2020 kicked off with a spike to Oil prices, as a sudden escalation in geopolitical concerns permeated market sentiment following the US airstrike in Iraq. WTI crude briefly breached $63.80/bbl as it claimed a year-to-date gain of 3.26%, while Brent broke above $69.00/bbl before moderating its way to a 3.94% gain so far in 2020.

The heightened tensions in the region should keep Oil prices elevated over the near-term, as market participants brace for any further moves by either Iran or the US that could ramp up supply-side concerns. As such fears gather a bigger crowd, that could easily send Brent well above $70/bbl and WTI past $65/bbl.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

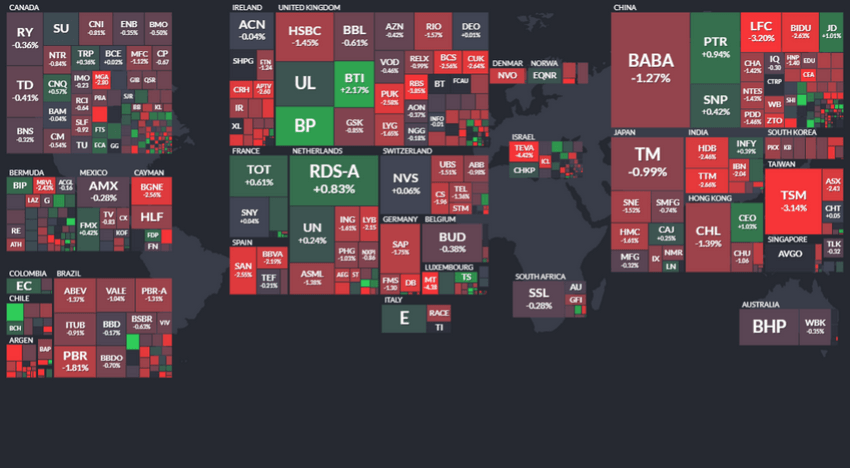

The US Stock Market contracted in early morning trading on Friday, January 3, by more than 1% after news of the missile attack in Baghdad targeting a top-level Iranian military General and others. After the attack on the US Embassy in Iraq last week, President Trump issued a strong warning that the US would act to protect its people throughout the world and Iran scoffed at this message. It would certainly appear President Trump means business and won’t hesitate to stop terrorists from acting against the US – no matter where they are in the world.

This news, overnight, pushed Oil, Gold, Silver and most precious metals higher. The fear factor associated with the unknowns of what may come from these actions shot through the roof over the past 24 hours. The global stock markets contracted by a fairly strong amount in Friday’s trading. Most global markets were off by 0.75% to levels well over 1%.

Global Market Selloff After Missle Strike – Canada, Brazil, China, UK…

The real question skilled technical traders must ask themselves is this “will this turn of events prompt a change in investor expectations/thinking over the next 12+ months”?

I can remember what happened in the markets and the US economy in 1991 when Desert Storm happened. Because this was one of the first US military efforts that were televised almost 24/7, almost immediately people were suddenly distracted by these war images and videos. They were entranced by the actions taking place half-way around the world. Local economies slowed because of this change in consumer sentiment and certain businesses struggled as their customers stayed home and watched TV.

A similar type of event happened after 9/11. The United States was in shock. People still attempted to conduct life as normal, yet our objectives changed. We lost a bit of that care-free American attitude that we had in place before the 9/11 event. We were more solemn, more conservative, more reserved in our daily lives. Could something like this happen if Iran (and neighbors) attempt to retaliate against the US for this missile attack? Could this change the thinking of consumers and investors as concerns about re-engaging in a Middle East conflict arise?

US Market Sold Off on Missile Attack

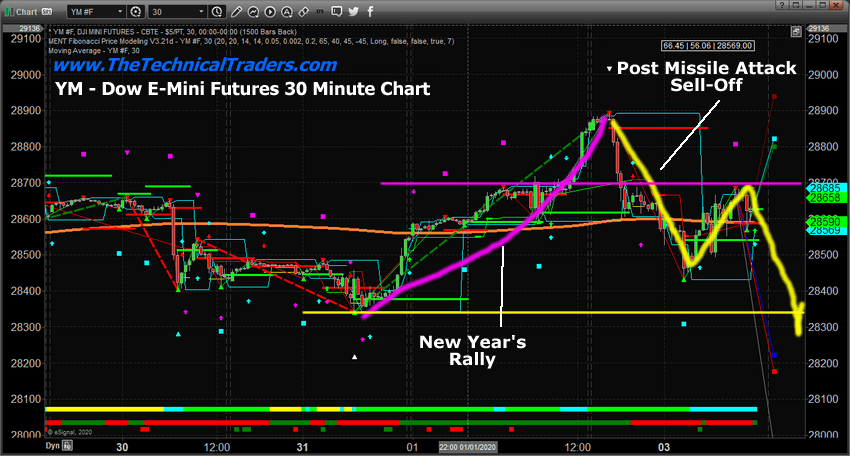

The US stock market contracted fairly strongly in early trading on Friday, January 3, 2020. Yet, by afternoon trading, support had pushed most prices off the lows. We authored a research article recently that suggested traders were very emotional near the end of 2019. We believe these emotions could continue to haunt the markets in various ways over the next 10 to 25+ trading days. One thing we are concerned with is a change in price trend sometime between January 13 and January 25. We believe these dates could prompt a major change in price trend and direction in the near future.

