On its latest 21-month chart we can see that about a week ago it tried and failed to break out of a large Cup & Handle base pattern. This failure was not negative, for several reasons. One is that the attempt occurred on strong volume, which is bullish, especially as this was the culmination of a build up in upside volume for a couple of months prior to it. Another is that the reaction back into the base was on much lighter volumeso it looks like it needs to do a little more work in the base pattern before it makes a sustainable breakout. Several factors support a successful breakout attempt soon. One is the buildup in upside volume already mentioned, another is the strong Accumulation line resulting from this, and still another is moving averages being in bullish alignment because the stock is trending higher.

We can see the breakout attempt and subsequent reaction back in more detail on the 6-month chart.

The long-term 18-year chart is also interesting, not just because it shows that Goldcliff is historically very cheap here, but also because it reveals that the Cup and Handle base that we looked at on the 21-month chart fits within a much larger Cup and Handle base that dates back to 20122013, which can be “opened out” using a log chart.

The conclusion is that Goldcliff is a speculative buy here after its reaction back of recent days to support in the vicinity of its rising 50-day moving average. The stock trades in light volumes on the US OTC market where limit orders should always be employed.

Disclosure: 1) Clive Maund: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. CliveMaund.com disclosures below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Goldcliff Resource Corp., a company mentioned in this article.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

Shares of Reata Pharmaceuticals are trading 12% higher today after the firm announced it had reacquired all licensing rights in the U.S. for bardoxolone methyl and worldwide rights for omaveloxolone and other next-generation Nrf2 activators from AbbVie.

Clinical-stage biopharmaceutical company Reata Pharmaceuticals Inc. (RETA:NASDAQ) yesterday announced the reacquisition of “development, manufacturing and commercialization rights concerning its proprietary Nrf2 activator product platform originally licensed to AbbVie Inc. (ABBV:NYSE) for territories outside of the United States with respect to bardoxolone methyl (bardoxolone) and worldwide with respect to omaveloxolone and other next-generation Nrf2 activators.” The company advised that “as a result it now possesses exclusive, worldwide rights to develop, manufacture and commercialize bardoxolone methyl (bardoxolone), omaveloxolone, and all other next-generation Nrf2 activators, excluding certain Asian markets for bardoxolone which are licensed to Kyowa Kirin Co. Ltd.”

The report outlined in the terms of the deal that “as consideration for the rights reacquired by Reata, AbbVie will receive a total of $330 million in cash, primarily for rights to bardoxolone. Reata will make an upfront payment of $75 million in 2019, with the remainder payable in installments in Q2/20 and in Q4/21. AbbVie will also receive low single-digit, tiered royalties from worldwide sales of omaveloxolone and certain next-generation Nrf2 activators, and no royalties on bardoxolone.”

Warren Huff, Reata’s CEO and president, commented, “AbbVie has been an excellent partner, and our collaboration was instrumental in the clinical development of bardoxolone and omaveloxolone…Regaining these rights will increase Reata’s strategic flexibility and control regarding the development and commercialization of our lead drug candidates, and our next-generation Nrf2 activators. We have been actively preparing for the commercial launch of bardoxolone and omaveloxolone in the United States, and we will now expand our efforts to include these international territories as well.”

Reata also reported that it amended its loan and security agreement with Oxford Finance LLC and Silicon Valley Bank with the overall term loan facility increasing by $30 million to $155 million. The company advised that the amendment will make $75 million available to Reata upon positive, topline, registrational data from either the CARDINAL study of bardoxolone methyl in patients with Alport syndrome or the MOXIe study of omaveloxolone in patients with Friedreich’s ataxia.

The company also announced today that three abstracts highlighting clinical and nonclinical data for bardoxolone methyl (bardoxolone) will be presented at the American Society of Nephrology Kidney Week 2019 Annual Meeting scheduled for early November in Washington, D.C.

The firm notes that the three titles for the presentations are as follows: “Activation of the Keap1/Nrf2 pathway increases GFR by increasing glomerular effective filtration area without affecting the afferent/efferent arteriole ratio,” by presenter Kengo Kidokoro, M.D. Ph.D., Department of Nephrology and Hypertension, Kawasaki Medical School, Kurashiki, Okayama, Japan; “Effect of Bardoxolone Methyl on Kidney Events in Patients with Chronic Kidney Disease Stage 4 and Type 2 Diabetes at High Risk of Adverse Kidney Outcomes,” by presenter Christoph Wanner, M.D., Department of Medicine and Chief of the Division of Nephrology, University of Würzburg, Germany; and “A Cardiovascular Risk Mitigation Strategy on the Safety of Bardoxolone Methyl Post-BEACON,” to be presented by Pablo E. Pergola, M.D., M.Ph., Research Director, Renal Associates, PA, San Antonio, TX.

