The US dollar strengthened slightly against a basket of major currencies. The dollar index (#DX) closed in the green zone (+0.15%) yesterday. Speech by US President Donald Trump in the American Congress addressing the nation supported the US currency. He said about the “incredible results” of the economic policies of his administration and the excellent prospects for the US economy. During the speech, he painted an encouraging picture of his presidency in the hope of convincing the Americans to give him another chance in the November 3, 2020 election.

The Chinese yuan has been growing after the World Health Organization (WHO) confirmed that coronavirus could be localized. The death toll in mainland China increased to 490, and the number of confirmed cases rose to 24,324. However, despite the increase in deaths, WHO is confident that the spread of the virus can be stopped, as 99% of infections so far are attributed to China. These reports have weakened the demand for safe assets.

The “black gold” prices have been growing after a protracted fall. Currently, futures for the WTI crude oil are testing the $50.80 mark per barrel. At 17:30 (GMT+2:00), US crude oil inventories will be published.

Market Indicators

Yesterday, there was the bullish sentiment in the US stock market: #SPY (+1.52%), #DIA (+1.43%), #QQQ (+2.29%).

The 10-year US government bonds yield has been growing. At the moment, the indicator is at the level of 1.62-1.63%.

The Economic News Feed for 05.02.2020:

– UK composite PMI at 11:30 (GMT+2:00);

– UK services PMI at 11:30 (GMT+2:00);

– ADP nonfarm employment change in the US at 15:15 (GMT+2:00);

The technical picture on the EUR/USD currency pair is ambiguous. At the moment the trading instrument is being consolidated. Investors are waiting for additional drivers. The local support and resistance levels are 1.10300 и 1.10500, respectively. Today, participants in financial markets will assess important economic releases from the United States. We recommend opening positions from key levels.

The Economic News Feed for 05.02.2020:

– Composite business activity index from Markit (EU) – 11:00 (GMT+2:00);

– Retail sales volume (EU) – 12:00 (GMT+2:00);

– Change in the employment numbers in the non-agricultural sector from ADP (US) – 15:15 (GMT+2:00);

– ISM’s supply manager index for the non-agricultural sector (US) – 17:00 (GMT+2:00);

The indicators do not give an accurate signal: 50 MA started crossing 100 MA.

MACD is in the negative zone, which indicates a bearish sentiment.

The Stochastic Oscillator is in the oversold area, the %K line is above the %D line, which gives a signal to buy EUR/USD.

Trading recommendations

Support levels: 1.10300, 1.10100, 1.09900

Resistance levels: 1.10500, 1.10650, 1.10950

If the price fixes above 1.10500, EUR/USD quotes are expected to rise to 1.10700-1.10900.

Alternatively, the quotes could descend toward EUR/USD currency pair to 1.10100-1.09900.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.29894

Open: 1.30316

% chg. over the last day: -0.27

Day’s range: 1.30088 – 1.30379

52 wk range: 1.1959 – 1.3516

GBP/USD quotes have retreated from local lows. At the moment the technical pattern is ambiguous. Sterling tests local support and resistance levels: 1.30050 and 1.30450, respectively. The trading instrument has potential for further recovery. Investors are waiting for important economic releases from UK. We also recommend you to pay attention to the news background on the US economy. Positions should be opened from key levels.

The UK news feed is calm.

Indicators do not give accurate signals: the price consolidates near 50 MA.

MACD is near the 0 mark.

The Stochastic Oscillator is located in the neutral zone, the %K line is above the %D line, indicating a correction in GBP/USD quotes.

Trading recommendations

Support levels: 1.30050, 1.29800, 1.29450

Resistance levels: 1.30450, 1.30850, 1.31100

If the price fixes below 1.30050, you should consider selling GBP/USD.

Alternatively, the quotes could grow toward 1.30800-1.31000.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.32869

Open: 1.32765

% chg. over the last day: -0.02

Day’s range: 1.32758 – 1.32981

52 wk range: 1.2949 – 1.3566

USD/CAD currency pair has stabilized after a long rally. At the moment, the CAD is in sideways motion. The local support and resistance levels are: 1.32650 and 1.33000, respectively. Technical correction is not ruled out in the nearest future. Today we recommend you to pay attention to the dynamics of oil quotations, as well as to economic releases from the United States. Positions should be opened from key levels.

