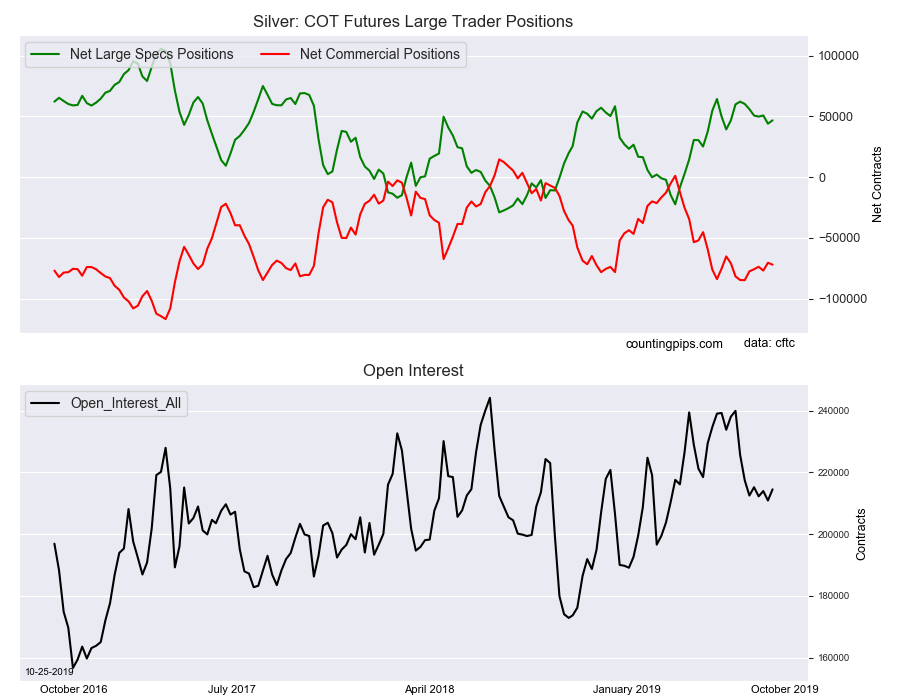

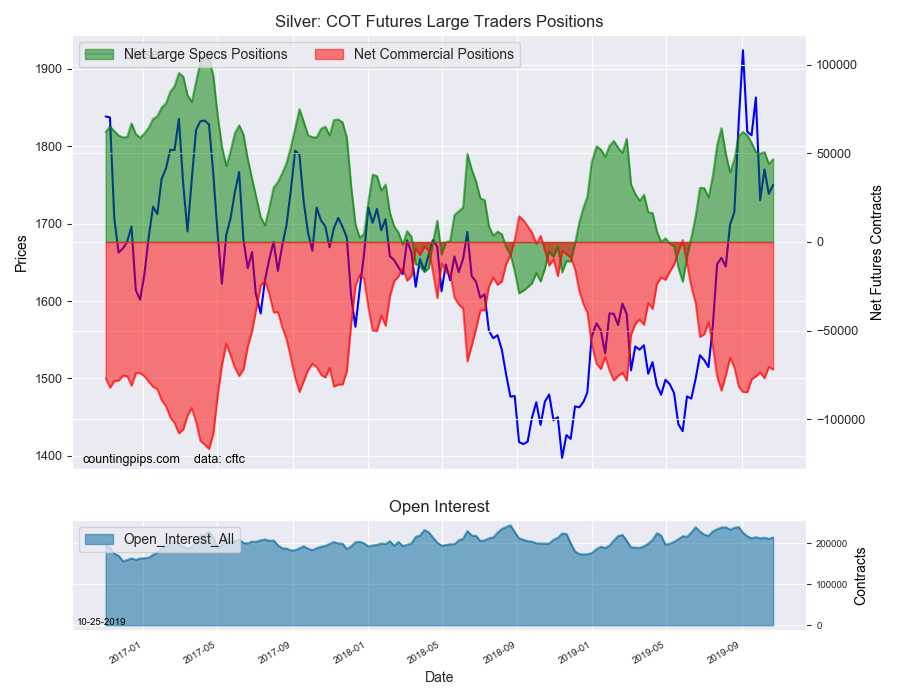

Large precious metals speculators boosted their bullish net positions in the Silver futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Silver futures, traded by large speculators and hedge funds, totaled a net position of 46,743 contracts in the data reported through Tuesday October 22nd. This was a weekly change of 2,754 net contracts from the previous week which had a total of 43,989 net contracts.

The week’s net position was the result of the gross bullish position (longs) ascending by 4,659 contracts (to a weekly total of 89,747 contracts) while the gross bearish position (shorts) rose by just 1,905 contracts for the week (to a total of 43,004 contracts).

Silver speculators raised their bullish bets for the second time in the past three weeks following a streak of four straight down weeks (September 10th through October 1st). The silver position continues to be in a fairly strong standing with the net contract level above +45,000 contracts. Overall, the silver net position has now been above the +40,000 contract level for ten straight weeks.

Silver Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -72,023 contracts on the week. This was a weekly fall of -1,536 contracts from the total net of -70,487 contracts reported the previous week.

Silver Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Silver Futures (Front Month) closed at approximately $1750.0 which was an uptick of $11.6 from the previous close of $1738.4, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

