The MSCI Asia Pacific Index is set to notch back-to-back gains for the first time in nearly three weeks, following the US stock market’s best session in 12 years. However, with US equity futures now in the red, it reinforces the notion that risk appetite is still struggling to find a firm footing, and the advances in global equities remain tentative at best.

With global stock markets seemingly closer to the bottom than to the top at this stage, investors who have been bruised by the stunning selloff in recent weeks are now desperate for any form of comfort, with the rollout of stimulus packages across the global economy being the likeliest source. Given the Fed’s plans for unlimited quantitative easing, the eagerly-anticipated $2 trillion US economic stimulus package, and Europe’s plans to unleash credit lines to the region, global stocks may be given cause to climb higher still over the near term.

Yet, the immediate efficacy of the broad swathes of support measures remains in doubt, given that the depth and the duration of the supply and demand shocks remain far from certain at this point in time. Hence it is uncertain whether recent advances in the stock markets will stick, considering that investors are still fearing the worst over Covid-19’s eventual toll on the global economy. With the VIX still at its highest levels since the global financial crisis, investors can expect to brave through choppy waters for a while longer.

Dollar moderates … but not by much

The Dollar index (DXY) has moderated below the 102 handle, after the Federal Reserve’s announcement over its plans for unlimited quantitative easing prompted broad-based easing in the Greenback. The Fed’s recent efforts to ease the Dollar-funding crunch, after opening up swap lines with more central banks around the world, have also offered some measure of relief for the broader currency complex.

Should Congress pass the $2 trillion US economic support package, that may lead to further waning in the Greenback as risk appetite attempts a comeback. However, persisting fears over a looming global recession are expected to mitigate any near-term declines for the Greenback, considering the refuge that King Dollar offers investors during times of economic turmoil.

Gold’s revival set to kick on

Gold is seeing a resurgence after breaching the psychological $1600 level. The swathes of fiscal and monetary support packages being rolled out around the world has fueled the tailwinds in Gold, as the liquidity-related selloff gives way to a buying spree that’s more corelated with fears of an impending global recession.

Oil’s gains may slip from investors’ fingers

Brent futures continue to be suppressed below $30/bbl, and would require a fundamental revival in order to see a sustained rise. While hopes of a $2 trillion US stimulus packages may offset some of the demand-side concerns, its impact on Oil prices are expected to be limited, considering the risk of global markets being inundated with cheap supplies amid the OPEC+ price war.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

When a trend is strong, related markets tend to move in unison.

However, when a trend is near exhaustion — a bullish or bearish trend, “non-confirmations” often occur. A non-confirmation occurs when one market makes a new high (or low), but a related market does not.

As cases in point, our November Global Market Perspective discussed the details of the non-confirmations in Europe as it showed two charts. Here’s the first:

The Euro Stoxx 50, the DAX and the FTSE 100 (top three graphs) have so far failed to confirm new multi-year highs in the CAC 40 and the Swiss Market Index (bottom two graphs).

Here’s the second chart with continued commentary:

The chart depicts [a] critical loss of juice in Britain’s higher-beta indexes. Notice that while the FTSE 100 is off 6% since its May 2018 high, the Small-Cap index and the AIM 100 are down 9% and 23%, respectively. These non-confirmations are important, because markets almost always splinter when big changes in social mood are afoot. … It’s only a matter of time before the broad indexes abandon the bull-market party.

As we all know, abandon it they did — big-time!

The media blamed the big plunge in global stock market values on the coronavirus.

Yet, it’s notable that our global analysts’ forecast for the end of Europe’s “bull-market party” occurred about two months before the coronavirus flared up in China — and six weeks before the outbreak hit Europe.

So, clearly, our bearish European forecast was not based on the coronavirus.

Elliott Wave International analysts base their financial forecasts on the Elliott wave model plus technical and sentiment indicators, not the news.

As the Wall Street classic Elliott Wave Principle: Key to Market Behavior by Frost & Prechter noted:

Sometimes the market appears to reflect outside conditions and events, but at other times it is entirely detached from what most people assume are causal conditions. The reason is that the market has a law of its own. It is not propelled by the external causality to which one becomes accustomed in the everyday experiences of life. The path of prices is not a product of news. Nor is the market the cyclically rhythmic machine that some declare it to be. Its movement reflects a repetition of forms that is independent both of presumed causal events and of periodicity.

Now is the time to get insights into what really governs the path of stock market prices — the Wave Principle.

You can do so by reading the online version of Elliott Wave Principle: Key to Market Behavior — free. This free access to the Wall Street classic is available when you join Club EWI. Membership is also 100% free.

You can have this “must read” book on your computer screen in just moments. Get started.

