The US dollar index was seen trading flat following two days of gains. Economic data was sparse on the day. The gains were also moderating after investors digested the progress of the US and China trade talks. Reports indicate that China is pressing Washington to roll back the tariffs imposed in September.

Eurozone Services PMI – Better Than Forecasts

The monthly services PMI data for September came out better than forecasts. Activity rose to 52.2 beating estimates of 51.8. The data was higher than the previous month’s reading of 51.8. Data from IMF showed that growth would slow for the Eurozone. The IMF said that the growth will be the slowest since 2013.

EURUSD Stalls at Support

The currency pair was seen stalling after support is being tested. The support area of 1.1075 – 1.1062 is holding the declines for the moment. This could offer some small respite as the currency pair could bounce to the upside. However, the gains might be limited in scope. Unless price rallies back to the upper resistance level of 1.1131, the currency pair will be range-bound.

Oil Prices Fall as Inventory Rises

Crude oil prices were down by over one percent on Wednesday. The declines came after the weekly crude oil inventory report saw an increase of 7.9 million barrels. This was more than the estimates of 1.5 million barrels for the week ending November 1st. The data corroborates the API’s report from earlier this week which also saw an increase in stockpiles.

WTI Crude Oil Retreats After Briefly Testing Resistance

Oil prices fell right after rising to test the resistance area of the 57.87 – 57.64 region. If the bearish momentum continues, then oil prices could slip further. However, there is a chance that support could form at the current levels of 56.40 – 56.50. If this support holds, then oil could potentially turn flat. To the downside, the lower support at 54.71 – 54.42 will be the level to watch.

Gold Snaps Back Recovering from Losses

The precious metal rebounded on Wednesday a day after price fell sharply. Gold prices are on track to recover close to 50% of the previous day’s losses. The rebound comes as the risk-on rally is starting to pause. However, gold will need to fully recover from Tuesday’s losses to maintain this short term uptrend.

Will XAUUSD form a Bearish Flag?

Price action on the 4-hour chart in gold indicates a potential for a bearish flag pattern. Currently, prices are testing the trend line. But a strong close above this trend line is needed to confirm the upside. Failure to post gains could see the bearish flag pattern coming into play. This puts the minimum downside target to 1440 support.

On Wednesday the 6th of November, trading on the euro closed slightly down at -0.07%. Following a rise to 1.1093, the bear hit fresh weekly lows in the Asian session. The effects of European data were short-lived. In the US session, the pair returned to 1.1065. There’s not much to say about what happened yesterday; better to get straight to analyzing our main pair.

Day’s news (GMT+3):

12:00 Eurozone: economic bulletin.

13:00 Eurozone: European Commission releases economic growth forecasts.

In today’s Asian session, the majors are trading down against the US dollar except for the safe havens. The yuan is falling, while the yen and gold are rising. Demand for the safe havens is rising amid speculation over renewed disputes between Washington and Beijing. China is seeking to have the 15% import tariffs imposed in September abolished. The US wants to conclude a deal without overturning previously imposed tariffs.

Yesterday’s target was missed. Today we expect a drop to 1.1043. The bears hit a new low in the Asian session, shifting the weekly low from 1.1064 to 1.1055. 1.1-43 is the minimum target for the double top model on the H8 timeframe. The question is via which model will this target be reached? Yesterday we wrote that we need to hit fresh lows before getting an upwards correction. This condition has now been fulfilled. Ideally, this correction should take place from the 112th degree.

By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

US-China trade deal could be delayed until December

Bank of England to keep rates unchanged

Sterling traders focused on MPC votes

A lot of excitement and positive news has been building in financial asset prices over the past few days. The three major US indices climbed to new highs, European and Asian stocks were also on the rise, the Chinese Yuan strengthened to below 7 per Dollar and most major currencies rallied against the Greenback. Most of this excitement was due to newsflow suggesting the US and China will finally sign a partial trade deal this month that will put an end to the 18-month trade war.

The latest reports suggest both President Donald Trump and Xi Jinping may not sign the Phase I trade deal until December as the parties seem to be in disagreement over where and when the deal should be signed. This shouldn’t be a big surprise given the history of tensions between the two countries. My concern is not the delay, as a few more days to sign the agreement won’t make a big difference. But, whether there are deeper conflicts within the agreement itself is my main concern, particularly the scale of tariff rollbacks that China may be asking for. China is now likely to consider itself in a better position given Trump’s impeachment inquiry and as we get closer to the US 2020 presidential elections. Investors will be in wait and see mode until a venue and a date is announced. Until then, expect equities to retreat from their multi-month and record highs.