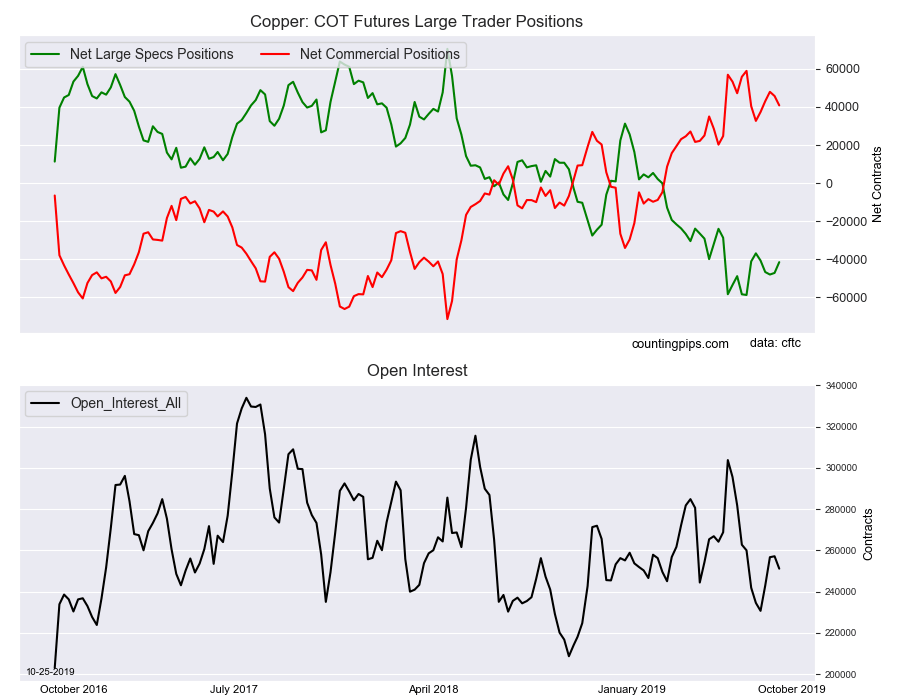

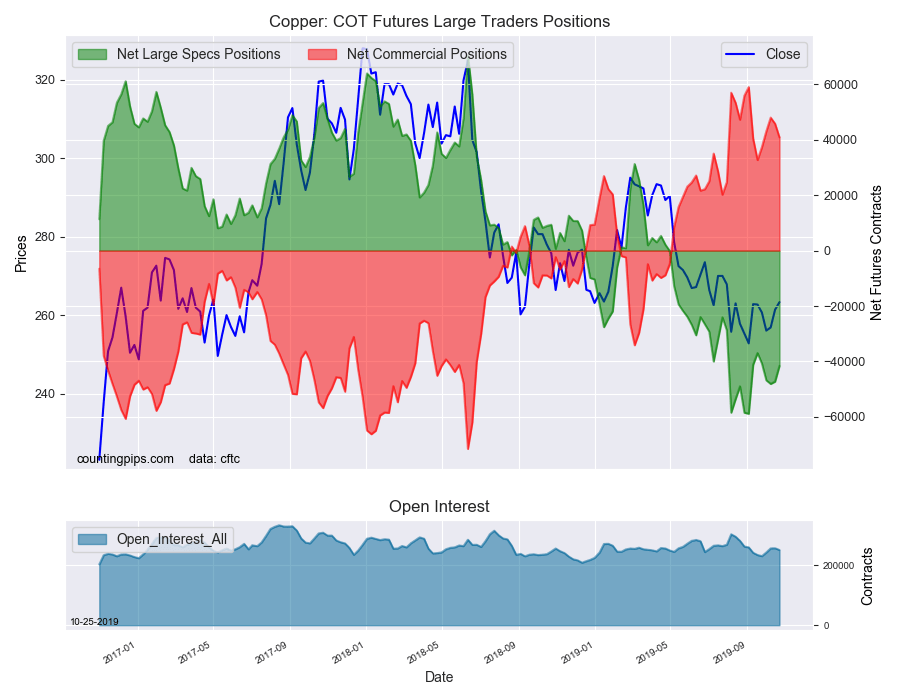

Large precious metals speculators cut back on their bearish net positions in the Copper futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Copper futures, traded by large speculators and hedge funds, totaled a net position of -41,573 contracts in the data reported through Tuesday October 22nd. This was a weekly change of 5,682 net contracts from the previous week which had a total of -47,255 net contracts.

The week’s net position was the result of the gross bullish position (longs) increasing by 1,361 contracts (to a weekly total of 68,744 contracts) while the gross bearish position (shorts) declined by -4,321 contracts for the week (to a total of 110,317 contracts).

Copper speculators pared their bearish bets for a second consecutive week and by a total of 6,520 contracts over the two-week period. Previously, bearish bets had risen for three straight weeks through October 8th and to the highest level since the record high of -58,841 contracts on September 3rd. The recent decline in bearish bets brings the current standing to the least bearish level of the past four weeks.

Copper Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of 40,840 contracts on the week. This was a weekly fall of -4,938 contracts from the total net of 45,778 contracts reported the previous week.

Copper Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Copper Futures (Front Month) closed at approximately $263.30 which was an advance of $1.90 from the previous close of $261.40, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets.

The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators).

There are several critical and challenging factors in relation to trading that can severely harm a trader’s potential trading success and prosperity. And if you fail to address the challenges, or ignore the impact these factors can have, the effects can be disastrous.

Overtrading, trading without a plan, being inexperienced, only having a thin grasp of market mechanisms, not understanding how fundamentals move our FX markets, these are just some of the barriers we can impose on ourselves, directly limiting our potential. The subject of trading from an under capitalised account is never discussed enough in trading circles, despite this crucial factor being a considerable block to progression.

The FX market, whether traded on a part time basis, or as a full time self employed activity, should be approached with professionalism. That professional attitude should be extended to trading with an account that allows the trader the freedom to function effectively in the market place. Whilst you know that you’re betting on markets, you shouldn’t adopt the various bad practices, associated with other betting industries.

You shouldn’t take punts, instead you risk a proportion of your account size per trade, after analysing your markets, using both fundamental and technical analysis. You don’t bet on hunches and you don’t suddenly decide to take a punt on the movement of a currency pair because you have a few spare dollars or Euros. Instead, as a professional trader who has self respect and who respects their industry, you plan everything in advance. Because you agree with the truism that; “if you fail to plan, you plan to fail”.

One simple, effective method to establish if the account size you’re trading is sufficient for your ambitions, is to firstly decide what targets you have for your trading. Are you looking to supplement your full time income, or are you looking to trade full time? The majority of traders are part time, generally swing or day traders, looking to supplement their income. Many have an ambition to reach a point of success and profitability, which will eventually allow them to become full time traders.

Let’s base our calculations on the premise that you’re a part time trader, a swing or day trader, who will trade EUR/USD exclusively. You have €5,000 to trade with, you now need to establish if it’s enough capitalization to trade effectively. And if so what parameters should you attach to your trading, in order to ensure you’re not trading from an under capitalised position? And what targets could you realistically attach to your trading, to achieve your ambitions? We’ve selected a figure of €5,000, as it’s the upper band of the €3-€5K average deposit/account size figure, which many brokers refer to as the deposit their clients hold with them.

As a trader only speculating on EUR/USD exclusively, you’ll enjoy some of the tightest spreads available, whilst the slippage and poor fills you experience should be significantly reduced, due to the increased liquidity available for the most traded currency pair globally 24-7. You can trade this security, through an ECN/STP trading model, safe in the knowledge that the conditions you’re trading in are as good as it gets. You have to now decide what risk to take on each trade, in relation to your account size.

If you’re prepared to risk 2% account size per trade as a swing trader, then you’ll be risking €100 per trade. For swing traders this is generally considered to be an acceptable level of risk. If you’re a day trader, taking several trades on EUR/USD per day, you may prefer to risk 0.5% account size per trade, therefore, you’ll be risking €25 per trade. The risk per trade has now been established, what returns should you aim for?

The account growth you aim for is often a contentious subject in the retail trading world, with many market commentators in the mainstream financial media, neglecting to understand the key difference between investing and trading. You’ll often see criticism that trading returns are way too optimistic, when traders report they’re aiming for gains of perhaps 50-100% per year. However, for successful traders such a return is neither delusional, or out of reach.

