Investor fears over Italy’s political turmoil eased on Wednesday, leading to a sharp recovery in Italian assets, the Euro and global equities. Investor confidence that Italy will manage to overcome the current political deadlock was reflected in a bonds auction, where the government managed to sell five and ten-year debt with a bid-to-cover ratio of 1.53 and 1.48, respectively. Confidence returned after Italy’s Prime Minister-designate, Carlo Cottarelli, said yesterday that “new possibilities for the birth of a political government have emerged”, suggesting that a snap election may be avoided.

The Euro rallied more than 1.4% against the Dollar from a 10-month low of 1.1506, its strongest daily performance since January. Also helping the Euro was the German jobs data report, which showed that unemployment fell to a new record low of 5.2% in May.

Given that political tensions in Italy have eased to some extent the focus will return to fundamentals, and today’s preliminary Eurozone May CPI data release will be of great importance for the ECB’s next meeting. A better than expected reading will support proposals for ending quantitative easing and beginning the normalization process.

Relieved about Italy? Let’s get the trade war back on

U.S. Commerce Secretary, Wilbur Ross, seems to have rejected Europe’s requests for a permanent exemption from metal tariffs, suggesting that tariffs on imports of European steel and aluminum will commence on June 1. In the meantime, President Trump’s economic advisor Peter Navarro hit out at Steve Mnuchin for declaring the China trade war as being on hold. It will be very interesting to see how talks over the weekend in Beijing evolve, but investors should get ready to re-price the trade risk.

Oil falls slightly after strong recovery

Brent prices fell slightly in the Asian trading session after a 2.8% jump on Wednesday. June 22 remains the most significant day for oil investors as a decision on the output from OPEC and non-OPEC producers will be taken. Given that there are still more than three weeks until the summit, any speech, headline or a comment from an official member will have a direct impact on prices. So, expect a very volatile three weeks ahead.

Oil traders will also be monitoring EIA inventories data out of the U.S. after API showed a 1 million rise in stockpiles last week.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

By CentralBankNews.info Fiji’s central bank kept its benchmark Overnight Policy Rate (OPR) at 0.50 percent and said its monetary policy stance would remain accommodative in light of the stable outlook for its twin objectives of inflation and foreign reserves. The Reserve Bank of Fiji (RBF), which has maintained its rate since October 2011, noted inflation rose to 4.0 percent in April, the highest in 12 months, from 2.6 percent in March but this was mainly due to supply-side shocks in the aftermath of natural disasters last month and relatively higher prices for kava and vegetables. This impact is expected to subside in coming months as the supply of most agricultural items normalizes, RBF said. On May 11 the central bank forecast upward pressure on prices in coming months but inflation would then stabilize around 3.0 percent by year-end and then average around 2.5 percent in 2019 and 2020. Fiji was hit by Tropical Cyclone Winston in February 2016, the worst ever cyclone in the Southern Hemisphere, and then by Cyclones Josie and Keni in April this year, which caused severe flooding and killed four people. But RBF Governor Ariff Ali said consumption remains upbeat and the economy is expected to register its ninth consecutive year of growth in 2018. Economic growth in 2017 has been estimated at 4.2 percent. Earlier this month the central bank lowered its 2018 growth forecast to 3.2 percent from 3.6 percent due to the devastating impact on agriculture from the cyclones in early April. But for 2019 the growth outlook was revised upwards to 3.4 percent from 3.2 percent while the 2020 outlook was unchanged at 3.2 percent. There has been a robust recovery in gold and timber production along with positive results in tourism and electricity production, while the global economic upswing continues to strengthen, underpinned by the recovery in emerging market economies, higher trade and investment. “However, geopolitical tensions between the United States and Iran and the general increase in commodity prices could pose risks” to the outlook, Ali added. Fiji’s foreign reserves rose to US2.163 billion as of May 31, up from $2.157 billion on March 29, sufficient to cover five months of imports and services, and are expected to remain at comfortable levels by year-end. In 2017 Fiji’s foreign reserves rose by $351.6 million to $2.272.8 billion end-year.