Currency traders will be focused on Sterling today as the Bank of England (BoE) announces its policy decision. In its September meeting, the central bank said it might consider a rate cut even if a no-deal Brexit is avoided on October 31. Since then, data has shown a mixed picture of the economy and is not likely to trigger a rate cut.

Despite the bank being expected to keep the key rate unchanged today, it will be interesting to see if one or two members of the MPC vote for a rate cut. Such a vote would suggest that the BoE is tilting towards a more dovish stance in monetary policy and will increase the odds of a rate cut early next year. Any signs of the BoE indicating an easing policy will likely lead to a further selloff in the Pound.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The rise of the Shanghai Import Expo reflects China’s huge transformation from world producer and cheap prices to world consumer and innovator.

Speaking at the second China International Import Expo (CIIE) in Shanghai, Chinese president Xi Jinping pledged China will stimulate increased imports, continue to broaden market access, foster a world-class business environment, explore new horizons of opening-up and promote international cooperation at multilateral and bilateral levels.

In order to safeguard and promote economic globalization, Xi said two years ago at the World Economic Forum in Davos, Switzerland that “efforts to reduce tariff barriers and open up wider will lead to inter-connectivity in economic cooperation and global trade.” In contrast, “the practices of beggaring thy neighbor, isolation and seclusion will only result in trade stagnation and an unhealthy world economy.”

Today, that message is critical. The World Bank has forecast only 2.6 percent global growth in 2019. That’s the lowest since the global financial crisis of 2008-9. And the collateral damage of trade protectionism is spreading worldwide.

China shifts from exports to imports

In the past, the best known trade event in China was the Canton Fair in the southern Guangdong province. In October, even amid the US tariff wars, it attracted more than 210 countries and regions, 25,000 companies and some 200,000 potential buyers, most of which were from Belt and Road countries.

China is now promoting the Shanghai CIIE as the world’s first international import expo. Its partners include the World Trade Organization and key United Nations trade organizations, which understand well that the CIIE reflects China’s structural rebalancing from investment and net exports toward innovation and consumption.

Shanghai, the most international Chinese megacity, is the natural host of the import expo. While the Canton Fair built its clout over decades, the Shanghai CIIE could develop its international influence in a matter of years.

Despite international tensions, it has attracted foreign leaders, such as French President Emmanuel Macron, diamonds from Belgium, Cambodian fragrant rice, and Kenyan farm products, along with US automaker Ford’s cutting-edge Ford and Lincoln brands. Despite the US tariff war against China, almost 200 US-based companies – from GE to Qualcomm – are participating in the CIIE and US companies have the largest exhibition space at the expo.

While the Canton Fair has morphed from traditional manufacturing exports to advanced technology, the Shanghai CIIE is focused on imports. It’s a massive shift in a country of more than 1.3 billion people. As China has prospered, Chinese companies have invested increasingly abroad, while Chinese consumers can afford foreign imports, thanks to reforms and opening-up policies, and Chinese innovation in ecommerce.

Middle-income consumers drive import growth

Recently, the European Union (EU) said that its firms had provided positive feedback on the CIIE last year, registered increased sales or met new potential buyers. Yet, EU wants more to do more vis-à-vis the EU-China investment agreement.

Obviously, the US, the EU and Japan would like to see China implementing the kind of reforms that support their exporters in the near term. But such reforms cannot happen disruptively. Even the advanced countries fought two world wars and were engaged in a Cold War before import growth truly picked up internationally.

While the middle class is shrinking in the West, China’s gradual reforms will ensure a rapidly expanding middle-income consumer base, the new precondition of international trade. As the world factory is morphing into the world’s largest market, rising numbers of consumers fuel import growth.

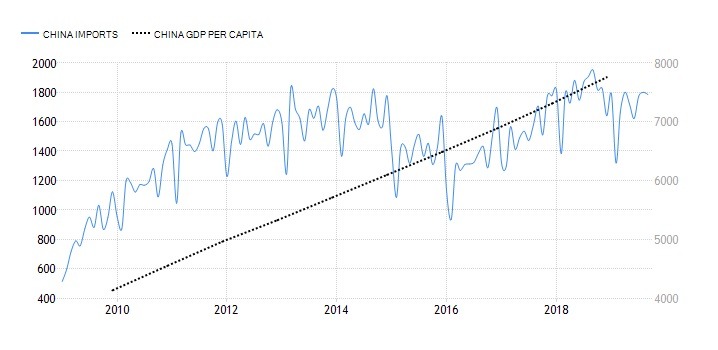

As China’s intensive industrialization shifts toward a post-industrial society, GDP growth is decelerating, but living standards, as measured by per capita income, are rising (Figure). That is vital for import growth over time and provides a blueprint for middle-income groups in other large emerging countries, such as India.