Many article writers will compare investment returns to trading returns when the two phenomena are mutually exclusive. Aiming for 1-2% return per week, is an entirely realistic proposition for traders who put their funds to work. Therefore, if you consider your original $5,000 account size and you’re aiming for 2% annual growth as a swing or day trader, you’ll be looking to double your account size to €10,000. If you dial down your ambitions and your risk per trade, you may instead aim for 50% account growth per year, which is roughly 1% gain per week.

Such targets are realistic and achievable, for proficient and disciplined traders, operating either full, or part time. The examples outlined illustrate that your capitalization should be directly related to your risk per trade and your target growth. The illustrations also provide evidence that any level of capitalization (in theory) allows you to trade effectively, if your broker allows you to take positions risking only, for example, the €25 per trade highlighted in the article.

However, the likelihood of achieving returns of any size will be enhanced if you stick to the parameters outlined, details that you’ll have embedded into your comprehensive trading plan, a plan which you’re continually perfecting, based around the trading discipline you’ve also developed.

Content Source: Mr. Asim from Forex Trading Dubai has contributed in this article.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up Chris Powell of the Gold Anti-Trust Action Committee joins me and updates us on the recent developments in the gold and silver manipulation prosecutions and discusses how the price spoofing schemes by the bullion banks may be tied to trades by central banks working to keep a lid on prices.

Chris also explains why he thinks the “powers at be” are losing control of the price and how the recent positive price action in the metals markets suggests they have lost some of their influence in the markets. So be sure to stick around for a jam-packed interview with Chris Powell of GATA, coming up after this week’s market update.

Well, another week, another new and expanded repo market intervention by the Federal Reserve. On Thursday, the Federal Reserve Bank of New York intervened twice with fresh liquidity injections. Fed officials raised their offerings for overnight repos up from $75 billion to a staggering $120 billion.

This comes on top of the $60 billion per month in Treasury bill purchases that will extend well into next year and possibly beyond. Over the past month alone, the Fed’s balance sheet has soared by $200 billion.

You might think numbers like these should be quite alarming to investors and to anyone who holds U.S. dollars. But the strange thing about these Fed interventions is that hardly anyone seems alarmed. There’s no sense of rising risk being priced into the stock market. And the mainstream media is barely even mentioning these massive transfers of paper wealth.

Perhaps after multiple rounds of Quantitative Easing over the past decade, this latest spate of money printing is just part of the new normal. But we remain concerned that something very abnormal could be unfolding.

At the very least, there is a persistent liquidity shortage in overnight lending markets. And Fed officials obviously feared that it could cause the banking system to freeze up and money market funds to fail.

We don’t yet have all the answers as to what’s really going on in the bowels of these institutional markets, but we will continue to question the line the Fed is putting out. When these repo market interventions were first announced, our research team here at Money Metals, as well as our recent guest experts on this podcast, immediately suspected a new Quantitative Easing program was beginning.

Now, despite the Fed chairman Jerome Powell’s repeated denials, it’s pretty apparent we were right. It is indeed QE, and we can only guess as to how much bigger it will get in the weeks to come. Fed money printing certainly does carry implications for higher rates of price inflation down the road in the real economy.

The inflationary effects of previous QEs were largely absorbed by capital markets and stunted by relative weakness in the economy. This time around the Fed’s balance sheet surge is starting with the stock market at extremely elevated levels and many conventional economic indicators coming in strong.

We wouldn’t be surprised if precious metals markets soon begin to reflect rising inflation risk.

This week gold and silver markets showed signs of moving toward an upside breakout. On Thursday, gold prices rallied above the $1,500 level while silver rallied up to its 50-day moving average.

As of this Friday recording, the metals are continuing the rally with gold prices now coming in at $1,512 an ounce, up $20 or 1.3% for the week. Silver shows a weekly gain of 67 cents or 3.8% to bring spot prices to $18.29 per ounce. Platinum is popping for a 5.1% gain this week to come in at $940. And finally, palladium is trading up 0.9% on the week and closing in on another new record at $1,777 per ounce.

Looking ahead to next week, metals investors will await the Fed’s decision on interest rates at its policy meeting. Fed policymakers appear likely to roll out another rate cut. It will come on top of all their other recent liquidity injections.

The risk for gold and silver markets is that Wall Street celebrates by pushing the stock market to a record high. If that happens, it could temporarily quell buying interest in the metals. But it won’t necessarily trigger any kind of big sell-off. A rising sea of liquidity does ultimately tend to lift all boats.

Precious metals markets have performed well overall this year on the heels of major multi-year breakouts. The consolidation phase over the past few weeks in no way undermines those breakouts or their longer-term bullish implications.

Looking ahead to next year, we can expect a very polarized and at times very nasty political campaign to begin moving markets once it’s clear who the Democrat nominee will be. Right now, the momentum within the radicalized Democrat voter base is behind Elizabeth Warren.

Given Warren’s plans to jack up taxes and break up large American companies, some on Wall Street fear a Warren victory would crash the stock market by 20% or more.

One of Warren’s signature campaign promises is to impose a “wealth tax.” It would introduce a dangerous new concept into the tax code – namely that the government gets to tax not just capital gains on investments, but also the market value of investments and other household assets taken together.

A wealth tax would force you to account for the value of all your assets – from your financial accounts to your home, your car, your personal possessions, and your gold coins.

Under current law, gold and silver coins generate no tax liabilities or reporting requirements until they are sold. Under a wealth tax, gold coins and other tangible assets in your possession could get an annual scalping by the government.

Regardless of whether such a proposal ever gets enshrined into law, and regardless of who wins next year’s election, the government will be looking for new ways to raise revenues as budget deficits expand. One way to hedge against a Warren wealth tax or a Biden capital gains tax hike is by moving assets into a tax-sheltered IRA.

The government can’t tax IRA assets, including IRA-eligible physical precious metals products, until you take distributions. And with a Roth IRA, you may be able to avoid taxes completely – even as tax risks and inflation risks rise.

In other news, there have been some more big changes in the retail precious metals industry.

Some of Money Metals’ well-known and/or younger competitors have run into some issues and officially changed hands in recent months, and they just announced a major reshuffle of their operations – fulfillment here, payment processing there, and customer service even somewhere else. Yikes!

Meanwhile, Money Metals Exchange has remained closely held by my family since its inception in 2010. We remain as stable as a rock, and we continue to build out new services and customer benefits with a laser-like focus – working obsessively to live up to our title as America’s best precious metals dealer.

All of Money Metals’ operations remain under one roof – customer service, fulfillment, depository, accounting, and our corporate offices.

It’s about security, efficiency, and absolute accountability to our customers and their needs.