We don’t have a confirmation, as of yet, that any major trend change is taking place – but we feel it would be unprofessional to not warn traders that an event like this could dramatically change the way traders view future expectations. We really have to understand one key factor about investing and trading – trends are the results of investors/traders believing the future revenues and results of a company, stock or economy will product greater or weaker returns. If investors believe the returns will be greater, then the trend tends to move higher. If investors believe the returns will be weaker, then the trend tends to move lower.

Event Could Change Equities Market Outlook – Dow Jones Index

Could this new event change future expectations for traders and investors? How will extended uncertainty or military engagement alter trader’s expectations over the next 12+ months?

Right now, we want to urge our followers to protect their open long positions and watch carefully as this event unfolds. We don’t have any confirmation that a trend change is taking place. If the YM price fell to levels below $28,000, then we would consider recent support near $28,350 breached and begin to take a look at other price modeling systems.

We suggest our followers read the following research post from the end of 2019. This will give you a better understanding of what is really happening right now and what would be needed to push the markets into a new bearish trend in early 2020.

As we warned throughout most of 2019, we believe 2020 will be an incredible year for traders with extended volatility and returns. You really don’t want to miss these bigger price moves when they happen. Our precious metals calls throughout all of 2019 were nearly perfect and our recent Gold calls have nailed this big move. Get ready – 2020 is going to be a great year for skilled technical traders.

With over 55 years of technical trading experience, we have been through a few bull/bear market cycles, I have a good pulse on the market, timing key turning points and what to buy and sell for both short-term swing trading and long-term investment capital. The opportunities are financially life-changing if handled properly.

I urge you visit my Wealth Building Newsletter and if you like what I offer, join me with the 1 or 2-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own.

Chris Vermeulen Founder of Technical Traders Ltd.

NOTICE: Our free research does not constitute a trade recommendation or solicitation for our readers to take any action regarding this research. It is provided for educational purposes only. Our research team produces these research articles to share information with our followers/readers in an effort to try to keep you well informed. Visit our web site TheTechnicalTraders.com to learn how to take advantage of our members-only research and trading signals.

Happy New Year, and welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up we’ll here part two of an interview Money Metals president Stefan Gleason did with Alan James on the Sustainable Money Podcast. Stefan gives some more advice on what to look for when choosing a precious metals dealer, when and how to sell when the times comes, and also talks about some of the ins and outs of gold and silver IRAs.

Don’t miss the conclusion of this informative interview, coming up after this week’s market update.

Precious metals markets have opened the New Year with some nice gains. Metals prices rose across the board yesterday and are adding to them today after U.S. drone strikes in Iraq killed Iran’s top military leader.

Concerns about a wider military conflict with Iran and the potential for disruptions in global oil supplies are weighing on global equity markets and boosting oil and gold prices.

Gold is now building on the solid returns recorded in 2019. Last year, gold gained 19%. Silver was up over 15%. Platinum emerged from deeply depressed levels to post a 22% yearly advance. And palladium led the pack in 2019 with a gain of nearly 60%.

The prospects for precious metals to match or possibly exceed those numbers in 2020 look promising. More on what will drive hard assets this year in a bit. But first, let’s review this week’s action.

Gold prices are up 2.4% this week to bring spot prices to $1,549 per ounce. Silver checks in at $18.14 an ounce after rising 1.7% since last Friday’s close. Platinum is powering ahead by 4.0% for the week to trade at $988. And finally, palladium is packing on another 4.3% to trade at a lofty $1,993 per ounce as of this Friday morning recording.

Well, speaking of lofty, the S&P 500 traded at a new record high to ring in the New Year before selling off here on Friday. The biggest component of the blue-chip index is Apple. It now sports a market capitalization of an astonishing $1.3 trillion. That’s more than the entire GDP of Mexico. It’s more than the entire GDP of Israel, Ireland, and South Africa combined!

Apple’s market cap is now bigger than the entire energy sector of the S&P 500 and dwarfs the mining sector. At some point, investors will have to ask themselves whether the natural resources that make technology possible are being undervalued.

Could the world as we know it continue if Apple suddenly folded and stopped making iPhones? Probably. An Apple-free world would be an inconvenience for a lot of folks, but they’d quickly flock to other device makers eager to fill the void.

If the entire mining sector or energy sector went under, the world economy simply could not function.

Last year saw a wave of bankruptcies in the oil patch. Marginal players laden with debt couldn’t make it in a brutal environment for the industry. The fracking boom is slowly going bust, and that will likely mean a drop off in domestic production in 2020.

A similar problem afflicts the beaten and battered mining industry. Mines have been depleting their reserves. They haven’t had the incentive to develop new projects given low spot prices and geological challenges due to declining ore grades.

Silver in particular is likely to face a fall off in mining supply perhaps lasting for years. Most so-called silver miners are primarily in the business of mining other metals such as lead, copper, nickel, zinc, or gold. They only mine silver as a byproduct.

The lack of a healthy primary silver mining industry can work to the advantage of physical silver investors. It means that supply will be tight, and even a slight uptick in demand could exert enormous upward pressure on prices.

Silver bulls will be eyeing the $20-$21 overhead resistance zone. The market made a move toward $20 an ounce last summer before getting slammed down. Once silver breaks through that multi-year line in the sand, the technical path could be clear for a run toward its old record high.