The Economic News Feed for 05.02.2020:

– Trade balance (CAD) – 15:30 (GMT+2:00)

The indicators signal the strength of buyers: the price has fixed above 50 MA and 100 MA.

Histogram of MACD is in the positive zone, which indicates a bullish sentiment.

The Stochastic Oscillator is located near the overbought zone, the %K line is above the %D line, which indicates that the price is above 50 MA and 100 MA.

Trading recommendations

Support levels: 1.32650, 1.32450, 1.32200

Resistance levels: 1.33000, 1.33400

If the price fixes above 1.33000, expect further growth toward 1.33300-1.33500.

Alternatively, the quotes could correct toward 1.32300-1.32100.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 108.687

Open: 109.515

% chg. over the last day: +0.69

Day’s range: 109.317 – 109.516

52 wk range: 104.45 – 113.53

Yesterday aggressive purchases were observed on USD/JPY currency pair. The growth of quotations exceeded 80 points. The trading instrument has set new local maximums. Demand for currencies save haven currencies has shrunk as investors have been encouraged by the Chinese government’s measures to to contain the coronavirus and limit its economic impact. At the moment, the USD/JPY currency pair is consolidating in the range 109.250-109.550. We do not rule out further weakening of the yen against USD. Positions should be opened from of key levels.

The news background on the Japanese economy is quite calm.

The indicators signal the strength of buyers: the price has fixed above 50 MA and 100 MA.

The MACD histogram is in the positive zone but below the signal line. It’s a weak signal to buy USD/JPY.

The Stochastic Oscillator is located in the neutral zone, the line %K is below the line %D, which indicates a bearish sentiment.

Trading recommendations

Support levels: 109.250, 109.100, 108.800

Resistance levels: 109.550, 109.750, 110.000

If the price fixes above 109.550, expect further growth of USD/JPY quotes toward 110.000.

Alternatively, the USD/JPY pair may decline to 109.000-108.800.

Gold showed a clear bullish tendency over the last week of trading, with clear attention being on the region around 1,555 USD, around 2019’s yearly highs.

The main driver certainly came from the latest news and developments concerning the Coronavirus, which resulted in a risk-off mode, driving US yields lower and thus Gold higher.

While the main question is how long these risk-off tendencies will last (based on a 2017 paper, economists calculated that the expected annual losses from pandemic risk could amount to ‘only’ about $500 billion (ca. 0.6% of global income) per year)), Gold still has other, still bullish drivers.

After the Fed rate decision didn’t deliver anything new last Wednesday, pressure on US yields diminished a little after ISM Manufacturing data jumped to 50.9 in January of 2020 from 47.8 in December, beating market forecasts of 48.5 and pointing to the first increase in factory activity in six months.

Still, the question is if today’s ADP Employment data set and ISM Non-Manufacturing can show similar tendencies. If they don’t and they come in below expectations, a drop in 10-year US Treasury yields below 1.5% could follow, levelling the path up to 1,600 USD in Gold again.

Such a push higher is also favoured from a technical perspective as long as we trade above 1,440/450 USD. The potential next target on the upside can then be found in the region around 1,650/700 USD.

A drop back below 1,550 USD would be short-term bearish, activating the region around 1,510/515 USD:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between November 2, 2018, to February 4, 2020). Accessed: February 4, 2020, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

“On a long enough timeline, the survival rate for everyone [and everything] drops to zero.”

For better or for worse, that grim and almost cynical quote by the charismatic anarchist Tyler Durden of Fight Club is set to one day become an existential crisis for the non-renewable energy sector.

The jury is still out regarding how close we are to hitting Peak Oil or even whether abiotic oil is a real thing.

Granted, the sun and other renewable sources will someday share the same fate as their more ephemeral cousins and succumb to the second law of thermodynamics–only that we are talking about some seriously dizzying timelines measured in the billions, not tens or hundreds of years–hence the distinction.

