Bob Moriarty of 321gold provides an update on this junior miner.

I did a good piece on GFG Resources Inc. (GFG:TSX.V; GFGSF:OTCQB) back in April, and anyone interested in the company should go back and read it. It doesn’t make a lot of sense for me to cover the same stuff again and again.

Watching the share price this year has been every bit as exciting as watching paint dry. It was $0.23 when I talked about it and dribbled down into tax-loss silly season (TLSS) last month where it hit a yearly low of $0.16. Some astute investors understood how silly TLSS was and have run the price of shares up by 50% in less than a month to $0.24.

GFG’s partner in the Rattlesnake project, Newcrest Mining Ltd. (NCM:ASX), had planned on spending somewhere between $33.5 million in exploration at the property for 2019 to do six to eight holes for 5,000 to 6,000 meters. They ended up doing 3,900 meters in three holes, including one 1,809 meter monster hole that was extended by an additional 300 meters because Newcrest liked the core.

GFG was talking about having the results out in December but I sorta doubt it’s going to happen. The junior resource market goes into hibernation about the 20th of December and nothing will attract the attention of investors until they sober up in January.

Newcrest is easily one of the best mining companies in the world. They do things right. Their deal with GFG values 75% of Rattlesnake at about $100 million. That infers a valuation of about $33 million just for Rattlesnake for GFG.

But GFG is not a one-trick pony. Understanding that nothing is going to happen in Wyoming during the winter months, they set up a Plan B in Ontario. Indeed, while the market eagerly awaits the drill results from Rattlesnake, GFG has announced the start of a 6,500-meter drill program at their Pen property. They believe they can have 2,500 meters done by the new year and an additional 4,000 meters in Q1/2020.

I just did an interview with Jay Taylor. He wanted my two best picks for 2020. GFG was one. I give Newcrest a 50-50 chance of catching the brass ring with their just completed drill program at Rattlesnake, with expected results in the next two weeks. If they hit big, GFG will run. If they don’t hit big, there are a lot more rocks at Rattlesnake that they can poke holes in. And Plan B is a solid plan in Ontario. There will be a constant flow of news for the next three to six months. Some might even be good.

I have participated in private placements in GFG in the past and also bought shares in the open market. GFG is an advertiser and as such I have to be biased. They do a good job of communicating, so go over their website. Do your own due diligence.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: GFG Resources. GFG Resources is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of GFG Resources, a company mentioned in this article.

This week – December 22 through December 28 – central banks from 4 countries or jurisdictions are scheduled to decide on monetary policy: Kyrgyz Republic, Egypt, Sri Lanka, and Trinidad and Tobago.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.

Shares of Paratek Pharmaceuticals traded 40% higher today after the firm announced it was awarded a BARDA BioShield program contract valued at up to $285 million for NUZYRA used to treat anthrax.

Late yesterday afternoon, biopharmaceutical company Paratek Pharmaceuticals Inc. (PRTK:NASDAQ), which is focused on the development and commercialization of innovative therapeutics, announced that “the U.S. Department of Health and Human Services, Office of the Assistant Secretary for Preparedness and Response, and Biomedical Advanced Research and Development Authority (BARDA) has awarded the Company a 5-year contract, with an option to extend to 10-years, to support the development of Paratek’s NUZYRA® (omadacycline) for the treatment of pulmonary anthrax, FDA post-marketing requirements associated with the initial NUZYRA approval, and the option to procure up to 10,000 treatment courses of NUZYRA for the Strategic National Stockpile (SNS) for use against potential biothreats.”

The firm outlined in the report that the BARDA BioShield program was created to accelerate the research, development, purchase and availability of effective medical products against chemical, biological, radiological or nuclear agents.

Dr. Rick Bright, BARDA Director and Deputy Assistant Secretary for Preparedness and Response, commented, “BARDA is encouraged by the opportunity to partner with Paratek Pharmaceuticals to further develop this critical antibiotic that will help us to combat antimicrobial resistance and treat anthrax infections…This award is an important step in BARDA’s efforts to enhance our national health security preparedness.”

The agreement provides for initial funding of approximately $59 million for NUZYRA development for treatment of pulmonary anthrax and the purchase of 2,500 treatment courses of NUZYRA to add to the current SNS. Additional potential time-based funding includes approximately $77 million for existing FDA PMR commitments and $20 million for manufacturing-related requirements. The remaining staged, milestone-based funding includes the potential for approximately $13 million to support development of NUZYRA for prophylaxis of anthrax and a maximum of around $115 million to provide for three additional purchases of NUZYRA for the SNS subject to anthrax development program milestones.

Paratek’s Chief Executive Officer Evan Loh, M.D., commented, “Through Project BioShield, BARDA has identified and validated the important role that Paratek and NUZYRA will play in helping to enhance the biodefense preparedness of our country, saving lives and protecting Americans…Paratek has been studying the potential utility of antibiotics against bioterrorism threats for over a decade. Through these activities, we have generated promising in vitro and in vivo animal data with NUZYRA against select biothreat pathogens. For these reasons, we believe that NUZYRA is well-positioned to help address potential public health emergencies at a time when antibiotic resistance is a growing global threat.”

The company identifies NUZYRA (omadacycline) as a broad spectrum, novel antibiotic with both once-daily intravenous and oral formulations for the treatment of community-acquired bacterial pneumonia and acute bacterial skin and skin structure infections. Paratek has entered into a collaboration agreement with Shanghai-based Zai Lab Ltd. (ZLAB:NASDAQ-ADR) for the development and commercialization of omadacycline in the greater China region and retains all remaining global rights.