The company explains that “bardoxolone is an experimental, oral, once-daily activator of Nrf2, a transcription factor that induces molecular pathways that promote restoration of mitochondrial function, reduction of oxidative stress, and inhibition of pro-inflammatory signaling. The FDA has granted orphan drug designation to bardoxolone for the treatment of Alport syndrome, autosomal dominant polycystic kidney disease, and pulmonary arterial hypertension. The European Commission has granted orphan drug designation to bardoxolone for the treatment of Alport syndrome. Bardoxolone is currently being studied in CARDINAL, a Phase 3 study for the treatment of Alport syndrome, FALCON, a Phase 3 study for the treatment of ADPKD, CATALYST, a Phase 3 study for the treatment of connective tissue disease-associated pulmonary arterial hypertension, and AYAME, a Phase 3 study for the treatment of diabetic kidney disease in Japan which is being conducted by Reata’s licensee Kyowa Kirin Co., Ltd.”

Reata Pharmaceuticals is based in Irving, Tex., and identifies its business as “a clinical-stage biopharmaceutical company that develops novel therapeutics for patients with serious or life-threatening diseases by targeting molecular pathways involved in the regulation of cellular metabolism and inflammation.” Reata indicates that “its two most advanced clinical candidates, bardoxolone methyl and omaveloxolone, target the important transcription factor Nrf2 that promotes restoration of mitochondrial function, reduction of oxidative stress, and inhibition of pro-inflammatory signaling. Bardoxolone and omaveloxolone are investigational drugs, and their safety and efficacy have not been established by any agency.” The company’s lead candidates, bardoxolone methyl and omaveloxolone, are being evaluated in pivotal clinical trials for the treatment of a variety of chronic and genetic diseases including: Alport syndrome (AS); Friedreich’s ataxia (FA); connective tissue disease-associated pulmonary arterial hypertension (CTD-PAH); and autosomal dominant polycystic kidney disease-chronic diseases (ADPKD). The company also is evaluating bardoxolone methyl for other rare forms of CKD, including: IgA nephropathy, type 1 diabetic CKD, and focal segmental glomerulosclerosis.

Reata Pharmaceuticals began the day with a market capitalization of about $2.6 billion with approximately 30.11 million shares outstanding. As of the close of business yesterday, the firm had a short interest of about 10.4%. RETA shares opened today at $87.23 (+$1.25, +1.45%) compared to yesterday’s closing price of $85.98. The stock has traded today between $87.19 and $95.70/share and currently is trading at $96.62 (+$10.64, +12.37%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Technical analyst Clive Maund explains why he believes this company with projects in Thailand and Indonesia is about ready to start another upleg.

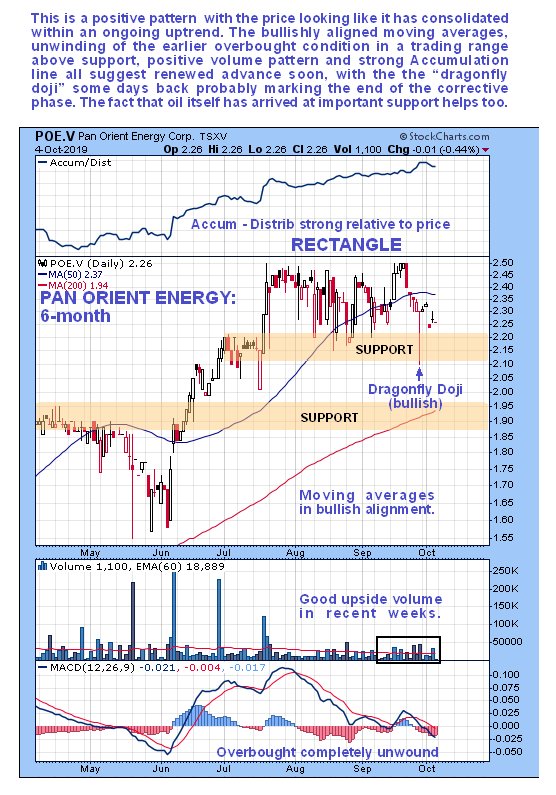

Pan Orient Energy Corp. (POE:TSX.V) presents an overall positive picture of a stock that is probably on the verge of breaking out of a large base pattern. On its 6-month chart we can see that it is definitely in an uptrend, within which it has been consolidating for about 10 weeks now. The sharp intraday drop about a week ago, which left behind a bullish “dragonfly doji” on the chart, marks the likely end of the correction / consolidation phase, and with the 200-day moving average pulling up beneath the price, it looks about ready to start another upleg. The recent volume pattern is favorable, with good upside volume that drove the accumulation line to new highs, a positive sign.

The 10-year chart reveals that a large Double Bottom formed in Pan Orient from early 2016 through late 2018, and the price now appears to be consolidating ahead of an attempt to break out of the entire base pattern which will be signified by a breakout above the resistance level shown which extends up to a little above C$2.50.

It is regarded as a good sign that Pan Orient has only reacted back modestly as the price of oil has reacted back quite sharply to an important support level shown on the 6-month chart for Light Crude below that has a good chance of generating at least a temporary reversal in the oil price, which will of course, should it happen, have a beneficial effect on the price of many oil stocks.