Broader inflationary pressures are building. Wages will be on the rise thanks in part to a host of minimum wage hikes going into effect at the state level. And the Federal Reserve will keep pumping fresh liquidity into the financial system with reckless abandon.

In 2019, the Federal Reserve did a dramatic about-face on interest rates. Instead of hiking, as was widely expected by mainstream forecasters, the Fed paused… then cut rates three times.

By the fall, it was engaging in massive interventions to prop up the repo market and launching what is effectively a new Quantitative Easing program.

The Fed is dropping helicopter money into the Treasury bill market, monetizing government debt through its network of dealers.

The central bank’s net asset purchases are up by more than $400 billion already and its balance sheet will likely rise to an all-time record by this spring, further cheapening the real value of the Federal Reserve Note in the process.

Fed Chairman Jerome Powell isn’t even trying to hide the fact that his goal is to engineer higher rates of inflation. During his last press conference, he said he would like to a see a significant and sustained rise in inflation before hiking rates again.

He wouldn’t dare hike in the midst of the election campaign season, barring some extraordinary circumstances.

So, the potential for a major acceleration in inflation this year certainly exists. Higher inflation coupled with accommodative monetary policy would potentially be rocket fuel for precious metals markets. Moreover, rising geopolitical risks could serve as a catalyst for safe-haven buying.

Will it be the “roaring 2020s” for hard assets investors? Time will tell. But for now, anyway, the outlook does look bullish on multiple fronts.

Well now, without further delay, here’s the conclusion of Money Metals president Stefan Gleason’s recent interview with Alan James on Sustainable Money. And we’ll pick up the conversation with Stefan giving some incredibly important advice on what to look for when choosing a precious metals dealer and talks about the dangers of what can and has happened to those who don’t do the proper due diligence.

Stefan Gleason: It is quite rare, but there have been a few horror stories, Tulving being an example of that. We are very competitive, I’m not going to say that on every product at every moment we’re the lowest price, that’s definitely not the case. However, I guarantee you that with our company, you’re going to get delivery, you’re going to get it fast, you’re going to get added value of content and we always over deliver on our promises, not under deliver and that is extremely important. Particularly when you’re asking somebody to send money somewhere else with the expectation that they’re going to receive their gold and silver.

Now some people will go to local dealers and I don’t want to discount that because that’s certainly something that people are able to do successfully. I would say that a lot of times the local dealers are at a disadvantage because they’re not as sophisticated as a company like ours or some of our competitors. They may not be hedging. They may be exposed to market more than they should be and they may not have access to the lowest cost inventory, so the pricing may not be the best.

Alan Stroup: Stefan, I know there are some consumers that are concerned about several thousand dollars let’s say worth of gold and silver being shipped to them in one by one either UPS or the United States Postal Service or Fed Ex or whatever. How does your company ship and how reliable is it?

Stefan Gleason: We ship virtually everything by the US Postal Service. And of course these are boxes that are not marked with their contents. You can’t source it. It’d be very difficult to determine where it was coming from exactly. The return address isn’t tied directly to our name. So, there’s some anonymity there and I think most wholesalers and retailers also are pretty smart about their shipping practices. Most do use US Postal Service. Some use FedEx or UPS. That’s not the most cost effective and it’s also not even the most secure. Believe it or not, US Postal Service has been extremely reliable when it comes to delivering precious metals. We’ve shipped tens of thousands of orders every year and had very few losses.

Now I’ll also say in our case and I think our competitors are similar. We ensure everything we ship and so we have a big insurance policy. If anything gets lost, and it isn’t received and signed for by the recipient, then there’s an insurance claim and we’ve had some of those of course. But it’s remarkably reliable and I hate to say that because it’s a quasi-government enterprise. It kind of rubs me the wrong way to say that the Postal Service does a good job. I don’t think they do in general but when it comes to our success and getting things successfully shipped quickly and cost effectively, the US Postal Service has done very well.

The other options are UPS and FedEx and they’re not bad either but they are more expensive and not necessarily faster. And fast delivery is actually quite important to people and important to us. We don’t like people to wait for their precious metals. I think people are already a little bit anxious particularly on the first purchase. As one of the reasons is that they’re buying previous metals is they’re concerned about what’s happening, they’re concerned about the dollar, they’re concerned about our country and if it’s their first experience buying precious metals, they’re probably nervous about that too. So, we are really trying very hard to not only delivery quickly but hold the person’s hand, make sure the communication is very clear, very frequent so that they understand where their order is and when it’s arriving.

Alan Stroup: How does the average person learn to trust the dealer or organization that supplied the coin or bullion? And doesn’t that have something to do with the conversations that take place during the purchase? In other words, the phone consultation?

Stefan Gleason: Yeah. Well, our company and we’re not the only ones, but again I think we’re one of the best when it comes to this is that we’re not trying to make a sale. Our sales associates are really just they’re people there to educate and guide the person. There’s no pressure. It’s not a commissioned situation where they’re trying to sell something to you. They’re there to help you understand the choices and make the best decision for you. So, I think that tone is definitely one thing that has done, has been a very important part of our growth as a business. We are not into making a sale, selling somebody something they don’t want and of course we don’t even deal with and actively really crusade against this whole rare coin thing. This bait and switch thing that’s been giving our industry a bad name and has been ripping a lot of people off. We won’t even sell those types of items. We don’t stock them. The only time that you’ll see any kind of rare or numismatic coin being sold by us is when the price on that has fallen to basically its melt value, at which time it’s actually a pretty good deal to buy.

