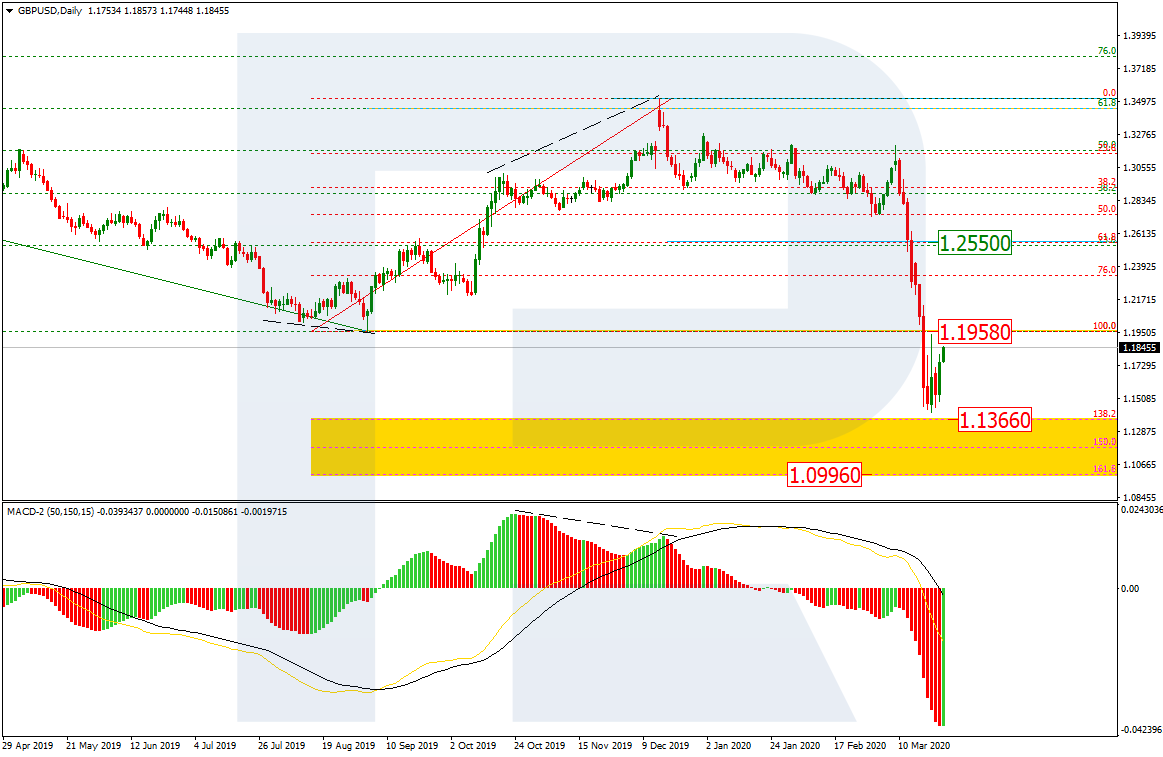

As we can see in the daily chart, GBPUSD is trying to fix below the low at 1.1958. At the same time, the current slight growth may be considered as a test of the broken low from below and a rising correction. After finishing the pullback, the pair may continue falling towards the post-correctional extension area between 138.2% and 161.8% fibo at 1.1366 and 1.0996 respectively. the resistance is 61.8% fibo at 1.2552.

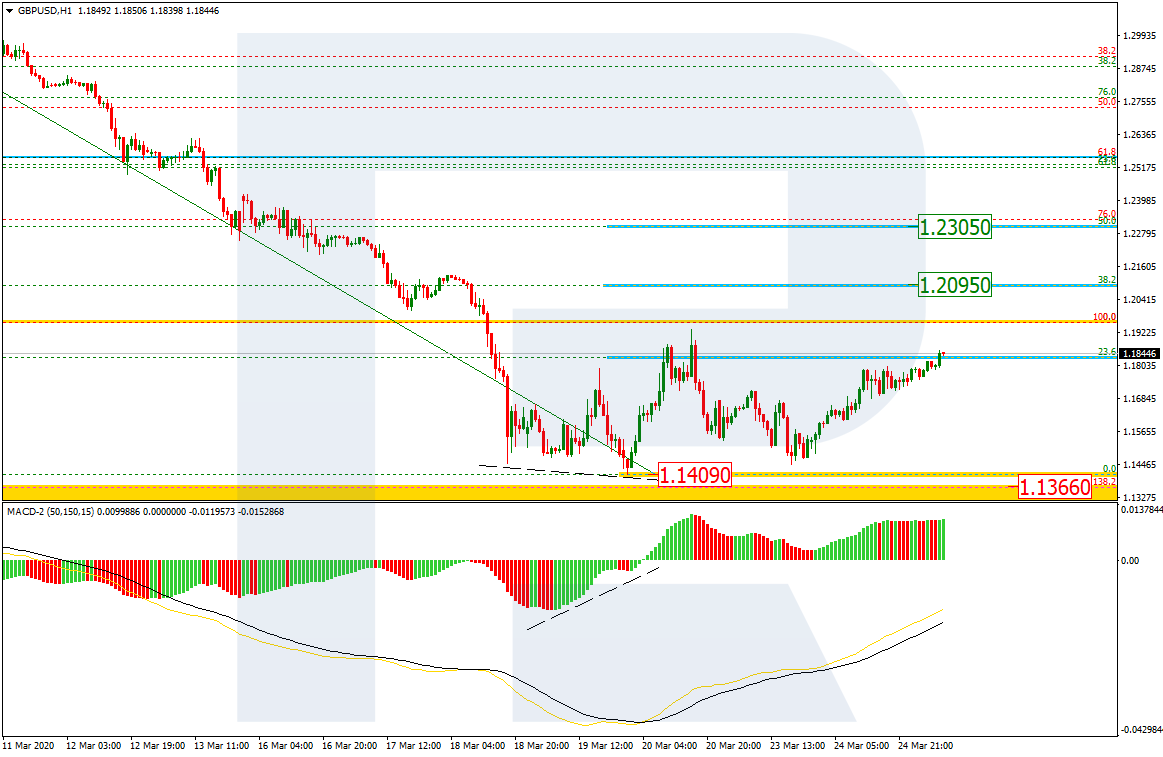

In the H1 chart, the convergence made the pair reverse and correct upwards to reach 23.6% fibo. The next upside targets may be 38.2% and 50.0% fibo at 1.2095 and 1.2305 respectively. the support is the low at 1.1409.

