The deal terms and the partner’s attractive attributes are discussed in an H.C. Wainwright & Co. report.

In a June 25 research note, H.C. Wainwright & Co. analyst Ed Arce reported that GENFIT SA (GNFT:NADSAQ; GNFT:EURO) outlicensed elafibranor for $228 million for development, registration and marketing in the Greater China area for nonalcoholic steatohepatitis (NASH) and primary biliary cirrhosis (PBC).

GENFIT entered into the licensing and collaboration agreement with Terns Pharmaceuticals Inc., a private company with locations in San Mateo, Calif., and Shanghai, China, that is targeting chronic liver diseases such as NASH, liver fibrosis and hepatocellular carcinoma (HCC).

Arce reviewed the terms of the agreement. Terns has the exclusive right to advance elafibranor in NASH and PBC. Should it commercialize the drug, GENFIT will earn royalties in the mid-teens on net sales.

Terns is to pay GENFIT $35 million up front as well as up to $193 worth in clinical, regulatory and commercial milestone payments. “The upfront payment from Terns serves to extend GENFIT’s cash runway by several months (more than a quarter),” Arce pointed out.

Both companies will conduct joint research and development projects in liver disease, concentrating on potential combination therapies for NASH of elafibranor along with one or more of Terns’ proprietary compounds. Terns currently has at least five of them targeting NASH. “Any resulting therapeutic treatment from this collaboration may potentially be commercialized worldwide,” noted Arce.

The analyst commented that “the deal checks a lot of the right boxes” in terms of Terns being a good match for GENFIT. Specifically, GENFIT selected Terns as a partner for a handful of reasons. Terns is an innovative company solely focused on NASH, has a broad pipeline in that indication and sees the value in combination NASH therapies. The company has a presence in both Northern California’s biotech center and in China and is backed by “a number of savvy, well-known biotech-specialist investors, including Orbimed, Lilly Asia Ventures, Vivo Capital and Decheng Capital.”

H.C. Wainwright has an Outperform rating and a $72 per share target price on GENFIT. The company’s stock is trading currently at around $19.87 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from H.C. Wainwright & Co., GENFIT S.A., First Take, June 25, 2019

Investment Banking Services include, but are not limited to, acting as a manager/co-manager in the underwriting or placement of securities, acting as financial advisor, and/or providing corporate finance or capital markets-related services to a company or one of its affiliates or subsidiaries within the past 12 months.

I, Ed Arce, certify that 1) all of the views expressed in this report accurately reflect my personal views about any and all subject securities or issuers discussed; and 2) no part of my compensation was, is, or will be directly or indirectly related to the specific recommendation or views expressed in this research report; and 3) neither myself nor any members of my household is an officer, director or advisory board member of these companies.

None of the research analysts or the research analysts household has a financial interest in the securities of GENFIT S.A. (including, without limitation, any option, right, warrant, future, long or short position).

As of May 31, 2019 neither the Firm nor its affiliates beneficially own 1% or more of any class of common equity securities of GENFIT S.A.

Neither the research analyst nor the Firm has any material conflict of interest in of which the research analyst knows or has reason to know at the time of publication of this research report.

The research analyst principally responsible for preparation of the report does not receive compensation that is based upon any specific investment banking services or transaction but is compensated based on factors including total revenue and profitability of the Firm, a substantial portion of which is derived from investment banking services.

The Firm or its affiliates did receive compensation from GENFIT S.A. for investment banking services within twelve months before, and will seek compensation from the companies mentioned in this report for investment banking services within three months following publication of the research report.

H.C. Wainwright & Co., LLC managed or co-managed a public offering of securities for GENFIT S.A. during the past 12 months.

The Firm does not make a market in GENFIT S.A. as of the date of this research report.

H.C. Wainwright & Co., LLC and its affiliates, officers, directors, and employees, excluding its analysts, will from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives (including options and warrants) thereof of covered companies referred to in this research report.

The reasons why this biopharma makes a compelling investment are outlined in a ROTH Capital Partners report.

In a June 18 research note, analyst Tony Butler reported that ROTH Capital Partners initiated coverage on Translate Bio (TBIO:NASDAQ), in advance of an anticipated Q3/19 data readout, with a Buy rating and a $25 per share target price. The company’s current share price is about $13.16.

Translate Bio is a Massachusetts-based company that is developing mRNA therapies for cystic fibrosis and ornithine transcarbamylase deficiency.

