Shares of Kiniksa Pharmaceuticals traded higher after the company reported early success in treatment response for mavrilimumab in six patients with severe COVID-19 pneumonia and hyperinflammation.

This morning, Hamilton, Bermuda based biopharmaceutical company Kiniksa Pharmaceuticals Ltd. (KNSA:NASDAQ)announced “early evidence of treatment response with mavrilimumab, an investigational fully-human monoclonal antibody that targets granulocyte macrophage colony stimulating factor receptor alpha (GM-CSFRα), in a treatment protocol in patients with severe coronavirus 2019 (COVID-19) pneumonia and hyperinflammation.”

The company advised that “the treatment protocol was conducted by Professor Lorenzo Dagna, MD, FACP, Head, Unit of Immunology, Rheumatology, Allergy and Rare Diseases IRCCS San Raffaele Scientific Institute and Vita-Salute San Raffaele University in Milan, Italy, within a COVID-19 Program directed by Professor Alberto Zangrillo, Head of Department of Anesthesia and Intensive Care of the Scientific Institute San Raffaele Hospital and Professor in Anesthesiology and Intensive Care, Università Vita-Salute San Raffaele.”

The firm stated that the treatment protocol tested the investigational drug mavrilimumab in an interventional, single-active-arm pilot experience. “Patients suffering from severe pulmonary involvement of COVID-19, acute respiratory distress, fever, and clinical and biological markers of systemic hyperinflammation status were treated with a single intravenous dose of mavrilimumab with the objective of reducing incidence of progression of acute respiratory failure, the need of mechanical ventilation, and the transfer to the intensive care unit.”

The company noted that so far six patients have been treated with mavrilimumab using the treatment protocol and that mavrilimumab has been well-tolerated. The firm reported that all of the patients showed an early resolution of fever and improvement in oxygenation within 1-3 days and none of the patients’ conditions progressed to require mechanical ventilation.

Professor Dagna commented, “Patients with COVID-19 die of a devastating pneumonia caused by a hyperinflammation syndrome…Last week my team administered mavrilimumab to 6 patients who were experiencing a steep decline of pulmonary status due to COVID-19 pneumonia. All patients responded on treatment, and 3 out of the 6 patients were discharged within 5 days. The data are compelling, and I look forward to continued studies of mavrilimumab in COVID-19.”

The company’s Chief Medical Officer John F. Paolini, MD, PhD, remarked, “These data are the first reported evidence of early treatment response with GM-CSF antagonism in COVID-19…By blocking GM-CSF signaling, mavrilimumab works upstream of interleukin-6 and potentially addresses the underlying pathophysiology of the hyperinflammation which may be responsible for the severe pneumonia of COVID-19. Controlled clinical studies are required to fully characterize the potential of mavrilimumab in this disease. Building upon our activities over the last several weeks, we continue to evaluate the data and next steps, including a potential Phase 2/3 clinical development program.”

The company explained that mavrilimumab has not yet been approved for any indication in any country and described mavrilimumab as “an investigational fully-human monoclonal antibody that is designed to antagonize GM-CSF signaling by binding to the alpha subunit of the GM-CSF receptor (GM-CSFRα).” The company listed that the lead indication for mavrilimumab is giant cell arteritis which is an inflammatory disease of medium-to-large arteries. The firm advised that mavrilimumab was safely dosed and met primary endpoints in Phase 2b clinical studies in Europe of more than 550 patients suffering from rheumatoid arthritis.

Kiniksa Pharmaceuticals is focused on discovering, acquiring, developing and commercializing therapeutic medicines for patients suffering from debilitating autoinflammatory and autoimmune diseases with significant unmet medical need. Kiniksa’s pipeline of product candidates across various stages of development include Rilonacept for the potential treatment of recurrent pericarditis; Mavrilimumab for the potential treatment of giant cell arteritis; KPL-716 for the potential treatment of a variety of pruritic diseases, including prurigo nodularis, a chronic inflammatory skin condition; and a few others.

Kiniksa Pharmaceuticals has a market capitalization of around $678.8 million with about 55.55 million outstanding shares. KNSA shares opened nearly 37% higher today at $16.74 (+$4.52, +36.99%) over the yesterday’s closing price of $12.22. The stock has traded today between $14.52 and $17.46 per share and currently is trading at $15.43 (+$3.21, +26.27%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Maurice Jackson of Proven and Probable discusses the future of DNI Metals with the company’s executive chairman.

Maurice Jackson: Today we will share a graphite development company set for production. Joining us for a conversation is Dan Weir, the executive chairman of DNI Metals Inc. (DNI:CSE; DMNKF:OTC).

Mr. Weir, welcome to the show, sir. Delighted to have you back to provide us with a number of updates regarding DNI Metals, which is focused on becoming one of the world’s leading graphite producers. Before we begin, Mr. Weir, please introduce DNI Metals and the opportunity the company presents to the market.

Dan Weir: Maurice, in late 2014, DNI Metals conducted research on the value proposition of graphite. We put together a team consisting of engineers, process engineers, mining engineers and geologists with expertise consisting in building four graphite processing plants in Canada [and] Australia, and had operated in graphite mines in Canada and Sri Lanka.

In our analysis we concluded that we wanted to position ourselves to become one of the world’s leading graphite producers. Graphite, which has a number of industrial purposes, will be seeing increased demand with electrification of cars, in particular, in lithium-ion batteries. To clarify, as demand increases for more and more lithium-ion batteries, the demand for graphite will increase. Why, 30% of a lithium-ion battery is graphite; by comparison it’s only about 2% of a lithium-ion battery that is lithium.

DNI Metals saw the demand curve increasing over the coming years and wanted to position our shareholders to take advantage opportunity before us. China dominates the graphite production in the world, therefore we needed to find a competitive advantage geographically outside of China that would allow us to have low production costs.

Our research determined that we should focus our efforts in Brazil and Madagascar. And the reason why we targeted Brazil and Madagascar is because of their similarities in climate. Both are hot and receive a lot of rainfall, which produces a weathering effect on rocks called a laterite or a saprolite. And really, it’s just a fancy word meaning that it’s a sandy, clay material that you can just go in with an excavator, dig it up and process out the graphite. In 2015 we acquired a promising graphite project in Madagascar and have since added a second project adjacent to our first property.

Maurice Jackson: And let me ask you, by the way, where are you today?

Dan Weir: I’m back in Canada. I’ve been home for a few months and like billions of other people in the world, I’m isolating myself here at home.

Maurice Jackson: And can you provide us with an update on the impact that the coronaviruses having in Madagascar?

Dan Weir: I checked this morning. Officially in Madagascar, there’s about 39 cases as of this morning. I can assure you I’ve been to hospitals in Madagascar before and that number is probably a lot higher. They don’t have the testing facilities, they don’t have the tests. So I’m confident that those numbers are or will be much higher. Madagascar has locked down the country.

What I mean by that is there are no flights in or out of Madagascar. There are no cruise ships allowed to dock in the countryno other boats except for container ships bringing goods and supplies in and out of the country. Everything else is locked down. The schools are shut down. I believe today the government will be institute a curfew. Citizens will be allowed to be out of the house between 5 a.m. and noon, but the rest of the time, you must stay at home and not work outside of that.

This will be quite a challenge because in Madagascar 58% of the population does not have access to clean drinking water, 75% of the population lives in poverty; that’s less than $1.90 a day. Maurice, as a comparison your Starbucks coffee this morning probably costs more than that. Or, now that you’re stuck at home, the coffee that you make, your instant coffee or whatever else, still probably cost you more than a $1.90 a day. So the other interesting fact is that 75% of the population doesn’t have electricity.

So they’ve got to go out every single day and get food, because they don’t have refrigeration. . .they’ve got all these little markets that people go to, and I’ve driven through many of those markets and there are thousands and thousands of people all next to each other, all shopping. So what they’re going to try and do is contain that as much as possible. But I think you’re going to find that it will spread pretty quickly in places like the capital city and some of the other cities.

Even within Madagascar, you’re not allowed to leave the cities. They have the military set up [so] you can’t leave the capital city. Nobody in or out of the major cities as well. So we’re home here in Canada; our management team and all our board are here in Canada isolating themselves. And as of right now, nobody’s showing any signs of the coronavirus.

Maurice Jackson: In our last interview we talked about the termination of personnel in Madagascar, environmental permits and Cougar Metals. Beginning with the former, shareholders were informed that DNI terminated its Madagascar team for falsifying government documents and misappropriating funds, and were taking the previous country manager to court. Has a court hearing taken place, and if yes, what was the verdict?

Dan Weir: On February 19, 2020, a trial was held. On March 5, 2020, a judgment and sentencing was released. The formal reports or court documents, we don’t have them yet. We were supposed to pick them up a few days ago, but because of the coronavirus, all the courts are locked down. So I’m not sure when exactly we’ll get that. So I don’t have all the details.