Pan Orient is therefore viewed as being at a favorable entry point here, and a stop may be placed just below the intraday low of the dragonfly candle at, say, $2.08.

Pan Orient Energy Corp. POE.V, POEFF on OTC, closed at C$2.26, $1.73 on 4th October 2019.

Originally posted on CliveMaund.com at 1.25 pm EDT on 6th October 2019.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Clive Maund: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. CliveMaund.com disclosures below. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Pan Orient Energy. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Pan Orient Energy, a company mentioned in this article.

Charts provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

There is a substantial amount of market-moving data coming out of Europe tomorrow.

The most important is likely to be employment data from the UK. The rate of job seekers is likely to stay at the lowest since the ’70s.

Half an hour later, we have a big event for the continent, the ZEW Economic Sentiment Survey from Germany. Expectations are for this to slip even further into contraction.

The theme of the day is the potential for currency divergence, which helps us understand long term trends for the euro and pound.

Is the UK diverging from the eurozone, or is the concern over Brexit leading to economic (and therefore, currency) convergence? Let’s have a look.

Data and Expectations

There are several bits of UK data coming out at the same time. However, it’s usually the Claimant Count Change that moves the market.

The consensus of expectations is that the UK lost a net of 16.6K jobs in September. This would be around half of the 28.2K registered in the prior month. It would also be the lowest number since March of this year, which was supposed to be another Brexit deadline. The number of people seeking benefits has slowly been increasing this year.

Despite rising employment claims, the consensus among economists is that the UK’s employment rate will stay at 3.8%. This appears to be a floor that the rate hasn’t managed to get below since April. This is also well below what most economists agree is the structural level, which would imply increasing labor tightness and higher inflation in the future.

Speaking of which, we also get Average Weekly Earnings. Expectations are for these to have grown by 3.7% in September, a slowing of the pace from 4.0% in the prior month. This is well above the inflation rate and would be expected to nudge the BOE towards keeping interest rates steady.

There are other data points that could also have a minor influence on the pound all happening at the same time. Employment Change is one example of them.

But, right after the data release, traders might want to keep an eye open for BOE Governor Carney’s Speech. He’ll be speaking in front of the Treasury Select Committee on the FSR. And his comments are likely to be relevant to the market if he were to unexpectedly give some change in the BOE’s guidance!

The Germany Effect

A bit later, we get the first survey of German businesses following the ECB’s latest rate cut.

Economic sentiment last month was boosted well above expectations as businesses priced in the potential of monetary policy. But it wasn’t enough to bring the outlook into the positive, and the consensus is for a more bleak outlook

Expectations are for the German ZEW Economic Sentiment Indicator to come in at -33.4, a substantial move back into contraction from -22.5 recorded in the prior month. This is the one that the market focuses on because it’s how businesses see the situation over the next six months. This is a key time period getting through the relatively lower production period in the winter.

We can also expect the German ZEW Economic Situation indicator to decline, but not so much. Projections indicate that it will go down to -23.2 from -19.9 prior. As usual, the current situation is better than the outlook, given the uncertainties in the future.

The ZEW also publishes an Economic Sentiment Indicator for the eurozone. We can also expect this to fall deeper into contraction at -33.0 compared to -22.4 prior. It will mostly be dragged down by poor performance in Germany.

After that, the market would be expected to trade primarily on technicals!

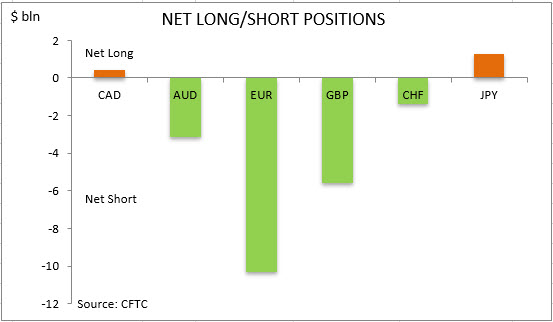

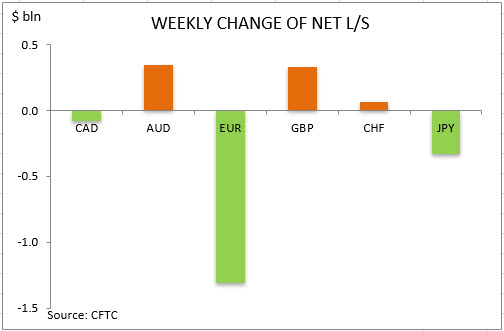

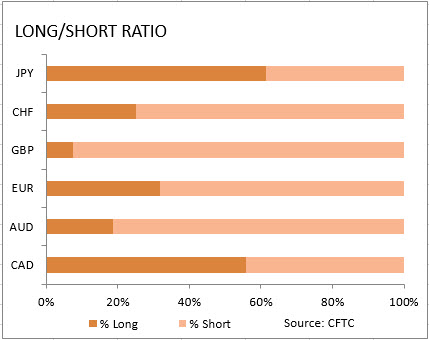

US dollar bullish bets rose to $18.78 billion from $17.80 billion against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to October 8 and released on Friday October 11. Increase in dollar bullish bests continued as US economy added 136,000 new jobs in September after 164,000 new jobs in August, and unemployment rate dropped to 3.5% from 3.7% in August.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of Ra Pharmaceuticals doubled today after the firm announced that it will be acquired by Belgian firm UCB for $48 per share in an all cash deal.

