Source: Kevin Michael Grace of The Gold Report (3/5/14)

http://www.theaureport.com/pub/na/ron-struthers-the-juniors-are-forging-the-path-forward

Is the bear market in mining equities finally over? It looks that way, says Ron Struthers, publisher and editor of Struthers’ Resource Stock Report. In this interview with The Gold Report, Struthers explains what distinguishes this recovery from past ones: TSX Venture Exchange stocks, not the majors, are leading the way. But which juniors should investors favor? Struthers names several with proven management, ample funding and good share structures.

The Gold Report: Back in July, you said that the bullion banks’ fractional reserve system was coming under stress. Do the big gains in gold and silver bullion this year suggest that this system is breaking down?

Ron Struthers: I believe the fractional reserve gold system has seen more stress and was probably in good part responsible for cementing the bottom in gold around $1,200/ounce ($1,200/oz). We know Germany has not even been able to repatriate the modest amounts it asked for. The gold is simply not there. The physical gold was leased or sold years ago.

We see that the gold inventories at COMEX and the bullion banks have been steadily declining for the past year. There are not too many places to turn to, if any, for physical supply. It is no secret that record amounts of physical gold have been moving into China, and India continues as a major buyer despite higher import taxes. I think that a change in the market sentiment, a belief that the bottom is in, and the large short position on the COMEX are the reasons for the recent rises in price.

TGR: Do you put any credence in the claims by the Gold Anti-Trust Action Committee (GATA) that there is an organized conspiracy by central banks and the gold and silver bullion banks to lower the prices of gold and silver?

RS: There has always been a lot of intervention in the markets by the central banks in currencies, of which gold is one. It wouldn’t surprise me if there is front running by bullion banks as well that are privy to any such action.

TGR: Do you think that we could see a divorce between physical and paper gold?

RS: I think we’ve already seen some of that. For instance, the SPDR Gold Shares (GLD) has been at about a 4% discount to the metal for the last couple of years. We’re seeing some very high premiums in Asia on the spot physical price compared to the COMEX paper price—as much as $70/oz.

TGR: The historical appeal of physical gold is that it is a real asset that cannot be duplicated endlessly, as fiat currencies can. That being the case, what is the appeal of paper gold?

RS: It depends where you are. Asians don’t think of paper gold at all. To them, it’s all physical. They buy it, keep it as savings and pass it from generation to generation. But North Americans like to trade things, to buy and sell for short-term profit, so they are more apt to buy paper gold products like futures and exchange-traded funds.

TGR: You’ve argued that quantitative easing (QE) is a ploy by the Federal Reserve to make the U.S. economy seem stronger than it really is. Does the tapering of QE indicate genuine confidence in the future, or is this another ploy?

RS: Actually, that is backward. I believe the Fed strives to make the U.S. economy look stronger than it is so it can try to reduce QE and increase confidence in the U.S. debt. If confidence existed, we wouldn’t need QE. We have QE because the Fed is the lender of last resort. There is not enough confidence from U.S. or foreign investors to fund U.S. federal government debt and real estate mortgage debt. In 2013 the Fed bought 150% more treasury debt than all foreign investors combined. Nor is there the will to reduce this debt. This lack of will is another reason for the lack of confidence.

The Fed has long been on record saying that its low interest rate policy will repair the U.S. economy, so it needs QE to maintain these low rates. And it must do all it can to demonstrate that this policy is actually helping the economy. The Fed is walking a tightrope. It knows it cannot keep QE going forever. It wants to make the U.S. economy look as good as possible to increase market confidence and to manage the debt problem and, eventually, resolve it.

TGR: David Stockman, President Reagan’s budget director, has argued that the hubris of the Fed and the U.S. Government has resulted in a situation whereby “gold could explode at any moment.” Do you agree?

RS: Yes. The whole world financial system is walking a tightrope. Structural problems and large debt loads have not been resolved, only Band-Aids applied. The longer you walk a tightrope, the greater chance of a fall, in this case, a financial fall or collapse. This would result in a big vote of confidence in certain fiat currencies and a huge flight to gold. But so much physical gold has gone to Asia, and it’s not coming back. So when investors come looking for it, there’s going to be a shortage of supply.

TGR: What is gold’s next resistance level?

RS: I’m looking at $1,360–1,370/oz.

TGR: If gold burst through $1,370/oz in the next couple weeks, would this signal a rather rapid acceleration?

RS: Yes, it could. The next level would be $1,450–1,500/oz; that could offer resistance.

TGR: Given the recent rises in gold and silver equities, is the bear market that began in April 2011 finally over?

