A small-cap company sitting on a massive field with potentially several billion barrels of crude oil has caught the attention of Keith Kohl, managing editor of Energy & Capital.

Again, I want to apologize for getting that wrong. Torchlight isn’t sitting on a billion-barrel field.

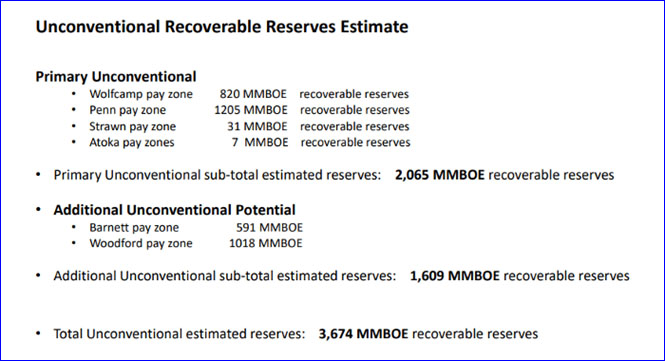

It’s actually 3.7 billion barrels of recoverable hydrocarbons.

Yes, you read that correctly.

Now, for those of you who were able to listen to the conference call on March 22, this blockbuster news won’t come as a surprise. If you weren’t able to catch that call, I highly recommend you listen to a replay of it. It was an extremely detailed presentation, and you can find a full re-cast of it right here.

So let’s have a quick recap

Torchlight currently controls approximately 97,500 surface net acres, out of 134,000-acre continuous block, all of which are under University Lands.

Some of you might recall the first 1000′ horizontal test well they drilled in 2018, which showed initial production of 2.2 million cubic feet of natural gas per day, and had a sustained rate of 1.2 million cubic feet of natural gas per day. The company holds a 72.5% working interest, and so far has drilled five pilot wells that have been instrumental in evaluating the Orogrande Basin’s potential thus far, and proven the play has a working petroleum system.

One interesting note you may see is that roughly 2 billion barrels of oil equivalent (2000 MMBOE) is located in just the Wolfcamp and Penn pay zones! Below, you can see a slide straight from the company’s presentation that breaks down these recoverable reserve estimates:

So, in addition to the Wolf-Penn potential, Torchlight has more than 1600 MMBOE of additional unconventional reserves that are considered recoverable.

Keep in mind that the Orogrande is more than just an unconventional play. This play also has areas with potential conventional pay zones, and Torchlight has confirmed the existence of structural pay and potential 4-way closures/fault closures (a structural feature of conventional pay zones) through its first vertical test well testing the structure, as well as the 2D seismic, gravity and magnetic information available.

In fact, that work shows potential of up to 20,000 acres of multiple conventional structural features. Factoring in both the unconventional and conventional resources at play, we’re talking about an absolute mind-blowing amount of hydrocarbons.

Remember, the U.S. Geological Survey’s (USGS’) most recent oil assessment in the Permian Basin pegged the amount of undiscovered, technically recoverable reserves in the Wolfcamp and Bone Spring formations at 46.3 billion barrels of oil.

Since the USGS assessment is based on public data in the Midland and Delaware basins, it didn’t factor in the potential of the Orogrande!

THAT, dear reader, is why we’ve been targeting trades in this area.

Furthermore, I completely agree with Torchlight that Texas will become the world’s new swing producer.

So you’re probably asking, “Okay, so what comes next?” Well, the company has said that it is now moving into the sales process.

In other words, it may be time for the big fish to come and scoop up Torchlight, and deliver some potentially monstrous value for its shareholders. Over the short term, the plan is for Torchlight to continue to define the potential size and scalability of the Orogrande. However, let’s not forget the kind of attraction that the drillers have had over in the Permian Basin. My readers and I took a nice profit from Energen after Diamondback Energy shelled out $9.2 billion for the company in 2018.

Just to give you an idea of some of the deals noted on the conference call, consider that WPX paid $2.75 billion to acquire RKI, or that Encana shelled out $7.1 billion for Athlon to help boost its presence in the Permian Basin.

Of course, Exxon paid $5.6 billion back in 2017 to double its Permian Basin resources.

Remember that as I write this, Torchlight is only trading with a market cap around $75 million.

Now it’s time to take the next step…

The company announced recently that it had made seven individual presentations to publicly traded industry majors and private equity-backed firms. Granted, they won’t tell us who they’re speaking with, but they’ve said that these potential buyers range in size from an enterprise value between $400 million and over $100 billion.

Truth is, Torchlight is sitting on a lot of oil, no matter how you look at it.

And Occidental’s $55 billion acquisition of Anadarko may have paved the way for more high value deals West Texas.

I told my readers at the end of 2018 that the harsh selling that took place was a strong buying opportunity for us.

And I was right

Shareholders saw their position explode 212% higher between December 24th and April 8th.

I think the latest sell-off is an even bigger opportunity for investors. You see, this time around we KNOW the potential size of the Orogrande play is absolutely massive. I wouldn’t expect companies with enough of cash in the bank or treasury stock to overlook a fresh 3.7 billion-barrel field.

And now that Torchlight is officially courting potential suitors, and whoever takes them to the prom may end paying a hefty premium to do so.

If you’ve been looking for a strong trade that the market hasn’t quite caught onto yet, Torchlight is it.

Investors interested in learning more can find Keith’s latest energy trades at Energy Investor and Pure Energy Trader. Request Information

Keith Kohl is the managing editor of Energy & Capital, an independent research service that focuses primarily on opportunities in the world’s energy markets. Kohl shares his vast knowledge of the global energy complex and the unprecedented opportunities offered in those markets with members of Energy Investor and Pure Energy Trader.

Disclosure: 1) Keith Kohl: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: I am a shareholder of Torchlight Energy Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company currently has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Torchlight Energy Resources. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Torchlight Energy Resources. Please click here for more information. An affiliate of Streetwise Reports is conducting a digital media marketing campaign for this article on behalf of Torchlight Energy Resources. Please click here for more information.

3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Torchlight Energy Resources, a company mentioned in this article.

Maurice Jackson of Proven and Probable and Rick Rule of Sprott USA engage in a wide-ranging discussion covering Pareto’s law, the importance of courage and conviction in investment, copper, mentors and the upcoming Sprott Natural Resource Symposium.

Maurice Jackson: Joining us for conversation is legendary investor Rick Rule of Sprott USA. Mr. Rule, welcome to the show. In our interview last month, we addressed a number of topics regarding where and what Sprott USA is focusing their attention on in the natural resource space. And at the conclusion of the interview, Rick, you stated that we should discuss Pareto’s law, which is known as the 80/20 law. But you put an interesting perspective on the law that I had not considered. Mr. Rule, expand the narrative on Pareto’s law and please introduce us to the concept of the 4%.