Prior to the market open this morning Ra Pharmaceuticals Inc. (RARX:NASDAQ) and Brussels-based UCB (UCB:Euronext)announced that they entered into a merger agreement in which UCB will acquire Ra Pharma for US $2.1 billion. Under the terms of the agreement, Ra Pharma shareholders will receive $48 in cash for each Ra Pharma share at closing.

The report advised that the Boards of Directors of both companies have “unanimously approved the transaction subject to approval by Ra Pharma shareholders and obtaining antitrust clearance and other customary closing conditions.” UCB advises that the acquisition of Ra Pharma will be financed by a combination of existing cash resources and new bank term loans and that the acquisition will not impact its 2019 financial guidance. UCB and Ra Pharma expect to complete the transaction by the end of Q1/20.

Ra Pharma identifies its business as a clinical-stage biopharmaceutical company that leverages its proprietary peptide chemistry platform to develop novel therapeutics for the treatment of serious diseases caused by excessive or uncontrolled activation of the complement system, a critical component of the innate immune system. The firm states that its “ExtremeDiversity” platform enables the production of synthetic macrocyclic peptides combining the diversity and specificity of antibodies with the pharmacological properties of small molecules.

Ra Pharma’s phase 3 product candidate zilucoplan is a once-daily self-administered, subcutaneous peptide inhibitor of C5. Zilucoplan is currently being tested in a phase 3 study for the treatment of generalized myasthenia gravis (gMG) with top-line results expected in early 2021. The company explains that “gMG is an unpredictable, chronic auto-immune condition in which auto-antibodies attack specific proteins in the neuro-muscular junction. This disrupts the way that nerves can communicate with muscles, resulting in muscle weakness and fatigue…gMG is a rare disease impacting almost 200,000 patients in the U.S., EU and Japan.”

Doug Treco, Ph.D., president and CEO of Ra Pharmaceuticals, commented: “UCB shares our commitment to the rare disease patient community and our goal of developing novel, accessible, and cost-effective therapies in the areas of immunology and neurology. I firmly believe it is the right partner for us to advance new treatment options from our unique early and late stage pipeline to patients. Ra Pharma’s technology platform is an ideal addition to UCB’s leading innovation capabilities, and our scientists are looking forward to working with the entire team at UCB.”

UCB’s CEO Jean-Christophe Tellier added, “Ra Pharma is an excellent strategic fit addressing multiple areas of UCB’s patient value growth strategy. Upon closing, the acquisition will add to our strong internal growth opportunitiessix potential product launches in the next five years, strengthening our neurology and immunology franchises with late and early-state pipeline projects. In addition, the combination will provide us with the opportunity to become a leader in treating people living with myasthenia gravis, an auto-antibody mediated neurological orphan disease with high unmet medical need, as well as adding a highly productive technology platform to our innovation engine.”

Ra Pharma is headquartered in Cambridge, Mass., and states it is “focused on leading the field of complement biology to bring innovative and accessible therapies to patients with rare diseases. The company discovers and develops peptides and small molecules to target key components of the complement cascade.”

UCB, based in Brussels, Belgium, is a “global biopharmaceutical company focused on the discovery and development of innovative medicines and solutions” for treating diseases of the immune and central nervous systems. The company employs more than 7,500 people in around 40 countries.

UCB, which trades under the symbol UCB on the Euronext Brussels exchange, has market cap of about 12.534 billion. UCB shares closed today in Europe at 11:30 a.m. EDT at 64.38 (+1.18, +1.87%) compared to Wednesday’s closing price of 63.20.

Ra Pharmaceuticals, which started the day with a market capitalization of about $1.1 billion, has approximately 47 million shares outstanding. RARX shares opened more than 100% higher on the news today at $45.76 (+$23.065, +101.63%) compared to yesterday’s $22.695 closing price. The stock has traded today between $45.31 and $46.00/share and at present is trading at $45.38 (+$22.685, +99.96%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Jerome Powell has something in common with Bagdad Bob, Saddam Hussein’s infamous press secretary. They’re both liars, suggests Money Metals podcast guest Craig Hemke of the TF Metals Report.

Telling obvious lies with a straight face is part of Powell’s job description. He hopes to maintain order even though anyone who is paying attention knows something extraordinary is going on.

When the Fed stepped into the “repo” markets at the end of September with hundreds of billions in short term loans for its owner banks, Powell stood out front telling everyone there is nothing to worry about.

The Fed’s repo market lending was initially sold as a very temporary measure to combat a quarter-end cash crunch in an otherwise healthy financial system.

Now it has morphed into a months-long effort which may ultimately involve trillions of dollars.

Powell hasn’t bothered to explain why there has been such a massive expansion of this program or apologize for the gross mischaracterization of the repo market activities when they originally began.