My lawyers, having talked to the prosecutors and the judge afterward, have told us that our previous country manager, Mr. Stephen Gertz, was convicted of fraud, and what that means is that he had misappropriated funds, and he had falsified government documents in relation to the environmental permits. Mr. Gertz had also made all sorts of different claims to the courts about me. One of the things that he went to the courts. . .and said [was] that I had illegally gone and falsified, or made a false declaration, to the police.

Mr. Gertz and his team were terminated on October 15, 2018. At that time, we requested that he return all documents owned or pertaining to DNI and its businesses. We requested that multiple times. Mr. Gertz refused to give us those documents. Therefore, in an attempt to retrieve our documents from Mr. Gertz, DNI Metals, under counsel with prepared documents, went to the police.

The documents were in French and stated that certain documents had been stolen from us. What came out in the trial [is that] Mr. Gertz said, “Well no, these documents haven’t been stolen. I have all these documents. Here they are.” DNI Metals had requested all documents in Mr. Gertz’s possession because some of them were required to file our tax returns. Okay. Mr. Gertz would not return the documents that we needed to file the tax returns. So what we did is, again, at the advice of counsel, we went and prepared a document.

I signed the document, it was taken to the police and registered. It was then we could go to the tax authorities, and the tax authorities could provide us with copies of the proper documents, in order to file the tax returns. Mr. Gertz, during the trial, went to the court and said, “Mr. Weir’s lying because I have all the documents. He’s lying if he says that they were stolen.” Anyways, it’s semantics and we are fully confident that the courts will drop all the charges against me in an appeal.

Maurice Jackson: Speaking of permits, what are the last developments regarding the environmental permits on the Vohitsara and the Marafody, respectively?

Dan Weir: I’m happy to announce that we have gotten conditional approval for all of the environmental permits. When we terminated the previous team, they had not filed the documents with the authorities, nor did they pay the proper fees. They did not conduct the public consultations out at the sites with all the different locals. And they also did not do the technical reports properly and did not have the technical meeting at the sites.

To ensure compliance moving forward on our permitting, I had to conduct a thorough investigation and analysis to determine they meet and or exceeded the Minister of Mines’ expectations and requirements. And I am happy to convey that applications process has been completed by DNI Metals and is awaiting final approval by the Minister of Mines.

The ONE, or the environmental agency, has conditionally approved all of our permits. The last step is that we need the official title cards for our permits, or for our projects, and that has to come from the Minister of Mines, which signs approval and sends it over to the Registration Office, which will provide us our title cards.

DNI owns two properties in Madagascar. Both of them are PE permits, meaning that they can go into production. The last thing we’re waiting for is just the title cards for both of our projects, and it’s the transferring of the name from the old owners over to us.

Under Malagasy law, the Registration Office has 45 days to respond. In practice, it has taken a lot longer for a lot of reasonsone being of the aforementioned, from our previous country management teams’ fraudulent activities. And there is now a new government, which came into power in January 2019. The new government has put a hold on issuing any documents, any title cards, any licenses.

DNI is having to wait for approval because the new government wants to make some changes to the mining code. They had talked like they were going to make some major changes. I believe that they have backed off on all of that. By June of this year, and you can see it in the press release, we anticipate that they will provide us their final answers on what they want to do.

I personally think what they want to do isor what will end up happening isthat they will probably increase the royalties they will be receiving. Currently in Madagascar, there is a 2% royalty on a project like ours, and the tax rate in Madagascar is 20%. We were always very happy with that. Just as a comparison, if you’re a mining company in Canada, your tax rate is probably somewhere around 2426%. I think if you’re in the United States you would probably be over 30%; don’t quote me on that, but I think you’d be well over 30%.

The new government wants to increase the royalty rate from 2% to 4%. We’ve run that through some of our models and it really doesn’t change much. Obviously, we don’t want to see any increase in the royalties, but it’s not really going to affect us in a material way on the project.

Maurice Jackson: And once you receive the environmental licenses, then it’s off to building the pilot production plant. Is that correct?

Dan Weir: Yes, and as we’ve stated before, it is designed and engineered. So we are ready to go. It’s been great working with the environmental offices. They were absolutely amazing to work with. We just need the Mines Minister to sign off, and we’re in constant contact. Just so readers are aware, I have people in Madagascar that keep in constant contact with Minister of Mines and the Registration Office. I’m in constant contact with them, and many other people as well.

DNI Metals keeps pushing on them, and we believe that it will come sooner [rather] than later. I know I’ve been promising that for almost two years. But as I said, we’re in the bottom of the ninth and it is all happening.

Maurice Jackson: Let’s move on to Cougar Metals NL (CGM:ASX). Are the any developments regarding Cougar Metals that shareholders need to be made aware of?

Dan Weir: Since our last press release, which we put out in December, there’s nothing really new. Cougar is currently in default of the agreement, and there are no payments that DNI is required to make at this time. There is nothing further material to comment on this matter at the present.

Maurice Jackson: Switching gears, let’s discuss trading. Provide us with some background on why trading halted on the Canadian Stock Exchange (CSE), and what actions have been taken to resolve this matter. And when can we expect to see trading resume?

Dan Weir: In order to run a public company, it’s very expensive. It can be somewhere between $100,000 and $200,000 a year by the time you pay audit fees and legal fees, and pay the monthly fees that you have to pay to the exchanges. DNI Metals completed the audited financial statements as of December 31, 2018.

It’s all about the money. The auditors also completed their work. The auditors and the audit committee and the board of directors have signed off on them, but the auditors won’t sign them yet, until we pay them. So we have their fees outstanding and to release those audited financials, we’ve had all the other financialsthe three other quarters throughout the yearand now we’re into the next year to complete the audit financials. We have been working and keeping track of everything, but it’s all about having the money to be able to do that.

We’re glad we have received verbal confirmation from a number of shareholders who have stated, “Hey, get the permits and we will give you money.” We’ve also been working with the regulators to get a partial revocation order. What that means is that we would be allowed to go out and raise some money here in order to finish off our financial statements, and get the stock up and trading.

So the short answer is, Maurice, I need money in order to get the stock up and trading. I’ve had many people say to me that they would give us money if we had the permits, so I’m in a Catch-22 situation right now.

Maurice Jackson: Understood. Dan, besides the aforementioned, what are some questions that you’re receiving from shareholders, and what is your message to shareholders?

Dan Weir: We know shareholdersthe board of directors, myselfwe all want to see the stock up and trading. We continue to work on that. We continue to look at all sorts of different options. Right now, with the coronavirus and very low oil prices, the demand for electric cars may trend downward near term. I am still confident that the future is strong for electric cars, and computers and cell phones. But right now it’s going to be a little bit up in the air.

The one thing that I’m seeing out here is that a lot of the different graphite mines in China have shut down. The largest graphite mine in the world, which is in Mozambique, has also shut down right now because of the coronavirus. So I think that demand will come back as we get out the other side of this. I can’t tell you what oil prices are going to do out here.

I do know that the future is still very strong, [based on] the need for more and more lithium-ion batteries, whether it’s for electric cars, or cell phones, computers. I know that we’ll be strong, but I can assure you that right now it’s going to be some tough times out here in the markets over the next while.

Maurice Jackson: Mr. Weir, for someone [who] wants to get more information on DNI Metals, please share the contact details.

Maurice Jackson: And as a reminder, DNI Metals is listed on the CSE, symbol DNI; and on the OTC, symbol DMNKF. DNI Metals is a sponsor of Proven and Probable and we are proud shareholders of DNI Metals for the virtues conveyed in today’s message.

Before you make your next bullion purchase, make sure you call me. I am a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio, from physical delivery, offshore depositories, precious metal IRAs and private blockchain distributed ledger technology. Call me directly at (855) 505-1900 or you may e-mail [email protected].

Finally, we invite you to subscribe to www.provenandprobable.com, where we provide mining insights and bullion sales.

Dan Weir of DNI Metals, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: DNI Metals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: DNI Metals is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

Few investments are working these days. Oil, blue-chip stocks, cotton, lumber major mining companies. . .all have been decimated in the past six weeks. Teck Resources Ltd. (TCK:TSX; TCK:NYSE) is down 73% from its 52-week high. Copper is 27% lower than it was a year ago. Yet the gold price has done quite well, up 30% from last year’s low and near a seven-year high.

With the strength in gold, gold juniors could make a move higher even as other stocks languish. Juniors with strong management teams, good projects in favorable jurisdictions and attractive valuations offer compelling upside potential, albeit with commensurate high risk. Precious metals companies in Canada are also benefiting from a significant move in the Canadian dollar/US dollar (CAD/USD) exchange rate (project costs in CAD declining versus USD gold price).

