Almost eight out of 10 millennials now prioritize socially responsible and impactful investing, according to a new global survey.

Some 77% of millennials – people who were born in the time period ranging from the early 1980s to the mid-1990s and early 2000s – cite Environmental, Social and Governance (ESG) investing as their top priority when considering investment opportunities.

The global poll of 1,125 people was carried out by deVere Group, one of the world’s largest independent financial services and advisory organizations, across the UK, Western Europe, the Middle East, Africa, North America, Australia, India, ASEAN and East Asia.

deVere CEO and founder, Nigel Green, comments: “This survey underscores that whilst traditional factors – such as anticipated returns (10%), past performance (7%), risk tolerance (4%) and tactical allocation (2%) – are important factors in millennial respondents’ investment decision-making, they are no longer enough.

“Indeed, Environmental Social and Governance considerations now sit at the heart of that process.”

Let’s break down the ESG acronym to understand the matters that millennials deem deserving of their investment. ‘E’ is for ‘environment’ and includes issues such as climate change policies, carbon footprint, and use of renewable energies. ‘S’ is for ‘social’ and includes workers’ rights and protections. ‘G’ is for ‘governance’ and includes executive compensations, diversity of the board and corporate transparency.

Mr Green continues: “Millennials appear to be leading the charge in socially responsible and impactful investing. They are keen to look for investment solutions that are progressive and forward-looking.

“And they might be right to do so too. Research has shown that investments that score well in terms of ESG credentials often out-perform the market and have lower volatility over the long-run.”

He goes on to say: “For this reason and, importantly, because the biggest-ever generational transfer of wealth – likely to be around $30trn – from baby boomers to millennials will take place in the next couple of years, ESG investing is set to grow exponentially in the 2020s.

“As responsible investing becomes increasingly mainstream, and millennials become the major beneficiaries of the transfer of wealth, we can also expect institutional investors, such as pension funds, amongst others, to pile into ESG over the next few years.”

The deVere CEO concludes: “Environmental, social and governance issues are now the top priority for millennials.

“They understand that it is perfectly possible – and increasingly necessary – to make a profit while positively and proactively protecting people and the planet.

“These principles will fundamentally reshape the retail and institutional investment landscape in the next decade.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement

The dollar index (#DX) ended this year with a decrease (-0.36%). However, today the US dollar is growing against a basket of major currencies. The news that the phase-one trade deal between the US and China will be signed at the White House on January 15 has supported the US currency. The deal will reduce some US tariffs on Chinese goods. China, in turn, will increase purchases of US agricultural, industrial, and energy products by about $200 billion over the next two years. After signing the phase-one trade deal, Trump will go to China for further negotiations.

Today, during the Asian trading session, weak economic data have been published in China. Thus, Chinese Caixin manufacturing PMI counted to 51.5 in December, while experts forecasted 51.8.

The “black gold” prices are rising. Currently, futures for the WTI crude oil are testing the $61.25 mark per barrel.

Market Indicators

Yesterday, the US stock market was closed due to the New Year celebration.

The 10-year US government bonds yield has risen slightly. At the moment, the indicator is at the level of 1.93-1.94%.

The Economic News Feed for 02.01.2020:

– German manufacturing PMI at 10:55 (GMT+2:00);

– Manufacturing PMI in the UK at 11:30 (GMT+2:00);

– Initial jobless claims in the US at 15:30 (GMT+2:00);

By Han Tan, Market Analyst, ForexTime – The first full trading day of 2020 is upon us!

After what had been a stellar 2019 for many, market participants are making their way back after the year-end festivities to offer some equilibrium to major asset classes.

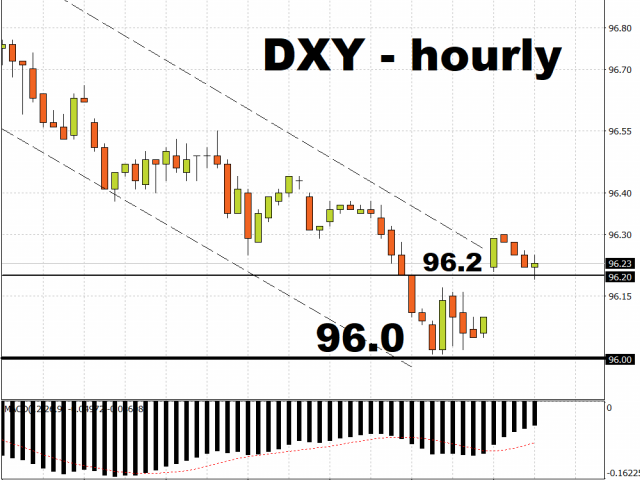

The Dollar index’s post-Christmas slide appears to be halted at 96.0 for the time being, as the DXY bounced off that psychological level to currently trade around 96.2. Still, more Dollar moderation could be in store if risk appetite shifts into higher gear on the back of a faster global economic rebound. However, given that the Federal Reserve is not expected to lower US interest rates further this year, that should gradually knock the wind out of the Dollar bears’ sails.

Safe haven gains halted as Dollar finds floor

Despite the risk-on environment, Gold and the Japanese Yen have certainly benefitted from the Dollar’s decline, gaining 3.6 percent and 0.8 percent respectively in December. After those year-end gains, Bullion appears to be settling around the $1520 mark for the time being, while the Yen’s gains have been capped at the 108.5 support level versus the US Dollar.

The market action suggests that it’s been a Dollar-driven theme that’s played out in these assets over recent weeks. Investors are now questioning whether this upward trend has run its course, considering that conventional wisdom calls for declines in safe haven assets amid heightened risk appetite. Safe haven assets are expected to adjust further as investors restore market volumes to normalcy.

Brent slides back below $67/bbl

Oil bulls have found it hard to justify the case for keeping Brent above the psychological $67/bbl level. With the Dollar pausing its decline for the meantime, Oil is lacking the catalyst for another push higher. From a fundamental perspective, investors will be closely monitoring OPEC’s decision on whether to prolong its output cuts past March 2020, amid hopes that global demand can stage enough of a recovery and stop the world from tilting into oversupplied conditions.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

US stock market ended the year on positive note on Tuesday propped by President Trump’s tweet he “will be signing our very large and comprehensive Phase One Trade Deal with China on January 15.” The S&P 500 added 0.3% to 3230.78, booking 28.9% gain for 2019, biggest since 2013. The Dow Jones industrial average rose 0.3% to 28538.44. Nasdaq advanced 0.3% to 8972.60. The dollar weakening slowed as October Case-Shiller home price index for 20 major metropolitan areas ticked up to 2.2% over year from a 2.1% rise in September. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, slipped 0.1% to 96.68 and is lower currently. Futures on US stock indices are pointing to higher openings today.

European stocks end 2019 23% higher

European stock markets pulled back on Tuesday in thin trading ahead of New Year. GBP/USD turned lower while EUR/USD continued climbing Tuesday with both pairs higher currently. The Stoxx Europe 600 ended down 0.1% on last trading session of 2019, however gaining more than 23% on the calendar year. German stock market was closed on Tuesday. France’s CAC 40 slipped 0.1% and UK’s FTSE 100 lost 0.6% to 7542.44.

Chinese stocks lead Asian indexes gains

Asian stock indices are mostly higher today with markets in Japan closed as yen climb against the dollar reversed. Chinese stocks are higher after the People’s Bank of China stated Wednesday that it would cut the amount of cash that banks must hold as reserves, releasing around 800 billion yuan ($114.9 billion) in funds for lending, effective January 6: the Shanghai Composite Index is up 1.2% and Hong Kong’s Hang Seng Index is 1.2% higher. Australia’s All Ordinaries Index added 0.1% with Australian dollar reversing its climb against the greenback..