Butler listed the key attributes of Translate Bio that justify ROTH’s Buy rating on it. They are as follows.

1. The company has a solid platform based on a modular manufacturing process for its mRNA and lipid-based nanoparticle delivery vehicle. With it, Translate Bio can make new mRNA therapies and, therefore, easily venture into new indications.

2. The company’s lead clinical program, MRT5005 for cystic fibrosis, is in the multiple ascending dose phase of the ongoing Phase 1/2 study. Translate Bio is expected to report interim data from the trial in Q3/19.

3. The company has a beneficial agreement with Sanofi to develop up to five vaccines. The partnership should diversify Translate Bio’s pipeline and provide it with revenue. Sanofi already paid a $45 million upfront payment to the company and will pay up to $805 million plus tiered royalties.

4. The company is well funded through year-end 2020, well past the data readout, thanks to its recent raise of $47 million.

Butler explained that ROTH’s $25 target price is based on these assumptions: a 45% probability that MRT5005 is successful in adults and a 35% chance of success in 12 to 17 year olds, a 7085% penetration rate during the fourth or fifth year of commercialization and about $1 billion in risk-adjusted revenues in 2028.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Translate Bio, Inc., Company Note, June 18, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Translate Bio, Inc. and as such, buys and sells from customers on a principal basis.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Mike Gleason, Money Metals Exchange: It is my great privilege now to speak with Steve Forbes, Editor-in-Chief of Forbes Magazine. He’s a prolific author and also a two-time presidential candidate, having run in the Republican primaries in both 1996 and in the year 2000.

Mr. Forbes, I really want to thank you for your time today and for joining us again.

Steve Forbes, Forbes Magazine CEO: Good to be with you. Thank you.

Mike Gleason: A lot of gold has been flowing from West to East in recent years. That trend seems to have accelerated lately. What do you make of the growing central bank gold reserves, particularly in the East?

Steve Forbes: Well, the dollar is the currency of the world, just out of convenience and the size and importance of the U.S. economy. Our capital markets, for example, are much broader, deeper, sophisticated than those of any other country.

In Europe, for example, most of their capital still comes from large banks, one reason why they don’t have the vibrant smaller company sector that we traditionally have had in the U.S. But the flow of gold to Asia, part of that is hedging, and part of it too is, I wouldn’t be surprised if one of those countries doesn’t move towards more of a gold-based standard, monetary system.

Just the other day, the prime minister of Malaysia proposed a gold standard as a way of replacing the dollar, having gold-backed currency. If China did it, that would be an enormous change.

And so I think, one, they want the gold just as a hedge, but two, I think one of them may have the idea of going to a new gold-based monetary system, which would be good. The dollar needs the competition.

Mike Gleason: Do you look at that the rapid flow of gold to Russia and China as an issue of national security in the long run?

Steve Forbes: It doesn’t really matter who holds the gold. It’s a broad international market. Every ounce of gold that’s been mined is still with us on Earth somewhere.

And the national security comes from not somebody holding some gold but from the fact that we haven’t learned yet, even though we once knew how to do it, of a stable dollar, strong, stable dollar, which would be tying it to gold as we did under a gold standard right up until the 1970s.

We did it for 180 years, and it worked pretty well. So the threat is an unstable currency, not who owns particular pieces of gold.

Gold is like a measuring rod, a ruler. It just measures value. It’s not using gold coins to buy stuff at Walmart. It’s like 12 inches in a foot or 60 minutes in an hour. And it’s worked for 4,000 years when people have done it and done it right.

Again, in terms of the currency, we once knew how to do it. I think we can learn quickly how to do it again. If not, I’ll be glad to show them in my books. That’s the threat, is we have an unstable dollar, because it hurts us and the world.

Mike Gleason: U.S. Congressman Alex Mooney of West Virginia recently introduced a bill in Congress to eliminate capital gains related to sales of gold and silver. Give us your thoughts on that bill and the IRS rule that taxes nominal capital gains on precious metals, which the Constitution says is money.

Rep. Alex Mooney (R-WV) has legislation to end income taxes on gold and silver.

Steve Forbes: Well, if you buy, say, 10 $1 bills for a $10 bill, you would be very surprised if the government said, “Oh, you should pay sales tax on that purchase,” or something like that. So, what should be done is the capital gains levy should be eliminated anyway on all things, and it should be eliminated certainly on gold and perhaps sliver as well, because it hurts having an alternative currency.

Governments like to have monopolies, but the best way to have governments behave themselves is by people having an alternative.