…our depository and its fully integrated systems make buying, storing, and selling precious metals a more secure and seamless process…

…our audited depository earned the coveted UL Class 3 security rating, has been thoroughly vetted and approved by retirement trustee companies to hold customers’ precious metals IRA assets, and offers the lowest storage fees for non-IRAs and IRAs alike…

…and we can now even offer low-interest cash loans of $25,000 or more to those who have significant precious metals holdings at Money Metals Depository.

Money Metals continues to add services and value because we absolutely do not take any of this success for granted. As an owner in our business, and on behalf of all of our dedicated employees, I want to say once again that we appreciate your ongoing business, trust, and support.

Well now, without further delay, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome in Chris Powell, Secretary-Treasurer at the Gold Anti-Trust Action Committee, also known as GATA. Chris is a long time journalist and hard money advocate, and through his tireless efforts at GATA, he is working to expose the manipulation of the gold and silver markets. Through GATA’s work over the years, some important revelations have come to light which quite honestly should concern everyone.

It’s great to have him back on with us. Chris, thanks for the time again today, and welcome.

Chris Powell: Oh, thanks as always for your interest, Mike.

Mike Gleason: Well, Chris, we think some people owe you and GATA an apology. You have been making the case for manipulation of gold and silver prices since GATA was formed in 1999, but lots of people dismissed everything you had to say. We now have incontrovertible proof of multiple banks and multiple traders running a decade-long scheme to “spoof” prices.

There are guilty pleas and piles of evidence exposing a scheme which involved thousands of bogus trades. We know senior people were training more junior employees on how to rig prices. The Department of Justice is going to prosecute using RICO laws because attorneys there can see this is organized crime. But somehow, it doesn’t look like the apologies will be coming anytime soon.

The same people who openly mocked the idea of price rigging a year or two ago now want us to believe that this sort of cheating is really just par for the course in any market. Bankers will be bankers – we should just expect they will occasionally cheat a little. They want everyone to know these markets are free and fair for the most part. At this point, I think it’s safe to assume that no amount of evidence could persuade them otherwise.

Why do you think people still refuse to acknowledge just how crooked these markets are? Wouldn’t most of these manipulation skeptics be better off if the markets were actually free and fair?

Chris Powell: Well, many people in the markets, Mike, and many people in the mainstream financial news media are dependent on ignoring this stuff. If people begin to realize that the markets are so heavily rigged, they’re not going to participate in them as much, and certainly, they’re not going to pay as much attention to the traditional market analysis that we’re provided with people trying to compare chart patterns and drawing lines and waves and everything like that.

Well, if we’re really just looking at holograms because people behind the scenes are rigging the markets, people, they’re going to lose faith in a lot of businesses and a lot of analysts. And I certainly understand why people are very reluctant to acknowledge this stuff. If they acknowledge it, they’re basically admitting that everything they’ve been telling people for years has been a lie or at least erroneous.

But we’re, of course, enjoying the Justice Department’s description of the JP Morgan Chase metals desk as a criminal organization, and we’re enjoying all the indictments of the traders at these big investment banks. But we’re the first to admit that we’ve been going after bigger game for a long time.

As reprehensible as this market rigging by the investment banks is, we’ve been concentrating on the market rigging by governments and central banks, and I think the indictments we’ve had so far are probably just a distant reflection of the rigging by the governments and central banks. I think that some of this rigging that has resulted in indictments and convictions is possibly front-running of government trades that have been undertaken by the investment banks fronting for central banks and governments.

But it’s not the big stuff we’re after. We’re after exposing the interventions of governments and central banks, particularly in the gold and silver markets. But with all this repo stuff going on, there’s no telling if there’s any end to their rigging.

Mike Gleason: Taking a step back here for people that may be somewhat new to this issue of this idea of manipulation of the gold and silver markets, give us a brief synopsis of why it is that you believe governments would have an incentive to rig gold and silver prices, suppress the prices. Talk about that if you would.

Chris Powell: Well, gold and silver are traditionally currencies. They’re the oldest currencies on the planet, and they compete with government currencies. They also have a powerful impact on the valuation of government currencies; on the price of government bonds; on interest rates; on the price of all other financial assets since financial assets all compete against each other for public investment.

Now, governments for many years have had an interest, and admitted their interest, in controlling the prices of the monetary metals. That’s what the gold standard was about. It was governments setting the gold price. Now, back when the government had a gold standard, gold was far more independent in its pricing because the public could pretty much control the gold price by deciding how much it thought government currencies were worth.

That was really before the surreptitious intervention in the markets came about. We’ve collected a lot of admissions by central bankers and government officials, things in government archives, memoirs written by central bankers, documents that are on the internet sites of governments showing that the gold price suppression is longstanding Western central bank policy. That’s all compiled in our documentation archive at the GATA internet site.

This is policy. This is not a conspiracy theory. We have admissions from various central bankers. Probably the best known one is Alan Greenspan who testified to Congress in 1998 that the purpose of gold leasing by central banks was to keep the gold price down when it was rising. The archives are full of this stuff, and we seldom get challenged on it because it’s just so overwhelming.

Mike Gleason: Alan Greenspan is an interesting case study. I don’t know that you’d call him a whistleblower necessarily, but he’s getting advanced in his years, and he’s starting to reveal some of the secrets of the central banks. There’s a guy who seemed to be somewhat of an advocate for gold before he became the Fed chairman, and then now, after he’s been removed from that role or taken a step back from that role and nearing retirement now, it seems like he’s sort of back to being a somewhat of an advocate for gold. It’s kind of an interesting telltale. Too bad he couldn’t have had any of those convictions while he was actually in power.

Precious metals mining companies that have long been a disappointment to us when it comes to this effort to reform these markets. When prices are rigged artificially lower, it hurts their bottom line, but with one or two exceptions, the miners have had almost nothing to say on the subject.

Now that banks have been caught running this scheme, we wonder if the miners will finally take some action. They have to be among the biggest victims of these crimes. What do you think? Are they going to step up now and demand some serious reforms? Are you seeing any movement there? Because I know we’ve talked with you in the past about this, and you’ve always expressed a lot of disappointment about the lack of an uproar among the mining executive community. Any change there?

Chris Powell: I’ve not seen any substantial reaction from the gold and silver miners to the convictions and indictments of the investment bank people for spoofing the monetary metals markets. And I understand it, Mike. The problem is the mining companies are afraid. They’re afraid of their governments. They’re afraid of their banks.

Mining is very probably the most capital intensive industry in the world. It takes hundreds of millions of dollars, sometimes billions of dollars, to discover and put a mine into production. And in doing that, mining companies are totally at the mercy of governments for first, their mining patents, then their environmental regulations and their royalty requirements to governments.

