The yellow metal was higher this week, driven by a surge in safe-haven demand as rising fears over the health of the US/China trade negotiations saw equities heavily lower. News that the US had passed legislation offering support to the pro-democracy protestors in Hong Kong was met with fury by China.

China had previously warned the US not to get involved in the situation. While Trump had done his best to stay neutral, he was eventually forced to support the bill under rising political pressure. China immediately postponed a US naval visit. Reports also circulated saying that trade talks had broken down. Equities prices around the globe were quickly lower. Losses increased on news that China was considering banning US diplomatic passport holders from traveling there.

Into the middle of the week, however, the situation appeared to calm down as China reassured markets that talks were continuing. China does, however, continue to insist that the US remove existing tariffs in order for the phase-one trade deal to be signed. The US continues to refuse to remove tariffs, meaning that the chances of a deal being done this year appear in jeopardy.

If a deal is not signed in the coming weeks, the threat of fresh tariffs from the US will come into focus. Such as development would likely see gold sharply higher on increased safe-haven flows, as equities prices sink lower again.

Technical Perspective

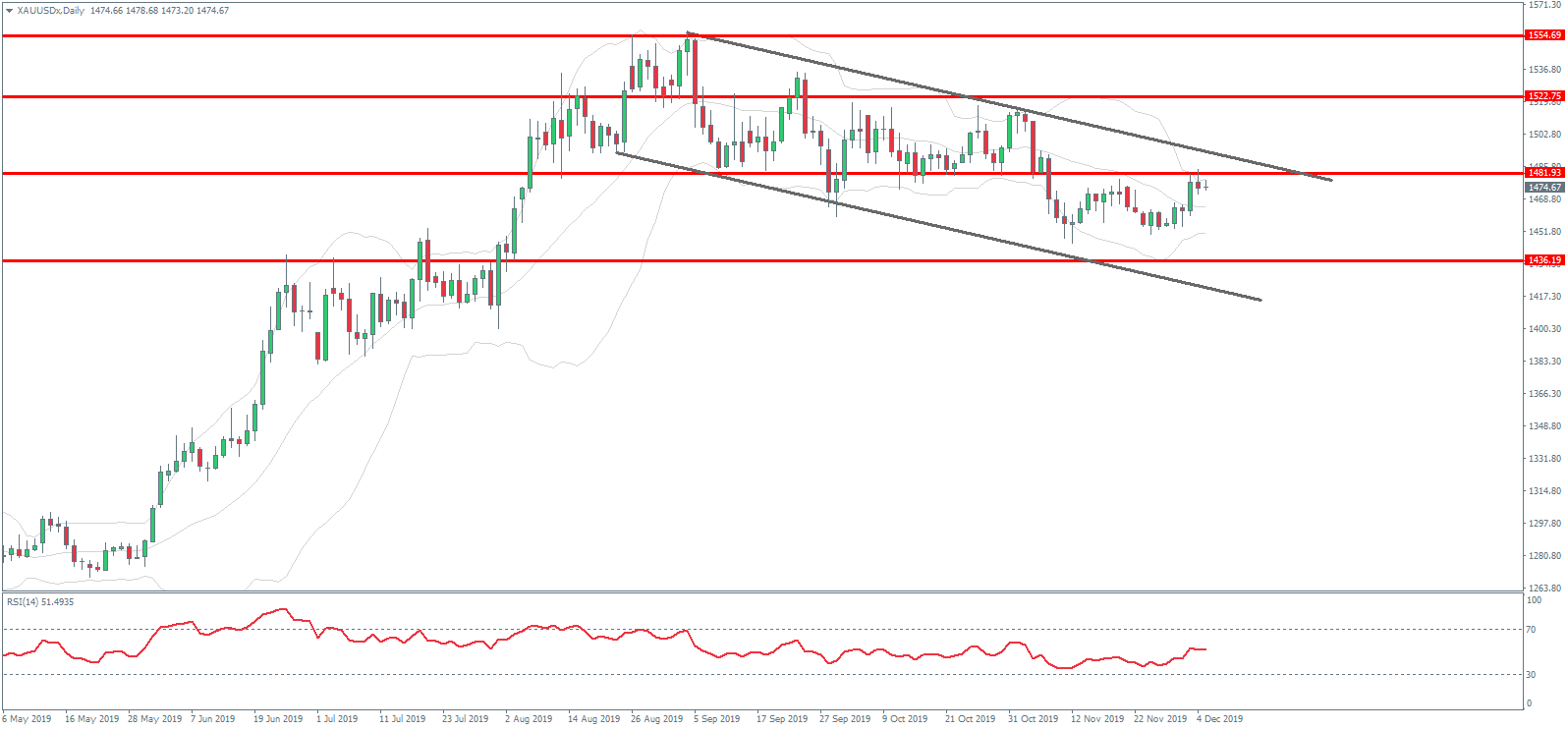

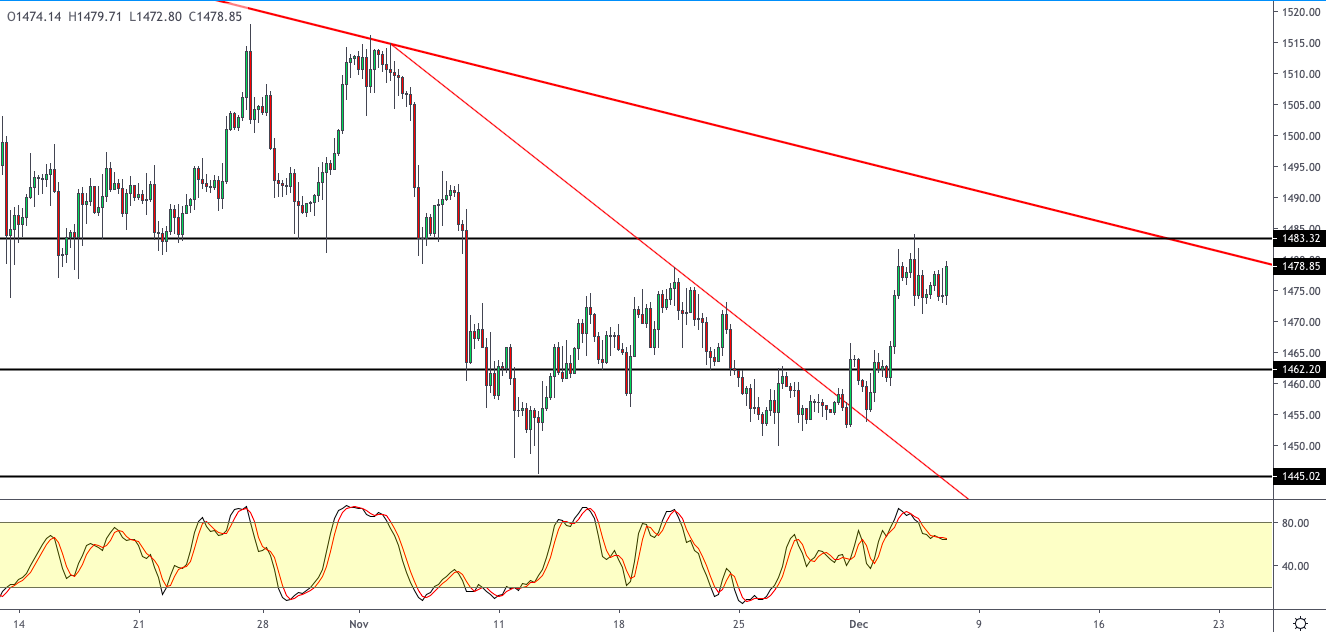

Gold prices have corrected higher within the bearish channel which has framed the sell-off from 2019 highs. Price is now retesting the 1481.93 level which is holding as resistance for now.

For now, the pattern can still be viewed as a corrective bull flag suggesting that upside could still materialize. If the price can break back above the 1481.93 level, the key level to watch in the short term is 1522.75. This is a major long-term pivot for gold. Above here, the focus will be on a move back up to the recent 1554.69 level.

Silver

Silver prices broke from their correlation with gold prices this week to trade lower. Despite the safe-haven support for gold, the rising uncertainty around the US/China trade talks is weighing on sentiment for silver. The sharp move lower in equities has also dampened price action in silver. The moves lower in industrial indexes are weighing down on prices.

Looking ahead to next week, the US FOMC meeting will be the key risk event for metals. A dovish outlook from the Fed might offer some support to metals though this might be offset by the ongoing uncertainty over the prospect of a US/China trade deal.