I’m surprised the cryptocurrency world hasn’t come up with a stable cryptocurrency, but in the meantime, gold should not be subjected to capital gains tax. It should not be subjected to sales taxes, any more than buying 20 $1 bills should be subjected to a sales tax.

Mike Gleason: I’m curious, how do you view gold as an investment? Some also consider it more like an insurance product, financial insurance in a way. How do you view it in terms of an asset class or an investment?

Steve Forbes: Gold is an insurance policy. And you should have it, because you never know what our political leaders are going to do. Whether you’re comfortable with 5%, 10%, pick a number, but it should be there, even though people say well, other assets have done better over time. Well, that’s just a reflection of currency fluctuations.

Gold keeps its intrinsic value better than anything else. When you see the nominal price change, that’s not the value of gold changing, that’s the value of the dollar or whatever currency you’re talking about, changing in value.

Gold is the constant, like the North Star. Yes, you should have it, a piece of it, just for peace of mind.

Mike Gleason: In terms of precious metals, if we have an inflationary environment, if the Fed does get the inflation that they’re looking for, what is your outlook for precious metals over, say, the medium to long term?

Steve Forbes: Well, it’s very basic. Here you can really plot a curve. When a central bank undermines the integrity of its currency, hard asset prices go up. Precious metals have been doing that for long before any of us were born, or even our ancestors.

We know it’s going to happen. That’s why you have a little bit as an insurance policy. These people don’t know better.

Mike Gleason: Well, we’ll leave it there. Mr. Forbes. It was a real pleasure, and we wish continued success to you and Forbes Magazine and Forbes Media. Thank you for everything you do for the causes of freedom, capitalism, and liberty.

Steve Forbes: Thank you. Have a good one.

For the full transcript and audio of Money Metals’ recent interview of Steve Forbes, please visit this page.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

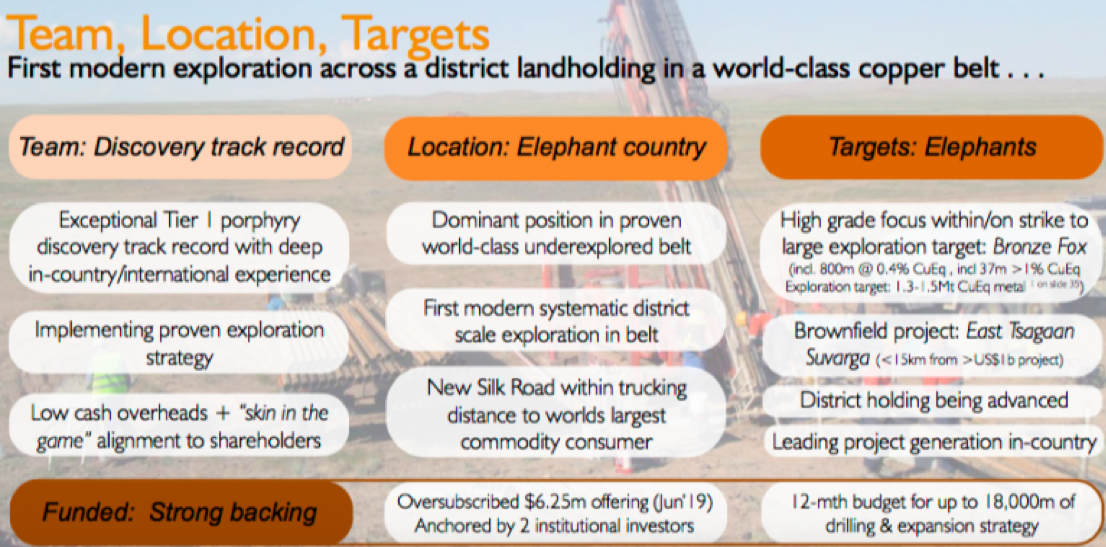

Peter Epstein of Epstein Research conducts an exclusive CEO interview with Sam Spring of Kincora Copper.

Kincora Copper Ltd. (KCC:TSX.V) fell off investors’ radar screens due to an extended period of inactivity in 2018, but now the company is cashed up, team in place, and ready for extensive drilling at five independent, large-scale porphyry targets with a 12-month funded budget for up to 18,000 meters (18,000m) of drilling.