Export ports in some countries may limit their work due to coronavirus

The main reason for the increase in grain prices is the return of China to the US market. As part of the first phase of the trade deal between the two countries, China pledged to buy agricultural products from the US worth $12.5 billion in 2020 and $19.5 billion. in 2021. U.S. Agriculture Department reported that so far, China has bought 756 thousand tons of American corn with delivery in the 2019/20 marketing year. This is the biggest deal since 2017. Also, an important reason for the growth of all agricultural products in price can be dockers’ strikes in the ports of developing exporting countries. They are afraid of getting infected by coronavirus and require quarantine. Particularly, the strike may begin in the largest Brazilian port of Santos in Sao Paulo. A similar demand was made by dockers of the Argentine port of Rosario and dockers of ports of South Africa. Note that corn quotes are now under pressure from low world oil prices. In the United States, 39% of corn is processed into ethanol and bio-fuels, which compete with oil. Accordingly, a rise in hydrocarbon prices may have a positive effect on corn quotes.

Shares of Total SA traded 14% higher today after the firm reported that has implemented a company-wide action plan to address the sharp decrease in oil prices.

Integrated oil and gas company Total S.A. (TOT:NYSE), today announced its immediate action plan to confront the recent sharp decline in oil prices.

The company stated in the report that on March 19, 2020, its Chairman and CEO Patrick Pouyanné addressed the group’s employees to mobilize them to face the challenges ahead. The firm noted that in Pouyanné’s remarks, “he recalled the resilience that the group’s teams demonstrated during the 2015-16 oil crisis as well as the two pillars of the group’s strategy which are the organic pre-dividend breakeven of less than $25/bbl and the low gearing to face this high volatility.”

The company advised that in the context of $30/bbl oil prices the firm reported an action plan to be implemented immediately. The plan will focus on three key areas of cap-ex reductions, operating costs savings and suspension of stock buybacks.

The company reported that it will cut its organic short-cycle flexible capital expenditures by $3 billion, a greater than 20% reduction of 2020 net investments to less than $15 billion.

The firm stated that it will now have increased 2020 operating costs savings of $800 million compared to 2019, versus the $300 million savings which was announced previously.

The company also stated that it was suspending its stock buyback program. The firm initially announced a $2 billion buyback for 2020 in a $60/bbl environment and stated that in the first two months of 2020 it had already bought back $550 million of its shares.

The company noted that it expects to release Q1/20 earnings during its conference call which is presently scheduled for April 30, 2020.

In a separate new release today, the company reported that in order to support healthcare staff of French hospitals who have been mobilized in the fight against the Covid-19 virus it will be supplying them with fuel for their travel. The firm indicated that it will provide hospitals with gasoline vouchers worth up to 50 million euros that can be used at Total stations.

Chairman and CEO Pouyanné commented, “In this period of crisis, Total’s teams remain mobilized to enable French people to make all their necessary travel arrangements. With its nationwide network, Total is working alongside those who are fighting the epidemic everywhere. Which is why the Group has decided to make this practical gesture of support for our hospital staff, who are working to ensure the health of patients.”

The firm additionally advised that “the Total Foundation will contribute 5 million to the Pasteur Institute and to hospital and health associations involved in the fight against Covid-19.”

Total SA is an oil and gas company headquartered in Paris, France. The firm has a market cap of over $140 billion, employs over 100,000 people and has active operations in more than 130 countries. Total is a major energy player that produces and markets fuels, natural gas and low-carbon electricity.

Total S.A. has a market capitalization of around $65.7 billion with approximately 2.586 billion shares outstanding. TOT shares opened higher today at $29.58 (+$4.16, +16.37%) over Friday’s $25.42 closing price. The stock has traded today between $28.17 and 29.58 per share and is currently trading at $29.18 (+$3.76, +14.79%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Seabridge founders Rudi Fronk and Jim Anthony provide an update on the Fed’s actions and the gold price.

Many times a day, we are asked what we think will be the impact on gold prices of the enormous money-printing by the Fed. We think the impact is much greater than you might imagine because it is in combination with huge fiscal stimulus. In a nutshell, we think the current path leads to a new all-time high in gold this year and a crisis of confidence in the dollar. It’s baked in the cake, in our view.

Please note, this is an opinion not investment advice.

Two points need to be made. First, most of the monetary stimulus to date is repo… money that must be returned in time certain and does not add to bank reserves. Repos unfreeze short-term liquidity but it’s the POMO…Permanent Open Market Operations or QE… that grows the balance sheet and bank reserves. There is much more QE to come, in our view, to keep mortgage rates down and bank balance sheets healthy (two Fed priorities). Repos have not satisfied the markets. To date, the Fed has announced $500 billion in new POMO Treasury purchases since COVID-19 of which more than half was used in the first few days. We expect new QE to total $4 trillion+ before the Fed is done.

