The Conference Board’s July consumer confidence report is due to come out later today. Consumer confidence is forecast to rise to 125.2.

In June, consumer confidence fell to 121.5.

The index for June missed estimates of 132.0 and fell from May’s headline print of 131.3. The present situation index fell to 162.6 from 170.7 in May. Meanwhile, the expectations index which is based on the short term outlook for income, business and labor market fell to 94.1 from 105.0 previously.

The consumer confidence index rose for three consecutive months until May before easing in June.

U.S. Consumer Confidence, June 2019

Consumer confidence has been gradually edging lower after peaking to 137.9 in October 2018. The steady decline reflects the ongoing uncertainty among consumers on a number of factors.

As of June, the consumer confidence index is at its lowest levels since September 2017.

The index is a leading measure of consumer spending which contributes to the overall gross domestic product activity in the United States.

Trade Tensions Weigh on Consumers

Consumers participating in the survey pointed to the trade tensions and higher tariffs. In the previous month, trade tensions had somewhat eased. However, with the US-China trade talks resuming, this issue is now back on the forefront.

Economists are yet to fully assess the impact of the trade wars so far. But it is the uncertainty that stems from them that affects consumer sentiment.

Although the consumer confidence index will not impact the markets much, it is seen as a leading indicator. Investors and consumers alike are no doubt concerned about slowing economic growth.

The Federal Reserve, on its part, has committed to lowering interest rates. The FOMC will be meeting this Wednesday, and interest rates are certain to be cut by at least a quarter basis point.

But the question remains whether this will be enough to bring back consumer confidence.

Within the short term, we expect consumer confidence to remain at the current levels. Despite the Fed rate cut, it will take at least a few months to see how consumers respond to lower interest rates.

With trade tensions still the main talking point, the effects of the Fed rate cut will see only a small impact.

Assessing the Economic Conditions in July

The general economic landscape in July was broadly stable. It wasn’t until the last two weeks of the month that the trade wars came up. Meanwhile, the International Monetary Fund lowered its growth forecasts.

However, for the US economy, growth was revised slightly higher to 2.6%.

In June, labor market data was robust, rebounding from the slump in the previous months.

Various Federal Reserve officials grew more vocal about cutting interest rates in a bid to avoid a sharper slowdown and perhaps even a possible recession. The general overview at the time is cautious.

Inflation for the month of June fell to 1.6% on an annualized basis. This was down from 1.8% in the month before. The core inflation rate, however, remained at 2.1%, beating forecasts of a decline to 2.0%.

As a result, we could possibly expect to see either the consumer confidence falling even further or perhaps a stabilizing. It is highly unlikely that consumer confidence will rebound sharply.

The data for July could still be well below the recent highs, especially that of October 2018 high of 137.9.

US stock indexes ended mixed on Monday dragged by financials and communication-discretionary sectors. The S&P 500 slipped 0.2% to 3020.97. Dow Jones industrial however added 0.1% to 27221.35. The Nasdaq composite slid 0.4% to 8293.33. The dollar strengthening decelerated ahead of Federal Reserve meeting starting today: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.1% to 98.05 and is higher currently. Stock index futures point to lower market openings today

FTSE 100 rallies while other European indexes slip

European stocks extended gains on Monday as companies reported positive quarterly results. The EUR/USD turned higher while GBP/USD accelerated its slide as the head of the Scottish Conservatives said that she would refuse to support the no deal Brexit, and both pairs are down currently. The Stoxx Europe 600 index ended 0.1% higher led by telecoms and financial services stocks. The DAX 30 slipped 0.02% to 12417.47. France’s CAC 40 slid 0.2% while UK’s FTSE 100 rallied 1.8% to 7686.61.

Nikkei leads Asian indexes rebound

Asian stock indices are recovering today after the Bank of Japan announced it will leave its monetary policy unchanged, as expected, and maintained its guidance of extremely low rates at least through spring 2020. Nikkei closed 0.4% higher at 21709.31 despite the yen climb against the dollar. Markets in China are rising ahead of U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin meeting with Chinese negotiators in Beijng: the Shanghai Composite Index is up 0.3% and Hong Kong’s Hang Seng Index is 0.2% higher. Australia’s All Ordinaries Index added 0.3% as Australian dollar continued its slide against the greenback.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

It has been under a week since Boris Johnson became the new UK Prime Minister and already the British Pound is sinking deeper into the abyss, sliding to a two-year low against the Dollar at 1.2220.