Kincora has been operating in Mongolia for more than eight years. In 2016, the company secured unencumbered access to its promising Bronze Fox project and consolidated the dominant landholding in the Southern Gobi copper-gold belt, between and on strike with Rio Tinto Plc’s (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) Oyu Tolgoi (OT) copper-gold mine, and the Tsagaan Suvarga porphyry project, via the merger with IBEX, a private vehicle indirectly controlled by Robert Friedland.

This attracted a world-class technical team, credited with multiple discoveries of Tier 1 copper deposits, looking to repeat such successes. Since then, the company has been executing the first modern systematic exploration program across a district-scale landholding in a highly mineralized, but vastly underexplored copper-gold porphyry belt. Now, drilling is just days away.

These are exciting times for Kincora, the most exciting in the company’s history. The company is in a prime position in the copper sector where new discoveries are being well rewarded and successful juniors acquired at significant premiums. For example, just this week Australian-listed MOD Resources was taken out by a billion-dollar market cap, Sandfire Resources NL (SFR:ASX).

A new cornerstone investor, Hong Kong-based New Prospect, now the second largest shareholder with about 12% of the company, is a natural resource specialist fund with an extensive global network. LIM Advisors remains the largest investor: One of the longest operating alternative investment managers in Asia, they invest across the capital structure in deep value and special situations.

Investors in small-cap natural resource stocks know that the best time to be in a junior is right before a big discovery. That’s the time we could be at right now with Kincora. Management just raised $6.25 million ($6.25M). Will there be a new discovery! More than one!! None!!! Yes, there could definitively be zero new discoveries. . .This is a highly speculative situation, but backed by a team that has an excellent track record of large discoveries.

Even without blockbuster discoveries, the company has planned a very detailed and well thought-out drill program that’s sure to cover a lot of bases and provide a pipeline of news flow over the next 12 months. Raising $6.25M in a very tough market at a $7M pre-money valuation was a big success in and of itself, demonstrating the strength of management, the projects/targets and the massive opportunity.

The derisking capital raise is strong evidence of the belief by cornerstone investors and seasoned management that Mongolia is a great place to, potentially, make the newest globally significant copper discovery since 2014. To learn more, please continue reading this interview of Sam Spring, president and CEO of Kincora Copper.

Peter Epstein: Can you talk about how we got to the point of a substantial drill program starting very soon?

Sam Spring: After 2018 being a transitional year of setting the right corporate foundations for success, we are entering an exciting period where the drill bit will drive Kincora’s valuation once again. This month we will commence an aggressive, multiple rig, fully-funded drill program. The focus is discoveries on five large, independent copper porphyry targets on our 100%-owned Bronze Fox and East Tsagaan Suvarga (East TS) projects.

This will be the first drill program conducted by our industry-leading technical team, which has found multiple Tier 1 copper assets. For the last three years, we have undertaken the first modern, district-scale, exploration across this vastly mineralized, but significantly underexplored Southern Gobi copper-gold belt.

As readers may know, there are two large-scale porphyry projects in this region, Rio Tinto/Turquoise Hill Resources’ Oyu Tolgoi open pit mine and underground development project, and a privately-held open pit development project called Tsagaan Suvarga. We believe there are more globally significant copper discoveries to be found.

Limited drilling supports our Bronze Fox project potentially hosting an independently defined, conceptual exploration target of 1.3 to 1.5M tonnes (midpoint = 3.086 billion copper equivalent pounds). That would be an in-situ value of $11 billion (1.32 CAD/USD, US$2.70/pound copper).

The first hole of the program will, for the first time, correctly test a very large zone (previously drilled in the wrong direction). However, prior drilling still managed to intersect 37m at >1% copper equivalent (Cu eq), within 864m of 0.38% Cu Eq.

Our East TS project sits in the shadows of a billion-dollar open pit construction project at Tsagaan Suvarga (TS). Within this brownfield setting, we’re drilling three separate targets that are the closet analogues to the high-grade ore bodies at OT. . .since OT! While just targets, readers should understand that what we’re exploring for is large and in a very favorable location and geological setting. OT’s ongoing underground expansion is the largest hard-rock mining project in the world. It could become the third largest copper mine on the planet, with a 100-year+ mine life.

Kincora was formed in 2011, but we are in the strongest position today that the company has ever been in. Yet, our current market cap of $12M, (with $6M cash!) is a fraction of our peak valuation of nearly $50M. At that time, we had attracted a buyout offer for the company and had signed 14 NDAs (nondisclosure agreements) with interested parties.

While naturally I’m biased, I think it would be hard to find many juniors with similar risk/return profiles and multiple near-term catalysts, backed by a world-class management, board, technical team, advisors and key shareholders, trading at such a low valuation.