Rick Rule: Sure. And actually I’ll take a little further than that with your permission. Most people have heard of the 80/20 principle, which suggests that in any sort of major field of human endeavor, 20% of the people engaged in that activity generate 80% of the utility. In other words, 20% of the people do 80% of the work.

This turns out to be, broadly speaking, true. And it was pointed out in social sciences by an Italian social scientist at the turn of the last century named Pareto. Hence it’s called Pareto’s law.

It’s appropriate to junior mining speculation because among other things, the performance dispersion curvesthat is, the performance of relative management teamsaligns well, meaning that 20% of the management teams in junior mining generate 80% of the money made.

What’s important for readers to understand is that if you take that successful population, the 20%, and you run them through the same performance dispersion curve, they conformably align. Meaning that 20% of the 20 do 80% of the 80. Or 4% of the population base generates about 65% of the positive utility in the sector.

And I think it works for at least one more standard deviation, which would suggest that 20% of the 20% of the 20%, or eight-tenths of 1% generate about 40% of the total utility generated in the sector. Which is to say that one of the most important things that you can do as a speculator is identify and align yourself very patiently with the serially successful operators in the sector. And that is probably the most important work that you can do as a speculator.

That isn’t to say that identifying a Robert Friedland, or a Ross Beaty, or a Lukas Lundin, or a Bob Quartermain, is the only work you need to do. The truth is that when you buy stocks that are headed by those people, you are still subjected to risk. You’re still subjected to volatility. You’re still subjected to the vagaries of exploration.

But your most important task is to identify the serially successful peopleparticularly identify the serially successful people in bad markets where you don’t have to pay a huge premium to be associated with them. And then hang on for dear life and let them work their magic over time.

Maurice Jackson: We brought you on today to share some of your golden nuggets of wisdom for those of us that ascribe to join you with the serially successful. Now you’re famous for stating you must have courage and conviction, which is a critical distinction you’ve mastered. Expand for us the psychology of courage, because this is a key attribute that you have.

Rick Rule: Well, it turns out it does take courage, Maurice. We were looking back over the exploration capital partnerships series, which is a series of investments managed by myself going back to 1998. And we found, interestingly, that first of all, the vast majority of the money that was made was made in a relatively small number of stocksones that increased in price 1,000% or more. Particularly where, of course, those investments were accompanied by warrants.

What was interesting was that despite the fact that we all want immediate gratification, the average holding period for a ten-bagger or 1,000% gain was almost five years. So one needs to be patient.

The courage comes in because almost every stock that we enjoyed 1,000% gain in, we experienced a 50% share price decline in at some point in time or another during our holding period for the stock.

The most dramatic example was the most successful stock that we speculated in during that period, which was Paladin Uranium. That stock was a bellwether in my career. We participated in a $0.10 financing, and I think it was probably 1999, when nobody cared about uranium. And we were rewarded for our contrarian genius by seeing the stock go from $0.10 to $0.01. That is, we experienced a 90% loss in the stock. When you experience a 90% loss, Maurice, there’s no such thing as a hold. It’s either a buy, or a sell.

Mercifully, we had the courage to reexamine our precept and determined that we were right, and the market was wrong. We did buy some more stock. And amazingly, over the next five years, that stock went from $0.01 to $10. Two times after the initial 90% decline, that stock fell by 50% or more.

So you had in the course of an almost fictionally good gain depending on how you count the start, $0.01 or $0.10 to $10. The initial test of courage came with a 90% loss, and there were two future losses in excess of 50%.

Similarly, Lumina copper backed by the serially successful Ross Beaty: We did the first financing, if my memory serves me well, at $0.50. And that stock ended up being liquidated in this series of seven transactions. I forget what the total was, but somewhere in the $140 range.

But either two or three times during the seven years that we held that stock, the stock declined by 50% or more. So it’s important that you understand that while price is interesting, price is only relevant to the extent that it varies appreciably from value, which means that you have to have an opinion as to value and an opinion as to the ability of a management team to continue to add value. Following price alone, if you experience a 50% decline and you assume as a consequence of that decline that there’s something wrong with the company, almost always you will be shaken out of circumstances that can give you a big gain.

And let me give you one further illustration, Maurice, that I think will amuse readers. We aren’t just talking about speculation in this context. Warren Buffett, the legendary investor and CEO of Berkshire Hathaway, points out that four times during his stewardship of Berkshire Hathaway, arguably the most successful investment company in the history of American investingfour times during his tenure, the stock has fallen by 50% or more.

Now interestingly, if you examine a price chart of Berkshire Hathaway going back to 1968, from 1968 until present, those 50% declines relative to the share price escalation can’t even be seen on the stock chart. They’re invisible because the stock has moved so much over 40 years. But if you experienced those 50% declines at the point in time when you experienced them, they still caused you trouble. So I think that’s where the courage comes in.

Maurice Jackson: And before we leave courage, does the thesis, or is the scenario, very similar with uranium and copper today?

Rick Rule: Well, I think it is. If I’m understanding the question correctly, the courage associated with commodity markets is that the real money is made by buying industries that are, in effect, in liquidation. And that does take special courage. Certainly, if you looked at the uranium business today, the industry suggests that the incentive price to produce uranium, including prior year write-downs, which the industry never likes to talk about, and cost of capital, is about $60 a pound. So you make the stuff for 60 bucks a pound and you sell it for 27. You lose 33 bucks a pound, a 100 million times a year. And that takes some courage. Buying companies that have no probability of making money at the current commodity price requires courage. Some would say it requires insanity.

The difference, I think, between courage and insanity is simple arithmetic. Uranium, even in the United States, a wealthy economy that allegedly can afford alternatives, generates about 15% of our base load power. So it seems to me that the equation around uranium is that in the next six or seven years, either the price goes up to the point where the industry stays in business, or the lights go out. Those are your two choices. There is no way to replace 15% of base load electricity supply with any form of electricity in the next six or seven years.

So the courage comes into play and displaces allegations of insanity, I think, when you recognize that if you have the courage to speculate in an event that has to happen, but where you’re just not sure when it’s going to happen, it’s still a rational activity.

Maurice Jackson: And how about copper as well?

Rick Rule: Copper’s more interesting. There are plenty of companies that make cash at $2.75 per pound ($2.75/lb) copper, but the incentive price for opening new copper mines is more like US$3.50/lb. And US$3.50/lb, because it’s a capital-intensive business, assumes the artificially low interest rate environment that we’re living in today. If you had market interest ratesthat is, if the prime interest rate was at 5%, or 6%, or 7%the incentive price to produce copper would be up in the four or four and a quarter range.

Now if the world economy doesn’t soften substantially, and I don’t know if it will or it won’t, the copper price will go higher, because on a global basis, we are living off of copper deposits that were discovered 30 and 40 years ago and put into production, in most cases, 20 to 30 years ago. Deposits are very long of tooth. The great deposits in the world, like Bingham Canyon, have been operating for 100 years, Chuquicamata 100 years, Freeport-McMoRan Inc.’s (FCX:NYSE) Grasberg deposit, 40 years, Escondida 30 years. These are very, very, very long of tooth. And we aren’t developing new copper deposits because we’re not at incentive price.