Concerns over the United Kingdom crashing out of the European Union with no Brexit deal in place is clearly haunting investor attraction towards Sterling which has weakened against every single G10 currency today. Michael Gove’s comments over the weekend on how the government is “operating on the assumption” of the UK leaving the EU has rubbed salt on an open wound for the British Pound.

With uncertainty over Brexit, the new conviction ahead of the October 31 deadline is that the path ahead for Sterling will be filled with many obstacles and more pain. If the GBPUSD can clear 1.2200, bears may be instilled with enough inspiration to test 1.2000.

GBPJPY tumbles to 2-year low

Fears of a no-deal Brexit have sent the GBPJPY tumbling to a two year below 133.00.

This currency pair is firmly bearish on the daily charts and is likely to sink lower once a daily close under 133.00 is secured. With attraction towards Sterling deteriorating by the day, the GBPJPY is set to test 132.00 in the short to medium term.

EURGBP blasts above 0.9050

A weaker Poundhas sent the EURGBP shooting back past 0.9050 today. A daily close above this point should open the doors towards 0.9170 this week.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

A description of this minerals firm’s findings and their implication are provided in a Haywood report.

In a July 23 research note, Haywood analyst Mick Carew reported that Osisko Mining Inc. (OSK:TSX) hit upon what it is calling Triple Lynx, four zones of gold mineralization between the Triple 8 discovery and the main Lynx corridor at its Windfall Lake project.

Carew depicted Osisko’s discovery. The new zones, he wrote, occur in a mineralized corridor at a depth of 650980 meters (650980m) below the main Lynx deposit. They continue downplunge beyond the scope of current drilling at the project.

Highlight drill hole OSK-W-17-1272 returned 12.1m grading 47.8 grams per ton (47.8 g/t) gold from a downhole depth of 858.4m, including 6.7m grading 63.5 g/t gold.

The gold mineralization encountered at Triple Lynx is characteristically similar to that of the upper Lynx deposit, according to Osisko. Both Triple 8 and Triple Lynx, which remain open in all directions, require further drilling to determine the relationship, if any, between them.

Osisko, Carew relayed, after hitting these new zones of mineralization, decided to add another 200,000m to its drill program at Windfall, taking it to 1,000,000m.

Carew concluded that “today’s results provide further support of our assumptions on the expansion potential of Windfall at depth. We await the results from further drilling.”

Haywood has a Buy rating and a CA$4.50 per share target price on Osisko Mining, whose stock is currently trading at around CA$3.67 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Haywood Securities, Osisko Mining Inc., Radar Flash, July 23, 2019

Analyst Certification: I, Mick Carew, hereby certify that the views expressed in this report (which includes the rating assigned to the issuers shares as well as the analytical substance and tone of the report) accurately reflect my/our personal views about the subject securities and the issuer. No part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendations.

Important Disclosures

Of the companies included in the report the following Important Disclosures apply: ▪The Analyst(s) preparing this report (or a member of the Analysts’ households) have a financial interest in Marathon Gold Corp. (MOZ-T), Pure Gold Mining Inc. (PGM-V).

▪ As of the end of the month immediately preceding this publication either Haywood Securities, Inc., one of its subsidiaries, its officers or directors beneficially owned 1% or more of Pure Gold Mining Inc. (PGM-V).

▪ Haywood Securities, Inc. has reviewed lead projects of Osisko Mining Corp. (OSK-T), Marathon Gold Corp. (MOZ-T), Pure Gold Mining Inc. (PGM-V), Treasury Metals Inc. (TML-T) and a portion of the expenses for this travel have been reimbursed by the issuer.

▪ Haywood Securities Inc. or an Affiliate has managed or co-managed or participated as selling group in a public offering of securities for Osisko Mining Corp. (OSK-T), Pure Gold Mining Inc. (PGM-V), in the past 12 months.

Other material conflict of interest of the research analyst of which the research analyst or Haywood Securities Inc. knows or has reason to know at the time of publication or at the time of public appearance: n/a.