The Reserve Bank of Fiji issued the following statement:

“The Reserve Bank of Fiji Board has agreed to keep the Overnight Policy Rate unchanged at 0.5 percent following its monthly meeting on 31 May. Announcing the decision, the Governor and Chairman of the Board, Mr Ariff Ali, stated that“sectoral performances in the year have been generally positive so far, attributed to robust recovery in gold and timber production coupled with positive outcomes noted for visitor arrivals andelectricity generation.” Governor Ali highlighted that “consumption activity remains upbeat as reflected in increased VAT collections, higher vehicle registrations, and rising commercial banks’lending.” He added that despite the natural disasters in early April, the economy is expected to register its ninth consecutive year of economic growth in 2018. On the international front, Governor Ali stated that the global economic upswing continues to strengthen underpinned by the recoveries in emerging market economies and the increase in global trade and investment activities. However, geopolitical tensions between the United States and Iran and the general increase in commodity prices could pose risks to our macroeconomic outlook going forward. Nevertheless, the outlook for the Reserve Bank’s twin monetary policy objectives remains intact.Annual inflation increased to 4.0 percent in April from 2.6 percent in March, attributed to supply- side shocks post-natural disasters and relatively higher prices for yaqona (kava) and vegetables. However, this is anticipated to subside in the months ahead as supply of most agricultural market items normalise. Foreign reserves were adequate at $2,163.3 million as at 31 May, sufficient to cover 5.0 months of retained imports of goods and non-factor services and are expected to remain at comfortable levels by year-end. Governor Ali concluded that in light of the latest global and domestic economic developments and the stable outlook for inflation and foreign reserves, the monetary policy stance would remain accommodative. The Reserve Bank will continue to monitor economic developments closely and will align monetary policy as and when appropriate.” www.CentralBankNews.info

The Canadian economy has been the big talking point of this afternoon with the Bank of Canada (BoC) keeping rates flat at 1.25%. The major change though was the removal of dovish wording from the monetary policy statement, and now starting to align that wording with their American counterparts the Federal Reserve. The odds now of a hike at the next meeting in July have increased drastically as a result and this should not come as to much of a surprise, given that inflation has been running at 2% recently which gives the bank the mandate to look to move rates higher from the artificial lows they’ve been sitting at for some time. The only thing that could derail things is upcoming GDP figures which are expected to be slightly weaker, though analysts may change this in the wake of the Bank of Canada’s confidence, and NAFTA – which continues to drag on with the US and Mexico. However Canada has said it won’t cut a deal which negatively impacts Canada’s main industries.

For the USDCAD some serious movement has taken place and the bears were quick to capitalise on the USD sell off today and the CAD’s strength. So far the USDCAD has moved below the 1.2881 level on the charts and if it can remain below this support level we could see some further selling pressure and potentially a move to 1.2693 on the next leg. At the same time if we close above this key support level then potentially it’s a sign that the bulls think the USD still has plenty in the tank to run with and we could see another leg back up to 1.3041. All in all, it’s looking quite bearish, and we could get another few days on the back of the BoC announcement.

The other major talk of the town today was the complete U-turn in Italian politics. With the President and PM coming together to allow more time for the government to set up its coalition, and also the 5 star movement asking that Savona not be nominated for the finance/eco minister role for Italy. This of course still has its challenges, but at the same time it removes a major euro sceptic from a key position in the goverement and euro bulls were quick to rally as a result. There are a number of challenges ahead, but at the same time it could in theory lead to a more stabilised, yet progressive Italian government, that won’t be so aggressive towards the euro-zone.

The EURUSD as a result has rallied strongly eclipsing all of yesterday’s losses, but has failed to capitalise on the follow days candle. This to me is a strong sign that perhaps markets are positive but being cautious here. Resistance at 1.1719 will be interesting, with markets likely to look for some sort of political relief before extending further to the next level at 1.1824. At the same time if the bears are serious in the market, they may look to jump on the news and push the Euro down to 1.1482 in the long run.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The Central Bank of Norway does not exclude a rate hike