So supply is going to be constrained in the copper business. The fly in the ointment here, Maurice, is if the economy does slow down, and I’m not saying it will. I don’t know. It could be that demand for copper declines a little bit too. I’m willing to take that bet, because my suspicion is that the ascent of man continueshat is, the billion and a half people at the bottom of the demographic pyramid continue to get richer, and continue to urbanize. And the consequence of urbanization is intensive use of electrical power, which requires lots of copper.

So my supposition is that even in an economic decline, that demand for copper will be surprisingly resilient because of its utilityand particularly, its utility to the poorest 20% of the people on Earth.

Maurice Jackson: How does the application of conviction fit into this narrative?

Rick Rule: Well, first of all, one needs to become educated enough that one can have conviction. The suggestion that I’ve made on your show so often is that one must be a contrarian or one will be a victim. That bear markets are the authors of bull markets.

My conviction with regards to that, Maurice, was born simply of experience. I’ve been in this business almost 45 years, and I’ve been through, depending on how you count, five cycles. And I understand the capital intention, the cyclical nature of the mining business. And I know very well by now that bear markets are the authors of bull markets. One of the things that gives me conviction that this market will turn is that that is simply the nature of markets for things like commodities, which are essential to mankind.

Other examples of conviction have to do with the intelligent application of science. If you have been around geologists and geology for a very long time, you begin to understand, first of all, what a good geologist is relative just to a geologist. And you understand what good geology is. And good geology overcomes a lot of sins. Market sins, management sins, all types of sins.

So I think that conviction is the conjunction of experience and education, which, while they’re related, are not the same thing. Having the education to understand the value of various inputs, and having the experience to have, in your past, seen outcomes associated previously with the same type of experiences that you’re having today, gives one conviction.

I guess, in my case, the third factor in conviction is having experience with people and teams. I have a high degree of confidence that if I go into a business with a Robert Friedland, or Bob Quartermain, or Ross Beaty, or Lukas Lundin, as a consequence of their past performance, I have a lot of conviction that, if I support them and stick with themif I’m patientthat I’ll have a happy outcome. And that’s really born of experience.

Maurice Jackson: You touched on science, but how about philosophy? How does that factor into your decision-making process?

Rick Rule: Well, I try not to let it enter in too much, to be honest with you. I try to be mathematically and empirically based. The truth is, in terms of philosophy, my own political philosophy is very much libertarian and free market oriented, which means that I’m always a sucker for the gold bug pitch. The consequence of that is that I try not to listen to my philosophical side as often.

Now, related to a libertarian philosophy is an acceptance of the precepts of Austrian economics and, in particular, the predictions with regards to the activities of markets and groups of people that was evidenced by Ludwig von Mises in Human Action. I would say, in that sensethe understanding of economic cycles and the understanding of the impact of cycles on human actionthat that part of my investing philosophy has been absolutely instrumental to my success.

Von Mises points out that although all of us believe ourselves to be rational fact-gatherers, that’s not what we are. We have a view of ourselves as impartial observers that gather information, hither and yon, and process it in a rational fashion. But that’s not what we do, in fact. We gather information that is convenient to our prejudices and our paradigms, and we use the information that we gather to support those same prejudices and paradigms.

Von Mises also points out that our expectation of the future is set by your experience in the immediate rather than the distant past, which is why bull markets go on longer than they should and why bear markets go on longer than they should. If you have done lots of work around an investment or speculation and you’re attracted to it, but your experience in the last five years has been that you get spanked for all your hard work, you tend to be cautious and conservative in bear marketswhich is precisely when the markets are cheapbecause your most recent experiences have been bad rather than good.

Conversely, in bull markets where stocks are doubling and tripling for no reason, you do two things. You confuse a bull market with brains. That is, you assume that your good performance is in some way, shape or form due to your own efforts. And you also become less cautious. Your expectation for the future being set in the immediate past means that you’re irrationally bullish. Even in a market that’s up 400% or 500%, which is, as you know by now, Maurice, something that’s not an uncommon phenomenon in our sector. Yeah, I’ll leave it there.

Maurice Jackson: Well, Rick, this is great information. Here’s one that really I find attractive with your thought process here, because most people shy away from this. And it sticks with courage and conviction. You’re not afraid to put capital into companies that are in challenging jurisdictions, either through civil unrest or through a silent partner known as our benevolent government wishing to do some profit-sharing with your capital. Why is that?

Rick Rule: I’ll tell you why, Maurice. It’s not like I think Congo, or Russia, or Sudan, or Bolivia are the greatest countries on the face of the earth. I’m certainly cognizant of political risk. The truth is, however, that I’ve experienced lots of political risk in places that are alleged to be good. My worst personal experience with political risk was here in the People’s Republic of California. But I’ve also had money stolen from me by legislatures in places like British Columbia.

The truth is that investors who look like me, old and Caucasian, tend for some reason to believe that money that’s stolen from us in English, according to the rule of law, is somehow less gone. So I’m not afraid of bad jurisdictions, it’s just I’m also afraid of so-called good jurisdictions. And what I’ve learned is that in jurisdictions where capital feels comfortable, a lot more exploration has taken place, which means that the probability that I’m going to find a high-quality deposit in a jurisdiction that I’m also comfortable in is very low. The probability is that I’ll find the type of deposit that will give me the returns I’m looking for1,000% plusare much more likely to occur in jurisdictions that have not been looked at as thoroughly.

Perhaps my most important mentor in the 1970s told me that in exploration, money is made employing new ideas in old placesthat is, new technologyor old ideas in new places. But if you’re using old ideas and old places, you’re assuming that you’re smarter than everyone that came before you, which is usually an incorrect assumption.

So, as an example, investments around the application of new technologies like three-dimensional seismic measurement while drilling, and new fracturing and recovery techniques, have revolutionized the old oil fields of West Texas. That’s a new idea in an old place. But old-fashioned exploration technologythat is, projection of existing trends, things like thatwork well in places like Congo and Kazakhstan, places that haven’t been explored thoroughly for 40, or 50, or 60 years, as a consequence of challenging social, economic, and political circumstances. So I would say that while I’m certainly cognizant of political risk, I define political risk much differently than many of my competitors.

Maurice Jackson: May I ask, was that Mr. Lundin that you were referring to there?

Rick Rule: Although Adolf Lundin would have said exactly the same thing, the guy I was referring to was a man named Jack Brown, of a private oil and gas company called Wagner & Brown.

Maurice Jackson: Before we leave speculation, we have a subscriber that wanted me to ask you if you would share three junior exploration stocks in the gold sector that you like best.

