By Hussein Sayed, Chief Market Strategist (Gulf & MENA), ForexTime

US indices near record highs after Trump’s impeachment

Sterling slumps more than 400 pips from 19-month post-election high

Bank of England to remain cautious at today’s meeting

The S&P 500 snapped a five-day winning streak to close slightly lower on Wednesday. Despite the slight retreat, investors still seem in a risk-on mode with all US major indices trading near record highs. Markets have largely shrugged off President Trump’s impeachment on Wednesday night as investors remain confident that the Republican-controlled Senate will vote against removing Mr. Trump from office. Instead, it’s the positive signs from the announced trade agreement that continue to dominate market direction.

With the holiday period to come, the S&P 500 is up 27.3% year-to-date and the tech heavyweight Nasdaq has surged 33.1% in what has been an exceptional year for investors and one that will be difficult to beat in the upcoming decade.

Sterling sheds all post-election gains

After climbing to a 19-month high of 1.3514, the Pound has lost more than four big figures in the past three trading days. The steep selloff has been driven by concerns that the UK may leave the European Union at the end of 2020 without a trade agreement in place. Prime Minister Boris Johnson is expected to publish legislation this week that will prohibit an extension of the transition period beyond December 2020. This means a no-deal Brexit remains on the table and that will prevent the Pound from testing new highs in the short term.

The Bank of England meets today and despite a major hurdle being cleared in the wake of the market friendly Conservative’s victory, the Bank is likely to remain cautious. Markets are anticipating a slightly more hawkish tone, but given that a hard Brexit remains a possible scenario, business investment and hiring are likely to remain muted in the first half 2020. Hence, the Bank is likely to keep its options open, including a rate cut if data deteriorates further. Expect this meeting to have little influence on the Pound as Brexit will continue to dominate the currency’s direction.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

On Wednesday the 18th of December, the euro finished down at the close of trading. At the end of the day, the EURUSD pair had fallen by 36 points (4 digits). This “southerly movement” was far from a smooth process, although, bears were able to bring the value down to 1.1111. The previous low of 1.1102, which was hit on December 13 is yet to be surpassed, and the technical picture remains bearish – let’s take a closer look at all the details.

Day’s events (GMT+3):

12:30 UK: Retail Sales (MoM) (Nov).

15:00 UK: BoE Interest Rate Decision.

16:30 USA: Philadelphia Fed Manufacturing Survey (Dec), Initial Jobless Claims 4-week average (Dec 13).

18:00 USA: Existing Home Sales (MoM) (Nov), Existing Home Sales Change (MoM) (Nov).

Current situation:

The price had fallen by the end of the day, but did not reach the calculated target of 1.1090/95. Growth stopped near the low which was set on December 13, when the euro price rose to 1.1199.

In the Asian markets, bulls’ activity resulted in the price moving back towards the trendline, which acted as yesterday’s support. Bears were slow off the mark, and news out of Australia temporarily changed the mood of market players. The catalyst for the strengthening of AUD and other currencies was the publication of favourable data concerning employment figures – the country’s unemployment rate fell from 5.3% to 5.2% in November.

The target is 1.1093/95 (1.1093 – 90th degree from 1.1199, 1.1195 – 67th degree from 1.1175). If you look at the downward channel, the target is lower at 1.1082. We believe that there is still further downward movement ahead. After the breakout at 1.1120, we expect increased pressure on the single currency. The target of 1.1195 is more than valid, so there is no real need to make any forecast.

A surge in volatility is expected at 12:30 (Moscow time), after the Bank of England’s announcement regarding its decision on setting the latest interest rate. Sharp fluctuations in the pound will affect the EURGBP cross currency if it is voted upon to reduce or maintain the current rate. If, at the same time, dollar trading is “calm”, then we can expect to see the EURUSD pair also affected.

Now a few words about yesterday’s debate on the impeachment of Trump. On Thursday, the US House of Representatives voted to impeach President Donald Trump on two counts: “abuse of power” and “obstruction of Congress.” The debate before the vote in the House of Representatives lasted more than six hours. However, this does not mean that Trump has to leave his post, for that to happen, the Senate must vote on the matter, after he has faced trial before them.

The Republicans currently hold a majority in the US Senate, therefore, it is highly unlikely that a guilty verdict will be returned and the President impeached. Trump is ready for the next stage of the proceedings and is very confident that he will retain office. As you saw, the markets were very calm in reaction to the decision of the US House of Representatives.

The Bank of Japan (BOJ) left its ultra-easy monetary policy steady, including the negative interest rate of minus 0.1 percent on banks’ excess reserves, and confirmed its guidance that it would continue with quantitative and qualitative monetary easing with yield curve control as long as necessary to reach and maintain its target for inflation to reach 2 percent.

BOJ also confirmed its guidance from October that it would not hesitate to take additional easing measures if the momentum toward achieving its price stability target were lost due to if there were significant downside risks to economic activity and prices, mainly from overseas economies.

Looking ahead, BOJ also maintained its view Japan’s economy will continue on a “moderate expanding trend, as the impact of the slowdown in overseas economies on domestic demand is expected to be limited, although the economy is likely to continue to be affected by the slowdown for the time being.”

Although Japan’s exports are likely to remain weak for some time, BOJ still sees them on a “moderate increasing trend on the back of overseas economies growing moderately on the whole.”

BOJ’s statement underscores the general view that further monetary easing by major central banks is on hold for now, with the BOJ also noting domestic demand will be supported by the government’s 13.2 trillion yen fiscal package that was approved by the cabinet this month.

BOJ has used a combination of negative interest rates and “yield curve control” in which its uses asset purchases to keep the yield on government bonds around zero percent, since September 2016.

Japan’s headline inflation rate was steady at 0.2 percent in October and September while the economy has been picking up speed in recent quarters with gross domestic product growing 1.7 percent year-on-year in the third quarter, up from 0.9 percent in the second and 0.8 percent in the first quarter.

In its latest economic outlook from Oct. 31, BOJ lowered its forecast for growth in fiscal 2019, which began April 1, to 0.6 percent from July’s forecast of 0.7 percent, the 2020 forecast to 0.7 percent from 0.9 percent, and the 2021 forecast to 1.0 percent from 1.1 percent.

BOJ also lowered its outlook for inflation, both for consumer prices excluding fresh food, and for inflation excluding the effects of the consumption tax hike.