FigureChinese Imports and GDP Per Capita, 2000-2019

As long as globalization advances in both rich and middle-income economies, imports to China increase. For instance, as the world economy was still recovering in early 2018, Chinese imports reached an all-time high. But after the US began imposing heavy tariffs on Chinese imports, businesses invested more cautiously and consumers became more cost-conscious. After all, China’s average per capita income remains only 15-25 percent of that in the US and Western Europe.

Long-term benefits require global cooperation

Some US research firms expect China to become the world’s top retail market this year, surpassing the US. The forecast may be optimistic, but the trend is clear. Today, China’s imports of goods and services are estimated to be about 10 percent of the global total and, given international peace and stability, they will continue to expand.

China’s focus is on economic development that shuns trade protectionism and seeks to balance the needs of the global economy and its own economy. That’s why, instead of promoting “China First” nationalism and imposing excessive tariffs on imports, China is helping the Canton Fair to expand international trade and the Shanghai CIIE to supports import and that’s why President Xi promotes globalization.

That’s very much in the long-term interest of both the advanced and developing economies.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar worldand the founder of Difference Group. He has served at the India, China and America Institute (US), the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

The original commentary was published online by China Daily on Nov 6, 2019, and in print on Nov 7, 2019.

US stocks recorded another session of mixed performance on Wednesday after reports of possible delay of China-US trade until December. The S&P 500 rose 0.07% to 3076.78. The Dow Jones industrial average slipped less than a point to 27492.50. Nasdaq lost 0.3% to 8410.63. The dollar strengthening continued as Chicago Fed President Charles Evan said the US economy may not need additional interest rate cuts. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.04% to 97.94 and is higher currently. Futures on US stock indices point to higher openings.

CAC 40 still leader among European indexes

European stock market extended gains on Wednesday as companies continued reporting quarterly results. Both GBP/USD and EUR/USD continued their slide yesterday with euro gaining currently while Pound lower still against the dollar. The Stoxx Europe 600 added 0.2% led by banking shares. Germany’s DAX 30 advanced 0.2% to 13179.89 as services sector accelerated expansion in October. France’s CAC 40 rose 0.3% and UK’s FTSE 100 gained 0.1% to 7396.65 ahead of Bank of England policy meeting today with market participants expecting no interest rate change.

Australia’s All Ordinaries Index leads Asian indexes gains

Asian stock indices are mostly higher today. Nikkei rose 0.1% to 23330.32 as yen resumed its slide against the dollar with the Bank of Japan Governor Haruhiko Kuroda comment the central bank would continue its massive monetary easing to achieve its 2% inflation target. The Shanghai Composite Index is marginally higher while Hong Kong’s Hang Seng Index is up 0.4%. Australia’s All Ordinaries Index turned 1% higher despite Australian dollar’s continued climb against the greenback.

Brent futures prices are recovering today. Prices fell yesterday on bigger than expected US crude inventories buildup as the Energy Information Administration reported US crude stocks rose by 7.9 million barrels, with gasoline supplies falling by 2.8 million barrels. January Brent crude fell 1.9% to $61.74 a barrel on Wednesday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Bob Moriarty of 321gold dives into rare earth elements and one company exploring a high-potential property in British Columbia.

I know of no sector in the resource space as hard to get a handle on as that of the Rare Earths or REOs, AKA REEs. In the last twenty years I have only come across one investor who actually understood which companies had red meat and which were pushing tofu. Since 321gold is a tofu free zone, I’ve been hesitant to even start writing about the sector.

Months ago one of my advertisers, Defense Metals Corp. (DEFN:TSX.V; DFMTF:OTC; 35D:FSEQB), approached me about writing a piece about them and their potential. More or less I agreed since I haven’t written anything about REEs for the longest time but I insisted they hand me something that would make it clear to my readers just what their potential was.

To be clear, REE or REOs are not rare. There are seventeen elements called Rare Earths and while they are quite common, it is not common for them to be concentrated sufficiently to justify the expense of exploration and building a processing facility for mining them.