Brent futures prices are edging higher today. Prices pulled back on Tuesday: February Brent lost 1% to $66.00 on Tuesday. The American Petroleum Institute reported late Tuesday US crude oil supplies fell by 7.8 million barrels in the previous week. The Energy Information Administration will report on Friday the change in US oil inventories instead Wednesday when markets were closed for the New Year’s holiday.

Gold strengthening dynamic while Dollar weakens halts

Gold prices are edging lower after Tuesday’s gain. The price of an ounce of gold for February delivery rose 0.3% to $1,523.10 Tuesday as the dollar wekening slowed.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of Savara opened nearly 140% higher today after the orphan lung disease company advised that the FDA has granted Breakthrough Therapy designation for the firm’s Molgradex for treatment of Autoimmune Pulmonary Alveolar Proteinosis (aPAP).

This morning orphan lung disease company Savara Inc. (SVRA:NASDAQ) announced that “the U.S. Food and Drug Administration (FDA) has granted Breakthrough Therapy designation for Molgradex, an inhaled formulation of recombinant human granulocyte-macrophage colony-stimulating factor (GM-CSF), for the treatment of Autoimmune Pulmonary Alveolar Proteinosis (aPAP).”

The company advised that “the Molgradex Breakthrough Therapy designation is based on data from IMPALA, a pivotal Phase 3 clinical study evaluating Molgradex for the treatment of aPAP.” According to the report, the data from the study was recently presented in Madrid to the 2019 European Respiratory Society International Congress.

Savara explained in the release that “Breakthrough Therapy designation is a process designed to expedite the development and review of drugs that are intended to treat a serious condition and preliminary clinical evidence indicates that the drug may demonstrate substantial improvement over available therapy on various clinically significant endpoints”.

The company’s CEO Robert Neville commented, “We are pleased that the FDA recognized Molgradex as a breakthrough therapy for the treatment of aPAP, a debilitating rare lung disease with no approved pharmacologic treatment options…We believe this designation reflects the significance of Molgradex as an investigational product that, based on the IMPALA study, has been demonstrated to improve patient outcomes. Breakthrough designation is designed to provide increased collaboration and more frequent dialogue with the FDA and is an important milestone as we work to determine the best path forward for this product.”

Savara is an orphan lung disease company headquartered in West Lake Hills, Tex., and states that “its management team has significant experience in orphan drug development and pulmonary medicine, identifying unmet needs, developing and acquiring new product candidates, and effectively advancing them to approvals and commercialization.” The company listed that “its pipeline comprises Molgradex, an inhaled granulocyte-macrophage colony-stimulating factor (GM-CSF) in Phase 3 development for autoimmune pulmonary alveolar proteinosis (aPAP), in Phase 2a development for nontuberculous mycobacterial (NTM) lung infection in both non-cystic fibrosis (CF) and CF-affected individuals with chronic NTM lung infection; and AeroVanc, a Phase 3-stage inhaled vancomycin for treatment of persistent methicillin-resistant Staphylococcus aureus (MRSA) lung infection in CF.”

Savara has a market capitalization of about $71.3 million with approximately 41.2 million shares outstanding. SVRA shares opened nearly 140% higher today at $4.12 (+$2.39, +138.15%) compared to Friday’s $1.73 closing price. The stock has traded today between $3.26 and $4.87/share on extremely high relative volume and currently is trading at $4.07 (+$2.34, +135.26%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Maurice Jackson of Proven and Probable interviews Andy Schectman of Miles Franklin Precious Metals Investments about the implications of monetary policies being implemented by central banks worldwide, and about the state of the U.S. economy.

Maurice Jackson: Joining us for a conversation is Andy Schectman, the president of Miles Franklin Precious Metals Investments. Today we will address Basel III, the state of U.S. markets and the Fed’s new bailout program, and how you may benefit financially.

Andy, you’re a big thinker, and I would say years ahead of most people in the space in your ability to critically and analytically think and cipher through the noise, which is why we’re delighted to have you on the program today. I want to begin our discussion at the 30,000-foot level, and have you share with us the implications of Basel III. Let me begin by asking, what is Basel III, and why should precious metals investors be aware of this decision-making body?

Andy Schectman: Well, first of all, Maurice, you’re too kind to say that. I appreciate that very much. As far as Basel III is concerned, I think it’s the most game-changing watershed event of my career, and I don’t say that lightly whatsoever. Let me explain. Prior to April 1, 2019, gold was considered a Tier-3 asset. What that would mean would be that a country that would own gold on their balance sheet would only be able to declare 50% of its value on the balance sheet, thereby denigrating the ability to transact international business and, probably more importantly, sell bonds. Now, Basel is the canton, or state, in Switzerland, where the Bank for International Settlements is located. Every single year the Bank of International Settlements, otherwise known as the central bank of central banks, [has] a meeting, and they invite all of the central bank representatives to Basel to discuss what’s happening, and what’s going to happen going forward.

In 2017, as the central banks take care of themselves, I believe they decided that in 2019, gold would be reclassified as a Tier-1 asset from a Tier-3 asset. You see, a Tier-3 asset would provide virtually no incentive to own it if you’re a country like any of the countries in Europethe PIGS, Portugal, Ireland, Greece, Spain, with a less-than-pristine balance sheetfor four reasons. Number one, it costs money to store. Number two, since 2011, gold and silver have moved sideways and down. Number three, there’s no interest paid. And number four, most importantly, was the denigration of the balance sheet, and how it would inhibit the ability to transact international business and write loans.

And so I believe that in 2017, when they met, they said things are going to change, and we’re going to reclassify gold as a Tier-1 asset in 2019. I say that to you because in 2018 the central banks bought more gold than at any time in the previous 55 years. In 2019, so far, the numbers reflect an 80% increase of central bank acquisition over 2018.

Putting it mildly, you have the most sophisticated, well-informed, and influential and well-financed investors on the planet rushing to accumulate gold and sell dollars. The only other Tier-1 asset prior to this year were U.S. treasuries and dollars. And so what you would have would be an incentive by the world central banks, evidenced by their selling of gold for many years, to shed gold and to accumulate dollars and treasuries. That Tier-1 asset status would make it easier to transact business and do loans, would not incur a storage cost [and] paid a rate of return in terms of interest.

The groundswell to sell gold was substantial for many, many years by the world’s central banks. And it was a tide that people were buying gold were fightingfighting the central banks for many years. And now all of the sudden they have an incentive, if you will, to de-dollarize. You don’t have to look any further than a country like Russia, [which] is shedding all of [its] U.S. Treasuries, and bought more gold than any country on the planet last year.

But even take it a step further, and look at the things that are happening on the periphery. You have the Chinese, with the Chinese petroyuan bond. They’re buying oil from Gulf states, and natural gas from Russia, paying in bond denominated in yuan that is immediately convertible into gold on the Shanghai Gold Exchange. That’s why the Shanghai Gold Exchange delivered almost 80 times more gold than the Comex did the last two years.

So you have countries that are setting up unilateral trade deals, that are usurping the petrodollar, that are reclassifying gold as a Tier-1 asset to challenge the treasury as the only Tier-1 status. You have the BRICS (Brazil, Russia, India, China, South Africa) nations setting up a system very similar to that of the Swiss system, with many of the European countries now, much to the dismay of the West, signing on to that system.

Basically what you have, I believe, Maurice, is the beginning of the end for the U.S. dollar in terms of its singular world-reserve status. You have J.P. Morgan Private Bank; they are the division of J.P. Morgan. They’re a division that works with the wealthiest of the wealth in the world, the centi-millionaires and the billionaires, who created quite a stir not too long ago by sending out a letter to all of their clients saying we want you to divest of dollars into foreign currencies and precious metals, as we believe the dollar will be challenged for singular world-reserve status in the near future.