Technical Perspective

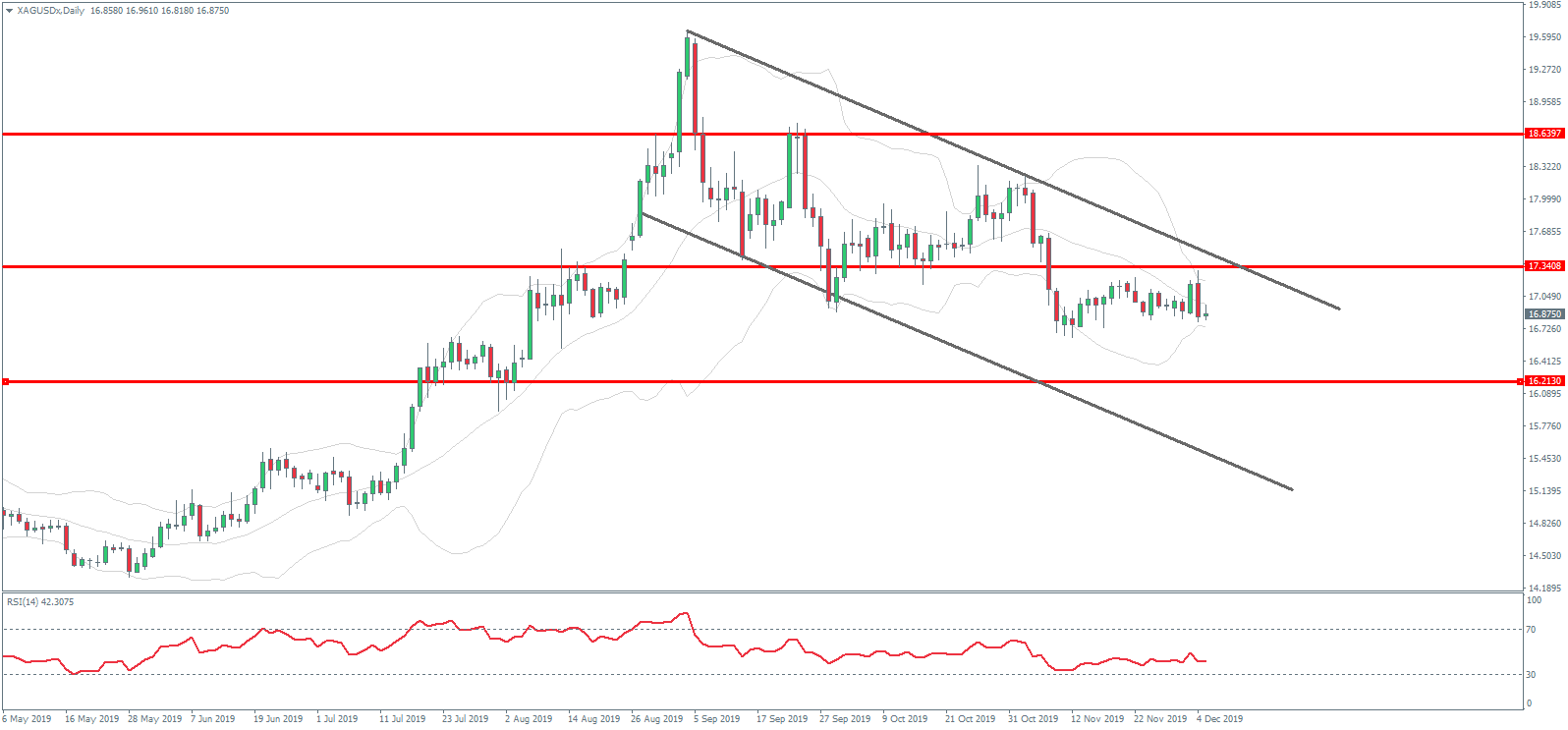

Silver prices are continuing to hold below the key 17.3408 level as the bearish channel develops further. While this channel can still be viewed as a corrective bull flag structure, for now, bulls will need to see price quickly back above the 17.3408 level.

Below 17.3408, the next major support level is down at 16.2130. This also holds the retest of the broken long term bearish trend line. To the topside, the 18.6397 level remains the key marker to break.

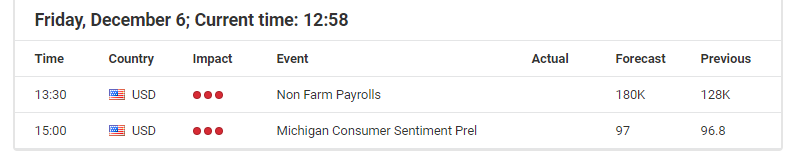

During yesterday’s trading, the EUR/USD quotes went up. Yesterday a positive report was published on the number of initial applications for unemployment benefits in the United States. So, the number of applications decreased to 203K, while experts expected 215K. Currently, the key support and resistance levels are 1.10900 and 1.11200, respectively. Open positions from these marks. We recommend that you pay attention to the US labor market reports.

The Economic News Feed for 06.12.2019:

– Labour Market Report (US) – 15:30 (GMT+2:00);

Indicators point to the strength of buyers: the price has fixed above 50 MA and 100 MA.

The MACD histogram is in the positive zone, but below the signal line, which gives a weak signal to buy EUR/USD.

Stochastic Oscillator is in the neutral zone, the %K line crossed the %D line. There are no signals.

Trading recommendations

Support levels: 1.10900, 1.10650, 1.10300

Resistance levels: 1.11200, 1.11500

If the price consolidates above the resistance level of 1.11200, expect further growth to 1.11500.

Alternatively, the quotes could consolidate below 1.10900 and descend toward 1.10650-1.10500.

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.31032

Open: 1.31622

% chg. over the last day: +0.42

Day’s range: 1.31280 – 1.31600

52 wk range: 1.1959 – 1.3385

During yesterday’s trading, the GBP/USD trading instrument increased slightly. Participants in financial markets expect a choice in the UK parliament on the Brexit issue, due on December 12th. At the moment, the key support level is 1.31000. The key resistance level is 1.30600. We recommend opening positions from these marks.

Today, we do not expect any news from UK.

Indicators indicate bullish sentiment: the price is being traded above 50 MA and 100 MA.

The MACD histogram is in the positive zone, but below the signal line, which gives a weak signal to buy GBP/USD.

The Stochastic Oscillator is in the neutral zone, the %K line crossed the %D line. There are no signals.

Trading recommendations

Support levels: 1.31000, 1.30500, 1.30000

Resistance levels: 1.31600, 1.31800

If the price consolidates above 1.31600, expect further growth toward 1.32000.

Alternatively, the quotes will fix below 1.31000 and descend toward 1.30500-1.30300.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.32003

Open: 1.31781

% chg. over the last day: -0.20

Day’s range: 1.31716 – 1.31732

52 wk range: 1.2727 – 1.3664

During yesterday’s trading, the trading tool USD/CAD slightly decreased. Canada released an optimistic economic reportyesterday, which supported the Canadian dollar. Thus, the Ivey business activity index (PMI) rose to 60.0 in November, although experts predicted a value of 53.8. At present, the local support and resistance levels are 1.31600 and 1.31900, respectively. We recommend paying attention to the dynamics of oil prices. Open positions from key levels.

Today at 15:30 (GMT+2:00) the data on the labor market of Canada will be published.

Indicators point to a bearish sentiment: the price is trading below 50 MA and 100 MA.

The MACD histogram is in the negative zone, but above the signal line, which gives a weak signal to sell USD/CAD.

The Stochastic Oscillator is in the oversold zone, the %K line is below the %D line, which also gives a signal to sell USD/CAD.

Trading recommendations

Support levels: 1.31600, 1.31400

Resistance levels: 1.31900, 1.32300, 1.32700

If the price consolidates below 1.31600, expect further decline toward 1.31400-1.31200.

Alternatively, the quotes could grow toward 1.32300-1.32500.