Defense Metals has a project they call the Wicheeda property located in central British Columbia about eighty km north of Prince George. The property has excellent infrastructure, is on a primary forest service road connecting to a major highway and has experienced mining professionals located nearby.

My primary problem was a lack of understanding of just what the value of a ton of rock could be. It’s all well and good to be quoting % grade and thickness of intercepts but that is pretty meaningless unless and until someone can come up with a value of the rock in the ground.

Management of DEFN answered me in spades. The company just drilled a 13-hole program at Wicheeda. They have released results from the first two holes, eleven more are coming soon. Two weeks ago they released results from a metallurgy study to determine their ability to concentrate the material and show recovery.

I’m astonished they have so far failed to post the press releases on their own site but they didn’t and the numbers are most important. They ran a flotation test and managed to produce a concentrate of 48.7% TERO (Total Rare Earth Oxide) from a head grade of only 4.81%. In addition they showed an 85.7% recovery. Those are exceptional numbers. With any mineral deposit, the cost of shipping concentrate is vital to know. To concentrate by a factor of ten fold is excellent.

The two holes released so far showed both good grade and length of intercept. From near surface, hole WI19-20 reported 64 meters of 4.32% TREO. Hole WI19-21 showed a grade of 3.26% REOs with a length of 110 meters. The company is using a cut off grade of 1.0% of LREE (Light Rare Earth Elements).

But without knowing some idea of the value of a ton of rock, investors are left alone in the cold and dark. I asked for some indication of what those assays meant in real dollar terms. And again, it’s a little loosey goosey because these metals are not traded on exchanges so these numbers are not written in rock, just an indication.

Based on the head grade of 4.81% of the material submitted for testing an approximated gross metal value at today’s indications of price would be about $585 USD per ton. You would need to discount that by 20% to get a recovered gross metal value in the ground. That’s about $468 USD per ton or equal to about 10 grams of gold. Those are great numbers for grade and for reported intercepts of the first two holes.

China and the U.S. are at loggerheads and engaged in a serious trade war. I am not a fan of any war, having been through two years of one. In my experience, no one wins any war; all that happens is that one side loses more than the other.

Since the Chinese have probably read a history book or two and U.S. politicians live in an echo chamber, the Chinese see the U.S. as a morally and fiscally bankrupt state in a rapid condition of decline. If the U.S. is going to become a third world country, the Chinese don’t care about doing trade with us.

Rare Earth Elements are necessary for all sorts of modern technology. If the Chinese maintain a strangle hold on supplies the U.S. had better put their spurs on and start developing supplies from more friendly neighbors.

I have maintained for years that the way to profit in any venture is as simple as buying cheap and selling dear. Everyone wants to make investing complex and that’s utter nonsense. If you can figure out when things are cheap you should buy them and when they get expensive you should sell them.

Defense Metals is certainly cheap. The company did their IPO at $0.15. All of the financings to date have been from $0.15 to $0.25. The serious long-term investors are all in at higher prices. The metallurgy is comparable to the top three REE mining companies in the entire world. At today’s price the company is valued at a tiny $2.5 million USD. That’s insane. The company has everything going for it except understanding from retail investors and I hope this piece helps.

I am an investor in DEFN. They are advertisers and naturally that makes me biased. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Defense Metals. Defense Metals is an advertiser on 321gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this interview, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Defense Metals, a company mentioned in this article.

The Bank of England will be holding its monetary policy meeting today. Officials at the central bank will, no doubt, be leaving interest rates steady.

The UK’s interest rates stand at 0.75%, for the most part, this year.

So far there is no evidence of pressure on the central bank. This comes as inflation has been weaker and falling below the BoE’s 2.0% inflation target rate. But the UK’s economic outlook remains weak.

The BoE is one of the few central banks which has not cut rates unlike the Federal Reserve or the ECB.

In its previous outlook, officials gave a forecast of 1.3% GDP growth for both this year and next year. This is unlikely to change at this meeting. The central bank continues to maintain that interest rates could rise in the longer term.

BoE Interest Rates

The central bank has repeatedly stuck to this tone as it expects that growth will start to kick in. But complicating the central bank’s monetary policy is the Brexit uncertainty.

The UK was supposed to leave the EU on the 31st of October. But this did not happen. In fact, the UK now sought another extension that sees the Brexit deadline pushed to January 2020.

Despite the rates staying steady, some officials remain wary that the central bank isn’t doing much. The current Brexit uncertainty has hit business investment very sharply. Therefore, some members of the BoE’s monetary policy committee see the need for a rate cut.