Second, and most important, the fiscal stimulus is even greater and far more problematic than the monetary stimulus. Fiscal stimulus requires an enormous increase in an already huge deficit. If the Treasury seeks to borrow the extra $2 trillion or more that is sure to be authorized, the issuance would drive up Treasury yields which are already rising at the long end. The Fed will attempt to prevent this by purchasing the newly issued debt. The Fed is already funding about 70% of the current deficit (just follow the cusip numbers). So, QE this time around is not only going into financial markets like it did in 2009…a huge amount of it is going to flow through the Treasury and into the economy (payments to businesses and individuals, the real helicopter money), adding artificial demand at a time when the economy is producing less. This is very damaging to dollar confidence and highly inflationary.

We think the Fed and the Treasury have decided to sacrifice the dollar. We think they will be successful. Gold’s price will reflect this.

Written March 21, 2020.

This article is the collaboration of Rudi Fronk and Jim Anthony, cofounders of Seabridge Gold, and reflects the thinking that has helped make them successful gold investors. Rudi is the current Chairman and CEO of Seabridge and Jim is one of its largest shareholders.

Disclaimer: The authors are not registered or accredited as investment advisors. Information contained herein has been obtained from sources believed reliable but is not necessarily complete and accuracy is not guaranteed. Any securities mentioned on this site are not to be construed as investment or trading recommendations specifically for you. You must consult your own advisor for investment or trading advice. This article is for informational purposes only.

Disclosures: 1) Statements and opinions expressed are the opinions of Rudi Fronk and Jim Anthony and not of Streetwise Reports or its officers. The authors are wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the content preparation. The authors were not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the authors to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 2) Rudi Fronk and Jim Anthony: we, or members of our immediate household or family, own shares of the following companies mentioned in this article: Seabridge Gold. We personally are, or members of our immediate household or family are, paid by the following companies mentioned in this article: Seabridge Gold. 3) Seabridge Gold is a billboard sponsor of Streetwise Reports. Click here for important disclosures about sponsor fees. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

By TheTechnicalTraders – Our continuing research into the state of the Real Estate market suggests the Covid-19 virus event will likely put extreme pressure on many sectors within the US and global markets. This, Part III of a multi-part research article, will highlight many of the key economic data points that will soon be released and how these numbers may shock the markets. Additionally, as consumers and businesses prepare for an extended shutdown, it is important to understand the psychological process that takes place in the minds of people. PART I, PART II

Initially, people naturally hope for a quick and reasonable solution. As the process continues where an extended shutdown of the US economy persists, consumers and business managers change their expectations from optimism for a quick resumption of economic activity to “how do we survive this extended closure event”. This is when traders and investors really need to pay attention to what is happening in their local and national economies. One of the most important things to consider throughout an event like this is to watch how your local economy is operating and what is happening with local consumers. This will help you understand what is happening elsewhere.

Demand for certain items will continue almost as normal. We call this the Personal Consumer Essentials. These items are typically things like toilet paper, toothpaste, over the counter medications, underwear, food, and water. These are the types of purchases that must continue for average people to survive this type of event. Luxury items, vacations, extras, and other purchases may suffer throughout this process.

The first 30 days will likely be a transition period for many consumers. Remember, this is still the “hope” phase where consumers and business managers believe the entire thing will be over in 15 to 20 days and everything will go back to normal. We really need to start to watch how China is engaging in trying to restart their economy and how other nations are dealing with the virus contagion. Maybe the US will regain economic activity faster than other nations – maybe not. The key to all of this is when consumers and business managers feel confident enough to engage in opportunistic growth investments and purchases – not just survival purchases.

Let’s take a look at some of the key economic data that will be presented over the next 15+ days… But first, be sure to opt-in to our free market trend signals before closing this page, so you don’t miss our next special report!

Consumer Spending

If consumer spending falls below 0.5% for an extended period of time, the largest part of the US GDP calculation will have essentially vanished (consumers). This will result in decreased economic activity, taxes, income and have far-reaching economic complications across the globe. It is our belief that the initial phase of the US shutdown sparked a decent wave of consumer spending for survival supplies. As we move further into this shutdown event, we believe Consumer Spending could easily fall below 0.5% for an extended period of time – possibly many months.

We expect Jobless claims to skyrocket. We are hearing from local sources that the true number of unemployed in the US as a result of this virus event could be well above 4+ million right now. It will take time for these people to process into the system – so this will be an interesting number to watch. This number could send a shock-wave throughout the investment community as an extended rise in the jobless claims values would suggest a very deep recession is setting up. No jobs, no income, no asset appreciation – it’s simple.

Personal Income has fallen into severely negative territory only a few times over the past 30+ years. We believe income levels will play an important role in understanding the true scope of this potential economic event and how to plan for a potential Real Estate collapse in the future. If you are following our logic in posting these data points, you’ll quickly understand that Consumer Spending is related to a psychological consumer belief (either opportunistic or survival). This psychological belief is related to having a job and a solid source of income.