We’re kicking off a really busy day for the markets in Japan! We have a host of key economic events coming out. And Wednesday and Thursday concentrate the bulk of Japanese corporate earnings.

After Friday, we could have a pretty good idea of what to expect out of the Nikkei for the next couple of months We will also get a better understanding of the respective impact that it will have on the currency.

What we’re focusing on right now is the main event of the week: the BOJ’s policy decision early tomorrow morning. As for a change in the interest rate, that’s largely ruled out. But what can drive the markets is the tone set by the bank. And there isn’t all that much consensus on what to expect – even from BOJ officials themselves.

What’s the Thinking Here?

Up until Thursday, there was something of a consensus that the Big Three of central banks – the Fed, BOJ, and ECB – would move in tandem, as part of a race-to-the-bottom scenario with interest rates.

Given the strong consensus of a rate cut from the Fed on Wednesday, the thought was that an ECB rate cut would be followed by some significant easing action from Kuroda.

But the ECB didn’t deliver, and there are lots of reasons for the BOJ to not want to cut rates either. This has left analysts divided as to how likely it is that we’ll get action. And, if we do, how strong it would be.

The thing is, weakness in the Japanese economy and a lack of inflation are sort of the norm for Japan. So, there isn’t really a pressing need for the bank to do something corrective about it.

It’s Outside

The case can be made that the biggest problems the Japanese economy has, in the short term, are rooted overseas:

Other countries are cutting rates, reducing the bond differential.

The trade wars of the US are catching Japan in the crossfire (as they are also renegotiating their trade agreement with the US).

The political dispute between Japan and Korea is escalating into economic actions, as well.

These issues are at least hopefully going to be resolved in the short term. The BOJ is notoriously out of ammunition by already having negative rates. And pushing further into unconventional measures would come at a high cost. So, if the trade issues are resolved quickly, that high cost will be in vain.

What to Do?

The latest survey of economists by Bloomberg shows an increasing move away from the BOJ keeping a dovish stance. Granted, it’s still a minority. Only a third of the economists polled think that the bank’s next action will be a step back from their historic accommodative cycle. The majority are still inclined towards easing.

The consensus, such as it is, suggests the BOJ will modestly change some of its forward guidance, by extending the outlook of when they plan to keep rates ultra-low. This wouldn’t be seen as a response to fundamentals, but simply as trying to appease the markets.

If, however, it’s interpreted as the BOJ being unwilling or unable to take stronger action, it can lead to substantial strengthening of the yen.

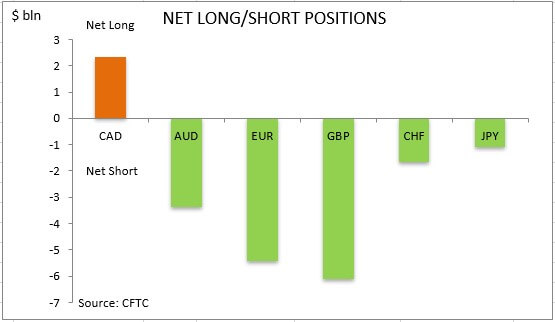

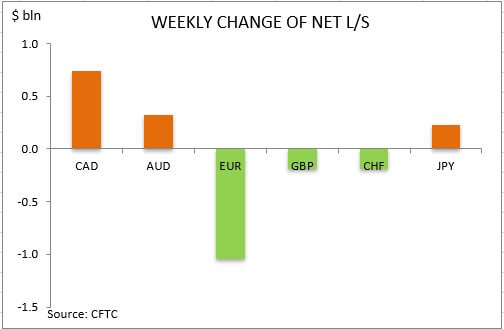

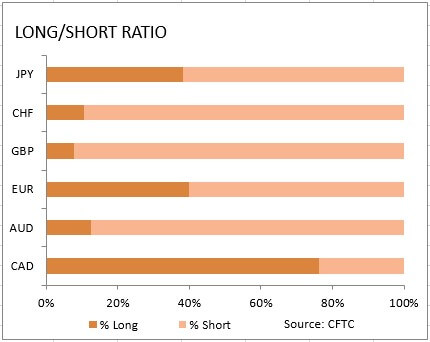

US dollar bullish bets inched up to $15.32 billion from $15.19 billion against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to July 23 and released on Friday July 26. The dollar strengthening resumed as steep interest rate cut expectations at July 30-31 meeting moderated after New York Fed said Williams’ comments about need to ‘act quickly’ referred to his academic research and not upcoming Federal Reserve meeting, and University of Michigan consumer sentiment index was revised upward.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

A Raymond James report indicates how it expects market conditions to affect margins of this Texas-based company in H2/19.