RS: I believe it is over, but the equities have given little sign yet of a bottom or new uptrend. Gold just went above the 200-day moving average. I would say it’s probably one of the strangest markets I’ve ever seen. We’re really in unprecedented times with all the market interventions, record debt, currency wars, distortion of economic and market data, computer trading and alternate trading platforms on markets.

Looking at the NYSE Arca Gold BUGS Index (HUI) on the gold stocks, we’ve not seen much of a move yet. It looks as if my downtrend line might be broken, but we have not seen a higher high in the index since the last low.

TGR: What do the shorts tell us?

RS: I have not seen short covering in the gold stocks yet. As of Feb. 15, there were seven gold stocks in the TSX Top 20 short positions, which is pretty significant given that they have much higher short positions compared to other stocks that have a much higher number of shares outstanding. We’ve seen covering only in Osisko Mining Corp. (OSK:TSX), which is subject to a hostile takeover bid by Goldcorp Inc. (G:TSX; GG:NYSE).

Another strange thing is the S&P/TSX Venture Composite Index, which is a good measure of the junior mining explorers. Typically, the juniors follow the seniors or producers: the trickle-down effect. Once the bigger stocks do well, the little guys start to follow. In the past 12 months, however, the TSX Venture Index is down about 10%, while the NYSE Arca Gold BUGS Index is down more than 30%.

This time around, the TSX Venture is leading the way up. It broke through the 200-day moving average in early January. It tested that in early February, and now it has broken clearly to the upside, a second higher high above 1,000. The 200-day moving average has started to turn up as well.

TGR: Do you think that all the bad press that the majors have gotten for bad decisions, inefficiency, bloated projects, etc., has caused this anomaly?

RS: Somewhat. The producers’ margins were hit pretty hard by the gold price decline. For junior explorers, however, $1,200–1,300/oz gold is still pretty good if an explorer makes a discovery. On the other hand, while the producers have struggled with rising costs, this bear market has cut the cost of exploration probably almost in half because of falling demand for related goods and services.

TGR: What qualities do you look for in junior explorers?

RS: I’m sticking with companies that have proven management, ample funding and/or good share structures, so they can still raise funds. Diversification is a good approach for investors.

TGR: After the gold price collapse last year, there was a renewed emphasis on the importance of high grade. How crucial is this?

RS: Grade is always important but becomes more so as the price of gold falls.

TGR: What are some companies leading the way in high grade?

RS: Roxgold Inc.’s (ROG:TSX.V) recent preliminary economic assessment at its Yaramoko project in Burkina Faso is projecting a metal grade of 11.9 grams per ton (11.9 g/t) in the first five years. That results in a low cash cost of just $455/oz, a high 47.7% internal rate of return and only a 1.4-year payback on initial capital. So you can see the big effect there.

TGR: Yaramoko’s initial capital expenditure is only $93.8 million ($93.8M). Isn’t that quite low?

RS: Yes.

Eastmain Resources Inc.’s (ER:TSX) Eau Claire deposit in Canada has at least 1.5–3 million ounces (1.5–3 Moz) and a grade higher than 3 g/t. The open-pit resource is 635,000 ounces (635 Koz) at 4.67 g/t, and the underground is 145 Koz Measured and Indicated at 6.3 g/t. These are attractive numbers. Goldcorp already owns almost 9% of Eastmain.

Richmont Mines Inc. (RIC:TSX; RIC:NYSE.MKT) produces good grades but has seen a temporary rise in production costs because its grade declined from about 5.5 g/t to 4.5 g/t. That had quite an effect on its earnings. But I think these numbers will soon reverse, which should make for a good turnaround there. The company is driving down a ramp to produce from its Island Gold Deep deposit in Canada. In late January, it updated that resource to 169 Koz Indicated at 11.5 g/t, with almost 1 Moz in the Inferred at 9.29 g/t. Again, very good grades.

TGR: Of the companies looking to improve grade, which stand out?

RS: A couple. We picked up Mandalay Resources Corp. (MND:TSX) at a good price in November because I like its Costerfield mine in Australia. It has gold grades: more than 9 g/t with 4% antimony on top. Its other mine, Challacollo, in Chile, has a very good silver grade.

TGR: Challacollo was a recent purchase, correct?

RS: Yes. It has a very good silver grade of 209 g/t with 2.28 g/t gold along with it. The company is very profitable, reporting net income of $29M for 2013. That’s $0.09/share, and it is paying a good dividend, too.

SilverCrest Mines Inc. (SVL:TSX; SVLC:NYSE.MKT) has been a great growth story with its Santa Elena mine in Mexico. It has been very profitable even at lower silver prices, and it put its profits into growth and expansion. The company’s 3,000 ton per day (3,000 tpd) mill is almost complete, and it will soon start producing underground reserves.