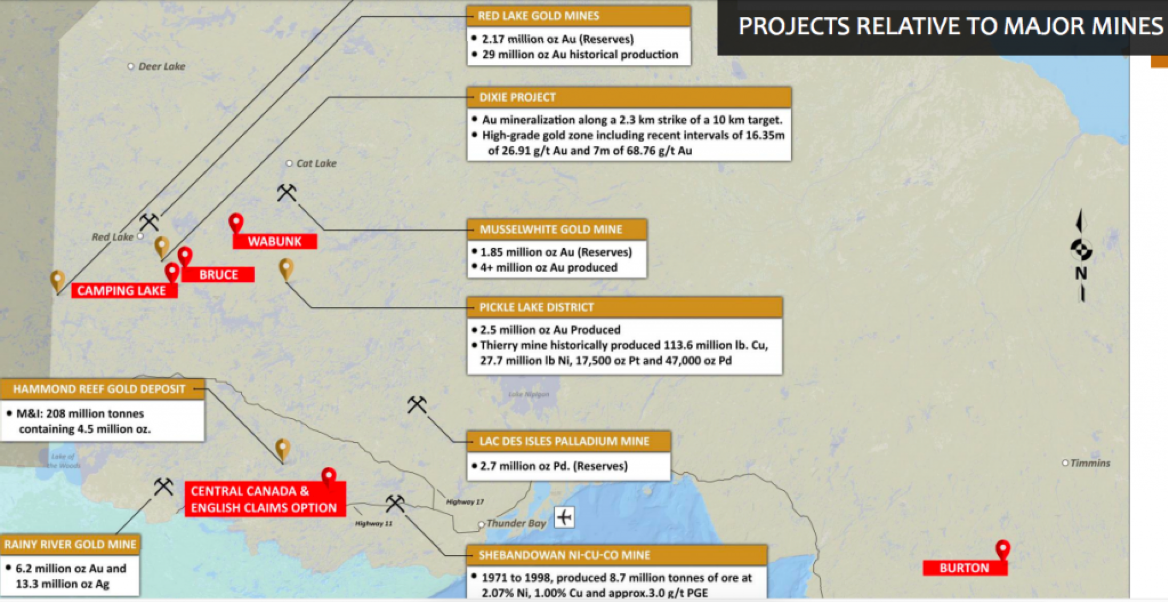

A small-cap company worth learning more about is Falcon Gold Corp. (FG:TSX.V). It has an amazing team for a company with a market cap of just CA$2 million. Management has a lot of skin in the game, there are multiple Canadian projects, and more assets are poised to possibly come into the company. The following interview is of CEO and director Karim Rayani. Please continue reading to find out why an investment in Falcon Gold is well worth considering [corporate presentation].

Peter Epstein: Please give readers a history of Falcon Gold Corp.

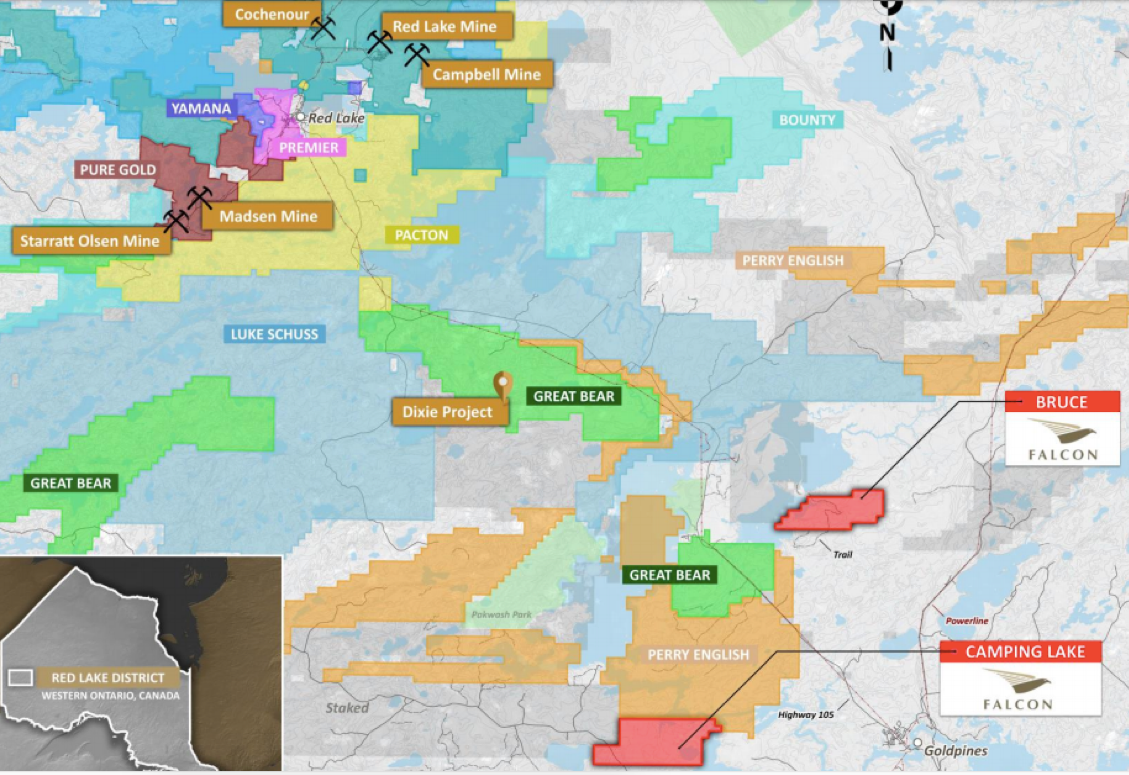

Karim Rayani: Falcon is a Canadian mineral exploration company focused on generating, acquiring and exploring high-grade opportunities in the Americas. Our Ontario, Canada, projects include the Central Canada gold project, the Wabunk Bay gold/base metals project in Red Lake, the Bruce and Camping Lake gold projects, also in Red Lake, and a 49% interest in the Burton gold property with Iamgold.

The company is focused on high-grade acquisitions [with] a lengthy history of mining, where we can generate results rapidly and cost effectively, using modern exploration methods, to update, enhance or introduce new NI-43-101-compliant mineral resource estimates. We have five Canadian projects at the moment.

PE: Can you tell us about Falcon’s management team, board & corporate advisors?

KR: Falcon is led by a seasoned team of mining execs. I stepped in as CEO about nine months ago and am the largest shareholder. I’ve been a financier for the past 15 years, focused on domestic and international exploration projects. We have assembled a world-class team that has had tremendous success in the mining sector.

Tookie Angus needs no introduction: He’s the former head of global mining group Fasken Martineau. For the past 40 years, Mr. Angus has focused on structuring and financing significant international exploration, development and mining ventures. He has had a long string of successes. Tookie’s a lawyer by trade and will be very valuable to us as we advance our Central Canada project.

On the geological side, top-shelf former Rio Tinto and Anglo American geologist Ian Graham is overseeing the planning of our exploration programs. Mr. Graham is an accomplished mining executive with over 20 years’ international experience exploring for and developing mineral deposits. He has vast experience in bringing projects to scale and seeing things that others don’t. Ian is ideally suited to be overseeing our data.

PE: You mentioned several promising properties/projects. Which are the top two priorities for 2020?

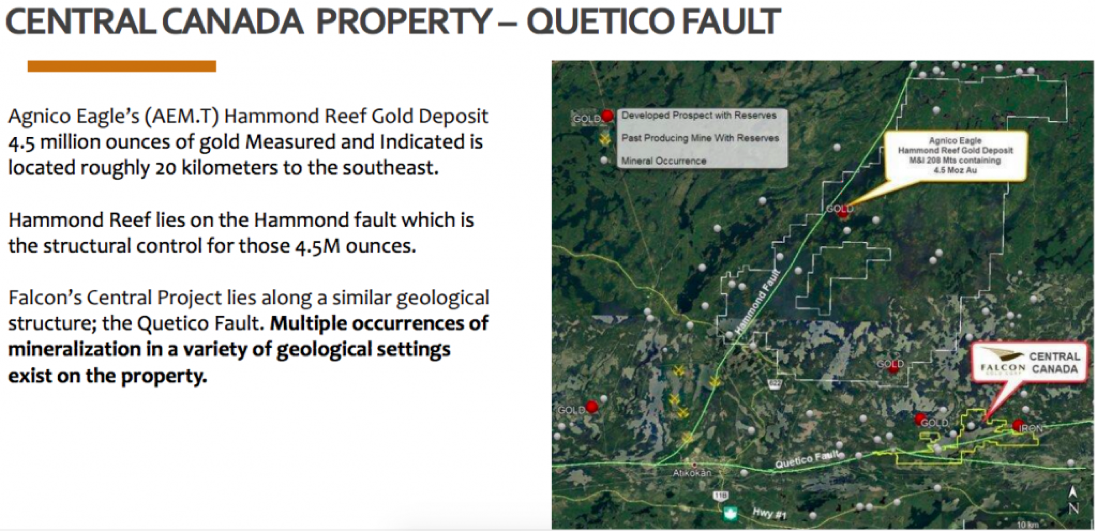

KR: Central Canada is Falcon’s flagship project. It’s 20 kilometers on a parallel system to Agnico Eagle Mines Ltd.’s (AEM:TSX; AEM:NYSE) Hammond Reef deposit in Northwest Ontario. They have a 4.5-million-ounce [Measured and Indicated] gold resource. The Hammond Fault is the structural corridor for those ounces.