All the pieces are being put in place, and the final piece of the puzzle, Maurice, is the Tier-1 asset change of gold from a Tier-3 status, by the Bank for International Settlements. And that went into effect April 1. So as far as I’m concerned, you’ll never see $1,000 gold ever again, and the floor is in on it, and all of the movements that we’re seeing right now is posturing, allowing the big money to reposition. They don’t want to let it go up too fast, to gain too much attention, to be crowded out of their own trade.

And I find it disturbing, alarming and grotesque that the entities that we call news services don’t tell us about things like Basel III, things that we should be knowing. And there are others that we’ll talk about later on in this interview, but Basel III being at the top of the list. I think the reclassification of gold from a Tier-3 asset to a Tier-1 asset is the most significant event in my career. Bottom line is you have an incentive and a vehicle to de-dollarize for the first time ever, and that is what’s happening.

And I think the central banks realize that the U.S. is at the end of its rope. A country that’s $120 trillion in debt, and the mismanagement of the world reserve currency has aggravated much of the world. And I think it’s time, they feel, for an alternative, and I think that’s where we’re headed.

Maurice Jackson: Andy, I think you’ve opened up a lot of eyes here, moving from a Tier-3 to a Tier-1 status. Now based on this action here, what prudent actions are your clients taking right now regarding this?

Andy Schectman: Not enough, to be honest with you, not enough. Gold’s up, I don’t know, 15%, 18% this year. That’s all as a result of central bank acquisition. Our business is actually quite good in terms of overall volume. We’ll do north of $200 million plus in sales. We’re doing just fine. We’re actually having one of our bigger years.

But the thing of it is, is that in 2011, when gold was approaching $2,000, and silver $50, we were getting 200 orders a day. And now in 2019, with gold doing very well, outperforming at the stock market in terms of total return, we’re getting 10% of that volume. But the order sizewe’ll do more volume in terms of total sales this yearin 2019, close to $300 millionthan we did in 2011 when gold was at its peak. So the bottom line, here again, is it’s emblematic of more institutional-accredited investors making larger purchases.

But the average Joe on the street [doesn’t] believe it to be true yet. And they still believe, as do most people in this country, that the road to retirement is only paved firmly with mutual funds and stock certificates. And so part of me understands that, and it’s hard to get behind a market that has been down so many years. When you take one step forward and two steps back for so long, it becomes difficult. But nonetheless, when you see a change like this, where you’re no longer fighting the largest investors on the planet, the central banksin fact they’re now joining the same side of the ledgerI guess all you just need to have are some strong fingertips to hang on and trust your conviction and your belief structure. And I think you’ll be rewarded.

You see, Rick Rule often says something to the extent of: the world deals in rhetoric, and he deals in arithmetic. And rhetoric is just that, rhetoric. And arithmetic always, in the end, finds a way to express itself. And I think this is a good example. The rhetoric that we see is of normalcy, everything’s OK, look the other way, but in the background it’s anything but that. We’ll talk a little bit about that, what’s going on here, but the central bank repositioning is a good example of that.

And the fact that no one talks about it in the media is exemplary, I think, of this phenomena where you have to almost trust your gut, and have strong fingertips, and hang on. Because I think we haven’t seen anything yet, and the arithmetic will bear that out. But the rhetoric will make it tough to trust your gut. Sometimes you just have to hope your intuition is correct and hang on tight, because it’s going to be bumpy. This is a high-stakes game, that’s for sure.

Maurice Jackson: And you were alluding to the media, and the psychological effects they can have on investors. I noticed recently on a mainstream media site regarding investing, they were talking about exactly what you’re referring to, the strong hands are hoardingthe word was hoardinggold. And I always chuckle when I say that, because when they purchased those 401Ks and those mutual funds they’re not hoarding, are they? To them it’s. . .

Andy Schectman: Absolutely. And those subtle plays on words, Maurice, are very significant. And that denotes the prepper, and the doomer and gloomer, and it has a negative connotation. And most of the mainstream analysis of gold will typically come with some sort of a backhanded compliment, even in a positive spin, and that’s a good example.

Maurice Jackson: Now let’s bring this conversation down to the 10,000-foot level and discuss the U.S. markets and the Fed. Beginning with U.S. markets, what has your attention and why?

Andy Schectman: This may be more alarming than anything we’ll talk aboutmaybe the most alarming thing I’ve ever heard actually, as it pertains to the U.S. market. So every single year the U.S. Treasury publishes a report on the status of the dollar in the markets. This year they published one, and they said some things that I find to be very, very alarming. And here again, I want you to think about what we just talked about with the media. And I want you to think, when we’re talking about this, about the Democratic candidates who have been debating and talking about their platforms. And I want you to think about these two things deeply, as I discuss what the United States has put in print and admitted in February. OK?

So the Treasury publishes a report. And they say we have $22 trillion in debt. We all know that, and that’s growing exponentially by the day. And they say we have a shortfall in Social Security of $53 trillion, and in 2034 it’ll all but insolvent. So let’s just stop for a moment. Just between the national debt and Social Security, my math says that’s $75 trillion in the hole. Now I want you to think not only about the media’s lack of attention, the candidates’ lack of interest, I also want you to think about the central banks taking care of themselves and repositioning before the crowd. And I want you to think about the fact that every media station, television, radio, magazine, newspapereverything in the United Statesis owned by four companies. And the information that they disseminate is purposeful.

But think about the central banks repositioning ahead of the crowd as we talk about this. So the U.S. government says OK, just between those two things we’re $75 trillion in the hole. Now, Maurice, a trillion seconds ago was 31,680 years ago. So when we talk about how big these problems are, the fact that it’s not front-page, center, news$75 trillion in the hole just between national debt and Social Security, Social Security to be insolvent in 2034 headlinethe fact that the Democratic candidates talk more about going after the rich, global warming or Trump, than about things that will completely destabilize the United States and destroy the lives of our children and grandchildren, is beyond me.

But it gets worse. So they said, when we take into account things like Medicare and Medicaid, and government and military pensions, our unfunded liabilities exceed $100 trillion. This is the government’s own admission. The government says we’re $100 trillion plus in the hole.But they say, waitwe have assets. Oh that’s great. They say we have $3.8 trillion in assets against north of $100 trillion in liabilities. Do you know what the largest singular asset is in the United States, Maurice, according to the U.S. government?

Maurice Jackson: No. Not knowing that report, I’m going to say it’s either bonds or gold.

Andy Schectman: Neither, actually. And this is where it gets, to me, incredibly alarming. Number three is land, $500 billion plus. Things like national parks and bridges. Number two, military, north of $1 trillion. Helicopters, military bases, aircraft carriers, bullets and the like. The number one largest singular asset of the United Statesthe land of the free, the world reserve currency, home of the brave, center of all marketsis student debt of $1.8 trillion.

Five years ago or so they passed a law that if you have student debt and you die, your children inherit it. If you have student debt and you file bankruptcy, they’ll attach your Social Security payments. You cannot get out of it. It is considered a receivable by the U.S. government. And so the largest asset of this country is student debt, and you have half of the Democratic Party trying to lobby to absolve it.

So, the bottom line is, when we talk about Basel III, and we see the most sophisticated countries on the planet, or banks or investors on the planetthey know what’s going on. And they see that, OK, so this country that we have given the privilege of being world reserve has north of $100 trillion in liabilities, against a backdrop of virtually nothing in assets. They, the U.S., don’t make anything anymore except debt, and it’s time for a change. So we need to classify gold as a Tier-1 asset so we all have a life raft before the U.S. dollar sinks. And I think the fact that this is not front-and-center news is absolutely deplorable.

And so what has my eye? That has my eye. The fact that we’re broke and we continue to print money, and it’s growing in an unabated fashion. And the rest of the world is looking for alternatives. And the worst thing that we can do is ask ourselves how much gold and silver we should own. A better question is how much of your life do you want tied up in a currency that is north of $100 trillion in the hole, that has nothing in the way of assets?