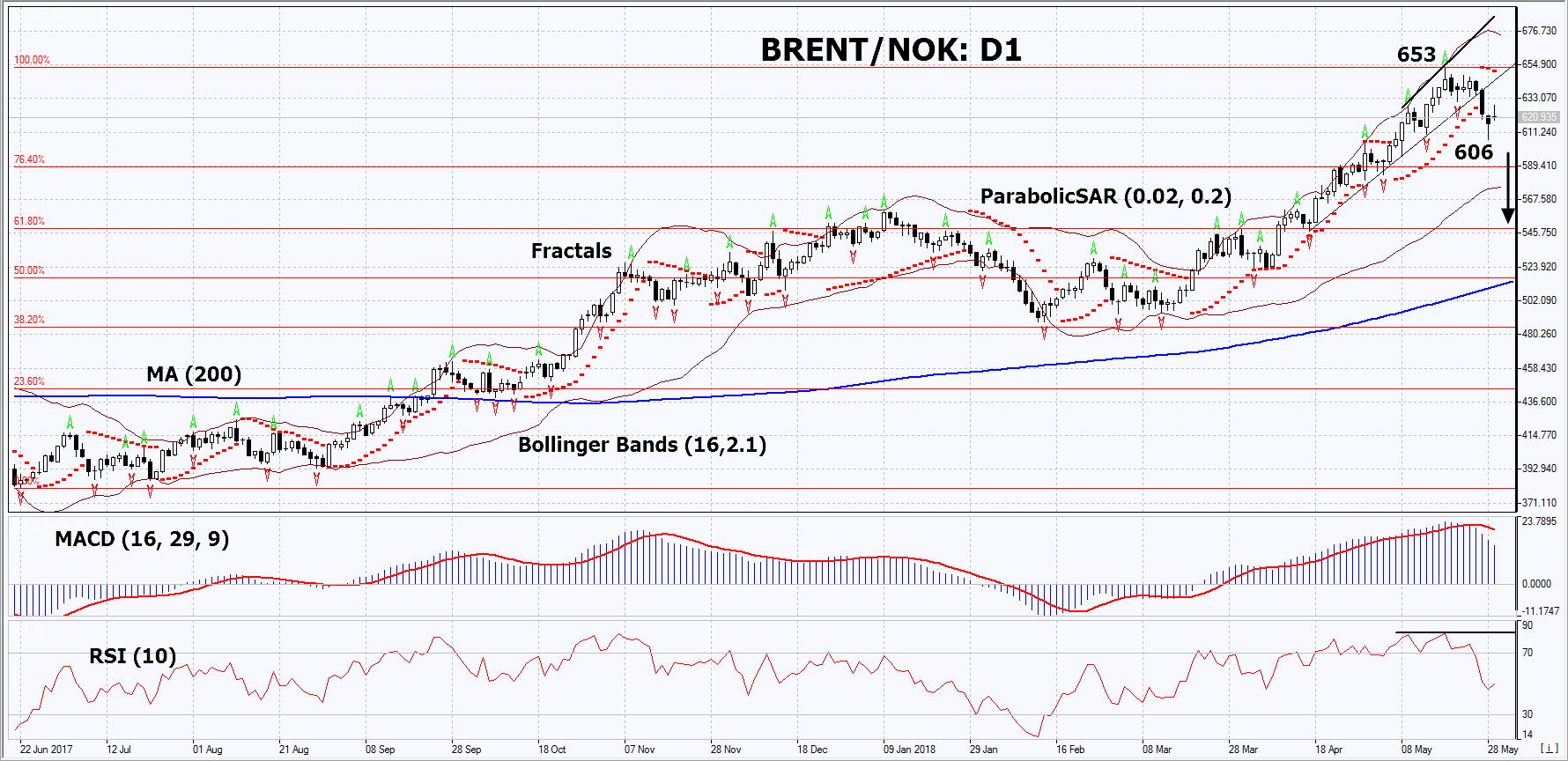

In this review, we suggest considering the personal composite instrument (PCI) “BRENT against the Norwegian krone”. It reflects the dynamics of the price change per barrel of Brent relative to the Norwegian currency. Will BRENT/NOK prices fall?

This movement would mean that oil prices fall, while the Norwegian krone strengthens. The current decline in oil prices is due to the expectations of market participants that the world major producers – Saudi Arabia and Russia will increase their production amid its possible reduction in Iran and Venezuela because of the US sanctions. Let us recall that the US is going to impose economic sanctions on Iran because of its nuclear program and on Venezuela, as the US does not recognize the results of the presidential elections, which again won Nicholas Maduro. At the next OPEC meeting on June 22, the production of the cartel and independent manufacturers, including Russia, could be increased by 1 million barrels per day. From its recent high (since November 2014), Brent prices have already fallen by 7%. The US oil production has grown by more than a quarter in the last 2 years and reached 10.7 million barrels per day. The US Oil reserves unexpectedly increased by 5.8 million barrels last week, which was an additional negative factor for oil. In turn, the statement of the head of Norway’s central bank Oeystein Olsen that the economic indicators of Norway correspond to the forecasts contributes to the possible strengthening of the Norwegian krone. The GDP in the 1st quarter of 2018 increased by 0.6% after a decrease by 0.3% in the 4th quarter of 2017. The Norwegian Central Bank may start to tighten monetary policy and raise rates this autumn. It should be noted that it is now 0.5% with a noticeably higher inflation at 2.5% in April in annual terms. Inflation data for May will come out on June 11 and may affect the rate of the Norwegian krone. The balance of the current account of Norway for the 1st quarter of this year will be published on June 6.