They argue that a rate cut will help to boost sentiment. But the rate cut could be unnecessary as the effects could be limited to a certain extent alone. As long as the Brexit uncertainty continues, investment will continue to remain weak.

UK’s Snap Elections to Keep BoE on Hold

The central bank also has to contemplate the December elections as well. After UK lawmakers failed to pass the Brexit deal within the October 31st deadline, PM Johnson called for a snap election.

The elections are seen by some as the UK’s ability to hold a second referendum.

The Labor party led by Jeremy Corbyn maintains that they will seek a new Brexit deal, which includes putting forth a second referendum. Whatever the case, the uncertainty will continue to take a toll.

The UK economy has been resilient. After initially contracting in August, the GDP has been put back on track. But officials from the UK Office for National Statistics say that they need to assess more information.

Therefore, the likelihood that the UK economy will be resilient to Brexit uncertainty is still questionable. For the moment, the UK’s extra public spending could add up to 0.4% to the GDP growth.

This reduces the risk of a recession at least for the short term.

The third-quarter GDP reports suggest that growth could rise above 0.3%, indicating that the temporary slip in growth was only transitory.

In January, the current BoE Governor, Mark Carney will also finish his term at the helm. The UK government was supposed to announce a new BoE chief last week, but it postponed the decision.

Thus, amid the uncertainty and chaos, the best possible solution for the BoE would be to remain on the sidelines. A lack of pressures on the central bank also makes it easy for officials to stay mum until there is some clarity to the near term horizon.

Fulgent Genetics shares traded more than 40% higher today after the company reported record revenue in Q3/19. The firm noted that it completed a record 20,697 billable tests in Q3/19, up 272% over the same period last year.

After U.S. markets closed yesterday, Temple City, Calif. based provider of comprehensive genetic testing and Next Generation Sequencing (NGS) solutions Fulgent Genetics Inc. (FLGT:NASDAQ), announced third quarter financial results for the period ending September 30, 2019.

In the report the company advised that revenue in Q3/19 increased 84% to a record $10.3 million, compared to $5.6 million in Q3/18. The revenue increase was driven by record billable tests completed, which grew by 272% year-over-year to 20,697.

During Q3/19 the firm indicated that gross margin improved by 8.9 percentage points to 62.45% up from 53.56% in Q3/18, and the cost per test performed improved 60% year-over-year and 15% sequentially.

The company stated that GAAP income for the Q3/19 was $1.5 million, or $0.08 per share, and non-GAAP income was $2.6 million, or $0.14 per share. The firm advised that in Q3/19 Adjusted EBITDA increased 950% to $3.0 million, compared to $281,000 in Q3/18.

The company’s Chairman and CEO Ming Hsieh commented, “We continued to build on our momentum in the third quarter and once again posted very strong results. Revenue and billable test volume reached new record highs in the third quarter, while cost per test continued to improve. Our strong top line results have been driven by the growing traction with our oncology and reproductive health businesses, as well as our sequencing-as-service offering. Our established strategic investments and partnerships are contributing to our ongoing momentum, and we have been successful in meeting the growing demand from our new commercial genomic customers. We believe our superior test capabilities, extensive and flexible test menu, along with our competitive pricing will continue to drive strong growth across our business.”

Paul Kim, CFO at Fulgent Genetics, added, “We once again achieved record results in the third quarter, exceeding our expectations for test volume, revenue and profit. At the same time, we have seen increasing efficiencies across our business which have resulted in ongoing improvements in gross and operating margins. These efficiencies coupled with our increasing scale resulted in meaningful EBITDA, net income and cash flow generation in the quarter. We expect to see continued progress as we close out the year.”

Fulgent Genetics describes itself as a technology company focused on offering comprehensive genetic testing in order to provide physicians with clinically actionable diagnostic information they can use to improve the quality of patient care. The company states that “it has developed a proprietary technology platform which allows it to offer a broad and flexible test menu and continually expand and improve its proprietary genetic reference library, while maintaining accessible pricing, high accuracy and competitive turnaround times. The company believes its test menu offers more genes for testing than its competitors in today’s market.”

Fulgent Genetics began the day with a market cap of about $173.8 million with approximately 18.49 million shares outstanding. FLGT shares opened more than 22% higher today at $11.50 (+$2.10, +22.34%) over yesterday’s closing price of $9.40. The stock has traded today between $10.90 and $13.59/share and reached a 52-week intraday high price in morning trading. At present, the stock is trading at $13.25 (+3.85, +40.96%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The Critical Investor delves into a lithium company’s financing and its implications.