TGR: How will this affect grade?

RS: The gold grade should remain about 1.6 g/t, but the silver grade should double, to well over 100 g/t. The company’s future is brightened by two other advanced projects. It looks to duplicate Santa Elena’s success at its La Joya project, again using a starter open pit. Its Cruz de Mayo project is just 35 kilometers (35km) from Santa Elena. With 2.3 Moz Indicated and more than 12 Moz Inferred, it could heap leach there and possibly ship the high grade to the Santa Elena mill.

TGR: Let’s talk about companies that have gained greatly in price recently but, in your opinion, still have room to grow.

RS: One that stands out is Avino Silver & Gold Mines Ltd. (ASM:TSX.V; ASM:NYSE.MKT; GV6:FSE). It rose from a bottom of $0.75/share in July to more than $3/share recently. It continues to expand production at its historic Avino project in Mexico, which was relaunched last year. Around year-end 2014, it will add a third circuit to production from the historic Avino mine. That will increase the mill run rate from 500 tpd to 1,500 tpd. Currently, most of production is from the nearby San Gonzalo mine. Its grade is high, recently processing gold at 1.98 g/t and silver at 358 g/t. That results in a low cash cost of under $7/oz silver equivalent.

TGR: With the recent tax-regime changes, there has been a lot of negativity about Mexico of late. What’s your view?

RS: I think the concern is somewhat overrated. Governments always want a bigger piece of the pie. Mexico retains a stable mining regime, a good labor force and infrastructure, and relatively low costs. I think the mining companies can live with the new tax regime.

TGR: Moving on to Nevada, now that Rye Patch Gold Corp. (RPM:TSX.V; RPMGF:OTCQX) has gotten $10M in its settlement with Coeur Mining Inc. (CDM:TSX; CDE:NYSE), does this gives it what it needs to find high grade there?

RS: It was a nice deal. Rye Patch also has a net smelter royalty (NSR) from Coeur, which will generate about $8M annually for the next three years. This should enable Rye Patch to explore actively. I think the bigger story is that the company already has a 1+ Moz resource it can expand on. Its properties are located very close to producing mines.

I’m not so concerned about grade there, as Nevada remains one of the lowest-cost gold jurisdictions. It’s all about the heap leach and good infrastructure. If Rye Patch could deal one or two projects to next-door majors, that could reward shareholders very nicely.

TGR: Is Rye Patch a possible takeout target?

RS: If it were able to grow one of these deposits substantially, I would say so. I think the company would more likely deal one of its projects with either a coproduction agreement or another NSR royalty.

TGR: Which explorers do you like in Nevada?

RS: Asher Resources Corp. (ACN:TSX.V) is fully funded for 2014. There were high expectations for its first drill program at its King property. It did not hit the big hole on the first round, but a lot was learned. It ended up drilling a halo of porphyry, so the real target is likely off to the left of the high induced polarization (IP). It appears it drilled under the gold structure on another target there, despite some good hits in two holes. Before a second round at King, it is drilling three holes on its Lavington gold project in British Columbia.

TGR: Which Canadian explorers do you like?

RS: TerraX Minerals Inc. (TXR:TSX.V). In the past six months it acquired the advanced-stage Northbelt gold property in the Northwest Territories. That had seen previous drilling of 463 holes, with about 25 gold zones, many with some pretty good high-grade numbers. The company has been reassaying previous drill holes and compiling the historic data ahead of a drill program planned for this summer. It has raised ample funding.

Zonte Metals Inc. (ZON:TSX.V), which has a unique group of projects in Newfoundland. It is also focusing on Colombia, and I expect acquisitions could be announced any time. It has a good share structure and strong insider backing. I don’t think it will have any trouble funding a new acquisition.

TGR: What else stands out in Colombia?

RS: Colombian Mines Corp. (CMJ:TSX.V) is well funded with about $4M. Its El Dovio project saw good drill results last year, with 16.8 g/t over 6.85 meters (6.85m). It has a number of other projects in Colombia, including Yarumalito, a joint venture with Teck Resources Ltd. (TCK:TSX; TCK:NYSE) that Teck is funding. Colombia remains one of the best jurisdictions for exploration. It has the oldest, most stable democracy in South America. It remains underexplored, even though it was once the world’s leading gold producer.

TGR: How about Mexico?

RS: Mammoth Resources Corp. (MTH:TSX.V) is funded for 2014 on its Tenoriba project. This shows high-grade gold and silver on surface and good drill results from a 2008 program that included 45 g/t over 1.9m. It is planning some IP and magnetic surveys over four main targets and some road development that could cut zones ahead of a drill program.