On the daily timeframe, BRENT/NOK: D1 breached down the support line of the accelerated uptrend. The medium-term uptrend endures, but the PCI is correcting down from the high since August 2014. Positive economic news from Norway and an increase in world oil production may contribute the decrease of prices.

The Parabolic indicator gives a bearish signal.

The Bollinger bands have widened, which indicates high volatility. The upper band is titled downward.

The RSI indicator is near 50. It has formed a weak, negative divergence.

The bearish momentum may develop in case BRENT/NOK falls below its last low and the two last fractal lows at 606. This level may serve as an entry point. The initial stop loss may be placed above the last fractal high, the 4.5-year high, the last fractal high and the Parabolic signal at 653. After opening the pending order, we shall move the stop to the next fractal high following the Bollinger and Parabolic signals. Thus, we are changing the potential profit/loss to the breakeven point. More risk-averse traders may switch to the 4-hour chart after the trade and place there a stop loss moving it in the direction of the trade. If the price meets the stop level at 606 without reaching the order at 653, we recommend to close the position: the market sustains internal changes that were not taken into account.

The past few days have not been kind to the Euro, which has tumbled to levels not seen since July 2017 amid the brewing political chaos in Italy.

With recent media reports stating that Italy’s PM-designate Carlo Cottarelli has simply failed to garner any support from major political parties, President Sergio Mattarella could dissolve Parliament in the coming days. The looming prospect of fresh elections potentially strengthening the position of Eurosceptic parties and resulting in a referendum on the Euro is likely to leave investors on edge. Sentiment remains bearish towards the Euro moving forward and the growing threat of a possible “Italexit” challenging the future of the European Union may spell more pain for the single currency.

It is worth noting that a depreciating Euro could somewhat support the ECB’s efforts to hit the 2% inflation target, by making exports more competitive and imports more expensive. However, signs of political instability in Europe negatively impacting growth may raise the prospect of QE rolling over into 2019.

Taking a look at the technical picture, the EURUSD remains bearish on the daily charts despite prices staging a rebound towards the 1.1600 level this morning. Previous support at 1.1600 could transform into a dynamic resistance that encourages a decline back towards 1.1450. Alternatively, a breakout above 1.1600 could invite an incline towards 1.1750.

Dollar eases ahead of ADP and GDP data releases

The Dollar retreated from a six-and-a-half-month high this morning, as investors engaged in a bout of profit taking ahead of the hotly anticipated releases of the ADP employment report & Q1 GDP figures.

ADP employment is expected to show a gain of 191,000 positions in May, while the second estimate of the first quarter US GDP is projected to hit 2.3%. Market expectations over higher US interest rates this year are likely to receive a boost if ADP and GDP figures exceed market forecasts.

Taking a look at the technical picture, the Dollar Index remains firmly bullish on the daily charts. Prices are trading above the daily 200 SMA while the MACD trades to the upside. Heightened US rate hike expectations have made the Dollar king against of major currencies. A decisive breakout and daily close above 95.00 may open the gates towards 96.00 and 96.60, respectively. Alternatively, if the Dollar Index fails to push above the 95.00 level, prices could dip towards 94.00.

Currency spotlight – GBPUSD

Sterling has suffered heavy losses against the Dollar thanks to growing fears of a possible Eurozone breakup.

A return of risk aversion amid the political turmoil in Italy simply encouraged investors to rush to safety, weakening the British Pound as a result. With Brexit uncertainty and fading BoE rate hike expectations adding to the Pound’s woes, further losses could be on the cards. Taking a look at the technical picture, the GBPUSD is under pressure on the daily and weekly charts. Sustained weakness below the 1.3340 level could encourage a decline towards 1.3170 and 1.3100, respectively.

Commodity spotlight – WTI Oil

Oil prices witnessed some stability on Wednesday, after depreciating sharply in recent days on prospect that OPEC and Russia will be easing supply curbs in response to falling global crude inventories.

With OPEC and Russia’s plans to boost output potentially scaring oil bulls away and reviving oversupply concerns, WTI Crude remains vulnerable to further losses. It should be kept in mind that geopolitical risk factors in the form of looming sanctions against Iran, falling output from Venezuela and tensions in the Middle East could support oil prices in the short term. However, the possibility of rising output from Russia and OPEC combined with robust US Shale production could create major headwinds for oil further down the road.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The euro currency continued to weaken amid the political uncertainty from Italy. The common currency fell to fresh yearly lows at 1.1510 on Tuesday. Economic data was sparse leaving investors to focus on Italy which soured the general market sentiment.