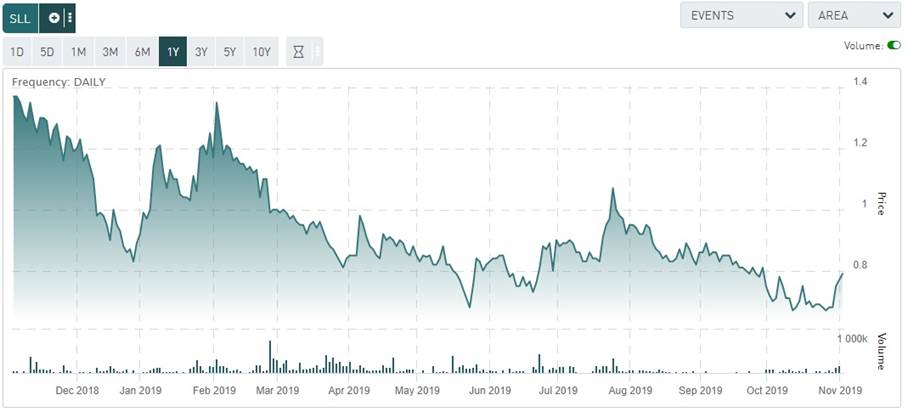

It seems more and more likely that Standard Lithium Ltd. (SLL:TSX.V; STLHF:OTCQX; FRA: S5L) is displaying a serious commitment of giant JV partner Lanxess these days, with construction of the demonstration plant advancing rapidly along the way. Standard managed to arrange a C$5 million (US$3.75 million) convertible loan and guarantee agreement with Lanxess AG (LXS:DE) on October 30, 2019, and has already been paid out to Standard. The proceedings will be used for the ongoing development of the mentioned demonstration plant, which is capital intensive.

All presented tables are my own material, unless stated otherwise.

All pictures are company material, unless stated otherwise.

All currencies are in US Dollars, unless stated otherwise.

According to the news release, the terms are as follows:

“The principal amount of the Loan will be convertible at the option of the Lender at a rate such that for each C$0.80 of principal converted, the Lender will receive one common share of Standard Lithium (each, a “Common Share”) and one-half of a warrant to purchase an additional Common Share with an exercise price of C$1.20 per Common Share and a term of three years (each whole warrant, a “Warrant”). Assuming full conversion of the Loan principal, the Lender would receive 6,251,250 Common Shares and 3,125,625 Warrants. All securities issued upon conversion of the Loan will be subject to four-month-and-one-day statutory hold period from the date the Loan was advanced.”

A conversion price of C$0.80 is reasonable, as the share price at the moment of publication was C$0.68:

Investors reacted immediately to the positive news, and after a few days of trading at increased volume the stock finds itself at C$0.75 now (November 5, 2019). If Lanxess would convert into shares, the dilution would be 7%, which is very decent. But as it is a loan, the prospect of future dilution is just an option of course for Lanxess. The news release continues:

“The outstanding principal amount of the Loan will bear interest at an annual rate of 3.0%, subject to adjustments. In the event that Standard Lithium has a positive consolidated operating cash flow, as shown on its financial statements, Standard Lithium will pay a fee to the Lender of 4.5% per annum on the average daily outstanding principal amount of the Loan from the issuance date to the date that the consolidated operating cash flow of Standard Lithium is positive. From and after the date on which the consolidated operating cash flow of Standard Lithium is positive, the annual interest rate increases to 7.5%. Pre-payments are permitted with prior written approval of the Lender and are subject to a prepayment fee of 3.0% on the portion of the Loan being prepaid.”

The initial interest rate of 3% is extremely low, meaning C$150,000 of annual interest payments until positive consolidated operating cash flow is achieved. The 7.5% rate in production stages is still very fair, as loans fetch often percentages around 1015% pre-production, as risks are high. Loan periods are often limited (12 years) as well, and this is something where Lanxess came in with a more realistic scenario:

“The Loan is due and payable in full on the fifth anniversary, subject to the provision that at any time after second anniversary, the Lender may elect an earlier maturity date on 60 days’ notice to Standard Lithium. The Loan is secured by a charge on the shares of Standard Lithium’s direct and indirect subsidiaries (collectively, the “Subsidiaries”) Arkansas Lithium Corp. (which operates the Demonstration Plant), Vernal Minerals Corp. (a holding company which owns the shares of Arkansas Lithium Corp.), and 2661881 Ontario Limited (which owns intellectual property rights to be used in the operation of the Demonstration Plant), as well as by a security interest in the tangible and intangible property of Standard Lithium and the Subsidiaries.”