So I think education, content, communication, no pressure, meeting your commitments… just developing that relationship so look for companies that do that.

Alan Stroup: Okay. So, people have invested, they’ve got their gold and silver or gold or silver or both, insurance policy if you will, the big question is when do you liquidate? When do you know when to sell?

Stefan Gleason: Right. Well first of all if you’re buying this because it’s financial insurance, I think you’ll probably always own some of it. Now, it just so happens as priced in dollars, still we think that precious metals are way undervalued to what they will be at in the coming years as things unfold. But I would think that you know people will always own, once they understand why they own it, they’ll always own some. Now that doesn’t mean that they may want to liquidate some of it if the price rises or if they need access to cash. Some might even you know at some point in a really bad situation, you might even instead of selling it, you might be spending it. It’s certainly possible. It’s happened in other countries.

Alan Stroup: Failure of the dollar, yeah.

Stefan Gleason: Venezuela has got a gigantic implosion going on right now. Argentina’s had it. Zimbabwe. So, in that kind of situation, you know that could actually become your money. But at the end of the day, you do want to have the ability to sell it. You want to be able to know when and how and where to sell it. Right now, I don’t think you should be selling precious metals. You should be buying it but the bottom line, unless you have a specific reason that you need access to cash. The bottom line is that our business and most dealers like us will both buy and sell. And I mean we’re a dealer. We’re not just a retailer. We’re a dealer. We buy and we sell. All day long. Whenever sell something, we replace our inventory. We always have a positive amount of precious metals available and as we sell whatever we sell, we replace it.

And we wouldn’t be selling if we couldn’t be buying because we don’t want to be out precious metals either. So, if you were to sell your precious metals, it’s really quite straight forward. It’s much like buying them. You lock a price…

Alan Stroup:Over the phone, right?

Stefan Gleason: Over the phone or on our website you can actually sell on our website back to us and then you ship us the metals and then we wire or send you a check or ACH credit funds to you as soon as we receive them. So, it’s a pretty straight forward process. You can also go down to your local coin dealer and sell there. There are other ways to sell but you know hopefully people are not looking to sell unless they really have to because we probably are going to see some pretty big gains in precious metals as we’ve seen over the last fifteen years, but you need to have that liquidity and we provide that and so do our competitors.

In fact, we’d rather buy from our customers than from mints because this is a very, very small margin business to begin with if you’re selling the right kind of stuff, like bullion as opposed to the rare coins which is you know has huge margins for the sellers but it’s not a good deal for the investor. So, that extra one or two percent that we can make on buying a product back from our customer instead of having a new one minted is great. So, we would love to be buying more metal from our customers even though we quite frankly don’t think it’s a good time for them to be selling but we will absolutely buy and we’ll offer them a good price. Usually at or above the spot price depending on the product and we pay quickly.

Alan Stroup: Stefan, briefly, I want you talk about the types of events that might precipitate liquidating all or just some of your gold and/or silver product.

Stefan Gleason: Well, if you see huge gain in dollar terms, then it doesn’t hurt to sell a little bit and take some money off the table. Depends on how much you own. I mean if you own a hundred percent of your first of all, nobody should have all their money in gold and silver, just like they shouldn’t have it in anything else. But ten or twenty percent is a very reasonable allocation and we recommend that people do look at having at least that much or in that range I should say. But there may be a point where gold has gone to five thousand dollars an ounce and your ability to turn that into some other asset maybe a piece of real estate or pay off a loan or whatever, there are reasons to do that but I would never let go of your full position because part of it is insurance and you never know what’s going to happen.

If we have a total collapse or breakdown, you’re going to be happy that you have gold and silver, I can guarantee it. And if we don’t have it, I think you’re going to be happy as well as you would be if you’d owned it over the last fifteen years.

Alan Stroup: Earlier we discussed this but is there a best place to liquidate gold and silver or a list of the best places to liquidate gold and silver?

Stefan Gleason: I don’t think there is a list unless if you do a search sell silver or sell gold, you’ll probably find again some of our competitors and us. You’ll probably find the “we buy gold” type people, I would steer away from those because they’re going to offer you a huge discount to the spot price.

You want to sell to somebody like us or to one of our competitors who are able to offer you probably close to spot if not more than spot for that thing. So, stay away from the “we buy gold” type places. You might get eighty percent, seventy percent, sometimes jewelry they give you forty, thirty percent of its melt value. Don’t sell to places like that. Sell to somebody like us. Now we don’t buy jewelry so you’ll have to find other options for that. But you want to sell to somebody like us who makes a market in these things.

Alan Stroup: I’ve seen a lot of TV ads about owning precious metals in your IRA. How does that work?

Stefan Gleason: Well it’s a great option for people who have most of their money. Most of the money tied up in IRAs. First of all, I think it’s important for everybody to own some precious metals outside of their IRA. But if a lot of your money is in IRAs then by all means, make sure you get some precious metals and that’s a great way to do that. The way that works is that you cannot take physical possession of the metals without jeopardizing the IRS considering it to be a distribution and causing your entire IRA to be subjected to taxation. And there are some people out there who have been talking about home storage IRAs and that is a very risk approach and we do not recommend it.

We have some customers that want to do that because they want to have it in their house but I think it’s not worth the risk considering the IRS is starting to pay attention to that. There was an article recently, in the last few days I believe, in the Wall Street Journal which referenced this that the IRS is starting to pay a little more attention to this concept of a home storage IRA so let’s just assume that you don’t that.