And since the industry is so capital-intensive, most mining companies are very dependent on the very biggest banks. And the very biggest banks, of course, are very directly government agents in the markets. Most of them are primary dealers and U.S. treasury securities and have very intimate relations with the U.S. government, which certainly does not want the monetary metals prices rising uncontrollably and displacing government currencies in the financial system.

The mining companies are terribly vulnerable to governments. They’re terribly vulnerable to the investment banks, which are central bank agents. And I understand why they do not want to support GATA, and they don’t want to endorse our complaints about the rigging of the markets: because they just figure the governments and their own bankers will come down on them and impair their business. But I would still suggest to them, do you want to die on your feet, or do you want to die on your knees? Because this industry is in a very strange position right now.

I think the objective of central banking and governments is to keep the monetary metals prices at pretty much subsistence level. They don’t want the monetary metals miners to go out of business. They need a supply constantly coming into the market, but they don’t want the price to be so attractive that people start investing in monetary metals as international reserve currencies and moving out of government currencies. The governments have got the miners at subsistence levels, and I don’t think they are very eagerly going to let the miners become substantially profitable in an attractive industry for investment, at least not until the government and central bank rigging is exposed.

Mike Gleason: Well-stated there, and certainly, you’ve got to really commend a guy like Keith Neumeyer, First Majestic Silver. I know there’s maybe one or two others who are kind of sticking their neck out there. You just sort of laid out a very good case as to why a lot of these guys don’t do that.

They have a lot to lose. They’re beholden to the banks that that loan them money for their projects and, of course, the government who approves their environmental cases and so forth. It’s kind of an interesting and difficult situation.

Chris Powell: Neumeyer has been very courageous, and he has put himself at risk. Eric Sprott is another. There are not too many like them. There’s a few others, but there’s not too many like them.

Mike Gleason: Agreed. Has GATA ever been called to testify, to provide any evidence in any of these criminal cases that are underway? Do you have a sense of whether prosecutors are on the right track?

Chris Powell: We’ve provided information to some of the lawyers involved in the class action lawsuits against the investment banks for rigging the monetary metals markets. I don’t think we’ve had any contact with prosecutors though.

All the documentation we have amassed and publicized is out in the open on the documentation page of our internet site. That’s accessible to everybody. I don’t know if prosecutors have ever looked at it. I know that the Russian government has been aware of GATA’s work since at least 2004 because a Russian central banker in 2004 gave a speech to the London Bullion Market association meeting in Moscow that summer, and the only words of English he spoke were “Gold Anti-Trust Action Committee,” which was pretty interesting to us because to the best of our knowledge, we’d never had any contact with anybody in Russia.

But it turned out the bank of Russia was watching us very closely. We know from the WikiLeaks cables from the U.S. Embassy in Beijing to the State Department in Washington that the Chinese government is very aware of gold price suppression by Western central banks because it’s often been written about in the government-controlled news organizations in China.

And the U.S. Embassy in Beijing translated a bunch of those reports and cabled them back to the State Department in Washington. And then when WikiLeaks got a hold of them some years ago, it was revealed that China knows all about the Western gold price suppression scheme and has reported it and complained about it in government publications in China.

The Chinese government knows all about gold price suppression by the Western central banks, and the U.S. government knows that China knows all about it because of the WikiLeaks cables of the translations that came from Beijing to the State Department. So, we know that gold price suppression is widely understood on an official basis around the world.

Mike Gleason: Well, as we begin to wrap up here, Chris, summarize the state of the state, if you will, with respect to the likelihood of the metals market manipulation coming to an end one day or at least the progress that’s being made on that front. Where are we here, and what are the prospects of finally achieving these free and fair markets that we all want so badly? And are you feeling any better about the possibility of seeing that one day now compared to, say, where you felt two to three years ago?

Chris Powell: Well, I have to admit being surprised that they’ve been able to pull it off for at least the 20 years that GATA’s been in business. It’s been very obvious to us what’s been going on. I think we’ve had the dispositive documentation in hand for at least 17 or 18 of our 20 years.

I am a little more encouraged over the last five or six months or so because there’s an obvious firmness, I think, to the gold and silver markets now. The interventional smash downs of the monetary metals prices are not having the effect they used to have. The central banks used to be able to knock down the gold price by 20, 30, 40, 50 dollars for months at a time.

And they haven’t been able to do that lately. I think it’s because the central banking cartel has split up on the gold front. We know a whole bunch of central banks have been buying gold lately. The central banks have switched in the last several years from net sellers to net buyers. There’s, I think, a lot of circumstantial evidence that China and Russia particularly are buying gold heavily in London.

So, I’m encouraged. I suspect we may be in a situation similar to the last months of the London Gold Pool back in 1967 and 1968, similar insofar as back then, the central bank gold cartel was dividing. There was division among the participants in the London Gold Pool.

France wasn’t playing along anymore. France started exchanging dollars for gold, and ordinary investment houses began to realize that the gold reserves at the participating banks were being run down and probably could not hold out much longer. I think we’re very likely in a similar situation now because central banks are now net buyers instead of net sellers, and they’re not telling us everything they’re buying.

I’m sure China has bought far more than it’s reporting. I’m hopeful about going on living for a few more years, but I can’t guarantee that anybody of my age is going to see the end of gold price suppression. I suspect we will have a day, perhaps not too distant, when the central banks have an international currency revaluation and revalue gold substantially upwards to re-liquify themselves after the redistribution of gold reserves around the world. And I think they may begin another half century of gold price control at a much more sustainable level, a much higher price.

Mike Gleason: You do have to be encouraged, just focusing on one thing that you said there, about how they are not getting the result that they used to be able to get when it comes to dragging down the price that they once did. So, they may be losing a little bit of control, and obviously, the whole game is sort of held up by confidence.

Maybe you’ve got nations that are going to start to scramble if they do see the end of fiat or the beginning of the end; that maybe there’s a mad dash into physical gold, and at that point, all bets are off. Maybe they won’t worry about colluding anymore and just fend for themselves.

Chris Powell: There’s so much central bank clamor now for devaluation of all the currencies, and there’s so much resentment of the weaponization of the dollar. All this is practically screaming for gold and silver, so I am hopeful, Mike.

Mike Gleason: Well, excellent stuff, Chris. We’ll leave it there. We certainly appreciate the time and your insights as always. Now, before we let you go though, please tell our listeners how they can get more information and learn more and follow GATA, and then also how they can get involved and maybe even donate to GATA so your organization can continue to fight this important fight.

Chris Powell: Well, thanks, Mike. Our internet site is gata.org. We are a tax-exempt educational and civil rights organization recognized as tax-exempt by the U.S. Internal Revenue Service. We’re a 501(c)(3) organization under the U.S. Internal Revenue Code.