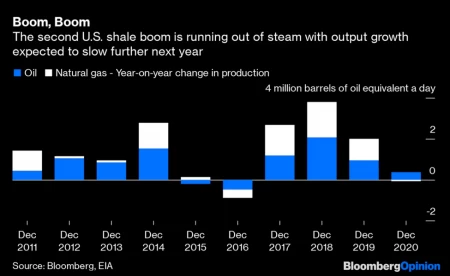

For the US shale industry, the future hangs in the balance. It’s now official: after a phenomenal decade-long run that has propelled the United States to the top of the oil producers’ league, America’s second shale boom is running out of gas.

According to the US Energy Information Administration, drilling in the Permian–easily the most prolific of the shale basins–declined 11% in the nine months to August. Output growth over the next year is expected to clock in at just 370,000 barrels a day–the slowest clip in four years. With oil prices remaining stubbornly low and no respite in sight, drillers in the shale patch are struggling and rig count has seen a steady decline.

The only thing supporting growth is a ‘fracklog’ of drilled but uncompleted (DUC) wells that are now coming online as shale producers like Apache Corp. focus more on well completion and less drilling under squeezed budgets.

The situation could get a lot more dire for the industry if Democratic presidential front-runners senators Bernie Sanders and Elizabeth Warren have their way and ban fracking after ascending to the Oval Office.

That’s decidedly gloomy.

But what’s the outlook for other parts of the globe?

Texas-based Permian and Eagle Ford might boast the most street cred of any shale plays, anywhere on the planet.

However, there are other regions that are pretty well endowed. Not only are they ready and willing to seize the moment, but they’re positioned to be the next major shale boom venues.

#1 Argentina’s Vaca Muerta

Vaca Muerta might mean ‘dead cow’ in Spanish; however, Argentina’s prized gem might soon become one of its leading cash cows instead.

Located on an arid steppe nestled against the Andes mountains along the western edge of Patagonia, Vaca Muerta is a continuous tight oil and shale gas reservoir that’s reputed to be one of the largest of its kind. The 30,000 square kilometers (12,000 sq mi.) patch of land consisting of lime mudstones, black shale and marl and is estimated to hold approximately 16.2 billion barrels of oil and 308 trillion cubic feet of natural gas as per the EIA. The shale is found at a depth of about 9,500 feet (2,900 m).

In comparison, the Permian Shale contains 20 billion barrels of oil and 16 Tcf of associated natural gas.

Unfortunately, Vaca Muerta has little to show for its vast riches with proper production yet to commence a century since oil was first discovered there by American geologist Charles E. Weaver–thanks to the region’s checkered history.

Over the past eight years, Chevron and YPF SA, the local oil giant, Royal Dutch Shell and Total have sunk between them $13 billion into exploration into this unconventional play. No company though had much to show for its efforts with obstacles popping up everywhere and production marginal.

That’s until this year when two companies managed to export light oil and liquefied natural gas in what the country’s officials said foreshadows a steady flow of shipments by year-end. Unfortunately, that too looks unlikely after the Argentina Energy Secretariat once again extended the deadline for bidding for a project to build a 1,000 km pipeline to carry gas from the giant formation.

With the Argentinian economy so weak, it could be years or maybe even decades before Vaca Muerta can rival US Permian Shale but make no mistake about it, the country appears dead-set at making this a reality. And Chevron, Shell and Total are likely to see their massive investments begin to pay off when it the region begins to turn around.

#2 Kavango Basin, Namibia

And if Karoo is a shale windfall, Kavango is its likely extension, according to geologists.

The Kavango Basin has the same Karoo geology, and it’s also been shown to have the same depositional environment as Shell’s Whitehill Permian shale play, part of the Karoo Supergroup in South Africa.

The 6.3-million-acre (25,000 square kilometers) Kavango Basin is similar in size to the Eagle Ford basin.

And right now, a 90% interest in the exploration license for the entire basin is owned by one small-cap explorer: Recon Energy Africa (TSX.V: RECO, OTCMKTS:LGDOF), with a market cap of only $40 million and shares selling for under $0.80.

It’s pretty unique for a company this small to have a basin this big, but while few have heard of the company, everyone in the business has heard of the geophysicist who examined the data on this basin. They’ve also heard of Recon’s CEO, Jay Park QC—the former director of Caracal Energy, which was acquired by giant Glencore in 2014 for $1.3 billion.