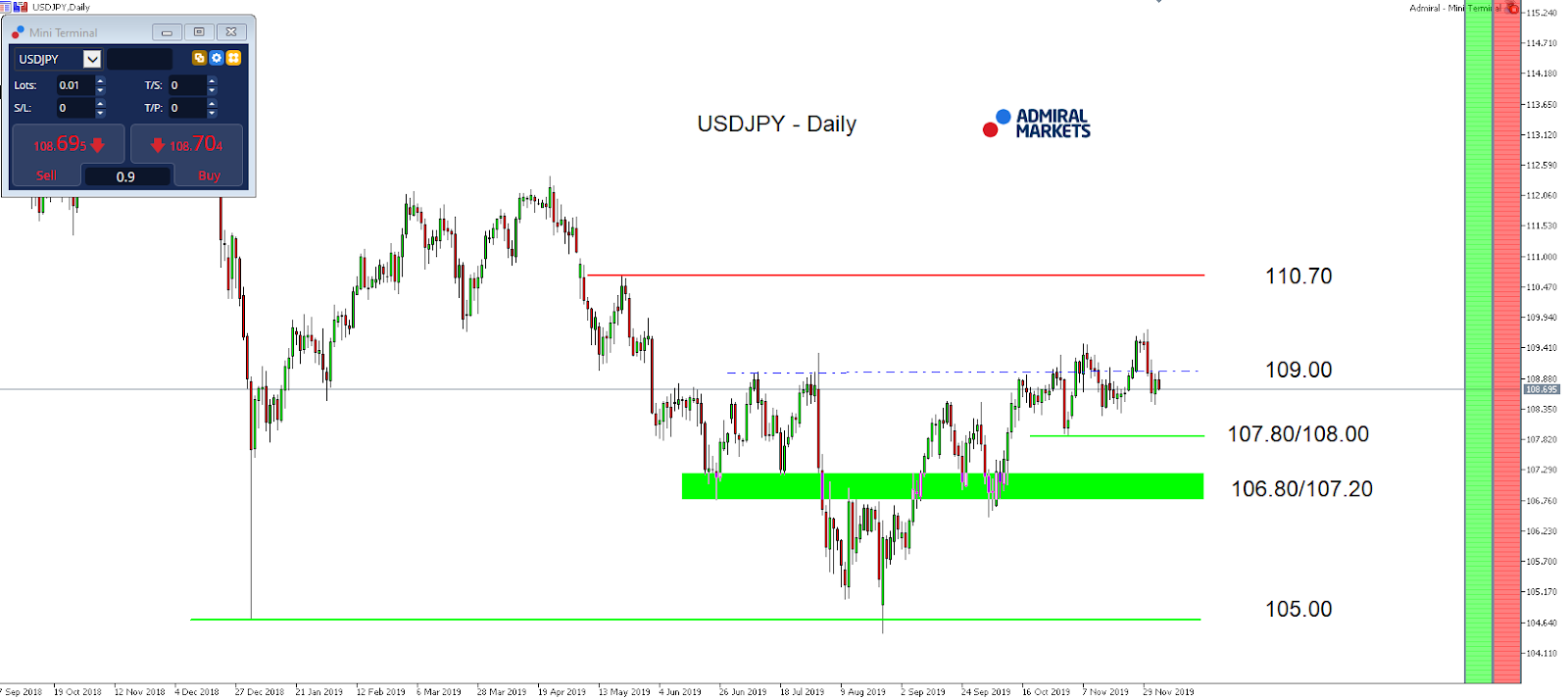

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 108.859

Open: 108.748

% chg. over the last day: -0.12

Day’s range: 108.574 – 108.600

52 wk range: 104.97 – 114.56

The USD/JPY currency pair went down due to the uncertainty surrounding Sino-US trade relations. Investors are interested in buying a safe haven currency. Currently, the key support and resistance levels are 108.500 and 108.800, respectively. Participants in financial markets expect additional drivers. We also recommend that you pay attention to the dynamics of yield on US government bonds. The trading instrument has the potential to further decline. Open positions from key levels.

The Economic News Feed for 06.12.2019 is calm.

Indicators point to the strength of sellers: the price is being traded below 50 MA and 100 MA.

The MACD histogram is in the negative zone, below the signal line, which gives a strong signal to sell USD/JPY.

The Stochastic Oscillator is in the oversold zone, the %K line crosses the %D line. There are no exact signals.

Trading recommendations

Support levels: 108.500, 108.250

Resistance levels: 108.800. 109.100, 109.500

If the price consolidates below the key support level of 108.500, expect the quotes to drop toward 108.250-108.100.

Alternatively, the quotes could grow toward 109.100-109.350.

Saudi Aramco Raises $25.6 Billion in World’s Biggest IPO

Gold steady ahead of US jobs data

Asian markets edged cautiously higher on Friday as investors took heart from President Donald Trump’s latest remarks on US-China trade negotiations.

Trump’s upbeat rhetoric on talks with China, which he said were “moving right along,” offered markets a glimmer of hope over both sides reaching the ‘phase one’ agreement. This comes despite repeated mixed signals on the trade front this week. Nevertheless, market sensitivity to trade headlines is set to intensify ahead of December 15 when the United States is expected to impose 15% tariffs on another $160 billion worth of Chinese goods. Given the lack of clarity on US-China trade developments and overall uncertainty, investors are likely to adopt a wait-and-see approach ahead of the US jobs report, scheduled for release on Friday.

OPEC and allies agree on deeper cuts…what next?

Oil prices spiked to levels not seen in over two months above $59.05 on Thursday. This comes after the Organization of Petroleum Exporting Countries (OPEC) and its allies reached a deal in principle to cut output by an extra 500,000 barrels per day in the first quarter of 2020. However, prices later retraced after OPEC+ failed to offer clarity as it lacked key details of the agreement for deeper production cuts. One important takeaway from the proposal is that Russia will be allowed to exclude its condensate volumes from the terms of production, which could see oil prices trade lower. Another complication in the OPEC deal remains compliance, with some nations frequently pumping above their target levels. Until there is a solution to improve compliance, Oil is positioned to depreciate despite the deeper cuts.

Investors will direct their attention towards the press conference on Friday which should offer key details on the agreement and how the production cuts will be distributed among members.

Saudi Aramco raises biggest IPO Ever

Yesterday saw Saudi Aramco’s initial public offering (IPO) priced at the top of its price range, raising $25.6 billion and making it the biggest IPO in history, surpassing the $25 billion raised by the Chinese online trading group Alibaba in 2014. The mammoth IPO size gives Aramco a market valuation of $1.7 trillion, taking the crown from Apple ($1.17 trillion) as the world’s most valuable publicly traded company.

The Aramco deal will be significant to Gulf capital markets as the IPO is seen as the centrepiece of Crown Prince Mohammed bin Salman’s Vision 2030. Given how revenues from the deal will be used to diversify the Saudi economy away from its dependence on Oil, this encouraging prospect should support capital markets in the region. Optimism over the IPO boosting government finances and supporting economic growth in Saudi Arabia should lift sentiment towards the Saudi economy while increasing appetite for Gulf stocks.

Commodity spotlight – Gold

Gold has appreciated over 1% since the start of the trading week thanks to mixed signals on the US-China trade front and Dollar weakness. Appetite towards the precious metal is set to remain firm until proper clarity and direction are offered on trade developments – Where the metal closes on Friday will be heavily influenced by the pending US jobs report.

Consensus expects US businesses to have created 185,000 jobs in November. This includes an obvious boost in the manufacturing payrolls of 50,000 after the GM striking workers returned to work and are added back into the data. Should the jobs data meet or exceed expectations, Gold will be one of the first casualties as the Dollar appreciates on fading rate cut bets.

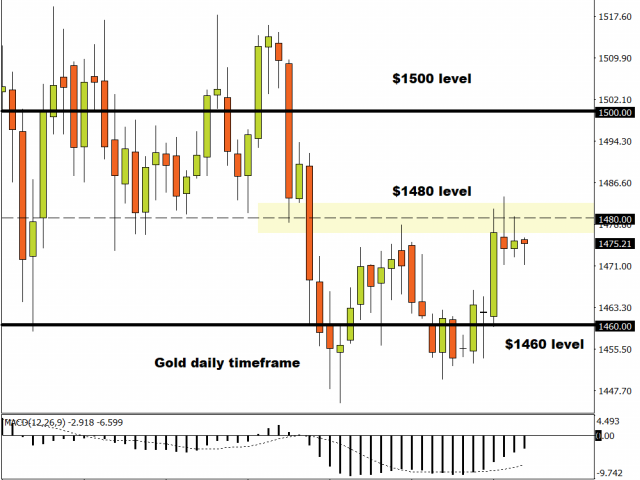

Technical traders will continue watching how prices behave around the pivotal $1480 level. Sustained weakness below here could encourage a move down towards $1460. However, a solid breakout above is seen as opening the doors towards the psychological $1500 level.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

The markets continue to whipsaw ahead of today’s payrolls report. This comes after the private payrolls, as reported by ADP hit a six month low. Private firms added just 67k jobs in November, falling well below estimates. The dollar remains weak, posting declines for five consecutive days. Equity markets were recovering from Tuesday’s sell-off, but sentiment is cautious.

Eurozone Final Services PMI Improves

The final services PMI report for the Eurozone came out better than expected. Services activity, as measured by IHS Markit, saw the index rising to 51.9 for November. This was higher than estimates of 51.5 and a modest increase from October’s 51.5. The increase in the index was driven by higher services activity from Germany and Spain.

EURUSD Rebounds off Support – Will the Momentum Keep Up?

The euro currency fell to the support area of 1.1062 – 1.1075 and promptly recovered. With support established at this level that previously served as resistance, further gains are possible. The next upside target for the EURUSD is at 1.1131. But we do not expect the euro to break past this level for the moment.