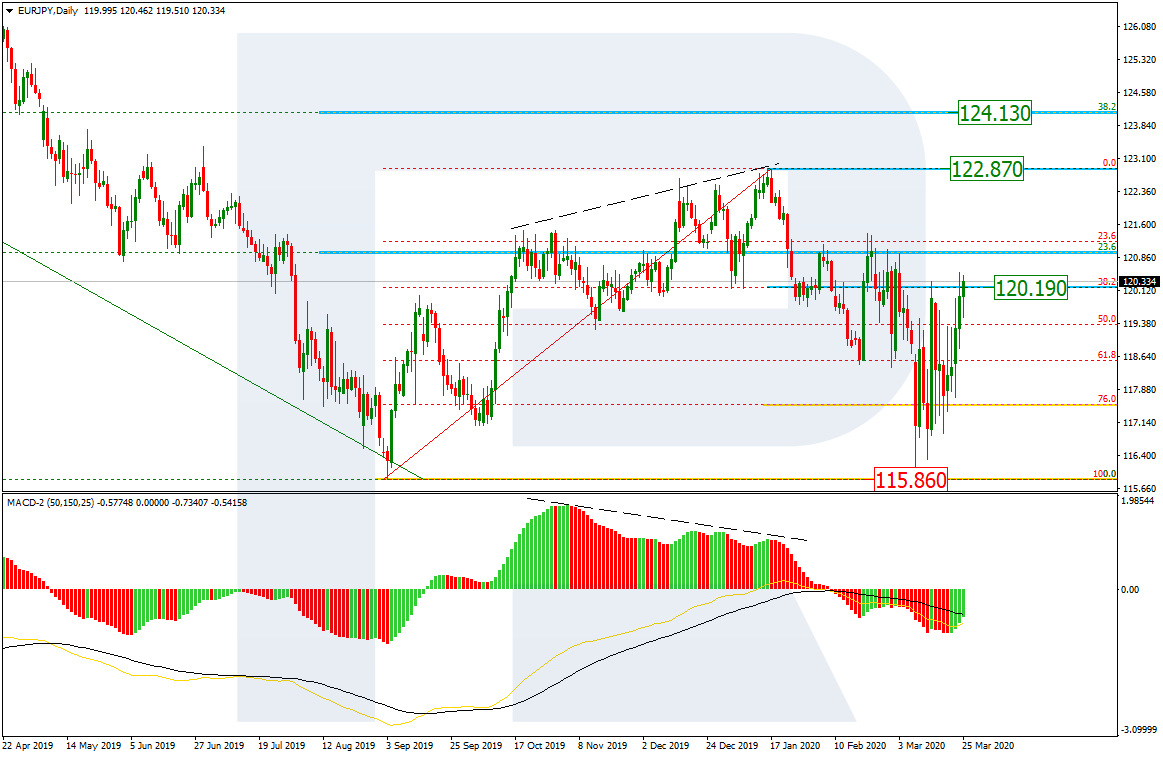

EURJPY, “Euro vs. Japanese Yen”

As we can see in the daily chart, after testing the low at 115.86 and rebounding from it, EURJPY may start a new long-term rising impulse. Right now, the pair is trying to break the resistance at 38.2% fibo (120.19). If the pair succeeds, it may grow to reach the fractal high at 122.87. If this level is broken as well, the instrument may start a new long-term growth with the first target at 38.2% fibo (124.13).

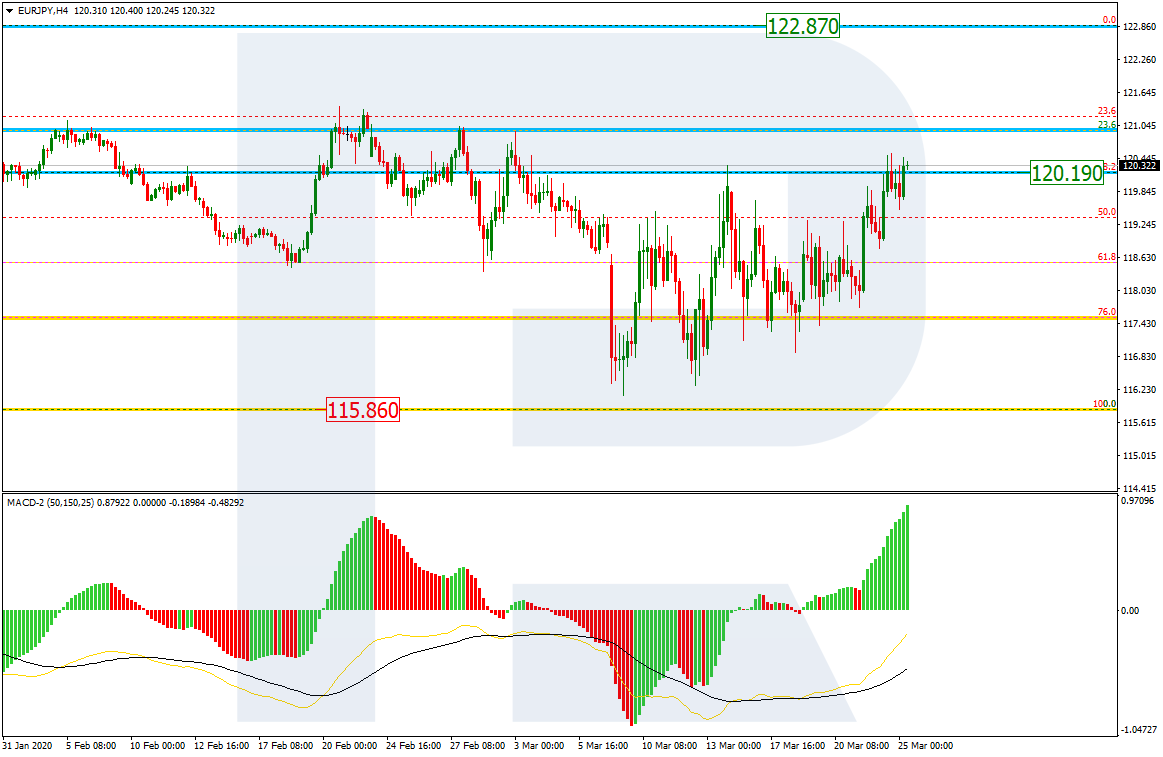

In the H4 chart, the pair is re-approaching 38.2% fibo at 120.19. In the future, the instrument is going to break this level. It’s only a matter of time.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The latest set of PMI data out of the UK and Europe painted a picture of doom and gloom this week. Amid the first set of data to properly account for the corona virus outbreak, the market was expecting weakness. However, there are some positives to take from this week’s releases. Broadly speaking, the data was not as bad as expected.

Eurozone Data Causes Concern

In the Eurozone, the overall manufacturing PMI for the bloc came in at 44.8. Although this was down from the prior month’s 49.2, and still below the neutral 50 level, it was not as bad as the 40.1 reading the market was looking for.

French manufacturing was also a little better than expected. Though again still in contractionary territory, at 42.9 vs 39.4 expected and 49.8 prior. German manufacturing was also a little better than expected, printing 45.7 vs 40.1 expected and 48 prior. German services PMI, however, was a major red flag. Data came in at a worrying 34.5 vs 43 expected and 52.5 prior. This is a drop of nearly 20 points on the index.

Indeed, the overall Eurozone services PMI was shockingly low. Data came in at 28.4 vs 40 expected and 52.6 prior. Marking a near 20 point drop, this reading is a fresh record low for the service sector. It is highly concerning insight into the impact the coronavirus outbreak is having on the Eurozone economy.

UK Manufacturing Back in Contractionary Territory

In the UK, readings were again weak. As with the Eurozone, however, manufacturing was a little better than expected. Data came in at 48 vs 45.1 expected, though down from 51.7 prior and back in contractionary territory. However, the services PMI was also troublingly weak. The reading came in at 35.7 vs 45 expected and 53 prior.

US Data Remains Weak

This theme also played out in US data. The US manufacturing data (which was the strongest among the three) printed 49.2 over the month vs 45.2 expected. This is still down from 50.7 prior and in contractionary territory. Again, the service sector was the worst hit. Services PMI printed just 39.1 vs 44.1 expected and 49.4 prior.

Fears For Service Sector

With many office-based companies in the US, UK and Europe on lockdown now, the service sector has come under increasing pressure and looks likely to remain so in the near term. Traders will now be equally waiting for the next reading. So, whether this trend develops further or whether we start to see some recovery. Much of this will depend on how long the current lockdowns last.

In the US, Trump has said that in 15 days’ time he will review the lockdown and promises that the US will be “open for business” again. In the UK, the PM has advised that the situation will be reviewed in 3 weeks. Finally, in Europe, countries such as Spain have extended the current lockdown into mid-April.

