By TheTechnicalTraders.com

On July 31, 2019, the US Federal Reserve decreased the Federal Funds Rate (FFR) by 25 basis points. We believe the US Fed was pushed to take this action for three reasons that are directly related to the fear and greed that is abundant in the global markets.

Reason #1 Fed Had To Cut Rates

First, the US Fed is very concerned that the US housing market has stagnated and weakened over the past 16+ months. The Fed has pushed the FFR towards our modeling system’s upper boundary (2.0 to 2.25) many months ago and this has pushed the housing market over a supply/demand precipice that may already be too far gone for a substantial recovery. The US Fed, attempting to prevent another housing market collapse, must attempt to ease lending in an attempt to spark new real estate activity.

Reason #2 Fed Had To Cut Rates

Second, the US Fed must attempt to ease the foreign market US Dollar carry trade liabilities and attempt to allow more US Dollar opportunity in the foreign economy. Over the past 2 to 3+ years, the supply of US Dollars within the foreign markets has diminished considerably while demand has increased. Because of this, a US Dollar shortage currently exists in much of the global economy. The US Fed is attempting to allow more US Dollar supply by lowering the FFR.

Reason #3 Fed Had To Cut Rates

Lastly, the US Fed, attempting to accommodate a more adaptable rates policy in order to more adequately facilitate the global economic turmoil that is persistent throughout the world. Even though the US economy is still very strong and showing only mild signs of weakness currently, the US Fed felt the need to become more accommodating to allow more flexibility for global central banks to navigate through the current trade and geopolitical issues.

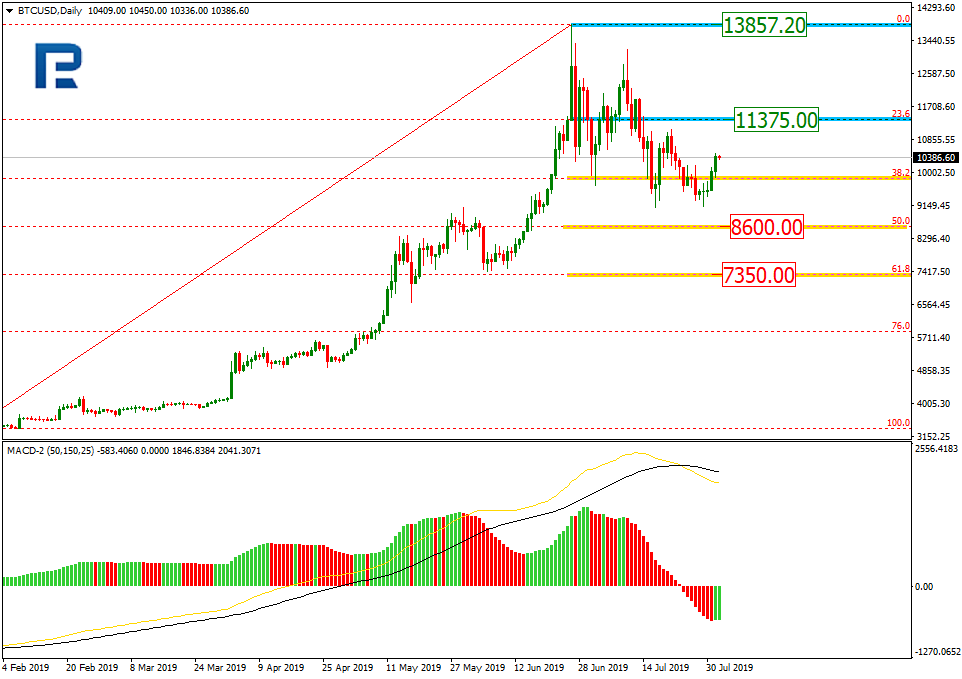

Dollar Hits Resistance And Should Reverse Down

Metals reacted by moving lower as the US Dollar rallied after the Fed announcement. The US Dollar is currently near the upper price channel that we believe will prompt a weaker US Dollar over the next few weeks and will likely prompt a move lower over the next few weeks – allowing metals the ability to skyrocket higher over this same span of time.

Gold Set To Rock Higher

Gold is reacting to the US Dollar/Fed news by rotating within the black line and magenta arc levels that we highlighted weeks ago. These Fibonacci Price Amplitude Arcs highlight key price levels that are acting as resistance for Gold right now. Once price breaks these levels, Gold will skyrocket above $1550 and likely target $1650 or higher.

Silver Ready To Rally

As we’ve highlighted several times, Silver is likely the best trading opportunity set up on the planet right now. We’ve highlighted where we are currently (“We Are Here”) and where we believe the price will move to in the future on this chart. Using our Fibonacci Price Amplitude Arc levels and Fibonacci price ranges, we can “guess” where price may target in the future and where peaks and valleys may form. We believe silver is setting up for a move to levels above $21~$22 right now and will begin this move higher within the next 2 to 5 weeks.

Even though the US Fed is attempt to act as a savior for the global central banks and attempting to easy US monetary policy while the global markets attempt to address their political and economic issues, we believe the US economy is uniquely strong in relation to other global economies and we believe the fear/greed factors will continue to increase over the next 15+ months or longer.

Gold and Silver are setting up to become some of the best trades we’ve seen in a very long time for us, technical traders. We believe Silver could rally well above $30 over a very short period of time. Don’t worry about the rotation in the metals markets as a reaction to the US Fed. The real news is that the US Dollar has reached the upper price channel limit which should prompt a bigger upside move in the US metals.

CRUCIAL WARNING SIGNS ABOUT GOLD, SILVER, MINERS, AND S&P 500

In early June I posted a detailed video explaining in showing the bottoming formation and gold and where to spot the breakout level, I also talked about crude oil reaching it upside target after a double bottom, and I called short term top in the SP 500 index. This was one of my premarket videos for members it gives you a good taste of what you can expect each and every morning before the Opening Bell. Watch Video Here.

I then posted a detailed report talking about where the next bull and bear markets are and how to identify them. This report focused mainly on the SP 500 index and the gold miners index. My charts compared the 2008 market top and bear market along with the 2019 market prices today. See Comparison Charts Here.

On June 26th I posted that silver was likely to pause for a week or two before it took another run up on June 26. This played out perfectly as well and silver is now head up to our first key price target of $17. See Silver Price Cycle and Analysis.

More recently on July 16th, I warned that the next financial crisis (bear market) was scary close, possibly just a couple weeks away. The charts I posted will make you really start to worry. See Scary Bear Market Setup Charts.

CONCLUDING THOUGHTS:

In short, you should be starting to get a feel of where each commodity and asset class is headed for the next 8+ months. The next step is knowing when and what to buy and sell as these turning points take place, and this is the hard part. If you want someone to guide you through the next 12-24 months complete with detailed market analysis and trade alerts (entry, targets and exit price levels) join my ETF Trading Newsletter.

Be prepared for these incredible price swings before they happen and learn how you can identify and trade these fantastic trading opportunities in 2019, 2020, and beyond with our Wealth Building & Global Financial Reset Newsletter. You won’t want to miss this big move, folks. As you can see from our research, everything has been setting up for this move for many months.

Join me with a 1 or 2-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next financial crisis.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities starting to present themselves will be life-changing if handled properly.

FREE GOLD OR SILVER WITH MEMBERSHIP!

Kill two birds with one stone and subscribe for two years to get your FREE PRECIOUS METAL and get enough trades to profit through the next metals bull market and financial crisis!

Chris Vermeulen – TheTechnicalTraders.com