Sterling Maintains Gains on Prospects of Johnson Re-election

The pound sterling continued to maintain gains rising to new seven month highs on Thursday. The gains come as traders are pricing in a Tory victory. The UK heads to the polls of December 12th. Re-Election of the incumbent PM Boris Johnson is likely to pave way for an orderly Brexit in January next year.

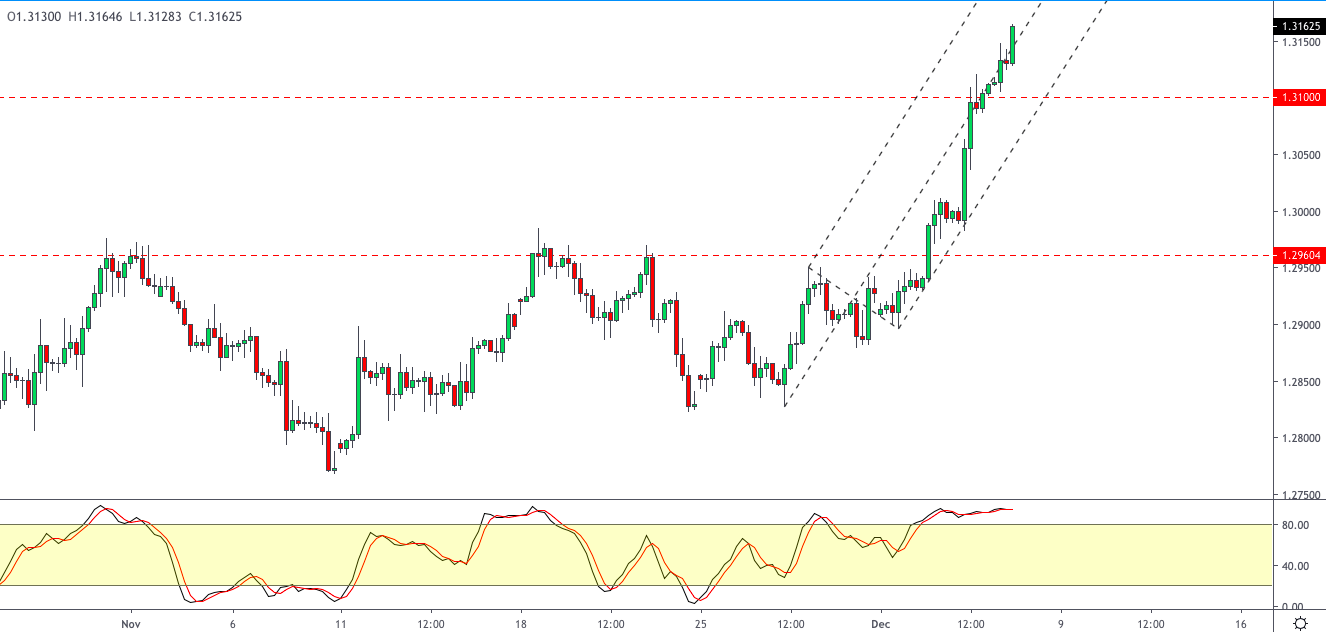

GBPUSD Could Correct Lower

Although the currency pair has been posting strong gains, there is scope for a pullback. This will lead to a short term correction. For the moment, the psychological price level of 1.3100 remains key. If this level fails to hold as support, we anticipate the declines to push the GBPUSD down to 1.2960 which is pending a retest.

Gold Regains Momentum Amid Weak US Data

The precious metal pared losses from Wednesday as investors turn cautious ahead of key economic events. The trade war narrative remains the major catalyst, however. The US is set to raise tariffs on China come December 15th. Therefore, with the markets uncertain about the deal, gold prices are recovering.

XAUUSD on Track to Hit Resistance

The precious metal is seen rising towards the resistance area of 1483. Although this level was previously tested, prices were promptly rejected. We expect to see a firmer test of this resistance area. In the event that XAUUSD breaks out above 1483, then further gains could be seen towards the 1490 region.

As we head towards the weekly close, our focus will be on the Non-Farm Payrolls, and by extension, the yield-sensitive currency pair, the USD/JPY.

After the drop back below 109.00, brought on by Monday’s announcement that US president Trump is to restore tariffs on steel and aluminium shipped from Brazil and Argentina, in addition to his administration proposing tariffs “up to 100%” on certain French goods (about $2.4 billion worth) in retaliation to France’s digital services tax, a risk-off kicked in and 10-year UST yields dropped alongside the USD/JPY.

In addition to that, mixed US data releases over the last days, such as the ADP (usually known as a solid indication of NFP performance) coming in at only 67,000 against an expected 140,000, made it likely for a disappointing NFP reading today, and a drop below 108.00 in the USD/JPY.

If Non-Farm Payrolls print below 150,000, the way that market participants priced the Fed to not move in regards to their interest rate level next week, could result in a sharper shift and bearish catalyst for the USD/JPY.

While we still don’t see the Fed shifting policy even if NFPs disappoint today, but increasingly dovish rhetoric becomes likely, and would drive the USD/JPY lower:

Source: Admiral Markets MT5 with MT5-SE Add-on USD/JPY Daily chart (between September 27, 2018, to December 5, 2019). Accessed: December 5, 2019, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of the USD/JPY increased by 13.7%, in 2015, it increased by 0.5%, in 2016, it fell by 2.8%, in 2017, it fell by 3.6%, in 2018, it fell by 2.7%, meaning that after five years, it was up by 4.1%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

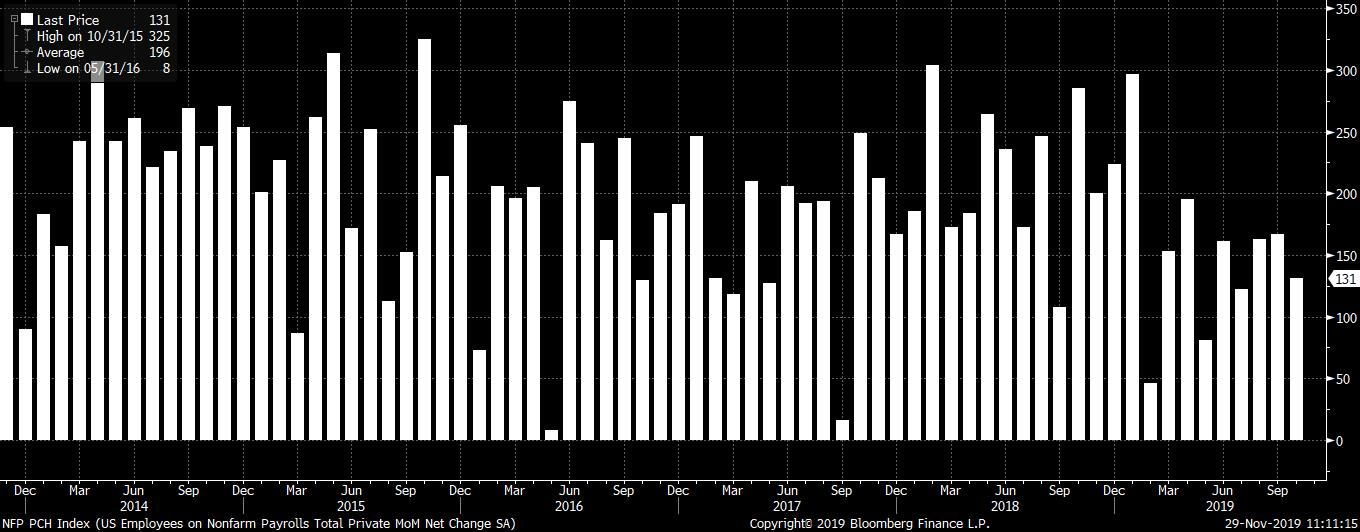

The penultimate payrolls report for the year 2019 is due to come out later today.

The report will be closely watched with economists forecasting that payrolls will rise 183,000 for the month of November. Elsewhere, the unemployment rate is tipped to hold steady at 3.6%. No changes are expected to wage growth which is forecast to rise 3% on the year.

The payrolls report will be key as investors assess the health of the US economy for the fourth quarter. While there was a slowdown in the previous quarter, the Fed rate cuts could see a reversal.

Nonfarm Payrolls – October 2019

The data for October surprised to the upside. Economists view a similar trend taking place in November as well. This comes after the impact of the strike at General Motors ended.

If the economic data comes in line with the estimates, the nonfarm payrolls for November would be the highest since August this year.

From a policy perspective, the November jobs report is likely to give officials enough breathing space. The central bank earlier indicated that it would prefer to wait for the impact of the three rate cuts delivered this year.

Following the higher revised GDP in the second quarter, and the likelihood that payrolls will rise in November, the Fed could be looking into not making any changes to monetary policy when it meets this December.

In October, the payrolls report managed to overcome the strike at GM. The data exceeded the expectations of a 75,000 increase to register 128,000 jobs for the month. However, we expect revisions to bring this figure more in line with reality.