Our project is on the Quetico fault, a similarly major structure in its own right. We have been successful in closing two joint ventures (JVs); in one we still hold a 49% interest, with IAMGOLD Corp. (IMG:TSX; IAG:NYSE) holding 51%. It’s a testament to our ability to source projects and package them without overly diluting shareholders.

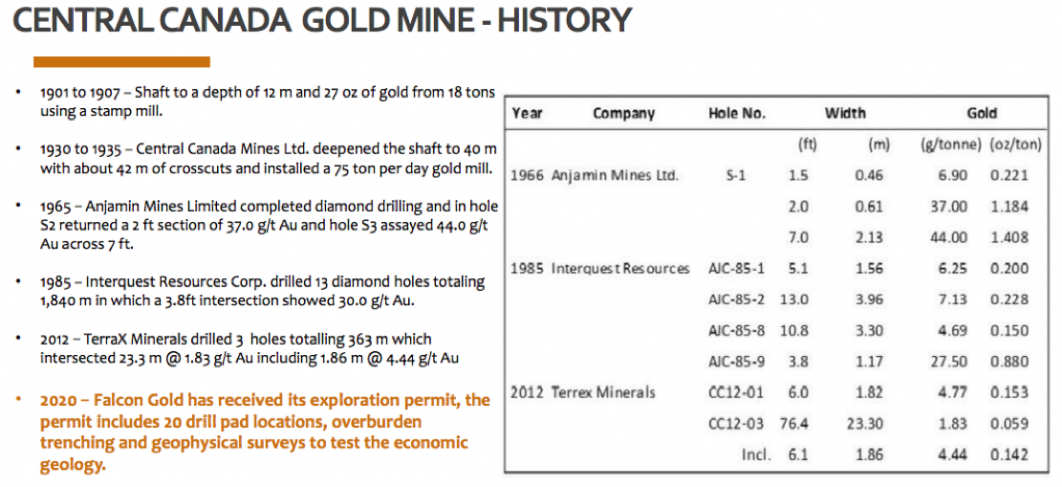

PE: Please give us more detail about the considerable amount of historical work that has been done on your Central Canada project.

KR: Gold mineralization can be traced widely across the Central Canada property. More recent drilling by Interquest Resources Corp. intersected over one meter at ~30 grams per tonne (g/t) gold in diamond drill core. In 2012, TerraX Minerals (now Gold Terra Resource Corp. [YGT:TSX.V; TRXXF:OTC; TXO:FRANKFURT]) hit 23.3 meters (23.3m) of 1.83 g/t gold.

Trenching work in 2011 indicated significant gold mineralization to the south of the historic Sapawe gold mine, where the operator sampled up to 6.7 g/t gold. Significant gold mineralization of up to 24 g/t has also been identified in the halo of the original Sapawe mine.

PE: Explain the English Claims option. How important is this option?

KR: The English Claims tie directly onto the Central ground. There are some very rich gold targets that we will be going after. Readers should note, only a small percentage of the property has been explored in any meaningful way.

PE: How far do you think that you will have to advance the Central Canada project before a strategic investor might want to invest in it?

KR: We think interest from strategic investors could come as soon as this year. Our objective is to start drilling right away, as we have received our drill permit. We are confident that we will come back with strong results from twinning historical high-grade holes.

We will update historical and new data into a NI-43-101-compliant resource. Upon completion of the twining of historical holes, infill drilling and testing the deposit at depth, we expect to get an indicative scope of the size and economic potential of the project.

PE: You have farmed out your Camping Lake property, retaining a small net smelter return (NSR). Could this asset still move the needle for Falcon Gold if your farm-out partner has success?

KR: Either way, Falcon is in a very good position. We still have a 49% economic interest once International Montoro Resources (IMT:TSX.V) spends $300,000 in the ground. They can opt for an additional 24% for a one-time payment to us of $500,000. At that point we would retain a 25% percent interest in the project plus a 0.5% NSR. So yes, we absolutely still have skin in the game here.

PE: No doubt your team likes northern Ontario quite a bit. What makes it a great place to explore, and potentially develop mining projects?

KR: We are in one of the best jurisdictions for mining, period. The amount of success in this area is quite profound. Great Bear Resources Ltd. (GBR:TSX.V; GTBDF:OTCQX) has had tremendous success. We are surrounded by multimillion-ounce deposits. The political environment could not be better. The area is prospective for both high-grade gold and base metals. The regional infrastructure is outstanding.

PE: Although there have been, and continue to be, notable success stories in the Red Lake mining district, why hasn’t the area become even more busy, with gold recently touching US$1,700/ounce, and now at about US$1,650/ounce?

KR: The sector has been beaten up. It’s only relatively recently that some of these companies have seen an influx of capital. Whenever there is a discovery there is a flow of money. Larger companies are paying dividends and reporting record revenues. In order to compete, we will need to see a further spike in the price of gold for the junior miners to gain real momentum. With current world events effecting the markets, it’s not a matter of if, but when, gold prices move even higher.

PE: How do you plan on funding your exploration programs?

KR: The company is currently fully funded for 1,000 meters of drilling. Could we use more money? Yes, of course. But we’re raising funds only when those dollars are used for drills turning. I’m committed to doing the work while preserving our cash and protecting the capital structure. That means no dilutive financings.

PE: There seems to be support for a strong gold price through at least the U.S. presidential election in November. What are your thoughts on gold?

KR: I don’t think there has been a better time to have exposure to precious metals. I have always been a gold bug, and we’re seeing near record highs since 2013. With inflation and global stimulus packages kicking in, I believe it’s only a matter of time before a wave of investment capital flows into our sector.

PE: Where do you stand with regard to acquiring new assets or farming out existing assets?

KR: Falcon’s flagship asset is our Central Canada project, but we are also focused on generating revenue through royalties and acquiring additional assets. It’s the only real way to set us apart and generate long-term shareholder value. We hope to be able to announce the addition of one or two new projects in coming months, so your readers should keep Falcon Gold on their watch lists!

PE: Thank you, Karim. There is a lot going on at Falcon Gold. I truly look forward to updates on the company this spring and summer.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed below. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: Gold Terra and Great Bear Resources. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Gold Terra Resource Corp., a company mentioned in this article.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Falcon Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Portofino Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Epstein Research [ER] has no prior or existing relationship with Falcon Gold, but is pursuing a marketing relationship. Readers should consider this interview to be biased in favor of Falcon Gold. At the time this interview was posted, Peter Epstein of [ER] owned no shares of Falcon Gold.

While the world has entered into a financial crisis, the worst is still yet to come. When the global contagion continues to spread, the crisis will turn into a FINANCIAL STORM, in which few are prepared. Unfortunately, the analysts on CNBC and Bloomberg continue to provide incorrect forecasts because they are looking at the markets in a linear fashion. What lies DEAD ahead is a collapse and disintegration of a way of life that won’t return as it was in December 2019.

Thus, it is important to understand that “Business, as Usual” is over for good. With the United States on lockdown for at least another month, the situation in the financial system and economy will continue to deteriorate. It won’t matter how much the Fed and central banks prop up the markets, because the Fundamental Economy has suffered a massive heart attack.

In my newest video update, Silver Investing During The Coming Financial Storm, I explain why it’s essential to acquire physical silver bullion as the negative impacts from the global contagion has just only begun:

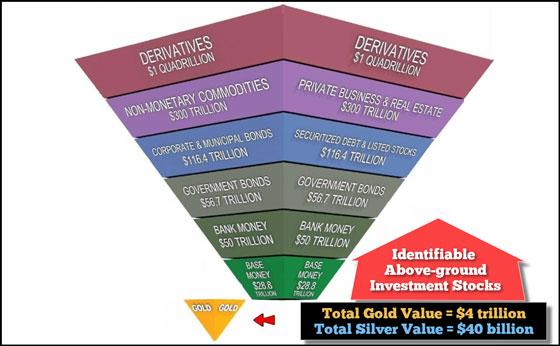

In the video, I explain how the global contagion has forced investors to move down the Exter’s Pyramid to safer assets, with gold and silver being at the bottom. The largest financial assets (in dollars) at the top, are the weakest. And, now, with Global GDP currently forecasted to decline 36% in Q2 2020, a lot of these financial assets are in serious trouble.

With Government Bonds, Bank Money, and Base Money being the safest financial assets at the bottom, totaling $136 trillion, gold and silver valued at $4+ trillion represents only 3% of those assets or supposed assets. Investors that are currently trying to acquire physical gold and silver bullion are finding it very difficult to obtain supplies. This will only become more difficult as time goes by.