CPI, less fresh food, is seen rising 0.7 percent in fiscal 2019, down from 1.0 percent. In fiscal 2020 inflation is seen at 1.1 percent, down from 1.3 percent, and in fiscal 2021 inflation is seen at 1.5 percent as compared with July’s forecast of 1.6 percent.

The Bank of Japan issued the following press release:

1.

At the Monetary Policy Meeting (MPM) held today, the Policy Board of the Bank of Japan decided upon the following.

(1) Yield curve control The Bank decided, by a 7-2 majority vote, to set the following guideline for market [Note 1] The short-term policy interest rate: The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank. The long-term interest rate: The Bank will purchase Japanese government bonds (JGBs) so that 10-year JGB yields will remain at around zero percent. While doing so, the yields may move upward and downward to some extent mainly depending on developments in economic activity 1

(2) Guidelines for asset purchases With regard to asset purchases other than JGB purchases, the Bank decided, by a unanimous vote, to set the following guidelines.

a) The Bank will purchase exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at annual paces of about 6 trillion yen and about 90 billion yen, respectively. With a view to lowering risk premia of asset prices in an appropriate manner, the Bank may increase or decrease the amount of purchases depending on market conditions. 1) In case of a rapid increase in the yields, the Bank will purchase JGBs promptly and appropriately.

b) As for CP and corporate bonds, the Bank will maintain their amounts outstanding at about 2.2 trillion yen and about 3.2 trillion yen, respectively.

Japan’s economy has been on a moderate expanding trend, with a virtuous cycle from income to spending operating, although exports, production, and business sentiment have shown some weakness, mainly affected by the slowdown in overseas economies and natural disasters. Overseas economies have been growing moderately on the whole, although slowdowns have continued to be observed. In this situation, exports have continued to show some weakness, and industrial production has declined recently, due partly to the effects of natural disasters. On the other hand, with corporate profits staying at high levels on the whole, business fixed investment has continued on an increasing trend. Private consumption has been increasing moderately, albeit with fluctuations due to such effects as of the consumption tax hike, against the background of steady improvement in the employment and income situation. Housing investment has been more or less flat, and public investment has increased moderately. Meanwhile, labor market conditions have remained tight. Financial conditions are highly accommodative. On the price front, the year-on-year rate of change in the consumer price index (CPI, all items less fresh food) is at around 0.5 percent. Inflation expectations have been more or less unchanged.

With regard to the outlook, Japan’s economy is likely to continue on a moderate expanding trend, as the impact of the slowdown in overseas economies on domestic demand is expected to be limited, although the economy is likely to continue to be affected by the slowdown for the time being. Domestic demand is expected to follow an uptrend, with a virtuous cycle from income to spending being maintained in both the corporate and household sectors, mainly against the background of highly accommodative financial conditions and active government spending, despite being affected by such factors as the consumption tax hike. Although exports are projected to continue showing some weakness for the time being, they are expected to be on a moderate increasing trend on the back of overseas economies growing moderately on the whole. The year-on-year rate of change in the CPI is likely to increase gradually toward 2 percent, mainly on the back of the output gap remaining positive and medium- to long-term inflation expectations rising, despite such effects as of the decline in [Note 2]

Risks to the outlook include the following: the consequences of protectionist moves and their effects; developments in emerging and commodity-exporting economies such as China; developments in global adjustments in IT-related goods; developments in the United Kingdom’s exit from the European Union (EU) and their effects; geopolitical risks; and developments in global financial markets under these circumstances. Downside risks concerning overseas economies seem to remain significant, and it also is necessary to pay close attention to their impact on firms’ and households’ sentiment in Japan.

5. The Bank will continue with “Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control,” aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner. It will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds 2 percent and stays above the target in a stable manner. As for the policy rates, the Bank expects short- and long-term interest rates to remain at their present or lower levels as long as it is necessary to pay close attention to the possibility that the momentum toward achieving the price stability target will be lost. It will examine the risks considered most relevant to the conduct of monetary policy and make policy adjustments as appropriate, taking account of developments in economic activity and prices as well as financial conditions, with a view to maintaining the momentum toward achieving the price stability target. In particular, in a situation where downside risks to economic activity and prices, mainly regarding developments in overseas economies, are significant, the Bank will not hesitate to take additional easing measures if there is a greater possibility that the momentum toward achieving the price stability target will be lost. [Note 3]

[Note 1] Voting for the action: Mr. H. Kuroda, Mr. M. Amamiya, Mr. M. Wakatabe, Mr. Y. Funo, Mr. M. Sakurai, Ms. T. Masai, and Mr. H. Suzuki. Voting against the action: Mr. Y. Harada and Mr. G. Kataoka. Mr. Y. Harada dissented, considering that allowing the long-term yields to move upward and downward to some extent was too ambiguous as the guideline for market operations decided by the Policy Board. Mr. G. Kataoka dissented, considering that it was desirable to strengthen monetary easing by lowering the short-term policy interest rate.

[Note 2] Mr. G. Kataoka dissented, considering that the possibility of the year-on-year rate of change in the CPI increasing toward 2 percent going forward was low at this point.

[Note 3] In order to achieve the price stability target of 2 percent at the earliest possible time, Mr. G. Kataoka dissented, considering that further coordination of fiscal and monetary policy was necessary, and that it was appropriate for the Bank to revise the forward guidance for the policy rates to make it a powerful one that specifically relates to the price stability target.”

US stocks ended mixed on Wednesday after five-session record run as US-China deal euphoria abates. The S&P 500 slipped 0.04% to 3191.14 ahead of impeachment proceedings against President Donald Trump led by House Democrats. The Dow Jones industrial average slid 0.1% to 28239.28. Nasdaq gained 0.05% to fifth-straight record close 8827.73. The dollar strengthening accelerated as New York Fed President John Williams qualified as success central bank’s actions in repo market in the aftermath of a sudden spike in short-term borrowing costs in mid-September. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, rose 0.2% to 97.40 but is lower currently. Futures on US stock indices point to higher openings today.

European stocks end mixed

European stock markets ended mixed on Wednesday as investors gauge the prospect of no-deal Brexit following UK Prime Minister Boris Johnson’s vow to leave the bloc by January 31, 2020. EUR/USD joined GBP/USD’s continued decline yesterday with both pairs higher currently. The Stoxx Europe 600 ended flat. Germany’s DAX 30 fell 0.5% to 13222.16 despite a report showing higher than expected German Ifo business sentiment for December. France’s CAC 40 slid 0.2% and UK’s FTSE 100 rose 0.2% to 7540.75 as UK inflation held steady at a three-year low of 1.5% in November.