The manufacturing sector which has also been weaker over the past months could start to show a slower pace of job hiring. This was evident from the October report.

Will the Slower Economy Weigh on Jobs?

Investors will be mainly looking for evidence that the slowing economy will have an impact on US jobs. So far, the jobs market has managed to buck the trend. But recent declines in both the manufacturing and services sectors could show otherwise.

The current estimates still prove to be hawkish. This means that if the data comes close to the estimates, then the Fed will have time for its monetary policy changes. Still, many economists believe that a slowdown in jobs is due over the next few months.

The markets are slowly giving rise to expectations that the Federal Reserve will cut rates at the March FOMC meeting next year.

This, of course, depends on how the economic data fares over the period.

The US economy has been holding on to the 2% average growth rate in the previous quarter. We could see similar results in the fourth quarter of the year as well.

Businesses are largely concerned about the uncertainty of the US and China trade wars. Secondly, the economic expansion has been stretching for a while. Therefore, it is not surprising to expect a slowdown in the economic boom cycle.

This will, of course, depend on how the labor market will respond. So far, there is a clear trend of a slowdown in the number of jobs being added. But the unemployment rate remains quite low.

Meanwhile, wage growth is also showing signs of stagnation. On average, the yearly wage growth is around 3%. But this comes as the inflation data remains sluggish, giving more spending power for consumers.

The revisions to the existing arrangement between the two U.S. firms are discussed in a ROTH Capital Partners report.

In a Nov. 21 research note, ROTH Capital Partners analyst Zegbeh Jallah reported that Harpoon Therapeutics Inc. (HARP:NASDAQ) and AbbVie Inc. (ABBV:NYSE) expanded their discovery and collaboration agreement and added to it a new component regarding Harpoon’s HPN217.

“We believe that this is 1) a strong indication of AbbVie’s confidence in the platform, 2) a superb strategic move for Harpoon to remain focused on its solid tumor efforts and 3) an excellent source of additional cash (up to $100 million likely to be received between now and H1/20),” commented Jallah.

The analyst described the changes made to the agreement.

Per the existing discovery and collaboration agreement executed in 2017, AbbVie has the exclusive rights to develop and commercialize Harpoon’s TriTAC technology with the soluble T-cell receptor sequences targeting two agreed upon areas of interest. After the discovery phase, AbbVie alone is responsible for developing, manufacturing and commercializing any products born out of this arrangement with Harpoon.

The recently amended agreement, however, adds four more targets, taking the total to six. With each target there are $310 million in upfront and potential development, regulatory and commercial milestone payments and royalties on global net sales. “We’ve seen several of these agreements in the biospecific space and believe that this is a competitive offer for Harpoon,” Jallah noted.

Also in the agreement is a new component, a licensing and option agreement regarding HPN217, Harpoon’s Tri-TAC that targets the B-cell maturation antigen. The agreement grants AbbVie the worldwide rights to HPN217 for $510 million in upfront, option and milestone payments along with royalties on all sales. AbbVie may exercise the option aspect once Harpoon completes the Phase 1/2 trial of HPN217, slated to start by Q1/20.

“We find it particularly impressive that Harpoon was able to complete the agreement based on preclinical studies for HPN217, at a very competitive transaction value,” Jallah indicated.

ROTH has a Buy rating and a $25 per share 12-month target price on Harpoon, whose stock is currently trading at around $18.19 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Harpoon Therapeutics Inc., Flash Note, November 21, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Harpoon Therapeutics Inc. and as such, buys and sells from customers on a principal basis.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Daniel Carlson of Tailwinds Research initiates coverage on this clinical-stage biotech whose drug candidate works to strengthen the innate immune system.

We are initiating coverage on INmune Bio Inc. (INMB:NASDAQ). According to the company, INmune is “Reprogramming the Innate Immune System for the Treatment of Diseases.” On the surface, this sounds like a fairly standard biotech tagline, but there’s a more here than meets the eye; by dealing with the innate immune system, INmune has the potential to treat multiple diseases with the same therapy. As such, this small company is targeting several large opportunities simultaneously.

INmune targets diseases that have end markets in the tens to hundreds of billions of dollars. To date their clinical data has been solid in all trials. Meanwhile, insiders have funded, and continue to fund, a significant portion of the company’s cash needs. In this report, we will delve into the company, its target markets, its approach to these markets and its products.

The Innate Immune System

It’s a little tough to get your head around the thought that this little $42 million market cap company, INmune, is going after three markets simultaneously, and that those three markets are some of the largest potential markets out there.

“You’ve never seen a company that has cancer, Alzheimer’s and NASH, ever before probably. Why can we do that? Because we’re dealing with inflammation and chronic inflammation plays a critical role in those diseases.” ~ David Moss, CFO

By going after cancer, Alzheimer’s disease (AD) and NASH (Nonalcoholic steatohepatitis), the company is targeting three totally different diseases that have a very common trait in their biologics. However, these are also areas of biotech that are crowded with well-funded competition and many therapies in development. What is INmune doing differently and how can it compete?

To answer this question let’s take a few steps back and look at human biology and the beginning of biotech as an industry. Starting with human biology, there is within each of us an immune system. The immune system is highly complex but can really be broken down into two constituents: the innate system and the adaptive system.

The innate immune system is a front-line defense against disease that gets its name from the fact that we are all born with it already in place, and it changes little throughout our lives. It provides protection by recognizing general features of possible pathogens. Pathogens would be any foreign invader that can cause disease. An example of the innate system is your skin, which blocks entry of many kinds of organisms. Cells of the innate immune system recognize general features of pathogens.

These cells of the innate system do not distinguish within the various classes of pathogens, instead attacking all of them. To use a military analogy, it would be like using the same type of missile to shoot at many different kinds of targets instead of having different missiles for different types of target. Macrophages, for instance, are cells that participate in the innate immune response by finding, eating and killing many different types of bacteria. Natural killer cells (NK cells) are another type of innate immune cell that function to eliminate cells that have become infected with viruses and cancer cells.

The adaptive immune system is more of a rifle shot approach to defending the body against individual pathogens. Unlike the innate immune system, the acquired immune system is highly specific to each particular pathogen. The adaptive system creates immunological memory after an initial response to a specific pathogen and leads to an enhanced response to subsequent encounters with that pathogen.

In a nutshell, the human immune system has its innate side that is a front line against everything bad for the body and its adaptive side that adapts to and targets specific pathogens. These targeted pathogens are diseases that have somehow made it past the innate system. This could be due to a heavy dosage, like a smoker developing lung cancer due to years of overwhelming his system, or it could be due to dysfunction of the innate system.

Since the beginning of the biotechnology industry, scientists have known about both sides of the immune system. This is still a young industry, however, and researchers have been strictly focused on the adaptive side of the immune system due to early success there. When you look at the biggest and most successful biotech companies to date, they are all focused on the adaptive immune system. Checkpoint inhibitors or T-cell therapies, for example, are therapies targeting adaptive immune defenses.

Thus, by definition, these firms and their research dollars have been a rifle shot after individual pathogens or diseases. As an example, CAR-T therapy has been very successful in targeting specific types of cancer by working on T-Cells, a part of the adaptive system. This has worked well as companies focus on taking care of one disease at a time with their drug programs.

It’s interesting to note that not all mammals have both sides of the immune system found in humans. Most only have an innate system, not the adaptive side. Yet, many animals with only an innate system don’t get diseases such as cancer. Researchers who have been focused on the adaptive system have really ignored an equally important defense in the innate system.

INmune is pursuing a radically different approach from the majority of other biotechs. As we mentioned earlier, the innate side of the immune system is like a missile that can work on any kind of target. INMB is focused on “reprogramming the innate immune system.” By working on the side of the immune system that can deal with any kind of pathogen, INmune has the potential to be working on products that span many different classes of disease. It is through this approach that INmune can afford to have a cancer, Alzheimer’s and NASH study all going on at the same time. It’s a different approach than most are taking and, as a result, is has the potential for broad-reaching success.

The Products

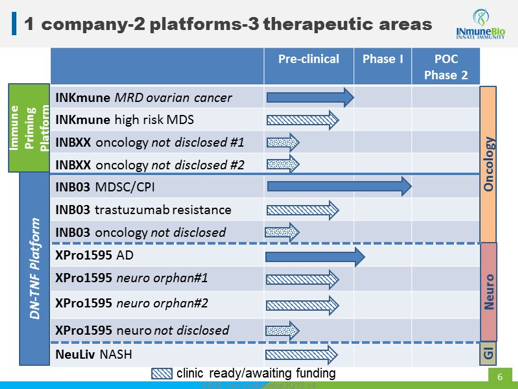

INmune has four programs in its business plan. These target three different therapeutic areas and come from two platforms the company is developing. Here’s the product roadmap from their recent presentation at the HC Wainwright Conference (btw, the webcast is a great resource).