Paratek Pharmaceuticals is headquartered in Boston, Mass., and describes its business as a commercial-stage biopharmaceutical company focused on the development and commercialization of innovative therapeutics. The firm’s lead commercial product, NUZYRA (omadacycline), is utilized in the treatment of adults with “community-acquired bacterial pneumonia and acute bacterial skin and skin structure infections” and is also being studied against pathogenic agents causing infectious diseases of public health and biodefense importance, including plague and anthrax. The company’s second FDA approved commercial product, SEYSARA (sarecycline), is used in the treatment of moderate to severe acne vulgaris.

Paratek Pharmaceuticals began the day with a market capitalization of about $98.2 million with approximately 33.29 million shares outstanding along with a 30% short interest. PRTK shares opened much higher today at $4.31 (+$1.36, +46.10%) over yesterday’s $2.95 closing price. The stock has traded today between $3.69 and $4.32 per share and is currently trading at $4.19 (+$1.24, +42.03%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

By CentralBankNews.info Jamaica’s central bank continued to keep its policy rate steady at 0.50 percent, saying inflation is likely to be higher than previously forecast over the next two quarters but still track within its target range of 4.0 to 6.0 percent over the next two years.

The Bank of Jamaica (BOJ), which has maintained its policy rate since wrapping up an easing cycle in August, added it considered the level of inflation in November a peak and prices should start to fall in December as agricultural production recovers.

“Bank of Jamaica will therefore continue to closely monitor the impact of the significant monetary loosening undertaken thus far on credit expansion, capital market transactions, overall economic activity and, consequently, the impact on inflation, to determine the appropriate future path for the policy rate,” BOJ said, repeating its guidance from November.

The Bank of Jamaica (BOJ) has lowered its policy rate 12 times and by a total of 325 basis points since July 2017 – including 4 times and by 125 points this year – when it adopted a new monetary policy framework that made the overnight deposit rate the new policy rate.

Jamaica’s inflation rate jumped to 4.6 percent in November, the highest rate in 6 months, from 3.3 percent in October, boosted by a 10.6 percent rise in vegetable prices due to drought that was then followed by heavy rains that hit the Caribbean island between June and October.

Excluding agricultural prices, inflation would have been around 1.9 percent, with transport-related prices also rising by 0.5 percent in the month in connection with a rise in retail petrol prices and higher seasonal airfares.

In its quarterly inflation forecast from November BOJ expected inflation to accelerate to 4.6 percent in December and 4.7 percent in March before decelerating slightly in June and remaining within the lower half of its target range for the following five quarters.

Jamaica’s economy has slowed this year after expanding in 2017 and 2018, with gross domestic product growing an annual 1.3 percent in the second quarter compared with 1.8 percent in the first quarter.

Last month BOJ forecast economic growth would be below potential over the next two years and said today it considers the risks to this forecast as balanced while other indicators continue to be positive, including foreign reserves that remain above levels considered adequate and a continued strong fiscal performance.

The Jamaican dollar has been volatile since early October and on Friday it was trading at 133.8 to the U.S. dollar, down 4.6 percent this year.

Last month BOJ Governor Richard Byles attributed the spike in demand for foreign currency to heightened demand from portfolio transactions combined with seasonal re-stocking by retailers ahead of the Christmas period.

In response to what he described as “unusual heightened demand,” BOJ had boosted the U.S. dollar supply selling $140.0 million between Oct. 18 and Nov. 14.

On that day BOJ also amended its rules requiring that all funds sold by it to dealers and cambios be re-sold to end-users as it felt large part of earlier intervention funds had not reached them.

The Bank of Jamaica issued the following press release:

“Bank of Jamaica announces its decision to hold the policy interest rate (the rate offered on overnight balances at Bank of Jamaica) unchanged at 0.50 per cent per annum, effective 23 December 2019. The decision to hold the policy rate unchanged is based on the Bank’s continued view that monetary conditions are generally appropriate to support inflation remaining within the inflation target of 4.0 per cent to 6.0 per cent over the ensuing eight quarters. The inflation target was set by the Government to facilitate a faster pace of economic growth. Bank of Jamaica will therefore continue to closely monitor the impact of the significant monetary loosening undertaken thus far on credit expansion, capital market transactions, overall economic activity and, consequently, the impact on inflation, to determine the appropriate future path for the policy rate. Inflation At its assessment in November 2019, Bank of Jamaica’s forecast was for inflation to average 4.5 per cent over the next eight quarters. 1 Inflation was projected to accelerate to 4.6 per cent at December 2019 and to 4.7 per cent at March 2020 before decelerating slightly at June 2020. Over the remaining five quarters, inflation was projected to remain within the lower half the 4.0 per cent to 6.0 per target. The forecast was mainly predicated on the impact of exchange rate depreciation, expectations of administered price adjustments, the lagged effect of previous monetary policy accommodation and a slight upward adjustment to crude oil prices. Annual inflation at November 2019, as reported by the Statistical Institute of Jamaica, was 4.6 2 percent, higher than the 4.1percent recorded at November2018. For the month of November, prices rose by1.3 per cent, which was above Bank of Jamaica’s forecast of 0.4 per cent. The main source of the higher-than-expected inflation rate for November was related to agricultural food prices. Vegetable prices rose by 10.6 per cent for the month and approximately 30 per cent for the 12 months to November. In particular, the prices for cabbage, lettuce, carrot, sweet pepper and potato rose significantly in the month, largely due to adverse weather conditions (drought followed by heavy rains) which affected the island between June and October 2019. Excluding the impact of the increases in agricultural food prices, annual inflation would have remained low at around 1.9 per cent. In addition, transport-related prices increased by 0.5 per cent during the month, associated with increases in retail petrol prices as well as seasonally higher airfares.