Bill Cathey is the geophysicist to some majors. When Recon brought the magnetic survey data from Namibia’s Kavango Basin to Cathey, Cathey said the data showed a 30,000-foot sedimentary basin. He also said that a basin this deep, everywhere else in the world, produces commercial hydrocarbons. Management of Recon dropped everything, so the story goes, got on a plane, and finalized the deal for an exploration permit for the petroleum and natural gas rights to the giant Kavango Basin.

So, now, tiny Recon (TSX.V: RECO, OTCMKTS:LGDOF) is sitting on a basin that’s the same size as the Eagle Ford.

Recon has a 4-year exploration license leading to a 25-year production license starting when it has made a commercial discovery.

Sproule–a tier 1 resource assessment company–estimated that Kavango has a potential 12 billion barrels of oil or 119 trillion cubic feet of natural gas. That’s for the shale and doesn’t count any conventional potential.

The first test wells are slated to be drilled in Q2 2020.

That’s just a few months away.

Namibia is one of the most oil-friendly up-and-coming oil venues in the frontier of Africa. Ask Shell, or Exxon, both of whom are acquiring assets there.

Shell (NYSE:RDS.A), for its part, is a veteran in the African oil and gas game. The company began drilling in the region in the 1950s, and now has assets in over 20 countries across the continent. Though it has sold off a number of assets in the region in recent years due to unfavorable regimes, it continues to maintain a strong presence in South Africa and Namibia.

Exxon (NYSE:XOM), on the other hand, is relatively new, but quickly upping its stake. The company has already added over 7 million acres in four additional deepwater blocks just this year. What Exxon’s banking on is that Namibia, which according to theory once fit together with Brazil, shares the same geology as Brazil’s pre-salt basins, Santos and Campos, which have already proved resource-rich, according to Deloitte.

Whether it’s Namibia, Argentina or South Africa, what we do know is that the U.S. has already had its shale boom, and the next multi-million-dollar oil play is probably going to come from somewhere else.

#3 Karoo, South Africa

The Karoo is a vast sedimentary basin covering more than 600,000 square kilometers in central and southern South Africa.

Although the sheep- and ostrich-dotted expanse is better known for its arid beauty and aching poverty, it could hold untold riches underneath the surface in the form of natural gas. Former South African governments placed restrictions that made Karoo out of reach for foreign companies. However, President Zuma’s government lifted the shale fracking ban in 2012 thus opening up 485 Tcf of gas reserves for drilling.

If the EIA estimates are accurate, the Karoo shale gas fields would qualify as the fifth largest in the world. The gas extracted could power the entire country for a good 400 years and create thousands of much-needed jobs.

The South African Journal of Science has, however, disputed the EIA reserve estimates saying that actual shale gas deposits are only 13 Tcf thus ranking the country 34th out of 46 nations in EIA estimates.

Although local farmers and environmentalists are opposed to any fracking activity in Karoo, three foreign companies-Falcon Oil, Royal Dutch Shell and Sunset Energy–have already been granted licenses to explore for gas in the basin.

Bonus: Big Oil Diving Into Uncharted Waters

Though there are a number of exciting hotspots popping up across the globe, it’s also important to pay attention to oil companies taking big risks on little-known exploratory projects.

Take Total (TOT), for example. It recently announced a major oil discovery offshore Suriname with its partner, Apache (APA). Apache’s agreement with Total included $100 million upfront payment and expenses incurred in exploration. The find was a major boon for both Total and Apache, especially considering there had not previously made any commercially viable oil discoveries. The find is doubly beneficial for Suriname, which could be a significant turning point for the small country’s economy.

Though it’s not entirely off the beaten path, Egypt has also captured the attention of Big Oil in recent years. Just last month, in fact, the country awarded Chevron (NYSE:CVX) and Shell key exploration blocks in the red-hot Red Sea. The blocks cover a total area of around 10,000 sq km and carry combined minimum investment of $326 million, Egypt’s petroleum ministry said, adding that potential investment would rise to “several billion dollars” if discoveries were made.