Contributions to us are federally tax-exempt in the United States. There’s a mechanism on our internet site for accepting donations. I’m grateful for anything. Anybody who wants to send us a dollar will be sending us more than we’ve ever gotten from Newmont Mining or Barrick Gold or some of those big guys.

Even the hedge fund managers around the world who are outspoken in favor of gold, they don’t want to have anything to do with us because I think they’re afraid that we’ll put them in even more trouble with the government. We also have a mailing list. We try to put out several dispatches a day on subjects of interest to gold investors and people who aspire to free markets.

You can enroll for our dispatches on our mailing list on our homepage at gata.org. There’s no charge for that. We just want to get our word out, and we’re very grateful to anybody who wants to help us.

Mike Gleason: I’m on that list. I get those dispatches regularly, and it’s excellent stuff and a great way to stay up on this issue in particular and others as well related to gold and silver.

Well, we appreciate you coming on and spending time with us, Chris. Look forward to catching up with you again down the road, and I hope you enjoy your weekend. Take care, my friend.

Chris Powell: Thank you, Mike.

Mike Gleason: Thanks again to Chris Powell at the Gold Anti-Trust Action Committee. Again, check out gata.org for more information. They publish a lot of great content there at GATA, and we highly recommend everyone check that out. You can also make a tax-deductible donation there on the GATA site as well. Again, gata.org is where you can do all that.

Well, that will do it for this week. Be sure to check back next week for our next Friday for our next weekly Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange, thanks for listening, and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Russia’s central bank lowered its key interest rate for the fourth time this year due to a faster-than-expected decline in inflation and said it would consider further rate cuts in coming months if inflation continues to fall.

The Bank of Russia cut its key interest rate by 50 basis points to 6.50 percent and has now cut it by a total of 125 points this year following cuts in June, July, September and today.

“The Russian economy’s growth rate still remains subdued,” the central bank said, adding there are still risks of a substantial global slowdown, inflation expectations are declining and disinflationary risks exceed pro-inflationary risks.

The central bank normally cuts its rate in 25 basis points increments, but last week Governor Elvira Nabiullina said slowing economic growth and faster-than-expected drop in inflation would allow the central bank to “act more decisively” in comparison with past rate cuts that were moderate.

Russia’s inflation rate decelerated for the 6th consecutive month to 4.0 percent in September and is estimated to have declined further toward 3.8 percent as of October 21, the central bank said, cutting its forecast for inflation to average 3.2 to 3.7 percent this year from an earlier forecast of 4.0 to 4.5 percent.

Inflation is expected to decline to slightly below 3.0 percent in the first quarter of 2020 as a rise in Value-Added-Tax drops out of the comparison and average between 3.5 and 4.0 percent next year, settling around the bank’s 4.0 percent target further on.

“If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at one of the upcoming Board of Directors’ meetings,” the bank said.

Economic growth in Russia remains subdued with annual growth of 0.9 percent in the second quarter of this year and the central bank is maintaining its forecast for 2019 growth of 0.8 to 1.3 percent.

The forecast for coming years was also unchanged, with growth seen gradually rising to between 2.0 and 3.0 percent in 2022 based on the expectation that structural reforms will be carried out.

“However, the global economic slowdown expected over the forecast horizon will continue to exert a constraining impact on growth of the Russian economy,” the bank said.

The ruble, which has strengthened this year and thus helped slow inflation, rose a further 0.3 percent to 63.8 per U.S. dollar to be 9 percent higher than at the start of this year.

The Bank of Russia issued the following press release:

“On 25 October 2019, the Bank of Russia Board of Directors decided to cut the key rate by 50 bp to 6.50% per annum. Inflation slowdown is overshooting the forecast. Inflation expectations continue to decrease. The Russian economy’s growth rate still remains subdued. Risks of a substantial global economic slowdown persist. Disinflationary risks exceed pro-inflationary risks over the short-term horizon. In these circumstances, the Bank of Russia has lowered its annual inflation forecast for 2019 from 4.0–4.5% to 3.2–3.7%. Given the monetary policy stance, annual inflation will come in at 3.5–4.0% in 2020 and will remain close to 4% further on.

If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at one of the upcoming Board of Directors’ meetings. In its key rate decision-making, the Bank of Russia will take into account actual and expected inflation dynamics relative to the target and economic developments over the forecast horizon, as well as risks posed by domestic and external conditions and the reaction of financial markets.

Inflation dynamics. Inflation slowdown is overshooting the forecast. Annual consumer price growth rate declined to 4.0% in September (from 4.3% in August 2019) and was close to 3.8% according to the estimate as of 21 October. September results show that annual core inflation also decreased to 4.0% as compared to 4.3% in August. According to the Bank of Russia’s estimates, inflation indicators reflecting the most sustainable price movements are close to or below 4%.

In September—October, disinflationary factors had a more pronounced influence on the slowdown of price growth rates than it had been estimated before. At the same, time pro-inflationary risks related to the external conditions did not materialise. Taking into account one-off factors amid a good harvest and expanded supply in individual food market segments, seasonally adjusted food price growth rates remained low. The ruble appreciation since the beginning of the year alongside with inflation slowdown in Russia’s trading partners limits the price growth of imports. In addition, the impact of subdued demand on inflation is becoming increasingly strong. Domestic demand dynamics is also affected by the persisting delay in the financing of budget expenditures, including the expenditures on national projects, compared to earlier announced plans.

In September—October, households’ inflation expectations continued to decrease, while remaining elevated. Business price expectations slightly lowered. Annual inflation slowdown paves the way for a future decline in inflation expectations of households and businesses.

The Bank of Russia has lowered its annual inflation forecast for 2019 from 4.0–4.5% to 3.2–3.7%. Meanwhile, annual inflation will be slightly below 3% in 2020 Q1 when the effect of the VAT rate hike is factored out from the calculation of annual inflation. Given the monetary policy stance, annual inflation will come in at 3.5–4% in 2020 and will remain close to 4% further on.

Monetary conditions. Monetary conditions have continued to ease since the last Board meeting. Among other things, this was driven by the change in expectations of financial market participants with regard to the Bank of Russia’s key rate path. OFZ yields and deposit and lending rates continued to decline. The Bank of Russia’s decisions to cut the key rate and the decline in OFZ yields create conditions for a further reduction in deposit and lending rates.

Real sector lending continues to grow on the back of eased monetary conditions. At the same time, annual growth in lending to households has been slowing down since June after noticeable growth in 2018 — early 2019.

Economic activity. The Russian economy’s growth rate still remains subdued. In these circumstances, the Bank of Russia keeps unchanged its 2019 GDP growth forecast in the range of 0.8–1.3%. However, current data suggests that the growth of the Russian economy might accelerate in 2019 Q3, partially driven by temporary factors.