Bank of Jamaica views the level of November’s agricultural food prices as a peak and expects those prices to start falling in December as agricultural production recovers. Bank of Jamaica’s current assessment is that inflation is likely to be higher than previously forecasted over the next two quarters but is expected to track within the target range of 4.0 per cent to 6.0 per cent. This updated inflation outlook stems from the CPI outturn for November 2019 and the near-term prospects for agricultural food prices along with the outlook for higher oil and international grains prices, the latter reflecting the impact of increased optimism about world growth and demand. In addition, for oil, there is the likelihood of a reduction in supplies by some of the main oil producers. Inflation may also be affected by higher than projected growth in credit to the private sector, reflecting a stronger impact of past monetary policy easing. Other Economic Variables At its assessment in November 2019, Bank of Jamaica’s forecast anticipated that, over the next eight quarters, the Jamaican economy would likely continue to reflect some slack (that is, projected GDP growth being lower than Bank of Jamaica’s estimate of potential GDP growth). The risks to this projection for real GDP growth over the next eight quarters are now balanced. The principal risk that could cause real GDP growth to be lower than anticipated stems from lower production in the construction sector as large scale projects are completed. However, higher than previously anticipated growth among Jamaica’s main trading partners could support higher domestic real GDP growth. In addition, GDP growth could be higher than anticipated in the context the Bank’s accommodative monetary policy over the last eight quarters. Other macroeconomic indicators continue to be positive. Foreign reserves remain above levels deemed to be adequate, market interest rates remain low, the current account of the balance of payments remains sustainable, labour market conditions are improving and fiscal performance continues to be strong. The next policy decision announcement date is 19 February 2020.” 1 Bank of Jamaica’s forecast horizon is eight quarters ahead as it covers the period in which changes in the policy rate has its largest impact on inflation.2 Underlying or core inflation (which measures price increases without the influence of agricultural food and fuel prices) remained low at 2.8 per cent at November 2019. www.CentralBankNews.info

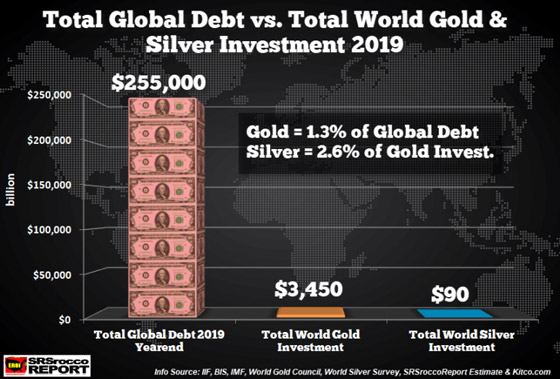

As Global Debt reached a new record high of $250 trillion this year, gold and silver came briefly back on the radar for investors. After five long years, the precious metals finally broke through key technical levels this summer. However, after the Fed started the Repo Operations in September and the $60 billion a month of “Not-QE” in October, the focus returned once again to the Bloated Stock and Bond markets.

What a drastic change from the Fed’s policy last year when it was reducing the size of its balance sheet until the stock market crashed in December 2018. Since then, the huge stock market reversal and all the additional gains have been Fed liquidity induced. Sven Heinrich continues to write and talk about this on his website, the Northmantrader.com. Here is a recent chart from his article, System Failure:

At the bottom left hand of the chart corresponds to the bottom of the stock market in January 2019 when Fed Chairman Powell caved in by ending the reduction of the Fed’s balance sheet. Since then, there have been three rate cuts, Repo Magic and $60 billion a month of U.S. Treasury purchases because there aren’t enough suckers to absorb all the new U.S. Govt issued debt.

The U.S. economy isn’t even in a recession, and the Fed is acting as if it was 2008-2009 all over again. What happens when the U.S. economy finally rolls over?? It’s going to be terrible news, especially considering the record amount of global debt. According to the IIF, the Institute of International Finance, global debt reached a record high of $250 trillion in the first half of the year. However, the IIF estimates that global debt will reach $255 trillion by yearend.

In just ten years since the 2008-2009 financial crisis, the world added another $100 trillion in debt. Now, the majority of that debt went into the Stock, Bond, and Real Estate Markets. This is precisely why the U.S. stock market has reached an all-time new high. Unfortunately, when the U.S. and the global economy finally enters into a recession-depression, the asset values will crash while the debts remain.

GOD hath a sense of humor.

We saw this happen during the U.S. Subprime Housing Bust. After millions of Americans refinanced their homes by cashing in on the equity, they were upside down with their mortgages when real estate prices plunged. The brutal truth of the market is that the DEBTS will remain while ASSETS evaporate.

In just the first half of 2019, total Global Debt increased by $7.5 trillion. Thus, global debt jumped by more than twice the value of all world gold and silver investment of $3.5 trillion:

According to the World Gold Council, World Silver Survey, and my estimate of additional privately held silver bullion, the total value of global gold investment is $3,450 billion, while silver trails way behind at $90 billion. These figures are based on 2.3 billion ounces of global gold investment and an estimated 5 billion ounces of silver. The World Silver Survey reported that above-ground silver stocks in 2018 were 2.5 billion ounces. I added 2.5 billion oz more of possible private held silver bars and coins. I doubt there is that much privately held silver, but even if we say there was 5 billion oz of silver investment held, it’s only worth $90 billion based on an $18 spot price.

As we can see in the chart above, total global debt will reach $255 trillion by the end of 2019 versus $3.4 trillion worth of gold and $90 billion in silver. Thus, the total world gold investment holdings are only 1.3% of the outstanding global debt, while world silver investment is a measly 2.6% that of gold.