The way it works then is that you would set up a IRA with a self-directed IRA provider and then you would roll IRA funds over to that self-directed IRA and there are several options. We have them on our website. They’re independent companies of us. So, you have your money in your IRA, in a self-directed IRA account and then you line up a with a dealer like us to purchase precious metal on behalf of your IRA and then you have it stored at a depository or other facility and we have recommended storage facilities that we can provide people. And so, your IRA pays for the order and then the metals are shipped to your IRA’s depository account where they are stored securely. And then in reverse, when you want to liquidate, you sell back to us or whoever. You don’t have to sell back to us if you bought it from us, you can sell it to anyone else and the metals get sent to them or us and then you’re paid, your IRA is paid back and then you move on to whatever you’re doing. Maybe distribute the funds or buy some other asset.

The nice thing about owning precious metals in an IRA is that capital gains are sheltered. So, unfortunately precious metals are taxed under federal law at a discriminatory high twenty-eight percent long term capital gains tax rate.

Alan Stroup: Any chance of that changing?

Stefan Gleason: There is a chance. We have a project, a side project, called the Sound Money Defense League, which is looking at public policies at the state and federal level. There has been talk about introducing a federal bill to repeal that. There isn’t one pending but I would say don’t plan on it but it’s certainly unjust. First of all, this is money. It’s not even, it’s not property. It’s money and the gains that you have to the extent you have gains, a lot of them are not real gains, they’re nominal gains. They’re gains in the terms of dollars but remember the dollar is being devalued by the day so the whole idea of having to pay taxes on gains on precious metals is an infringement to your financial freedom and the concept that gold is money because you know taxing you for holding money, for buying and selling money… for exchanging your gold which is money for Federal Reserve notes, which really isn’t money but they call it money and that that’s somehow a taxable event.

When a lot of that gain is really just a result of the devaluation of the Federal Reserve note in proportion or relation to the gold. So, it’s really an unjust system but I wouldn’t plan on it but the IRAs are a great way to shelter yourself from that taxation.

Alan Stroup: We’re about out of time and I have two more questions I want to get in here quickly. Should you own physical metal or shares of money backed exchanged rated funds?

Stefan Gleason: Now if you’re a trader, then maybe the ETFs aren’t a bad idea for you because of the transaction cost but there is significant counter-party risk involved in the exchange traded funds. Even if they are gold backed, where they supposedly own the bars or the physical metals somewhere but you don’t own direct title to those things. When you own it in your IRA or you own it personally, you own direct title and that’s one of the main reasons that you own previous metals is to eliminate risks. So, introducing risk into your insurance investment is not probably a great idea. So we definitely don’t think that you should be putting significant amounts of money into gold or silver ETFs. And the fees every year end up being similar if not higher to just owning the metal outright and storing it if that’s what you want to do.

So, ETFs are a proxy for gold. They are in many cases supposedly backed by gold but you don’t have direct title and there are risks involved in that. And you can’t get your hands on it.

Alan Stroup: I think that we’ve given, had a very good educational seminar here but what sorts of additional things besides listening to this, what sorts of education can the average person do for themselves to be better prepared to consider precious metals investing?

Stefan Gleason: Well first of all, I’d encourage people to get on the Money Metals Exchange email list by going to MoneyMetals.com. We publish several articles a week of original content and commentary on the markets, on the Federal Reserve, things that are impacting your money and your investments. We do a weekly podcast. We have a lot of great guests. So that’s one thing, get educated. Start looking at some of the websites including ours. Get up to speed, but most importantly start by owning a little bit of precious metals. If you don’t own them already, get started as soon as possible. You really can’t afford to wait and I’ve found that just putting a piece of silver in somebody’s hand, it kind of gets a process started in their mind. You start thinking about what is value, what is money, what gives money its value. What is the system of the Federal Reserve that we have? How does this all work?

That’s how it started for me about eighteen years ago so I think just getting into the market and start paying attention and you’re going to make lots of progress.

Alan Stroup: Stefan Gleason, president of Money Metals Exchange that’s at MoneyMetals.com. This has been another edition on our Sustainable Community Summit, entitled Gold and Silver Buying Made Easy and I hope that we were able to make it easier for you. I’m Alan James, thanks for joining us.

Hope you’ve enjoyed that interview, and that will do it for this week. Be sure to check back here next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange. Thanks for listening and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

The transaction is briefly reviewed and assessed in a BMO Capital Markets report.

In a Dec. 23 research note, BMO Capital Markets analyst Jackie Przybylowski reported that IAMGOLD Corp. (IMG:TSX; IAG:NYSE) agreed to sell its 41% interest in the Sadiola gold project in Mali to Allied Gold for $31.1533.65 million plus payments for two future sulphides-related milestones there. The deal is expected to close in April 2020.

“This is a fair price as the transaction is in line with (or slightly better than) our $30.5 million net asset value for the asset,” Przybylowski commented and summarized the deal.

IAMGOLD’s co-owner of Sadiola, Ashanti Gold, also agreed to sell its 41% interest, for an equal amount. (The Mali government owns the other 18%.)

The total consideration going to IAMGOLD for Sadiola, its founding asset, will consist of $25 million, up to $2.5 million in cash to account for the cash balance at the asset and $6.15 million in a cash dividend. The two milestone payments are $12.5 million on production of the first 250,000 ounces and $12.5 million on subsequent production of the same amount, all from the Sadiola sulphides project.