Economic activity continues to be constrained by weakening external demand for Russian exports on the back of a global economic slowdown as well as by weak investment activity dynamics, including government investment expenditures. August-September saw continuing annual growth of industrial production; however, leading indicators point to worsening business sentiment in the industrial sector, which is mostly specific of export orders. Growth in real disposable household incomes has yet to influence the dynamics of retail trade turnover. The labour market creates no additional inflationary pressure. The fact that unemployment remains near historic lows is not driven by expanding labour demand but rather by a simultaneously contracting number of employees and the labour force.

Since the beginning of 2019, fiscal policy has had a constraining effect on economic activity. This is in part related to a slower than expected implementation of national projects planned by the Government. Going forward, the rise in government expenditures, including investment ones, and their impact on economic growth will be more distributed over time.

The Bank of Russia has left the 2019–2022 GDP growth forecast unchanged. The GDP growth rate will gradually increase from 0.8–1.3% in 2019 to 2–3% in 2022. This will be possible should the Government’s measures for overcoming structural constraints, including the implementation of national projects, be realised. However, the global economic slowdown expected over the forecast horizon will continue to exert a constraining impact on growth of the Russian economy.

Inflation risks. Disinflationary risks exceed pro-inflationary risks over the short-term horizon. This is primarily related to the weak dynamics of domestic and external demand. Disinflationary risks associated with movements in prices of certain food products persist, including on the back of a rise in supply of farm produce. Pro-inflationary risks posed by budget expenditures growth in the second half of 2019 — early 2020 hold low because the rise in expenditures is likely to be more distributed over time. At the same time, should global economic slowdown be more pronounced, including due to tightening international trade restrictions and on the back of other geopolitical factors, this might lead to strengthened volatility in global commodity and financial markets, affecting exchange rate and inflation expectations.

A number of internal conditions continue to pose pro-inflationary risks over a longer-term horizon. Significant risks are posed by elevated and unanchored inflation expectations. The mid-term inflation dynamics may also be affected by fiscal policy parameters, including decisions on the investment of the liquid part of the National Wealth Fund in excess of the threshold level set at 7% of GDP.

The Bank of Russia leaves mostly unchanged its estimates of risks associated with wage movements and possible changes in consumer behaviour. These risks remain moderate.

If the situation develops in line with the baseline forecast, the Bank of Russia will consider the necessity of further key rate reduction at one of the upcoming Board of Directors’ meetings. In its key rate decision-making, the Bank of Russia will take into account actual and expected inflation dynamics relative to the target and economic developments over the forecast horizon, as well as risks posed by domestic and external conditions and the reaction of financial markets.

The Bank of Russia Board of Directors will hold its next key rate review meeting on 13 December 2019. The press release on the Bank of Russia Board decision and the medium-term forecast are to be published at 13:30 Moscow time.

In the follow-up to the Board of Directors meeting of 25 October 2019 the Bank of Russia released its medium-term forecast in connection to the publication of Monetary Policy Guidelines for 2020–2022, which are to be issued on 29 October 2019.”

There are two major components to becoming a successful forex trader.

The first is what we are all aware of: you need to be able to read and understand the forex market.

The second is just as important, and often is the difference between FX traders who consistently make money, and those who don’t: risk management.

So, it’s really important to know what your risks are when trading the forex markets. And one of the things about margin trading is that it magnifies risk. It, of course, also magnifies profit, which is the reason people use it.

In fact, the point of trading on margin is to magnify the effects of things.

What is Margin Trading?

Simply put, margin trading is when you borrow money from your forex broker to invest in the markets.

Usually you will put up a percentage of the money yourself, and the rest will be supplied by the broker. 1:10 margin means that for every $1 you put up, the broker loans you $9 so that you can enter $10 in trades.

The first risk here is pretty obvious. If the market goes your way, you stand to make ten times as much. But if the market goes against, you will lose ten times as much.

In some cases, you can lose more than you invest, which is why you want to trade with a forex broker that offers protection against your account going negative.

Mitigation

There are quite a few tools that you can use to minimize your losses, such as diversifying your trades, putting a limit on the size of the trade you make, and placing stop-loss orders.

Because trading with margin always implies a calculation of the ratio between how much you are risking compared to how much you have in your account, margin trading accounts are more sophisticated and complicated than your average cash accounts.

Many brokers offer you protections that can become risks of their own.

In order to prevent FX traders from losing more than they are willing to, forex brokers will often stop a trade when it loses the amount that was put up in margin. This protects you from going broke on a bad trade, but it also creates the dreaded margin call.

Margin Call

Originally, the margin call was literally a call: as in, when a forex trader’s leveraged position was losing to the point that the amount of money in his account was getting low, the broker would call him on the phone to ask if he wanted to put more money in to increase the available funds.

Nowadays, most FX brokers will simply terminate a trade that risks blowing out someone’s account when it reaches its margin level. It saves you from a negative balance.

But, that also means that you have significantly less money available in your account for trading. And that will make it a lot harder to recover the money you’ve lost.

The Greed Factor

Generally, forex traders run afoul of risk when they are trying to make trades that are too big, putting too much money into the market at once.

The simplest way of avoiding margin calls is to make smaller trades, and use reasonable stop losses. Most experts recommend not taking a trade that requires you to risk more than 3% of your account.

The thing is, when you have a usual cash account, you generally want to put most of it in the market so you can maximize your returns. Money without investing is not doing anything, especially in this low-interest environment.

But, with margin accounts, you have access to significantly more funds to invest. So, not only do you not need to have most of your account in the market at once, but you also don’t want to.

You want to keep your funds in reserve to mitigate risk and be ready for the next market opportunity.

The US dollar has been lower across the European morning on Friday on the back of further data weakness yesterday. IHS manufacturing reading for October did come in better than expected. However, the durable goods number was far worse than expected at -1.1% on the month. Continued data weakness is boosting market expectations of a Fed rate cut next week keeping USD pressured. The USD index trades 97.37 last.

EUR Lower On ECB

EURUSD has been a little higher today on the back of USD weakness though is only recovering the losses seen yesterday in response to the October ECB meeting. The meeting, which has the last for Draghi, saw the bank keeping the prospect of further easing alive. This is given the persistent weakness in the European economy. EURUSD trades 1.1117 last, back below.

GBP Soft Ahead of EU Decision

GBPUSD has been weaker across the European morning today. The EU has yet to grant the UK its Brexit extension request. This means that the UK could still crash out of the EU without a deal on October 31st. However, in line with recent recommendations from EC president Donal Dusk, the EU is likely to grant the request which should help lift GBP again. GBPUSD trades 1.2835 last.

Risk Pauses Into Weekend

Risk assets have been a little subdued on the final day of the trading week, though, the SPX500 remains supported near highs. With the Fed expected to cut rates next week, the outlook remains bullish for equities. Furthermore, with the US and China on course to do a deal and Brexit looking like it will be delayed again, the risk environment is encouraging.