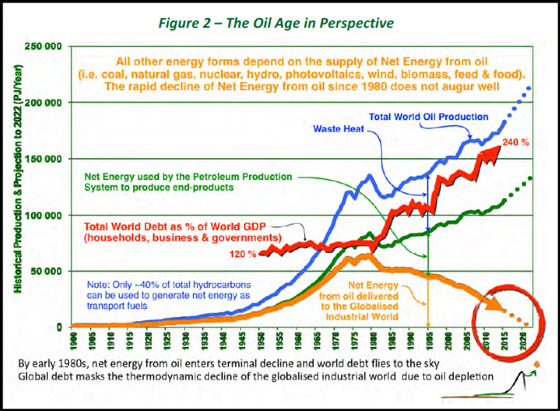

Currently, the massive Global Debt Time-Bomb isn’t impacting the values of the precious metals. This is because the mentality driving the market isn’t considering the FUTURE ENERGY needed to pay back all this debt. We must remember that Debt represents future obligations that can be paid back only when the global economy BURNS ENERGY.

The following chart from Louis Arnoux, based on work from the Hills Group provide the MAIN FACTOR that is pushing the global economic and financial economy to the brink:

This chart is very easy to understand. All one has to know is that as the NET ENERGY from oil delivered to the market (Orange line) has declined, the total World Debt to GDP (Red line) has increased. The data in the chart is a bit old, but the trend continues in the same direction. Based on the total global debt reaching $255 trillion by the end of 2019 and the estimated $88 trillion in world GDP, that equals a World Debt to GDP of 290%, much higher than the 240% shown in the chart. So, as you can see… the world continues to head towards the ENERGY CLIFF.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

So much of our research and analysis as forex traders focuses on figuring out when to get into the market. That’s why we often neglect to consider when staying out of the market is a better option.

In fact, learning how to handle when not to trade and avoid taking unnecessary risks, for a lot of forex traders, is the key to success.

The simple answer for when you shouldn’t trade is when your strategy says you shouldn’t.

There are a lot of circumstantial reasons why you should stay out of the market at particular times. After a while, you get a handle on them. But there are also some general guidelines that might help most FX traders avoid being in the market when they shouldn’t.

If it Doesn’t Feel Right, Don’t!

This might sound like common sense. But, especially for newer forex traders, there is this drive to jump on every opportunity. Even if you’re not sure about it!

No one has a gun to your head to trade. And there will always be another market opportunity coming up.

If you absolutely have to trade and can’t let a potential trade go by, then there’s probably something wrong with your money management strategy.

For many FX traders, it takes some convincing to get them to accept that they can let a trade opportunity pass and hold out for better circumstances. It’s almost like you “lost” when you decide to not jump on a trade.

However, a very important part of forex trading is risk management. And if you are unsure about a trade, you’re better off passing on it.

High Volatility

Unless you have a strategy that is specifically oriented towards trading in periods of high volatility, then you might want to stay away from the markets when there is increased erratic movement in the markets.

This is different from generally increased volatility due to more traders, for example, during the London-New York session. If there is a major geopolitical event, such as a war, or an election, the markets can react to rumors and incomplete information that can render an otherwise good strategy useless.

News Releases

Again, unless you have a strategy that is specifically built around certain news releases, major economic data can cause the market to veer into a new direction.

Many technical FX traders hold off on trading ahead of major fundamental events. These can cause high volatility and typically include interest rate decisions, NFP and GDP figures.

Holidays

When countries go on holiday, usually the major FX traders from those countries won’t be active in the market.

If a significant number of countries or a major economy’s markets are closed for holidays, it can pull a lot of liquidity from the market. This causes it to act more erratic and uncertain.

Usually, in the two weeks around Christmas and New Year’s, most major forex traders take a vacation.

This means that many trading strategies won’t perform as well during that period. Other major holidays that sap liquidity from the markets include Easter, May 1st and Thanksgiving.

Many forex traders also avoid trading on those days.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up Jp Cortez of the Sound Money Defense League joins us to discuss the latest on the state legislative front when it comes to taxation of gold and silver, an issue that is becoming more and more important for precious metals investors, many of whom are now facing the prospects of having to pay sales tax when they buy precious metals.

Jp also gives a rundown on the 2019 Sound Money Index – a rating of which states are friendly towards precious metals, and which states are the enemies of sound money. So be sure to stick around for a fascinating and informative conversation with Jp Cortez of the Sound Money Defense League, coming up after this week’s market update.

Well, as Democrats in Congress impeached the President of the United States, investors yawned. U.S. stock market averages quietly advanced to new record highs in low volume trading. Meanwhile, gold and silver markets made advances within their narrow trading ranges.

As of this Friday recording, gold prices are up a slight 0.2% for the week to trade at $1,481 per ounce. Silver shows a weekly gain of 1.5% to come in at $17.28 an ounce. The Platinum Group Metals are slumping today and are now down for the week with platinum off 1.0% to check in at $924. And finally, the leader of the pack palladium sports a spot price of $1,898 after falling by 2.2% this week.

The big question is, when will the other metals catch up to palladium? They could start on that path soon. Gold, silver and platinum are each now tantalizingly close to breaking above trading range resistance.

Precious metals have played second fiddle to the stock market this fall. Perhaps the winter solstice, which arrives on Saturday, will usher in a seasonal change of character in these markets when they open next Christmas week.

Stocks could get a Santa Claus extension to their rally. Christmas week gains are typical but not guaranteed. With the S&P 500 having gone essentially straight up for the past 11 weeks, the market is overdue for a correction.

Gold and silver, on the other hand, are overdue to break out from their sideways consolidation phase one way or the other.

The longer-term outlook for precious metals will depend largely on where interest rates and inflation head. We’ve heard in previous podcasts trends forecaster Gerald Celente say that negative interest rates are coming to the U.S. That would certainly bolster the appeal of hard money as a superior form of cash.

