US stock market closed at new record on Monday led by technology stocks after president Trump agreed with his Chinese counterpart to resume trade talks as they hold off on imposing additional tariffs. The S&P 500 rose 0.8% to 2964. Dow Jones industrial added 0.4% to 26717. The Nasdaq composite surged 1.1% to 8091. The dollar weakening reversed as both the Markit’s purchasing managers index and Institute for Supply Management’s manufacturing indexes showed US manufacturing sector continued expanding in June. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, jumped 0.7% to 96.81 but is lower currently. Futures on US stock indices point to higher openings today.

European indexes advance despite weak manufacturing data

European stocks accelerated gains on Monday after US and China agreed on trade truce Saturday. Both GBP/USD and EUR/USD turned lower but are higher currently. The Stoxx Europe 600 index rose 0.9% led by chip maker shares despite weak euro zone PMI data. The DAX 30 advanced 1% to 12521.38 despite a report German manufacturing sector activity slowed in June for the sixth month in a row. France’s CAC 40 added 0.5% and UK’s FTSE 100 gained 1% to 7497.5 while UK’s June manufacturing PMI reading fell to its lowest since October 2012.

Hang Seng leads Asian indexes gains

Asian stock indices are mostly rising today after president Trump said Monday that renewed talks have “already begun”. Nikkei closed 0.1% higher at 21754.27 with yen little changed against the dollar. Markets in China are mixed: the Shanghai Composite Index is down 0.03% while Hong Kong’s Hang Seng Index is 1.4% higher. Australia’s All Ordinaries Index extended gain 0.1% as Australian dollar resumed climbing against the greenback despite a 25 basis points cut in interest rates to 1% by the Reserve Bank of Australia.

Brent futures prices are extending gains today ahead of OPEC official meeting with non-OPEC producers. Prices rose yesterday after OPEC said it officially agreed to extend production curbs by nine months: September Brent crude rose 0.5% to $65.06 a barrel on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Dr. John-Mark Staude, CEO of Riverside Resources, speaks with Maurice Jackson of Proven and Probable about his company’s recent agreement to acquire a portfolio of properties in Sonora.

Glad to have you back on the program to discuss Riverside Resources’ latest press release regarding the strategic acquisitions for the Riverside Property bank, but before you share the exciting details, Dr. Staude, introduce us to Riverside Resources and the opportunity you present to the market.

John-Mark Staude: Riverside is a prospect generator with projects in Canada, United States and particularly in Mexico. We have joint venture programs and major projects with major companies like BHP and smaller companies and we provide multiple different commodity exposure of gold, silver, copper. We’ve been able to operate for 13 years, have no debt and have a very strong balance sheet. We’re a wonderfully driven prospect generator company.

Maurice Jackson: Let’s go to Sonora, Mexico, where you are right now, and where Riverside Resources just entered into a binding letter of agreement with the proud sponsor of Proven And Probable and that will be Millrock Resources Inc. (MRO:TSX.V; MLRKF:OTCQX). John-Mark, Riverside is acquiring five projects with no reversionary interest from Millrock Resources. Why these projects and why now?

John-Mark Staude: Why now? Because the market has been low and Riverside’s been working on this for a while, and we’ve been successful in acquiring some key projects that fit for us. I think for Millrock it works for them as they’re working more in Canada and particularly in Alaska. For us, we know these projects well. They have been on our radar for a number of years. We tried to get a larger position in Millrock’s in Mexico, but Millrock beat us in that when they acquired Paget Minerals. What Riverside sees is specific opportunities on these projects and a number of them that fit within the BHP strategic area, where we’re working with BHP and thus we can see that there’s a possibility of bringing these projects with BHP forward as porphyry coppers as well.

Maurice Jackson: On behalf of the Riverside shareholders, provide us with project descriptions for each project, please.

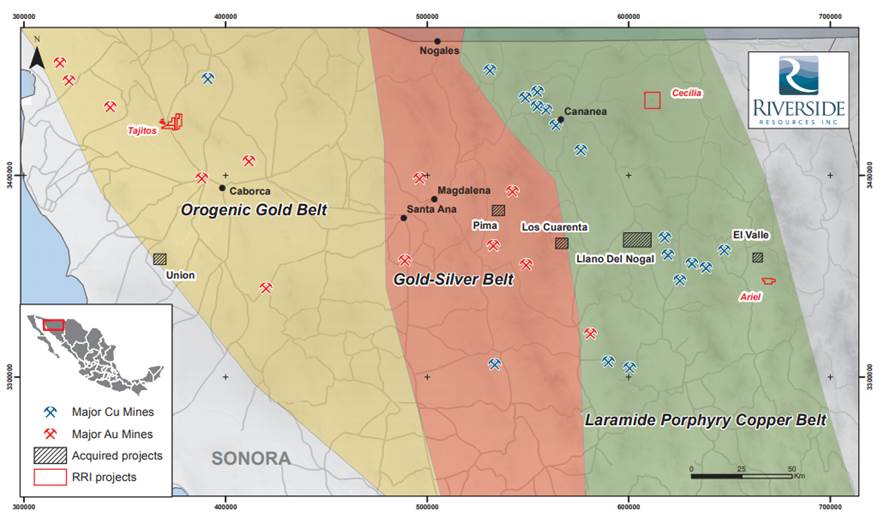

John-Mark Staude: Well, I think one of the key projects Riverside is excited about is the Los Cuarenta project that you can see on the map above. We’re in the state of Sonora; there’s a location map on the left corner. In the northern part of Mexico, along the border, we have the Los Cuarenta project, which is a very good project, close to other mines such as Las Chispas and also the Mercedes Mine. Great location.

A second project we like a lot is in the west, Union. What we like about this project is it’s in the orogenic gold belt, similar to where we have our Tajitos project and many other mines in this region of western Sonora, Mexico. Three projects to the east, Llano del Nogal, El Valle and Pima, also are porphyry copper related systems that we see as possibly fitting with BHP.

We’re very excited to have this portfolio now ready to go with a locked-in partner, BHP, and you can see it fits around our other projects, the Cecilia, Ariel and also Tajitos, so we’re in a great location that we know how to operate. This fits Riverside like a hand to a glove, a perfect fit.

Maurice Jackson: John-Mark, I noticed that a lot of excitement there and attention was put on Los Cuarenta. What specifically excites Riverside here?