Shanghai Composite flat while Hang Seng dips

Asian stock indices are mixed today after US House of Representatives voted to impeach President Donald Trump, with Senate’s turn now for trial. Republicans who control Senate say they plan to acquit him. Nikkei lost 0.3% to 23864.85 with yen little changed against the dollar after the Bank of Japan kept its monetary policy unchanged. Chinese stocks are mixed: the Shanghai Composite Index is flat while Hong Kong’s Hang Seng Index is down 0.3%. Australia’s All Ordinaries Index lost 0.3% with Australian dollar accelerating its climb against the greenback after stronger-than-expected November jobs report.

Brent gains support Saudi Aramco after its inclusion in indexes

Brent futures prices are marginally higher today. Prices rose yesterday after Energy Information Administration reported US crude oil inventories fell by 1.1 million barrels last week, smaller than SP Global Platts analysts’ forecast: February Brent crude rose 0.2% to $66.26 a barrel on Wednesday. Rising oil prices support also shares of Saudi Arabia’s and world’s biggest oil company – Saudi Aramco. However Saudi Aramco’s shares fell almost 3% during Wednesday’s session after being included in the MSCI Emerging Markets Index (ETF: EEM) and the Saudi Tadawul Index. This is the result of profit taking of funds or retail investors who bought in advance of the company being added to the index. The company’s stock was first offered for 32 riyals ($8.53) per share on December 10. Shares closed about 0.7% lower on Tuesday, the first decline since its record-breaking initial public offering, but were still up about 18% from the IPO price. Aramco closed 10% higher after its first day of trading on December 11. Only 1.5% of the company has been sold despite an announced goal of 5%, with wealthy Saudi families and regional allies as main investment and over 97% of the retail investors exclusively from Saudi Arabia and the Gulf.

Gold up

Gold prices are edging higher today. The price of an ounce of gold for February delivery lost 0.1%, to $1,478.70. yesterday as the dollar strengthened.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

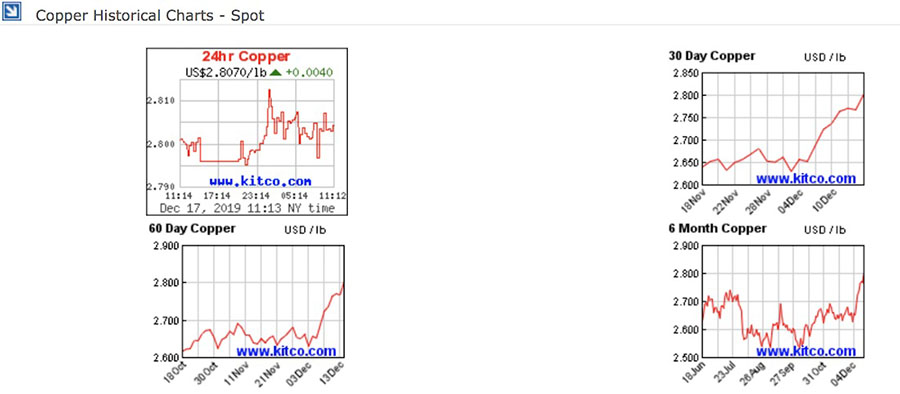

Bob Moriarty of 321gold discusses recent copper price moves along with those of a new copper producer.

A very short nine weeks ago I was giving good advice to my readers when I said:

“I was writing about Nevada Copper Corp. (NCU:TSX; NEVDF:OTC) five months ago and the shares were $0.395. Today as the price of copper has gone down by ten percent and we move into tax loss silly season, the shares are $0.215. They were cheap then, they are cheaper now along with most of their brethren.”

Those wise enough to invest are up 40%, which beats the heck out of a red-hot stick in your left eyeball.

Nevada Copper had two things providing a potential tail wind. We moved into Tax Loss Silly Season a month ago. NCU-V hit a new yearly low at $0.185. And when nothing at all has changed except for the price, when you are in TLSS from mid-November to mid-December that is a great time for picking up quality shares in the bargain bin.

There is a third factor that investors need to consider. The world is working with a 10-day supply of copper on hand. Traditionally copper supply bottoms with price. Certainly the recent prices for copper support the idea that a bottom has been reached with prices up 10% in the last two weeks alone.

Nevada Copper promised production in Q4 almost a year ago and unlike 90% of the promises made to me in the last 18 years, they didn’t change at all. They charged forward and are producing now. By the way, did I fail to mention that just before a company goes into production and for the first six months is the sweet spot of investing? Long patient shareholders are rewarded and new shareholders often see nice profits at once. Add to that the irrational as hell TLSS and the price of copper going up and you have a perfect storm.

I love working with Nevada Copper. They do what they say they are going to do. Management is brilliant. Nevada Copper is an advertiser and I own shares bought in the open market. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Nevada Copper. Nevada Copper is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Shares of Tallgrass Energy LP traded 20% higher after the firm advised that it entered into a definitive merger agreement with Blackstone Infrastructure Partners to acquire all of the company’s publicly held outstanding class A shares for $22.45 per share in cash.

Midstream energy infrastructure company Tallgrass Energy LP (TGE:NYSE) today announced that it has entered into a definitive merger agreement with Blackstone Infrastructure Partners (BIP) and its investment partners Enagas, GIC, NPS and USS to acquire all of the publicly held outstanding Class A Shares of TGE for $22.45 in cash per share.

Tallgrass Energy stated that its Board of Directors’ Conflicts Committee has already unanimously approved the transaction and determined it to be in the best interests of the company and its public shareholders.

The report indicated that the transaction is expected to close in Q2/20 subject to satisfaction of customary conditions, including approval of the merger by holders of a majority of the outstanding Tallgrass Class A and Class B shares. This majority is inclusive of the approximately 44% of the total Class A and Class B shares that are already held by the BIP consortium sponsors. The BIP sponsors stated that they expect to fund the bulk of the purchase of the Class A Shares with approximately $3 billion of equity with the remainder of the transaction funding to be financed by debt.