With the company shortly ramping up drilling of our existing exploration portfolio, and focused on ongoing expansion opportunities, Kincora is the most active foreign-listed junior seeking to make the next Tier 1 discovery in Mongolia.

Peter Epstein: You just closed on a $6.25M capital raise in a very difficult market. Who were the key investors in this very important round?

Sam Spring: About 60% was taken up by two large natural resource funds and associated groups, who will represent more than 40% of Kincora’s shares going forward. These groups, LIM Advisors and New Prospect Capital, are both Hong Kong-based funds and have a track record investing in Mongolia.

In total, there were about 30 investors in the deal, with strong board/management participation and good support from high-quality sophisticated investors. As you can imagine, given current market conditions, a lot of work went into this raise. We truly appreciate the vote of confidence from those who invested.

Peter Epstein: How much of that $6.25M will go toward exploration? Please describe the upcoming drill program.

Sam Spring: The vast majority will support Kincora undertaking the most aggressive exploration and discovery drill program anywhere in Mongolia this year. About $5M will cover up to 18,000m of drilling at Bronze Fox and East TS, plus project generation activities and advancing earlier-stage exploration targets.

Mongolia has unique geological potential to host globally significant discoveries, and that is what we are focusing on. This raising, with the accompanying warrant package, aligns our capital markets strategy with our exploration and expansion plans and gives us a good shot (but no certainty) at making new discoveries.

We are on record stating that these drill targets are as good as you get within a global setting for their respective stages. The key driver in the next 12 months is proof of high grade and our geological concepts, to confirm our models and interpretations with positive drill results.

Peter Epstein: In addition to your management team and board, please describe recent due diligence done by independent advisors, consultants and analysts. Didnt your largest shareholder also commission a study?

Sam Spring: Our drill strategy is the culmination of almost 30 years’ copper exploration experience in this belt by senior members of our team, five years of exploration work and model refinements by ourselves and previous owners (including Ivanhoe Mines Ltd. [IVN:TSX; IVPAF:OTCQX] and IBEX Technologies [IBT:TSX.V; ]) that provide us with strong conviction to focus on the selected five targets.

Kincora has been through five technical reviews since mid-2017, including from 1) a leading natural resource private equity group; 2) the European Bank for Reconstruction and Development (EBRD); 3 and 4) LIM Advisors (twice); and 5) New Prospect Capital, all of which have resulted in capital being invested.

As you have picked up on, Peter, our largest shareholder commissioned an independent technical review of our targets, work programs and strategy before becoming a cornerstone investor in our latest offering. This review suggested a discovery had already been made at Bronze Fox, within the underexplored target zone to the west of a key regional fault in an area we are calling West West Kasulu. This is where the first drill hole will go. In the independent consultant’s opinion, this target area has been significantly upgraded by recent exploration activities.

While we are optimistic, and management participated in the recent raising and have undertaken detailed systematic exploration, there’s nothing left to do but drill these targets. Please let me reiterate that Kincora is a high-risk exploration play. Hence, there are high rewards for success.

Peter Epstein: A risk is that it might cost tens of millions to delineate an attractive NI-43-101-compliant resource. What is your team’s goal for the upcoming drill program? Can you articulate what success might look like?

Sam Spring: Absolutely. We appreciate the fact that porphyries are capital intensive, and that exploration is very risky. More meters of drilling provide us a better chance of confirming our geological concepts and riding the value creation curve for shareholders.

The best recent example of a large-scale copper porphyry discovery is that of SolGold plc (SOLG:AIM) at its Alpala project in Ecuador. The deposit at Alpala is deep, so drilling costs there are significantly more than in Mongolia. In March 2016, SolGold raised AU$5.7 million at 2.3p/share, having drilled 13 promising holes and seeking to confirm its discoveryan equivalent drill program to what Kincora is now looking to complete at our two projects. They had fantastic results. . .Over the course of 31 months, SolGold drilled a further 54 holes, attracted both Newcrest Mining Ltd. (NCM:ASX) and BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK) as strategic investors, and rerated 20 time for shareholders.

That’s what success at the target-testing phase of drilling can result in, even in difficult capital markets and a flat/decreasing copper price environment, which we believe is temporary.