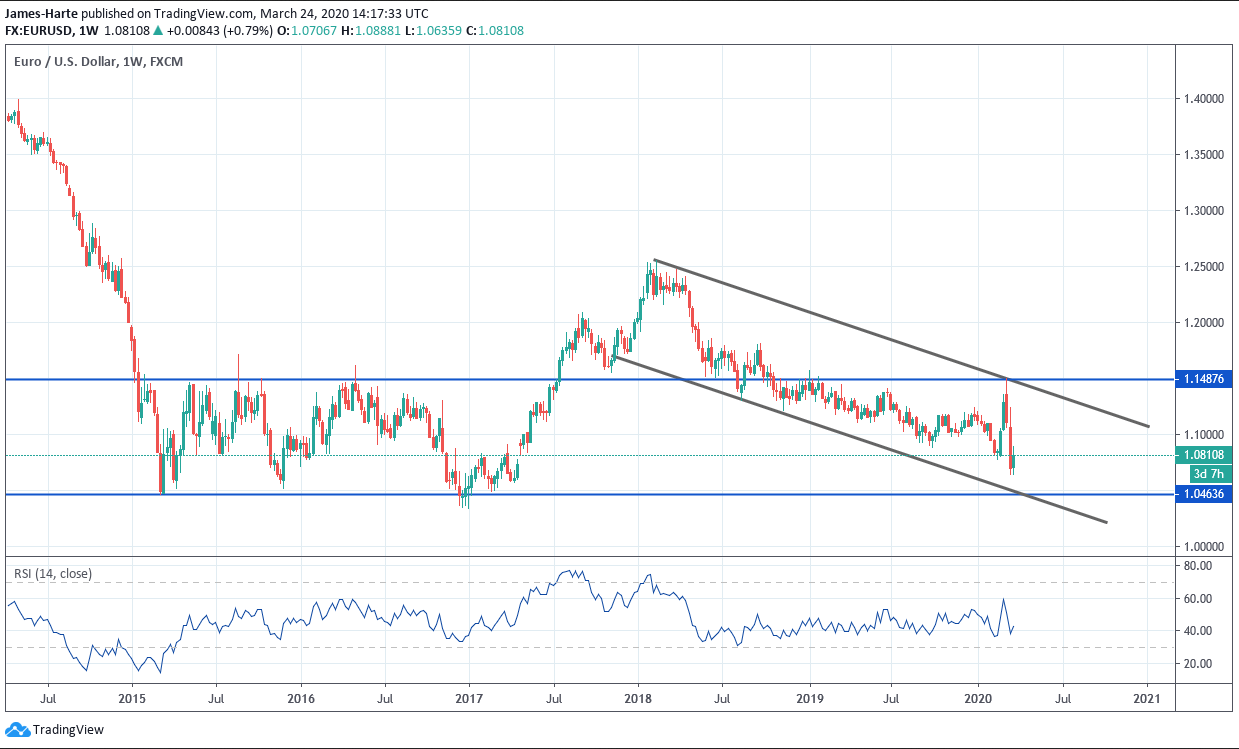

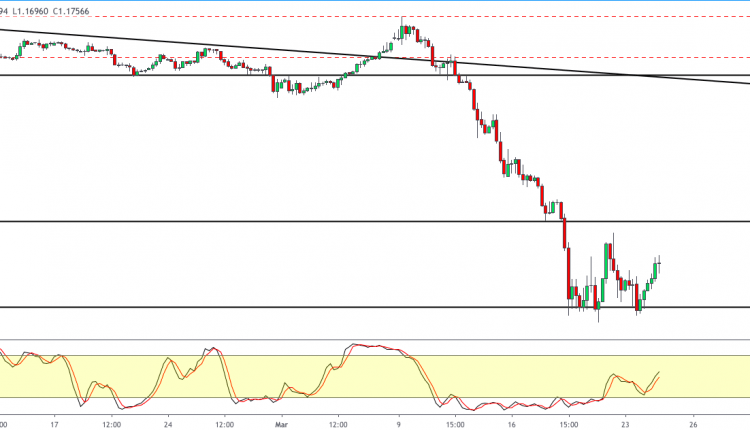

Bullish Divergence Appearing in EURUSD

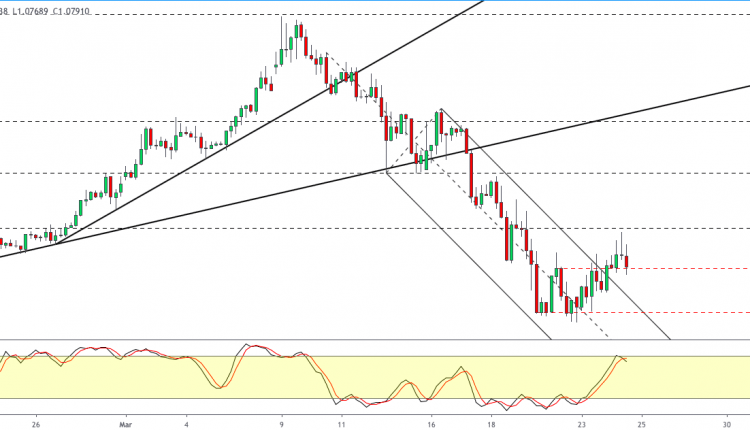

Looking at EURUSD on the weekly timeframe you can see that price has been moving in a well defined bearish channel from the 2018 highs. The recent recovery was capped once again at a test of the 1.1487 level. However, you will notice that the RSI indicator is starting to flag bullish divergence as we approach the key 1.0463 level support. Provided this level isn’t broken, this suggests a potential for a reversal higher in the medium-term.

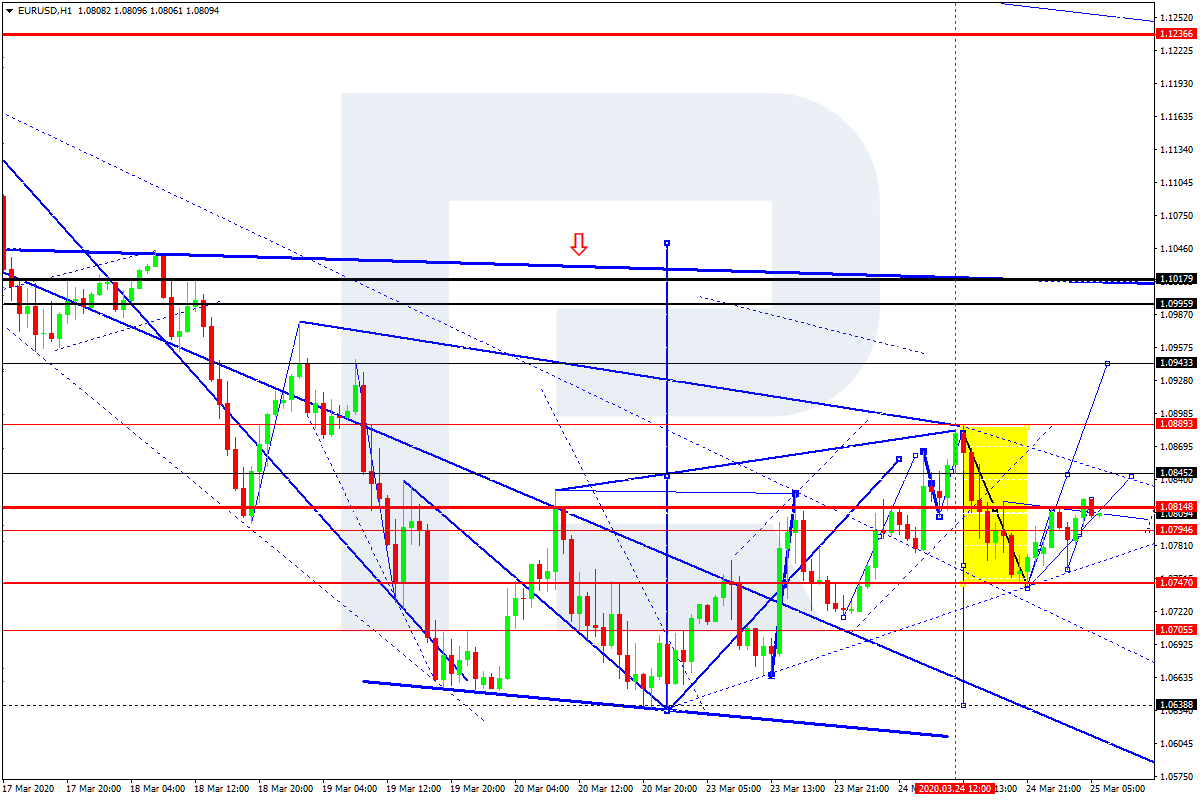

After forming the ascending impulse towards 1.0887 and completing the correction at 1.0744, EURUSD is moving upwards. If later the price breaks 1.0815 to the upside, the market may continue growing towards 1.0943; if 1.0740 to the downside – resume trading downwards with the target at 1.0700.