Rick Rule: I’m not allowed to do that. I’m U.S.-securities licensed. And the consequence is that I can’t make anything that smacks of a recommendation to people whom I don’t know. I can repeat the offer that I’ve made on your show so many times, which is to evaluate people’s portfolio, rank people’s portfolio for them, if they e-mail it to me. But a general set of things that can be construed as recommendations is something that I can’t do. Is the person who’s talking particularly about precious metals?

Maurice Jackson: Junior mining stocks. Junior explorations stocks for gold companies.

Rick Rule: OK. If they’re for gold companies, I can tell you that I have been buying two recently. This doesn’t suggest that your subscribers should buy them. This isn’t a recommendation. This is simply a disclosure about two companies I’ve been buying. One is Pan American Silver Corp. (PAAS:TSX; PAAS:NASDAQ), run by Ross Beaty, which is down really substantially in price as a consequence of, I think, the market misunderstanding the acquisition of Tahoe Resources. And the other would be Sabina Gold & Silver Corp. (SBB:TSX; RXC:FSE; SGSVF:OTCPK), which is a very large project in northern Canada, which is access constrained, meaning that access to it is by a winter ice road. It’s a very large deposit that people are afraid of because they don’t understand when it’s going to come in production. But we see it as both a large and high-grade deposit that is highly likely to come into production.

It’s important that your listeners note that these are not recommendations. These are not suggestions. These are not tips. These are merely two companies that I have been buying.

Maurice Jackson: Well, Rick, thank you for sharing that. And Rick, speaking of gold, you’re a strong advocate for owning physical precious metals. But not in the context that we usually hear from those who advocate having physical precious metals. Why does Rick Rule own precious metals?

Rick Rule: Fear. I regard precious metals as insurance. And insurance, in particular, against political interference with living standards. I believe the most important determinantcertainly not the only determinant, but the most important determinantof the gold price is faith, or lack of faith, in the U.S. dollar as expressed by the U.S. 10-year Treasury, which is the world’s benchmark security. The dollar is very, very strong, despite historically low interest rates.

I think that’s partly about strong equities markets. I also think it’s about the relative weakness of competitors to the U.S. dollar. While I consider the U.S. dollar to be a flawed instrument, it is certainly a less-flawed instrument than the Japanese yen, the Chinese yuan, the euro, the Canadian dollar all of those. Doug Casey famously says that the U.S. dollar is the prettiest mayor at the slaughterhouse. That might be a bit extreme.

But I need to say that I’m less sanguine about the U.S. economy. I’m less sanguine about our balance sheet; $22 trillion in on-balance sheet liabilities and $100 trillion in off-balance sheet liabilities. And our ability to service those debts, given the fact that we’re running a federal deficit at a trillion and a half dollars a year. I have less faith in the U.S. dollar than many of my global counterparts.

And my suspicion is if you saw a circumstance where faith in the U.S. dollar began to roll over, as it did in 2001, the price response that you’d see in gold would be one where, even if you had a substantial holding of U.S. dollars in your portfolio, the money that you would make on your insurance policy, which is gold, could offset the money that you would lose in your U.S. dollar-based accounts. I see gold, myself, as a medium of exchange that’s simultaneously a store of value. And the consequence of that is that I own gold for insurance purposes.

Maurice Jackson: You’re also famous for saying that it is payment in full. Can you elaborate on that for us?

Rick Rule: I think that’s very important. The U.S. dollar is a promise to pay. It supposes that people will continue to accept it. Almost every fiat currency in history has always retreated to its intrinsic value, which is, of course, zero. If, as an example, rather than having U.S. dollars in your jeans, you had Venezuelan bolivars, you would understand the promise for what it was. Something that could be broken.

Gold is very different. It doesn’t rely on faith. Gold isn’t a promise to pay. It is, in and of itself, payment. It is an asset that isn’t simultaneously somebody else’s liability. And I think that’s very, very important. I don’t think, as an example, that you’re seeing the Chinese government, the Chinese Central Bank, buying gold because they like the chart. I think that you’re seeing them buy gold because they’re afraid that the U.S. government will use U.S. financial markets and U.S. dollars as a weapon in foreign exchange transactions.

And so the Chinese are lookingand I just point out the Chinese, others are looking the same wayto a medium of exchange that isn’t under anybody’s control and isn’t a promise to pay, but rather constitutes payment in and of itself.

It’s interesting to note, Maurice, that over the last couple of days in the news, you will see that Venezuela exported seven tons of gold to Uganda, and then apparently onto either Dubai or Turkey. A pariah state that can’t necessarily trade in U.S. 10-year Treasuries can trade, can buy and sell gold. But even more interestingly, apparently those gold bars date from the 1940s, and they were payment from the United States to Venezuela for oil that was sold in World War II, when the Venezuelans had some doubt as to the outcome of the war, and weren’t willing to take U.S. dollars for their oil. They were willing to take gold.

So even a creditor as strong as the United States has periods of time, has circumstances, where their promise, which is what their currency is, isn’t acceptable. But there hasn’t been a time in recorded history when gold wasn’t acceptable.

Maurice Jackson: Well, I tell you what, I’m loving the insights that you’re sharing with us. What do the current metal prices suggest to you right now?

Rick Rule: A mixed message, really. I think the very recent strength in the gold priceby very recent I mean the last 10 daysis a function of investors’ realization that the United States is unlikely to let the market dictate the interest rate. That is, society in the United States has decided that spenders should prevail over savers, and that the interest yield on the U.S. 10-year Treasury should be artificially lowered.

When the U.S. Fed does [this], it’s called quantitative easing. If you and I did it, it would be called counterfeiting. I think there’s a realization in the market that the United States government is at the very least considering another round of counterfeiting.

Now, in terms of counterfeiting, although the United States is a very competitive economy, we don’t lead in counterfeiting. In the Euro Zone, there are many countries that are already paying a negative interest rate yield. Euro Zone counterfeiting is much more pronounced, as is Japanese counterfeiting, then American counterfeiting. But, as you know, Maurice, we’re in an extremely competitive society, and we want to finish first at everything, even including the debasement of our currency. And the consequence of that, I think, is the very recent strength that you’ve seen in gold.

Maurice Jackson: And may I ask you this as well? We all have our favorites, but right now, what is your favorite? Gold, silver, platinum or palladium?

Rick Rule: For me, because I’m buying out of cowardice, it’s gold. I don’t necessarily think that has the most price upside. A speculator might look at silver, gold’s so-called ugly stepchild. The silver price moves after the gold price moves, but if past is prologue, moves further when it does move. So a fear buyer would be in the gold trade. A greed buyer might be in the silver trade. The silver trade is something I probably would have done in my twenties. The gold trade is something that I do in my sixties.