The U.S. consumer confidence index from the conference board showed a decline to 128.0 on the index with previous month’s data also revised down to 125.6. The U.S. dollar however maintained its stronghold across the board.

The economic calendar picks up pace today starting with the import price and retail sales data from Germany. Revised GDP numbers from France for the first quarter will be coming out which is expected to confirm a 0.3% increase. Germany will also be reporting on the preliminary inflation figures which are expected to show a rebound of 0.3% in consumer prices on a monthly basis.

The ADP/Moody’s private payroll numbers will be coming out ahead of this Friday’s official payroll figures. Economists forecast that the private sector added 186k jobs during the month of May. This marks a somewhat slower pace of job gains compared to 204k that was registered previously. The private payrolls data will be followed by the final revised GDP estimates from the U.S. which is expected to remain unchanged at 2.3%.

The Bank of Canada will be holding its monetary policy decision later. Interest rates are expected to remain unchanged at 1.25% at today’s meeting.

Will you be trading the NFP this coming Friday? Register now for our Live NFP Webinar, coming to you before, during and after the release!

EURUSD intra-day analysis

EURUSD (1.1534): The EURUSD currency pair continues to post losses with price action touching down to lows of 1.1533. The declines are likely to persist with the next downside target seen coming in at 1.1500. This would mark a fresh yearly low to this level. However, there is scope for the EURUSD to potentially post a bounce to the upside. With the resistance level at 1.1730 being tested any retracement in price action could be limited to the recent local highs of 1.1638.

USDJPY intra-day analysis

USDJPY (108.70): The falling market sentiment was reflected in the USDJPY currency pair which was seen clearing the lower support level of 108.90. The current retracement at this level is expected to see 108.90 level being retested for resistance. To the downside, we can expect to see continued decline. The next main support level comes in at 107.64 which marks an unfilled gap from April 20, 2018. The downside bias will shift unless USDJPY posts a rebound above 108.90 and clearing the next resistance at 109.43 – 109.57.

XAUUSD intra-day analysis

XAUUSD (1298.89): Gold prices have been hovering near the resistance level of 1304 – 1301 for nearly five consecutive days. Price action could possibly breakout above this level. Clearing the resistance level could signal an upside momentum in prices. If support is established on a retest, then we expect USDJPY to potentially post gains toward 1325 level. To the downside, a retest of 1282 support is still pending which could be tested more firmly.

You may be a complete trading newbie and maybe you’re an experienced trader, but you’ve heard all the news about the cryptocurrency market and you want in. Maybe you read the Financial Times or the Wall Street Journal to keep on top of the economic news, but do you really know enough to jump into crypto?

Probably not.

What is Cryptocurrency?

In short, cryptocurrencies are digital money created on encrypted software called a transaction blockchain. That encryption software also verifies all transactions. Currency is created on the blockchain by ‘mining’. Every time a transaction is made it is added to the blockchain ledger, making it public and irreversible.

The software is spread around the globe on hundreds of decentralised machines called ‘nodes’. A ‘full node’ carries a complete copy of the blockchain while other ‘nodes’ only carry fractions. There is no central storage point for all of this information so it can never be a single point of weakness in the transaction chain.

Every time a node is used to perform a transaction, using computational power (and let’s face it, electricity), it is paid in the newly created digital currency. That’s how new currency is created and how ‘miners’ accumulate their cryptocurrency.

As more service and retail providers begin to accept Bitcoin, Ethereum and Litecoin (to mention a few) as valid payment, the more it strengthens the cryptocurrency standing as an actual currency, rather than a digital asset.

Where do I start and what do I need?

Firstly decide what you want to do with cryptocurrency. Do you want to trade it against fiat currency? There are plenty of brokers and platforms available that do that. If you are already an active trader there is a fair chance that you can do the same with crypto through your current platform. However, leverage against crypto trading as CFD tends to be Low.

If you want to invest in cryptocurrency it is a different animal altogether.

Unlike trading stocks or the Forex market, entering the realm of cryptocurrency has fewer barriers for the small first-time investor. The initial investment doesn’t need to be high and while volatile crypto markets may wipe value from your coins, you still own the currency and can try to wait it out (no guarantees on that score though).

Three things you need in order to start:

Money– Good old-fashioned fiat money. Most fiat-crypto exchanges work in US Dollars (USD, $), but some have included other currencies such as Euro (EUR), Canadian Dollar(CAD), British Pound (GBP), Japanese Yen (JPY) and Hong Kong Dollar (HKD). There are more, but the two main fiat currencies accepted are USD and EUR. Other currencies will need to go through an exchange process first.