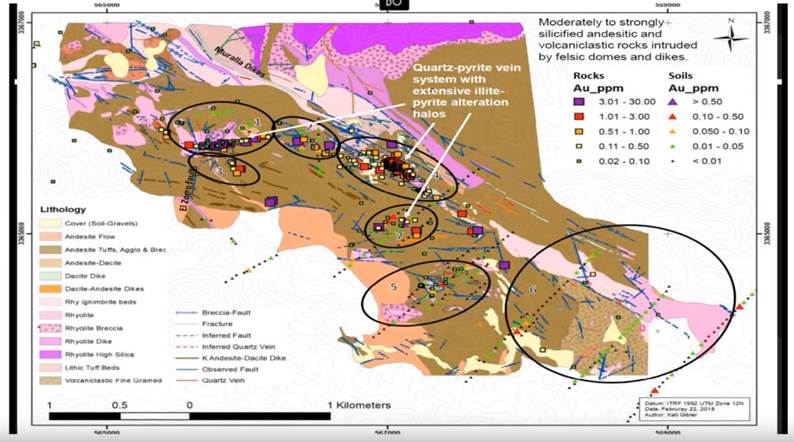

John-Mark Staude: The thing about Los Cuarenta that excites us is the location. It’s near other deposits and also has really great geology. Taking a closer look at the geology, we have seven different areas of mineralization along a trend that is over four kilometers. The veins shown here are similar to the veins and mineralization we see at the Mercedes Mine that’s operated by Premier Gold, and also similar to the over half a billion dollar value, very exciting project that’s only 30 kilometers away, Las Chispas that’s operated by SilverCrest Metals.

So Riverside having a project that’s very much like SilverCrest Metals’ with high-grade mineralization on veins, lots of good extent and in a largely un-drilled area makes this a really great acquisition. Riverside’s excited to add Los Cuarenta to the property bank. As you can see, we have much to be excited about from the images on the map.

Maurice Jackson: John-Mark, congratulations on what looks to be a very prudent move on the behalf of shareholders. I continue to be impressed with the geological and business acumen of Riverside Resources. It’s strategic moves such as these that increase Riverside’s probability for the next big discovery. Let’s switch gears here. John-Mark, Riverside is thriving, juxtapose to the share price that is near a 52- week low. What would you like to tell the shareholders regarding the current share price?

John-Mark Staude: I think the share price has been pushed low and I think we’ve demonstrated we have cash, have we have deals, we have deal flow, and we also think that now gold are prices going up, it really should help rebound the share price. Gold has gone up quite a bit, well over $1,400, and we see Riverside having gold resource assets and having gold royalties and having gold deals, makes Riverside in a very good position. So we see ourselves as really undervalued in this condition and we think that these types of deals will help us to get the share price going.

Maurice Jackson: Are you currently buying shares?

John-Mark Staude: During July, I look forward to buying shares. I couldn’t buy any now; I’ve been in a lock-up period waiting for the completion of this deal and recently before that the BHP deal. So being locked out of that because we had material information and we never want to have trading on that, but now that we’re in a position, we’ll move ahead. I’ll have an opportunity to accumulate more shares. I’m already a large shareholder. I’ve never sold a share of Riverside in my whole life, but look forward to adding more into my portfolio of Riverside.

Maurice Jackson: Well, that speaks volumes. John-Mark, for the next unanswered question for Riverside Resources, when can we expect an answer and what will determine success?

John-Mark Staude: In the coming three weeks, we look forward to having more results coming out from some of our programs and I think what we’ll see from those programs is increased high-grade gold. We have some high-grade gold results coming along, working those up and that’ll be good. Also during the latter part of this summer, we’ll look forward to expanding in Canada and giving the investors just an update on our Canadian program that we’re working, taking advantage of the summer where our VP exploration Freeman Smith and the rest of our team have been adding there as well, so we’re in a great position coming into the fall. Really good for Riverside.

Maurice Jackson: Dr. Staude, before we close, what keeps you up at night that we don’t know about?

John-Mark Staude: You know for me, the key thing is people and what keeps me up at night is just how do we keep these great people working with the BHP alliance and program. Working with BHP is a great place, so I’m so excited. I’m sleeping much better at night now, having such a major partner and we’re now moving forward with programs to bring forward with them. So Riverside’s really in a great position for coming years. Really having fun with Riverside now.

Maurice Jackson: All right, Dr. Staude, for someone listening that wants to get more information on Riverside Resources, please share the website address.

Maurice Jackson: Riverside Resources trades on the TSXV symbol RRI and on the OTCQB symbol RVSDF.

As a reminder, I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide unlimited options to expand your precious metals portfolio from physical delivery, offshore depositories, precious metal IRAs and private blockchain distributed ledger technology. Call me directly at 855-505-1900. Or you may email [email protected].

Finally, we invite you to visit provenandprobable.com, where we provide Mining Insights and Bullion Sales. Riverside Resources is a sponsor of Proven and Probable and we are proud shareholders of Riverside Resources for the virtues conveyed in today’s message.

Dr. John-Mark Staude of Riverside Resources, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Riverside Resources and Millrock Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Riverside Resources and Millrock Resources. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Millrock Resources and Riverside Resources, companies mentioned in this article.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

The deal and its benefits to the energy firm are addressed in a ROTH Capital Partners report.

In a June 27 research note, ROTH Capital Partners analyst John White reported that W&T Offshore Inc.’s (WTI:NYSE) proposed acquisition of assets from ExxonMobil for $200 million is “very positive.”

Those assets include oil and gas producing properties in the eastern Gulf of Mexico that generated $70 million in operating cash flow in 2018 along with related onshore processing facilities.

White highlighted that in terms of benefits of the deal to W&T Offshore, the acquisition will nearly double its Proven reserves from 84,000,000 barrels of oil equivalent (84 MMboe) to 158 MMboe. It will boost its pro forma production by about 59%, to 53,149 barrels of oil equivalent (boe). Also, the properties to be acquired will offset W&T Offshore’s Fairway field in offshore Alabama.

Because W&T Offshore’s management team has successfully executed this acquisition strategy several times in the past, White noted, it likely will “be able to lower operating costs, add synergies and increase production and reserves” with this transaction.

The analyst also pointed out that the acquisition metrics are “very favorable,” at $2.70 per boe or $0.45 per thousand cubic feet equivalent (Mcfe) on Proven reserves and $10,100 flowing boe per day or $1,684 flowing Mcfe per day. “The median figure of our coverage on flowing boe per day is $35,000,” he indicated.