By. Joao Piexe

**IMPORTANT! BY READING OUR CONTENT YOU EXPLICITLY AGREE TO THE FOLLOWING. PLEASE READ CAREFULLY**

Forward-Looking Statements. Statements contained in this document that are not historical facts are forward-looking statements that involve various risks and uncertainty affecting the business of Recon. All estimates and statements with respect to Recon’s operations, its plans and projections, oil prices, recoverable oil, production targets, production and other operating costs and likelihood of oil recoverability are forward-looking statements under applicable securities laws and necessarily involve risks and uncertainties including, without limitation: risks associated with oil and gas exploration, development, exploitation and production, geological risks, marketing and transportation, availability of adequate funding, volatility of commodity prices, imprecision of reserve and resource estimates, environmental risks, competition from other producers, government regulation, dates of commencement of production and changes in the regulatory and taxation environment. Actual results may vary materially from the information provided in this document, and there is no representation that the actual results realized in the future will be the same in whole or in part as those presented herein. Other factors that could cause actual results to differ from those contained in the forward-looking statements are also set forth in filings that Recon and its technical analysts have made, We undertake no obligation, except as otherwise required by law, to update these forward-looking statements except as required by law.

Exploration for hydrocarbons is a speculative venture necessarily involving substantial risk. Recon’s future success will depend on its ability to develop its current properties and on its ability to discover resources that are capable of commercial production. However, there is no assurance that Recon’s future exploration and development efforts will result in the discovery or development of commercial accumulations of oil and natural gas. In addition, even if hydrocarbons are discovered, the costs of extracting and delivering the hydrocarbons to market and variations in the market price may render uneconomic any discovered deposit. Geological conditions are variable and unpredictable. Even if production is commenced from a well, the quantity of hydrocarbons produced inevitably will decline over time, and production may be adversely affected or may have to be terminated altogether if Recon encounters unforeseen geological conditions. Adverse climatic conditions at such properties may also hinder Recon’s ability to carry on exploration or production activities continuously throughout any given year.

DISCLAIMERS

ADVERTISEMENT. This communication is not a recommendation to buy or sell securities. Oilprice.com, Advanced Media Solutions Ltd, and their owners, managers, employees, and assigns (collectively “the Company”) may in the future be paid by Recon to disseminate future communications if this communication proves effective. In this case the Company has not been paid for this article. But the potential for future compensation is a major conflict with our ability to be unbiased, more specifically:

This communication is for entertainment purposes only. Never invest purely based on our communication. We have not been compensated but may in the future be compensated to conduct investor awareness advertising and marketing for TSXV:RECO. Therefore, this communication should be viewed as a commercial advertisement only. We have not investigated the background of the company. Frequently companies profiled in our alerts experience a large increase in volume and share price during the course of investor awareness marketing, which often end as soon as the investor awareness marketing ceases. The information in our communications and on our website has not been independently verified and is not guaranteed to be correct.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares of this featured company and therefore has an additional incentive to see the featured company’s stock perform well. The owner of Oilprice.com will not notify the market when it decides to buy more or sell shares of this issuer in the market. The owner of Oilprice.com will be buying and selling shares of this issuer for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

NOT AN INVESTMENT ADVISOR. The Company is not registered or licensed by any governing body in any jurisdiction to give investing advice or provide investment recommendations. ALWAYS DO YOUR OWN RESEARCH and consult with a licensed investment professional before making an investment. This communication should not be used as a basis for making any investment.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Investing is inherently risky. Don’t trade with money you can’t afford to lose. This is neither a solicitation nor an offer to Buy/Sell securities. No representation is being made that any account will or is likely to achieve profits similar to those discussed.

Later tonight we will be getting the most important data release of the week for NZD. This is probably the only chance the currency has to revert its current trend!

However, expectations are that the labor market hasn’t improved significantly since the last measure. Consequently, this won’t change the outlook for the RBNZ’s next meeting.

New Zealand publishes its employment figures only once per quarter. That makes them both more anticipated by the market, as well as behind the times.

A lot has changed in the world of finance since the job measurements were taken. Chief among these changes is that the US and China finally signed a trade agreement. There’s also the unfortunate spread of the coronavirus.

The data we get might be a bit out of step from other fundamentals. However, it is still relevant to consider in terms of the RBNZ’s dual mandate.