*Just remember that it needs to be an amount you can comfortably live without, potentially for the long-term.

Wallet – You NEVER leave your digital currency on an exchange, so you will need a wallet before you even go near an exchange. Do your homework and find the one that works for you. If you are looking to diversify into cryptocurrencies other than Bitcoin, you’ll want something that can handle that. There are several out there; web-based, desktop, mobile, and hardware. You can even have a paper wallet.

Bitcoin (or Ethereum)– This is your final point for entering crypto-land. Bitcoin is the one everyone has heard of and the one that all exchanges support. It was the first and is still the biggest. The number of exchanges that allow fiat-crypto exchange is small in comparison to the number of exchanges out there and they tend to have higher transaction fees to cover this additional layer of functionality (and insurance). Smaller exchanges will only accept crypto-crypto exchange but have a lower transaction fee, which makes them more favourable to new customers.

What to Avoid

As a new entrant to the crypto market there are some things that should be avoided:

ICOs– These are Initial Coin Offerings. I’m not saying that ICO’s aren’t a valid entry to a new currency. I am saying that until you have been in the game a while, know your way around the whitepapers, and have a good grasp of what a valid ICO looks like, you should avoid them. Too many people have been caught out by scams and gambled their capital on “The Next Big Thing”. You should only invest in an ICO if you have put the time in to do thorough research on the entity concerned.

Coins claiming instant returns – This is probably a given considering the number of scammers who have jumped on the crypto money train

Exchanges with low volumes – Not many people using it so not a lot of liquidity available.

Coins with low volumes and low market cap – Coins with low volumes and a low market cap have less demand and you may find it hard to trade in them if very few others even know about them and even fewer want to buy them.

Overconfidence & Emotional Trading –Confidence is good, but the overconfidence that can come with successive profitable trades can be detrimental to your trading strategy. Emotional trading is the same. Fear, Uncertainty and Doubt (otherwise known as FUD) are common reasons for cashing out early or buying high.

Okay, What now?

You’re in! You have entered the crypto sphere. What you choose to do now is entirely up to you. You can hold on to your purchases and wait to see if they increase in value (HODL is the term often used as a mistype of hold from many moons ago, now standing for Hold On for Dear Life), you can diversify into other cryptocurrencies with potentially greater gains, or you can sell and get out again (no one is forcing you to stay).

You could keep adding to your crypto portfolio by injecting more USD or EUR – some people are doing this as a type of ‘retirement fund’. Like any financial trading or exchanging game, there are risks and there are potential gains. In this, Cryptocurrency is no different from any other commodity.

Bottom line

There are very few barriers to getting into cryptocurrency and if you do join the party it doesn’t have to be in a big way. Cryptocurrency is NOT a guaranteed return on investment. It doesn’t matter how many people tell you that it is (those lucky ones that mined Bitcoin for a while and then kept a few, just in case). You do have the benefit of being able to learn as you go. Start small and as you learn more about the world of cryptocurrency you can diversify into emerging coins, ICOs and other crypto markets.

Like any other technology or development, it will take time for cryptocurrency to become mainstream and for the underlying tech to be adopted by big businesses. If Cryptocurrency is really the currency of the future, then the best time to get in is now. If it isn’t the way forward, well, you didn’t need much to get in the game and maybe you’ll turn a profit along the way.

About the Author:

Amie Parnaby is a professional writer with an experience in a broad range of industries, from I.T to training, from optics to banking. Within these settings, Amie has provided quality web content, training materials and technical documentation. She is currently an in-house Content Writer at Leverate.

It has been all about Italy today in the markets, as they’ve completely turned and now taken a risk aversion approach compared to last week. This is not shocking news, but it has led to a lot of concern among the euro-zone members especially around the Italian political situation which is beginning to look like some sort of drama regarding the Euro and the euro-zone. In all reality a new government will need to be elected, and it’s likely to be a very euro-sceptic government which will be bitter about the recent moves from the President – certainly a battle of ideology between the two sides. If the current climate persists then we could see the Euro take a hammering from traders and hedgers, and the return of strong currencies like the CHF and JPY against the Euro, but for now it has been all about the EURUSD.

What looks like a bear market for the EURUSD is certainly turning into a major one with the current climate, as traders exit in the droves. The market is now looking to extend down to support at 1.1482 after crushing through the upper support level at 1.1582 yesterday. The bears are clearly looking to take advantage of the chaos but they may run out of steam as the election is some time off, and positive EU comments could potentially help some of the rebel parties gain a clear majority. In the case of bullish movements resistance can be found at 1.1582 and 1.1719 but I would be careful of the 20 day moving average here which is likely to fight off any large movements higher at this stage, especially as Italy will remain on everyone’s mind for some time. With the real threat being Spain and Portugal further down the line; even potentially Greece.