Other analysts believe the global negative yield bubble is an unsustainable aberration that is about to burst. On Thursday, Sweden’s central bank ended its five-year experiment with negative rates. The Swedish Riksbank raised its benchmark interest rate from slightly below zero to zero.

Other central banks may follow suit. There is little evidence that negative rates spur economic growth, but Sweden and other countries are finally seeing a slight uptick in inflation.

Other central banks, including the European Central Bank and the Bank of Japan, are still holding rates below zero. But that could change next year. If Europe and Japan are hiking rates while the U.S. Federal Reserve holds its benchmark rate steady, that would be dollar bearish.

If the Fed gets the rise in inflation it has repeatedly called for, that would be a huge potential catalyst for precious metals markets. The inflation trade has been quiet for several years, but we are seeing some signs of it picking back up late this year in commodity markets.

If inflation and interest rates instead hold steady where they’re at with the stock market continuing to advance, then we wouldn’t expect gold and silver markets to do much.

Perhaps the Trump rally has enough gas left in the tank to carry the president to re-election next November. President Trump seems to be enjoying an impeachment boost in the polls right now, but momentum will probably swing back and forth between him and his Democrat rivals multiple times in the months ahead.

The bullish dynamics for the stock market will eventually swing to the bearish side, whether before or after the election.

In the meantime, patient precious metals investors are still being rewarded with decent gains this year. And from a technical perspective, gold has quietly been in a bull market since bottoming four years ago around $1,050 an ounce.

Silver also put in a major bottom then, though its chart looks messier as it has lagged behind gold. Silver has yet to trade above its 2016 high at $21 per ounce.

However, the white metal is notorious for spiking higher rather than trending higher. When it is ready to spike again, it can be expected to deliver spectacular returns in a matter of weeks.

It’s certainly a good idea to be well positioned in silver before then. Investors will also need to be prepared to hang on for the ride. It won’t be a smooth one. But it will ultimately be rewarding when it’s silver’s time to shine and reach for new all-time highs at multiples of today’s prices.

Well now, for a look at a topic that many gold and silver investors don’t even want to think about, that being sales and income taxes, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome in JP Cortez with the Sound Money Defense League, a nonpartisan national public policy organization working to restore sound money at the state and federal level. JP is a proponent of and has studied in the Austrian school of economics and his role at SMDL as Policy Director has him regularly testifying at legislative hearings and speaking at various events around the country. His articles and analysis have appeared in many national news publications including the Washington Examiner, Huffington Post, Mises Institute, Foundation For Economic Education and many more, and he’s a frequent guest on various podcasts and national radio shows to talk about the importance of sound money legislation. And it’s a real pleasure to have him back on here with us on the Money Metals Podcast.

Jp, thanks for the time today. Welcome and how are you ?

Jp Cortez: Mike. Thanks for having me on. I’m doing great. How are things over there?

Mike Gleason: Well we’re doing well, excited to talk about this topic and as many of our regular listeners know, we had you on several months back to talk about this issue and we figured it was time to have you on again and talk about it and get an update from you on the state of the state, if you will, when it comes to sound money here in the U.S… as things are continuing to develop on that front, some of which is good and some of which is not what we would term as positive. And then we’ll also get into your group’s latest release of the Sound Money Index for 2019. But first let’s begin with having you lay out for us what your group does. What is the mission and why is there a Sound Money Defense League to begin with? Let’s start there.

Jp Cortez: Well, like you mentioned earlier, we’re a nonpartisan national public policy group and we work to restore sound money and that mostly happens on the state level, but we work on the federal level as well. So, primarily what we’re doing here is re-monetizing gold and silver by removing the taxes that surround its use, its sale, its purchase, because that’s most of the reason why people don’t use gold or silver today. It has nothing to do with its legal tender status or anything like that. It’s just that you would practically need a CPA by your side every time if you had to calculate your cost basis every time you wanted to buy a gallon of milk at the store and you’d have to go through this onerous process. So, by removing the taxes on precious metals, we hope to have the metals naturally find their way back into the system.

Mike Gleason: Talk about the successes that you’ve had there, Jp, because I know it’s been a busy couple of years at the state legislative level on the sound money front. Now there’s obviously a lot more work to be done there. We’ll get into that, but talk about some of the achievements of the Sound Money Defense League thus far, Jp.

Jp Cortez: The Sound Money Defense League was started in 2015 and since then it’s grown as a real leader on this issue we’ve been a part of and we’ve led efforts to introduce and pass legislation to remove sales tax on gold and silver in Alabama, Georgia, West Virginia, Wyoming and Louisiana, Wisconsin. In Arizona and Wyoming we’ve also worked to eliminate capital gains taxes from the sale of precious metals and we’ve also defended a couple existing exemptions this past session in Washington and Nebraska. In Washington’s case this was an exemption that was passed back in the mid-eighties that revenue hungry politicians were trying to appeal or were trying to repeal, but thankfully we were able to get that stopped and we hope this year to pick up a couple more victories in states like Tennessee and Mississippi on the sales tax issue.

Mike Gleason: Okay, so let’s get into the 2019 Sound Money Index, which you just released first. Why don’t you give us an overview of how the index was created and what it tells us about the various States about their friendliness or lack thereof towards sound money?

Jp Cortez: Yeah, the Sound Money Index is the first index of its kind where we’ve ranked all 50 states using a variety of criteria to kind of determine which states offer the most pro and anti-sound money climate. This was a project that we started last year, so this is our second annual report. In the first iteration of the Index, we used nine criteria, but and this year we’ve expanded that to 12 different indicators. We did that because we think that this gives us a more robust picture of where each state is at, where each state stands on sound money. And so the index evaluates each state’s sales and income tax policies involving precious metals. Whether a state has holds any precious metals in its pension funds or reserve funds, whether a state has passed or imposed any of these very onerous, very restrictive precious metals dealers or investor harassment laws is what we call them. And some more.