What We Are Looking For

The consensus among economists is that the fourth quarter will, broadly speaking, repeat the less than stellar third quarter. The bit of data that usually captures the market’s attention, Employment Change, is expected to grow by 0.3% compared to 0.2% in the prior quarter (note that is within the rounding margin.)

Despite holding the line, that would still be relatively poor performance, since typically Q3 is when New Zealand has the worst jobs data of the year. And, in the final quarter, it’s already supposed to start to improve as tourism grows.

The employment rate is projected to stay at 4.2%, which is apparently within the comfort zone for the RBNZ. Expectations are for labor costs to slow just slightly to 0.5% growth from 0.6% in the prior quarter.

Going Forward

The thing that worries most analysts with regard to New Zealand’s jobs market is what’s already dominating world news: the spread of the coronavirus. This is likely to have a two-fold impact on the Kiwis.

The most immediate is the travel prohibition to New Zealand from China, which is the largest group of tourist arrivals. Many Chinese tourists travel not just to visit, but also for shopping. So, retail sales are expected to be impacted until the disease is contained and travel conditions normalize.

It’s the Kiwis’ turn

The second effect is on the country’s largest trade partner, which could mean this time around New Zealand will be more affected than Australia.

The outbreak has closed stores and considerably discouraged people from shopping. This has affected consumer demand all across China.

New Zealand primarily exports consumer goods such as dairy and seafood to China. And it’s generally at the higher end of the price range!

While this helped New Zealand to weather the effects of the tariff war, affecting Australia more, this time it could be that the roles have reversed with implications for AUDNZD.

We won’t get another batch of employment data until the important summer season is already over. The RBNZ could turn to other proxy measurements if they try to head off potential fallout in the jobs market.

So far, though, it seems that it’s very unlikely the central bank will cut rates when it meets next week.

The US dollar reversed losses on Monday after the Institute for Supply Management’s PMI report on manufacturing beat estimates.

Not only did the data outperform forecasts of 48.5, but it also rose to 50.9. A reading above the 50-level on the index indicates expansion.

The data for January puts an end to nearly five months of contraction in the sector. ISM prices paid also rose to 53.3, beating estimates of 52.0.

Eurozone Final Manufacturing PMI Stays Flat

The final manufacturing PMI figures for the eurozone saw a meager 0.1 point increase in January. Data from IHS Markit showed that the PMI in the manufacturing sector rose from 47.8 to 47.9.

Despite the small increase, the manufacturing sector remains in contraction.

Regionally, Germany’s manufacturing sector was also weaker, with only the French manufacturing PMI staying afloat the 50-level on the index.

EURUSD Pares Gains from Last Week

The currency pair slipped sharply in the early trading session on Monday. Failing to capitalize on the gains after closing at 1.1095, the common currency gave up the gains easily.

The EURUSD is trading below the 1.1072 level. If resistance forms here, we expect the downside momentum to build up.

Sterling Under Pressure After PM Johnson Hits Back on EU

The pound sterling came under strong selling pressure on Monday, just two days after it formally left the EU. PM Johnson said that he will not accept the EU standards in return for an EU trade deal.

The remarks once again heightened the odds of a no-deal Brexit. Both the EU and the UK have until the end of the year to negotiate on various aspects including trade.

GBPUSD Moves Back into the Range

The currency pair fell after reaching a one-month high into last Friday’s close. Price action is in a steady decline since the start of Monday’s trading session. As a result, GBPUSD is back inside the range of 1.3100 and 1.2960.

There is scope for prices to slip to the lower end of the range in the near term.

Crude Oil Drops Over 2% on Lower Demand

Crude oil prices fell sharply on Monday as price nears the $50.00 level. The declines came as the impact of the Coronavirus outbreak intensifies.

China’s demand for crude oil is forecast to fall by 20%, leading the way to a slump in oil prices. Saudi Arabia is reportedly mulling over the option to cut oil production in response.

WTI Crude Oil Could Stabilize at $50

The steady declines in crude oil prices could halt once it hits the psychological level of $50.00 a barrel. We expect price action to stabilize a bit.

In terms of a correction, the falling trend line will need to be broken to confirm any upside in prices. With the key price level of $51.00, oil prices could face resistance on any rebound.