In the past, we’ve often referred to the global economy as a “living being” operating in a localized environment – like a plant. Typically, if the environment is healthy and abundant, the plant adopts a “growth phase” where it attempts to flower and expand into the environment. If the environment is unhealthy, the plant changes into a “survival phase” where it attempts to shed unneeded shoots and stems while trying to simply survive the unhealthy environment. The plant can’t get up and walk to a better environment – it is forced to operate in either of these modes because it has no other choices.

Within a global event like the Covid-19 virus event, we are like these plants that I’m describing. We can’t pack up and move to a better environment – we just have to deal with the phases and processes that are taking place within our environment – hoping to survive enough to be able to grow when the environment gets more healthy.

If personal income collapses, consumers will shift into a survival mode much quicker. This is similar to the environment turning completely toxic over just a few days.

Non-Farm Payroll data will also help us understand how toxic the economic environment has become in the US. We purposely included the 2008-09 data on this chart to show you how the payroll data turned negative in late 2007 and early 2008 – well before the collapse really started to happen. With the Covid-19 event taking place, we believe the process will be much quicker and violent. If the nation-wide shutdown continues for more than 60+ days and/or the spread of the virus is not under some type of containment within the next 60 to 90+ days, the damage to the jobs market could be extensive. That translates into the Real Estate market as very bearish.

Even though the Fed has dropped interest rates, consumers may not be willing to engage in purchasing homes while this Covid-19 virus event continues. Home prices are extremely high compared to historical values. The Case-Shiller home index (below) suggests a move down to the 140~150 level would not be unreasonable – even with interest rates near ZERO again.

If we are correct and an immediate and rather deep price decline takes place in the US housing market, it will set up a “race to real value” in terms of the market attempting to find what we call the “equilibrium” within the supply/demand curve.

A decrease in the Case-Shiller National Home Price Index to levels near 150~160 would represent a nation-wide price collapse of about 25~35% in the housing market. Certain segments of the housing market may fall by even more extreme levels whereas other segments may fall by smaller amounts.

We believe the economic reaction related to the Covid-19 virus event will result in a “shock wave” type of collapse as the March 2020 (Q1) data is released in April and May 2020. We believe the revised expectations and continued battle to contain the virus will continue to place extreme pricing pressure on certain asset values. Commercial and Residential real estate is some of the largest price assets anyone could purchase and they’ve experienced a solid 8+ year price advance. It does not seem illogical that a 20% to 30% decline could take place as a result of this Covid-19 virus event.

When you consider the real process of combating this virus event and the destruction that will take place across the US and the global economy over the next 6 to 12+ months, it is very likely that both commercial and residential real estate will fall from current lofty levels to price levels that are closer to the equilibrium of the supply/demand curve.

We also believe that foreclosures will continue to stack up – even if the banks are told not to process foreclosures for a 12 month period of time. This does not stop the flow of consumers unable to continue their mortgage obligations – it just stops the banks from engaging in near foreclosure activity for a period of time. The hope is that the markets may settle a bit before banks open the flood gates and start processing these faulty mortgages again.

In the next, last, portion of this research article, we’ll try to share some predictive analysis that may help you understand where the US stock market may find support and where the US real estate market may find a bottom.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for short-term swing traders.

Visit my ETF Wealth Building Newsletter and if you like what I offer, and ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own during the next financial crisis.

Sector expert Michael Ballanger describes what he believes is really behind the market crash.

“Never let a good crisis go to waste.” Sir Winston Churchill

My late older brother Donnie was a quasi-anarchist tax collector for the Canadian government who self-educated himself and then morphed from a grumbling, cynical security guard/starving artist to a very successful 20-year career auditor with the Canada Revenue Agency (CRA) before his untimely passing in 2014. Within weeks of the 9/11 terrorist acts that brought down the Twin Towers in New York City in 2001, he summoned me for a beer conference at the local suds parlor in the West End of Toronto. Holding court for around an hour and a half and three pitchers of local stout, he set about to convince me that all those aircraft slamming into major American landmarks of symbolic importance could only have been a “false flag” operation that was the design and execution of the American government.

His cynicism could be aggravating at times, but it was never, ever without argumentative substance. It was only until after the second Gulf War and subsequent confiscation of Iraqi oil fields, and the almost twenty-year “War Against Terror,” that evidence has come to light that in retrospect makes Donnie look somewhat clairvoyant.

Saudi terrorists carrying out multiple terrorist missions invoking massive retaliation against Iraq and Afghanistan might appear somewhat “misdirected,” but that is a discussion for the beer tent and not today’s microphobic maelstrom. The point is that all one sees may not be what it appears to be, and with markets melting down in a conflagration of fund redemption and debt liquidation, it is important to ask whether or not the arrival of a viral pandemic was the actual source of the financial implosion.