GBPUSD, “Great Britain Pound vs US Dollar”

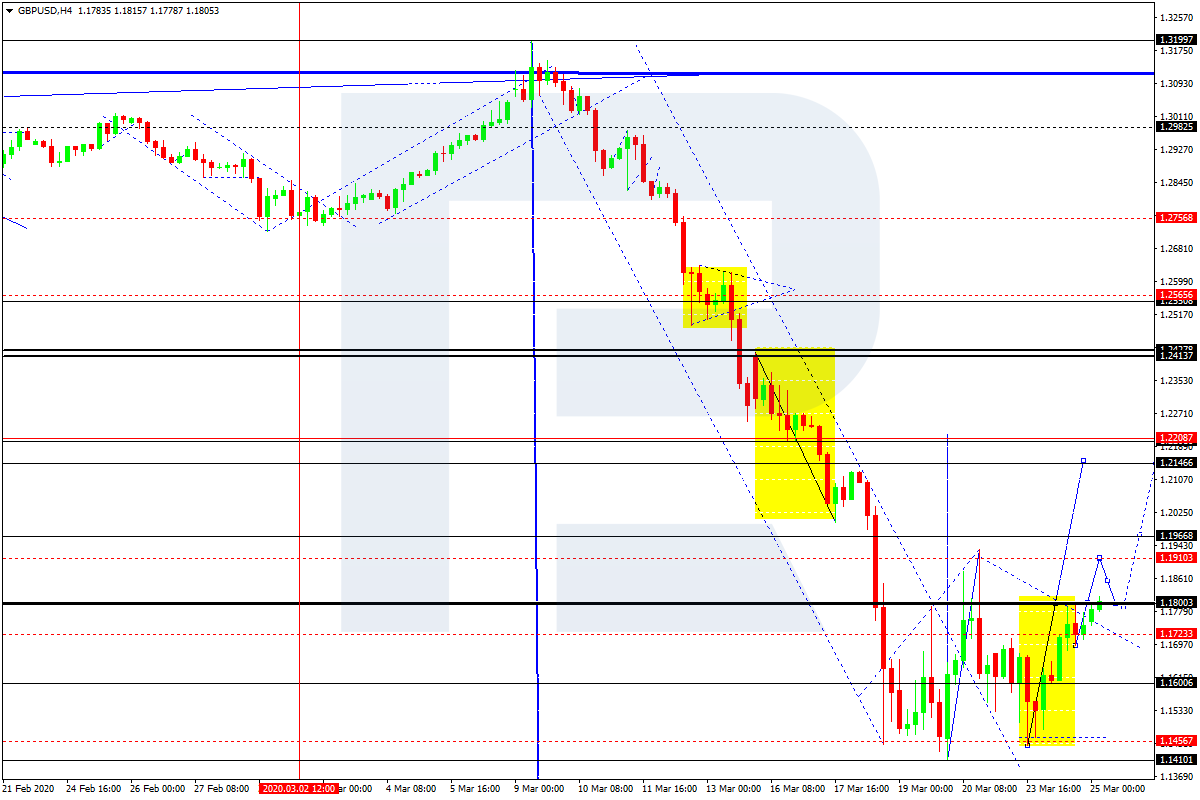

GBPUSD has finished the ascending impulse towards 1.1800; right now, it is consolidating below this level. Possibly, the pair may break this level to the upside and then trade upwards to reach 1.1910. After that, the instrument may break the latter level as well and then continue growing with the target at 1.2145.

USDCHF, “US Dollar vs Swiss Franc”

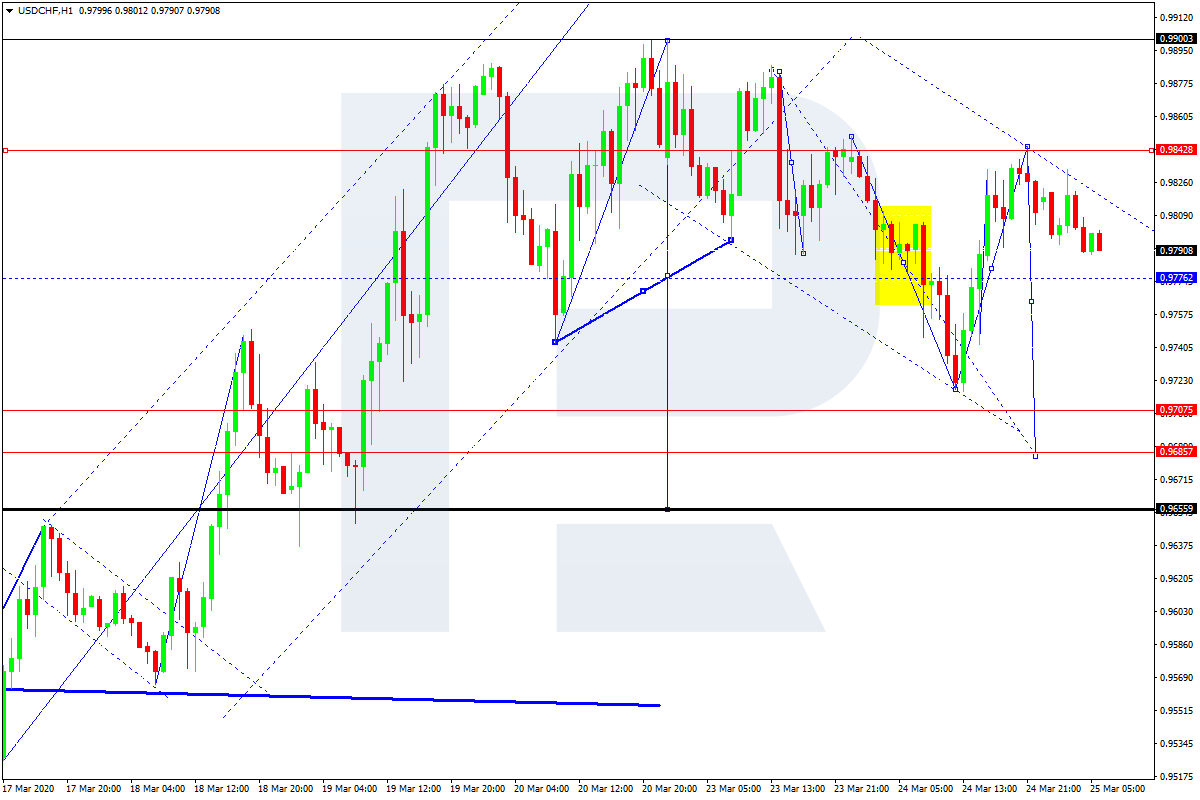

After finishing the correction towards 0.9842, USDCHF is falling to break 0.9760. Later, the market may continue trading downwards with the short-term target at 0.9686.