The US dollar has been higher again today, extending yesterday’s gains seen in response to stronger US data. The ISM manufacturing number was seen at 50.9 in January, moving back into expansionary territory for the first time in six months. The data reflects a higher degree of optimism among the factory sector following the signing of the US/China trade deal. However, it doesn’t account for the recent downside impact from the coronavirus outbreak which has yet to be determined. USD index trades 97.73 last.

EURUSD Holds Steady

EURUSD has been a little firmer today, despite the strength in USD. Price has recovered off yesterday’s 1.1035 lows to trade 1.1055 last, heading back up towards the 1.1072 level resistance. A quiet data-sheet means that flows are likely to be muted today though any USD action could offer volatility.

GBP Shaky Over Brexit Talks

GBPUSD had been weaker initially today, trading below the 1.2978 level support, though price is now trading back above the level following a recovery rally. There are fears over the likelihood of the UK and the EU agreeing to a trade deal in the current timeframe. This is given the clashing statements delivered this week. Yesterday, UK manufacturing data showed the sector having recovered to the neutral 50-mark last month. GBPUSD trades 1.2988 last.

Risk Appetite Improves

Risk assets have had a much better day today. Despite news of the coronavirus outbreak worsening (over 20,000 confirmed cases in China, death toll 400+, second death confirmed outside of China) risk appetite appears to be improving. Better manufacturing data from the UK and US is helping boost confidence with the SPX500 trading back up to 3283.18 last, just shy of the 3285.55 level.

JPY & Gold Lower

Safe havens have been weaker today In light of the recovery in equities prices which has seen both JPY and gold lower against the US dollar. XAUUSD trades 1567.16 last, heading back down towards the 1554.69 level. USDJPY trades 109.06 last, as the rally off the rising trend line support continues.

Crude Rallies Again

Oil prices have posted a recovery today also, in light of the better tone to risk markets generally. Following a move below the 50.65 level yesterday, crude is now trading 51.11 last. Later today traders will receive the API inventories report ahead of tomorrow’s headline EIA release.

Loonie Capped At 1.33

USDCAD has been weaker today. Price rallied as high as the 1.33 level yesterday, briefly piercing above, before reversing back beneath as the rally in crude prices helped lift CAD. While below here, there is a risk of a further drop lower to the 1.3207 level, though such a move would require a much larger correction higher in crude.

RBA Holds Rates Steady

AUDUSD has weakened a little today, giving back some of the gains made overnight in response to the RBA meeting. The RBA kept rates on hold, which came as a surprise to some players who ere expecting a rate cut in light of the economic damage caused by the bushfires recently. The RBA cited strength in labor conditions and the property market as supporting factors though highlighted risks from the downturn in China. AUDUSD trades .6711 last.

The US dollar exploded higher yesterday in response to yet another domestic beat. The latest ISM Manufacturing PMI showed that the US manufacturing sector posted its first expansion in six months over last month.

Manufacturing Well Above Expectations

Jumping to 50.9 in January from four-year lows of 47.8 over the last month of 2019, the increase in the manufacturing sector was the biggest monthly gain since 2013. Notably, the gain was also well above the 48.5 figure projected. This meant that the recovery in manufacturing occurred at a far quicker pace than most players were anticipating.

New Orders Jumped

The breakdown of the data was particularly encouraging with the new orders component surging to an eight-month high of 52. Production was also up by just shy of 10%. This is its biggest gain in over six years. The data has been a big boost for US bulls and reflects the level of optimism that kicked in as a result of the US/China trade deal. The deal was signed at the beginning of the month.

US/China Trade Deal Boosts Sentiment

Following tense negotiations last year, the two leading economies were able to finally sign off on the phase-one trade deal first agreed in October 2019. The deal broadly comprises of the US agreeing to reduce and, in some cases, remove tariffs on Chinese goods. China has agreed to greatly increase its purchase of US goods.

The US/China trade war has ravaged global manufacturing over the last two years with manufacturing sectors in the US, UK, and Europe all heavily weakened by the drop in trade. These latest US figures are highly encouraging that the factory sector can start to recover quickly.