Another I’ve looked at lately is Tosca Mining Corp. (TSQ:TSX.V). Its Carol copper-gold project is just 5km from the Piedras Verdes copper mine, the third largest in Mexico, which produces 70 million pounds annually. Invecture Group got this from Frontera Copper, which it bought and took private.

Invecture bought out Kimber Resources Inc. late last year, as well as Vista Gold Corp.’s (VGZ:TSX; VGZ:NYSE.MKT) Los Cardones project. I think Tosca is probably its next target. Invecture has staked all the available ground around Tosca’s project. Carol has seen excellent trench results, including 1.9% copper, 19% zinc, 0.93% lead, 36 g/t silver and 0.59 g/t gold over 10m. Its upcoming drill program should prove quite interesting.

TGR: Any other gold explorers you could mention?

RS: Garibaldi Resources Corp. (GGI:TSX.V) has done much better than many juniors. It was funded throughout the downturn by a big block of Paramount Gold and Silver Corp. (PZG:TSX; PZG:NYSE.MKT) shares it held. It has advanced a number of its projects: La Patilla, Tonichi, Iris and Rodadero in Mexico and Grizzly in Canada. The company is awaiting drill results from La Patilla and has pretty high expectations for good numbers based on previous exploration.

TGR: And there is a uranium junior you’re sweet on, correct?

RS: Yes. Zadar Ventures Ltd. (ZAD:TSX.V) is well funded by two recent financings. It has an advanced portfolio of projects in the prolific Athabasca Basin. Its management has a proven record of uranium discovery in the basin. Its geologist, Kieran Downes, is the former vice president of exploration with Cameco Corp. (CCO:TSX; CCJ:NYSE). And its PNE project is adjacent on trend to the recent significant Patterson Lake discovery.

TGR: Given how depressed the junior sector has been since 2011, seeing the TSX Venture leading the way, as you put it, has to be pretty encouraging, no?

RS: I agree. We’ve had a brutal downturn and washout. For almost two years, the market had little access to capital. This resulted in share consolidations, mergers and many companies disappearing. Now we’re seeing some momentum. This could be the start of quite a turnaround.

TGR: Ron, thank you for your time and your insights.

Ron Struthers founded Struthers’ Resource Stock Report 20 years ago. The report covers senior and junior companies with ample trading liquidity.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Kevin Michael Grace conducted this interview for The Gold Report and provides services to The Gold Report as an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Mandalay Resources Corp., Roxgold Inc., Richmont Mines Inc. SilverCrest Mines Inc. and Rye Patch Gold Corp. Goldcorp Inc. is not affiliated with The Gold Report. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Ron Struthers: I or my family own shares of the following companies mentioned in this interview: Asher Resources Corp., Avino Silver & Gold Mines Ltd., Colombian Mines Corp., Eastmain Resources Inc., Mammoth Resources Corp., Richmont Mines Inc., TerraX Minerals Inc., Tosca Mining Corp., Zadar Ventures Ltd. and Zonte Metals Inc. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

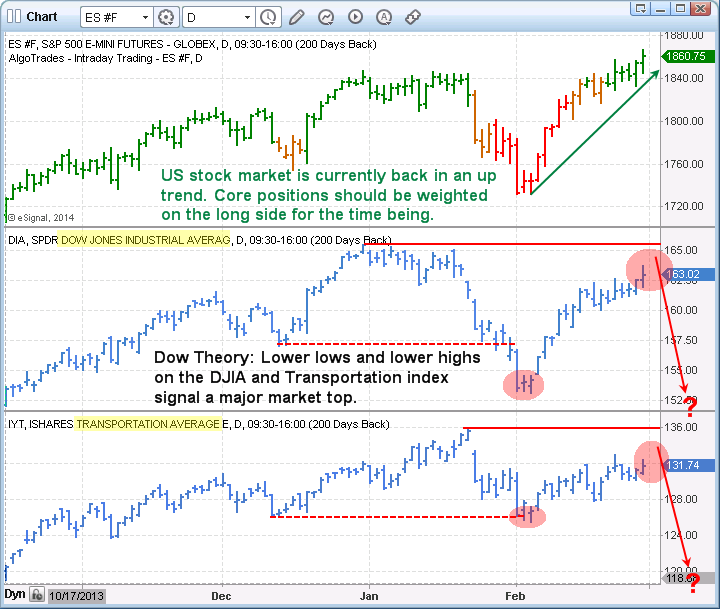

Over the past few weeks I have been watching the DOW and Transportation index closely because it looks and feels like the Dow Theory may play out this year and the stock market could take a 15% haircut.

Over the past few weeks I have been watching the DOW and Transportation index closely because it looks and feels like the Dow Theory may play out this year and the stock market could take a 15% haircut.