The contrarian, of course, would be in the platinum space. About 60% of world platinum production is uneconomic at present. Most of it is coming out of South Africa, a place that has its very own social and political challenges, which could disrupt supply. Note that I said could, not will.

So I think, as important as the attributes ascribed to each individual metal are, what’s more important is the investors’ needs and perceptions. Why he or she is doing what they’re doing? I have other ways to make money, which is to say, speculate in equities or participate in debt markets. For me, the principal utility in precious metals is for insurance, in effect, allowing me to sleep nights and stay calm.

Maurice Jackson: Rick, thank you for sharing your golden nuggets of wisdom. Let’s switch gears here. On the 29th of July through the 2nd of August, the Sprott Natural Resource Symposium will be held at the historic Fairmont Hotel in beautiful downtown Vancouver, British Columbia. Rick, introduce us to this world-class event and who will be some of the featured speakers at the symposium?

Rick Rule: Well, it’s going to be, in all humility, a spectacular event. Nomi Prins will be speaking, you know. She’s a veteran financial commentator, a veteran banker, an investment banker. Danielle DiMartino Booth, formally from the Dallas Fed, will be speaking. We’re bringing back, of course, Jim Rickards, Doug Casey, Steve Sjuggerud, Alexander Green; many of the gurus that have traditionally been so well received in the mining space.

But the part of the conference that I actually like the most is we’ll have a lot of speakers from the industryin particular, speakers who have passed the Pareto’s law test. Speakers who have built multibillion-dollar mining businesses from scratch. People whose experience building businesses has allowed them to become successful speculators too. And hearing from a business builder what he or she thinks are the important characteristics of success in the mining business is invaluable. Hearing Robert Friedland, who is the most successful exploration speculator of my generation, talk about the process of making money in exploration. Hearing Ross Beaty, who has built 14 successful mining companies, talk about how you build a successful mining company. That’s really where the rubber meets the road.

Another thing we’re doing this year, since all the guys I’ve talked about before are of my vintage approaching or past their sell-by date, is we’re bringing in some people in their thirties and forties who have already exhibited success, and who we suspect will be the mining titans of the future, so that investors can get to know the people who will make them as successful over the next 20 or 30 years, as I’ve been in the past 20 or 30 years. A lot of the success, Maurice, to people ascribed to me is really a consequence of my having identified and hung onto the Lundins, the Ross Beatys, the Robert Friedlands, the Bob Quartermains, the Clive Johnsons of the world.

It’s important that speculators and investors your age and younger find that next generation of superstar entrepreneurs. And we’ve tried to do the dirty work for people by assembling as many of the high-quality youngsters as we can in one place.

The other thing that’s really useful, I think, Maurice, is that you’re going to have 600 high net worth investors in one location. The idea that all of the knowledge in the room emanates from the dias is ridiculous. There are a lot of experienced investors there, including many mining industry professionals. And interacting with your peers, listening to the questions that they ask in workshops, watching the way that they react to presentations, is useful.

Finally, an important difference between our conference and every other conference that we know of, is that our attendees have told us that the exhibitors at our conference aren’t advertisers, which is how they’re regarded at most conferencesthat they are in fact investment opportunities or content.

The consequence is that if you are a public company exhibitor at the Sprott conference, you need to be owned in a Sprott-managed account. In other words, they have been vetted by us. That doesn’t, unfortunately, guarantee that every stock goes up. But it does say that we know enough about every exhibitor that we have our own capital at risk in them, which I think is really important criterion.

And finally, Maurice, if I can continue this commercial, it is possible to have fun in Vancouver. You’ve been there, you can attest to this. Vancouver is a beautiful city. The weather in late July, early August is sublime. Any investor who comes up there and doesn’t go on the attendee boat cruise with us needs his or her head examined. The hotel itself is within walking distance of 200 restaurants. And Vancouver’s an amazingly scenic city, with mountains rising above 6,000 feet from sea level right in front of you, and an embarcaderoa walkway along the waterwhere you will hear six, or seven, or 10 different languages spoken. It’s truly a spectacular place. And I think it’s going to be difficult this year not to make money as a consequence of attending the conference.

Maurice Jackson: Ladies and gentlemen, this is truly a world-class event, as Rick just shared. To purchase admission to the Sprott Natural Resource Symposium, visit our home page and simply click on the icon, and you’ll be forwarded directly to the registration tab.

We touched on philosophy earlier. A day after the symposium, you’ll be speaking at Capitalism and Morality, founded by a mutual friend of ours, Jayant Bhandari. I love the timing of the events. Rick, for someone new to Capitalism and Morality, what would you like to share?

Rick Rule: Well, it’s more philosophically oriented. Capitalism and Morality is a lot of fun. The Adrian Days, and the Doug Caseys, and the Maurice Jacksons, and the Rick Rules of the world, talking about issues that are mostly unrelated to money. I’m going to be very amused this year to be involved in public debate with my friend Jayant Bhandari, who is, you know, of Indian descent, and who is, of course, a viciously anti-Indian racist.

A white guy accusing a brown guy of racism at a public forum is only something that could occur in a libertarian or anarcho-capitalist event. I think it’s going to be a lot of fun. Not merely for that, but for people who have a philosophical or political interest, Capitalism and Morality is wonderful value.

Maurice Jackson: To register for Capitalism and Morality, simply visit our home page and right below the Sprott Symposium you’ll be directed to the registration tab. Sir, before we close, you referenced earlier a free grading of one’s natural resource [portfolio]. Fill us in on the details on that, please.

Rick Rule: Sure. That’s pretty simple. Your listeners who are interested in my opinion about their natural resource-related equity investments need only e-mail me, [email protected], with the names and symbols of their resource holdings in the e-mail text, not as an attachment. Remember, I’m 66 years old, and not always good at opening attachments. I will rank their holdings on a 1-to-10 basis and return those via e-mail. It’s something I frankly enjoy doing. I learn a lot by researching companies that I haven’t known as well as I should. So I look forward to conversing with your listeners, Maurice, and attempting to assist them with at least my analysis of their holdings

Maurice Jackson: And to assist in streamlining these e-mails, please make sure that you put in the subject line Proven and Probable. Last question, sir. What did I forget to ask?

Rick Rule: I don’t think much. I think we’re doing a reasonably good jobyou in particular, Maurice, picking up bite-sized topics to talk about. I enjoy talking about people. I remember we did that once before, two or three years ago. And I enjoyed the process and I enjoyed the product. So I don’t think we’ve missed very much. I also think we’ve probably worn out the audience, should we decide to prolong it at any rate.

Maurice Jackson: I don’t believe so, sir. For additional inquiries about Sprott USA and all their products and services, please visit sprottusa.com or call (800) 477-7853.

And as a reminder, we discussed physical precious metals. I’m a licensed broker for Miles Franklin Precious Metals Investments, where we provide unlimited options to expand your precious metals portfolio, from physical deliver, offshore depositories, precious metals IRAs, and private blockchain-distributed ledger technology. Call me directly at (855) 505-1900 or you may e-mail [email protected].