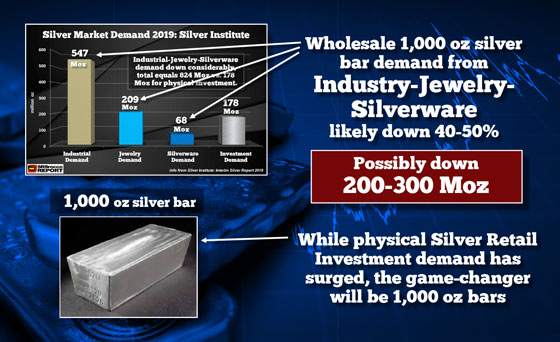

One question that I receive the most is… “Why is the paper futures silver price so much lower than the physical retail bullion price?” While I explained it briefly in my last video, I provide more details using the chart below. HOWEVER…. this is only a temporary situation.

I forecast that as the financial system continues to implode, Large Investors, Hedge Funds, and Institutions will start acquiring 1,000 oz wholesale silver bars to protect wealth. They will not be buying these bars for Industrial-Jewelry-Silverware consumption, but rather, to protect their wealth during the coming Financial Storm.

If it is challenging to acquire smaller retail silver productions (1-100 oz), back ordered for weeks-months, then it makes logical sense to seek out the larger (lower premium) 1,000 bars. While some investors may acquire these 1,000 oz silver bars to make smaller retail products, I believe a large percentage will hold them as an investment while a lot of financial assets continue to lose value.

If you haven’t purchased any Gold or Silver Insurance, you may want to consider doing so before it’s difficult to acquire the physical metal.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Since the outbreak of the novel coronavirus, central banks from the South Pacific to the North Atlantic have slashed interest rates 103 times, injected trillions of dollars of liquidity into the financial system, launched a flurry of loan programs and bought bonds in a firefighting exercise to prevent a global recession from becoming a global depression.

Judging from the recent easing of strains in financial markets, this massive bout of monetary stimulus, along with a trillions of dollars of spending by governments worldwide, will help the global economy overcome the shock from the shutdown of large parts of the global economy to limit the spread of Covid-19.

But in the process, interest rates at all the world’s major central banks, are now effectively at the zero-lower bound, raising uncomfortable questions about the future of monetary policy. Even if policy makers are successful in engineering a recovery, both in asset markets and the underlying economy, is there any ammunition left to tackle the next downturn or a sudden crises? And if asset markets fail to recover, what then? More stimulus? With interest at rock-bottom, the answer by central banks in advanced economies is large-scale purchases of both government and private securities, a tactic now used by all Group of Seven (G7) central banks: the U.S., Japan, the euro area, the U.K and Canada. But it’s not just central banks in developed markets that are using the monetary tool of asset purchases, or quantitative easing. Now it’s being used worldwide. Chile’s central bank is buying bank bonds while the central banks of Israel, Poland, Colombia, the Philippines, South Africa, Jamaica and Iceland are buying government debt in the secondary market. The problem is this tool has been employed to little avail by the Bank of Japan for almost two decades, by the European Central Bank for five years and by the Federal Reserve in various phases since the global financial crises in 2008. While asset prices prices have risen and debt has accumulated, economic growth has trended downward and the wealth gap has widened.

2020 This year started out on a promising note, with uncertainty from the U.S.-China trade conflict easing, confirming the general view the global slowdown was bottoming out. Several important emerging markets, such as Turkey, South Africa and Malaysia, still lowered rates in January due to lingering uncertainty and domestic weakness. Meanwhile, under the radar of most investors, the coronavirus claimed its first Chinese victim on Jan. 11 before authorities on Jan. 23 shut down the industrial of Wuhan, the epicenter of the outbreak, to prevent the spread of the virus. Despite a 10 percent drop in Shanghai stocks in late January, U.S. and global stock markets continued their upward march until Feb. 19, despite the growing storm on the horizon. Although central banks normally trail changes in financial markets, this time they were ahead. Illustrating just how interwoven the global economy has become, Sri Lanka’s central bank was the first central bank to refer to the coronavirus when it lowered its rate on Jan. 29, days before China’s central bank on Feb. 3 began to pump in liquidity to the banking system at lower interest rates. Thailand’s central bank then followed suit by cutting its rate on Feb. 5 and since then the rate cuts have come at a fast and furious pace, spanning the globe from Mongolia to Mauritius.

Since late January, when the outbreak of the coronavirus first began to affect financial markets, policy rates have been cut an astounding 103 times, with many central banks cutting rates multiple times in response to the growing threat to economies worldwide. Illustrating the speed with which the threat to economic growth has mushroomed, 53 of those rate cuts have been taken at multiple extraordinary policy meetings, such as those by the U.S. Federal Reserve, the Bank of Canada, the Bank of England and the Reserve Bank of Australia. From the beginning of 2020, 67 different central banks have cut policy rates 111 times by a cumulative 86.28 percentage points, or a net reduction of 81.88 points when taking into account the four rate hikes seen this year from Kazakhstan, the Czech Republic, the Kyrgyz Republic and Denmark. Including other measures taken to ease monetary policy in addition to rate cuts – such as cutting lowering reserve requirements, countercyclical capital buffers, injecting large-scale liquidity, launching new low-cost loan programs or restarting asset purchases – there have been at least 189 steps to ease monetary policy. The global monetary policy rate (GMPR), the average interest rate by 97 central banks worldwide, has plunged 84 basis points this year to 4.85 percent from 5.69 percent at the end of 2019, 6.42 percent at end-2018 and 5.99 percent at end-2017. 2020 MONTH-BY-MONTH The following 62 central banks cut rates 83 times in March: Australia (twice), Malaysia, USA (twice), Saudi Arabia (twice), Bahrain (twice), UAE (twice), Qatar (twice), Kuwait (twice), Jordan (twice), Hong Kong (twice), Macau (twice), Moldova (twice), Canada (three times), Paraguay (twice), Argentina, Mauritius, UK (twice), Iceland (twice), Serbia, Mongolia, Ukraine, Norway (twice), New Zealand, South Korea, Sri Lanka, Czech Republic (twice), Egypt, Chile (twice), Costa Rica, Armenia, Turkey, Pakistan (twice), Vietnam, Tunisia, Morocco, Poland, Fiji, Trinidad & Tobago, Ghana, Sierra Leone, Brazil, Dominican Republic, Taiwan, Philippines, Indonesia, South Africa, Honduras, Thailand, Namibia, Romania, Mexico, Eswatini, Seychelles, Lesotho (twice, Kenya, Bangladesh, Democratic Republic of Congo, Albania, Zimbabwe, India, Colombia and Barbados. Singapore is not included in this list as it uses the exchange rate as a monetary policy tool. However, it has also eased its policy by letting its dollar depreciate. Kazakhstan and Denmark stand out as the only central banks to have raised rates in March. FEBRUARY 14 central banks cut rates 15 times in February: Iceland, Thailand, Brazil, Honduras, Philippines, Russia, Belarus, Mexico, Argentina (twice), Namibia, Turkey, China, Indonesia and The Gambia. Two central banks, the Czech National Bank and the National Bank of the Kyrgyz Republic, raised rates. JANUARY 11 central banks cut rates 13 times in January: Argentina (3 times), North Macedonia, Turkey, South Africa, Malaysia, Kenya, Lesotho, Sri Lanka, Ukraine, Costa Rica and Azerbaijan, with rates lowered by a cumulative 1,125 basis points while Tajikistan raised its rate. 2020 BY MARKETS Central banks worldwide have taken 198 policy decisions so far this year, with policy rates cut 111 times and only raised five times. DEVELOPED MARKETS Central banks in developed markets have decided on monetary policy 29 times this year, with seven banks cutting their rates 14 times: Australia, the United States (twice), Hong Kong (twice), Canada (three times), the UK (twice), Norway (twice) and New Zealand. Denmark raised its rate but this is the context of a policy framework in which the Nationalbank pegs the krone to the euro. The rate hike should support the krone which has come under downward pressure as capital flows to more liquid currencies. EMERGING MARKETS Emerging market central banks have decided on monetary policy 58 times, with 21 banks cutting rates 34 times: Turkey (three times), South Africa (twice), Malaysia (twice), Thailand, Brazil (twice), Philippines (twice), Russia, Mexico (twice), China, Indonesia (twice), UAE (twice), Qatar (twice), South Korea, Chile (twice), Czech Republic (twice), Egypt, Pakistan (twice), Poland, Taiwan, India and Colombia cutting policy rates. After raising its rate in February, the Czech Republic reversed course in March and cut its rate. FRONTIER MARKETS Central banks in frontier markets have decided on monetary policy 41 times, with 15 banks cutting rates 26 times: Sri Lanka (twice), Kenya (twice), Ukraine (twice), Bahrain (twice), Kuwait (twice), Jordan (twice), Mauritius, Serbia, Morocco, Tunisia, Vietnam, Ghana, Romania and Bangladesh. Argentina has cut six times. Kazakhstan has raised its rate once while Nigeria raised its reserve requirement. OTHER MARKETS Central banks in other markets have decided on monetary policy 69 times, with 24 banks cutting rates 33 times: North Macedonia, Kenya, Lesotho (twice), Azerbaijan, Honduras (twice), Iceland (three times), Belarus, Costa Rica (twice), Namibia, The Gambia, Saudi Arabia (twice), Macao (twice), Moldova (twice), Mongolia, Trinidad & Tobago, Dominican Republic, Sierra Leone, Paraguay (twice), Fiji, Eswatini, Seychelles, Democratic Republic of Congo, Albania and Zimbabwe. Kyrgyzstan and Tajikistan have raised their rates while Curacao has raised its reserve requirement to curb liquidity. 2019 Prior to the outbreak of the coronavirus, 2019 was characterized by the most synchronized monetary easing since the global financial crises in 2008-2009.