W&T Offshore will fund the acquisition with cash on hand, $86.1 million, plus the bank revolver, up to $229 million available, both figures accurate as of March 31, 2019, White wrote.

ROTH has a Buy rating and a $9.50 per share target price on W&T Offshore. The company’s current share price is around $4.96.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, W&T Offshore Inc., Flash Note, June 27, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of W&T Offshore, Inc. and Callon Petroleum Company and as such, buys and sells from customers on a principal basis.

Shares of W&T Offshore, Inc. may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

The Critical Investor provides an update on recent developments with an explorer that has projects in the Yukon and Nevada.

Although Alianza Minerals Ltd. (ANZ:TSX.V) had to wait for better weather until exploration programs could kick off in the Yukon, the company hasn’t been sitting on its hands in the meantime. Very recently, it signed a LOI with a subsidiary of Coeur Mining Inc. (CDE:NYSE) to explore the high-grade silver/lead/zinc Tim project in the Yukon, it raised C$750k on June 25, 2019, and a bit further back it also arranged a JV with Hochschild Mining Plc (HOC:LSE) about three Nevada projects, and started field work on all three, funded by Hochschild. As sentiment in metals and mining turned slightly more negative after PDAC in March, Alianza was testing the 5-6c support (which I mentioned in my first article around that time) earlier than I thought:

Fortunately, sentiment turned positive after gold started a strong upward move, even to the tune of a breakout, after it breached a longstanding resistance (US$13601380/oz), causing everybody to have a more positive stance. As silver didn’t follow gold as aggressively, the Alianza share price didn’t react, but this changed quickly after the financing and the Coeur LOI were announced.

Let’s have a closer look at Alianza’s activities.

The financing is a combination of flow through (4,166,666 shares @6c) and non-flow through (10,000,000 units @5c including a 3 year full warrant exercisable at 10c), adding C$500k for exploration and working capital and C$250k for Yukon exploration. The financing is expected to close within two weeks, and finder’s fees of 7.5% in cash/warrants will be paid to eligible parties. These terms indicate the harshness of the current investment climate in mining, as in better times just 5% in cash is normal.

8% is about the highest I have come across in 2015, so Alianza management did good to raise some cash at all nowadays. It is not that it really needed the fresh cash for exploration, but it is working on six projects now, four of them being funded by JV partners, so it wanted to expand on its own exploration program for Haldane, and expand on investor relation programs to increase investor awareness further, with news flow incoming.

On June 20, 2019, Alianza signed a Letter of Intent (LOI) with Coeur Explorations, a wholly owned subsidiary of Coeur Mining, to explore the road-accessible Tim Property in southern Yukon Territory. Exploration at the Tim Property is targeting high-grade silver-lead-zinc mineralization similar to that being currently mined by Coeur at its Silvertip mine located 12 km to the south of the Tim Property. Coeur was a logical suitor for an eventual JV, as there were apparently so many similarities between Tim and Silvertip that the owners at the time literally rolled the dice when to decide which property to drill first. Alianza and Coeur are obviously hoping for Tim to become another orebody for feed at Silvertip. Let’s wait and see.

Tim project; Yukon

Coeur can earn a 51% interest in the property by funding C$3.5 million in exploration over five years and making staged cash payments totaling C$275,000. Coeur can elect to complete the option to earn 80% in the property by funding a positive feasibility study in the following three years and making annual payments of C$100,000. Coeur is the operator here. I estimate the budget of a FS for this project in the range of $5-8 million, so it is an interesting JV for Alianza.

Exploration for Tim is targeting high-grade silver-lead-zinc Carbonate Replacement Mineralization (CRM), similar in style to that found at Coeur Mining’s Silvertip Mine, located 12 km to the south. Alianza also received a small YMEP (Yukon Mining Exploration Program) grant for the Tim project. Under this program, the Yukon government provides funding to support mineral exploration activities for 50% of eligible expenditures to a maximum of $40,000.

Haldane project; exploration camp

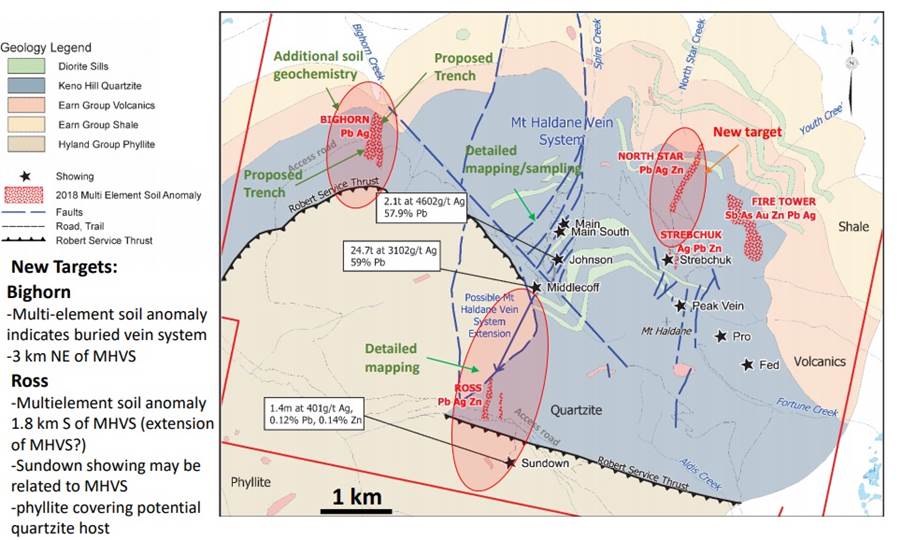

For Haldane, the 2018 field program identified a new silver vein target at the Bighorn Anomaly, 2.5 km from known mineralization at the MHVS (Mount Haldane Vein System) targets where work extended the potential strike length to over 3.5 km. Trenching and/or drilling are planned for these targets, and good results will upgrade the project for further work which may be funded by a partner. I contacted CEO Jason Weber about the program, and he provided me with this map with additional comments in green:

According to Jason Weber, this is setting up and refining the drill hole locations for phase II (later in August). Alianza has planned detailed mapping and trenching at the Bighorn anomaly to define potential mineralized structures and controls. Also, additional soil sampling will be completed to the west of the Bighorn anomaly.