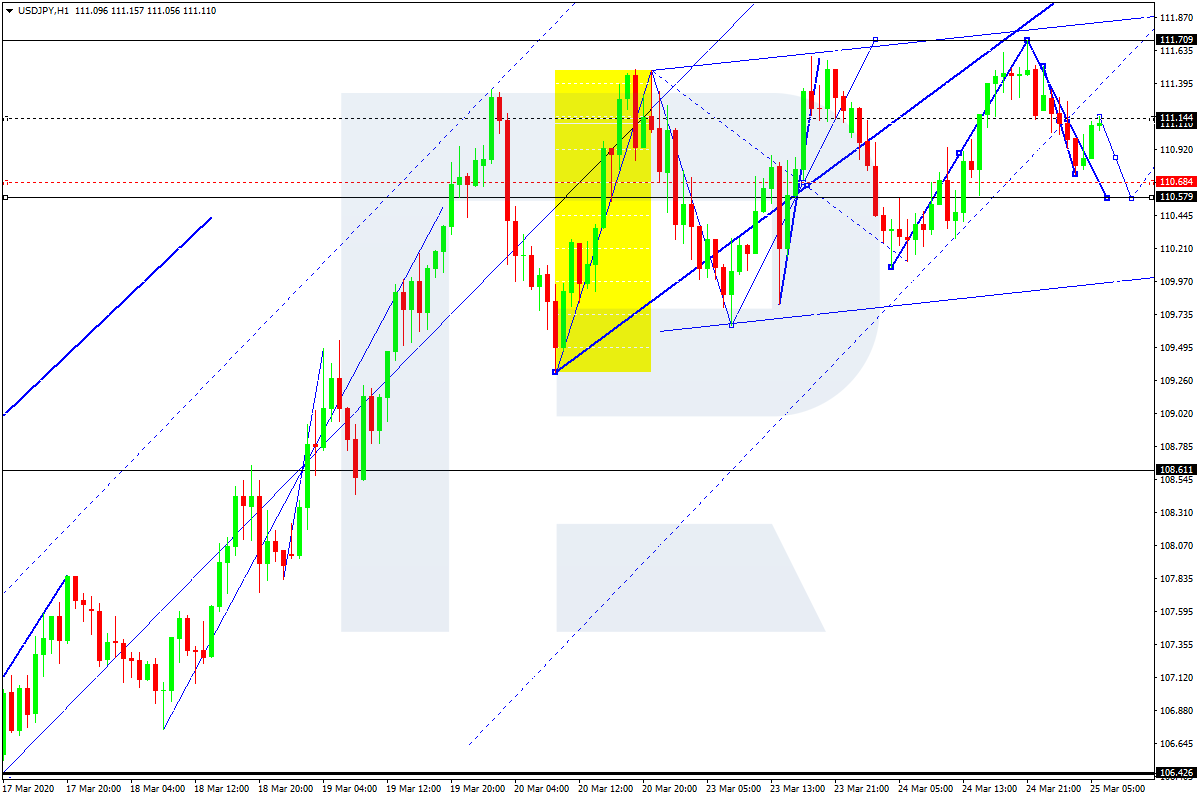

USDJPY, “US Dollar vs Japanese Yen”

USDJPY is still consolidating around 110.70; it has expanded the range up to 111.70 and right now it falling to test 110.70 from above. After that, the instrument may start another growth to reach 111.90 and then form a new descending structure with the target at 110.70.

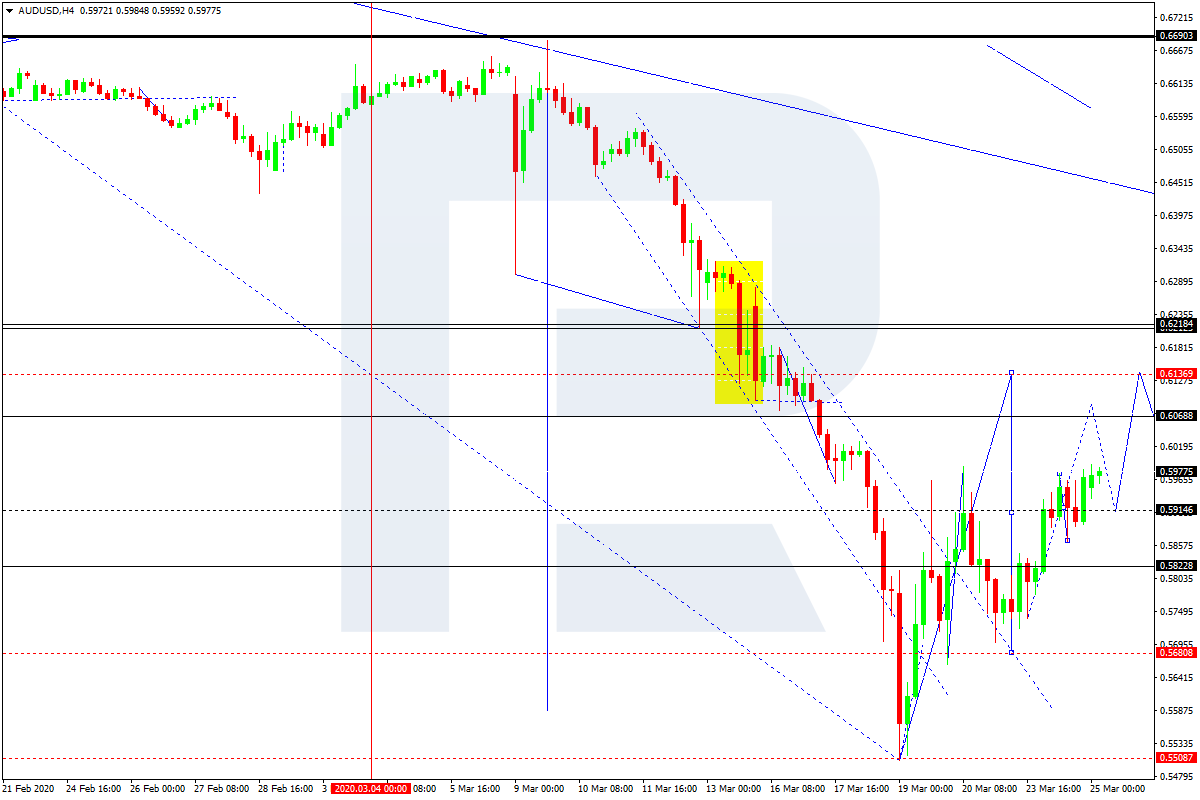

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is still trading upwards to reach 0.6136. After that, the instrument may correct to the downside with the target at 0.5822.

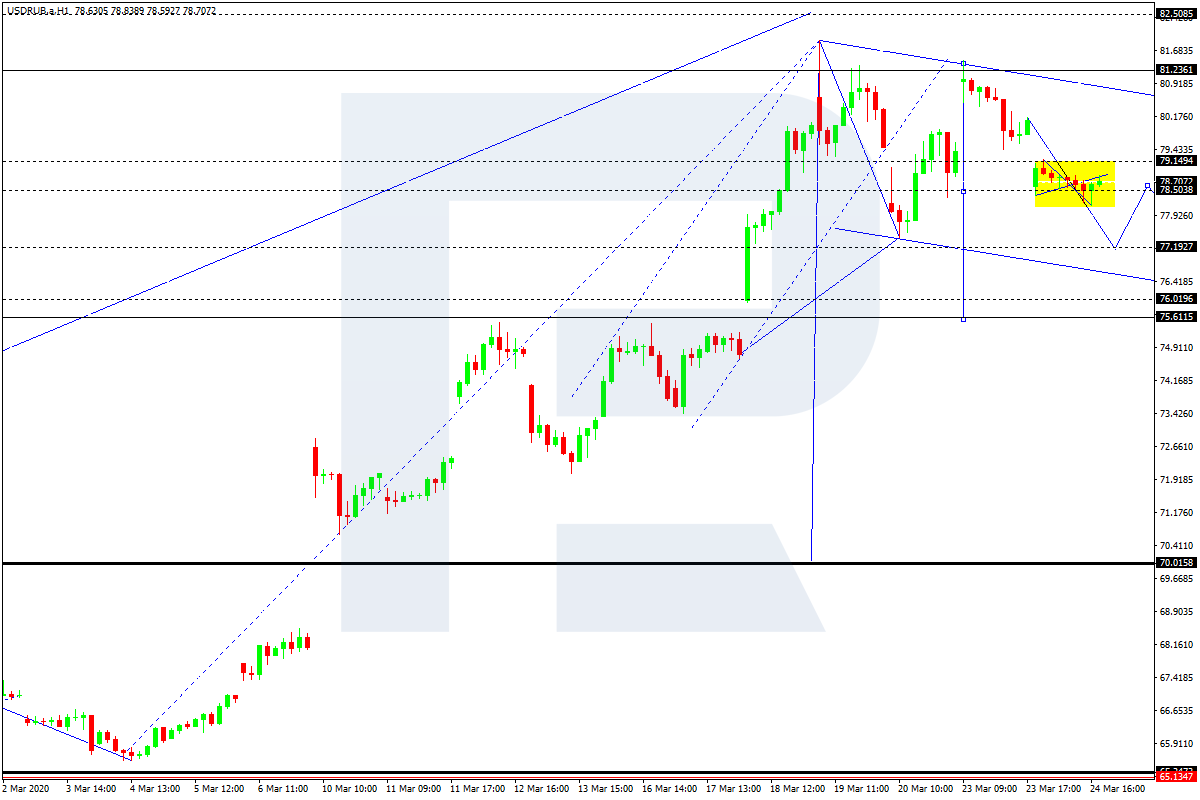

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is falling towards 78.38. Later, the market may break this level and continue trading downwards with the short-term target at 76.02.