Tallgrass Energy LP is a growth-oriented midstream energy infrastructure company headquartered in Leawood, Kansas. The firm indicated that “it operates across 11 states with transportation, storage, terminal, water, gathering and processing assets that serve some of the nation’s most prolific crude oil and natural gas basins.”

Blackstone is one of the world’s largest investment firms with its asset management businesses having over $554 billion in assets under management. The firm stated that infrastructure is one of its most active investment areas, and that over the last 15 years, it has invested more than $45 billion globally in infrastructure-related projects.

Tallgrass Energy started off the day with a market capitalization of about $5.1 billion with approximately 281.3 million shares outstanding. TGE shares opened 21% higher today at $22.17 (+$3.88, + 21.21%) compared to yesterday’s $18.29 closing price. The stock has traded today between $22.09 and $22.18 per share and at present is trading at $22.10 (+$3.81, +20.86%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Axsome Therapeutics shares reached a new 52-week high price today after the company reported that its AXS-05 drug achieved primary endpoint in the GEMINI Phase 3 trial in Major Depressive Disorder. The firm indicated that the positive results support a New Drug Application filing in H2/20.

Early this morning, clinical-stage biopharmaceutical company, Axsome Therapeutics Inc. (AXSM:NASDAQ), which focuses on developing novel therapies for the management of central nervous system (CNS) disorders, announced that “AXS-05, a novel, oral, investigational NMDA receptor antagonist with multimodal activity, met the primary endpoint and rapidly and significantly improved symptoms of depression in the GEMINI Phase 3 trial in major depressive disorder (MDD).”

The company advised that the GEMINI study was a double-blind study of AXS-05 (dextromethorphan/bupropion modulated delivery tablet) in 327 adult patients with confirmed moderate to severe MDD. The firm indicated that AXS-05 was well tolerated in the trial and met the primary endpoint by demonstrating a highly statistically significant reduction in the Montgomery-Åsberg Depression Rating Scale (MADRS) total score compared to placebo.

Professor Maurizio Fava, MD, psychiatrist-in-chief at Massachusetts General Hospital (MGH), director of the Division of Clinical Research of the MGH Research Institute, and associate dean for clinical & translational research at Harvard Medical School, commented, “AXS-05 demonstrated a rapid and very clinically meaningful improvement in depressive symptoms, observed after only one week, in this large and well-controlled Phase 3 trial in major depressive disorder. Given the known challenges of conducting trials in psychiatry, it is very encouraging to see replication of Phase 2 findings in such a robust way…Clinical depression is a potentially life-threatening condition. Currently marketed antidepressants fail to provide adequate treatment response in almost two thirds of treated patients, and may take up to six to eight weeks to provide clinically meaningful response. These data suggest that AXS-05, as an oral NMDA receptor antagonist with multimodal activity, may represent a novel treatment for major depressive disorder.”

The company’s CEO Herriot Tabuteau, MD, added, “We are very pleased with the compelling results of the GEMINI trial which demonstrate the potential for AXS-05 to provide significant benefits to patients living with depression, based on observed rapid and sustained antidepressant effects, resulting from its potentially first-in-class, oral NMDA receptor antagonist and multimodal mechanism of action…The progress of the AXS-05 clinical program in mood disorders reflects Axsome’s commitment to accelerating innovation to address serious CNS disorders. With GEMINI and the previously completed ASCEND study, the efficacy of AXS-05 in major depressive disorder has now been demonstrated in two positive well-controlled trials, enabling the filing of an NDA for AXS-05, which is anticipated in the coming year.”

The firm explained, “AXS-05 was granted Breakthrough Therapy designation by the U.S. Food and Drug Administration (FDA) for the treatment of MDD in March 2019, and that based on the outcome of the FDA Breakthrough Therapy meeting, Axsome believes the positive results of the GEMINI and ASCEND trials of AXS-05 in MDD, are sufficient to support submission of a New Drug Application (NDA) for AXS-05 for the treatment of MDD in H2/20.”

Cedric O’Gorman, MD, SVP of clinical development and medical affairs of Axsome, remarked, “Depression is a major public health concern with most patients failing to adequately respond to currently approved antidepressants…The positive results of the GEMINI study are significant and exciting because they bring us closer to our goal of addressing this public health need with a potentially first-in-class, rapid-acting, effective, oral, antidepressant which can be safely administered at home. With its modulation of glutamate neurotransmission, if approved, AXS-05 would represent the first mechanistically novel oral pharmacotherapy for depression in over 30 years.”

Axsome stated that “major depressive disorder (MDD) is a debilitating, chronic, biologically-based disorder characterized by low mood, inability to feel pleasure, feelings of guilt and worthlessness, low energy, and other emotional and physical symptoms, and which impairs social, occupational, educational, or other important functioning. In severe cases, MDD can result in suicide…Patients diagnosed with MDD are defined as having treatment resistant depression (TRD) if they have failed to respond to two or more antidepressant therapies.”

Axsome Therapeutics is headquartered in New York. The firm states that its core CNS product candidate portfolio includes four clinical-stage candidates: AXS-05; AXS-07; AXS-09 and AXS-12. Ongoing studies include a phase 3 trial of AXS-05 in treatment resistant depression, a phase 3 trial in major depressive disorder, and a phase 2/3 trial in agitation associated with Alzheimer’s disease. The company also has two active phase 3 trials of its AXS-07 for the acute treatment of migraine, and a phase 2 trial of AXS-12 in narcolepsy.

Axsome Therapeutics began the day with a market cap of about $1.6 billion with approximately 34.51 million shares outstanding and a short interest of 17.7%. AXSM shares opened much higher today at $85.2965 (+$38.51, +82.30%) compared to Friday’s $46.79 closing price. The stock has traded between $72.85 and $88.00 per share today and presently is trading at $84.38 (+$37.60, +80.35%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Here is a news flash: I am sick to death of The Fed, unelected demigods that rarely, if ever, had to meet payroll. I am also completely disgusted with this unholy “Divine Right of Banks” to hold sway with politicians, gaining total control over the purchasing power of my savings (currency units) by way of an ordained edict giving them the right to manufacture any and all amounts of said currency units (debt) with nary a shred of governance.