At Bronze Fox, our drill campaign is designed to advance the strike potential away from the fault to the west, demonstrate the interpreted, significant increase in tonnage and grade potential, and confirm a new discovery. Prior higher-grade intersections include three of four holes drilled by Kincora that returned >1% Cu and/or Cu eq, including the best hole, F62, which hosted 13m of 1.15% Cu/1.41% Cu eq, within 37m at 0.83% Cu/1.04% Cu eq and 864m at 0.38% Cu eq.

At our East TS, the geological concept we are seeking to confirm is that OT-style mineralization is present. Each of the three targets at East TS have large-scale potential, with individual coincident geophysical anomalies equivalent in size to ore bodies at OT and SolGold’s Alpala project.

While more conceptual and risky than the two targets at Bronze Fox, such a setting and scale of targets is unique. If located in more established copper districts around the world, it’s likely the area around TS and East TS would have already seen extensive drilling.

A rule of thumb for porphyry discoveries is that ~50,000m of drilling generally provides visibility for ~5M tonnes Cu eq metal. Exercise of the warrants that were part of the recent offering would bring in an additional $15M (2.5x the recent raising), and enable another 100,000 meters of drilling.

Peter Epstein: There are many copper bulls, yet the price at US$2.70/lb is half of what some bulls think is coming. Do you have a view on the copper price?

Sam Spring: A good question; we get asked that a lot. I will leave the forecasting to the experts, but we’re noticing that most investors see the writing on the wall. Like us, they believe the supply side will at some point (perhaps soon?) struggle to meet even average-trend demand growth, let alone any acceleration from increasing global electrification. This theme is being picked up by generalist investors as well, who have noticed what an unexpected supply shock has done to the iron ore price this year.

Regarding the industry players (mid-tiers and majors), there has been a notable, but quiet, shift toward looking at new growth projects again over the last 18 months. BHP and Rio Tinto are even talking about organic exploration success stories, focusing on copper as a preferred commodity for expansion. That said, we are just starting to see more of the traditional miners expand into earlier stage projects to rebuild their pipelines.

Time will tell, but I certainly think that even at current copper prices, if we find what we’re looking for, there will be significant interest in Kincora. A tailwind from rising copper prices would, of course, be welcomed, but given the lack of exploration success industry-wide, globally, for many years now, the project pipeline is in great need of new, sizable discoveries. That is what we believe Mongolia and our targets offer investors.

Peter Epstein: Please talk about Mongolia. Some readers probably won’t invest there. What do you tell investors, shareholders, prospective investorsabout Mongolia country risk?

Sam Spring: At the time I joined Kincora in 2012, Mongolia was the fastest growing economy in the world. This was driven by the first phase emergence of delivering previously untapped resources to international markets.

This emergence meant that at the time it was almost mandatory for coal and copper majors to be seeking entry into the southern Gobi regions, with product trucked to the world’s largest consumer of both commodities. We are five prime ministers, two governments, a number of high profile disputes and reversals to unfavorable investment laws later, but the rocks and big-picture potential remain unchanged.

In a landscape of few significant greenfield projects recently being commissioned, OT is proof of concept that Mongolia is a mature mining jurisdiction. OT is the largest development project in Mongolia’s history. It’s expected to account for up to a third of Mongolia’s GDP (gross domestic product) by the mid 2020s. It paves the way for companies like ours by lowering barriers to entry, and we and others greatly benefit from newly built regional infrastructure.

When one looks at other copper jurisdictions, it’s becoming harder and more expensive to operate. Chile’s 2018 copper output was greater than the second, third and fourth largest country producers combined. The multibillion-dollar capex profile for Chile’s Codelco, just to keep production flat, shows the increasing challenges regarding water, community relations and high altitude, not to mention a declining copper grade!

Many other large copper supply regions are also difficult and/or increasingly difficult to operate in; look at recent developments in the Democratic Republic of Congo, China, Panama, Russia, Zambia, Indonesia, Papua-New Guinea, etc.

Given the team and operational track record we have at Kincora Copper, we are eyes wide open to the risk/reward scenario in Mongolia, which we find compelling, exploring for the next globally significant copper discovery.

Your readers should stay tuned for drill results, which should start arriving in five to six weeks’ time. We expect results to be ongoing for the rest of the year.