Rick Rule of Sprott USA, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. I’m a licensed broker for Miles Franklin Precious Metals Investments. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

We have tracked the U.S. Federal Reserve’s interest rates decisions for years. This week, the Fed once again decided to keep the funds rate unchanged. We expect the Fed to change course soon.

By Elliott Wave International

We have tracked the U.S. Federal Reserve’s interest rates decisions for years.

In December, we wrote an article titled “Interest Rates Win Again as Fed Follows the Market,” where we observed that although most pundits believe that central banks set interest rates, central banks actually follow the freely traded bond market in their rates decisions.

We noted that the December federal funds rate hike followed increases in the three-month and six-month U.S. Treasury bill yields set by the market.

In March, we pointed out that the Fed followed the market yet again. T-bill rates had gone sideways since November, and the Fed correspondingly kept the federal funds rate unchanged.

This week, the Fed once again decided to keep the funds rate unchanged. We expect the Fed to change course soon.

The chart shows the fed funds rate (red line) and the yield on both 3-month and 6-month U.S. T-bills (yellow and green lines, respectively). The latter two rates are freely-traded, while the former rate is set by the Fed. Observe the growing gap between the yield on short-term T-bills and the present fed funds rate. The market is leading the Fed to lower its fed funds rate.

The same behavior occurred in 2007. By June 18, 2007, the 3-month U.S. T-bill yield had declined to 4.52% since trending sideways after the Fed raised the fed funds rate to 5.25% in June 2006. The market was leading the Fed to cut rates. The spread between the two became even wider, and at its September 2007 meeting, the Fed finally acquiesced to the market and lowered the funds rate from 5.25% to 4.75%. The Fed chased T-bill rates lower in a series of rate cuts all through 2008, finally dropping the fed funds rate to 0.25% in December 2008. Meanwhile, the DJIA declined more than 50% during the entire episode, highlighting the central bank’s impotence in controlling markets.

Based on current dynamics, the market is signaling that at some point in the coming months, the Fed will lower its Fed Funds rate to align with T-bill rates. We’ll be watching.

This article was syndicated by Elliott Wave International and was originally published under the headline Elliott Wave: Market Signaling Fed to Cut Rates Soon. EWI is the world’s largest market forecasting firm. Its staff of full-time analysts led by Chartered Market Technician Robert Prechter provides 24-hour-a-day market analysis to institutional and private investors around the world.

Precious metals expert Michael Ballanger looks at the recent run-up in gold and reveals his recent trades.

I am so confused tonight that I had to crowbar the booze cabinet in order to calm my scrambled soul and ease the pain in my pseudo-analytical chest. That’s right. “PSEUDO” as opposed to “QUASI” and as opposed to “FAUX.” The latter two adjectives imply vagueness and deceit and I would expect that my ramblings are a far cry away from vague and, despite the fact that I spent thirty-seven years employed peddling securities to people, certainly not with “deceit.” Well, maybe a tad of deceit but never of my making and always with honorable intent. Then again, deceit is deceit and it might take a hard look into the inner workings of the mirror to honestly decipher “intent.” Outcome and impact are far better conditions to observe in order to make any semblance of “moral judgement” so I beg you all to be the final arbiters of this tripe.

What sent me into veritable agony was the ease with which the surgeons of market operations were able to pivot from “fiscal integrity” to “monetary irresponsibility” with nothing more than a “written statement” and a “rehearsed press conference.” Every single Federal Reserve Board “event” is rife with drama, suspense and the inevitability of surprise, but not this one. It was carefully scripted, cautiously crafted, and magnificently delivered by a man who claims that the current POTUS has no authority to “fire” him. The result is that we have just entered into the Twilight Zone of pre-election politics with the “mightily revered stock market” as the scorecard from which the U.S. voting public will decide. You will recall that in all elections prior to the Millennium, GDP and employment numbers were all that mattered while the stock market averages were a mere yawn on the face of John Q. Well, welcome to the world of instantaneous satisfaction, delivered by others and appreciated by none. The scorecard has been now officially rendered: Speculators 10, Savers 0 (as in a great big fat ZERO). No need to ever again shop the oh-so-trustworthy banks for a “competitive rate”; they have been ordered to screw you by taking your savings with a positive-return “teaser” with the full knowledge that in due course, you will be paying THEM for the privilege of using their “services,” which is capsulized by the term “usury,” which is a felony in most countries.

We, as a global money-changing populace, are now officially embarked upon the ultimate fiscal and monetary voyage of “Spin ’til you Win” processing; it is government officials telling you upon which horse to bet, which lottery ticket to own, which roll of toilet paper to buy. It is about everything about to which Ayn Rand objected; she wrote “Atlas Shrugged” in 1957 and spoke of “totalitarian capitalism” where citizens were no longer assisted by government but where government DEMANDED the assistance (obedience) of its citizens, resulting in a total and complete breakdown in cause-effect outcomes. Anyone who has never read the book has zero knowledge of the significance of what this Russian Jew told us. Her father, well-trained in free market capitalism until 1917, had his business taken from him by the Bolsheviks in the year after the revolution, the impact of which prompted his daughter’s masterful work. It is now far beyond the time that citizens of North America demand that our elected and non-elected “officials” step up to the plate of fiscal integrity and swing the bat as opposed to hiding from TV cameras and radio microphones and every other type and sort of digital sound byte audit trail. Elected officials absolutely MUST defer from any person representing the banks because the Canadian banks are the financial valets for the government; bankers and government bureaucracy are like moss and lichens: they are completely dependent upon one another and represent the true and final definition of the “symbiotic relationship,” where both parties are totally reliant upon one another for survival.

Speaking of co-dependence, gold and uncertainty used to enjoy a wonderful symbiosis; in the 20th century, every time a saber rattled, the gold price shot up and took gold miners and gold explorers along for a wonderful ride, and every time that peace was celebrated, it declined. It was only in the 1970s with the oil shock that people actually began to understand the relationship between oil and cost-push inflation. A higher gasoline price was the primary component of consumer inflation and when the supply of gas at the pumps in Des Moines, Iowa, and Little Rock, Arkansas, and Stockton, California, became non-existent, creating huge lines of cars waiting for fill-ups, then and only then did the American public arise from the post-WWII slumber upon which the media and politicians dwelled until the Vietnam War defeat cemented the definition of failure, so alienated from the American conscience until then.