A five-year period is very generous for these kind of loans, and to me it speaks volumes about the positive intentions of Lanxess as a JV partner. They really want this to proceed, and if possible make a decent amount of money on equity if successful in my view. This didn’t come for free of course, Lanxess wanting to secure the loan against not only the demonstration plant but also the intellectual property rights, as the plant in itself probably only represents an average breakup value of 2025% at most as it is very specific, which alone would barely cover the principal.

With this money, Standard will be able to complete the construction, installation and first testing of the demonstration plant, which is planned to start commissioning during November. This is one month later than planned in August of this year, but compared to your average pilot plant project this is still very acceptable and hardly worth mentioning. Keep in mind that Standard is planning to raise another C$1015 million to continue testing and optimizing for the next 1218 months, which is planned to go on parallel to construction of the large commercial plant if everything works out as hoped, even if Lanxess eventually decided to do so in Q3, 2020. As a reminder, the demonstration plant is designed to continuously process an input tailbrine flow of 50 gallons per minute (gpm; or 11.4 m3/hr) from the Lanxess South Plant, which is equivalent to an annual production of between 100150 tonnes per annum lithium carbonate equivalent (LCE) (see news release Oct. 15,2019).

The demonstration plant is roughly designed at 1/100 of the final nameplate production capacity, should provide sufficient testing data in Q1 2020 for a planned upcoming Pre-Feasibility Study (PFS) in Q2 2020, and if the testing is successful it should be straightforward to scale to nameplate capacity after the investment decision would have been made by Lanxess. The demonstration plant is based on Standard Lithium’s proprietary LiSTR technology, that uses a solid sorbent material to selectively extract lithium from Lanxess’ tailbrine. The environmentally friendly process eliminates the use of evaporation ponds, reduces processing time from months to hours and greatly increases the effective recovery of lithium.

To see Lanxess seriously providing funding for the first time with hard cash, besides providing Standard with a location for the demonstration plant and the opportunity to test the proprietary lithium extraction process, is noteworthy in my view. Up until this point it was risk-free sailing for Lanxess, having Standard raising all the cash and developing methods, economic studies and demonstration plants. After this loan, things seem to get more serious for the giant chemical company from Germany, as it is very involved in material innovations for batteries and electromobility. Lanxess already offers many products and solutions along the value chain of lithium-ion batteries, and a wide range of polyamides and polyesters for the electric powertrain. It specifically mentions the project for extraction of lithium from in-house sources besides the other two I just mentioned, indicating the importance for them.

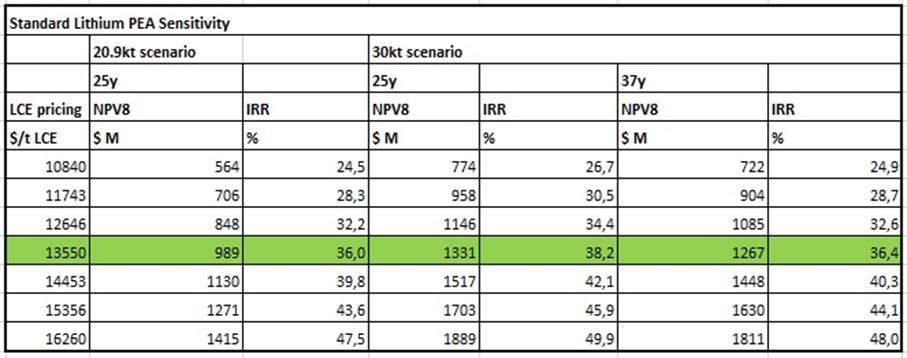

As a reminder: the economics indicate a pretty robust project, at a capex of US$437 million an operation can be constructed with an after-tax NPV8 of US$989 million and an after-tax IRR of 36%, based on an average long term LCE price of US$13,550/t. I viewed this base case price as high, as it was based on a 3-year average, which is not very realistic in the lithium product realm. However, based on current LCE spot prices of about average US$11,500/t, after tax figures would still come in economic, and this is important. Depending on successful testing of course. Three scenarios are presented, the 20.9kt LCE pa (per annum) base case, and the hypothetical 30kt LCE pa expansion scenarios:

These figures are based on 100% project ownership economics, and 100% equity financed, which is standard for economic studies or hypothetical estimates like this. In the news release dated November 12, 2018, Lanxess is committed to provide project finance to the JV when testing and the PFS are successful for them, and Standard will probably be an estimated 30% JV partner (according to company documents filed on Sedar). Regarding the NPV8, I have been very conservative, taking into account that management indicated to me that they expect a lot from optimization programs for brine and processing. This could actually imply improved economics for the upcoming PFS.