Sixty-seven different central banks cut their key interest rates 159 times in response to the lowest growth of in a decade due to the damaging effect of trade conflicts on global manufacturing, confidence, and the lagged effect of monetary tightening in 2018.

In discussion with Maurice Jackson of Proven and Probable, the Mercenary Geologist offers his take on the coronavirus pandemic, its impacts on economic policy and what he’s buying (or not buying) right now.

Maurice: Today we will find out if we are at risk of losing our liberty to the coronavirus, along with buying opportunities for your investment portfolio. Joining us for a conversation is Mickey Fulp, the world-renowned Mercenary Geologist.

Absolute delight to speak with you sir. Mickey, you are the Mercenary Geologist, but you’re equally regarded highly for your views on philosophy and politics, and every time we speak my neurons expand. You and I have shared concerns regarding the erosion of liberty as the federal government and municipalities have been perniciously increasing their influence over the years, and in particular in the response to the coronavirus. Sir, what concerns should we have regarding our liberties that many people are not considering due to the government’s response to the coronavirus?

Mickey: Well, I think it really comes from state and local governments now, and rightly so. The state and local governments are responsible ultimately, not the federal government, for instituting policies regarding what I prefer to call the Wuhan flu, but they are increasingly infringing on our basic freedoms as expounded in the Bill of Rights to assemble peacefully, to move about freely, the separation of church and state. You have governments outlawing people’s right to congregate and practice their religion, confiscate property without due process.

California now has emergency regulations that allow them to commandeer private property to set up emergency hospitals, and now there are number of euphemisms such as, social distancing, self-isolation, shelter in place. I thought that’s what your snowflake generation did when they went to their parents’ basement as a safe space. Quarantines, curfews, checkpoints, lockdowns, containment zones. . .what I fear is this will progress to some euphemism for martial law.

Maurice: Truly, truly concerning. Let’s discuss the economic policy response. Are you as surprised on how much emphasis the Fed and Congress has placed on the economy rather than on providing supplies toward the hospitals and the true heroes, who are the healthcare workers making so many selfless sacrifices?

Mickey: I think this is a media- [and] government-created economic recession in response to a medical event. There’s a sayingnever let a good crisis go to wasteand the media and the government have instilled first fear, then panic, then irrationality, now approaching hysteria. That’s not to belittle the impact of the Wuhan flu, but let’s just step back and put this in perspective. So far, I think as of Friday afternoon, March 27, there are approximately 95,000 confirmed cases in the U.S. and around 1,300 deaths, so do the math.

That’s about 1.4%, but that’s from the number of people that tested positive. That does not imply the number of people that have had the virus with no symptoms or mild symptoms; these are the people that are extremely ill to begin with. Here’s some perspective, according to the Centers for Disease Control and Prevention (CDC), as of March 21, for the 20192020 flu season so far, 39 million cases, 400,000 hospitalizations and 24,000 deaths.

I’m a bit of a numbers wonk, and let’s just do a little thought experiment. We have 95,000 cases, but those are people that are ill enough to get tested. Let’s just suppose that those 95,000 cases are even upward of 10x that, with people walking around not even know they have it. They’ve got a cold, because it is a virus very similar to the common cold. If we assume that 10 times that number actually have been exposed and have antibodies to the virus, then that’s 950,000 cases right there.

Then let’s go back and do the math on that. That gives us a mortality rate of about 0.1%, which is just about the average of the common flu season that kills on average 36,000 Americans every year.

Maurice: Now, that’s truly unfortunate for the victims and the families. But, as you stated, if cooler heads prevail and you put it into perspectivebecause the opposite response from all the mainstream media is hysteriaI believe we should be proactive in trying to prevent the spread of the disease. But you stated it correctly: “Never let a good crisis go to waste.”

Mickey: I’m going to say something fairly radical in today’s environment. When it’s all said and done, I think that this is going to be a serious illness, a serious flu. I think we will develop a vaccine for it quicker than usual. In retrospect, we will look back at this and say, well, was it as bad as the swine flu in 20092010? Was it as bad as 86,000 people, if memory serves, killed during that flu season? What’s the ultimate outcome? That remains to be seen, but that’s my position right now, and I’m sticking to it.

Maurice: Let’s focus back on the economic response here. Our currency is being inflated at an unprecedented rate in the past couple of weeks. What are your thoughts on the economic policy response and the potential ramifications?

Mickey: Simply put, I think if the governmentand I include the Federal Reserve as the fourth branch of the United States of America’s governmentcreates $6 trillion on a keyboard to fend off economic recession/depression, which is defined as deflation, then an inflating U.S. dollar must be the result.

Maurice: What ramifications do you foresee on globally on supply and demand of goods and services?

Mickey: We have severe demand destruction. Look at the oil business right now. We have an oil price somewhere between $20 and $25 [per barrel]. It’s about $22 as we speak, and that’s because of demand destruction. We’re producing, on average, 20 million barrels of oil worldwide more than demand, and are simply awash in oil. Carry that on out, and we will be, until supply goes away because of low prices. This demand destruction is going to lead to oversupply and falling prices.

Maurice: That will lead to some buying opportunities, potentially, that we’ll get to later on in this conversation. Let me ask you this, is government rewarding bad behavior and if so, how?

Mickey: Well, you can argue that. Let’s look at this $2 trillion stimulus package, which includes $75 million for the National Endowment for the Arts; $75 million for the Corporation for Progressive Broadcastingwhat I like to refer to it as; $25 million for the Kennedy Center after it was remodeled a couple of years ago at a price of $250 million, so lots of waste there.

Going on with that thought, that bill is rewarding bad behavior because it’s giving $1,200 to every American that earns less than a $100,000 a year. Just going to write them a check or probably deposit in your bank accountI don’t think they write checks anymore for those sorts of things. This has severely affected a portion of people in this country because they’ve never saved.

In addition to a usual state where you’re able to collect unemployment for a period of six months, some portion of that, they’ve extended unemployment benefits at 100% for another four months. In New Mexicoand I’m not sure if other states or notyou don’t even have to look for a job during that period of time. The idea that people who do not accumulate nest-eggs, who are deeply in debt, who live hand-to-mouth, from paycheck to paycheck, they’re certainly going to be adversely affected.

But here comes Uncle Sam, with all these reasons not to work. So someone gets unemployment for six months and they’ve got another four months of unemployment. If they’re minimum wage, what incentive do they have to go back to work?

Maurice: Which leads to my next question, once citizens receive their first stimulus payments for not working, what are the chances of more checks and increased amounts on the horizon by the government?

Mickey: Well, I think everybody has already said in government that this is a startthis $2 trillion plus the $4 trillion the Feds created on a keyboard. There’ll be another bailout package, or there’ll be another stimulus package, or whatever euphemism they choose to call it. It’s not good. The ultimate result of this is we’ll default on our debt once again; we’ve done that twice since 1930.

Maurice: Somewhat counterproductive. You correct me if I’m wrong: If you inflate your currency, the result is higher prices. Well, why are so many people, especially those that advocate for a minimum wage increase, stating that the cost of living is so high, right? There’s your culprit. It’s the Federal Reserve. It’s expansion of our currency.

Mickey: Absolutely.

Maurice: They look at the short term as, I want this paycheck. And now multitrillion-dollar question: Who is going to pay for this; when and how?

Mickey: We ultimately do, as citizens of the United States of America. And I’ve already said this: It’s going to result in a default on the debt, and demise of not only the US dollarthe worlds reserve currency, as this is happening all over the worldultimately, it will result in a demise of all the world’s fiat currencies, and that’s the natural order of things. Every fiat currency since the Roman Empire, and perhaps longer than that, has inflated itself and resulted in default. I just can’t tell you when that’s going to happen.

Maurice: If you, Mickey Fulp, were a member of Congress, what would you recommend as an appropriate economic response?

Mickey: Well, I’m going to call that an inappropriate question because I consider myself an honest and forthright man.

Maurice: I think we can read between the lines on what the response would be, and I would echo that I second that emotion, sir.

Mickey: I think there are a couple of honest politicians: Dr. Ron Paul, when he served in the U.S. Congress and his son, Dr. Rand Paul. Those are honest, forthright men that I admire.