In a July 22 research note, analyst Praveen Narra reported that Raymond James lowered its target price on Halliburton Co. (HAL:NYSE) to $37 per share from $39 (the current share price is $23.03). The change reflects Raymond James reducing its H2/19 estimates on the energy company by 2% due to current weakened oilfield activity in North America and lower drilling and evaluation (D&E) margins.

Narra highlighted that despite those factors, Halliburton’s Q2/19 results were “ahead of expectations on better-than-expected completion and production (C&P) margins.”

Further, looking forward, Narra purported that Haliburton should continue generating free cash flow despite today’s flat oil prices if it continues cutting costs and potentially reduces capex in 2019. Raymond James expects Halliburton to generate, assuming a higher oil price, free cash flow of around $1 billion and $1.6 billion for 2019 and 2020, or, at today’s prices, a yield of 5% and 8%, respectively.

With respect to margins in specific corporate divisions, Narra pointed out that Halliburton likely will not see a rebound in its C&P numbers until 2020. This is because a slowing U.S. North American oilfield typically translates to depressed C&P margins for the company. Another reason is the likely continuing uncertainty in Q4/19 due to seasonality and exhausted budgets.

In contrast, Narra noted, D&E margins are “poised for improvement” because “international markets are expanding with early signs of pricing strength in pockets.” That stronger offshore and international activity could offset some of the weakness in North America. Also, as the rigs get working at the company’s North Sea and India projects, “this should lead to strong incremental margins,” added Narra. For D&E in Q3/19, Raymond James models roughly 65% incrementals and in Q4/19, 11.4% margins.

The financial services firm maintained its Strong Buy rating on Halliburton, wrote Narra, with its “significant upside to a U.S. oilfield recovery in 2020 under our group’s bullish oil price environment.”

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Raymond James, Halliburton Company, July 22, 2019

ANALYST INFORMATION

Analysts Holdings and Compensation: Equity analysts and their staffs at Raymond James are compensated based on a salary and bonus system. Several factors enter into the bonus determination, including quality and performance of research product, the analyst’s success in rating stocks versus an industry index, and support effectiveness to trading and the retail and institutional sales forces. Other factors may include but are not limited to: overall ratings from internal (other than investment banking) or external parties and the general productivity and revenue generated in covered stocks.

The analysts Praveen Narra and J. Marshall Adkins, primarily responsible for the preparation of this research report, attest to the following: (1) that the views and opinions rendered in this research report reflect his or her personal views about the subject companies or issuers and (2) that no part of the research analysts compensation was, is, or will be directly or indirectly related to the specific recommendations or views in this research report. In addition, said analyst(s) has not received compensation from any subject company in the last 12 months.

RAYMOND JAMES RELATIONSHIP DISCLOSURES Certain affiliates of the RJ Group expect to receive or intend to seek compensation for investment banking services from all companies under research coverage within the next three months.

Raymond James & Associates, Inc. makes a market in the shares of Halliburton Company.

Additional Risk and Disclosure information, as well as more information on the Raymond James rating system and suitability categories, is available here.

Daniel Carlson of Tailwinds Research examines the “blockbuster” implications of a recent announcement about this company’s OnTrak program.

Sometimes big news falls on deaf ears. Which, by the way, is one of the reasons I like the micro-cap space. With only a few analysts, if any, focused on a company, meaningful news can often be overlooked for days or weeks. What happened July 23 in Catasys Inc. (CATS:OTCBB) is a classic example of the market not fully grasping the importance of a press release.

In our opinion, the news out of Catasys was game-changing and deserving of a revaluation in the market. Instead, the stock went down. The result of this is a great buying opportunity for those who have yet to get their fill of CATS.