Here in the very early days of summer 2019, we have a rocketing gold price and an elevated stock market. We have trade wars and partisan battles and those that would have us eagerly believe that all is well in the world of “Growth” and “Productivity” and “American Capitalism” have pulled out all the stops to ensure that stocks continue to fuel the lifestyle requirements of the elite classes. As much as I detest the methods used to create asymmetrical wealth by way of rising equity values, I sit back in awe of the sheer genius behind the execution whether from the central banker news cycle management to the FOMC drumrolls to the financial media coverage finally resting with the futures markets interventions which conveniently and collusively confirm that every bullish murmur uttered by POTUS, Mnuchin, Jay Powell, Mario Draghi, Kuroda, Leishman, Santelli, and finally, Jim “BUY,BUY,BUY” Cramer must absolutely be true.

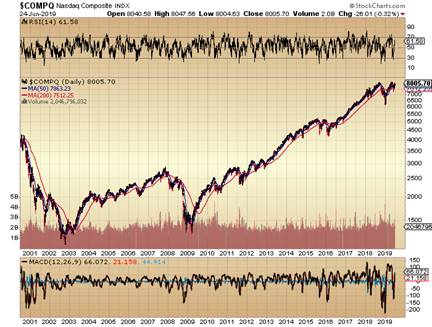

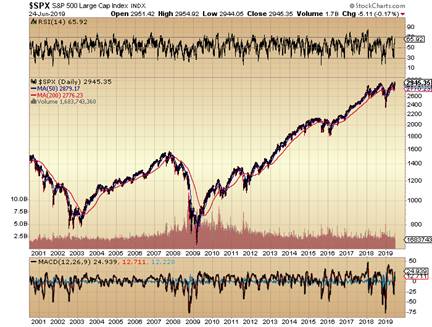

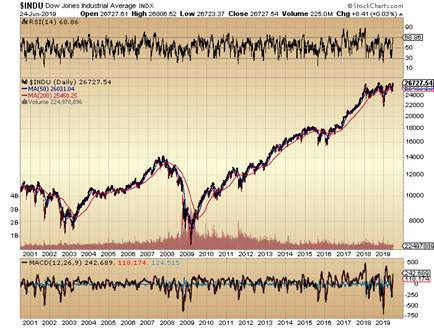

As a result, I present the first of a series of charts. First and foremost resides the reigning heavyweight champion of the financial world, the mighty NASDAQ, replete with every wild-eyed IPO-runner on the planet and the birthplace of every great technology company of the past fifty years. Beside it is the chart of the S&P 500, the index most representative of the broad market and its performance has been utterly magnificent. The last bastion of conservative companies is the Dow Jones Industrials and one glimpse at all three as they are presented below gives you all that need; they are all governed by the same master and that is why they all look so much alike. Those three charts are the hideous horns of “managed capital markets” where only the privileged few are allowed unblemished entry into “the club.”

Ladies and gentlemen, the charts posted above are 20-year charts that clearly show how effective the price management doctors have been in ensuring the patient’s health. Just as an aging superstar is forced to listen to his doctors, these aging bull markets have been attended to better than Bobby Orr’s knees, Whitey Ford’s elbow or Mickey Mantle’s liver. These are masterfully painted charts and they embody the highest order of excellence and vigor in both their form and their symmetry, and it is the word “symmetry” that has, over the years, sidled me with Bobby Orr’s knees (from kicking the dog), Whitey Ford’s elbow (from throwing far too many quote monitors from the 9th floor window), and Mickey’s eviscerated liver (from over-medication brought about by maniacal frustration) all the result of government intervention in our once-sacred FREE capital markets. Now, does ANYONE, ANYWHERE, for as much as a New York minute, believe that the charts shown above represent “FREE” capital markets? It is as if we are looking at three sisters, all less than a year apart, and all daughters of the greatest plastic surgeon in world history. They all appear youthful and spry with vivacious smiles when in reality they are old and saggy and very frail, filled with steroids and opioids and sedatives and tranquilizers all designed to make all around them feel happy and SAFE in their presence. In reality, they are clinging to life because their bankster doctors have no other recourse than to administer meds they surely know shall kill the patient.

Now, the charts posted below are of a shorter-term duration than the equity charts shown above but the intent is to define where we are in entry-point analysis. As I have boasted about since late 2015, the birth of the “New Bull Market in Gold” occurred in early December 2015 with the miners following in January 2016. You can see most clearly the unmistakeable bottom in the metal but you really don’t see the bottom in the miners until a month later. Importantly, those investors (like me) that were long (and levered up to the small intestine) were able to get that first double off the lows in unimaginable speed. It was on April 25th of this year that I posted a chart of the JNUG at $6.35 with the annotation that it “could be the bottom” only to watch it close on Friday at $12.70. However, of utmost importance to all is a) what to do with the basket of gold stocks we owned BEFORE the rally and b) what to do if we had NONE and want to own SOME. Well, turn off your TVs and block your gold bull Twitter feeds and try to think and process the charts on your own and by yourself.

Before I explain the obvious caution I am advocating in the arrow and dotted lines in these charts, be it known that the explosion in RSI levels, which has taken my beloved gold and gold miners to record RSI levels, is emphatically bullish from both sentiment and technical perspectives. Massive changes in DESI (not shown here) and RSI are incredibly bullish inputs to the monthly charts and to the weekly charts BUT (and I shout “BUT BUT!”) they are NOT telling you to load the gun tomorrow. I have liquidated all of my late-April leveraged gold positions (GLD calls, NUGT, JNUG) while retaining all non-leveraged ETF positions (GDX, GDXJ) and getting whacked for a 0.1% portfolio hit on DUST and a 0.07% hit on the GLD puts. Make NO mistake; when the RSI went into the 70s 10 days ago, I was taking profits like a drunken sailor with 40% gains across the board on the leveraged gold miner ETF’s and as I look back, I was in error. I THOUGHT I was going to be a “legendary timer” in the call but you just know that just when you think you are the next coming of Nostradamus, you wind up as “The Simpleton of Saint Pierre” and wind up in well off the beaten track, at least for a while. The impact of the jump from RSI 72 to RSI 85 was significant in that it took many of the positions up another 30% from my exit level. AS much a bummer as it was, you will recall that the only reason the GGMA portfolio outperformed the S&P in the past 24 months is that I used RSI and the COT report to avoid the drawdowns that have been horrific for long-term portfolio managers dealing specifically in gold and gold miners.

Listen carefully: Gold has been in a bull market since December 2015. It has been experiencing a series of higher lows and higher highs since 2016 and has slowly decoupled from the trend of the U.S. Dollar Index. It is now unarguably in a MASSIVE bull uptrend called to the exact DAY by this publication 3.45 years ago; it is today in a feeding frenzy mania of buying from generalist portfolio managers following the likes of Paul Tudor Jones, Ray Dalio and Stanley Druckenmiller. Despite all of that, I urge you all look at the charts posted above and ignore all of the “I told you so” rhetoric you’re now hearing from the gold newsletter crowd. The metal (which I love) and the miners (which I adore) are in the singular most overbought position EVER. I advise that you take profits on 50% of your holdings NOW while getting ready to sell the balance at HUI 205 (now 195). I swore I would never sell my physical metals back in 2009 and I will not; I will however put up 50% of the GDX @ $27 (cost $20.27) and 50% of the GDXJ (cost $30.22) @ $37.