Could it not have been something else?

If one turns the pages in the Book of Bond Insolvency back to last September, every single release from the U.S. Department of Commerce was upbeat; everything coming from the Fed was positive; and stocks around the world were shrugging off the Trump Trade War, the woes of Deutsch Bank, the ever-ballooning U.S. deficit, and the extreme overvaluation (by all measures) of the global markets. In what I penned as “the greatest fiscal policy about-face in history,” I asked in October 2019 “what exactly it was that Jerome Powell saw that spooked him into a sudden series of multibillion- (then trillion) dollar liquidity injections?”

We now know that these “liquidity problems” originated, once again, in the C-Suites of the Wall Street banks, because we know now from statements from JPMorgan CEO Jamie Dimon that banks were having a few “issues” lending to one another. A booming economy with stocks at record levels and a president firing off numerous self-congratulatory tweets with deal flow booming and the banks are having “issues” lending to one another?

As followers of this missive know all too well, I am a full-on cynic of the highest order and not without justification. My lifelong hero of history, Sir Winston Churchill, underscored peak cynicism by offering the quote “Never let a good crisis go to waste,” in reference to taking of advantage of voter anxiety in order to advance a silent agenda or “false flag.” The actions of the Fed last fall were baffling to me, and as REPO ops began to balloon in the final days of January, it was the bond market’s crashing yields that I addressed in my February e-mail alert, not some Asian flu, that accelerated my shorting campaign that was looking really quite foolish until late February.

So, when I look at the slag heap of failed dreams and faulty assumption lying in ruin and despair on the floor of the New York Stock Exchange, I am today asking whether it was really the COVID-19 outbreak that caused the meltdown or is it the cover story that now allows the banco-political alliance to plead in the bended-knee style of Hank Paulson back in 2008 for a legislated bailout of the global banking system, not to combat the global pandemic of viral infection but the more insidious global pandemic of debt, as in “way too much of it.”

Now, with people dying and people close to my place of residence infected, I am not suggesting that this tragic outbreak is to be understated or dismissed. What I am raising is the manner in which the media and the governments around the globe have handled this crisis. Secretary Mnuchin’s first statement pledging action by the Trump Administration was “to support the U.S. economy,” with nary a mention of the health of its citizens. It would seem to me that you help the ill first, the unemployed second and the profit and loss statements of your Wall Street pals last.

Further, just as the banker-politico alliance opted to bail out the banks rather than the citizens losing their homes in 2008, it seems that history is once again rhyming, but not pleasantly nor with the numbing calm of a Robert Frost soliloquy.

After a week of total and complete market mayhem and monetary madness from the banco-politico alliance, I feel the same today as I did in 1987, 2001, 2009 and December 2018. Most importantly, I feel the same way I did in April 2011, when the central banking interventionists took down the gold and silver market in what is still, to date, the singular most blatant example of “free market” abuse ever.

That feeling is one of violation, but the odd part about it this time is that we, in the precious metals fraternity/sorority, have had to live through financial armageddons before, such that our emotional coping mechanisms are more conditioned to external violation than the current generation of stock junkies that have been day-trading the “Spoos” with “the Fed at their back” for over twelve years. Only now are they discovering the horror of financial loss at the hands of an external perpetrator. Only, for them, it is a microbe, while for us it was, and is, an entity. Nemesis arrives in different disguises.

Navigating the current investment landscape is not unlike “shooting the rapids” in a kayak, and the important tip in doing so is to keep the paddle perfectly balanced in order to keep the upper body out of the water. In terms of trading, I take position sizes down and try to avoid leverage where possible, but I go into a trade or a theme knowing full well that these are not normal times.

The performance of the gold miner exchange-traded funds (ETFs) run by Van Eck has been a disgrace, with massive swings in discount-to-net-asset-value (NAV) settlement prices and shoddy rebalancing. I must assume that I could lose everything if my judgment is off by as much as a blink, so while prudence is of the utmost importance, paralysis is not.