First off, a little background. We have been bullish on Catasys for a long time here at Tailwinds. The main thesis of our recommendation has been the incredible growth opportunity in front of them as they roll out their OnTrak program to larger patient populations. Based on historical numbers, if nothing changes, they are poised to earn $120 million or more in revenue in 2020, up from around $38 million this year. Catasys is a great growth story just starting to unfold.

However, what has always intrigued us, and why we have made this such a large holding here at Tailwinds, is the upside to the story. Yes, Catasys is making great progress in diagnosing and treating mental health disease, but there’s an even bigger opportunity here. As we wrote about over a year ago, Catasys is in the process of gaining more access to medical records, and outcomes, than any other company out there.

Here’s a portion of what we said at that time:

“If Catasys signs seven of the eight largest health insurers as clients, which they are well on their way to doing. . .and, if these clients continue to roll out OnTrak across their network. . .Catasys could, theoretically, have the patient healthcare data for well over half of all Americans.

“The implications of this are incredibly broad and extend well beyond their OnTrak program and its effectiveness. With more data on patients, including outcomes, Catasys will be able to create many different programs to offer to insurers. The potential of OnTrak is huge; the longer-term potential inherent in them having the most healthcare data on the planet is much bigger.”

The July 23 press release, in which the company discussed expanding their capabilities beyond behavioral health conditions, is the start of what we saw coming. Catasys is taking their unprecedented access to medical records and combining it with an industry-leading artificial intelligence (AI) team to start looking for more ways they can help diagnose disease and, thereby, help patients while saving insurers money.

As their CEO, Terren Peizer, stated in the press release:

“The data from healthcare delivery is complex, rarely interoperable and therefore underused. Using the latest techniques in AI and over a decade of research, Catasys has solved these challenges by creating what we believe to be the most valuable technology platform for populations that are care avoidant or not engaging in care. We can now predictively and rapidly identify care avoidant individuals with major chronic disease and those for whom targeted interventions will improve outcomes and reduce the cost of care.”

The implications of this are absolutely huge for investors in Catasys. The number of Americans who suffer major chronic disease is a much larger pool than those with only behavioral health disease. These people also cost the healthcare system a lot more money. This is the reason that Peizer said, “Catasys health plan partners have encouraged us to make these new AI capabilities available as soon as possible.”

By expanding their offering, Catasys has greatly expanded the number of potential enrollees in their programs. They have also given service providers an increased urgency to sign onto the platform and roll out new territories and diseases.

We believe Catasys will be announcing new programs with healthcare plans soon. OnTrak 2.0, which really leverages the data Catasys has at their fingertips, has been in development for a while. These newfound capabilities will be part of OnTrak 2.0, making it that much more compelling; I suspect we’ll start seeing adoption by insurers in the near future.

Meanwhile, the target outreach pool for Catasys has just grown exponentially. And this might only be the tip of the iceberg. What other products will they be able to develop with their AI capabilities? Catasys has access to more healthcare records than anyone, plus a team that knows how to leverage this information. One can imagine numerous other products over time.

Despite this blockbuster announcement, shares of Catasys are have traded down over the last week. What is causing this? I believe there are two reasons for the weakness in CATS. First, former board member David Smith has been a continual seller of shares. As of July 15, he still owned over 1 million shares, despite ongoing sales. This has certainly been an overhang for the stock.

More importantly, the short interest in CATS has been increasing, along with the borrowing rate for shares. I believe the shorts are hurting in this trade and are trying to push shares down. There’s been a persistent rumor of a secondary offeringa rumor that Peizer has continually refuted. However, as long as the company burns cash and there’s a short position, that rumor will persist.

From our perspective, the sales by Smith and a potential (albeit unlikely) secondary don’t worry us. We prefer to look at the big picture here. And, with the July 23 press release, the picture has gotten that much bigger.

Catasys is on the verge of being a powerful force in finding and treating mental, and now physical, health diseases. We eagerly look forward to watching the story unfold over the next several years as bigger rollouts happen, and as CATS continues to diagnose and treat more diseases. The current business is great, but the future remains even bigger than most investors can believe.