And when the rest of the world is quietly setting the stage, both in the way oil is traded, the way transactions are routed, like the SWIFT system, and now in the reclassification as a Tier-1 asset. The rest of the world is looking for alternatives to the dollar because of these things. And the question that we should be asking ourselves is how much of our wealth do we want tied up in a currency that appears to be in this much trouble? And then work backward from there.

Maurice Jackson: Andy, we’re not here to provide financial advice, but you have relationships with some of the world’s financial elite. Can you share with us how much of an allocation toward gold and silver they feel comfortable with?

Andy Schectman: I spent three summers in Zurich in the ’90s, learning our business. Our business, when we started it, was heavily wrapped up in Swiss investments. And I haven’t met a Swiss banker in my career that wouldn’t tell you in the very best of times 10% of your assets should be in gold. But let me explain something to you, and maybe the readers can think for themselves and look at this a little bit differently. Most readers, and yourself too, will probably know who Morningstar is.

Maurice Jackson: Yes, sir. The Morningstar report grading service?

Andy Schectman: Yes, that’s right. So Morningstar has a company that they purchased out of Chicago called Ibbotson, and Ibbotson is a service very similar to Morningstar, before they were purchased by Morningstar. Now Morningstar owns them. But they’re a research service, and basically they were tasked with finding alternatives to the stock market. There was a time when stocks were risk-on and bonds were risk-off. And they would say that because bonds would pay a fair rate of return, 4%, 5%, 6%, 7%.

So when you’re working, you take your money and put it into the risk-on category, stocks, earn a return. If it’s volatile it’s OK, because you’re young and working. And as you get older you take a portion of that risk-on money, and. . .move it into the risk-off category, into bonds paying a fair rate of return. And then you retire safely, comfortably. At 7% interest on a couple million dollars over time, you’re making nice money. You’re making $150,000 a year in interest. You’re fine.

So now, with interest rates at the lowest level in human civilizationand really, when we talk about manipulation, it’s been interest rate manipulation more than anything that has skewed all the markets, because the interest rate manipulation has created this illusion of prosperity in our 401Ks and in our home values.

But anyway, so what Ibbotson basically said was because of the interest rate manipulation, because interest rates are so low, the inverse correlation between stocks and bonds is gone, and they are now positively correlated. . .If we wake up one morning, heaven forbid, to see OPEC say, “You know what? We’ve struck a deal with Russia and China. They’re going to protect us as well. We’re going to offer up oil in yuan, in ruble and in euro.” Overnight, the dollar would implode. People would be dumping dollars so fast. All of these countries that are forced to buy oil in dollars would be dumped. Like the U.S. would dump dollars so fast it’d make your head spin, and interest rates would shoot up quickly, as inflation was bearing down on the U.S.

If interest rates rise it is the perfect storm to kill all of the financial markets in the United States, because the stock market is overvalued by every single metric you can think ofevery single metric. It is at its all-time high, at the lowest interest rates in the history of human civilization. And the bond market, which went from 7% in the late ’80s’90s, down to where we are now at 2%that’s an enormous bull run, one of the biggest ever. For 25 years this has been a bull running unabated. And now, with $1718 trillion in negative-yielding interest rate bonds across the globe, and the U.S. paying 2% on a ten-year, when money creation and inflation is running north of 4%, we’re basically 2%.

But if interest rates rise, it absolutely kills the stock market, because who would buy stocks at their highest level ever by every metric, when you can buy treasuries paying a fair rate of return without risk? It kills the bond market, the mother of all bubbles. If you’re loadedif you’re a corporation with a billion dollarswhere do you put your money? You go into government treasuries, because nowhere else will protect it. And even if you’re a huge corporation in Europe with billions of dollars, where do you put your money? You go into those government treasuries paying 99.5%, so you’re happy to lose a half percent and be guaranteed the majority of your money.

And so all of this big money, and all this money creation and easy money that we’ve seen over the years, and the money that’s being pumped into the system by the Fed, has gone into financial assets like bonds and stocks, creating these inequities.

The bottom line is Ibbotson came out and said the only asset class on the planet that is inversely correlated to the U.S. Stock Market [is] precious metals. So not only are the central banks divesting of dollars. . .but now you have the most mainstream reporting service on the planet saying if you want protection from a fallen stock market, you have to own precious metals, because there is nothing else inversely correlated.

And so you put it all together: You have stocks and bonds protection by buying precious metals. And you have currency protection by buying precious metalsat least that’s what we’re hoping for. And so I think the question is not how much should you own, but rather what exposure do you want to the dollar? And then work backward from there. I think anything under 20% to 25% of investible assets is foolhardy right now, to be honest with you.

Maurice Jackson: I’m so delighted that you’re here, because you’re sharing with us so many insights that we don’t hear on the financial news networks, that we don’t receive from financial planners; because I see a correlation. I get a lot of phone calls in reference to the same question: How much allocation should I have in precious metals? And then they always ask me, why is it my financial advisor doesn’t ever share that with me? Why don’t I ever hear it on these financial news networks? And I’m like, the data’s there. It’s just. . .where you’re receiving it from may not be willing to share with you because they don’t benefit from it. And it’s truly disheartening, because they should be in it for the best interest of everyone.

Andy Schectman: Well, think about it, Maurice. When I started in this industry in 1989, there were stock brokers. And in a brokerage house there may have been two or three financial advisorsthe guys that had been there for 30 yearsbut everyone else was a broker making 1% of your trade. You’d spend $1 million buying a stock, they make $10,000. And so that’s the way that it used to work, until the Internet came along and rendered brokers obsolete. Now trades are free. And so everyone’s an advisor, which is a Series 25 [test], I believe. . .It’s test on ethics. It’s the easiest test I ever passed. I used to be a financial advisor. It’s a joke. So you have to be a high school graduate or a GED, and pass a Series 7, which allows you to be a stockbroker. That’s a tough test. But to be a financial advisor, it’s 100 questions on ethics. It’s the easiest test ever, excuse me. And now, passing that one test you’re “an advisor.”

And so many financial advisors learn more and more about less and less, until they know everything about nothing. And they are the ones who perpetuate the fact that there’s only one way to retire, and that’s mutual funds and stock certificates.

And the difference between an advisor and a stock broker is a broker made money for a trade. An advisor makes money by keeping money under management. And so if you pull money out of management to buy gold that’s that much less that they’re making. So you’re taking food off your plate every time you pull money out from management. Therefore, human nature would dictate that most of the advisors, unless they are independently wealthy through a successful career, would find every alternative to recommending what’s best for the client. They call that OPM, Other People’s Money. It’s a lot easier to make a proclamation about someone else’s money than it is about your own, because when it’s your own you’re emotionally attached. When it’s someone else’s you don’t have the same vested interests.

I think you need to use your gut, but the bottom line is that 25% of investible assets minimum, to me, is a minimum that you would want to do. And quite frankly, if I told you what I really believed I’d probably lose credibility. But suffice it to say, I think 25% is a good starting point right now, becomes times are not normal, and the big money is proving that by their movements.

Maurice Jackson: Now for our audience members, yes we’re biased. We want you to purchase precious metals, by all means. But you notice the difference here is the allocation was 25% max, whereas what we were referring to is 100% allocation toward bonds and mutual funds in your 401K. That’s not being balanced at all, and so I just want to make sure we’re clear on that.

And you were referencing rates here. The Federal Reserve was a much-discussed topic on the news this month, as they announced their decision not to increase rates. But you believe the elephant in the room really is the Feds participation in overnight repos, which is another form of bailout. What can you share with us?

Andy Schectman: Well, it’s insidious. Here again, our media doing a bang-up job of telling us what’s really going on. And it’s just disgusting to me that people consider themselves well informed by reading their local newspaper or USA Today, or scouring the mainstream investment sites. And yet anyone you talk to has no idea what Basel III is, has no idea that we’re this much indebted, has no idea that a trillion seconds ago was as long as it was. And no one knows about the open market operations that are going on, and the repo programs, which I find to be tremendously frightening right now.