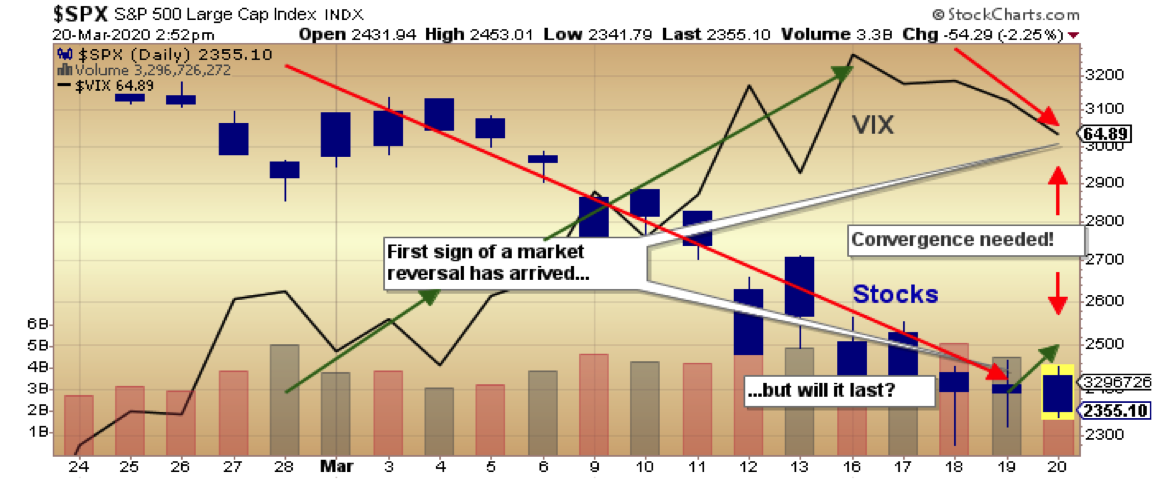

At the top of most advances there usually occurs a divergence, whereby stocks advance and volatility advancesa most unusual condition. At bottoms, there occurs an opposite divergence, and we are getting just that. Much as I detest the term “green shoots,” the first of them are beginning to poke their heads above the receding snow cap with the action in the SPX/VIX relationship. The chart below shows a definite divergence between stocks and volatility, and that has always been the first signal that a turn is possible.

Similarly, silver outperformed gold on Friday (gold up 0.26% versus silver up 2.07%), in what may yet another positive divergence in our favor.

Over the weekend, we will all be reading dozens of apocalyptic prophesies by various market gurus, complete with pointed fingers, raised hands, bulging eyes and crocodile tears everywhere. While I like to pore through their rationales for whatever investment thesis they currently hold, in the end, the question I ask is, “Did they see the crash coming?” I did, and I gave the reasons why in the Jan. 12 missive. But that, my friends, is “old news.” I am now flat; covered way too early; own no shorts or puts; and am looking for a trade-able rally in the senior and junior gold miners (GDX/GDXJ) to new highs by the end of the summer.

Further, unlike the past two months, those miners are now undervalued relative to the metals they produce. The big gains will in the shares.

Lastly, the weekly gold-silver comparison chart shown below starts in December 2015, at the onset of the current (yes, I said current) bull market in gold. In the singular largest deflationary crash in financial market history, gold is down 2.53% year to date, versus declines of 28.66% and 23.33% in the S&P and NASDAQ, respectively. Gold has done its job of protecting one’s assets from those lifestyle-ending drawdowns from which it is so difficult to recover. The important points to observe in this chart are as follows:

Gold remains in an uptrend;

The gold-to-silver performance differential is an astonishing 51.58%;

Being a weekly, note the negative crossover in the gold MACD lines circled in red;

Note the weekly relative strength index (RSI) at 45.67; oversold (bottoming area) is under 30;

The uptrend line for gold remains around US$1,425. Gold must hold that long-term support line;

The silver market remains an enigma to all metals analysts that I know. It is either supernaturally cheap right now or something fundamental to its long-term pricing mechanism has changed. Whether or not to buy it here remains the biggest singular investment decision of my 43-year career, and I must tell you in all candor, this is a really tough one. My heart is saying “Buy it!” but something ain’t quite right.

To sum up this past meteor storm of a week, I remain a staunch bull and grateful to have been overweight gold rather than the miners (or anything else) during the crash. I am now moving aggressively to replace all of the positions sold at or near the peak in February and last August. There are numerous names that have moved down to multiyear lows due to this forced liquidation from the EFTs and other funds, and surprisingly, there are juniors (that I own) that are actually up year to date

If there is one dominant investment theme to which I am adhering, right now, it is to focus on those microcap juniors with defined ounces. If I am right, we have now entered a new paradigm where preservation of value will be paramount. Since counterparty risk fears were what triggered the REPO explosion last fall, those same fears place gold (and ounces in the ground) front-and-center in this value proposition. Accordingly, a basket of companies producing or developing gold resources are going to be reconsidered, reranked and revalued.