Besides this, detailed mapping at the Ross anomaly is planned in order to define controlling structures and refine the location of the offset fault on the Robert Service Thrust (see low right on map). This too will aid in the location of drillholes for the phase II drill program. Additional detailed mapping and sampling will be done in the MHVS main area. This includes old trenches, where again, structural mapping will be stressed.

As management doesn’t expect veins to outcrop at surface (although they hope to get lucky), they are looking for signs of faults (that if having the right orientation, may host target veins) and any altered float material that may be weathered from vein structures. These may manifest themselves as breaks in slope, linear gullies (TCI: large ditches), etc. Any information the geologists can gather in this way can be compiled to infer structure location and therefore to help refine drill hole locations.

Another interesting development was the JV with Hochschild from March 4, 2019. They have optioned three Nevada sediment-hosted gold properties from Alianza. The BP and Bellview properties are located in the southern extension of the Carlin Trend, while the Horsethief property represents an off-trend gold target located 26 km east of Pioche, Nev. The Horsethief property is considered the most prospective by Alianza, and already was the focus of attention. Hochschild seems to think in the same direction. It can earn a 60% interest in each property by making the following exploration expenditures:

over 4.5 years totalling US$2.5 million at BP and totalling US$3.5 million at Bellview and

over 5.5 years totaling US$5 million at Horsethief.

Under these agreements, the 2019 exploration programs will total at least US$700,000 as a firm commitment from Hochschild and will include drilling at Horsethief and drill target identification and definition at BP and Bellview.

Here are the full terms of the option agreements of the Hochschild JV, per the news release:

Horsethief PropertyHochschild can earn a 60% interest in the Horsethief Property by conducting US$5 million in exploration on the property over a 5.5 year period, with a committed minimum expenditure of US$500,000 in the first 18 months and a minimum US$500,000 in each subsequent year. Within 60 days of acceptance of the first option, Hochschild may elect to undertake a second option to earn an additional 10% (total 70%) in the property by funding a further US$5 million in exploration over 3 years (minimum US$500,000 in exploration per year).

Bellview PropertyHochschild can earn a 60% interest in the Bellview Property by conducting US$3.5 million in exploration on the property over a 4.5 year period, with a committed minimum expenditure of US$100,000 in the first 18 months and a minimum US$500,000 in each subsequent year. Within 60 days of acceptance of the first option, Hochschild may elect to undertake a second option to earn an additional 10% (total 70%) in the property by funding a further US$3.5 million in exploration over 3 years (minimum US$500,000 in exploration per year).

BP PropertyHochschild can earn a 60% interest in the BP Property by conducting US$2.5 million in exploration on the property over a 4.5 year period, with a committed minimum expenditure of US$100,000 in the first 18 months and a minimum US$500,000 in each subsequent year. Within 60 days of acceptance of the first option, Hochschild may elect to undertake a second option to earn an additional 10% (total 70%) in the property by funding a further US$2.5 million in exploration over 3 years (minimum US$500,000 in exploration per year).

Alianza will be the operator. Hochschild will reimburse Alianza for 2018 property taxes and permit costs, totalling approximately US$41,600.

Conclusion

Alianza Minerals is successful so far in following the hybrid prospect generator model, as it raised over C$1.5M since December 2018, and signed two deals with Hochschild and Coeur, two household silver names in the space. The foundation seems to be solid; now it is time to build on it by own and JV exploration work, preferably drilling as soon as possible. After target refining, drilling at Haldane will finally start in August of this year, and I am looking forward to it. According to Jason Weber, drilling funded by Hochschild could start in Q4 2019, Coeur is defining targets this year and will look into drilling next year.

As a reminder, I view the 100% earn-in flagship project Haldane as a prospective high-grade silver exploration opportunity, and I’m very interested if it can hit some really high-grade intercepts, as has happened in many places at and around Haldane in the past. The projects funded by Hochschild and Coeur should generate news flow as well this year, so it will be a busy year for Alianza Minerals, hopefully with good news for investors.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The author is not a registered investment advisor, and currently has a long position in this stock. Alianza Minerals is a sponsoring company. All facts are to be checked by the reader. For more information go to www.alianzaminerals.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure: 1) The Critical Investor’s disclosures are listed above. 2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

U.S. Gold Corp.’s President and CEO Edward Karr, in this interview with Bill Powers of Mining Stock Education, provides an overview of the company and explains why geologist Dave Mathewson has called the Keystone project “the best exploration project he has seen in his career.”

In this interview, U.S. Gold Corp.’s (USAU:NASDAQ) President and CEO Edward Karr provides an overview of the company and explains why the upcoming drill program at its Keystone project in Nevada is so prospective. Dave Mathewson, who is Nevada’s most-successful gold exploration geologist and current Vice President of Exploration for U.S. Gold Corp, has called the Keystone project “the best exploration project he has seen in his career.”

Bill Powers: How and why was U.S. Gold Corp. formed?

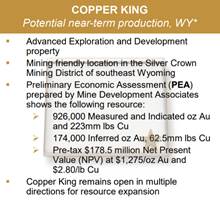

Edward Karr: We formed U.S. Gold Corp. as a private company back in 2014. The reason we founded U.S. Gold Corp. really was to acquire our flagship property called Copper King. Copper King is located in the state of Wyoming about 20 miles outside of Cheyenne. It has a very robust resource. It is an open pit gold, copper, silver, zinc, polymetallic porphyry deposit, and comes right up to surface. We bought Copper King off another publicly traded company called Energy Fuels Corporation. Energy Fuels is a uranium company based out of Denver. They had acquired Copper King when they took over Strathmore Minerals Corporation, and it was a non-core asset for them being a gold/copper deposit. That’s how we originally set up and formed U.S. Gold Corp.

Bill Powers: Your other flagship project is the Keystone project in Nevada. How did that come under the control of U.S. Gold Corp.?