The repo program; now let me just kind of set the stage. In 2008, the Federal Reserve went to Congress and asked for $700 billion to bail out the banks, all at once, when Bear Stearns and Lehman went belly up. Since September, through the Federal Reserve, typically the banks would borrow from one another overnight, for whatever reason. They would borrow each other’s money, and they would do so through what’s called a repo agreement.

So I’m a bank and you’re a bank, and I happen to have IBM on my payroll, and it’s a $5560 million obligation every two weeks or whatever, and maybe tonight I’m $10 million shortI’m just using this as an exampleon top of all of my other obligations. So I would then, through a third-party intermediary, pledge a certain amount of U.S. treasuries, the Tier-1 asset, to you, and you would loan me the money overnight for 1% annualized rate. And I would then meet my obligations on payrolls. I would be made whole, and I would pay you back, and the treasuries would then be returned to my account. Simple.

Well, in September the repo rates went up as high as 10%. That’s called backing away. What that basically means is, is that the other banks who trade with one another, they don’t trust one another. They think that they’re going to go out of business and not get their money back, basically is what they’re thinking. They’re thinking thatand that perhaps the treasuries have been rehypothecated, pledged many times to other people. So the bottom line is that the banks stopped lending with one another, and interests rates started to spike on the overnight lending. And the Fed had to step in as the lender of last resort.

Now here’s where it gets frightening. Last night, I believe, the number was $365 billion that the Fed injected into the system last night, just to keep the banks alive. Every night going forward, over $365 billion. Bix Weir thinks the numbers are going to get as high as $700 or $800 billion. But they don’t have to declare it on their balance sheetsthe Fed doesn’t have tobecause it settles every day, overnight.

So the bottom line is the banks are so far under-capitalized and overextended that they need $365 billion per evening just to stay afloat. Every single evening since September this has been going on and increasing. It was $40 billion, $50 billion, $100 billion, $200 billion. Now it’s up to $360 billion and growing. And that way they don’t have to go to Congress and ask for a bailout. They’re doing it every single night. Every single night they’re pumping this money into the system just to keep the banks afloat.

Does that sound like a place you want to keep your life savings? In a system where the Federal Reserve has to quietly. . .And no one’s talking about the fact that these loans are oversubscribed, that there are more banks trying to borrow money overnight than the Federal Reserve is willing to lend. They’re not only oversubscribed, they’re growing in size, on top of their open-market operations, which are buying $60 billion a month in U.S. treasuries.

Monetization, it’s called, to try to buy the back end of the curb, to keep interest rates low, to inject liquidity into the system, which is only being put into bonds and stocks, further creating a bubble and a dislocation. The bottom line is that the Federal Reserve is pumping hundreds of billions of dollars into the banking system every night through these repo loans that don’t have to be declared because of the way they’re doing it, just to keep things afloat.

To me, look at all of the things we’ve talked about. Put them all together. You don’t think that the most sophisticated, well-informed traders on the globe know this? And you don’t think that’s why they reclassified gold? You don’t think that’s why they’re repositioning the way that they are? You don’t think that’s why the European, or the Eastern Block nations, have set up a system to usurp the petrodollar, and to usurp the SWIFT system? The handwriting is on the wall. And so when I see now the banking system, with the huge derivative exposure, the contagion would spread across the globe.

And I think there are some people who believe that this is the final stage, if you will, of a knowing attempt to blow up the system. That we never intended, we reached a point somewhere, where we never intended to pay back the debt. And we’ll milk as much infrastructure as we can, cities and bridges, and military and things, out of the system and then default. Because it’s getting to a point where it’s either inflate or diedie being default. And they’ve chosen, obviously, the inflation path, but at some point we may have no choice but just to default, as the rest of the world has not had alternatives to choose from. And it’s changing now.

This is the beginning of, I believe, the end of the dollar as the singular world reserve currency. And when you see the banks, all of which keep our money in for safety, beginning to be on thin ice the way they are right now, needing $360 billion a night just to stay afloatand the way that they’re doing it in a nefarious fashion, to keep it from being on their balance sheets and everyone to know what’s going onin other words, it’s not QE [quantitative easing] if it has a different name. These are all very ominous, dark clouds. I don’t like what I see on the horizon as it pertains to the dollar, and the future my children are going to grow up in.

Maurice Jackson: Before we close, last week it was announced that Metals.com was being sued by the state of Massachusetts. Do you have any comments?

Andy Schectman: Yeah. I think they were sued by the state of Minnesota as well. I’m almost positive. This is a federally non-regulated industry, and there are a lot of companies out there who have done a huge disservice to their client base, selling them overpriced crap, making them promises that would never happen. It’s federally non-regulated, and it means that there’s not an oversight out there to protect the consumer.

Minnesota is the only state in the United States, where we’re located, that regulates this federally non-regulated industry. We are licensed. We are bonded. We are background checked annually for this exact reason. And that’s why almost every single precious metals company outside the state of Minnesota has boycotted the state, because they don’t want to be subservient to the regulations that we have, to be, namely, licensing every year, bonding every year, background checks every year.

This is the same scenario that we have seen over and over and over again for the last several years, where precious metals companies are defrauding the consumer. I’m very proud of the fact, and I think you, Maurice, wouldn’t associate with Miles Franklin if this wasn’t true, that in 29, almost 30 years this February, we’ve never had a customer complaint ever. We have an A+ rating with the Better Business Bureau, without ever having a complaint.

And when we talk about reasoning, to buy from a company who may be a few cents cheaper across the board, these are reasons why you don’t. Because it wasn’t too long ago that it was Tulving who defrauded almost $50 million from the public, and then went to jail after that. It was Northwest Territorial Mint: They defrauded almost $35 million from the public and are in prison, or are still fighting it out in court. And then there was the one in Austin, TexasI forgot the name of it now, but he stole $35 million, and these were always the three most underpriced companies on the Internet.

The bottom line is, you get what you pay for. And there’s something to be said for working with a company with a great reputation like ours, and with a gentleman like yourself, with a stellar reputation. You get what you pay for, and part of that is accountability.

And it doesn’t surprise me that Metals.com was sued, and they’ll be many more like it. And that’s why we would recommend that you call Miles Franklincall Mauricebecause reputation is really, really important when it matters. And you never realize how important reputation is until you get screwed, and then all of the sudden you realize that being pennywise and pound foolish is never a good idea.

Maurice Jackson: Couldn’t have said it better, and thank you for the compliment sir. Prior to me joining Miles Franklin, one of the mistakes I would have made, and I couldn’t figure out, I should say, is this: I’m listening to this interview, and I look at the precious metal prices, and Miles [Franklin] is a little bit higher than a competitor. But if I go to that competitor’s website, there is no education. They are just simply waiting for Miles Franklin to educate me, and then I would go there for a lower price.

Andy, please share the website address for someone that’s interested in becoming a client of Miles Franklin.

Andy Schectman: It’s www.milesfranklin.com, and in your case, www.provenandprobable.com. But we also would more than welcome phone calls at (855) 505-1900. All of our brokers have a long tenure, and can speak to a wide range of topics from politics to economics, to geopolitical events to current events.

And what we do pride ourselves on, is accountability and accessibility. We’re accessible. I am always accessible by cell phone to my clients seven days a week, and it’s something I pride myself on. In a world that is very homogenous, we like to hang our hat on our reputation, our accountability and our accessibility.

Maurice Jackson: And as a reminder, I’m a proud licensed representative of Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio. From physical delivery, off-shore depositories, precious metal IRAs and private block-chain-distributed ledger technology. Call me directly at (855) 505-1900, or you may e-mail [email protected].