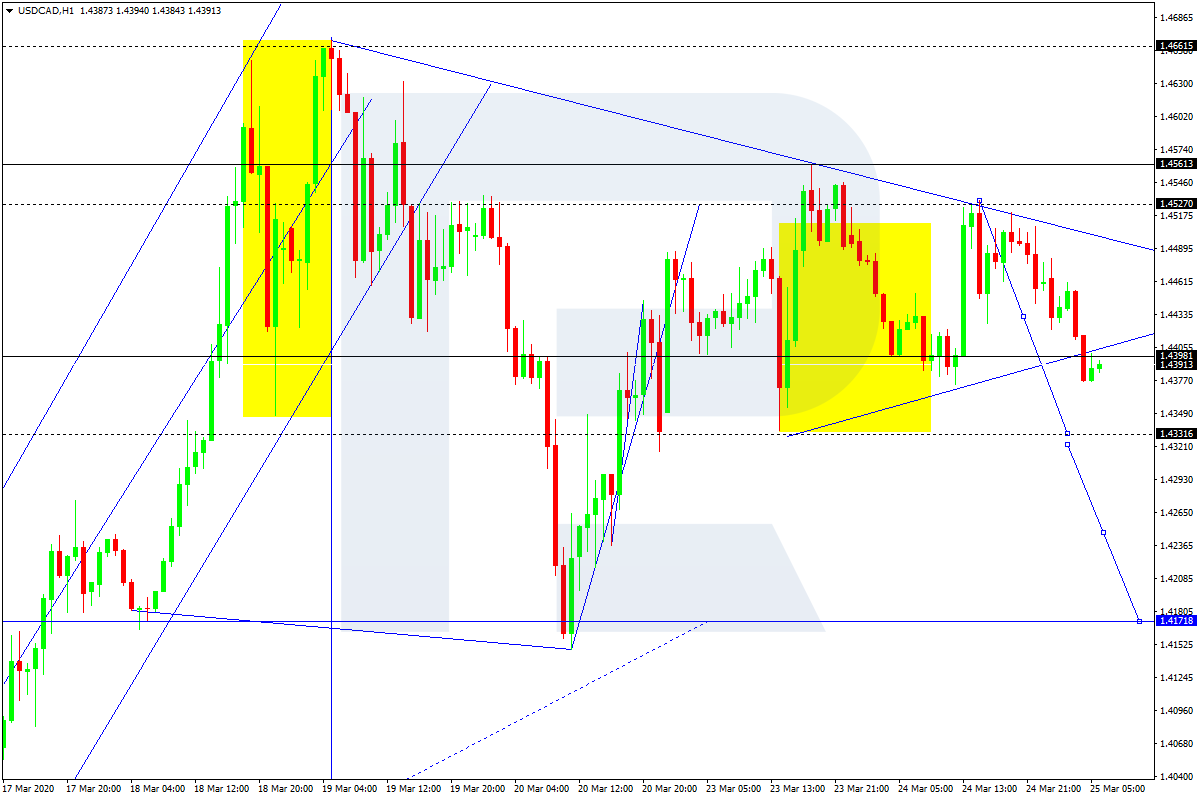

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is falling. Possibly, today the pair may reach 1.4333 and then consolidate below it. After that, the instrument may break 1.4333 to the downside and continue the descending wave with the target at 1.4171.

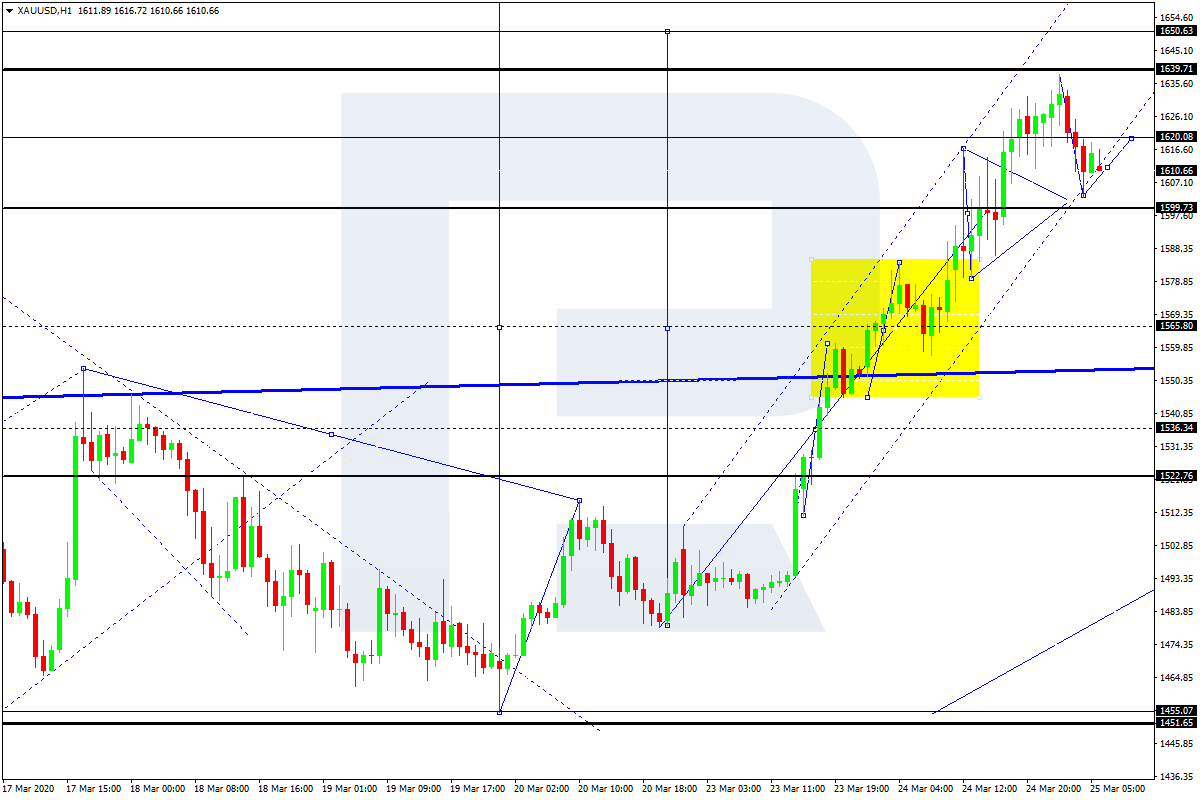

XAUUSD, “Gold vs US Dollar”

After completing the ascending structure at 1577.50 and forming a new consolidation range around it, Gold has broken the range to the upside. Possibly, the pair may continue trading upwards. Today, the price may reach 1650.50 and then start another correction with the target at 1577.50.