All we know for sure is that the Fed is acting as the lender of last resort in a market where banks are no longer willing or able to lend to one another at less-than-punitive rates. Fed officials are now committed to playing that role through January, at least.

Maybe they don’t fully understand what the troubles in the repo market portend. It is more likely they are whitewashing some emergency.

Perhaps the repo market operations are a backdoor bailout for one or more major banks. Whatever is happening, it can’t be good.

Fortunately for Powell the media isn’t asking many questions. And the Fed remains wholly unaccountable. No one there can be forced to explain what is actually going on.

Alert citizens can spot the lies and obfuscation. But, it’s hard to know exactly how bad things are. Eventually some crisis could overwhelm all of the official efforts to manage the story, and the truth will be out.

The Fed may be working to fend off just such a crisis now.

Last week, central bankers announced a program to buy $60 billion worth of Treasury bills each month. This effort will be in addition to the hundreds of billions being pumped into the repo markets.

“Baghdad Jerome” says this program should definitely not be considered QE.

He told reporters it “should in no way be confused with the large-scale asset purchase programs that we deployed after the financial crisis.”

His less-than-compelling explanation about why the current program to buy Treasury debt is vastly different than prior programs to buy Treasury debt can be heard here.

We understand why Powell is so anxious to avoid the label of “QE.” It would be awkward answering questions about why prior rounds of the program failed to promote lasting economic recovery, or why more of the same should work this time.

Also, central bankers desperately want to promote the idea that they have a large and varied set of tools they can use to perfectly plan the economy.

The truth, which must be hidden, is that there is really only one tool — the variable-speed printing press. And it only works to make bankers richer and ensure government spending is unrestrained.

Quantitative Easing was itself just a clever and technical sounding label officials cooked up to obscure that program’s base nature. Powell can call the new program whatever he likes, but it has an awful lot in common with prior initiatives.

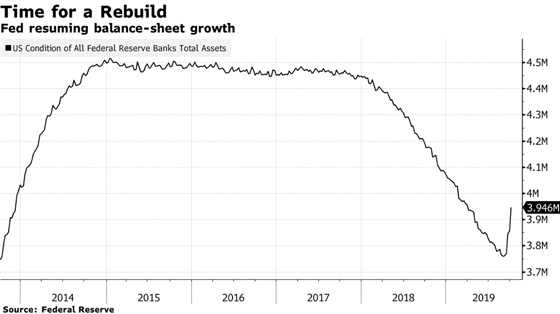

The scale is massive. Fed balance sheet has grown by roughly $200 billion in two weeks.

The Federal Reserve is buying Treasuries from the banks, rather than directly from the Treasury. It is a handout to the banks who profit from their role as unnecessary middlemen.

It’s a step toward Third-World-style debt monetization. The hundreds of billions in freshly printed dollars will be funneled to Wall Street and then to the U.S. Treasury, not Main Street.

Perhaps the biggest takeaway from these events is that Fed stimulus is a one-way train.

Anyone who bought the official promise that central bankers would withdraw stimulus as markets recovered should abandon that notion, now and forever. They tried. They failed.

Stimulus is better understood as an addictive drug. The Fed can never withdraw it without crippling or killing the markets. Plus, there is always the risk of an overdose.

Take a look at this chart and guess how long will it take to undo all of the ‘Quantitative Tightening” done since 2018?

The operations needed to keep the wheels on the cart are getting more extreme. We will find out whether the increasingly flimsy assurances from Powell and other officials are enough to maintain order in the markets.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

The US dollar has been a little lower over the first European session of the week despite weakness in equities prices. We have a quiet US datasheet this week so flows are likely to remain linked to incoming headlines around the initial US/China trade deal agreed last week. USD index trades 98.15 last with price reversing from overnight highs.

EUR Higher on Weak USD

EURUSD has been firmer against USD today though price action remains muted and corrective at best. The release of the ECB meeting minutes last week cast doubt over any further action from the ECB in the near term, highlighting the level of division among ECB policymakers. A quiet data calendar this week will keep the focus on Brexit and trade war headlines. EURUSD trades 1.1038 last, sitting back above the 1.1025 level for now.

GBP Lower on Brexit Uncertainty

GBPUSD has fallen back a little today as the EU has warned Boris Johnson to move “further and faster” if he wishes to secure a Brexit deal this week. The Queen is due to open parliament today with a speech outlining the domestic agenda though many are calling the speech a “sham” given that the focus is on holding elections in the immediate future. GBPUSD trades 1.2549 last as Brexit uncertainty once again drives flows.

Risk Assets Rocked

Risk assets have softened today following moves higher late last week in response to news of an initial US/China trade deal. Despite the step forward, the deal contains no progress towards resolving the more substantial issues between US and Chinese trade. Many remain skeptical that these issues will be resolved in the near term. Furthermore, China has said that it wants to run through some of the key details of the deal before signing anything. SPX500 trades 2955.38 last, sitting back under the 2959.04 level.