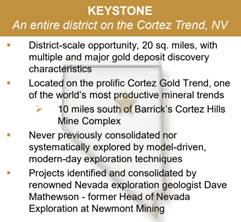

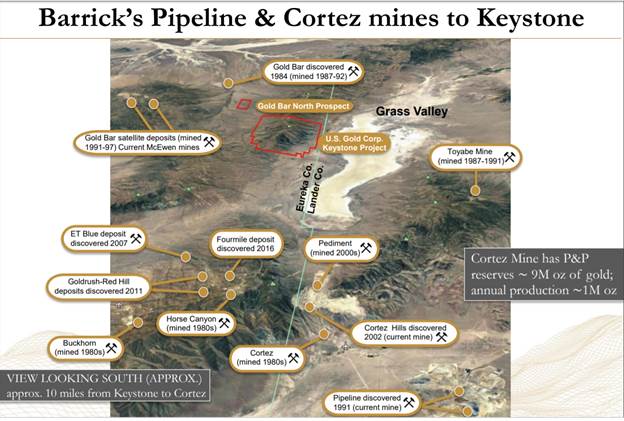

Edward Karr: We had an opportunity come along while were still private and only had our flagship project Copper King. In 2016, I received a telephone call from Dave Mathewson, the well-known Nevada exploration geologist, and he had a new exploration project called Keystone. Dave told me that he believes Keystone is the best exploration project he has seen in his career. It has an incredible address being located in Nevada on the Cortez Gold Trend. It’s about 12 miles south of Barrick Gold’s Cortez Hills complex, which includes the Cortez Hills Mine, the new discoveries, Gold Rush, ET Blue and Fourmile. We are right below that and it looks very prospective. When Dave told me about it, I just knew we had to do a deal, so we acquired Keystone into U.S. Gold Corp.

Bill Powers: What are your plans for Keystone this year?

Edward Karr: That was 2016. In the last three years, we have been hard at work at Keystone. We have done a tremendous amount of advancement of the project. We’ve increased our land position. We’ve run a bunch of geophysical surveys over the project, gravity surveys, geochemistry, district-wide mapping. We’ve done a bunch of scout hole drilling. The host rocks and the geology look amazing. Now, we’re really to the point that we are targeting in on what we hope are future potential discoveries.

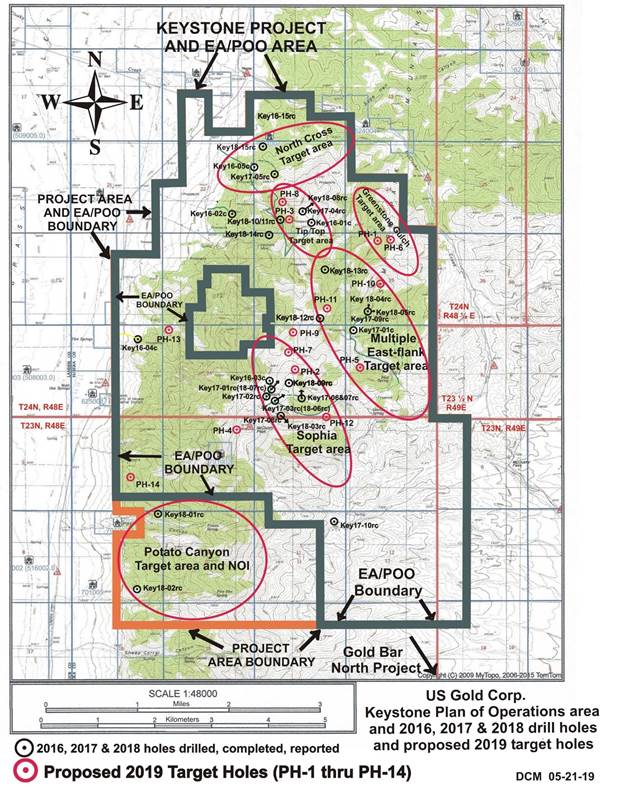

Last year in October, we received the approval of our environmental assessment and our plan of operations. That was a major, major factor for us. We now have no limitations as to where we can go in the district. We can basically explore and drill anywhere. We put out a press release recently outlining our 2019 planned Keystone summer exploration programs. We’d like to go out and drill potentially 14 to 15 holes this summer. These are fairly deep holes. They’re down to about 2,000 feet, and we put out a map on that press release that shows where we would like to go and some of the geological reasons why we would like to go there.

This will most likely be a two-phased program, like we did last year. It’s been a very, very wet winter, lot of snow, lot of precipitation out in Nevada, and a wet spring. Right now as of the third week of June, the property is just finally drying out. I think we can get a drill rig out on property by second half of July, so we will start drilling then. Drill July, August, probably into September, maybe an initial 10 holes for our first phase. From mid-September to, let’s say, through the end of October, we will send all of those chips and core to the laboratory for assays. Hopefully, we have some assay results back by the end of October this year. Then depending on those results, that will really guide our thinking for our second phase in the fall of 2019.

Bill Powers: If you’re successful at Keystone, what gold discovery analog might we compare this project to?

Edward Karr: There are a bunch. Really, I think one of the best comparisons just looking at where we are geographically is our northern neighbors. You look at Cortez Hills, that’s basically a big high-grade breccia of pipe deposit across the valley pipeline, a little lower grade big 25 million ounce deposit. You look south of Cortez Hills, one of Barrick’s big discoveries that is now going into production will be an underground mine called Goldrush. Goldrush is about 10 million ounces, a nice high-grade deposit, definitely an underground mine. A lot of the drill holes that we’re seeing with the geological conditions, the geochemistry, it really looks very similar to a Goldrush type of environment. I give you an example.

Last fall down in our Sophia target area, one of our drill holes, which was drill hole 18-09, you can go out and look at some of our prior press releases on this, that was an extremely exciting drill hole for us. We had great brecciation and alteration. It shows us that the rock is really beat up, and at the bottom of the drill hole, we lost the hole. We literally drilled into a void. Well, a void is a cave, and a cave can be a very positive thing. The Goldrush deposit north of us is littered with caves. You have these caves and then right below the bottom of those caves, that’s the big mother lode of the Goldrush deposit.

When the drill drills into one of these caves, it cavitates in that open space, because the drill is meant to be drilling through difficult rock. Open air just cavitates and then ultimately you lose it. But, for about 100 feet before we hit that void, we had some of the best geochemistry indications we have seen of any hole. All of the indicators literally spiked off the charts. This is the model. It is a Cortez-Carlin style deposit; collapsed breccia, geochemistry is there. We do not have a high-grade gold intercept yet, but a focus of our summer 2019 exploration plans is going to be following up on that hole. We believe if we can step out a little ways and get through that void, there could be something very, very exciting right below that. That’s certainly something all of your readers should be paying attention to.

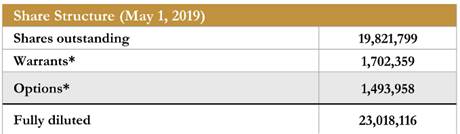

Bill Powers: Your company is very unique in that you are listed on the NASDAQ Exchange as a junior gold explorer. Can you comment on your share structure and who owns the shares?

