusting timetables, processes and deadlines. For example, the ECB will consider rescheduling on-site inspections and extending deadlines for the implementation of remediation actions stemming from recent on-site inspections and internal model investigations, while ensuring the overall prudential soundness of the supervised banks. In this context, the ECB Guidance to banks on non-performing loans also provides supervisors with sufficient flexibility to adjust to bank-specific circumstances. Extending deadlines for certain non-critical supervisory measures and data requests will also be considered. In the light of the operational pressure on banks, the ECB supports the decision by the European Banking Authority to postpone the 2020 EBA EU-widestress test and will extend the postponement to all banks subject to the 2020 stress test.

Banks should continue to apply sound underwriting standards, pursue adequate policies regarding the recognition and coverage of non-performing exposures, and conduct solid capital and liquidity planning and robust risk management.

These actions follow a letter sent on 3 March 2020 to all significant banks to remind them of the critical need to consider and address the risk of a pandemic in their contingency strategies. Banks were asked to review their business continuity plans and consider what actions could be taken to enhance preparedness to minimise the potential adverse effects of the spread of the coronavirus. ECB Banking Supervision will engage with banks to ensure the continuity of their critical functions. The ECB Supervisory Board is monitoring developments; these measures will be revised as necessary.”

French CPI isn’t usually one to trade. However, with all the noise surrounding coronavirus, this particular print might be a little more sensitive than usual.

The German CPI, on the other hand, will be one to keep a closer eye on. In case we get a negative print, and the French figures align with that result, then we could see markets falling harder.

French CPI At Better Levels Than the German Rate

The CPI in France increased to 104.55 points in February from 104.54 points in the previous month. The latest numbers are expected to stay in line with the previous readings, at 0.0%.

Interestingly, the strongest ever CPI posted by France was back in Dec 2019.

The CPI in Germany increased to 105.60 points in February from 105.20 points from the previous month. The latest numbers are expected to stay in line with the previous readings as well, at 0.4%.

At the start of the first quarter, the German economy showed signs of an improving economy compared to the last 2 years. Over that period, German indicators showed poor growth and a slowdown in economic activity overall.

Why Are Economists Alarmed?

Coronavirus will have a say in next month’s release as it is affecting most European economies and it’s likely to affect the rates going forward.

On top of that, we’ve seen the prices of oil deteriorating at an extremely alarming rate too. With crude down too, inflation will again be affected in energy terms, at least.

However, for the current estimates, economists are not and cannot rely on forward rates to calculate estimates. They need to look at existing figures. That said, all-item HICP has fallen in January from 1.4% to 1.2% on a year-on-year basis.

A major drop from 1.9% to -0.3% is expected to be seen in energy-related inflation. However, some of this will be offset by the food, alcohol and tobacco-related inflation, and particularly from unprocessed food. This is expected to increase from 2.3% to 2.7% on a year-on-year basis.

When looking at January’s CPI, this came out at -0.7% on a month-on-month basis. Growth is out of the question and the print drifts further away from the 2.0% target the ECB wants to achieve.

Will the EURO be Affected by the CPI Prints?

Well, with the ECB surprising markets, things could take a different turn. While usually, we can expect at least the German CPI to move the markets a bit, on this occasion, perhaps we won’t, despite the environment being more sensitive.

Now imagine though that the numbers come out positive for both Germany and France. Would you attempt to buy against a falling knife?

It was another brutal day for stock markets as Wall Street hit critical circuit breaker levels only minutes after the US opening bell on Thursday!

The S&P 500 tumbled 7% consequently halting all trading on the New York Stock Exchange for 15 minutes. Even when US markets restarted, all major indices fell below -8% as risk aversion intensified on fears around the coronavirus global pandemic. With investors are clearly keep a safe-distance from riskier assets amid the chaos, US stocks are positioned to extend loses which could trigger the level 2 circuit breaker – marked as a 13% decrease against the prior day’s S&P 500 closing price.

Focusing on the technical picture, the S&P 500 is heavily bearish on the daily charts. A solid daily close below 2500 could open the doors towards 2450.