It was a difficult week for all, and it is my sincere wish that everyone stays safe and rides out the current storm in the company of healthy family and friends.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

By CentralBankNews.info Pakistan’s central bank lowered its policy rate for the second time in a week as the number people infected by the coronavirus has risen considerably, prompting social distancing and reduced activity, which it said was expected to lead to a “noticeable” slowdown in domestic demand. The State Bank of Pakistan (SBP) cut its key rate by a further 150 basis points to 11.0 percent, bringing the total easing since the cut on March 17 to 225 points. “The MPC was of the view that this cumulative easing would cushion the growth slowdown while protecting inflation expectations,” SBP said, referring to the decision by its monetary policy committee at an emergency meeting. This month’s rate cuts come after the central bank paused in its tightening campaign in July 2019 following 9 rate hikes to curb inflation from a fall in its rupee. Since July last year SBP had kept its rate steady until the spread of the virus began to affect demand and it cut the rate by 75 basis points on March 17. At that point, SBP said it was ready to take further action when more information became available. Overt the last week, the spread of the virus, Covid-19, has caused major disruptions to the global economy and trade, with the International Monetary Fund slashing its 2020 growth forecast to below zero from 3.3 percent. This implies the outlook for growth and inflation is likely to be revised down further, SBP said, adding it “remains ready to take whatever further actions become necessary in response to the evolving economic impact of the Coronavirus.” SBP said it would soon announce further regulatory measures with banks to address the pressure on borrowers’ cash flows from disruptions by making deferment and loan restructuring easier.

The State Bank of Pakistan issued the following statement:

“1. At its last meeting on 17th March 2020, the Monetary Policy Committee (MPC) noted considerable uncertainty about how the Coronavirus outbreak would impact the global economy and Pakistan. In the statement issued following that meeting, the MPC “emphasized that it stood ready to take further actions if and when needed as more information becomes available on the outlook for inflation and growth.”

2. Substantial new information on global and domestic developments has become available since the last MPC meeting. Globally, the Coronavirus has severely increased in reach. This has caused major disruptions to economic activity and the IMF has also significantly downgraded its global growth outlook for 2020 from 3.3 percent growth previously to below zero. These global developments have also led to a sharp fall in international trade. On the domestic front, since the last MPC, the number of COVID-19 cases has increased considerably, prompting social distancing and curtailment of activity. This is expected to lead to noticeable slowdown in domestic demand.

3. The developments discussed above imply that the outlook for growth and inflation in Pakistan is likely to be revised down further. In the wake of this new information, the MPC agreed at its emergency meeting today, to take further action. Accordingly, the MPC has decided to cut the policy rate by a further 150 basis points to 11 percent. This brings the cumulative easing over the past one week to 225 basis points. The MPC was of the view that this cumulative easing would cushion the growth slowdown while protecting inflation expectations.

4. The MPC also noted that SBP is in the process of taking necessary regulatory measures in coordination with banks to address pressures on cash flows of borrowers affected by Coronavirus related disruptions through facilitating deferment and restructuring of their loans. The announcement of these measures is expected soon and will complement the action being taken by the MPC on interest rates today.

5. The MPC remains ready to take whatever further actions become necessary in response to the evolving economic impact of the Coronavirus.”

By CentralBankNews.info The Central Bank of Seychelles (CBS) cut its monetary policy rate (MPR) by 100 basis points to 4.00 percent, saying this is the first phase of its response to the challenge from the spread of the coronavirus, which is expected to slash this year’s earnings from tourism by 70 percent and trigger a double-digit drop in economic growth. It is the second rate cut by CBS since it introduced the policy rate in January 2019 and set it at 5.50 percent. In September last year CBS cut the rate by 50 basis points. In addition to the cut in MPR, the bank’s standing deposit facility (SDF) will be cut to 10.0 percent and the standing credit facility (SCF) to 7.0 percent. The minimum reserve requirement (MRR) will remain unchanged at 13 percent. “The CBS remains vigilant and stands ready to adjust its policies as needed to promote price stability, the bank said in a statement following a board meeting on March 23. The Republic of Seychelles, which comprises 115 islands in the Indian Ocean, relies heavily on tourism, which is being devastated by the closure of borders in most countries. As of the second quarter, CBS said limited inflows are expected from its services sector, with early estimates showing a fall in tourism earnings in 2020 of 70 percent in euro terms from 2019. “This is likely to place severe pressure on the exchange rate and requires a significant decline in national consumption if the economy is to sustain a stable exchange rate,” CBS said, adding it is unclear whether the fisheries industry or other export-oriented sectors can compensate for the loss of earnings in tourism. “The main aim of the reduction in MPR is to support a decline in interest rates as a means of alleviating future stress on borrowers,” CBS said, adding the loss of tourism earnings will lead to “high levels of uncertainty in all sectors of the economy.” Against the euro, the Seychellois rupee has been appreciating since March 2018 and today it jumped almost 10 percent to 14.9, up 12.5 percent since the start of 2020. Against the U.S. dollar, the rupee also rose sharply in response to the rate cut to 12.6 to the U.S. dollar and is now up 8.6 percent since the start of this year. A coordinated and urgent policy response is needed to moderate the impact of the virus but even with an alignment of monetary, financial and fiscal policies, CBS said large drops in consumption and shifts in “social behavior” are critical in maintaining economic stability given the uncertainty. In the third quarter of 2019 the economy of the Seychelles decelerated to to annual growth of 3.8 percent from 7.1 percent in the second quarter and in February CBS forecast growth could decelerate to 3.5 percent in 2020 from an estimated 3.9 percent in 2019. Given the current challenges, CBS said growth is forecast to contract by double-digits this year. Inflation in the Seychelles has been falling since May last year and fell to 0.76 percent in February and CBS said inflationary pressures are likely to be be moderate due to the general fall in global demand and the large shock in oil prices.