On the other side of the world the NZD has been in the spotlight as well as traders, as mentioned above, have gone off the idea of anything risky at present. Traders will also be focused on the upcoming business confidence figures to see how the economy is going at present, and if potentially we may get to a level where rate rises are back on the cards – something that feels very far off.

Looking at the NZDUSD on the charts it’s clear to see that it’s lacking bullish potential at present as even the 20 day moving average is stopping traders in their tracks. There was also a brief touch on resistance at 0.6966 before the market slipped back. If the bulls do regain control the next level up is 0.7054, but this is also a key psychological level for markets and would be tough to beat without any positive risk sentiment. If the bears look to swipe harder in the current market climate then support at 0.6819 will be the level to beat, but it may take some serious effort to get there.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

According to the 2018 IMD World Competitiveness report, Philippines ranking plunged nine notches. In reality, competitiveness indexes often fail to capture disruptive change.

According to the IMD report, executed in cooperation with the Asian Institute of Management, Philippines fell by nine places to 50th among 63 countries.

Nevertheless, Socioeconomic Planning Secretary Ernesto Pernia called the findings a “misobservation” – and rightly so.

Economic realities vs. Index data

After the global crisis, the Philippines’ economic performance quickly bounced back, but did not provide sustained growth in the first half of the 2010s. Despite stated struggle against corruption, the Aquino administration neglected systemic graft and drugs proliferation focusing on geopolitics, at the cost of economic development. Investment was ignored. Relatively low debt benefited mainly the financial elite.

How were these trends depicted by the IMD at the time? Actually, the IMD data suggests nothing much happened in the Philippines in the early 2010s (Figure).

Figure Philippine Economic Performance Vs IMD Ranking, 2008-2018

Source: World Bank (annual real GDP growth); World Competitiveness Index (IMD ranking)

Ironically, the Index ranking also indicates that the country’s competitive performance improved in 2013-14, when narco-corruption grew pervasive creating odd bedfellows in politics. As the Liberal Party saw Manuel Roxas as the next president, a wasteful “election stimulus” supported growth in Aquino’s last days.

In contrast, Duterte began a historical infrastructure investment push, while initiating the requisite changes to boost foreign investment, with his economic team, including Secretary of Finance Carlos Dominguez III, Secretary of Budget and Management Benjamin Diokno and Secretary of Public Works and Highways Mark Villar. That required greater debt-taking and would lead to deficits in the short-term. Philippine peso would soften against the US dollar, as a result of conservative monetary policy in the past and the Fed’s rate hikes. Yet, the Philippines is positioned to enjoy 6-7 percent annual growth and rapidly rising living standards until the early 2020s.

How has the IMD measured these realities? The simple answer is: Poorly. Basically, the Index insulated short-term trends – e.g., debt, deficit, exchange rate – from the transformative investment program, and then mistook its own misreading as the government’s policy mistakes.

As the Philippines is now positioned for sustained growth, the IMD Index suggests that economic performance has been hit the worst, when in fact it is more sustained than in years as the government’s infrastructure program is integrating and connecting the country domestically, regionally, and internationally.

So why do the competitiveness indexes often fail to capture transformative change?

Five caveats

In the past 25 years I have been involved with global competitiveness and innovation initiatives, while lecturing and speaking in MBA and Executive MBA programs from New York University’s Stern School of Business and Columbia’s School of Business to Harvard Business School, Tsinghua and Fudan in China, Singapore Management University, Nanyang Technology University and INSEAD, to mention some.

When the Cold War ended, economic competitiveness came to substitute for geopolitical rivalry. That’s when I began cooperating with the leading strategy and cluster analyst, Prof. Michael E. Porter in Harvard Business School. His approach framed the original Global Competitiveness Index by the World Economic Forum (WEF), along with Jeffrey Sachs’s macro index and Xavier Sala-i-Martin’s research.

Of the two competitiveness indexes, IMD’s World Competitiveness Yearbook is the minor one. It deploys both hard data and executive surveys but features only 63 economies. Much of the WEF data is based on executive surveys and a third on hard data, but it features some 140 economies.

The not-so-secret secret of the competitive indexes is that they tend to reflect slowly-changing historical realities. So they often fail to capture rapidly-changing, future-driven and disruptive economic realities, such as Duterte’s transformative leadership.