Safe Havens Rally

Safe havens have had a strong start to the week as fading optimism around the US/China trade deal announced last week has seen equities cascading lower today. Both JPY and gold are higher against USD so far today. USDJPY trades 108.13 last as price reverses from recent three-week highs. XAUUSD trades 1495.30 which is still below the 1500 level for now.

Oil Slips on Trade Deal Fears

Oil prices have been sharply lower today also as a shift in sentiment over the US/China trade deal has weighed on prices. Crude has been higher initially in response to news of the deal though subsequent reports that China is stalling over signing off on the deal has seen a heavy reversal in crude which trades 53.51 last. With the EIA continuing to upgrade its US production forecasts, unless we see a big improvement in global trade, the weakening demand for oil is likely to keep prices pressured going forward.

CAD Crumbles

USDCAD has been higher today in light of heavily weaker oil prices which have weighed on CAD. CAD has been sharply higher late last week in response to the reporting of a US/China trade deal. However, today, USDCAD is sitting back above the 1.3207 for now.

Aussie On The Way Down

AUDUSD has been sharply lower today also as concerns over the likelihood of the US/China trade deal being signed are taking their toll on the Aussie. AUDUSD trades .6754 last, retesting highs from mid-week last week. Back below here and focus will be back on a retest of the year to date lows.

Sector expert Michael Ballanger’s take on this week’s news from the financial markets informs his most recent investment decisions.

It’s a funny thing that happens when the stress of financial insolvency bubbles up to the surface. Decisions once considered “routine” (like brushing one’s teeth or walking one’s dog) suddenly have life-or-death outcomes, complete with cold sweats, sleepless nights and self-prescribed medicinal relief. Whenever I turn on the financial news stations, such as Fox, Bloomberg or CNN, I get the impression that I am watching Kabuki theatre, with exquisitely-designed puppets playing out exquisitely crafted scripts. I am immediately faced with the ageless problem of whether or not to consider the content “news,” or should I view it as simple “entertainment.”

By example, the saber-rattling of the United States of America in its anti-China rhetoric is playbill material of the highest order. You have in the red corner the aging heavyweight champion, long seated on the throne of global military and economic dominance, while in the blue corner, you have the spry young contender, hungry from decades of communist suppression and poverty with a highly motivated populace and a powerful and rapidly growing military. As much as the world may loathe it, it appears that the bell is soon to sound and the battle for global supremacy is about to begin.

The problem lies not in the war itself but in the collateral damage about to be inflicted upon the those close to the battlefield. However, at the end of the day, as the night when a youthful Rocky Marciano knocked an over-the-hill Joe Louis through the ropes, 330 million Americans trying to engage 1.433 billion Chinese is like taking a knife to a gunfight, and by that, I do not refer to an altercation of armies. I refer to an altercation of willpower.

For thousands of years, Chinese culture has taught people to think in terms of generations, while American culture has been trained in terms of days, hours and minutes. Since the end of WWII, America has fancied itself as the rightful heir to the hegemonic throne, aided and abetted by Hollywood, and its educational system that has promoted the concept that the only soldiers fighting on the side of freedom and against the Axis of Evil were the Yankees. All through the Cold War and now into the New Millennia, the Teddy Roosevelt concept of “speak softly but carry a big stick” has been replaced with “shoot first and ask questions later,” with the American forces, for the first to time invading a foreign nationunprovoked (remember the imaginary weapons of mass destruction of the second Iraq Invasion?).

By contrast, the Chinese have opted for symbolic power, and as a result, the world is now ablaze with confrontations, literally everywhere, as the result of American-led imperialism. Only just recently has China flexed its muscle with the protests ongoing in Hong Kong, but by and large, the ramifications of two mammoth economies now in all-out conflict stands to be seen as epic, and there is very little if anything that can be done to prevent an economic winter in trade and standards of living.

The first casualties of such conflict will be currencies, where purchasing power begins to erode slowly but then completely vaporizes, as seen throughout history, in Wiemar Germany, Zimbabwe and, more recently, Venezuela. The first beneficiaries of such conflict are the ageless stores of value in gold and silver. Physical possession of one’s wealth is the cardinal rule of survival when financial Armageddon arrives; just ask any of the survivors of the nations hit with hyperinflations the importance of possession. Nowhere is the phrase “possession being nine-tenths of the law” more relevant than in chaotic societies.

The financial news and, more recently, social media have become the preferred conduits for financial propaganda by corporations, investment houses, politicians and presidents. Whatever the medium, managing both expectations and behaviors of the consuming public is used by everyone to advance either a product or a concept, and it has grown out of control to the extent that I now find it virtually impossible to differentiate between targeted messaging and actual reporting. So when I read that there is a “pending trade deal with China,” I completely discount it, because 90% of the time it is floated by either an administration official (like Larry Kudlow) or a Wall Street reporter (like Steve Liesman) in order to herd the algobots into buying stocks.