Przybylowski noted that IAMGOLD intends to use the proceeds to fund future growth projects that include Saramacca at Rosebel, slated to commence production in 2021, as well as Côté Lake and Boto.

BMO has a Market Perform rating and a US$3.75 per share target price on IAMGOLD, whose stock is currently trading at around US$3.77 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from BMO Capital Markets, IAMGOLD, December 23, 2019

IMPORTANT DISCLOSURES

Analyst’s Certification I, Jackie Przybylowski, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Analysts who prepared this report are compensated based upon (among other factors) the overall profitability of BMO Capital Markets and their affiliates, which includes the overall profitability of investment banking services. Compensation for research is based on effectiveness in generating new ideas and in communication of ideas to clients, performance of recommendations, accuracy of earnings estimates, and service to clients.

Company Specific Disclosures

Disclosure 9B: BMO Capital Markets makes a market in IAMGOLD and AngloGold Ashanti in United States.

For Important Disclosures on the stocks discussed in this report, please click here.

The meeting minutes from the December 11th monetary policy meeting will be released today by the Federal Reserve bank. The Federal Reserve Bank kept interest rates steady in December at 1.50% – 1.75%.

Investors will be looking to today’s release for any clues on the future course of monetary policy. In a holiday-shortened week, besides the ISM manufacturing report, this will be the biggest headline.

The impact of today’s report is unlikely to play a big role in the markets unless the information reveals information not previously known.

The Fed has been responsive to the current state of the US economy. Despite concerns of a possible recession, the economy will no doubt see a slower pace of growth. But still, this remains within the acceptable limits.

In some aspects, the Fed’s decision to cut rates is seen as a positive for the markets. Amid faltering growth and trade tensions, lower rates remain consistent with the current economic situation.

Recap of December FOMC Meeting

At the December meeting, the decision to leave interest rates unchanged was widely expected. This was after the Fed lowered rates three times during the year. While initially, the Fed started out with a one and done rate cut, its views changed.

As global trade tensions simmered, the impact was felt across the global economy. The manufacturing sector, in particular, took a big hit, with the ISM’s index falling below the 50-level, indicating contraction.

Meanwhile, despite President Trump’s calls for bigger rate cuts, the Fed asserted its independence by staying the course.

At the December meeting, the Fed also published its quarterly economic outlook. As per the report, policymakers see interest rates staying steady this year. However, given that the Fed remains data-dependent, it will be quick to react to any overheating in the economy.

The central bank’s key worry is the lack of price pressures. But all things considered, the current landscape remains supportive of growth. Sluggish price pressures mean that consumers have more to spend.

With the labor market in the United States staying resilient, it is likely that price pressures will rise eventually. Part of this is also due to the recent rise in oil prices. This comes as OPEC members voted for deeper production cuts.

Although energy prices remain volatile, they play a bigger role in the face of inflation. Higher oil prices could give consumer prices a boost.

Questions Remain

At the moment, the big question on everyone’s mind is the direction of interest rates. A lot of this will depend on how the economy will fare. For one, investors will get to see if the initial trade deal with China will help in any way.

Over the holiday period, China announced a series of measures by lowering tariffs not just for US goods, but for also most of its trading partners.

This easing of trade stance could be encouraging, giving global growth a bit of a boost.

The most critical juncture will, of course, be the March Fed meeting. There is a slight chance that the Fed could cut rates once again. But having said that, it will depend on economic performance during the first quarter of the year.

Overall, today’s FOMC meeting is unlikely to reveal any new information. There are still some dissenters in the FOMC who are in favor of rate hikes. But they are unlikely to influence the rest of the voters.

Pulmatrix’s shares opened 90% higher today after the firm reported that it has signed a kinase inhibitor licensing agreement with the Lung Cancer Initiative at Johnson & Johnson.

Prior to the U.S. markets open this morning on the first day of trading in 2020, clinical stage biopharmaceutical company Pulmatrix Inc. (PULM:NASDAQ), which is “developing innovative inhaled therapies to address serious pulmonary diseases,” announced that it has signed a licensing and development agreement with the Lung Cancer Initiative (LCI) at Johnson & Johnson. The company indicated that “through the agreement, the LCI gains an option to access a portfolio of narrow spectrum kinase inhibitors intended for development in lung cancer interception.”

The company’s CEO Ted Raad commented, “Pulmatrix’s iSPERSE platform has the ability to enhance the safety and efficacy profile of promising drug candidates…We applied the iSPERSE technology to RV1162/PUR1800, the lead in-licensed inhibitor and helped unlock its clinical potential by improving the product’s profile from the original formulation. In 2020, we anticipate clinical data from the first of these inhibitors in a disease area with significant unmet medical need. We look forward to collaborating with the Lung Cancer Initiative at Johnson & Johnson as we advance this important program. Additionally, in 2020, we anticipate data from our phase 2 Pulmazole program and we plan to introduce new proprietary, wholly owned iSPERSE enabled 505(b)(2) assets to our pipeline.”

The company advised that according to the terms of the agreement, “the LCI will pay a $7.2 million upfront payment and an additional $2 million milestone payment upon completion of the ongoing Phase 1b study of RV1162/PUR1800 in stable COPD patients, on-track for year-end 2020. If the LCI exercises the option on RV1162/PUR1800 and the portfolio of these kinase inhibitors, Pulmatrix is eligible for up to $91 million in additional development and commercial milestones, as well as royalty payments.”