Edward Karr: We have today as of the end of June 2019, just around 20 million shares issued and outstanding of common stock. We have recently closed a $2.5 million financing, that was a non-brokered financing predominantly done by existing supporting shareholders of the company. That was structured as a series F preferred. It was an at market deal, so the preferred converts into common stock at $1.14 per share. The only reason we did it as a preferred is one of the investors wanted a beneficial owner limitation on it.

Our stock today is about 20 million shares. Management, insiders and a couple close shareholders own almost 30% of the company. The other 70% is owned by thousands and thousands of retail shareholders. Our public listing has a long history because we merged into a publicly traded technology company that had been trading since 1971. We have a very, very large shareholder base. We do not have a lot of marquee institutions in our company. We really don’t have any. That’s just because it’s been a very challenging, very difficult market for the junior exploration sector, and our market cap is only today around $2021 million. It’s really, really, really, really cheap. Most of these institutions want to see a $50-plus million market cap, and we’re very hopeful as we advance our projects that we can get some big named institutions into our shareholder registry in the future.

Bill Powers: As we conclude, what would be three things that most likely could go wrong with U.S. Gold Corp.’s plans for the next year?

Edward Karr: Well, number one I would think is if the price of gold were to collapse. Today as of this interview we’re about $1,410/oz. Looks like a pretty good break out and a lot of us believe it’s the beginning of a new bull market. But, if that turns out to be wrong and this is just a head fake and the world moves into a deflationary collapse and gold goes back to $1,100 an ounce, I think it’s going to be very challenging.

Number two, a real challenge in the junior exploration sector has been access to capital. Getting good money from good investors on good terms. Because, this industry, it really is difficult because we’re constantly burning money. We don’t have any revenues, very similar to biotechnology, and we’re trying to get to discovery success. We constantly have to raise money and that’s been challenging. Hopefully if the gold market continues, it’ll be easier.

I’d say the third thing is always business challenges. We are very, very prudent, we believe, with our treasury. We don’t just go out and drill the Keystone project to Swiss cheese. Every one of these drill holes is expensive, they cost money, and we have to be very precise. This is trying to hit the bulls eye of a target 1,000 yards down range. You got to have a good gun, you got to have a really good scope, you got to have a good spotter, and all the conditions need to be right to come up with that discovery.

We believe we are very, very, very close at Keystone to discovery success. Everything is looking really good. But ultimately, what we can’t predict in any way, is that going to be five drill holes, 15 drill holes, or 25 more drill holes? It’s this challenge of raising enough capital on the best terms to be able to fund the company and those exploration budgets without diluting all the shareholders too much. Those are probably the three biggest challenges we have in the near future.

Bill Powers: To learn more about U.S. Gold Corp you can go to www.usgoldcorp.gold. Ed, thank you for providing an overview of your company.

Edward Karr: Thanks so much Bill. I appreciate the interest.

Bill Powers is the host of the Mining Stock Education podcast that interviews many of the top names in the natural resource sector and profiles quality mining investment opportunities. Powers is an avid resource investor with an entrepreneurial background in sales, management and small business development. His latest interviews can be found at MiningStockEducation.com.

Disclosure: 1) Bill Powers: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: U.S. Gold Corp. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: U.S. Gold Corp. My company has a financial relationship with the following companies mentioned in this article: U.S. Gold Corp. Additional disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Energy Fuels. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of U.S. Gold Corp., a company mentioned in this article.

The content produced by Bill Powers and Mining Stock Education LLC is for informational purposes only and is not to be considered personal, legal or investment advice or a recommendation to buy or sell securities or any other product. It is based on opinions, public filings, current events, press releases and interviews but is not infallible. It may contain errors and we offer no inferred or explicit warranty as to the accuracy of the information presented. If personal advice is needed, consult a qualified legal, tax or investment professional. Do not base any investment decision on the information contained on MiningStockEducation.com, our podcast or our videos. We usually hold equity positions in and are compensated by the companies we feature and are therefore biased and hold an obvious conflict of interest. MiningStockEducation.com may provide website addresses or links to websites and we disclaim any responsibility for the content of any such other websites. The information you find on MiningStockEducation.com is to be used at your own risk. By reading MiningStockEducation.com, you agree to hold MiningStockEducation.com, its owner, associates, sponsors, affiliates, and partners harmless and to completely release them from any and all liabilities due to any and all losses, damages, or injuries (financial or otherwise) that may be incurred.

The potential effects of the event on the copper market and the project’s major joint venture partner are outlined in a BMO Capital Markets report.

In a June 27 research note, BMO Capital Markets analyst Ed Sterck wrote that the fatal mine collapse from suspected illegal mining at the KOV open pit at the Kamoto Copper concession in the Democratic Republic of the Congo will impact Glencore International Plc (GLEN:LSE) and the copper market. News reports indicated at least 36 people died in the accident.

Kamoto is a partner with Glencore in the Katanga joint venture, Glencore holding a majority 64.75% interest. Katanga accounts for about 14% of Glencore’s net present value. The joint venture is projected to produce 269,000 tons of copper and about 24,000 tons cobalt in 2019. Although uncertain, the KOV mine is thought to supply about two-thirds of the ore processed at Katanga.

Sterck purported that if the mine collapse was related to illegal mining then it could impact production there but only short term after an investigative period. However, “preventative action will likely be needed, and it could impact Glencore’s social license to operate.”

More certain, the analyst pointed out, is the effect the event will have on the copper market, already suffering this year. “We see the market as very sensitive to further supply disruptions such as this.”

Due to rainfall in South America’s Atacama Desert, cuts in Zambia and the ongoing strike at Chuquicamata in Chile, the annualized rate of copper disruptions in the first six months of 2019 is already higher than it was last year, at 5% versus 3%. Further, spot treatment and refining charges being at multiyear lows and Chinese cathode inventories drawing quickly indicate copper market tightness.

Sterck concluded that “with managed money net short positions still representing 15% of total open interest on the COMEX, there is potential for relatively aggressive short covering in the financial market, which could see an outsized price reaction. This should boost other copper mining equities.”