Peter Epstein: Thank you Sam, I think we covered a lot of ground. Bottom line, drill results will define Kincora Copper going forward, and a lot of smart money is betting on good drill results between now and year-end.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Peter Epstein’s Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Kincora Copper including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Kincora Copper are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owns shares in Kincora Copper, and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes hes diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed above. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

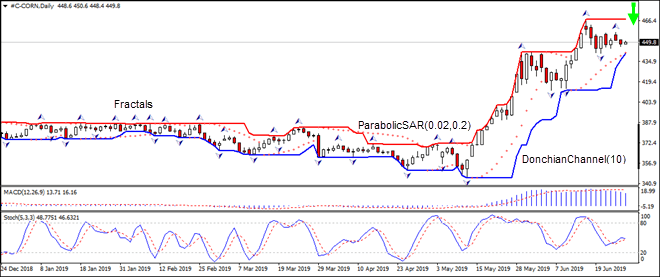

Drier weather across US Corn Belt this week will allow more planting of corn. Will the corn prices continue declining?

National Oceanic and Atmospheric Administration forecasts relatively drier conditions this week through July 2 across the upper Midwest and Corn Belt of US. Drier weather, which allows to plant more area when rains delayed plantings, is bearish for corn prices. At the same time the United States Department of Agriculture is expected to revise downward its estimate of corn planting area in annual acreage report due on Friday. This is an upside risk for corn.

On the daily timeframe the CORN: D1 is retracing lower after hitting 5-year high in mid-June.

The Parabolic indicator gives a buy signal.

The Donchian channel indicates uptrend: it is narrowing up.

The MACD indicator gives a bearish signal: it is above the signal line and the gap is narrowing.

We believe the bearish momentum will continue after the price breaches below the lower boundary of Donchian channel at 441.30. This level can be used as an entry point for placing a pending order to sell. The stop loss can be placed above the upper Donchian boundary at 467.40. After placing the order, the stop loss is to be moved every day to the next fractal high, following Parabolic signals. Thus, we are changing the expected profit/loss ratio to the breakeven point. If the price meets the stop loss level (467.40) without reaching the order (441.30), we recommend cancelling the order: the market has undergone internal changes which were not taken into account.

Later today we have one of the more important events on the economic calendar for the Mexican peso: the Bank of Mexico’s interest rate decision.

Just ahead of that we have the trade balance data, which might have a more muted reaction as traders await the more important event later. As usual, when a central bank holds pat, the focus is more on the monetary policy statement that accompanies the decision.

The Banxico has been fighting increasing inflation for quite a long time now. And it has repeatedly expressed concern over the economic effect that the exchange rate would have on the economy. This has led to what some analysts call an “unwarranted hawkish” tone in their communications, especially in the recent months where the economic outlook has been worrisome.

What We Are Looking For

There is an almost unanimous consensus that the bank will hold rates steady at 8.25%. This would be the fifth consecutive hold after a hiking cycle from 3.0% in late 2015. Where there is a certain amount of discrepancy among analysts is regarding how the hawkish the tone of the policy statement and the guidance will be.

Where we could also see some market action is if there is a change in the votes for the rate decision. The last time around, the decision was unanimous. If there is a change in the vote pattern to support a 0.25% cut, then we could see the market react.

The Bank’s Stance

When comparing to the prior monetary statement, the key things that the bank has been focusing on in terms of determining policy are the exchange rate pass-through. That means how the exchange rate is affecting the Mexican economy. The US is Mexico’s largest trade partner, and while a weaker peso helps exports, it increases inflation.

Concerns about inflation are the second aspect that the bank will focus on. Last time around, they said the inflation situation is transitory. If their language changes and sees inflation as more long term, then that would be hawkish and support the peso.

Finally, we have their perception on the balance of risk, which last time, they said had “become more uncertain” and continued to tilt downwards. This is the only part of the statement that is able to offer an opening to express dovishness.

The Fed

The Banxico does take into account the relative policy difference between the US and Mexico since it has implications for the exchange rate and inflation. With analysts penciling in a rate cut by the Fed next month, this would open the possibility that the Bank of Mexico could cut rates to keep pace. Given the drop in economic performance, the bank is under pressure to lower rates. However, it can’t justify doing that given current inflation.

A cut by the Fed would widen the bond yield spread. It would also give Banxico some room to cut rates in a pattern following the Fed. This is the argument offered by the analysts expecting more dovishness and arguing for the beginning of an easing cycle by the end of the year.

The Markets

The USDMXN has remained largely stable since the last meeting, and inflation has slowed a bit (supporting the bank’s argument that the increase was transitory). The peso also gets support from the price of crude, which has increased lately over tensions in the Middle East. With little change in the indicators that the bank follows since the last meeting, there is a good chance of a broad reaffirmation of views.