Finally, we invite you to subscribe to www.provenandprobable.com, where we provide mining insights and bullion sales. Andy Schectman, thank you for joining us today on Proven and Probable.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Statements and opinions expressed are the opinions of Maurice Jackson and not of Streetwise Reports or its officers. Maurice Jackson is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Maurice Jackson was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

The year ahead promises to be an eventful one. It will, of course, be dominated by political headlines leading up to the 2020 election. It could also be a big breakout year for precious metals.

In the second part of Money Metals’ 2020 Outlook, we’ll drill down on the fundamental and technical setup for gold and silver…

However, in this first part, we’ll set the stage by digging into the macro forces at play in the economy, monetary policy, politics, and geopolitics.

Economy

Over the summer, the mainstream financial media ran hard with the “recession” angle. A manufacturing slowdown seemed to be afoot. But the main impetus for all the recession talk was an inversion of the yield curve – putting short-term bond yields below those of longer-term bonds.

Democrats were nearly gleeful at the prospect of a recession. But such thinking proved to be premature.

The economy does not appear to be headed into recession as we begin 2020. Official employment numbers continue to come in historically strong. And GDP growth, though modest at 2.1% as of Q3, is still indicating an overall expansion.

As for the yield curve inversion, the Fed got the message and drove short-term rates back below long-term rates. The inversion still serves as a possible precursor to a recession, but it may not actually hit until 2021 or later.

Continued global economic growth in 2020 could drive a late-cycle bull market in commodities, including the metals complex.

Leading up to a recession, the energy and materials sectors tend to outperform the broad market before rolling over. Gold and silver tend to peak later, with gold often rising counter-cyclically to economically sensitive assets.

Monetary Policy

In 2019, the Federal Reserve did a dramatic about-face on interest rates. Instead of hiking, as was widely expected by mainstream forecasters, the Fed paused… then cut rates three times.

By the fall, it was engaging in massive interventions to prop up the repo market and launching what is effectively a new Quantitative Easing program.

Nobody in the financial “mainstream” saw that coming at the beginning of the year!

The Fed is now back on pause for an unknown period. At his latest press conference Fed Chairman Jerome Powell indicated he would like to a see a significant and sustained rise in inflation before hiking rates again.

Higher inflation coupled with accommodative monetary policy would potentially be rocket fuel for precious metals markets.

A weaker Federal Reserve Note “dollar” versus foreign currencies isn’t necessary for hard assets to gain, but it certainly wouldn’t hurt. The U.S. Dollar Index peaked for 2019 in late September after a modest run-up. It has since retraced and will finish the year nearly flat.

The dollar has fallen in the fourth quarter along with the QE surge in the Fed’s balance sheet. The central bank’s net asset purchases are up by $400 billion already. Its balance sheet will likely rise to an all-time record by spring 2020, further cheapening the real value of the Federal Reserve Note in the process.

Politics

There is no shortage of opinion on who will, and who should, win the 2020 election. But we’ll stay out of the political “horse race” debate that fills the airtime on all of the cable news channels hour after hour, day after day.

We note only that political prediction markets currently give the upper hand to President Donald Trump. As long as the economy doesn’t dip into recession, the smart money seems to be on Trump to triumph over a weak Democrat field.

Should the economy falter or Trump get bogged down in a new controversy that erodes his support, the political dynamics could shift – and potentially roil markets.

Several outspoken billionaires – from Ray Dalio to Paul Tudor Jones to Stanley Druckenmiller to Leon Cooperman – have each warned that a Democrat victory over Trump could trigger a stock market meltdown (especially if the victorious Democrat is a Bernie Sanders or Elizabeth Warren-type anti-capitalist firebrand).

Such an event, in turn, would enhance the safe-haven appeal of precious metals.

So far during the Trump presidency, “fear trade” demand for physical precious metals has been mostly muted. The metals have made modest gains based on other factors. But before we see truly spectacular gains in gold and silver, we will likely need some sort of economic, political, or geopolitical black swan event to shake investors out of their complacency.

Geopolitics

The big geopolitical story of 2019 was the trade standoff between the United States and China. Every week, seemingly, brought us either one step closer or one step further behind a trade deal.

Much – perhaps too much – was made of the impact of trade wars on market trends. But a favorable outcome in 2020 would certainly go toward boosting manufacturing activity and demand for industrial metals.

Other geopolitical threats loom in 2020 as well.

As the U.S. continues to ramp up economic sanctions on Russia, the Russians continue to look for ways to retaliate. One if its long-term strategic aims is to secure international trade deals outside the Federal Reserve Note dollar system. It is finding willing partners in U.S. adversaries who have been hit or threatened with sanctions.

The U.S. has shown in the past that it is willing to go to war to defend its fiat dollar.

A possible war with Iran, North Korea, Russia, or China – or a shutdown of oil production from the Middle East – would be extremely disruptive to markets and could send safe-haven demand for precious metals skyrocketing.

Barring an unforeseen black swan event or crisis, the big picture backdrop for precious metals looks constructive for another year of significant but not necessarily spectacular gains.

At some point, though, whether next year or in future years, mounting risks will propel gold and silver higher with explosive force.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

By Lukman Otunuga, ForexTime – 2019 was another action-packed trading year for financial markets, jampacked with many surprises, volatility and market shaking themes.

Investors charged into the trading year with a renewed sense of confidence after the Federal Reserve signalled further increases in US interest rates during the final weeks of 2018. However, market players across the globe were left empty-handed in January after the Federal Reserve executed one of its sharpest policy U-turns in recent memory. Not only were interest rates left unchanged at 2.5%, but Fed Chair Jerome Powell also expressed concerns over slowing growth in China and Europe, trade tensions, Brexit and the federal government shutdown. The S&P 500 and Dow Jones gained more than 7% in January despite the Fed’s caution. Those marked the biggest gains since January 1987.

In February, the International Monetary Fund (IMF) warned governments to gear up for a possible economic storm as growth falls short of expectations. Rising fears over trade tensions and tariffs, financial tightening, uncertainty related to Brexit and spillover impact from China’s slowdown prompted the IMF to lower its global economic growth forecasts for 2019 from 3.7% to 3.5%. A highly anticipated summit between Donald Trump and the North Korean leader Kim Jong-un also ended without an agreement this month – ultimately hitting risk sentiment.

Risk aversion made an unwelcome return in March as global recession fears sent investors rushing towards bonds and safe-haven assets while stocks tumbled. The Treasury yield curve inverted for the first time since the last financial crisis which triggered fears of an impending global recession and looser monetary policy. The S&P 500 concluded march gaining only 1% while Gold struggled to benefit from the risk-off sentiment, ending the month on a muted note.

Oil was under the spotlight in April after the Trump administration announced it will no longer grant sanction waivers to any country that imported Iranian Oil. The prospects of 1 million barrels per day being wiped off the markets sent Oil prices surging to a fresh 2019 high above $66.50. The European Central Bank left interest rates unchanged at -0.4% but warned of ‘risks’ to eurozone growth.

Donald Trump escalated the trade war with China in May by announcing plans to hike the tariff imposed on $200 billion of Chinese goods from 10% to 25%. China wasted no time retaliating by imposing new tariffs on $60 billion of US import. The tit-for-tat trade war fuelled concerns over slowing global growth and weighed heavily on investor sentiment. In the United Kingdom, the Brexit drama reached new heights after Theresa May announced she will step down as Conservative party leader on June 7, essentially paving the way for a leadership contest inside the party.

The Federal Reserve cut interest rates the first time in more than a decade in July, as it tried to keep America’s record-long economic expansion going by shielding the economy from mounting global risks. This move by the Fed opened the path for other central banks across the world to ease monetary policy in the face of slowing global growth. Trade uncertainty also forced the IMF to cut its growth forecast for the global economy for 2019 and 2020. It predicted growth of 3.2% in 2019, down from its April forecast of 3.3%.