I am further revolted by this all-encompassing blanket of regulatory malfeasance that condones and, in fact, encourages behaviors by C-suite officials, politicians and bankers in direct violation of securities laws. I refer to the practices of interventions (e.g., the Dec. 24, 2018, call by Treasury Secretary Steve Mnuchin for a meeting of the Working Group on Capital Markets”), manipulations (“tweets” designed to trigger software-generated reactions (President Trump, Elon Musk), and fraud (JP Morgan’s securities violations and RICO indictment). Lastly, this malevolent seepage of an innate sense of entitlement across the civilized world now threatens the foundation, support beams and roofs of the democratic system and along with it, free market capitalism, a phrase whose meaning Larry Kudlow would be wise to revisit.

In contract law, “due consideration” is that thing that allows a transaction to occur. It might be labor or a product or even advice, but essentially, it is a rules-based tenet that prevents theft. I cannot take something that is yours without you agreeing to that which I offer in trade. Last week, Fed chairman Jerome Powell explained the rules of the 2020 financial landscape by confirming to us all that “balance sheet normalization,” the implementation of which caused a20% meltdown in the S&P last year, is now, to borrow a phrase from Ebenezer Scrooge, “. . .an undigested bit of beef, a blot of mustard, a crumb of cheese, a fragment of an underdone potato.” In its place, we can now celebrate massive bloating of the Fed balance sheet, along with annual deficits to the order of $1.7 trillion.

In response, stocks began to slide, and precious metals began to rise, as the olfactory senses detected the imminent return of that elusive beast, inflation. It is said that inflation has been “muted” in the U.S. by way of cheap foreign goods (China) and subdued wage inflation. Mr. Powell told us, in his “prepared remarks,” that he and his co-conspirators are going to let the economy “run hot” for a while to allow Middle America to play “catch-up” in the disparity game of chance they are now playing with reckless abandon. The problem, my dear readers is that “inflation is like toothpaste; once it’s out you can hardly get it back in again” (Karl Otto Puhl).

What Chairman Powell meant to say is that Fed policies that have been engineering, promoting and cheerleading monetary asset inflation (all banker collateral, including stocks, bonds, and real estate) are now being back-burnered in favor of wage inflation (the income earned by the average Joe). News Flash #2: This policy “initiative” has no foundation in economic theory; it is a response to a societal trend whereby the disenfranchised segment of “The American Dream” is beginning to spiral out of control, with aberrant behaviors now more the norm than the isolated.

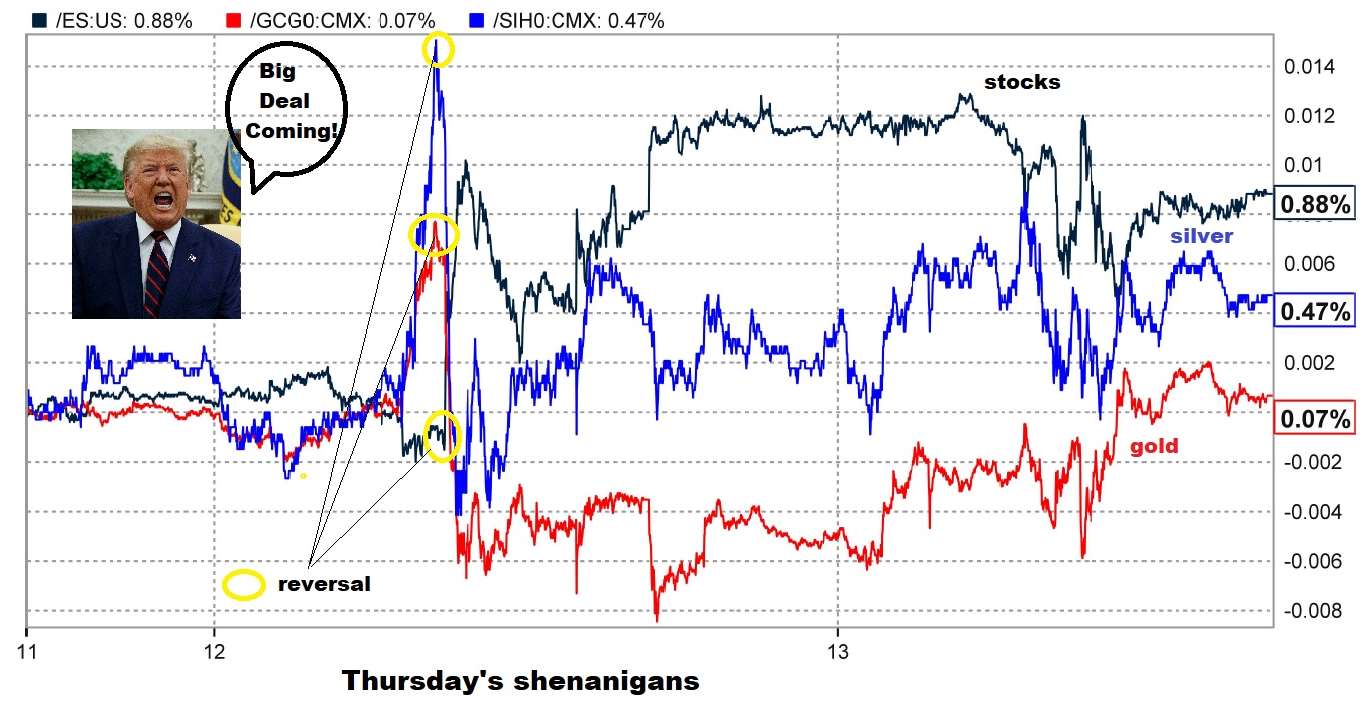

However, as minutes and seconds elapsed after the Powell Pronouncement, gold and silver began to escalate, with stock prices moving sharply lower. At this point, out of the blue and without explanation nor reason, Donald Trump fired off a tweet that was immediately absorbed by thousands upon thousands of pattern-recognition software word cloud analyzing “algobots,” stating emphatically that he is on the verge of signing a “BIG DEAL” with China that the markets “will love.”

As can be seen from the chart below, gold, silver and stocks all reversed and by the end of the day, the Dow had advanced over 200 points and all the beautiful gains in gold and silver had evaporated. All because a “China deal” tweet by Donald Trump, the fiftieth such market-moving utterance of 2019, spooked the algos into action, a manipulative trick well known and faithfully employed by the current Administration and its market co-managers.