AUDUSD is trading at 0.6990; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test the cloud’s upside border at 0.6975 and then resume moving upwards to reach 0.7065. Another signal to confirm further ascending movement is the price’s rebounding from the channel’s downside border. However, the scenario that implies further growth may be cancelled if the price breaks the cloud’s downside border and fixes below 0.6945. In this case, the pair may continue falling towards 0.6895.

NZDUSD, “New Zealand Dollar vs US Dollar”

NZDUSD is trading at 0.6675; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test the cloud’s downside border at 0.6650 and then resume moving upwards to reach 0.6770. Another signal to confirm further ascending movement is the price’s rebounding from the support level. However, the scenario that implies further growth may be cancelled if the price breaks the cloud’s downside border and fixes below 0.6615. In this case, the pair may continue falling towards 0.6545.

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is trading at 1.3130; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test the cloud’s downside border at 1.3145 and then resume moving downwards to reach 1.3030. Another signal to confirm further descending movement is the price’s rebounding from the resistance level. However, the scenario that implies further decline may be cancelled if the price breaks the cloud’s upside border and fixes above 1.3190. In this case, the pair may continue growing towards 1.3275.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Oil prices traded higher again yesterday in response to the latest industry reporting which showed a further drawdown in US crude stores last week. The API report on Tuesday indicated such movement in inventories. This was then confirmed yesterday by the weekly report from the Energy Information Administration.

The report showed that in the week ending June 21st, crude inventories fell by a massive 12.8 million barrels. This decline was over five times the expected 2.5 million barrel decrease the market was looking for. The statistics office of the Department of Energy confirmed that the moves were the largest increase since September 2016.

US Crude Exports Hit New Record

Elsewhere, the report showed that net US crude imports decreased by 1.2 million barrels per day. Net exports jumped by 3.8 million barrels per day. This beat the prior 3.6 million barrel per day record set in February. Refinery runs were also seen rising by 73k barrels per day over the week with refinery utilisation rates edging higher by 0.3% to 94.2% of total capacity.

Gasoline Stocks Down

Gasoline stocks were seen falling over the week by 996k barrels which was in stark contrast to the expected 288k barrel gain forecast ahead of the release. Distillate stockpiles, including diesel and heating oil, were down by 2.4 million barrels. This is again in contrast to the expected 522k barrel increase the market was projecting.

Middle East Tensions Keeping Crude Supported

In all, the report was solidly bullish and helped keep crude prices supported as they continue their run-up back towards $60. They fell just short at $59.92 yesterday before softening a little so far today.

Crude has been well supported over recent weeks due to rising tensions in the Middle East as the standoff between the US and Iran continues. Following the downing of a US spy plane by Iran, the US president initially reacted by calling an airstrike. This was then later canceled ahead of execution. On Monday however, Trump announced fresh sanctions on Iran. This time aimed at the country’s supreme leader as well as other key senior figures. Given Iran’s opposition to the sanctions, the prospect of military conflict remains elevated.

Upcoming OPEC Meeting in Focus

Looking ahead, the market will next be focusing on the July 1st/2nd meeting of OPEC. The OPEC production cuts initiated at the start of the year drove a sizeable rally in oil before the impact of surging US crude production and a fresh escalation of the US/China trade war took its toll. There is now speculation that the group will announce an extension of those cuts at the upcoming meeting which would again put upward pressure on oil prices.

Technical Perspective

The rally in oil has seen prices breaking back above the 58.04 level with the market now sitting just below big technical confluence at the 60.12 level where we have structural resistance and bearish trend line resistance from the 2019 highs. A break higher here could open the way for a test of the 63.83 level much higher. Any further flaring of tensions between Iran and the US could easily drive such a move in the near term.

As we can see in the H4 chart, the ascending tendency continues. After forming Shooting Star pattern outside the channel, XAUUSD started to reverse and returned inside the channel. Right now, price is forming a slight correction. If the pair reverses, it may resume falling towards 1382.22. At the same time, we shouldn’t exclude an opposite scenario, which implies that the price may update its closest high and continue moving upwards to reach 1441.85.

NZDUSD, “New Zealand vs. US Dollar”

As we can see in the H4 chart, after testing the horizontal resistance line, NZDUSD formed Hanging Man pattern at 0.6681. Right now, the price is trying to reverse. If it succeeds, the pair may fall towards the support line 0.6575. At the same time, one shouldn’t exclude an opposite scenario, according to which the instrument may update the high and grow to reach 0.6722.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.