By TheTechnicalTraders – As you may or may not know, the markets have a way of making it extremely difficult to trade in general almost all of the time if you do not have a trading plan.

One of the ways the market likes to pull money from traders is through morning opening gaps. For example, yesterday, the inflow of emails about gold, silver, and gold miners was insane. I keep trying to keep everyone in check with how to handle high-risk, high uncertainty, and volatile times, which, for our case right now, is a cash position for a few more days.

Unfortunately, big moves in price trigger emotions with some of you. It causes you to start trading just because you think you need to trade, which can be for many different reasons I won’t get into here. You should know my stance by now, which is cash is a position, and retaining our capital is more important than trading some times.

I know for a fact that all successful traders have a detailed trading plan, they can control their emotions, are logical, and they wait for opportunities vs. jumping at anything that moves more than normal.

Below is our portfolio equity curve, which we hit an all-time new high just days after the stock market started its crash. Maybe if you see what your portfolio growth curve would look like if you followed my trades, you will finally see the value in CASH.

I don’t trade a lot, and we are in cash when we don’t have any positions. Other times we will have 2 or 4 positions open, but it all depends on the market and volatility. You want trading to be simple, boring, and profitable, trust me on this.

PORTFOLIO GROWTH CHART

AVERAGE PORTFOLIO RESULTS THIS YEAR

Ok, enough of that rant, BACK TO MORING PRICE GAPS! The stock market loves to do most of the day’s price range and profit potential in a way the average trader is not able to catch the move. Even more so, it is trying to get traders the worst entry or exit price.

New members over time will see and understand this when I talk about these gaps getting faded in my morning videos, which I will explain in a minute. For now, let’s take a look at the price of gold and the market sentiment from yesterday.

Yesterday gold traders were acting like a school of piranha’s. A big one day pop in price is like a drop of blood in the water, and it created a feeding frenzy. There was so much momentum going into the closing bell that the market makers will take advantage of this and walk the price up in pre-market trading the next day and try to reach the next resistance level before the opening bell.

This is what happened to gold, and miners this morning. Market makers know there are still a ton of gold and miner stock buyers out there who are going to BUY as soon as the market opens, so what happens?

The general public pays the high price, way up at resistance, and the market makers get to sell any access shares they have for a huge profit. After that, the price generally fades (falls) back down, and the majority of buyers that day just bought at the high because of pure emotions and a lack of understanding. This happens for gaps to the downside as well in a similar manner.

Now, keep in mind, this is a very short term price action. The gap may fade down over the rest of the session or a few days, but it does not mean the uptrend is the price is finished longer term.

My point is, the market has a way to get you a bad fill MOST of the time if you do not understand how and why the price moves the way it does. Even if you know all this, sometimes we have no choice to pay the price depending on the trade setup if we want to get into a position. I just wanted to share this small tidbit on how the market moves with price gaps because almost all price gaps fill, fade back down to the previous days high for the stock indexes. Commodities gaps don’t always fill, because they are a very different asset class than equities.

My current outlook and thinking for gold, silver, and miners?

In short, gold is the only one in a bull market, and it’s been the definite leader time and time again for the past year almost. It remains in a bull market, and all the money printing/QE, and zero interest rate things are very bullish on metals long term. I like gold a lot, have for a while. I think it’s going higher still as I pointed out in yesterday’s afternoon video, $2600 is my primary target long term. If you didn’t watch yesterdays afternoon video be sure to do so here:

As for gold miners and silver, well today is the same story as yesterday, everyone wants to own them and thinks they are missing the train. How you should see these charts and how to best trade them I tell you in yesterday’s afternoon video.

Trading now, in my opinion, is pure speculation and emotionally driven. Sure, you could be right, and this could be the bottom, but as technical traders using rules, logic, and a proven strategy, we are not cowboys trying to pick a bottom to be early. A broken clock is right two times a day. You may get lucky, but because bottom picking without any technical confirmation is a sucker’s (gamblers) game in the long run.

As our portfolio graph above speaks for its self, in that we do not need to catch every move, in fact, we just need to catch a couple of low-risk trades and slowly build our capital. I was told by one of my mentor traders years ago, once trading becomes slow and boring to you, that’s when you finally understand the market and have a proven trading strategy.

I hope you find this helpful, and if you want this type of info every day, plus my videos, and winning trading strategy, become a member right now!