Daniel Carlson is the founder and managing member of Tailwinds Research Group and its parent company DFC Advisory Services, which is a licensed registered investment advisor (CRD # 297209). Tailwinds is a microcap focused research company that provides research on and consults to over 20 emerging growth companies in the technology and life sciences arenas. DFC Advisory Services is an RIA that manages money dedicated to investing in the companies covered by Tailwinds. For more information on these two companies and their track record, please see www.tailwindsresearch.com. Prior to founding these two entities, Dan spent many years working with small public companies, having been CFO of two public companies and helping finance many others. A 1989 graduate from Tufts University with a degree in Economics, Dans formative years in business were spent as an equity trader, first on the Pacific Coast Stock Exchange then on the buyside at several multi-billion dollar firms.

This article was submitted by Tailwinds Research. For more information on Tailwinds Research or on Catasys, please visit www.tailwindsresearch.com.

Tailwinds owns stock in Catasys. For a complete list of disclosures, please click here.

Disclosure: 1) Daniel Carlson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Catasys. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. Additional disclosures and disclaimers are above. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The issue of potential US currency intervention has taken on greater focus over recent months.

This view has grown steadily, in line with consistent comments made by President Trump regarding both the excessive strength of the US dollar as well as his desire for the Fed to refrain from tightening monetary policy.

However, despite the comments which Trump regularly makes on Twitter and in interviews, the President has yet to intervene in the markets. That being said, recent reports indicate that such a move has been considered.

White House Adviser Says Currency Intervention Ruled Out

Speaking with CNBC last week, White House adviser Larry Kudlow said:

“Just in the past week, we had a meeting with the president and the economic principles and we had ruled out any currency intervention”.

During the interview, Kudlow explained that officials had discussed all the options open to them in the meeting. This included using the US Treasury’s $94 billion exchange stabilization fund, which they ultimately rejected.

Trump Backpedals

However, Trump confusingly told reporters, only hours after Kudlow’s interview:

“I didn’t say I’m not going to do something”.

The situation is the latest in a series of recent public back-and-forth policy blunders from Trump. And it echoes the ordering of an airstrike on Iran not too long ago.

For the market, it was a telling insight into the administration’s preoccupation with USD strength. Indeed, Kudlow’s comments will likely have added further support for the greenback.

The USD has been rallying strongly ahead of the FOMC this week.

FOMC In Focus

At this point, we can expect the Fed to cut rates by .25% this week. However, USD has been supported by the pullback in market pricing for a larger .50% rate cut which has seen its odds slashed from around 70% to 20% in light of better than expected US data last week, as well as clarification around dovish comments made by Fed’s Williams.

Fed Clarifies Dovish Comments

During a speech at the Central Bank Research Association, Williams said that the Fed “should act quickly” and should not look to keep its powder dry. These comments were taken by the market as a sign that the Fed would likely cut by the larger .50%.

However, the Fed then made the unusual move of clarifying William’s comments. A spokesperson for the Fed said of Williams’ comments:

“This was an academic speech on 20 years of research. It was not about potential policy actions at the upcoming FOMC meeting,”

The greenback continues higher today as the market now perceives a lower likelihood of the Fed cutting by .50%. In fact, there is a risk now that if the Fed does proceed and cut rates by the expected .25%, that USD will continue to trade higher out of disappointment.

The market is hopeful that the two sides will be able to deliver a deal this time around, avoiding further tariffs and the accompanying global uncertainty. The talks will be closely watched by the Fed, given the importance it has placed on risks from the trade war. However, any deal will likely take a long time to come to fruition and talks are likely to be labored once again.

Technical Perspective

The USD Index continues to rally higher this week as the recovery above the 97.11 level continues. For now, price is trading in the middle of the recent bullish channel nearing the 2019 98.30 highs. Above here, the next level to watch will be the channel top with further structural resistance around 99.24. To the downside, any move lower here will put a focus on a test of the channel low, with structural support coming in also around 95.42.

First, a bank’s commodities trading department takes metals investors for a ride like unwitting victims in the back of Jeffrey Epstein’s “Lolita Express.”

Now federal prosecutors have extended the same sort of cozy non-prosecution agreement to shield the bank itself from a criminal indictment.

Federal prosecutors signed a non-prosecution agreement in June with Merrill Lynch Commodities, Inc. (MLCI) and Bank of America (Merrill’s parent company) for rigging the precious metals markets.