Mike Gleason: Yeah. So I wanted to dive into some of that criteria and so forth. But what did the top rank states do, right that led to their high scores on the index. And then what were those States who scored well?

Jp Cortez: This year, Wyoming, Texas and Utah kind of rounded out our top three. And these are three states that are all excellent on the issue of sales tax on precious metals. They’ve each got a full sales tax exemption on all gold and silver coins and bullion, that is Wyoming, Texas and Utah. They’ve also taken steps to exempt the gold and silver from the income tax. Utah was the first to do so, I believe. Texas has no income tax. And Wyoming, while it does not have a state income tax passed legislation two years ago now that does not allow for a capital gains tax on precious metals if an income tax were ever to be introduced.

Mike Gleason: So, what states are the worst on sound money? JP

Jp Cortez: So Arkansas, New Jersey, Maine, Ohio, Tennessee, Vermont. Unfortunately there are a couple of kind of a real baddies here. And these are the worst states in the country. These are states that levy sales tax on precious metals. They hammer you with income tax on the sale of sound money. They hold no metals in any of their reserve funds, any of their pension funds. They restrict dealers and investors with some of these crazy regulations regarding collecting personal data, reporting, regular submission to police. And these states, the ones I just mentioned are rife with these kinds of onerous laws and just generally they have high rates of taxation compared to the rest of the country. Ohio here kind of stands out last year in the first annual Sound Money Index, Ohio ranked 17th. This past year, unfortunately, Ohio voted to repeal its sound money sales tax exemption and it fell, talk about a fall from grace, all the way from 17th to tied for 49th place.

Mike Gleason: Yeah, ouch. We’re of course well familiar with that here at Money Metals Exchange, we are now collecting sales tax in a half dozen States. Ohio is one of those, this all happens in the wake of the Wayfair Supreme Court decision that forces out of state companies to charge tax and submit it to the states where there is no sales tax exemption for precious metals. Wayfair obviously was dealing with this not necessarily precious metals related, but we’re now sort of falling under law. So, there’s about 15 to 20 states that don’t have a sales tax exemption for precious metals and we and other national dealers are having to charge sales tax now and collect those in those jurisdictions even though we don’t have a physical business presence in those states. That’s what Wayfair a addressed kind of hitting those online retailers. So, this is a very important issue and passing laws in the remaining states that haven’t passed a bill exempting sales tax on precious metals yet would be huge for the citizens in those states.

But yet sales tax is not the only thing we have to deal with when it comes to taxes, Jp. You alluded to this a moment ago with some of those states that don’t have this, but we also have the income tax in most states and certainly at the federal level that are owed when there is a gain, and I say the word gain in quotes because it’s really just an illusory gain as we know because it’s not that the price of gold and silver has risen necessarily, it’s more a matter of the fact that the dollar has lost value, but yet the governments both at the state and federal level wants to tax you on the inflation that they’ve created, that’s caused that nominal gain. Talk about that Jp.

Jp Cortez: That’s right. Like you just said that this gain many times isn’t an actual gain. It’s not a real gain. It’s just a nominal gain that results from the inflation caused by the Federal Reserve. An ounce of gold is still an ounce of gold. The value of the ounce of gold hasn’t changed. It just takes more individual Federal Reserve notes to purchase the same ounce of gold. The Federal Reserve note is losing value. It’s not the gold is gaining value and yet, like you mentioned, this gain is taxed at the federal level and then again at the state level. To make things worse in states with no sales tax exemption then you’re hit with a nefarious kind of double taxation here where you’re taxed on the purchase of your metals and then taxed again on the sale.

Mike Gleason: Not to mention that the gain is at the 28% a collectibles rate to begin with, and in many cases, this isn’t collectible, this is bullion and yet it’s still taxed at an onerous 28% rate.

Jp Cortez: Yeah, that’s right. Long-term capital gains rate, discriminatorily high 28%. So, that’s taxed just as if you were talking about beanie babies or baseball cards or art. The IRS unilaterally decided that precious metals are collectibles and so now here we are.

Mike Gleason: Yeah, it’s the height of ridiculousness. I know at the federal level our good friend Alex Mooney, a Congressman from West Virginia has I believe, introduced a bill in Congress to repeal that tax at the federal level at anything you can tell us there. I do I have that right.

Jp Cortez: Yeah, that is correct. Congressman Mooney from West Virginia has introduced a couple of laws to remove these capital gains that we see here and hopefully these get passed. There are a couple of these laws that are coming down the pipes and hopefully we can kind of gain some traction and get some or one or maybe some of these passed.

Mike Gleason: Yeah, obviously many things happen at the state level and that sort of builds the momentum nationally and I know that’s where you’re focusing most of your efforts and it’s very important to do that. That’s where things often get started when it comes to change at a federal level as well.

Well, what other kinds of owner’s restrictions do states place on dealers and investors? Is there anything else that we haven’t covered aside from the tax issue that your group is focusing on, fighting and bringing to light?

Jp Cortez: Yeah, this is a new criteria that we’ve included this year on the Sound Money Index. We call it a dealer harassment laws, investor harassment laws, and some of these are really quite ridiculous. Some states require collecting your fingerprints, your physical measurements, your height, your weight, your hair color, your eye color, your social security number, other forms of identification, all of these things that the state requires precious metals dealers or sellers to collect. And then you couple that with the requirements to submit all of the sensitive information to law enforcement in some cases daily and some cases weekly. So, it’s really quite restrictive and quite pervasive. Some states have made it to where you can’t sell any gold or silver purchased from the public for a specified amount of time. In an industry like precious metals where prices are regularly changing, asking dealers to hold on to inventory for days or weeks could make a huge difference and could cause huge harm.