Larry Summers was the master of “behavioral economics,” and it was here that was born the acceleration of the asymmetrical wealth effect as an economic tool by which policymakers could sway consumer buying trends. From the Crash of ’87 onward, the importance of elevated stock markets morphed into an important policy tool, to the point where here, in 2019, President Trump appears obsessed with it and tweets algobot-sensitive buzzwords like “China deal” and “lower rates” in order to goose the markets. The underlying reason for all of this is to distract the masses away from the reality of the disintegrated middle class and eroded living standards, all the direct result of the errant actions of the Federal Reserve and its global central banking brethren, who collectively have brought a new level of disrespect for the integrity of purchasing power of all currencies in all nations. “If stocks are up and gold is down, things must be good, right?” Perception is nine-tenths of reality.

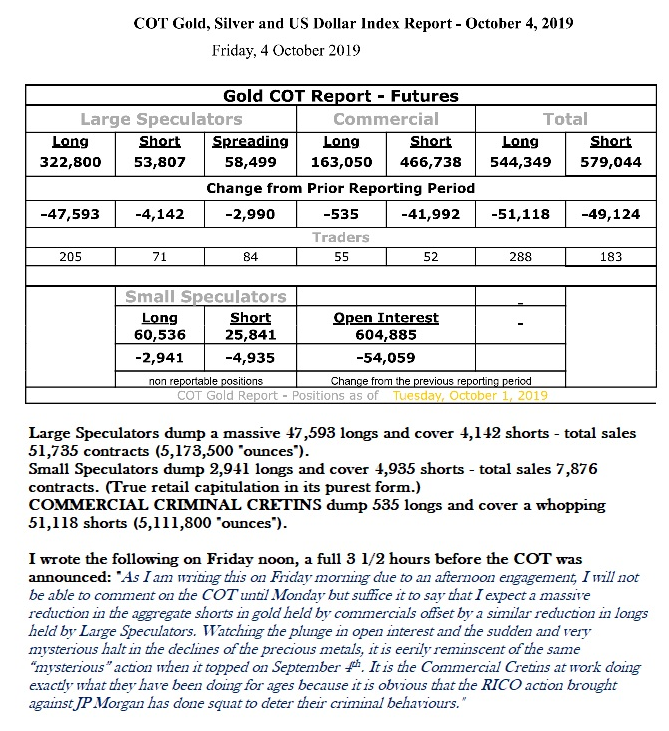

COT Report

Comments are found in the graphic provided below.

I scooped the chart shown below from my buddy David Chapman (enrichedinvesting.com), with whom I used to work while toiling for Union Securities from 20042011. David is a market historian and a card-carrying member of the Society of Technical Analysts, and feels that the markets have topped, as shown in the breakdown from a rising wedge formation from last week.

With bearish chart configurations such as this, I normally opt for a smattering of shorts and put options. As we have seen in the past, they have tended to be lucrative until that point where the screams from Wall Street and the sitting President force into action the Working Group on Capital Markets (the PPT), after which short sellers get immolated in a frenzy of government-triggered buy orders from a financial source that rarely, if ever, gets a margin call, and has deep, unlimited pockets. Market adversaries like the U.S. Treasury are not to be trifled with because they cannot and do not lose. Hence, I opt for volatility trades such as the TVIX or the UVXY, or calls on the VIX index. It is akin to betting on “weather” as opposed to choosing “sun” or “rain.”

For those of you following my Twitter feed, you know that I have called for a huge spike in volatility (VIX) since Sept. 16, and have already traded the TVIX once from the low $13s to over $16. Well, yesterday, I reloaded the gun with a full long position in the TVIX at $13.75, and was tempted to add more prior to Jerome Powell’s “This is not quantitative easing (QE)” speech, which has to be the most laughable plausible denial in history. You are buying several hundred billions of T-bills in order to force short rates lower while bragging of a 3.5% unemployment rate and a “booming” economy, and yet you refuse to call it QE? These are the times that I want to launch my Groucho Marx paperweight directly into the Jumbotron TV showing the professorial forehead of not only Powell but also the shiny cranium of CNBC economics reporter Steve “The Fed Can Do No Wrong” Leisman.

I am long a substantial TVIX position in the GGMA portfolio from yesterday, committing 50% of all cash reserves to the TVIX, representing a 19.66% allocation. That is a rather large bet for a portfolio dominated by gold, silver and miners of same. It is also a testimonial to my current state of readiness, alarm, and apprehension as to the risks inherent in the global markets. As I wrote about a few weeks ago in “Something Wicked This Way Comes,” dated Sept. 24, I cannot exactly pinpoint the precise reason for my anxieties, but I can say that trading against my gut feel has hurt me immeasurably over recent years and with today’s absurdity levied upon us by the Fed Chairman, these REPO operations are not carried out because things are rosy. They are “emergency measures,” and if you want me to wage a guess, I would say that a large Eurozone bank whose noxious derivative tentacles intertwine with Walls Street’s (and whose response to questions regarding possible insolvency is an abrupt “Nein!!”) is in big trouble. I’ll let you figure it out. . .