JPY & Gold Firmer Over USD

Safe havens have both been higher against USD today given the weakness we have seen in the greenback. It seems that traders are covering riskier positions heading into the weekend with both JPY and gold firmer. USDJPY trades 108.63 last while XAUUSD trades 1504.78.

Crude Lifts Higher

Oil prices have risen firmly over the week and are currently trading in the green so far today. This week, the EIA reported an unexpected drawdown in US crude stores as a result of a sharp drop in US crude imports. The data has helped offset some of the downside pressure in oil along with optimism over ongoing US/China trade negotiations.

CAD Climbs On Oil Comeback

USDCAD continues to push lower today marking a week of losses as rising oil prices and increased Fed rate cut expectations are allowing CAD to recover. The potential for a US/China trade deal is also helping lift CAD which would benefit from the increase in commodity prices as trade recovers. USDCAD trades 1.3061 last having now broken below the 1.3068 support.

Aussie Down But Not Out

AUDUSD trades a little higher today also, taking advantage of the weaker USD, though finishes the week lower as of writing. AUD is very much tied to the ongoing US/China trade talks. Therefore, if we see positive headlines on the back of today’s meetings between US/Chinese officials this should help AUD at the start of next week. AUDUSD trades .6823 last, sitting off the .6850 level for now.

Azerbaijan’s central bank cut its benchmark discount rate for the 11th time since February last year and said further decisions on the interest rate would depend on the impact of internal risks on inflation and external factors, with the aim of reaching the targeted inflation.

The Central Bank of the Republic of Azerbaijan (CBA) reduced its discount rate by another 25 basis points to 7.75 percent and has now cut it by 7.25 percentage points since February 2018.

It is the 7th rate cut this year and the rate has been lowered by 200 basis points.

Azerbaijan’s economy is recovering from a banking crises and a prolonged downturn, but a stable exchange rate, lower food prices, anchored inflation expectations and an improving fiscal position prices has kept inflation subdued, allowing the central bank to ease its policy.

Inflation was steady at 2.6 percent in September and August and CBA expects inflation to be close to the center of its target range of 4.0 percent, plus/minus 2 percentage points by the end of 2019.

The economy is expanding due to higher natural gas production and domestic demand, with growth in the first 9 months of the year of 2.5 percent, including 3.5 percent in the non-oil sector.

Last year Azerbaijan’s economy grew 1.4 percent, bouncing back from a contraction in the previous two years, and the International Monetary Fund has forecast growth this year of 2.7 percent and 2.1 percent in 2020.

The yellow metal has been higher again this week. Gold posted its second consecutive positive week as of writing.

The main driver behind the move is the expectation that the Fed will cut rates again when it meets next week. Since the September FOMC meeting, data has been consistently poor. In particular, the manufacturing reading that we saw for September.

While this week, we saw manufacturing rebounding slightly over October, the data was accompanied by a sharp drop in US durable goods. With data remaining weak, the market is now looking for the Fed to ease again in October. This is keeping gold prices supported in the interim as the outlook for USD remains subdued.

Weakness in USD and expectations that the Fed will ease again this month have been providing upside pressure for gold. However, this upside has been offset somewhat by improved risk appetite thanks to increased expectations of a US-China trade deal.

The two countries have continued talks this week. There have been several phone calls between deputies on Monday. And today’s meeting (Friday) between the US Treasury Secretary and Trade Representatives and their Chinese counterparts will follow.

The market senses that the “phase one” trade deal Trump announced this month will be signed, as planned, at the upcoming APEC meeting. However, risks remain and the deal jas yet to be signed. Negotiations have broken down in the past and given the stubbornness of both sides, there is still room for upset.

Technical Perspective

Gold prices are now testing the upper trend line of the falling wedge pattern which has framed the recent consolidation near highs.

The recent 1481.93 level has formed interim support and while above here, a further push to the upside is still in the outlook. However, If we break below, the focus will shift to the 1436.19 level next and the 1392.28 level beyond that.

Silver

Silver prices have been higher across the week, tracking the moves in gold.

Metals have been higher despite the moves upwards in equities prices thanks to the recovery in risk appetite.

Supportive developments in US-China trade negotiations are keeping risk assets well bid with the SPX500 sitting just off all-time highs. However, despite the upside in equities, there are expectations that the Fed will cut rates this month.

If the Fed does press ahead with a rate cut, the market will be closely watching the monetary policy statement and conference after. They will pay special attention to gauge if any further cuts are likely this year. Especially given that currently, pricing for a December rate cut reflects divided opinions!

Technical Perspective

Silver prices have risen off the 17.3408 support and have broken above the upper trend line of the bull flag pattern which has formed on the pullback from recent highs. While above 17.3408, the focus remains on a further move higher with the 18.6397 the next topside level to watch.

However, If prices break down below the current support, the next major support level is down at 16.2130 which also holds the retest of the broken long term bearish trend line. To the topside, the 18.6397 level remains the key marker to break.

Expectations of higher crop and exports bearish for sugar price

Brazil’s sugar output is expected to rise in September while India subsidizes its exports. Will the sugar prices continue declining?

Sugar global price is depressed due to ample global supply. India’s government established export subsidy in the end of August to support sugar mills in shipping 6 million tons of sugar in 2019/20 October-September season. India is the fourth largest sugar exporter in the world. And Indian sugar mills are aggressively selling 2018/19 old crop sugar to Iran: they reached agreement to export 350,000 tons of sugar to Iran a week ago. A couple weeks ago S&P Global Platts analysts survey projected the sugarcane crush in the key Center-South Brazil region is expected to total 36.44 million tons in the second half of September, an increase of 30.9% year on year. And the proportion of cane used for sugar production is expected to be 34.44%, up from 33.02% a year earlier. Brazil is top sugar exporter in the world. Expectations of ample global supply are bearish for sugar prices.

On the daily timeframe the SUGAR: D1 is below the 200-day moving average MA(200) which is falling, this is bearish.

The Parabolic indicator gives a sell signal.

The Donchian channel indicates no trend: it is flat.

The MACD indicator gives a bearish signal: it is below the signal line and the gap is widening.

The RSI oscillator is rising but has not reached the overbought zone.

We believe the bearish momentum will continue after the price breaches below the lower boundary of Donchian channel at 12.05. This level can be used as an entry point for placing a pending order to sell. The stop loss can be placed above the last fractal high at 12.60. After placing the order, the stop loss is to be moved every day to the next fractal high, following Parabolic signals. Thus, we are changing the expected profit/loss ratio to the breakeven point. If the price meets the stop loss level (12.60) without reaching the order (12.05), we recommend cancelling the order: the market has undergone internal changes which were not taken into account.