Global markets tumbled around the world in August after Donald Trump threatened to impose tariffs on $300bn (£247.6bn) of Chinese goods. The risk aversion boosted appetite for safe-haven assets with Gold concluding the month 5.2% higher above $1440.

In September, the Federal Reserve cut interest rates a second time as a safety net against geopolitical risks, trade tensions and slowing global growth. The central bank also cut interest rates for the third time in October. The European Union also agreed to extend the Brexit deadline to January 31.

December was a monumental month for financial markets as the UK general elections and US tariff deadline left investors on edge. A landslide Conservative win in the general election on December 12 opened a near term path for Brexit while investors heaved a sigh of relief after Trump announced a ‘phase one’ deal. Despite the growing concerns and trade uncertainty, global equity markets performed well in 2019 with the S&P 500 gaining over 28% year to date.

As 2019 slowly comes to an end, investors may start pondering how US-China trade developments, Brexit and other geopolitical risk factors will influence financial markets in 2020. Will the new trading year be as volatile as 2019? This is a question on the mind of many market players.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Technical expert Clive Maund charts the reasons the precious metals have entered a bull market.

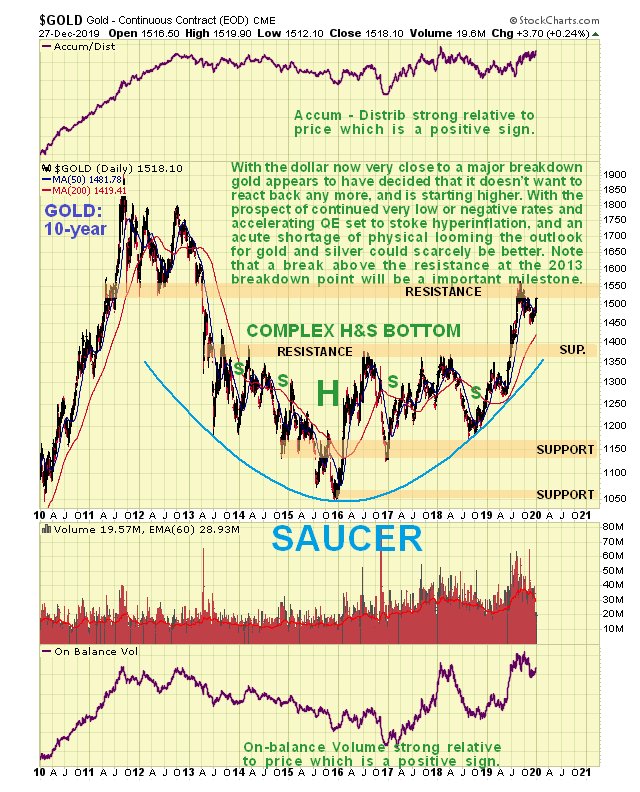

Gold is now a major bull market, as evidenced by its strong breakout from a giant 6-year long base pattern in August. The larger trend is up. We had thought that it might react back closer to the breakout point before turning higher again, but it didn’t, and started higher again in recent days over the Christmas period. This is a sign of greater strength.

There is a broad array of fundamental reasons for a bull market of unprecedented magnitude in gold, but by far the most important of them is the ongoing and accelerating destruction of currencies by central banks. They are responding to crushing debt burdens with money creation on a gargantuan scale, and we can expect them to maintain a low or negative interest rate environment and to pump money like crazy, since faced with a choice between a liquidity lockup and systemic implosion, and rampant money creation leading to hyperinflation, they are bound to follow the latter course. It is more gradual and buys them more time. While all central banks around the world are playing the same game, they will find it very hard to keep up with the Federal Reserve of the U.S., which is ramping up money creation at a frenetic pace, the effect of which will be to collapse the dollar, which is already starting to break downhence last week’s rally in gold and silver.

In late Augustearly September, gold stalled out exactly where we would expect it to, at resistance at the underside of the 20112013 top pattern, as we can on its 10-year chart below. This is a key important resistance level, because once gold succeeds in breaking above it, it will be in position to make a run at the 2011 highs. Once those are taken out, it will have nothing but blue sky above it. With the dollar looking vulnerable to dropping hard soon, all this could happen with remarkable speed. Before leaving this chart, note the bullishly aligned moving averages and strong volume indicators, with the accumulation line on the point of making new highs.

On the latest 6-month chart we can see recent action in detail, and how gold broke out of its intermediate downtrend from the September peak early last week on of all days, Christmas Eve. I have had some mails from people wondering if, because this breakout occurred on low volume on such a day, it makes it invalid. I don’t think it does and here’s why: While many ordinary investors are rushing around like headless chickens in the lead up to Christmas doing late present buying, etc., Big Money is probably much more calm and collected.

The reason for this is that they sent Jeeves to do most of the present buying in the sales back last January, and he probably had an assistant to keep driving the limo around the block for perhaps several hours before he emerged with a trolleyload of presents. Don’t laugh; this is what the wealthy used to do when they shopped at Harrods in London, where parking was almost impossible.

The point is that buying around this time is more likely to be Big Money, and we saw an example of it with the dramatic reversal in the stock market around Christmas last year. Light volume or not, this breakout looks like the real thing.

Although a tad overbought after the rally of recent days, gold is thought unlikely to react back much, if at all, before continuing higher, largely because of the fragile state of the dollar.

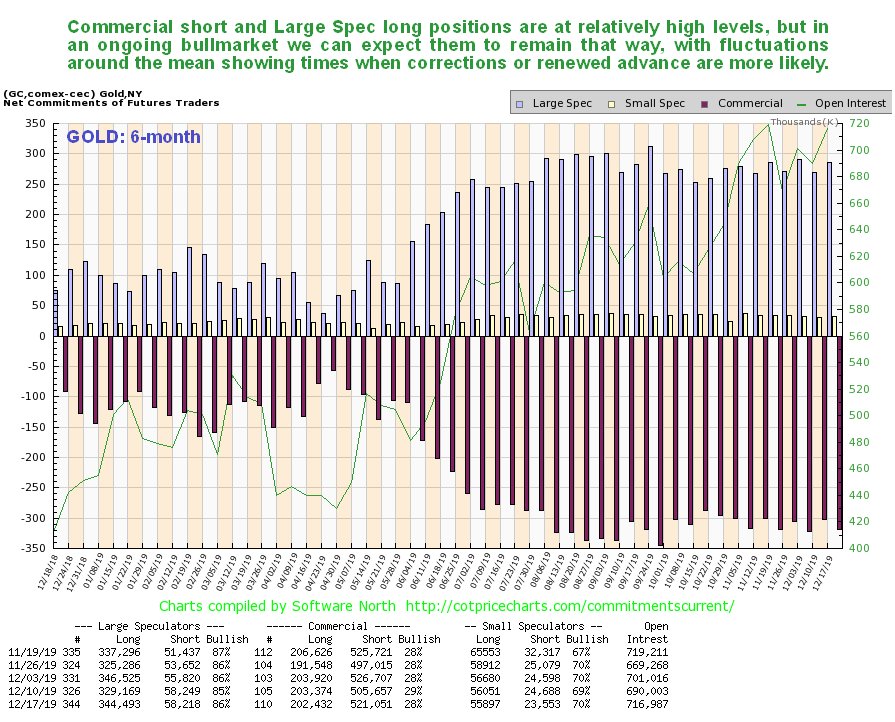

What about the COTs, which made us wary in the recent past? The situation requires a rethink given the rapidly changing environment that we are moving into. While we recognize that readings are at levels that normally lead to a significant reaction, the current setup suggests that readings are likely to stay high as this bull market progresses, only moderating somewhat on minor corrections. Of course, there is nothing to say that Commercial short and large spec long positions can’t reach higher levels in the event of gold continuing to advance. So we should be mindful of COT readings, and be aware that from now on they are likely to fluctuate around mean levels that are considerably higher than they have been in recent memory.