These markets have now become unglued with the unbridled thirst for gold exposure and if you have never been exposed to “gold fever,” you have zero clue to which I refer. RSI readings above 80 are massively bullish when accompanied by sustained above-average volumes and there is no question that some very large unencumbered pools of capital have decided to descend upon our market like terminal predators, therein creating the problem for us all. Have these monstrous pools of capital finally decided to take on the bullion banks? IF (and that is a very large “IF”) they have, then we have a problem in that it is a problem based upon the definition of “infinity.” Since central bank liquidity has been proven to extend into “infinity,” where is the point where they are incapable of being issued a margin call? Better still, does the Fed “ever” get a “margin call” that requires a cash injection? We absolutely KNOW from experience that the average investor and the typical fund all get “calls” but if the bullion banks are short 500,000 August gold futures contracts, are they obligated to deliver if called? Or is it a “delivery notice” presented to the U.S. Treasury? This is what is going to emerge now that the CNBC mega-Titans have decided to engage. Whether or not you decide to invest, we are in a continuation stage of a massive bull market that began on December 4, 2015, and received validation when Jay Powell told the world that “Trump can’t fire me” in June 2019.

You all know where I sit on gold and silver; there is nothing more I can write that could convince you.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

Bob Moriarty of 321gold examines the potential of a new discovery in Ecuador.

Aurania Resources Ltd. (ARU:TSX.V) seems to have turned into one of those bad news/good news stories. Keith hasn’t found the Lost Cities Gold mines. Yet. However his team of crack geologists led by Dr. Richard Spencer may have stumbled across something a lot bigger and more valuable.

These sediment-hosted systems tend to be very big in lateral extent and rich. Much of the copper for the Bronze Age derived from Kupferschiefer mines in what is now Germany and Poland. Archeological artifacts from smelters and slag heaps indicate production going back as far as 4,000 years ago and written records date from 1199.

The KGHM Polska Miedz mining company in Poland ranks #8 in copper production worldwide and #6 for silver production. They are mining a Kupferschiefer copper/silver project.

These Kupferschiefer deposits were formed in shallow freshwater seas with lower saline-rich layers filled with hydrogen sulphides from rotting vegetation that dissolve the copper and silver from a mineral source. When those fluids combine with carbonaceous material in shales and sediments the copper and silver precipitate out of solution as copper oxides.

This is key for Aurania and Ecuador because these deposits tend to be so large. So far Aurania has tracked Kupferschiefer material as long as 22 kilometers (22 km) and 1 km wide. You can see in the picture above a classic Kupferschiefer material with over $400 rock. It’s oxide copper highly suitable for inexpensive processing with SX-EW techniques.

I would love to see Aurania and Keith Barron discover the Lost Cities and I have no doubt that in time they will. But if they screw up and stumble across a billion-dollar copper/silver prospect by accident, well, I’ll take that too.

The good news is that Aurania has a new highly potential target. The bad news is that big projects consume big money. Aurania is going to need to do a financing soon. I think the big boys understand that and are driving the share price down in order to get a lower price in a private placement. Not all sharks are found in oceans.

Aurania is an advertiser. I have participated in two private placements and will participate in more. I am biased, do your own due diligence.

Bob and Barb Moriarty brought 321gold.com to the Internet almost 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Aurania. My company has a financial relationship with the following companies mentioned in this article: Aurania is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of XXXXXX, a company mentioned in this article.

By CentralBankNews.info Iceland’s central bank lowered its benchmark policy rate for the second month in a row as a contraction in the economy is expected to become more obvious in coming months with the decline in tourism now seen deeper than previously expected. The Central Bank of Iceland (CBI) cut the rate on 7-day deposits by 25 basis points to 3.25 percent and has now cut it by 75 points this year following a cut in May when the outlook for the economy worsened sharply from a fall in tourism and a plunge in exports of marine products. Iceland’s economy expanded by an annual 1.7 percent in the first quarter of the year, the slowest growth since the first quarter of 2014 and line with CBI’s forecast from May when it slashed its outlook for 2019 output to a shrinkage of 0.4 percent from an earlier forecast of 1.8 percent growth and 2018’s robust expansion of 4.6 percent. Although CBI said the latest economic data do not change its view of the expected slowdown, domestic demand could turn out to be more resilient than assumed but “the outlook is for the contraction in tourism to be deeper than previously expected.” In May the central bank forecast tourist arrivals would drop 10.5 percent this year from 2018 due to the combination of a collapse of budget airline WOW, the impact of the strong krona, temporary strikes and uncertainty surrounding Icelandair’s use of Boeing 737 Max jets. Inflation is also largely in line with the central bank’s forecast that it has peaked and will decline toward the bank’s target of 2.5 percent during the year though a further decline in the krona’s exchange rate could change the outlook. “Inflation expectations have fallen since the MPC’s last meeting, and the monetary stance has therefore tightened again,” CBI said. Iceland’s inflation rate eased to 3.3 percent in June from 3.6 percent in May. After rising steadily from early 2015 to mid-2017 on Iceland’s economic boom, the krona has been dropping since April 2018 and was trading at 124.6 to the U.S. dollar today, down 6.6 percent so far this year. While the central bank acknowledged the economic contraction would present a challenge to both households and businesses, it said the economy was much more resilient than before and it has considerably more scope to respond to the weakening economy while proposals to ease fiscal policy will also pull in the same direction. The Central Bank of Iceland issued the following statement:

“The Monetary Policy Committee (MPC) of the Central Bank of Iceland has decided to lower the Bank’s interest rates by 0.25 percentage points. The Bank’s key interest rate – the rate on seven-day term deposits – will therefore be 3.75%.

The most recent data on economic developments do not change the assessment of the economic outlook as presented to the Committee at its last meeting. GDP growth in Q1/2019 was in line with the Bank’s May forecast; furthermore, a contraction in the domestic economy is still anticipated and is expected to show more clearly in coming months. However, stronger private consumption in Q1 and leading indicators could imply that domestic demand has been more resilient than previously assumed. On the other hand, the outlook is for the contraction in tourism to be deeper than previously expected.

As yet, inflation has been in line with the Bank’s last forecast. According to that forecast, inflation has peaked and will ease back to target as the year progresses. Further depreciation of the króna could change these prospects, however. Inflation expectations have fallen since the MPC’s last meeting, and the monetary stance has therefore tightened again.

Although the economic contraction will be challenging for households and businesses, the economy is much more resilient than before. Furthermore, monetary policy has considerable scope to respond to the contraction, particularly if inflation and inflation expectations remain close to the target, as is currently envisioned. The proposed fiscal easing will pull in the same direction.