Tuesday’s session ended poorly, with stocks going out “hard on the lows,” but with the VIX and the precious metals well-bid. Gold miners (HUI + 2.96%) outperformed the metals, with silver (+1.43%) outperforming gold (+.45%), a letter-perfect configuration for a continuation move. Last year’s stock market blow-off started to gather steam around this time and didn’t end until Christmas Eve, after Smilin’ Stevie Mnuchin called in the PPT goons to save Wall Street from a year-end disaster never before seen in the annals of Wall Street History.

Just as past performance is no guarantee of future results, past equity market crashes accompanied by gold market advances are by no means a guaranteed repeat, but the fact remains that the global economy has slowed to a standstill, and that the singular driver that has justified the past 10-year bull marketgrowthis now gone. Without it, all that remains is the music, and when the music stops, try finding a chair when all of them are owned by Fed governors.

The words of Fed chairman Powell were as chilling as I have ever heard. In forty-two years of reading and listening to the words of Paul Volcker, Alan Greenspan, Ben Bernanke, Janet Yellen, and now Jerome Powell, I have never before heard such an astonishing display of prevaricative showmanship, through which he attempted to convince us that a Fed balance sheet expansion was not in any way a return to the 2008 crisis policy actions known as QE. To be clear, all moves by central banks to “shore up liquidity” involve the simple process of manufacturing cash, a process known as “counterfeiting,” to the average law enforcement officer.

The mere mention of Fed “stimulus” in prior times has resulted in massive upswings in stocks. But today (Tuesday), unlike 2008, and unlike 2002, and unlike 1998, and unlike 1987, the markets heard the news of a return to Fed balance sheet expansion and they indeed rallied. Sadly, after things settled down, the light bulb went on and the words of “economic health” were replaced by that malaise of which I referred last monthmistrust. Realizing that Powell had the lipstick out, they sold them hard right into the final bell.

Stay long precious metals and add on dips. Sprinkle in a tad of volatility and a sprig of index puts and we may all have a very peaceful Thanksgiving and remember, something wicked. . .

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Statements and opinions expressed are the opinions of Michael Ballanger and not of Streetwise Reports or its officers. Michael Ballanger is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Michael Ballanger was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

The global economy has been trending lower over recent months, sparking recessionary fears across the globe.

In light of this, the markets were treated to some relief as the first signs of a potential end to the US-China trade war emerged late last week.

Representatives from both sides were engaged in the thirteenth round of negotiations last week. On the back of these talks, President Trump announced that the two sides have agreed on a “tremendous”, initial trade deal.

Tariffs Cancelled

The official details of the deal have not yet been published. However, according to President Trump, the deal consists of a pledge from China to buy between $40 and $50 billion worth of US agricultural products.

The pledge also involves the Chinese working hard to protect US intellectual property and welcoming more foreign financial services.

In return, the US has promised to abstain from increasing 25% tariffs on $250 billion worth of Chinese goods to 30%, as was scheduled to happen on Tuesday.

Phase Two

Trump has dubbed the deal “phase one” and it includes a commitment to continue negotiating towards delivering a “phase two”.

This second stage of the trade deal would include commitments over more contentious issues. These include China stealing technology from foreign firms, as well as regulations that sabotage US companies.

Phase two will also include a consultation process for how to resolve disputes and handle enforcement. Trump has outlined that if talks proceed as expected, he will cancel the next wave of tariffs due to land in December.

China State Media Sounds Cautious

Despite Trump’s praise for the deal, the reaction from the Chinese has been more moderate.

Over the weekend, Chinese state newspaper the China Daily commented on the deal saying:

“While the negotiations do appear to have produced a fundamental understanding on the key issues and the broader benefits of friendly relations, the Champagne should probably be kept on ice, at least until the two presidents put pen to paper.”

The article went on to say:

“As based on its past practice, there is always the possibility that Washington may decide to cancel the deal if it thinks that doing so will better serve its interests. The US should avoid backpedaling, as it has in the past, and instead cherish what has been achieved as a manifestation of a healthy and steady China-US relationship that serves the interests of both countries and the world,”

Election Boost For Trump

The initial deal, while still just verbal at this stage, works in favor of both leaders.

Trump will likely receive a boost ahead of the 2020 elections if he critically secures farm purchases. That should help swell his support again among farmers who have been hit the hardest by the trade war.

Xi, meanwhile, has been able to avoid a further escalation in tariffs that have been crippling the Chinese economy. A deal would mean he can celebrate the start of a return to stability.

Market Reaction

We saw some initial upside across equities markets in response to news of the deal.

The canceling of another round of tariffs is good for global trade. However, many remain skeptical.

The deal is yet to tackle any of the more important issues which have broken down relations between the US and China. Although this certainly marks the first step towards a proper deal, there is still the risk of talks faltering.

This is especially true further down the line once the US starts looking for China to compromise over some of the more contentious areas of its economic practices.

Technical Perspective

SPX500 broke above the 2959.04 highs and the local bearish trend line in reaction to the news. Despite some softening so far today, price remains above the trend line for now. While above here, focus remains on a further push higher. The resistance zone between 3020.23 and 3028.38 (all-time highs) is the key area to watch.