When we decide to enter markets, we are told that manipulation is a violation of securities bylaws and an indictable offense. You can go to J-A-I-L for even attempting to influence markets by “spoofing” (stacking bids or offerings with phony orders never intended to be executed). Similarly, releasing false or misleading corporate or economic data is an action in violation of the rules as well. How the current POTUS can engage in such fraudulent behavior is astonishing; he has been calling for a China trade “deal” since 2018 and each and every time, the stock market rallied. Elon Musk was sanctioned for tweeting out that he was about to do Tesla deal at prices way above the current market, which also turned out to be a pile of horse manure designed to fry the shorts (which it did).

Now, “in the end,” you will say, “markets will revert to the norm and ignore the tweeting and spoofing and fraud,” because you believe these are “free markets.” News Flash #3: These are not, in any way, shape or form, free markets. These are the most compromised, corrupt entities in the world and until order is restored, they are as dangerous as a Cambodia mine field in the fog after a fifth of bourbon at midnight. And that restoration means jail time for violatorsperiod.

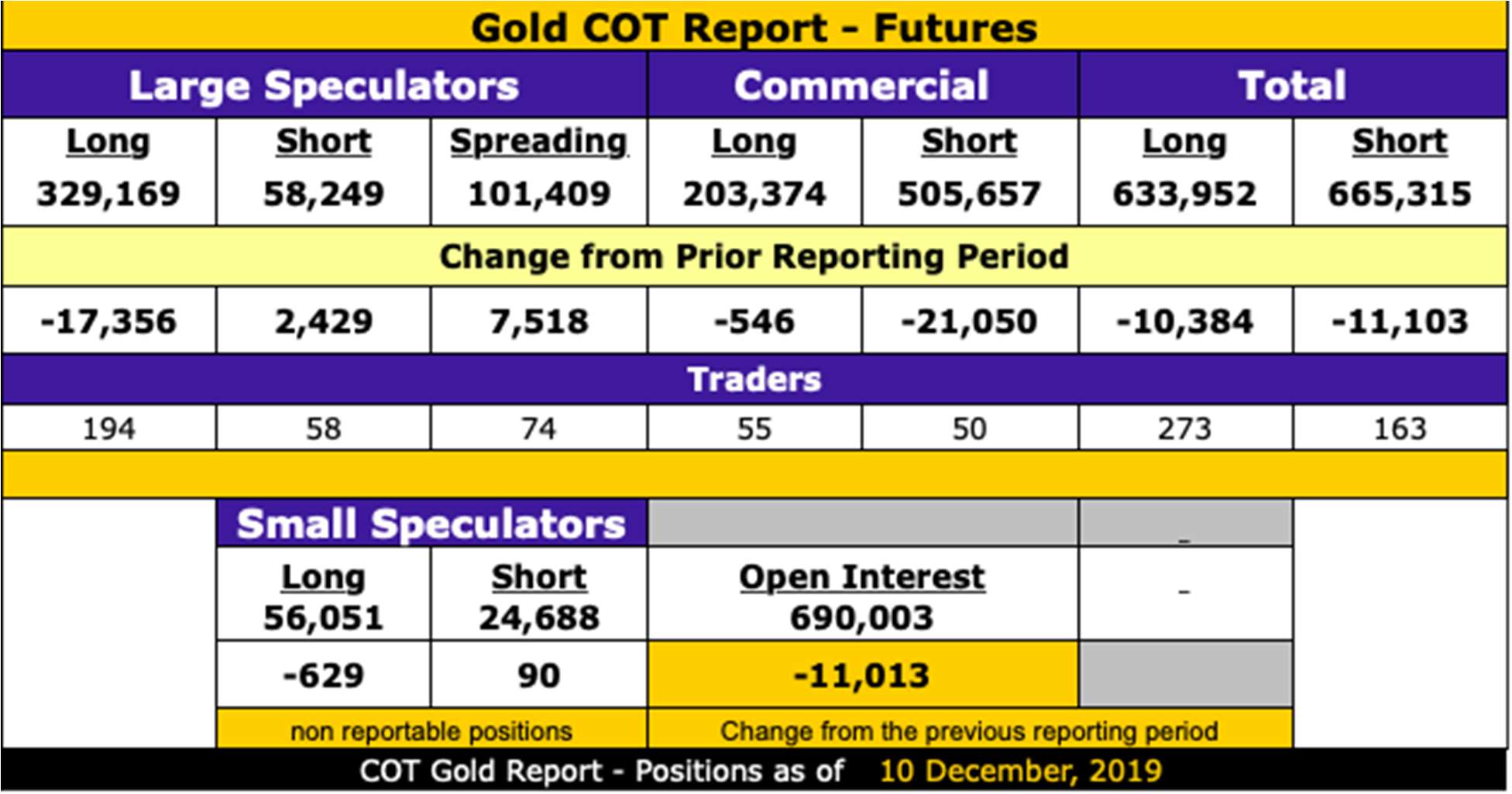

Nevertheless, for the week ended Dec. 13, the precious metals ended higher with the COT report, indicating good news for gold and great news for silver.

You can see that the weakness in early December triggered long liquidation by the Large Specs, accompanied by the usual reactionary short covering by the Commercials (bullion bank behemoths), along with the expected drawdown in open interest. While the strength this week will have prompted the reverse, the gold COT was positive and bodes well for a strong close for 2019.