Pulmatrix is a clinical stage biopharmaceutical company headquartered in Lexington, Mass., that is developing innovative inhaled therapies to address serious pulmonary disease using its patented iSPERSE technology. The firm explained that iSPERSE is a dry powder engineered delivery platform created to improve therapeutic delivery to the lungs by maximizing local concentrations and reducing systemic side effects. The company states that “its proprietary product pipeline is focused on advancing treatments for serious lung diseases, including Pulmazole, an inhaled anti-fungal for patients with allergic bronchopulmonary aspergillosis, and PUR1800, a narrow spectrum kinase inhibitor for patients with obstructive lung diseases including asthma and chronic obstructive pulmonary disease.”

Johnson & Johnson (JNJ:NYSE) is based in New Brunswick, N.J., and has a market cap of around $385 billion. JNJ claims to be the world’s largest and most broadly based healthcare company. The company operates through three business segments: Consumer, Pharmaceutical and Medical Devices, and employs more than 130,000 employees worldwide. JNJ has research facilities in the U.S. and about 13 other large developed countries including Brazil, China, France, Germany, India, Japan, and the United Kingdom.

Pulmatrix Inc. began the day with a market capitalization of about $17.2 million with approximately 20 million shares outstanding. PULM shares opened nearly 90% higher today at $1.63 (+$0.77, +89.53%) over the prior trading day’s closing price of $0.86. The stock has traded today between $1.41 and $1.79 per share on very high relative volume and is presently trading at $1.75 (+$0.89, +103.49%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

With most traders back at their desks after the holidays, there’s a host of key economic data coming out of the US on the last day of the trading week.

Chief among them is what looks like will be a less than stellar performance by US manufacturing, with the release of ISM Manufacturing PMI. Despite the stock market hitting record highs recently, the manufacturing sector doesn’t seem to be as optimistic.

We should note that the survey was conducted through the time in which the Phase 1 US-China trade deal was announced.

Although it was widely expected, the formal release might have had an effect on the projections from corporate executives. The result could come in significantly above market expectations. And this could be adjusted following the Markit PMI survey scheduled to be released later today.

What We Are Looking For

The key data to keep an eye on is the headline ISM Manufacturing PMI.

Expectations are for this to stay in contraction at 48.3 with a slight improvement over the 48.1 in November. The result would imply that the indicator has found something of a floor after slowly declining since the middle of last year.

Generally, the weakness in PMI figures has been attributed to the global trade situation. The easing trade tensions might mean the manufacturing sector could be getting some relief going forward.

Other analysts have argued that the damage of the trade war has already been done. And without any certainty that tariffs might be ramped up again, wholesalers are going to stick with their new suppliers.

The Components

The ISM employment survey is not immediately market-moving. However, it’s still relevant to projecting the market.

This is especially true regarding what we could expect from the NFP that will be released next week.

Surveyed economists are expecting manufacturing to have added a significant amount of jobs. This would push the indicator to 53.5 from 46.6. That’s a major improvement and could foreshadow better performance in the main indicator.

So far, US manufacturers have been grumpy about their new orders numbers, seeing declines over the last several months. New orders would have to rise before they start ramping up production. So, this would be a good bellwether to keep an eye on this time around.

The Situation

Despite less than stellar manufacturing numbers, the US economy continues to forge ahead with record low unemployment and high consumer demand.

Consumer confidence remains high, and many analysts are expecting a generally positive year as election spending ramps up.

The dollar has been weakening in the wake of the Phase 1 trade deal as risk appetite kicks off. We would expect a weaker dollar to push inflation and make exports easier for manufacturers.

If traders come back more optimistic from the holidays, we could see that trend continue. This would help support the euro as a couple of analysts have been predicting.

However, we’ll have to wait for the rush of final quarter and year-end data expected over the next couple of weeks.

Bob Moriarty of 321gold discusses the similarities between this project and the Witwatersrand deposit in South Africa.

I’ve been writing about Novo Resources and their Witwatersrand lookalike deposit for over five years. Well, Quinton Hennigh is associated with another Wits lookalike, this time in Brazil.

Yamana’s Jacobina deposit is the same age as another similar type deposit in Brazil named Castelos de Sohnos owned by TriStar Gold Inc. (TSG:TSX.V). In both deposits free gold of unusually high purity is found in reefs of quartz cobbles. While the “experts” call these deposits “paleoplacer,” they aren’t placer. All “paleo” means is old so “paleoplacer” simply means old placer.

Since the discovery of gold in the Witwatersrand Basin in South Africa during 1886, experts have debated the origin of the gold there. In general there have been two camps. One camp holds that there were giant mountain ranges containing veins of rich gold and as the earth aged, rain and erosion caused the gold to be released from the rock and washed downstream. That’s the “paleoplacer” group.

The other group believes that in a way similar to many gold deposits today, gold deep in the earth is taken into solution in the presence of hot, caustic solutions of sodium and chloride and brought to the surface through fissures in the ground. When either the chemistry or pressure or temperature of the water changes, the gold precipitates out forming gold deposits. These systems are named epithermal deposits.

You can go to any bar in Toronto during PDAC or Vancouver during Roundup and start a fight just by supporting one theory or the other. Everyone has a dog in the fight and wants to defend their position. Often to the death, it appears that nothing in life outweighs defending one’s pet theories. Alas, there was a third theory of where the gold came from in the Wits Basin, long since forgotten.