BMO has an Outperform rating and a £3.20 per share target price on Glencore, whose stock is currently trading at around £2.73 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from BMO Capital Markets, Glencore, June 27, 2019

IMPORTANT DISCLOSURES

Analyst’s Certification I, Edward Sterck, hereby certify that the views expressed in this report accurately reflect our personal views about the subject securities or issuers. I also certify that no part of our compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Analysts who prepared this report are compensated based upon (among other factors) the overall profitability of BMO Capital Markets and their affiliates, which includes the overall profitability of investment banking services. Compensation for research is based on effectiveness in generating new ideas and in communication of ideas to clients, performance of recommendations, accuracy of earnings estimates, and service to clients.

Analysts employed by BMO Nesbitt Burns Inc. and/or BMO Capital Markets Limited are not registered as research analysts with FINRA. These analysts may not be associated persons of BMO Capital Markets Corp. and therefore may not be subject to the FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Company Specific Disclosures Disclosure 2: BMO Capital Markets has provided investment banking services with respect to Glencore within the past 12 months. Disclosure 4: BMO Capital Markets or an affiliate has received compensation for investment banking services from Glencore within the past 12 months. Disclosure 5: BMO Capital Markets or an affiliate received compensation for products or services other than investment banking services within the past 12 months from Glencore. Disclosure 6A: Glencore is a client (or was a client) of BMO Nesbitt Burns Inc., BMO Capital Markets Corp., BMO Capital Markets Limited or an affiliate within the past 12 months: A) Investment Banking Services Disclosure 6C: Glencore is a client (or was a client) of BMO Nesbitt Burns Inc., BMO Capital Markets Corp., BMO Capital Markets Limited or an affiliate within the past 12 months: C) Non-Securities Related Services. Disclosure 9C: BMO Capital Markets makes a market in Glencore in Europe.

For Important Disclosures on the stocks discussed in this report, please click here.

By CentralBankNews.info Argentina’s central bank lowered its minimum interest rate for benchmark Leliq notes to 58.0 percent for the month of July, when seasonal demand for working capital rises, as it met its objective for the monetary base for the 9th consecutive month in June. Since October 2018 the Central Bank of the Argentina Republic (BCRA) has used a monetary policy framework where the Leliq rate fluctuates daily and is set through auctions. Since April 1, when the central bank set a minimum rate of 62.50 percent, the weighted average adjudicated rate, or the monetary policy rate, for Leliq notes has fluctuated between 68.1 percent and 74.1 percent in May to 63.8 percent on June 24. BCRA’s monetary policy committee COPOM said the average monetary base in June was $1.342 billion, slightly below the goal of $1.343 billion. To better manage liquidity conditions during July, when demand rises from the collection of bonuses and expenses in connection with the winter break, and strengthen the transmission of Leliq rates to savers, BCRA is also lowering the minimum rate of cash requirements for time deposits by 300 basis points, releasing about $45 billion. But to ensure monetary policy is not relaxed during this seasonal phenomenon, the central bank will retain the June goal for the monetary base during July. In coming months the target for base money would be then be lowered further to ensure continued disinflation. Argentina’s inflation rate rose to 57.3 percent in May from 55.8 percent in April, with the central bank’s poll last month showing analysts expect full-year inflation of just over 40 percent, down from 2018’s almost 50 percent, and economic contraction of 1.5 percent. COPOM today also extended its limits for exchange rate intervention at 39.755 to 51.448 peso per U.S. dollar until Dec. 31, 2019. During March and April Argentina’s peso was battered by volatility over nervousness of elections in October and the economy’s weakness, but in on April 29 the central bank decided to intervene more actively, boosting the daily limit for sales to $250 million from $150 million and raising fears a return to intervention could put it on course to draw on its foreign reserves. Last year BCRA used up $16 billion on its reserves between March and September when the International Monetary Fund boosted its support program to $56 billion. After hitting a record low of 45.8 to the U.S. dollar in late April, the peso has rebounded and was trading at 42.4 to the dollar today, down 11 percent this year.

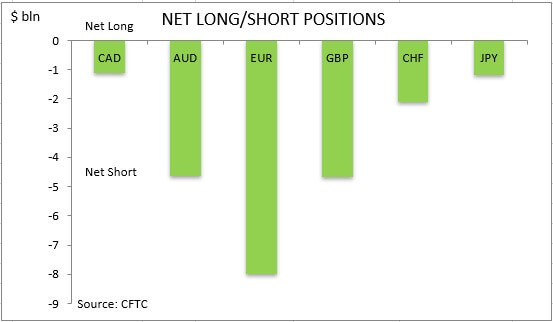

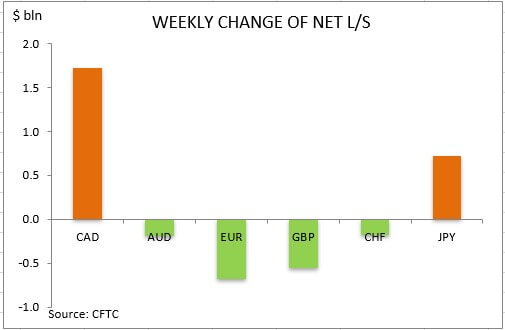

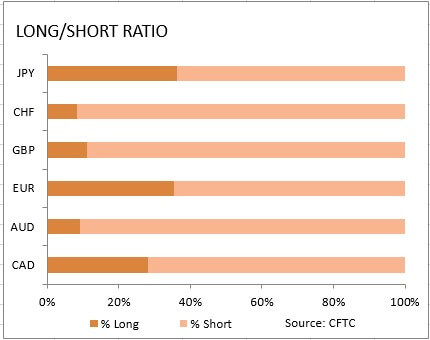

US dollar bullish bets declined continued to $21.75 billion from $22.60 against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to June 25 and released on Friday July 1. The dollar weakened after weak as the Federal Reserve left interest rates unchanged but indicated it would “act as appropriate to sustain the expansion”.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

This past weekend was full of exciting news and information. Combine this with the strong US economic activity, the potential for some type of reprieve in the US/China trade issues and the historic meeting in North Korea between President Trump and Kim Jun Un, and the markets were set up for a big move at the open of trading in Tokyo.

The other big news originated from the Bank of International Settlements (BIS). This Swiss-based central banking committee for “central banks” released an annual report on the progress of global central banks and the global economy last weekend. They urged central banks not to chase easy money policies any longer and to focus on core policy changes, practical economic practices, and real leadership to help drive future growth. They urged nations that easy money policies may help to show some types of immediate economic improvements – but that the risks of continuing such policies and lack of true economic reforms do nothing but pack risk into the back end of these efforts.