Additionally, if you consider that now dealers have to hold more inventory maybe than they would feel comfortable with otherwise by law, now it’s a liability. Now the dealer has to provide security, has to provide insurance to adequately safeguard these now these precious metals that they’re being forced to hold. And then I think the worst of all probably in my opinion is that a few states prohibit cash transactions when buying gold or silver. The argument being of course that sales are better tracked. Safety is a priority and so we need digital records of every transaction. But this is nearly unprecedented in American commerce. To restrict metals purchases to digitally tracked credit purchases or checks only is quite invasive.

Mike Gleason: Yeah, I couldn’t agree more. Obviously we’ve got the $10,000 cash payments money laundering, sort of restriction Form 8,300 that people have to fill out. If you’re buying a over $10,000 in cash in anything where there’s gold and silver, a vehicle or what have you, you’re supposed to submit that form if you’re taking payment that way in that amount. But yeah extending it beyond that. And lower thresholds is pretty ridiculous. There is a nearby cities here, and we’re in Idaho, which is a pretty friendly state when it comes to precious metals, but there’s a nearby city that has a lot of those laws in place. And as it stands, there’s zero precious metals dealers. There’s zero local coin shops because they don’t want to have to fingerprint everybody, submit it to the local police. Just completely ridiculous. They’ve driven several businesses out of the city completely. It’s a real shame.

Jp, it also looks like there’s zero states that have at least 10% of their reserve funds held in in gold and silver. I know you’re trying to work to change that, talk about that.

Jp Cortez: Well, frankly, the financial powers that be simply haven’t allowed for it. An allocation of gold and silver provides many helpful things to investors, and to states if they choose to invest in gold and silver, that is a hedge against inflation debt, default risks, stock market declines volatility. And yet there isn’t a single state that’s holding at least 10% of its reserves in the metals. And of course, that it is more egregious when it’s coupled with the fact that their portfolios are full of nothing but risky assets. A considerable amount of emerging market debt, risky bonds, ETFs, different trading instruments, people chasing returns rather than protecting and taking prudent care of money that retirees and savers and pensioners rely on.

Mike Gleason: Yeah, they certainly should not be risking that money and of course, gold and silver and the ultimate safe havens, gold specifically. And you would think that there would be at least some appetite for some of those states to put some of those reserves in in some kind of a gold fund or physical gold better yet. None has really done yet. I guess Texas has, is it the state teacher’s pension funds that that has some physical gold? Is that the only one that’s done that?

Jp Cortez: Yeah, Mike. That’s correct. The Texas Teacher Pension Fund, they’re holding about a billion dollars’ worth of physical gold. Wyoming considered a few measures this past year to protect some of their reserve funds, their rainy day funds, their pension funds with physical metals held within the state or near the state. And believe it or not, these measures were not received warmly by different constituencies, by the pension fund managers, the reserve fund managers, banking. There were several constituencies that were not too keen on this idea.

Mike Gleason: Imagine that, the financial elites or wall street types, not wanting to see money leave the system and go into gold and silver. I can’t say, I can’t imagine why they wouldn’t like that.

Well, before we let you go here, is there anything else you would like to share with our listeners today maybe that we haven’t covered yet? Or certain things that you see in movements of sound money that you think people should be keeping in mind?

Jp Cortez: Yeah. I think just one more note on the Sound Money Index. We’ve taken the time this year to kind of extend out what we’re doing and so we’ve scored different states on a number of interesting criteria. Some of the stuff we didn’t get to hear in this conversation, like the enforcement of gold cost contracts for example, or holding metals in state reserve funds like we mentioned, whether a state has established an in-state depository, of course Texas. And then this year we’ve included a section on whether or not a state has issued a gold bond. So, it’s really interesting stuff. We encourage everyone to check out the Sound Money Index.

Mike Gleason: Yeah, they can do that either at SoundMoneyDefense.org or on the MoneyMetals.com site as well, that information will be available there. Keep up the great work Jp in our industry, the sales tax issue has become quite a big one. So, the work you’re doing there is vitally important and we appreciate all you’re doing to defend sound money. We appreciate the time today and look forward to having you on again in the future to update us on a lot of these legislative fronts, because I know you’ll have your finger on that pulse as much as anyone and we wish you continued success in those efforts. Take care and thanks for coming on.

Jp Cortez: Great. Thanks a lot, Mike.

Mike Gleason: Well, that will do it for this week. Thanks again to Jp Cortez Policy Director at the Sound Money Defense league. For more information or to follow these ongoing sound money efforts or even to make a donation to help support the mission of sound money advancement, please visit SoundMoneyDefense.org.

And check back here next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange, thanks for listening and Merry Christmas everyone.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

On Wednesday, the US House voted to begin impeachment hearings against President Donald Trump.

However, the markets were unmoved by the developments. The focus now shifts to the Senate which is controlled by the Republicans.

There is a strong chance that the President will not be convicted.

Euro Trades Modest on Weak US Data

The euro was seen posting some modest gains on Thursday. The gains came largely on data from the US amid a lack of any fundamentals from the eurozone.

The Philly Fed manufacturing index fell to 0.3. This was well below the estimates of a decline to 8.1. The weekly unemployment claims also rose more than expected.

EURUSD Testing the Trend Line

The currency pair is consolidating below the support level of 1.1131. Price action was briefly retesting the minor trend line as well as the confluence of the horizontal price level. As long as this price level holds, we do not expect to see prices rising further.

Bank of England Holds Rates Steady

The Bank of England held its monetary policy meeting on Thursday. As widely expected, the central bank left interest rates unchanged at 0.75%. The bank did, however, cut its growth forecasts for the United Kingdom.