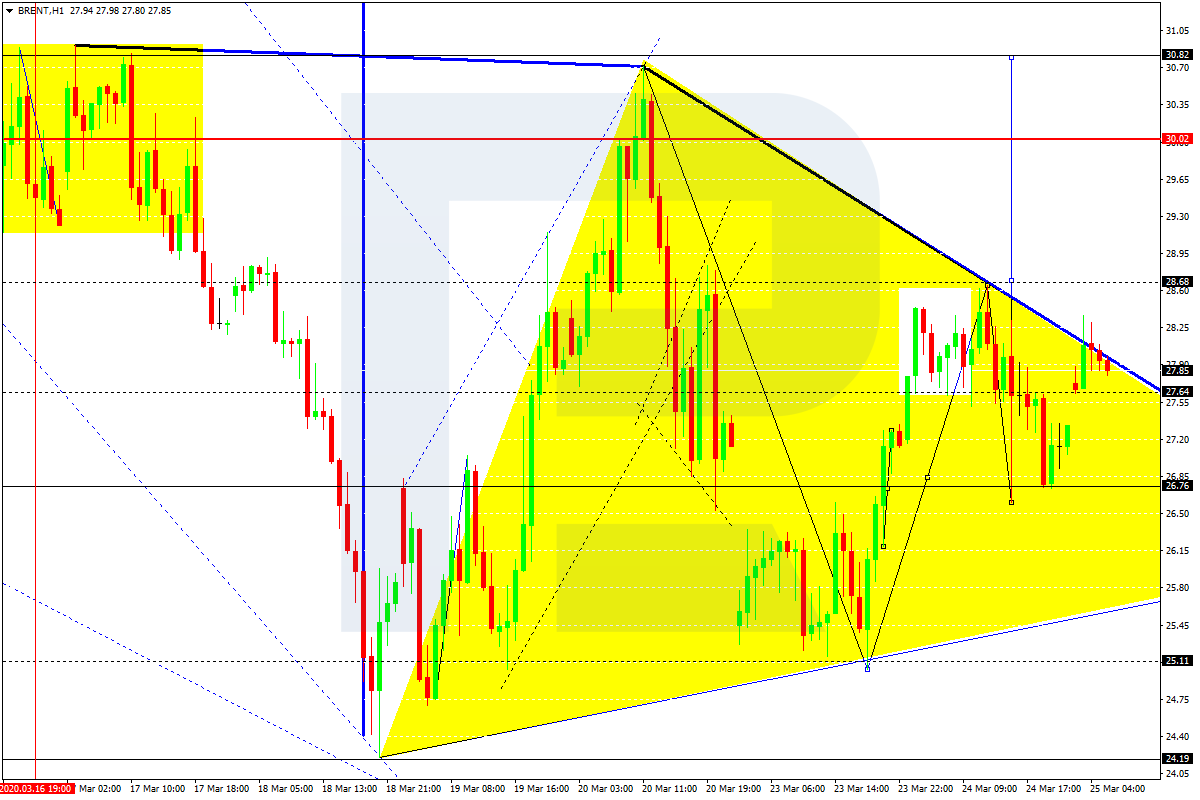

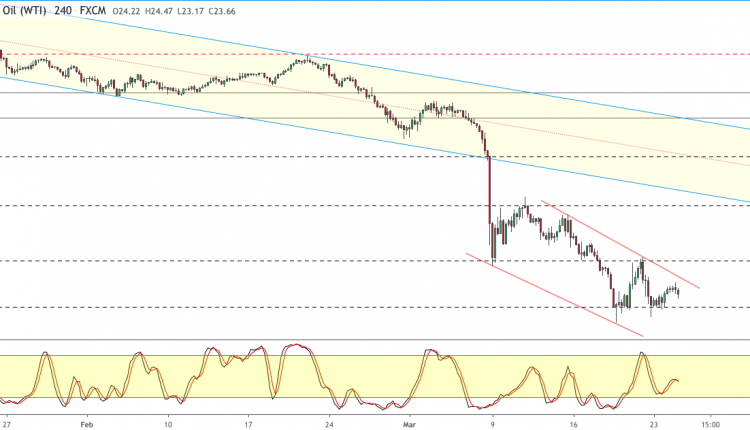

BRENT

Brent is still consolidating around 27.77. Today, the pair may grow to break 28.70 and then continue trading upwards with the target at 30.80.

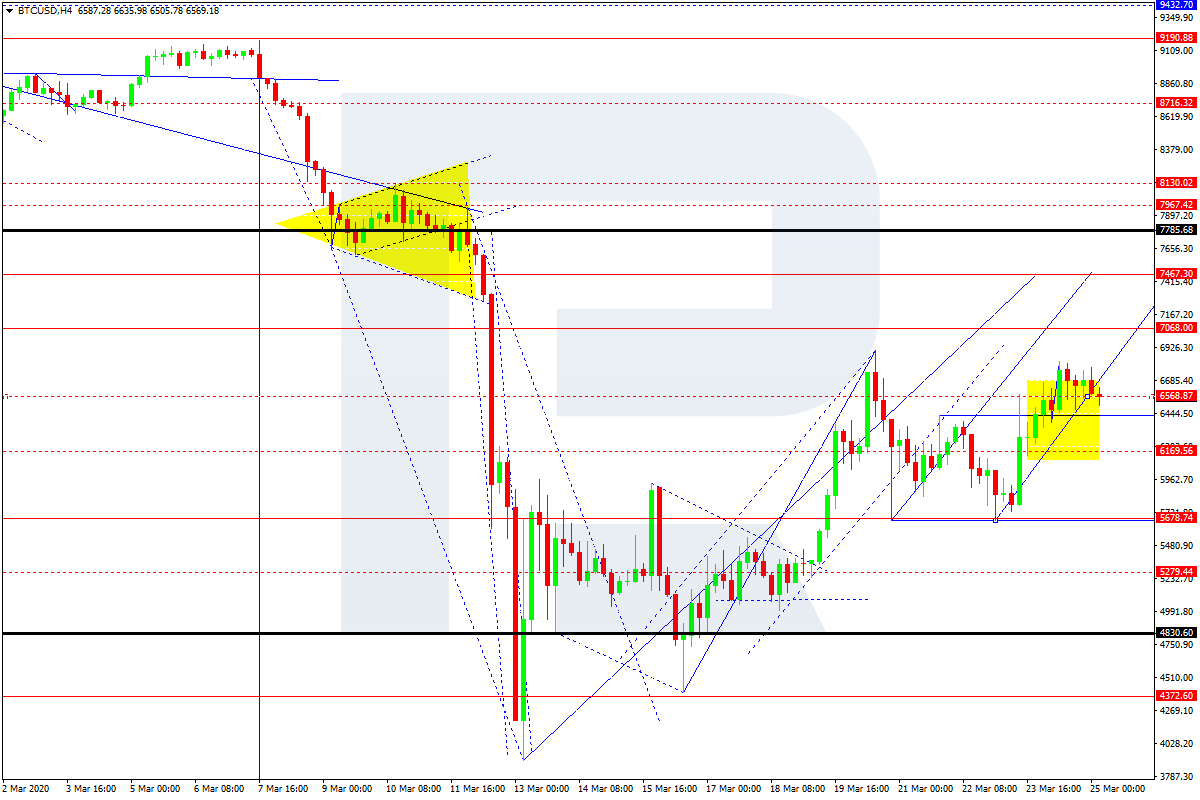

BTCUSD, “Bitcoin vs US Dollar”

BTCUSD is consolidating around 6500.00. The main scenario implies that the instrument may resume growing to reach 7500.00 and then correct towards 5700.00. After that, the instrument may start another growth with the target at 7000.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

On Tuesday, US stock quotes rose for the 2nd day in a row. US authorities are going to adopt a package of measures to support the US economy in the amount of $ 2 trillion. The voting in Congress on this issue may be held today. The S&P 500 (+9,4%), Nasdaq (+8,1%) and Dow Jones Industrial Average (+11,4%) rose for the 2nd day in a row. US authorities are going to adopt a package of measures to support the US economy in the amount of $ 2 trillion. The voting in Congress on this issue may be held today. The Boeing aircraft manufacturer soared 21% after reporting a possible resumption of 737 MAX flights this year. The airline sector of the S&P 500 stock index grew by 15% due to the state aid allocation to the industry in the amount of $ 40 billion. Industry indices showed impressive growth – energy (+ 16%) and banking (+ 13%). Yesterday, the turnover of US exchanges was not too large and amounted to 15.3 billion shares. This is less than the 20-day average of 15.9 billion shares. US macroeconomic data on Tuesday was very weak. All business activity indicators calculated by IHS Markit (Composite, Manufacturing and Services) fell in March to a record low. The growth of unemployed per week was the highest since 2012 and amounted to 70 thousand people. The total number of new unemployed per week was 281 thousand, which is a maximum for 2 and a half years. Today data on durable orders for February will come out in the United States. The ICE exchange’s dollar index is down for the fourth day in a row today. Investors fear that the Fed’s monetary emissions to implement measures for the US economy support may weaken the exchange rate.

European stock indices continue to rise today

European stocks rose yesterday in anticipation of measures to support the US and global economies. The daily increase in the EU STOXX 50 pan-European stock index by 10% was the highest since 2008. Growth was led by industry indices of mining and oil and gas companies, which added more than 15%. Today, European exchanges continue to grow. Shares of German metallurgical holding Thyssenkrupp soared 12.5% thanks to reports on cost optimization and staff reductions. IFO business activity indicators are coming out in Germany today. EUR/USD quotes are growing today for the 4th day in a row amid weakening dollar. There are not yet any particular positive factors in the EU, but they may occur if the number of patients with coronovirus is reduced in the main European countries.