It’s a large bite to swallow, targeting GI, neuro and oncology at the same time. However, here’s what Dr. R.J. Tesi, the company’s CEO, calls its “dirty little secret”; INB03, XPro1595 and NeuLiv, which is its “DN-TNF Platform,” are all the same product, just being tested in different indications. When the innate immune system becomes dysfunctional, reprogramming it can lead to benefits in many of the areas where it’s effective. Which means that a therapy targeting the innate immune system can be effective across a broad swath of pathogens and, thus, many target indications.

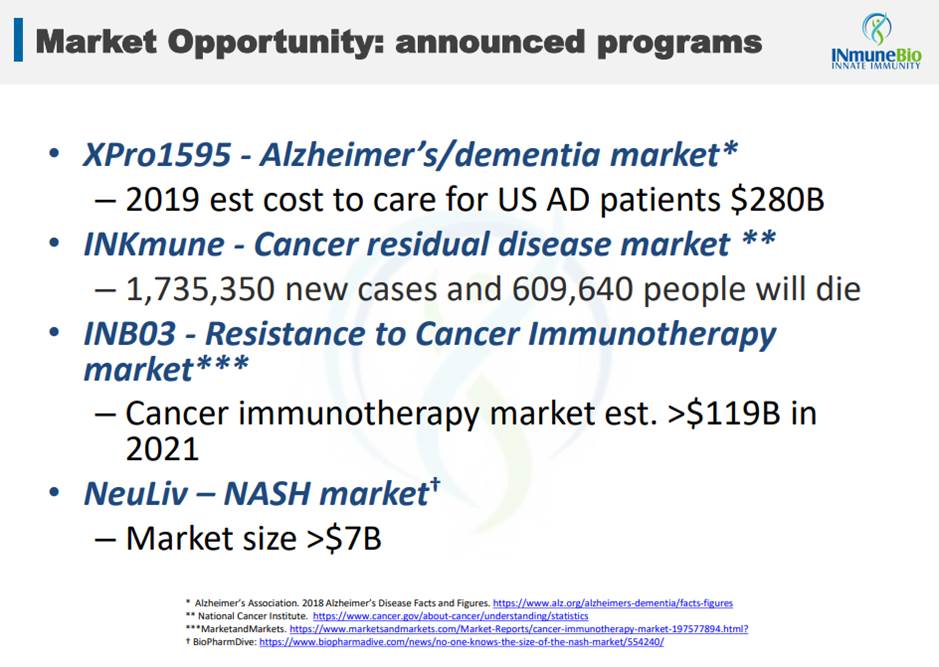

Looking at these diseases, the market opportunity being addressed by both platforms is massive.

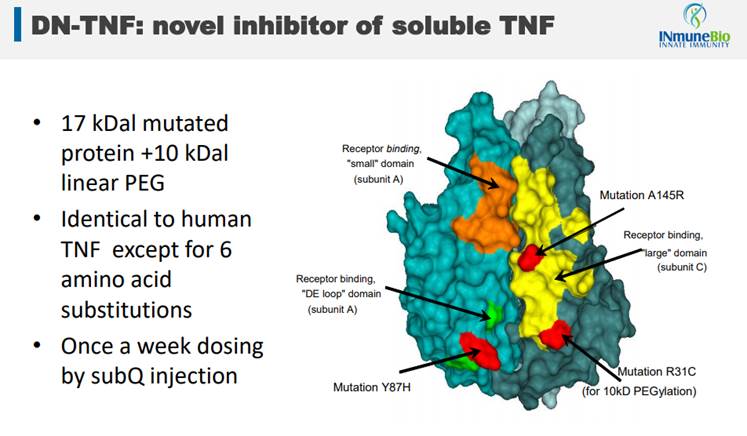

Success in any one of these areas would obviously lead to a great outcome for investors. But, what gives INmune any confidence that success is going to be achieved, particularly across these three indications with one DN-TNF therapy targeting them? It’s the method of action that the drug brings to the patients. Its drug is an off-the-shelf version of a novel TNF inhibitor, a depiction of which is below.

It’s the three red dots on the image above that differentiates INmune’s drug from soluble TNF found in humans and from TNF inhibitors (blockbuster drugs like Humira, Enbrel and Remicade) that have been around for a while and are very popular drugs. TNF inhibitors are drugs that help stop inflammation. They’re used to treat diseases like rheumatoid arthritis (RA), juvenile arthritis, psoriatic arthritis, plaque psoriasis, ankylosing spondylitis, ulcerative colitis (UC) and Crohn’s disease.

Inflammation plays a role in cancer and other diseases. However, because of the side effects of the existing TNF inhibitors suppressing a patients’ immune system, they can’t be used. INmune believes that with its targeted DN-TNF inhibitor, which is designed to remove the side effects of the existing TNF drugs, they can greatly expand the market opportunity while reducing the number of patients suffering side effects from the treatment. Thus, they can go after markets like cancer and neuro where the existing TNF players can’t.

And, that’s just in cancer patients. Alzheimer’s has been directly linked to inflammation as is NASH. A targeted therapy that blocks the “bad” TNF has possibilities across many diseases. The innate immune system hasn’t been working in these patients and this therapy has the potential to re-energize it.

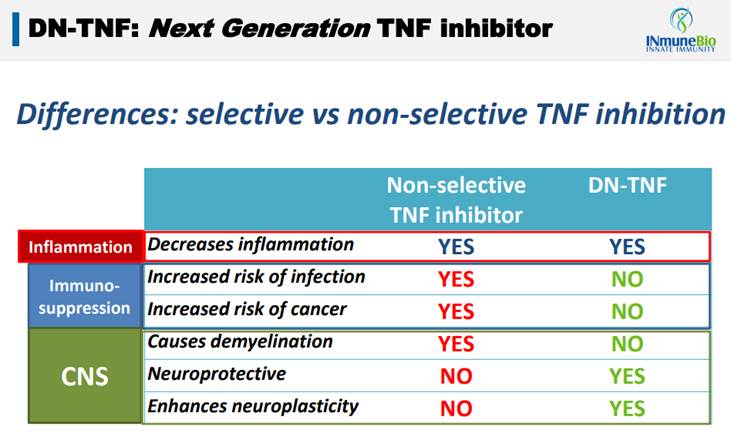

The problem with other TNF inhibitors, and this is a very large class of drugs, is that they are non-selective. There are two kinds of TNF found in humans, Soluble TNF and Trans-Membrane TNF, and the existing class of drugs attacks both of these. This is why they are good at stopping inflammation (blocking Soluble TNF stops inflammation) but carry with them a plethora of side effects. Because, by blocking Trans-Membrane TNF, patients have increased risk of diseases like cancer, infections and CNS disease.

INmune’s drug is not a front-line therapy per se. But it does do a better job of treating inflammation caused by Soluble TNF while allowing the important Trans-Membrane TNF to do its job. In this way INmune’s first platform has the potential to be an important adjunct therapy in many diseases that have inflammation as an associated problem with curing them, which is how it has multiple treatments undergoing clinical testing.

INKmune, the other therapeutic platform under development, works with NK cells in the innate immune system. Before the adaptive systems is even aware of a threat to our body, the Innate immunity is acting as our first line of defense against infection and cancer. Around 10% of the lymphocytes in our peripheral bloodstream are part of the innate response, and 95% of those are natural killer (NK) cells. Each of these innate killer cells can recognize, target and kill harmful cells through recognition of proteins and glycoproteins, which are expressed on “stressed” cells, such as tumor and virally infected cells.

Why is innate immunotherapy likely to improve outcomes? Cancer cells are constantly arising in our bodies as a consequence of random genetic mutations, some of which give a cell a survival or proliferation advantage. These random changes are mostly novel and have never been presented to the adaptive immune system. The only cells able to detect the “stress” signals of a tumor cell that is dividing too frequently are NK cells, which can eliminate tumor cells before they become a clinically detectable cancer.