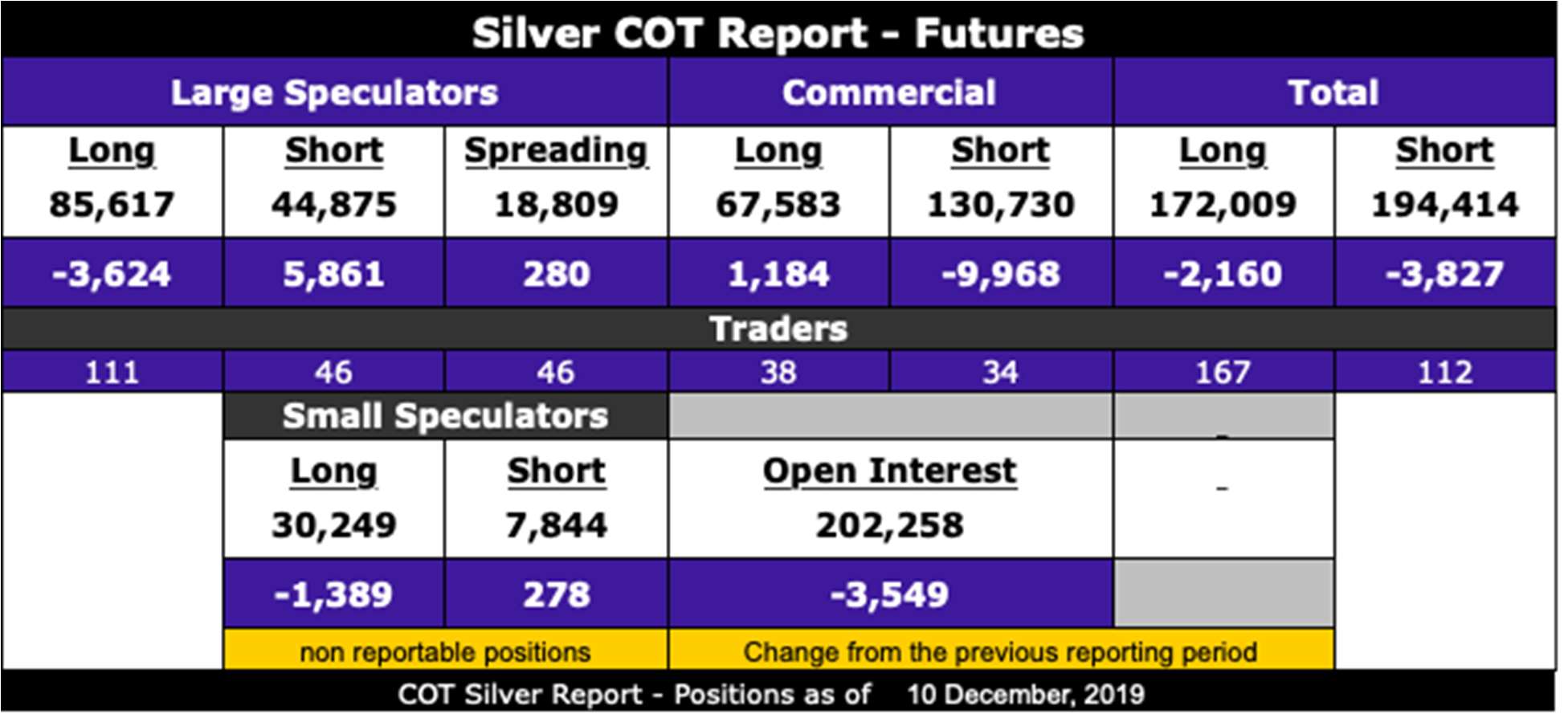

The silver COT was a shocker; the Commercials took full advantage of the big drop in early December, which came after First Notice Day (to my surprise and chagrin), and covered a massive 9,968 shorts, as well as adding 1,184 new longs representing 55,745,000 ounces of phony, never-to-be-delivered, “silver” with a fantasy-world notional value of US$947,665,000.

These bullion bank traders can whip around nearly a billion dollars’ worth of illusionary silver, materially impacting the livelihoods of mine laborers, pension fund managers, jewelers and solar energy dealers without as much as a whimper from the Securities and Exchange Commission, the U.S. Commodity Futures Trading Commission or the U.S. Department of Justice. However, it is what it is, and with silver ending the week higher, it remains my numero uno investment theme for 2020, as it was for the latter half of 2019.

In fact, it was silver options, futures and miners (as well as the Great Bear Resources Ltd. [GBR:TSX.V; GTBDF:OTCQX] trade, of course) that were responsible for the 273% advance in the GGMA portfolio, originally constructed in January 2019 and presented in the 2019 Forecast Issue. The silver market remains in a declining pennant formation, but with last week’s action, has clearly launched an assault on the downtrend line drawn off the Sept. 4 top (which I was lucky enough to have identified to the day back in late August).

I have identified the 200-day moving average (dma) at US$16.26 as the line-in-the-sand for short-term trading positions but certainly the actions on Thursday and Friday are encouraging.

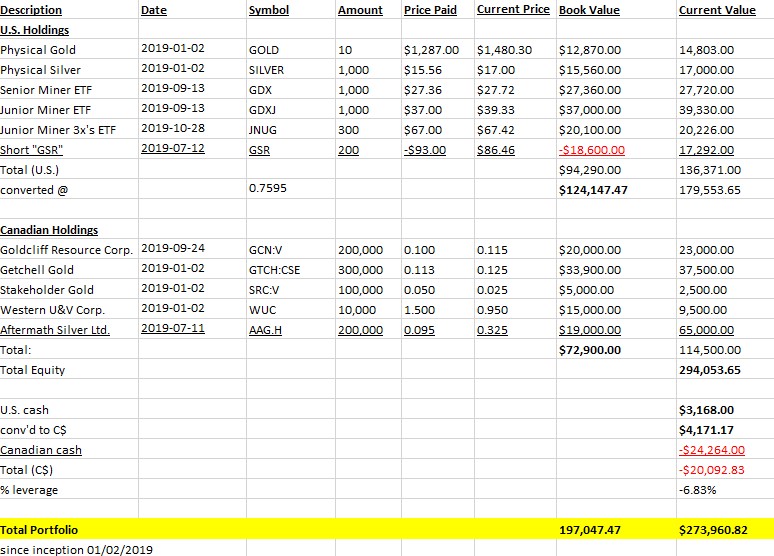

Turning to the GGMA portfolio, I am keeping the U.S. holdings intact going into the New Year but may take down the 3x-leveraged Junior Miner (JNUG), which is back into the black after going red almost immediately after acquisition. The original portfolio was purchased on Jan. 3, 2019, with CA$100,000, and with trades, additions and deletions, now resides at $294,053, with a CA$24,264 margin position, leaving total equity at CA$273,960. A return of 2.73 times original invested capital is both spectacular and unusual and was the product of some fortuitous positions taken in silver calls, Great Bear Resources (since sold) and Aftermath Silver Ltd. (AAG:TSX.V) (still holding and looking to add).

(As a bookkeeping note, the “Short GSR” position shows a red (negative) book value because it is a short sale andthe only way I could get it to jibe with the overall portfolio is to format it as such.)

As for the individual names, the Canadian dollar allocation is comprised of exclusively junior mining deals comprised of five exploration/development companies, all of which save one (Stakeholder Gold Corp. [SRC:TSX.V]) are sitting with established resources of either gold, silver or uranium. I am reviewing the SRC position closely but being a disappointment (verging on hallucinogenic flop), it is too small a holding to sell but providing zero impetus to buy. My top pick for 2019 was originally Great Bear, but has since been replaced with Aftermath Silver to close out the year.