Nikkei showed strong growth along with other world indices

All Asian indices are up today. Yesterday, Nikkei climbed 8%, the highest daily growth since 2008. The shares of the telecommunications company SoftBank Group Corp grew by 20.5% due to the announcement of the assets sale in the amount of $ 41 billion and the buyback of shares. Over the past 3 days, their growth amounted to 55%. The postponement of the Olympic Games for a year had a positive impact. Today, Nikkei added another 5%, as it became known that the games would still be held in Tokyo. Shares in sportswear manufacturer Asics Corp were up by 17.5%. Hong Kong’s Hang Seng Index rose 3.8% today. Mainland China has announced a slowdown in the spread of the coronavirus epidemic and quarantine cancelation in some parts of the country.

U.S. crude futures’ quotes are traded below $ 25 a barrel. The cost of hydrocarbons rose slightly from multi-year lows. However, market participants almost did not respond to large-scale measures by the Fed and the US government to support the US economy. The major banks are slow to increase their forecasts on oil prices.. In particular, ING Bank lowered its forecast for Brent prices in the 2nd quarter from $ 33 to $ 20 per barrel. Yesterday, an independent American Petroleum Institute unexpectedly announced a decline in US oil inventories over the week, while all analysts, of course, expected their increase. Today, the Energy Information Administration will release official data on changes in US oil reserves. If they decline, oil quotes may rise.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

The situation in Gold remains very tense, even though it is holding above 1,440/450 USD, which is a positive sign from a technical perspective.

While Gold, given the recent developments around the massive monetary stimulus from the Fed on March 15, stays bullish in the mid- to long-term (especially after the March 23 Fed announcement to go for “QE Infinity” making a run above 2,000 USD only a question of time), the short-term picture is bearish and selling pressure on the precious metal is likely to persist.

The reason for that is the US dollar. The Fed emergency statement on March 15 pointed to the re-installation of swap lines with global central banks.

To make long things short: this step clearly aims to make sure that global central banks have enough USD available, overcome the current USD shortage in global financial markets.

That said, we expect the demand for the greenback to stay high. The same should be expected in regards to the pressure on credit markets, forcing further liquidations, also in Gold, in our opinion.

If in addition to that, if the Durable Goods Orders come in better than expected, US yields could see another lift and a deeper corrective move back above 1% in 10-year US Treasuries could be seen.

Out of this, a short-term a drop below 1,440/450 USD would technically darken the picture, activating 1,250/260 USD as a first target.

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between December 21, 2018, to March 24, 2020). Accessed: March 24, 2020, at 22:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

– As President Trump recently discovered, the novel coronavirus cannot be “talked down.” Delays and unpreparedness in the US and Europe are proving costly to the rest of the world in terms of public health and economic damage.

The epicenter of the novel coronavirus outbreak is now in Europe and the United States, where the number of the infected may soon exceed those in Italy and China, respectively. Since complacency and inadequate preparedness prevailed outside China until recently, the human costs of the global pandemic are accelerating.

By calling the virus “Chinese,” even against the reprimand of the WHO, the Trump administration is appealing to the worst racial instincts, thereby contributing to hate speech, stigmatization, as well as anti-Chinese and anti-Asian incidents in America.

The White House hopes to disguise its inadequate preparedness, followed by the failure in containment and local testing (which has barely started).

On March 16, the New York Times released a balanced investigative report about the Trump administration’s mishandled virus response. A day later, the administration shared with the Times its pandemic report. Ostensibly, the White House hoped to show it was in control.

But timelines reveal tell a different story.

Costly complacency

Even though the leading US health executives had been monitoring the crisis since early January and the first COVID-19 case was confirmed in the state of Washington on January 20, followed by the WHO alerts, White House failed to act upon pressing evidence – even against the warnings of the US national intelligence community.

Not so long ago, Trump’s still said publicly that any danger would pass by April 1. When he finally understood the risks, he botched his error-ridden Oval Office virus address and the subsequent mistake-ridden Rose Garden address. Until mid-March, the infection enjoyed a relatively free ride in America.

The pandemic report was clear about the consequences: “A pandemic will last 18 months or longer and could include multiple waves of illness… Increasing COVID -19 suspected or confirmed cases in the U.S. will result in increased hospitalizations among at-risk individuals, straining the health care system.” Shortages would ensue.

In the UK, comparable stumbling has caused a similar debacle, which Prime Minister Boris Johnson has tried hard to express in optimistic terms: “We can turn the tide within the next 12 weeks.” Yet, that cannot be achieved without restrictive measures, which, in turn, could have been launched weeks ago.

In contrast, German Chancellor Angela Merkel has been blunt: “Not since World War II has our country faced a challenge that has required such a high degree of common and united action. We can succeed as long as everyone truly understands what’s needed.”

What could have been a multi-month pandemic has now potential to become a multi-year challenge.

Explosion of new cases in the US and Europe

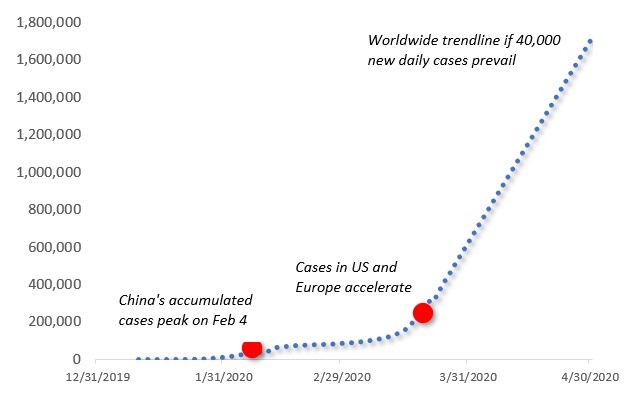

The cold reality is that the US and Europe are mobilizing with a delay of 4 to 8 weeks. As the number of accumulated confirmed cases worldwide is approaching half a million, new cases are increasing by more than 40,000 daily; that is, nearly four times faster than just one week before.

In the worst phase of the Chinese outbreak, the comparable acceleration was barely 4,000; that is, only a tenth of the acceleration outside China today. This escalation is largely attributable to the virus situation in Europe and the US, where the number of accumulated cases will soon exceed that in China.

Assuming that new cases in China will remain low and imported cases can be quarantined; the volume of accumulated cases could remain less than 85,000 at the end of April. But if cases will continue to soar by 40,000 daily outside China – particularly in the US and Europe – through April, worldwide cases would soar to some 1.8 million (Figure).

Figure One trendline scenario (through April 2020)

Source: Difference Group; data from WHO

Over time, such a scenario could translate to huge collateral damage in emerging Middle East, Latin America, Asia and Africa – through plunges in world finance, trade, investment, and migration.

However, since such a projection is based on current acceleration and steady increases, it is only one possible scenario. In reality, the final figure will prove lower, if the acceleration slows down – or even higher, if it doesn’t.

Cooperation vital to preempt new virus waves, outbreaks

After the restrictive measures are phased out in major economies, certain countries are likely to record odd spikes in death rates, particularly in the virus risk groups. It is a discrete modern-day version of the old eugenics, which permits certain policymakers in the West to bury their mistakes, literally.

As poorly-enforced quarantines are phased out in these countries, flows of people, many of which may be asymptomatic, will start traveling again. Eventually, they will show up in the borders of countries that have managed the crisis relatively successfully – as evidenced by recent spikes of imported cases in China, Singapore and Hong Kong.

What is desperately needed to avoid further nightmare scenarios is multipolar cooperation among major economies and across political differences. In this quest, China, where containment measures have been successful, can show the way, along with major advanced and emerging powers.

Effective global cooperation is urgently needed to reduce the subsequent collateral damage.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

This commentary is an updated part of Dr Steinbock’s COVID-19 briefing on March 16, released as “The Global Coronavirus Contraction” by the World Financial Review (March/April) on March 23, 2020