The U.S. Department of Justice (DOJ) found gold and silver traders working at Merrill Lynch had “schemed to deceive other market participants by injecting materially false and misleading information into the precious metals futures market.”

The agreement references “thousands of fraudulent orders” – intended artificially to move the markets up or down by “spoofing” other traders and investors – over a period of 6 years.

Two traders have been indicted on criminal charges so far. The non-prosecution agreement was only for the mega bank, not for its more expendable staff.

The bank gets off with a less-than-consequential $25 million fine, a promise not to do it again, and a commitment to set up more controls… which they can self-monitor.

The generous agreement was granted in part because “MLCI has no prior criminal history.” The prosecutors who drafted the agreement must not have had access to the Department’s own files, or the internet.

Suffice it to say the malfeasance covered here isn’t the first bit of shady activity Merrill has been involved in. DOJ prosecutors also didn’t take into consideration Bank of America’s own record. Both organizations have been implicated in schemes, scandals, and frauds going back decades.

Here is a partial list of what the bankers have been accused of doing to clients, shareholders and other victims (a more complete accounting can be found here):

Screwing the State of California as its Bond Trustee

Charging excessive fees

Withholding information from shareholders

Foreclosure fraud

Deceptive sales practices

Maybe prosecutors limited their definition of “criminal history” to past criminal convictions. There would undoubtedly be a lot more of those if Justice Department prosecutors stopped settling and signing non-prosecution agreements and instead started taking the banks to trial for their role in crimes.

Bank of America has a history of cutting deals with the Department of Justice.

In 2014, for example, the DOJ crowed about “the largest civil settlement with a single entity in American history.” Prosecutors settled allegations of massive mortgage fraud in return for $16.65 billion in penalties and restitution.

Prosecutors seem to have forgotten the bank’s involvement in that mess.

It isn’t clear whether any amount of crooked behavior would be sufficient for officials to finally prosecute and seek to ban these banks from trading in the markets.

As part of the June agreement, Bank of America agreed to ramp up internal controls and training to prevent future fraud.

That will be small comfort to anyone who has read the Bank’s rap sheet, but DOJ prosecutors seem confident that Bank of America will start policing itself. They “determined that an independent compliance monitor was unnecessary.”

The agreement not to pursue criminal charges is, naturally, framed as a big win for victims in the DOJ press release.

In order to see just how much “winning” there is, we encourage victims to send an email to [email protected]. The DOJ promises to reply with more information about how victims of the market rigging can get compensation.

We have yet to receive a response to the email we sent.

Those with the time can also call the toll-free victim hotline – 888-549-3945 – where they will go straight to voicemail. There has not yet been a reply to the message we left there either.

Victims may have to accept the Justice Department’s word that the $25 million penalty “represents the combined appropriate criminal fine, forfeiture, and restitution amounts in this matter.”

It’s a good round number – probably crafted to sound like a hefty amount to average citizens. It is, however, a paltry sum for the behemoth bank. It sounds woefully inadequate given the thousands of fraudulent orders and 6 years of history under review.

Plus, the agreement makes no mention of the huge numbers of metals investors who didn’t trade in the futures markets, but who relied upon the phony price setting that goes on there. This includes investors in physical bullion.

The beauty (for DOJ prosecutors and perpetrators cutting these deals prior to evidence being heard in court) is that there is no accounting as to whether the penalty is commensurate with the crime.

Victims don’t know, for example, what officials estimate as the total illicit gains related to the price rigging. It’s possible nobody at Justice bothered to make an estimate.

Thus far Deutsche Bank and Bank of America have cut deals on the issue of price rigging in the precious metals markets. Meanwhile the high-profile indictments, based on all the “cooperation” prosecutors are supposedly getting, have yet to materialize.

Perhaps the DOJ plans to secure non-prosecution agreements with the other bullion banks involved. It is not hard to imagine a scenario where several banks agree to cooperate against one another, but none gets convicted because prosecutors gave them each one of these nifty shields.

The sordid story of Jeffrey Epstein case reveals something really important about how non-prosecution agreements are used to protect the well-connected from accountability.

It is time the Department of Justice stopped settling out with terrible human beings and the organizations they run. Actual justice for precious metals investors will involve throwing cheating bank executives in prison and tossing the crooked banks out of the markets.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.