Looking out to 2020, the forecast issue is in the oven, with a sneak peek available as to possible changes to the portfolio through my “2019 tax-Loss list,” where I have identified six companies floating in and around the 52-week low list being buffeted by wave after wave of tax-loss selling. (E-mail me at the address shown below on the contact card to receive a complimentary copy: [email protected].)

As much as I remain a staunch precious metals bull, I don’t think valuations here in late 2019 are as compelling as they were in August 2018 or April 2019. Those two entry points came off Daily Sentiment Index (DSI) readings of <10% bulls, whereas today we are about 60%. By contrast, zinc, uranium and cannabis now reside in the low end of the sentiment spectrum and without debating their merit, the “no-brainer” aspect of precious metals investment is arguable.

I hope to have the “2020 Forecast Issue” ready for launch by next weekend but will await the end-of-month marks to finalize the 2019 portfolio return and to insert acquisitions points for the new names.

I am bidding for a few of the beaten-down weed stocks as this is being typed, so as a teaser, have a look at these two charts. One year ago, the cryptocurrency deals were the most reviled, hated, scorned-upon group of companies in all of the deal world. One year later, a new dartboard group is taking the heatcannabis. Look at the JanuaryJuly performance of Bitcoin. From tax-loss trough at US$3,180 to mid-July peak at US$11,778, speculators made 2.7 times their money. I see a similar pattern unfolding for the weed stocks.

Fido is sleeping quite contentedly beneath my desk now and in the kitchen, I hear the machinations of oven doors and beaters, fruitcakes and Jolly Dollies being conjured up for seasonal consumption. Fido was banished to the woodshed yesterday for getting his nose into the safe in which I keep my coins and certificates and cash. It seems that Fido has the same regard for my savings as does Fed Chairman Jerome Powell. . .

Bad Fido!

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Aftermath Silver, Stakeholder Gold, Goldcliff Resources, Getchell Gold, Western Uranium and Vanadium. My company has a financial relationship with the following companies referred to in this article: Aftermath Silver. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Great Bear Resources, Goldcliff. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Aftermath Silver and Western Uranium and Vanadium. Please click here for more information. Within the last six months, an affiliate of Streetwise Reports has disseminated information about the private placement of the following companies mentioned in this article: Aftermath. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Aftermath Silver, Goldcliff, Getchell, Western Uranium and Vanadium and Stakeholder Gold, companies mentioned in this article.

Charts provided by the author.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

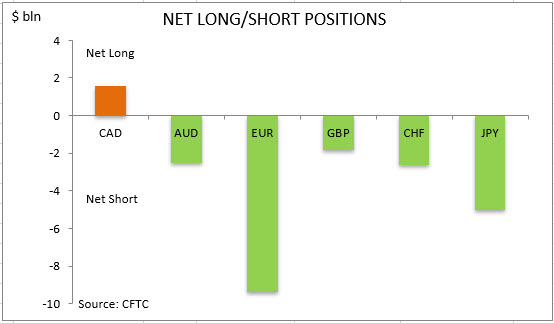

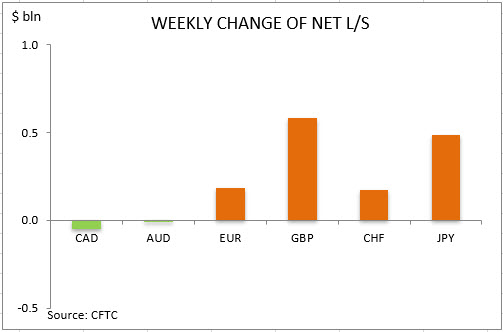

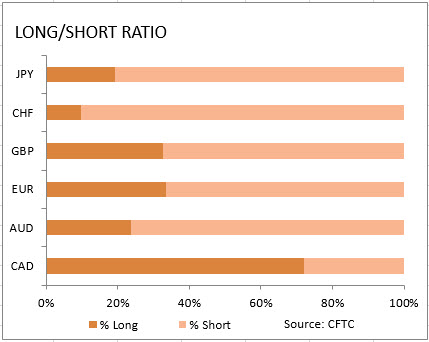

US dollar net long bets rose to $19.84 billion from $18.36 billion against the major currencies during the last three weeks, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to December 10 and released on Friday December 23. The increase in bullish dollar bets continued as durable goods orders resumed growing in October (rising 0.6% after a 1.4% decline in September) as did factory orders, and the unexpectedly strong nonfarm payrolls report showed US economy added 266,000 new jobs in November.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Recent drill results from both assets are provided in a ROTH Capital Partners report.

In a Dec. 11 research note, ROTH Capital Partners analyst Jake Sekelsky reported that Kirkland Lake Gold Inc. (KL:TSX; KL:NYSE) hit high grades on recent drilling at its Fosterville and Macassa properties. “While we view the exploration results as positive, we expect the market to remain focused on the recent proposed acquisition of Detour Gold,” he added.

Sekelsky provided the findings from both assets, “the key cash flow generators of Kirkland Lake’s existing portfolio.”

At Fosterville, specifically the Robbins Hills area, 66 holes over 36,428 meters (36,428m) returned “multiple occurrences of visible gold,” the analyst noted. Hole RDH334A, for instance, showed 24.5 grams per ton (24.5 g/t) gold over 3.7m. As such, Robbins Hills “appears to be emerging as a potential second source of throughput for the Fosterville mill going forward,” commented Sekelsky.

Based on these results, ROTH expects Kirkland Lake to conduct follow-up drilling early next year to eventually incorporate Robbins Hill into the Fosterville mine plan.

At Macassa, Sekelsky relayed, 30 holes totaling 7,792m drilled at the point where the amalgamated break and SMC West merge returned strong intercepts including 32.5 g/t gold over 3.5m. “While Fosterville receives the vast majority of the market’s attention towards exploration due to its ultrahigh-grade potential, we believe Macassa has somewhat unrecognized exploration potential,” he added.

Going forward, ROTH anticipates that Kirkland Lake will keep working to extend mineralization and grow reserves at Macassa.

ROTH maintained its Neutral rating and US$50 per share price target on Kirkland Lake Gold, whose stock is trading at around US$41.92 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from ROTH Capital Partners, Kirkland Lake Gold, Company Note, December 11, 2019

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of Kirkland Lake and as such, buys and sells from customers on a principal basis.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.