Maurice: Mickey, who is ultimately responsible for the decline and degradation of the United States?

Mickey: It’s the politicians that we, the people, voted in. But most importantly, I think it’s the Deep State bureaucrats who actually run the government. They are entrenched in jobs for their entire careers, and they answer to no one except the ephemeral bosses that are appointed by one set of politicians or the other that we have elected.

Maurice: Switching gears, do you have any buying opportunities at the moment that you would like to share with us?

Mickey: I think it’s not too late to buy gold. That’s assuming you can find someone who is selling gold and delivering it promptly, and that’s a problem right now.

Maurice: Besides gold, are there any other precious metals that would peak your interest at this time or just gold?

Mickey: Just gold for me.

Maurice: Mickey, how does owning physical precious metals fit into today’s discussion?

Mickey: Maurice, I think it’s the key ingredient in any recipe to ensure financial security for you and yours.

Maurice: May I ask what are you buying and why?

Mickey: I’m not buying anything this week because gold is up $140 bucks, and it’s even more than that, with really huge premiums coming in at this point because of its physical scarcity.

Maurice: Just to caveat to what you’re sharing, I had a discussion with Bob Moriarty of 321gold recently. I think he stated: “Anyone who does not own gold is financially ignorant.”

Mickey: I would agree with that take, and specifically gold, because gold is the only real money.

Maurice: In closing, sir, what keeps you up at night that we don’t know about?

Mickey: Right now, I would say it’s the next good novel I’m reading about yet another dystopian society.

Maurice: All right, Mr. Fulp, last question: What did I forget to ask?

Mickey: My website and my Twitter feed: www.mercenarygeologist.com; and my Twitter feed is @mercenarygeo.

Call me directly at (855) 505-1900, or you may e-mail [email protected]. Last but not least, please subscribe to www.provenandprobable.com for mining insights and bullion sales.

Mickey Fulp, the Mercenary Geologist, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Statements and opinions expressed are the opinions of Maurice Jackson and not of Streetwise Reports or its officers. Maurice Jackson is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Maurice Jackson was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us, we were all going direct to Heaven, we were all going direct the other way.” Charles Dickens

When I was in university in Saint Louis, I was once ordered by one of the Jesuit priests to submit a “review” of a book entitled “A Tale of Two Cities” by an author that I later grew to greatly admire, Charles Dickens of “A Christmas Carol” fame.

However, at the time, I had no interest whatsoever in picking up that book and opening its dust-ridden pagesunless, of course, it was shortly after midnight and lacking the sleep-inducing influence of draft beer and pizza, I needed a sedative. As vigorously as I might protest, the cassock-clad professor took me aside and explained in minute detail that this was anything but a “polite request.” Quite the opposite, this was a directive, an edict, an order, and failure to comply would result in a failing grade, a suspension from the varsity hockey team, and total personal humiliation, ignominy and disgrace.

Begrudgingly, I returned to my dormitory, cracked open a Bud, and with a sigh of resignation and gritty resolve, I tore into “A Tale of Two Cities,” an extraordinary novel written in 1859 but one whose opening paragraph (shown at the beginning) could have originated today in the mind of the author, given the surrealism of the events of the last three months. What I had rued as a totally unnecessary and agonizingly dull task turned into a delight, and the book remains one of my favorites of all time.

Watching this gaggle of TV-star politicians around the world scramble to try to halt the inevitable arrival of this economic winter is like watching the mighty Mississippi in the springtime overflow its banks, tossing aside sandbagged defenses as though they were Styrofoam coffee cups. As I opined last weekend, this Kilimanjaro of debt, amassed around the world in staggering size and reach over the past five decades, has now overrun its banks and threatens to flood the economic heartland with defaults, bankruptcies and massive unemployment. Painfully and predictably, the banco-politico elite have turned to their problem-solving toolkit and engaged the only implement they knowthe printing press.

Even more excruciating than listening to these opportunistic counterfeiters is seeing the queue of corporate crybabies, complete with extended hands and pointed fingers, blaming the government-imposed shutdown on the demise of their company stock prices and accompanying destruction of their option-package enrichments. The cruise lines that operate out of tax-friendly Panama bellying up to the bar of taxpayer libation for relief packages is not only an outrage, it is an embarrassment. If the average breadwinner can squirrel away a few acorns for a rainy day or for a winter of frozen ground and lean pickings, why is the corporate world entitled to relief in the trillions and the average worker a month’s rent?

This is not just a Tale of Two Markets (and I’ll get to that in a moment), it is a Tale of Two Societies, the first being “entitled” and the second, “not so much.” After all, did we not just go through a self-inflicted immolation of the banking cartel and subsequent public bailout of same a mere twelve years ago? Did the corporate world not learn any degree of prudence during or since that time? Could that last $1.5 billion stock buyback (into which they exercised options and sold their stock resulting in massive self-enrichment) not have been delayed or avoided, and instead gone into a rainy-day war chest of sorts?

The actions of the US Treasury, Federal Reserve and Congress (and their Canadian and European counterparts) have unleashed the hounds of fiscal and monetary hell upon the world, with the term “moral hazard” standing out like a lighthouse beam at midnight. Sir Winston was so very much on-the-mark with his now-famous quote, “Never let a good crisis go to waste,” to the extent that there now exists an inverse correlation between decibel level of political and corporate wailing and the level of the Dow Jones Industrial Index. And if it weren’t so pathetic, it would be laughable.

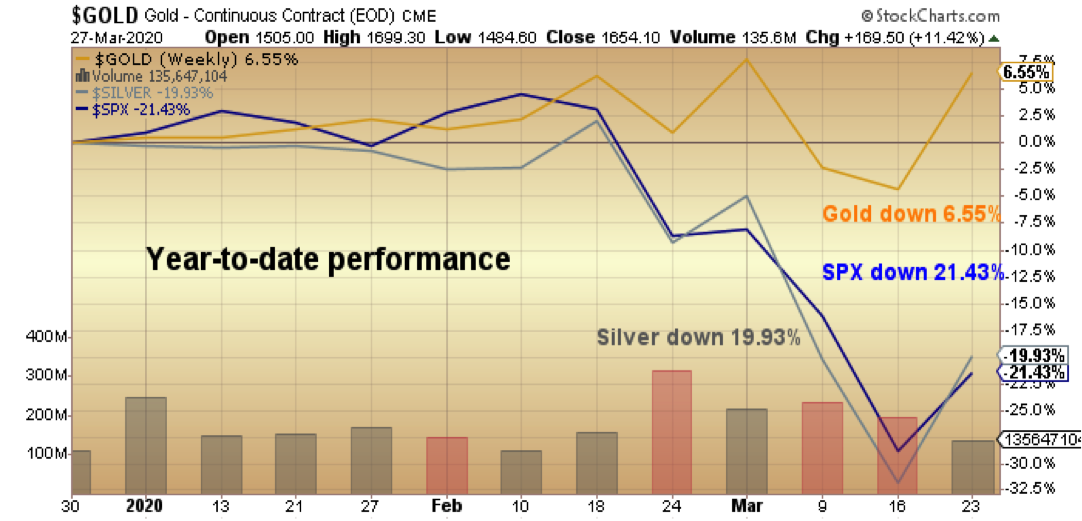

Most markets found their footings last week, with gold, silver and the S&P all staging sharp reversalsbut then again, it was an easy call with the Fear-Greed Index at “1.” Performance year to date has once again placed gold in the “outperformer” category (an event that must be driving White House economic advisor Larry Kudlow absolutely off his rocker). Gold has done exactly what it was supposed to do in times of turmoil, and while silver has not, it is still performing better than the S&P year to date.

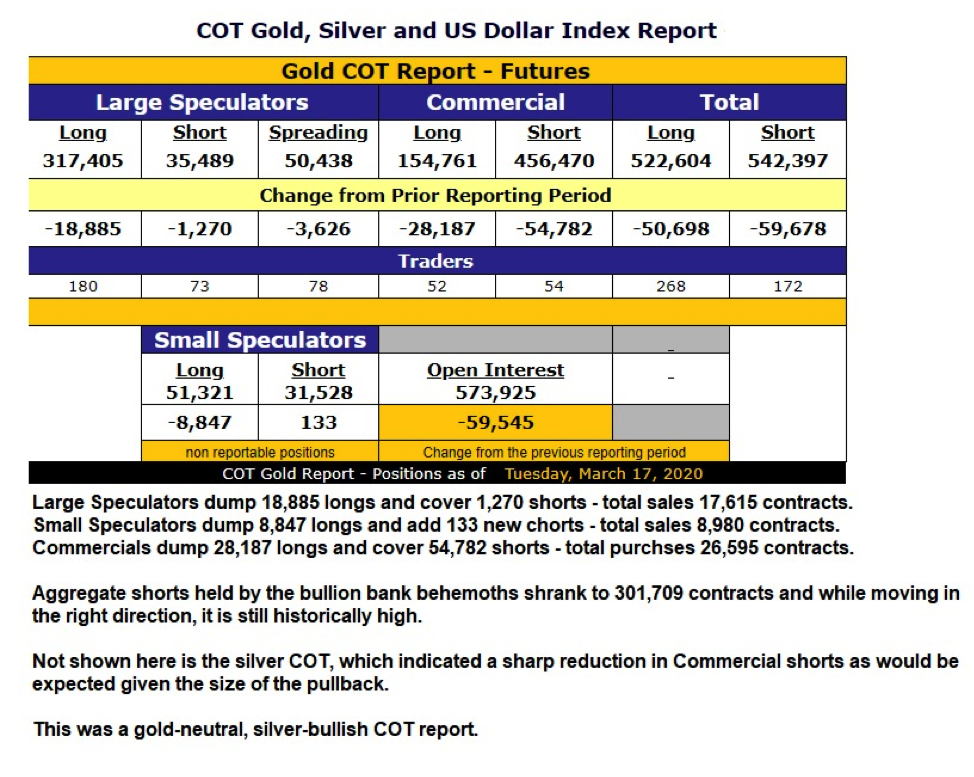

Further, the March 17 COT report has finally tilted in favor of a silver rally, and it couldn’t happen at a more opportune time.