As initial capex is US$437 million, and Lanxess would provide financing for the entire project for construction, and as reported in the company’s prospectus filed last spring Lanxess will take 100% of the off-take, the current market cap of Standard Lithium is just C$69.6 million (or US$52.9 million), it seems to make more and more sense to me that Lanxess will buy out Standard outright when testing and PFS proves to be successful, as the Standard market cap is just about 25% of their attributable base case NPV8. Even at a double from now it seems Standard will be a bargain, not accounting for any expansion and/or optimization programs. I’m very much looking forward to the all-deciding testing that is about to start.

Conclusion

Standard Lithium received another strong vote of confidence from JV partner Lanxess, by providing hard cash. This is a pretty encouraging sign in my view, as up to now Lanxess only provided support through means that hardly cost them anything. As Lanxess is now showing its attention to the importance of electrification with their New Mobility business (p.54), it seems very interested in production of lithium products themselves, and combined with upside potential for their JV project with Standard and low valuation of Standard compared to NPV8 it doesn’t seem very unrealistic for Lanxess to buy out Standard outright when testing and PFS deliver economic results during Q1/Q2 of next year, as the project is already totally in their own backyard, and a potential cash cow bolt-on on existing operations.

I hope you will find this article interesting and useful, and will have further interest in my upcoming articles on mining. To never miss a thing, please subscribe to my free newsletter on my website http://www.criticalinvestor.eu to get an email notice of my new articles soon after they are published.

The Critical Investor is a newsletter and comprehensive junior mining platform, providing analysis, blog and newsfeed and all sorts of information about junior mining. The editor is an avid and critical junior mining stock investor from The Netherlands, with an MSc background in construction/project management. Number cruncher at project economics, looking for high quality companies, mostly growth/turnaround/catalyst-driven to avoid too much dependence/influence of long-term commodity pricing/market sentiments, and often looking for long-term deep value. Getting burned in the past himself at junior mining investments by following overly positive sources that more often than not avoided to mention (hidden) risks or critical flaws, The Critical Investor learned his lesson well, and goes a few steps further ever since, providing a fresh, more in-depth, and critical vision on things, hence the name.

The Critical Investor Disclaimer: The author is not a registered investment advisor, and currently has a long position in this stock. Standard Lithium is a sponsoring company. All facts are to be checked by the reader. For more information go to www.standardlithium.com and read the company’s profile and official documents on www.sedar.com, also for important risk disclosures. This article is provided for information purposes only, and is not intended to be investment advice of any kind, and all readers are encouraged to do their own due diligence, and talk to their own licensed investment advisors prior to making any investment decisions.

Streetwise Reports Disclosure: 1) The Critical Investor’s disclosures are listed above. 2) The following companies mentioned in the article are sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

The central bank of Belarus cut its benchmark refinancing rate for the second time this year, saying this would help ensure a neutral monetary policy as inflation continues to slow. The National Bank of the Republic of Belarus cut its refinancing rate by another 50 basis points to 9.0 percent and has now cut it by 100 points this year, extending an easing cycle since April 2016. Since then the repo rate has been lowered by 16 percentage points.

The bank also narrowed its interest rate corridor to 2 percentage points from 2.5 points to increase the efficiency of the transmission of monetary policy on inflation. The overnight loan rate was cut 75 basis points to 10.0 percent and the overnight deposit rate by 25 basis points to 8.0 percent to help narrow the range of rates on instruments that regulate bank liquidity.

“Subsequently, these rates will change simultaneously with the refinancing rate by an appropriate amount,” the central bank said.

Inflation in Belarus slowed to 5.3 percent in September and the central bank said it expects inflation to be near its 5.0 percent target by the end of 2019 and during 2020. Last month the central bank’s deputy chairman, Sergei Kalechits, said the main objective next year is to keep inflation below 5 percent, to maintain the level of foreign exchange and gold reserves, develop financial market instruments and strengthen the banking system.

Belarus’ gross domestic product slowed slightly to 1.3 percent year-on-year in the first quarter of this year from 1.4 percent in the previous quarter.