Our opinion is the US stock market is poised for a big move based on this news and continued economic activity. If the US is able to settle trade issues in a manner that supports a strong future economic output and restore some balance to foreign trade, as well as continue to produce strong economic activity and output levels throughout the last 6+ months of this year, we could see a very strong price rally setting up into the end of 2019. This could prompt a big move to the upside IF all things line up properly as we have suggested.

If things take an ugly turn over the next 2 to 4+ months, then we believe current support levels will likely act as a floor in the US stock market as the global economies struggle to find their “launch button” to jump-start their economies. As the news stated, the economic factors of the globe are in a transitional state at the moment. The US is the leading global economic engine and many other foreign economies must transition away from easy money policies and make hard choices to drive future growth. Volatility will be KING over the next few months/years and the US Dollar will likely continue to strengthen as this transition plays out.

This ES chart highlights the resistance levels just below $3000 that we are watching as a critical ceiling in the ES. As we have suggested, the news last weekend is driving upward price activity into this resistance area. Traders should be cautiously bullish right now and should be keenly aware of risks that could prompt a breakdown in price. Current support is near $2700.

Technology could be a huge winner if the US/China restore proper trade relations and establish a stronger future economic tie going forward. In fact, the relief of a US/China trade deal could easily spill over into the DOW and Mid-Cap stocks as general trade and infrastructure deals will likely ramp-up quickly. Our researchers believe the technology sector is the “canary in the coal mine” for the future of price related to trade and global economic activities. We believe the technology sector is unfairly weighted in either direction based on the uncertainty of the global economy right now.

Resistance near $8000 is key. Support near $6800 is also very important. This leaves a $1400 range for price rotation within critical levels. Our Fibonacci price modeling system is suggesting even bigger price volatility ranges totaling over $3000 between target levels. This suggests that volatility is still increasing and that traders should understand the risks of this volatility. Currently, we are cautiously bullish as the NQ attempt to breach into new all-time high territory again.

Gold paused in the rally early in trading today, breaking back below $1400. We have confidence in out research that Gold will continue to react to the Fear & Greed that is rampant throughout the globe at the moment and begin another upside move over the next 10+ days. This move below $1400 is an excellent opportunity for traders to identify new Long entry positions for the future upside move.

Remember, the transition that is required over the next 2+ years will require many difficult decisions and a means of transitioning away from easy money policies towards more practical economic policies. This will not be an easy task for many. The fear/greed cycle will show up in precious metals early and quickly. The next upside move should be towards levels above $1550 to $1650.

As we’ve been saying for many months, this is the time to be a skilled trader. These volatility spikes, huge moves in the markets and incredible trade setups are fantastic opportunities for traders. Join us in picking apart these moves, setups, and opportunities.

CONCLUDING THOUGHTS:

I can tell you that huge moves are about to start unfolding not only in real estate, but metals, stocks, and currencies. Some of these super cycles are going to last years. Brad Matheny goes into great detail with his simple to understand charts and guide about this. His financial market research is one of a kind and a real eye-opener. PDF guide: 2020 Cycles – The Greatest Opportunity Of Your Lifetime

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

I urge you to visit my Wealth Building Newsletter and if you like what I offer, join me with the 1 or 2-year subscription to lock in the lowest rate possible, get a FREE BAR OF GOLD and ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own during the next set of crisis’.

The gold and silver markets rarely get much love on Wall Street and from the average investors who only listen attentively to what CNBC and stock brokers have to say.

Nearly a decade of underperformance in the metals markets certainly isn’t helping draw attention. Recently, the gold market started to move, and the rising price has thus far gone mostly unnoticed.

Everyone is watching the equity markets continue the surge higher that began the day after Christmas.

Investors who wonder how long the stock markets will continue to outperform gold ought to consider these little-known facts. They won’t be hearing them on TV or from their broker until after it is too late.

Gold Recently Began to Outperform Stocks

The equity markets just finished their best June in 80 years. That has been trumpeted everywhere in the financial press. The Dow Jones Industrial Average gained 7.2% for the month. That’s hard to beat, but at least one unloved asset managed to do it. Gold gained 8% in June.

It’s worth pointing out that gold has also dramatically outperformed gold in the longer term. The metals has roughly quadrupled in value since Jan. 1, 2000 when it traded at $285/oz. Compare that to the S&P 500 which is just slightly more than double its value at 1426 as we began the new century.

Yes, gold has had trouble relative to stocks if you only consider the past decade. But there is good reason to think the next decade will be very different indeed.

Central Banks Are Losing Control

One of the reasons gold performed so well in June is that the Fed is abandoning their plan to raise interest rates and most watchers now expect officials to begin lowering again at the end of this month.

Officials cut rates to zero in an effort to spur growth. The move certainly worked wonders to drive stock prices, but it apparently didn’t do much to build lasting economic strength.

Share prices began collapsing late last year when it appeared the stimulus would be withdrawn.

Investors should be asking why, if the economy is so strong, is the Fed getting ready to change course and start cutting rates. After all, the idea was that officials should step on the gas (lower rates) when the economy is weak, and hit the brakes (raise rates) when the economy recovers.

Instead of viewing interest rate policy as a set of car pedals, FOMC officials should have looked at it like a dangerous drug. The financial markets are now hopelessly addicted to cheap money.

Spineless Fed bankers now only see one real option, where they had planned to have two.

They will try to keep rates artificially low – most likely until the nation overdoses on debt.

Stock Prices are Rising on Declining Volume While Gold Prices Are Rising on Increasing Volume

Fewer investors are inclined to buy shares, though they have not yet decided to sell. Among the players still inclined to buy are Central Banks which granted themselves a mandate to intervene anywhere and everywhere they see fit following the 2008 financial crisis.

The current rally in stocks may well be totally driven by the combination of officials promising to lower rates and instructing their internal trading desks to buy shares whenever there is even a whiff of trouble.

We can’t say for certain this is the case because central banks are the opposite of open and accountable. However, this amount of strength in share prices coupled with extraordinarily low volume sure smells fishy.

Many investors have concluded the Fed and other central banks are propping up the equity markets and they are determined not to sell. However, as mentioned above, central bankers appear to be losing control.

Now might be a good time to prepare for the day when all control is lost, rather than waiting until after. Given the rising trading volume in gold, perhaps that is exactly what some people are doing.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.