It was the same story with the Dow Jones with bears in the driving seat as prices tumbled over 7.5%. Prices are approaching the 21500 support level as of speaking. Weakness below this level could encourage a decline Ttowards 21300.

One would have expected Gold prices to exploit the risk aversion but this was not the case on Thursday afternoon.

The precious metal found itself under renewed selling pressure, shedding over 3% as institutions and traders offloaded their Gold holdings to cover margin requirements for stocks. An appreciating Dollar also added to the pain with prices trading marginally below $1580 as of writing.

A solid daily close below this level should open the doors towards $1555.

Currency spotlight – GBPUSD

A growing sense of unease over how badly the coronavirus outbreak will hit the UK economy is haunting investor attraction towards the British Pound.

Market players are waiting for fresh details on the U.K response to the coronavirus pandemic after the emergency rate cut earlier this week. The overall uncertainty should result in the Pound weakening against the Dollar and other G10 currencies in the short to medium term.

The GBPUSD is trading around 1.2626 as of writing and could test 1.2550 in the short term.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The current bearish structure on AUDUSD suggests that the cycle-degree correction might not have ended just yet. Wave c, which marks the end of the primary wave ⑤ as well, could slide further down for a fresh low below the 63c. round support (either for a false break or for an extended 5th wave).

When keeping the sharp drop in mind, a range can be expected.

Adding to that the rule of alternation (particularly for multiple degree impulse waves), the decline into intermediate wave (5) then could reinitiate following the breakout of a triangular formation.

Perhaps, this could come in as a standard or a complex zigzag too, as all we need is a longer sideways market when compared to minor wave 2.

Judging by the structure, however, it is possible than the latest decline is part of a zigzag correction. This intermediate degree alternative, of course, suggests that we’ve marked a multiyear support at the pin bar low and prices are now reversing up.

With primary wave ① completed, the current formation indicates than we’re likely to see a bounce at some level near the 63,43c. level. This is the 90% Fibonacci retracement and could be the last sign bulls can expect.

Should we see a bounce anywhere above the previous low (but not at the previous low), then this will likely shoot higher to fresh multiweek highs. The primary wave ③ will cross above ①, unless if a more complex corrective structure invalidates both scenarios analyzed here.

Crude oil prices have remained under pressure this week in response to the latest data from the Energy Information Administration.

The data showed a further rise in US crude stores. The report covering the week ending March 6th showed that US crude stores jumped by 7.7 million barrels.

This latest inventory increase came above the expected 2.3 million barrel increase and casts further concern over the global oil demand environment.

However, the report was not totally bearish. The EIA reported a 5 million barrel drop in gasoline inventories, outstripping expectations of a 2.5 million barrel drop. Distillate stockpiles were also lower by 6.4 million barrels, versus an expected drop of 1.9 million barrels.

EIA Slashes Demand Outlook

Along with the latest build in US crude stores, the EIA has also slashed its global oil demand projections.

The administration now forecasts global oil demand to decrease by 910k barrels per day over Q1 and by 6660k barrels per day over the year.

The EIA cited the global impact of the ongoing coronavirus outbreak which is threatening to push the global economy into a recession. In the US, forecasts indicate that demand will fall by 350k barrels per day over Q1, a further reduction from the prior 260k barrel per day forecast.

Russia & Saudi Arabia Clash

Crude prices have also come under pressure from the tensions between Russia and Saudi Arabia over crude production levels.

Russia refused to join OPEC in increasing its oil production cuts. In response, Saudi Arabia announced that it will now massively increase its oil production in a bid to force Russia to agree to step up production cuts or risk a further collapse in oil prices.

This latest development highlights the growing concern around the fall in oil prices. Crude prices are now down by nearly 50% since the start of the year.

Technical Perspective

The technical picture in Crude at the moment is currently best viewed on the higher timeframes where you can clearly see the extent of the collapse in prices this year.

Following the gap lower at the start of the week, price traded as low as 27.41, just ahead of testing the 26.21 2016 lows. Price has so far recovered to 33.19 last. However, while price remains below the 42.40 broken support, further downside looks likely.