Second, these rankings rely significantly on executive surveys, which reflect the views of incumbents rather than those of the challengers. When I projected in the US National Interest in 2005 that Chinese and Indian multinationals were becoming competitive and innovative, most observers had not heard of Huawei, Alibaba, Tata and Infosys, and other future leaders. Like the Philippines today, Chinese competitiveness was downplayed for years. Yet, Chinese government leaders and executives remained focused on economic progress – as Filipino leaders do today.

Third, when competitive realities change rapidly and disruptively, hard data is absent and surveys reign. In such situations, domestic media should mirror economic realities. But when that media is linked with domestic monopolies and vested interests, such neutrality is often absent. When Nokia and Ericsson conquered mobile markets in the 1990s, most executives still focused on Motorola and AT&T, which failed in the GSM era – as I discovered advising them in New York City.

Fourth, as most competitiveness indexes represent multinationals headquartered in advanced economies, they offer lessons that don’t always work for late entrants from emerging economies. Last summer, when I spoke in Jollibee’s executive summit, I recalled that when I began to use the company in case studies a decade ago, foreign execs often said: “Jolly, who?” Today, Jollibee is far better known, thanks to its international strategy and quest for excellence.

Finally, there are political linkages behind all indexes. Michael Porter became more widely known in the 1980s, when the Reagan administration made him the head of its competitiveness commission. Jeffrey Sachs’s ideas of “shock therapy,” which monetarist Milton Friedman had first applied during Pinochet’s Chilean dictatorship, contributed to Russia’s Great Depression in the 1990s. Sala-i-Martin used to cooperate with Robert Barro who built his growth theory on neoclassical economics, which has been the cornerstone of post-Cold War US administrations. But what works for US dominance may not always be good for other nations.

The long and short of it is that many competitiveness indexes look into the future by staring at the rear-mirror. That’s not a receipt for future , but for crashes.

It is not the Philippine economic performance that is failing. Rather, it is the competitiveness indexes that fail to capture the country’s new economic progress – for now.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served as research director at the India, China and America Institute (USA) and visiting fellow at the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

The original commentary was published by The Manila Times on May 28, 2018.

A negative vibe is being felt across the financial markets, as political chaos in Italy has caused an eruption of risk aversion and revived fears over a possible Eurozone breakup.

In a move that raised the possibility of a snap election in Italy, President Sergio Mattarella rejected the coalition’s nomination of Paolo Savona as finance minister. Fears are likely to heighten over another round of elections strengthening the position of anti-EU parties and potentially resulting in a referendum on the European Union.

With concerns heightened over political risk in Italy threatening the stability of the European Union, the Euro remains heavily at risk to sudden losses.

Adding to the Euro’s woes is the upcoming data that Spanish Prime Minister Mariano Rajoy will face a vote of no confidence on Friday in parliament.

The Euro has tumbled below the 1.16 level for the first time since November 2017 thanks to the political drama in Italy and Spain. With uncertainty eroding buying sentiment towards the Euro currency, the EURUSD has scope to extend losses. Previous support around 1.160 could transform into a dynamic resistance that encourages a decline towards 1.145.

Global stocks fall on Italian turmoil

The political turmoil in Italy has triggered risk-off trading across the board, with global stocks and riskier assets vulnerable to heavy losses.

Most Asian stocks have already closed in the red amid the risk-off mood, with the caution and uncertainty dragging European shares lower. The negative sentiment from Asian and European markets could infect Wall Street this afternoon. Global equity bears are likely to remain in the vicinity as heightened political uncertainty in Europe prompts investors to maintain a safe-distance from riskier assets.

Japanese Yen powered by risk aversion

The Yen sharply appreciated against the Dollar this morning, as traders rushed to safety amid the political drama in Italy.

With market anxiety likely to heighten over fears of an early election in Italy resulting in a referendum on the European Union, the Yen could remain a trader’s best friend. Taking a look at the technical picture, the USDJPY is under noticeable pressure on the daily charts with prices trading marginally below 109.00 as of writing. Sustained weakness below 109.00 could encourage a decline towards 108.00 and 107.40, respectively.

Commodity spotlight – Gold

Gold popped above the $1300 level as political uncertainty in Europe accelerated the flight to safety. However, gains were capped below $1307 by a broadly stronger US Dollar.

Although risk aversion has the ability to support Gold in the short term, an appreciating Dollar and expectations of higher US interest rates are likely to continue weighing heavily on the yellow metal in the medium to longer term.

Focusing on the technical picture, prices have breached above the $1300 psychological level. A daily close above this key level could encourage an incline towards $1324. Alternatively, a failure for bulls to maintain control above $1300 may invite a decline back towards $1280.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.