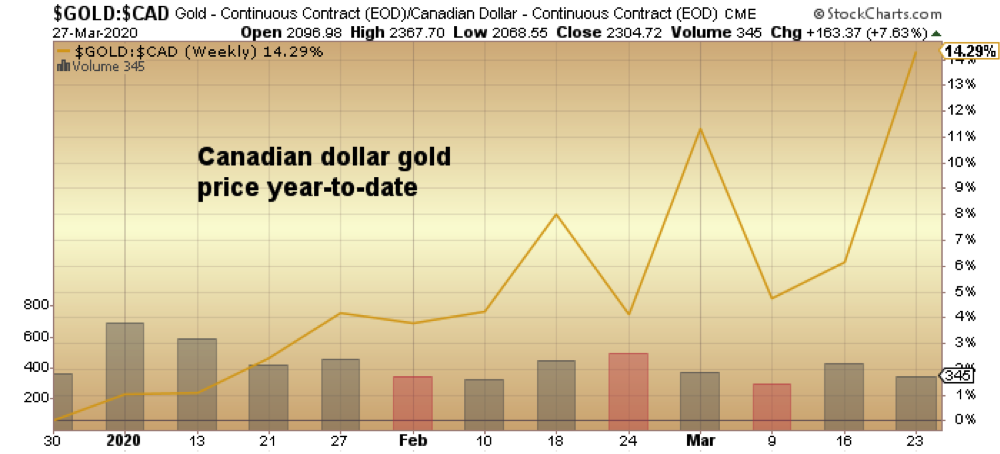

Of even greater significance is the performance of gold in non-US-dollar currencies and no better one to show than the Canadian dollar gold price which, for Canuck investors, has been a veritable nugget of safe-haven alpha for the prescient portfolio manager.

If you are an American investor looking for a currency play, the gold miners whose production is primarily in Canada or Australia (or both) are enjoying the dual benefits of weak domestic currency and weak energy. This allows a huge boost in revenue while expenses drop, and what falls out of the bottom is increased profits, the mother’s milk of all bull markets.

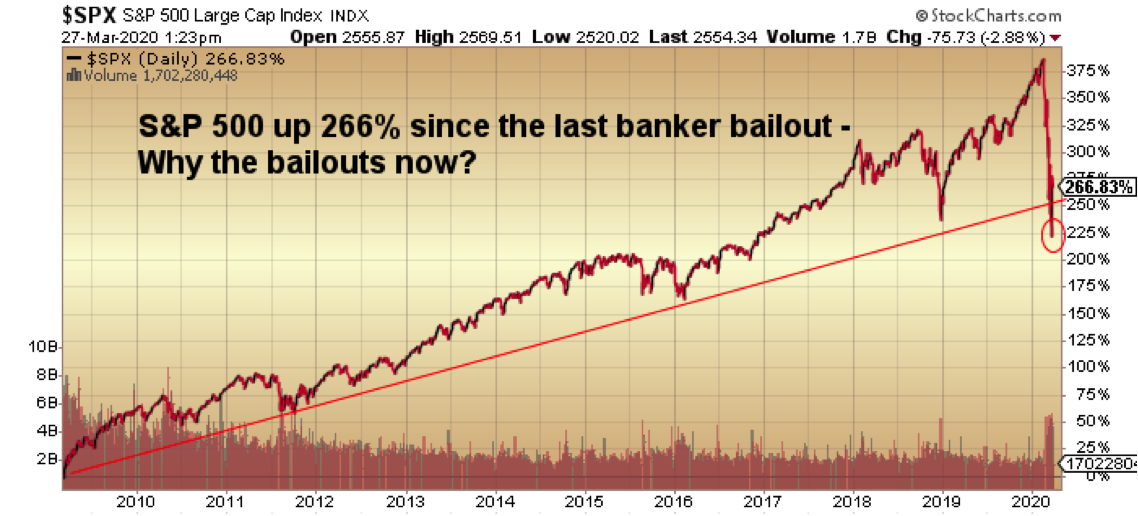

It was two weeks ago that I published the two charts of GDX and GDXJ with the caption “Generational Buying Opportunity.” The lows of that following Monday were textbook bottoms, with those purchases now serving to significantly repair the damage done by the silver takedown, an event I most surely did not expect.

I elected to go “all-in” with the Senior Gold Miner exchange-traded fund (ETF) (GDX:US), not because of any self-congratulatory “analysis” but because I totally missed the March 16 lows in the junior ETF (GDXJ:US), under US$20, because a) I was overly pessimistic about the opening price (I bid $16idiot), and b) I was terrified. Actually, I have learned over the decades that fighting the terror of a knife-catching bottom is, if successful, a 100% winning trade and no better example was the GDXJ that day.

The only problem I have right now with the gold and silver miners is this: Will they, as “stocks” be able to decouple from the algobot-driven attack dogs that are controlling the broad stock market. With gold back in the US$1,600s and with oil around US$21, you could not get a more bullish fundamental backdrop for the gold producers. But as we know, when you are up against a swarm of bid-destroying algos, fundamentals don’t count, and therein lies the conundrum.

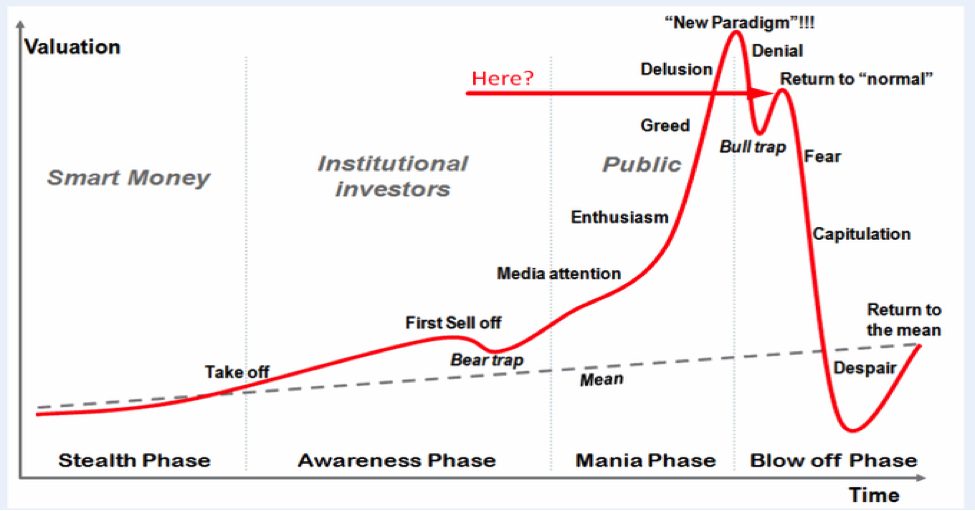

The stock market has bounced, but as I have preached for years, there is always a retest. If one looks back to 20092011, the bailouts occurred three months before the actual bottom, so I post the above chart not to frighten anyone but more as a reminder that the impact of this lockdown upon the global economy might be mild. But it might also be severe, and anyone who makes a prediction on his or her blog is only making a guess, because nobody has a clue, least of all me, as to the outcome.

From the chart shown above, I think that as far as the precious metals and their publicly traded brethren are concerned, we are somewhere between “fear” and “capitulation.” However, will a deflationary wave swamp the golden vessel, or will the hyperinflationary policy moves be a surfer’s dream? Only time will tell.

As for silver, the biggest question that I get from subscribers and followers constantly is why the GSR (gold-to-silver ratio) exploded to 130 when all the rocket scientist “analysts” have pounded the table in abject certainty that silver is in “shortage.” How can something in shortage be allowed to trade at US$14.50 in one market and $24.50 in another? How can retail websites be quoting one-ounce silver buffaloes at US$24.23? That is where the title of today’s missive comes in; this is “a tale of two markets.”