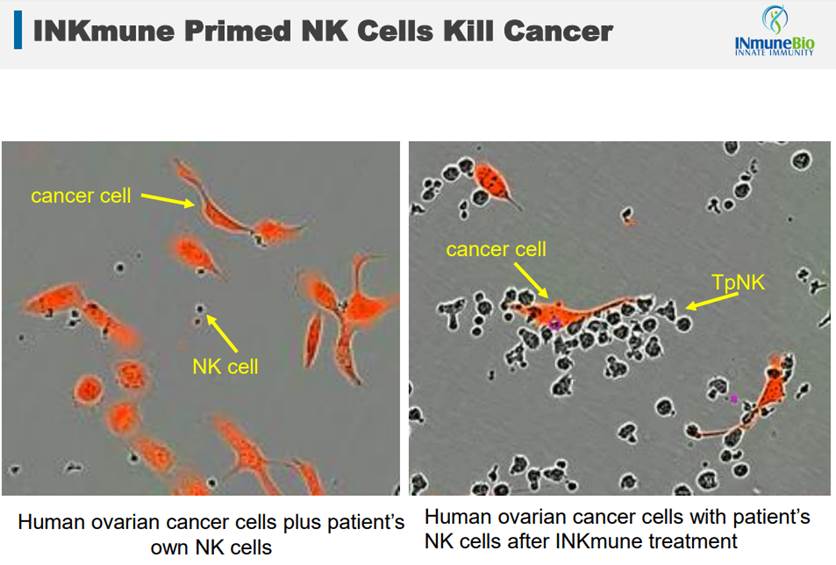

However, eventually cancer cells get smart and they evade NK cell killing. By reprogramming signals on the cancer cells surface they are able to avoid NK cell detection. INKmune provides these missing signals to the patient’s own natural killer cells to help them target tumors, unlike how CAR-T works on T-Cells but without having to individualize treatment and that associated expense.

As this slide from their presentation shows, INKmune primed cells recognize cancer and overwhelm it. By altering the NK cells, INKmune (TpNK) turns them into cancer killers.

Similar to the other platform, INKmune is likely to be a combination therapy. The best use case will be found in cancer victims who have a high likelihood of recurrence. This is a frequent case in situations like breast cancer, where many survivors get another form of cancer after several years. In these situations, taking INKmune as an ongoing therapy could be a possible preventative measure against a return of cancer.

Success to Date and Plans for Future Trials

So far we’ve discussed the immune system, what the innate immune system is and why INmune is pursuing a strategy of focusing here, and the two platforms that the company is developing. Now let’s turn our attention to the progress that has been made by INmune as this is where the story starts to get very exciting.

There are very few, if any, biotech companies in phase 1 clinical trials that have over 70 published reports on their technology. The large number of research institutions that have done work with either of these platforms is testament to the possibilities of the underlying science. More importantly, the fact that early stage testing has been consistent and positive across both product lines is highly encouraging.

Focusing on the DN-TNF product line, containing XPro1595, INB03 and Neuliv, there have been over 60 research papers published. A complete list of them is available on INmune’s website.

INB03, INmune’s cancer drug, has completed a phase 1 trial, the interim results of which were released in August. Final results from this trial are expected to be released in the first half of December. Here’s what the company had to say about the interim results

“No drug-related serious adverse events have been reported, and INB03 was well tolerated The inflammatory cytokine IL6, a biomarker of soluble TNF function, decreased by more than 50% in half of the patients, suggesting a pharmacodynamic effect of INB03.”

Based on these statements it stands to reason that the final results will be positive. In addition, the company is already working on its phase 2 trial design, which should also be released soon, further suggesting positive results are coming.

Furthermore, based on prior history of other TNF inhibitors, it stands to reason that the drug will be successful. This product is also a TNF inhibitor, albeit different from the others in the market. TNF inhibitors are one of the leading classes of drugs (on sales dollars) sold in the world and their effectiveness is well understood. The fact that, in its phase 1 safety trial, INmune saw suggestions of a pharmacodynamic effect says that the product is simply working as one would expect it to.

Meanwhile XPro1595 has also demonstrated effectiveness in animal studies and is in the middle of a phase 1a trial at this time, with a phase 1b having started this week with the first patient being injected. With recent data showing correlation between Alzheimer’s disease and inflammation, it stands to reason that XPro1595 could be effective here. Remember, XPro1595 and INB03 are the same drug, just going through trials for different diseases. If those diseases share a root problem of inflammation and one drug works on inflammation, the other should as well; the positive pharmacodynamic effect of INB03 bodes extremely well for its partner drugs.

Finally, the other platform drug, INKmune, has also received a fair amount of research attention, with similar positive results. INmune expects to launch the phase 1 trial of INKmune shortly.

Insider Support and Strong Balance Sheet

Having had nothing but consistently positive results, INmune appears to be a path toward clinical success and, hopefully, eventual success in treating sick patients with FDA approved products. But, it’s early stage and there’s more to a company than simply clinical success, a lesson I’ve learned the hard way in some recent investments.

Beyond the clinic, the quality of the management and having deep pocketed investors willing to back a company through their cash-burning early stages is equally important to the success of a company. Without access to funds from investors who are fundamental in nature and willing to fund a company in a clean transaction at a decent valuation, a stock can suffer tremendously. This can happen even in the face of strong data.

INmune is a company that has done all the right things in its public market strategy, in my opinion. The balance sheet is pristine. The company has been funded through straight equity with zero debt or converts in place.

More exciting is the fact that insiders have put a lot of capital into this company. After INmune went public at $8 per share the insiders, including management and the board, put an additional $5 million into the company’s coffers. At $9 per share! And, they have been adding to their holdings in the open market more recently, as the stock has trended lower.

By the way, potential investors might want to check out the bios of management and the board. This is a seasoned team with a track record of success. They also have the financial wherewithal to continue funding the company if necessary.

I stated earlier that the interim results bode well for success in the ongoing trials. However, remember that these early trials are not double-blind; the data is open to the company all along. Thus, insider buying, like we’ve been seeing, could be an even bigger indicator as to how things are progressing.

The Bottom Line

Investing in biotech is not without risks. These risks, generally speaking, relate to the clinical success of a company and its ability to fund the business. As companies progress to later stage, both of these risks diminish to some degree and the share price rallies. Before this happens, however, early-stage biotech stocks can languish. This creates opportunity for those investors who are willing to take the risk of investing in an early stage company.

INmune is, potentially, one of those rare opportunities where the market is pricing in risk that may not exist to the degree the market seems to think exists. The clinical data to date for INmune has been very strong. These trial results have been consistent across more than 60 published papers. Yes, there is clinical risk here, but it certainly seems that the plethora of data out there suggests the products stand a better than average chance of success.

Meanwhile, the company will indeed require more funding, but this may not be as substantial an overhang as is typical in micro-cap biotechs. The funding required is not in the hundreds of millions, rather in the $15 million or so amount. Insiders have deep pockets and don’t look forward to dilution at levels well below where they just invested $5 million. It’s very conceivable that funding risk will be removed by insider participation once again.

I see INMB as a potential platform company that can, through its dealing with the innate immune system, develop products that work alongside existing therapies across many diseases. The areas of treatment are huge, the products have great results to date and insiders are strong and committed to this company. INmune has all the hallmarks of possibly being that one in a million micro-cap biotech and Tailwinds is excited to be covering the stock and following its progress.

Daniel Carlson is the founder and managing member of Tailwinds Research Group and its parent company DFC Advisory Services, which is a licensed registered investment advisor (CRD # 297209). Tailwinds is a microcap focused research company that provides research on and consults to over 20 emerging growth companies in the technology and life sciences arenas. DFC Advisory Services is an RIA that manages money dedicated to investing in the companies covered by Tailwinds. For more information on these two companies and their track record, please see www.tailwindsresearch.com. Prior to founding these two entities, Dan spent many years working with small public companies, having been CFO of two public companies and helping finance many others. A 1989 graduate from Tufts University with a degree in Economics, Dans formative years in business were spent as an equity trader, first on the Pacific Coast Stock Exchange then on the buyside at several multi-billion dollar firms.

This article was submitted by Tailwinds Research. For more information on Tailwinds Research or on INmune Bio, please visit www.tailwindsresearch.com.

Tailwinds owns stock in INmune Bio. For a complete list of disclaimers and disclosures, please click here.

Disclosure: 1) Daniel Carlson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: INmune Bio. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: INmune Bio. Additional disclosures and disclaimers are above. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Newark, Calif.-based Protagonist Therapeutics’ shares traded 70% higher today after the firm reported preliminary Phase 2 results for Hepcidin Mimetic PTG-300 in the treatment of transfusion dependent beta-thalassemia.

Clinical-stage biopharmaceutical company Protagonist Therapeutics Inc. (PTGX:NASDAQ)announced preliminary results from the company’s ongoing Phase 2 TRANSCEND study of PTG-300 in patients with transfusion-dependent beta-thalassemia. The firm noted that in the trial, dose-related drug exposure and significant reductions from baseline serum iron and transferrin saturation levels were observed providing the first evidence of pharmacodynamic effects in patients.

Protagonist’s Chief Medical Officer Samuel Saks, M.D., commented, “The dose-related pharmacodynamic responses in serum iron and TSAT levels observed in this preliminary analysis provide the first evidence of the effects of PTG-300 in patients with beta-thalassemia, who have highly elevated levels of iron in the body…These early results suggest the potential of finding an appropriate dose of PTG-300 for continued development in the treatment of beta-thalassemia…We look forward to the results from further study with additional dose regimens and longer follow-up, with clinical efficacy results expected in 2020.”