Besides the BoE meeting, Scotland’s DUP also formally requested for a Scottish independence referendum, which if approved could lead to a possible exit of Scotland from the United Kingdom.

GBPUSD Extends Below Support

The currency pair continues to extend its declines further. The cable fell below the support area of 1.3100. This now opens the way for further declines to 1.2960 where support is likely to be established. We expect the currency pair to maintain the sideways range within the levels of 1.3100 and 1.2960.

Gold Trades Flat Amid Lack of Fundamentals

Gold prices continue to trade mixed amid a sparse economic calendar. On Thursday, the BoE and the Norges bank kept rates steady. The Swedish Riksbank, hiked rates from -0.25% to zero percent.

But the decisions did not impact the safe haven asset. There was also no flight to safety despite the impeachment process in the US House.

XAUUSD Stays Flat

The precious metal continues to remain range bound with no direction in sight. XAUUSD remains range bound within the 1483 resistance and 1462 support. As long as this range is not breached, we expect the precious metal to remain range bound.

The longer term ascending triangle pattern remains in play for the moment. But a breakout above 1483 is needed to confirm this upside bias.

Its been an unusually quiet week for gold prices following the large move over the prior week in response to news of the US-China trade deal.

With the two sides agreeing on the phase-one trade deal, risk sentiment has been much better supported this week, limiting the upside in gold. The US has agreed to a substantial reduction in tariffs in exchange for China agreeing to heavily increase US agricultural purchases.

The trade talks will then move onto discussing the next phase of the trade deal in January. The market is hopeful that the superpowers can finally dismantle the tariffs which have been in place over the last two years. This could be a major boost for risk appetite, likely seeing gold trade lower on reduced safe-haven demand.

The upside in gold has also been capped by a recovery in the US dollar this week. Despite the continued rally in equities, the USD recouped some of last week’s losses as the market reacted with relief to the latest US manufacturing data.

While the reading was slightly lower than expected, it showed that the sector remained in expansionary territory last month. This assuaged some of the recessionary fears for the US economy.

Technical Perspective

Gold prices made a further test of the 1481.93 level which is still holding as resistance for now as price continues to correct higher within the bearish channel which has framed the sell-off from 2019 highs.

For now, we can still view the pattern as a corrective bull flag suggesting that the upside could still materialize. If the price can break back above the 1481.93 level, the key level to watch in the short term is 1522.75.

This is a major long-term pivot for gold. Above here, the focus will be on a move back up to the recent 1554.69 level.

Silver

Silver prices have tracked the moved in gold, moving higher over the course of this week’s trading. However, prices are still within last week’s range, for now, reflecting a loss of momentum in the market.

News of a US-China trade deal should see silver prices supported over the medium term through increased industrial demand. Any further downside in the US dollar should also keep silver prices supported in the near term.

Technical Perspective

Silver prices continue to hold below the 17.3408 for now, but are testing the bearish channel top. While we can still view the current bearish channel as a corrective bull flag structure, for now, bulls will need to see price quickly back above the 17.3408 level.

Below 17.3408, the next major support level is down at 16.2130. This also holds the retest of the broken long-term bearish trend line. To the topside, the 18.6397 level remains the key marker to break.

USD has continued to drift higher over the week, supported by better manufacturing data earlier in the week. Trading has been fairly light, however, ahead of the Christmas week next week which will see a big reduction in daily traded volumes.

Over today’s US session there are a few economic releases that might cause some movement with final GDP, core PCE, and personal spending all due. USD index trades 97.01 last.

EUR Higher on Friday

EURUSD has been a little higher today so far, despite the continued move higher in USD. EUR too has seen better data this week with the German Ifo business climate reading coming in better than expected.

ECB chief Lagarde recently noted that risks to the eurozone had diminished with the recent slowdown showing signs of bottoming out, which has supported EUR. EURUSD trades 1.1120 last.

UK Brexit Vote Due

GBPSD has been a little softer this week with price grinding lower, following last week’s elections rally. Today, UK MPs will vote on whether to back the PM’s Brexit deal. With a strong majority in parliament now, Johnson’s deal is expected to pass, confirming that the UK will leave the EU on January 31st 2020. GBPUSD trades 1.3029.

SPX500 Ends Week Near Highs

Risk assets have softened a little on Friday though have been well supported across the week. The trade deal is keeping risk appetite positive into the end of the year, seeing the SPX500 trading into fresh record highs again this week. SPX500 trades 3206.43 last, still above the 3199.22 level for now.

JPY & Gold Down on Friday

Safe havens have had a softer day so far on Friday with both JPY and gold lower in light of the recent rally in both equities and the USD. XAUUSD trades 1477.80 last, pulling back further from the week’s highs. USDJPY trades 109.36 last.

Crude Hold Above 60

Oil prices have had a quiet start to the day on Friday though are ending the week firmly higher. On the back of the US-China trade deal news, which has been a major supporting factor for oil, crude prices were also higher this week.

This is in response to a bullish report from the EIA which reported a drawdown in US crude stores last week. Crude trades 61.02 last, ending the week above the 60 level as of writing.

Loonie Lifts Off Lows

USDCAD has been a little firmer so far today, despite the rally in crude. The strength in USD has helped USDCAD recover some ground, though the pair is still ending the week lower. USDCAD trades 1.3136 last, having broken down through the 1.3145 level.

Aussie Ends The Week in the Green

AUDUSD has rallied again on Friday with price trading .6893 last, just off the week’s highs as of writing. The domestic unemployment rate was seen moving lower again last month, to 5.2% from 5.3% prior. Along with the US-China trade deal news, better data has helped support AUD across the week.