Now we come to the real concrete reason for gold and silver breaking out last week: the ailing dollar. Faced with a full frontal assault on it by the Federal Reserve printing money like crazy in a manner that no other central bank can hope to keep up with, the dollar is at last buckling under the strain and breaking down, as we can see on the latest 2-year chart for the dollar index shown below.

Given that it is breaking down from a long, shallow, ponderous uptrend that has been going on for about 20 months, this is viewed as a major development that could lead to a rapid and severe decline, especially as a so-called “death cross” looks imminent, where the 50-day moving average crosses below the 200-day. The last time this happened was early in 2017, and that lead to a big drop.

With the outlook for gold and silver now so favorable, it should come as no surprise that the charts for precious metals (PM) stocks are shaping up very well indeedand the good news is that the real big action hasn’t even started yet, as we see on the latest 10-year chart for GDX.

In response to one or two accusatory e-mails I have received in recent days along the lines of “You missed ityou missed the breakout!”, my response is yes, we did, but we aren’t worried because the upcoming bull market in this sector is going to be so massive that we can afford to wait for it to “tip its hand” before we go all in. The rally of the past few days is a mere pinprick compared to what lies ahead.

The main point to observe on the chart below is that GDX still hasn’t broken out of the giant, complex, head-and-shoulders bottom that has been forming since 2013, whose upper boundary is the zone of resistance around the $30 level. But it looks like it is very close to doing so, and once it does we can expect it to accelerate to the upside.

While there is resistance on the way up, it is not hard to understand that with gold set to advance in the not-too-distant future to the $3,000$4,000 area, GDX should have little trouble working its way through the resistance, approaching earlier peaks, and breaking out to new highs.

There are other important factors that point to a major sector bull market developing from here. Not least of these is the silver-to-gold ratio, whose chart is included in the parallel Silver Market update, and is reproduced for convenience below. This shows that extreme and widespread pessimism still exists toward the sector, with the ratio being at the extreme low levels it plumbed in 2003, ahead of a long and glorious bull market that ended in 2011, and again in 2008 at the general crash lows, and more recently early in 2016, when the sector was afflicted with severe depression. All those lows were followed by big and prolonged rallies, so this low should be too.

Lastly, the HUI Gold BUGS index-to-gold ratio, likewise shows that the sector is still very close to long-term cyclical lows. This ratio [has] formed a giant base pattern that may be classified either as a double bottom or as an irregular cup-and-handle base, as we see on its 20-year chart below.

The psychology behind this is simple and is as follows: When investors are fearful and negatively disposed toward the PM sector, they favor bullion over stocks, because they reason that it is a lot safer. This is, of course, true, and so at these times stocks are cheap relative to bullion, while at tops the reverse is true, with speculation rampant in stocks, which are favored over bullion. With this ratio still at a very low level, but starting to emerge from a giant base pattern, this looks like an excellent time to go overweight in this sector.

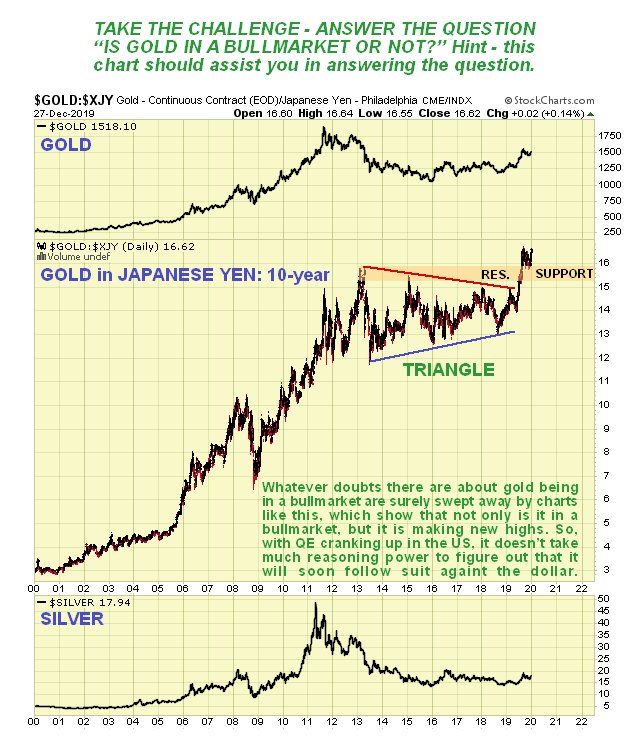

If, after reading all of the above, you are still not convinced that gold is in a bull market, the following two-step process should assist you in assuaging your doubts.

Step 1: Take a look at the following chart of gold in Australian dollars, and answer the question, “Do you think this is a bull marketyes or no?”

Step 2: Take a look at the following chart of gold in Japanese yen, and answer the question, “Do you think this is a bull marketyes or no?”

Article originally published on CliveMaund.com on Sunday, December 29, 2019.

Clive Maund has been president of www.clivemaund.com, a successful resource sector website, since its inception in 2003. He has 30 years’ experience in technical analysis and has worked for banks, commodity brokers and stockbrokers in the City of London. He holds a Diploma in Technical Analysis from the UK Society of Technical Analysts.

Disclosure: 1) Statements and opinions expressed are the opinions of Clive Maund and not of Streetwise Reports or its officers. Clive Maund is wholly responsible for the validity of the statements. Streetwise Reports was not involved in the content preparation. Clive Maund was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Charts and graphics provided by the author.

CliveMaund.com Disclosure: The above represents the opinion and analysis of Mr Maund, based on data available to him, at the time of writing. Mr. Maund’s opinions are his own, and are not a recommendation or an offer to buy or sell securities. Mr. Maund is an independent analyst who receives no compensation of any kind from any groups, individuals or corporations mentioned in his reports. As trading and investing in any financial markets may involve serious risk of loss, Mr. Maund recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction and do your own due diligence and research when making any kind of a transaction with financial ramifications. Although a qualified and experienced stock market analyst, Clive Maund is not a Registered Securities Advisor. Therefore Mr. Maund’s opinions on the market and stocks can only be construed as a solicitation to buy and sell securities when they are subject to the prior approval and endorsement of a Registered Securities Advisor operating in accordance with the appropriate regulations in your area of jurisdiction.

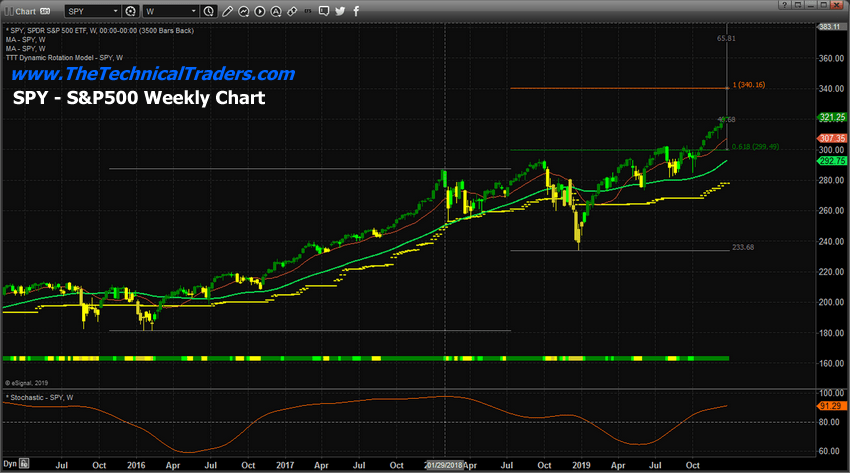

By TheTechnicalTraders.com – The US stock market has recently rallied throughout most of the last year after the very deep downside price rotation in late 2018. Our researchers believe there is a very high likelihood of this trend continuing in early 2020, yet we would need to see confirmation across various broader indicators before we could determine the strength of this upside price trend.