Ashutosh Lal, M.D., program director of the Comprehensive Thalassemia Center at the UCSF Benioff Children’s Hospital, Oakland, and PTG-300 beta-thalassemia study investigator, remarked, “Treatment options for patients with beta-thalassemia are limited and the complications associated with transfusion are serious…The TRANSCEND trial is examining whether constraining iron availability improves endogenous hemoglobin synthesis in patients with beta-thalassemia, an endpoint for which there exists considerable preclinical evidence. These results demonstrating the pharmacodynamic activity of PTG-300 in reducing TSAT, though preliminary, warrant continued evaluation of PTG-300 for the potential treatment of beta-thalassemia.”

The company’s President and CEO Dinesh V. Patel, Ph.D., added “The consistent and significant effect on iron levels observed in normal healthy volunteers in a previous study, and now in patients with beta-thalassemia, provides strong rationale for potential utility of PTG-300 in blood disorders directly dependent on disruption of normal iron homeostasis in the body…We are encouraged by these findings and are continuing with our original plans of conducting clinical proof-of-concept studies with PTG-300 in different blood disorders such as beta-thalassemia, polycythemia vera, hereditary hemochromatosis, and an investigator sponsored study in myelodysplastic syndromes. We are well financed to conduct these studies and our corporate objective is to make data-driven decisions in 2020, with the intent of choosing our first clinical indication for a potential pivotal study to begin in 2021.”

The firm indicated that PTG-300 was well-tolerated in the study and systemic and non dose-related adverse events were only mild to moderate in severity and typical for patients with TD beta-thalassemia.

The company explains in the release that “PTG-300 is an injectable hepcidin mimetic in clinical development for the potential treatment of beta thalassemia and polycythemia vera. Hepcidin is a natural peptide hormone that is a critical regulator governing iron absorption, recycling and utilization by the body…PTG-300 has been granted Orphan Drug designation in the U.S. and EU and has received Fast Track designation by the FDA for development in the treatment of beta-thalassemia.”

Protagonist Therapeutics, headquartered in Newark, Calif., describes its business as “a clinical stage biopharmaceutical company that utilizes a proprietary technology platform to discover and develop novel peptide-based drugs to transform existing treatment paradigms for patients with significant unmet medical needs.” The company’s drug candidate pipeline includes PTG-300 used in the treatment of iron overload anemia and related rare blood diseases including beta-thalassemia and polycythemia vera; PTG-200, which is currently in Phase 2 clinical development for the potential treatment of inflammatory bowel disease, with Crohn’s disease as the initial indication; and PN-943, which is in clinical development for the potential treatment of inflammatory bowel disease, with a Phase 2 ulcerative colitis study expected to commence in Q2/20.

Protagonist Therapeutics has a market capitalization of about $127.6 million with around 27.2 million shares outstanding and a short interest of approximately 3.74%. PTGX shares opened higher today at $5.50 (+$0.81, +17.27%) over yesterday’s closing price of $4.69. The stock has traded today between $5.40 and $8.51/share and at present is trading at $8.06 (+$3.37, +71.43%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

By CentralBankNews.info Botswana’s central bank left its Bank Rate steady at 4.75 percent and reiterated its forecast from October that inflation should remain below the lower bound of its target range in the near term but then bounce back to within its target range of 3-6 percent in the second quarter of 2020. The Bank of Botswana (BOB), which cut its rate by 25 basis points in August after keeping rates unchanged for two years, noted inflation decelerated to 2.4 percent in October from 3.0 percent in September and is expected to remain below 3 percent for a few more months due to the comparison with an increase in domestic fuel prices in the fourth quarter of last year. “Subdued domestic demand pressures and the modest increase in foreign prices contribute to the positive inflation outlook in the medium term,” BOB said. Upside risks to this forecast stem from a potential rise in administered prices and government levies or taxes beyond the current forecast while downside risks stem from lower growth in the global economy along with productivity improvements and technological process. Botswana’s economy has slowed this year due to a weak diamond market, severe drought and slower growth in neighboring countries but is expected to bounce back next year as the diamond market normalizes and copper production comes on stream. In the second quarter annual economic growth slowed to 3.1 percent from 4.3 percent in the first quarter, with mining output up by only 1.4 percent in the year to June compared with an increase of 5.6 percent in the same 2018 period mainly due to a planned maintenance shutdown of the Orapa Mine in April. Weak output from the diamond industries also affected Botswana’s non-mining output, which slowed to growth of 4.2 percent in the 12 month to June compared with 4.8 percent growth in the same period as the trade, hotels and restaurant sectors saw slower growth. BOB said the government had lowered its forecast for economic growth this year to 3.6 percent from an earlier 4.3 percent, and to 4.4 percent for 2020 from 4.6 percent. Last week the International Monetary Fund forecast Botswana’s economy would grow around 3.5 percent this year and 4.2 percent in 2020, with growth hovering around 4 percent thereafter, a rate it said was too low to achieve the country’s development objectives and create enough jobs to absorb new entrants to the labour market.

The Bank of Botswana issued the following press release:

“At the meeting held on December 5, 2019, the Monetary Policy Committee (MPC) of the Bank of Botswana decided to maintain the Bank Rate at 4.75 percent. Inflation fell from 3 percent in September to 2.4 percent in October 2019, breaching the lower bound of the Bank’s objective range of 3 – 6 percent. Inflation is forecast to remain below the bottom end of the objective range in the near term, but should revert to within the objective range in the second quarter of 2020 and into the medium term. Subdued domestic demand pressures and the modest increase in foreign prices contribute to the positive inflation outlook in the medium term. This outlook is subject to upside risks emanating from the potential rise in administered prices and government levies and/or taxes, beyond current forecasts. However, lower growth in global economic activity, technological progress and productivity improvement present downside risks to the outlook. Real Gross Domestic Product (GDP) grew by 3.9 percent in the twelve months to June 2019, compared to a faster expansion of 4.9 percent in the corresponding period in 2018. The lower increase in output is mainly attributable to a deceleration in growth of the mining sector. Growth in non-mining GDP also slowed in the review period. Mining output grew by 1.4 percent in the year to June 2019, compared to an increase of 5.6 percent in the corresponding period in 2018. The lower increase is, in the main, due to the significant reduction in growth of diamond output from 11.8 percent to 1 percent in the review period, attributable to the decline in production by Orapa Mine, following a planned plant shutdown in April 2019. Non-mining GDP grew by 4.2 percent in the twelve months to June 2019, compared to 4.8 percent in the corresponding period ending in June 2018. The lower expansion in non-mining GDP was largely due to slower growth of the trade, hotels and restaurants sector, mainly reflecting weak performance in the downstream diamond industries.

Projections by Government indicate that domestic economic activity will expand by 3.6 percent and 4.4 percent in 2019 and 2020, respectively. The projections have been revised downwards by 0.7 and 0.2 percentage points for the two respective years. The weaker performance is mainly attributable to the expected decline in the rate of growth of the mining sector due to lower diamond production. However, it is anticipated that the increase in government spending, as well as ongoing structural reforms, such as improving the ease of doing business and concerted efforts channelled towards the transformation of the economy, should also be supportive of economic activity. Overall, the economy is projected to operate close to, but below full capacity in the short to medium term, thus not adding to inflationary pressures going forward. Global output growth is projected to ease to 3 percent in 2019, the lowest since the global financial crisis of 2008-09, down from 3.6 percent in 2018. The slowdown is due to, among other factors, broad-based deceleration in growth of industrial output and trade, as well as low business confidence and weaker investment amid trade and geopolitical tensions. Furthermore, global economic performance is undermined by lack of traction of structural reforms in the advanced economies and China, while country idiosyncratic factors weigh down on growth in some emerging market economies. Overall, global output is expected to expand modestly by 3.4 percent in 2020. The projected recovery, mainly driven by emerging markets and developing economies, remains precarious with elevated downside risks in an environment of policy uncertainty and sustained negative impact of trade and geopolitical tensions on business confidence, investment and growth. Regionally, economic activity in South Africa remains subdued and the South African Reserve Bank projects GDP growth rates of 0.5 percent and 1.4 percent in 2019 and 2020, respectively, a 0.1 percentage points downward revision for both years. The current state of the economy and the outlook for both domestic and external economic activity suggest that the prevailing monetary policy stance is consistent with inflation being within the objective range of 3 – 6 percent in the medium term. Consequently, the MPC decided to maintain the Bank Rate at 4.75 percent.

The next full update of the Bank’s outlook for the domestic economy and inflation will be published on February 25, 2020 in the Monetary Policy Statement. MPC meetings for 2020 are scheduled as follows: February 26, 2020 April 30, 2020 June 18, 2020 August 20, 2020 October 8, 2020 December 3, 2020″ www.CentralBankNews.info