Coronavirus Poses Risks

However, while the data is promising, recent developments bare considering. The outbreak of coronavirus over the last few weeks is not accounted for in the data. As the spread of the virus is worsening (with the death toll rising), there is a risk that this could prove to be a temporary rebound in manufacturing activity. Global asset markets have been lower over recent weeks. This comes as a result of rising uncertainty linked to the virus’ spread. Traders will now be eagerly awaiting the next manufacturing data to see if the rebound was able to withstand this uncertainty or if the factory sector has once again fallen into negative territory.

Technical Perspective

The USD index is fighting to hold above the bearish channel broken last week. The retest of the 97.42 level found support, though the move remains shallow for now. If price can hold above here, the focus will turn back to the 98.25 level next as the main upside objective. However, any deeper move lower will put the focus on the 96.37 level support next.

As we can see in the H4 chart, after completing another growth and forming Shooting Star pattern, the pair is reversing. The current situation implies that USDCAD may form a slight correction and then resume growing towards 1.3373. At the same time, one shouldn’t exclude an opposite scenario, according to which the instrument may start a new decline to reach 1.3160 to continue forming the ascending channel.

AUDUSD, “Australian Dollar vs US Dollar”

As we can see in the H4 chart, the pair is trading sideways; it has formed several reversal patterns, such as Hammer, not far from the channel’s downside border. Right now, AUDUSD is starting to reverse; the upside target may be at 0.6801. However, we shouldn’t ignore an alternative scenario, which implies that the instrument may continue falling towards 0.6670 without reversing and forming another rising wave.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

The Institute of Supply Management (ISM) will be releasing the monthly non-manufacturing PMI report for January today. The report marks the performance of the US services sector in the first month of the year.

Economists forecast that manufacturing activity, as measured by ISM will rise slightly to 55.1. This marks a modest increase from 55.1 in December 2019.

The US services sector has managed to buck the trend so far, unlike the performance in the manufacturing sector. Thus, it is somewhat safe to say that the services sector still remains robust.

Another fact that substantiates this view is the payrolls report for December. The services sector was the biggest driver of jobs which even offset a fall in the net job gains from the manufacturing sector.

So far, the services sector has been bucking the trend. Due to the US and China trade dispute last year, manufacturing was hit hard.

But besides the trade spat, the global economic landscape also turned weaker, as a result of the US going after its trading partners to lower tariffs. After the US economy enjoyed one of the longest patches of expansion since the 2008 global financial crisis, investors are concerned about a downturn in the economic cycle.

The overall result, including the impact of the slowdown in the manufacturing sector, was felt in the fourth quarter advance GDP report.

The US economy maintained a quarterly growth rate of 2.1% for the three months ending December 2019. This was in line with the estimates, albeit economists forecast a much bigger slowdown.

So far, the US economy remains somewhat resilient. Still, with the business cycle heading into the late growth phase, the prospect of strong numbers in the manufacturing sector is a thing of the past.

US Non-Manufacturing PMI to Remain Comparatively Stable

On the optimistic side, economists are hopeful that the current sluggish growth in the non-manufacturing sector is only temporary. But there are no signs of this just yet. In December, the services PMI was higher, despite factory orders falling during the same period. The rebound was largely due to an increase in sales and production.

Besides the ISM’s report, IHS Markit will also be releasing its own PMI data on non-manufacturing.

In recent months, both these measures of the services sector have been somewhat consistent. This is contrary to the reports on the manufacturing where both Markit and ISM’s numbers have been diverging.

Preliminary data from IHS Markit shows that non-manufacturing growth is easing. The flash services PMI suggests that the services sector in the US fell from 52.4 in December to 51.7 in January.

There is scope for the data to beat estimates. This comes as, during the month of January, the US and China signed the phase one deal, soothing concerns. Although the larger issues still remain to be sorted, the impact of the decision could be boosting the services sector.

Besides the global theme, the services sector could feel the pressure of the outbreak from the coronavirus. The hospitality and travel services could see a bit of a slowdown with travel bans being considered amid a host of other measures.

With the manufacturing sector in a slump, the focus will shift to the services sector to do the heavy lifting. Therefore, a weaker than forecast print could see a negative reaction from the markets.

While it is still too early to speculate on the performance of the US economy in the first quarter of the month, today’s non-manufacturing PMI will certainly set the stage for the expectations on growth during the current quarter.