It wasn’t long after the discovery of the Wits that someone sat down and thought about how the gold got there. The author of the 3rd theory rejected both the paleoplacer concept and the epithermal theory because while elements of each existed, neither gave a really satisfactory and simple answer to the question.

This theory suggested that the gold was in solution in the water and as the chemistry of the water changed the gold came out of solution. We know that today the most gold in the world is found in salt water due to the presence of both sodium and chlorine. Working backwards, our expert determined that due to the chemical composition of salt water 2-3 billion years ago, it had the potential for containing a lot more gold than salt water does today. Between a thousand and ten thousand times as much.

That’s the same theory that Quinton Hennigh has proven in Western Australia in the Pilbara Basin with Novo Resources. He has not only put a small test mine into production at a very low cost, he is hitting bonanza grades intersections in drilling and taking surface samples.

I’m not sure it makes a world of difference in a mining project as to just how gold got there. The Wits is a perfect example, it’s produced over 40% of all the gold ever produced yet the source is still subject to a constant debate. But I think understanding the source of the gold would give a higher potential to finding a bigger deposit if you fully understood it.

What everyone seems to be missing in the paleoplacer theory is that placer deposits generally are found in rivers and streams where the heavier gold than the background gravels gets washed downstream and trapped in lower flow areas. No one mines basins for placer gold. It just isn’t done. Rivers and creeks flow. In basins the water pretty much sits. If the gold was associated with the cobbles in these “paleoplacer” deposits why isn’t there any gold within the cobbles? The experts have mistaken coincidence with causality. The gold is associated with the water, not the rocks.

In addition, the purity of the gold in Western Australia with Novo Resources and in Brazil with both Jacobina and the Castelo de Sonhos deposit is nearly pure, measuring as high as 95-96 parts pure. Placer deposits in the Mother Lode Belt in California are typically 75-90 parts pure and purity above 85 parts is unusual in Alaska placer deposits. In placer deposits, the gold is always mixed with silver and copper as well.

TriStar Gold, headed by Nick Appleyard as President and CEO, was smart enough to ask Quinton Hennigh to come on board as an outside director. No matter how the gold got there, the similarities in the type of deposit and age of deposit between the two companies are striking.

TriStar was formed in 2010 and picked up on option from a private owner on the 72,067 ha Castelo dos Sonhos gold project in Brazil. The property is a plateau measuring 15km by 12km standing 300 meters above the surrounding terrain. Between the 1980s and the mid-90s the creeks and drainages from the plateau were mined by local artisanal miners who recovered an estimated 250,000 to 320,000 ounces of gold.

The option agreement called for TriStar to pay the owner $2.4 million over a three-year period for 100% ownership of the deposit. In addition, the company was required to incur exploration expenses of about $3.25 million over two years. The owner retained a 2% NSR and will receive an additional $1 per ounce of gold over 1 million ounces defined in a reserve.

Barrick worked on the project in 1995 and 1996. TriStar has their entire exploration data and drill core. The project had a 43-101 done on it in 2014 that showed 182,000 ounces of gold in the indicated category and an additional 98,000 ounces in inferred.

In January of 2016 after a reevaluation of the project and direction by management the project, TriStar issued a exploration target range at Castelo de Sonhos of between 2.1 million ounces of gold in 50 million tonnes at 1.3 g/t to 4.3 million ounces of gold in 84 million tonnes at 1.6 g/t. Those numbers are conceptual in nature and will require more drilling and surface sampling. There is no guarantee that any future resource will achieve those targets.

What is clear is that this is a Wits lookalike. The deposit has been barely explored so there is a high potential for the company meeting their target goals. Due to the price of gold, TSG has been fairly quiet for the last couple of years but with the renewed interest in gold and higher prices, the company has come back to life with a vengeance.

Two drill rigs have been mobilized to the project. Phase 1 drilling will begin shortly and continue through January. TriStar plans on issuing an update 43-101 resource and PEA by mid-2017. A phase 2 program is scheduled to begin in January/February and continue though May.

Given that Quinton Hennigh has spent 15 years thinking about how gold precipitated from salt water into conglomerate reefs in the Witwatersrand Basin and the Pilbara Basin, it was a good move of TSG to request his help. Quinton has developed a low cost way of mining the reefs in Western Australia that is easily transferrable to Brazil as well. Once you understand the limits and potential of Wits type system, exploration and exploitation become cheap and easy.

I really like the TriStar story. They have a resource now. They have the money to add to that resource. They have the technical and management bandwidth to keep things under control and best of all, they have a financial tailwind from the higher price of gold that will make financing possible without terrible dilution.

Given all the positives, I’m a bit surprised the market hasn’t given them a higher valuation. That will change as their story becomes better known. Brazil happens to be one of the more mining friendly jurisdictions in South America and that’s a giant plus.

TriStar is an advertiser and I am biased naturally. Please do your own due diligence. I share in neither your profit nor your losses.

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: TriStar Gold. TriStar Gold is an advertiser on 321gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Gold continues to move higher due to trouble in the Fed Repo and U.S. Treasury Market. In the first hour of business today, the Fed has already injected $57 billion in the Repo Market. While the Fed’s Repo Market injections didn’t spike during the last few days of 2019, as many analysts forecasted, there’s still BIG TROUBLE ahead.

Many reasons have been attributed to the break-down in the U.S. Repo Market that started on September 17th when the daily repo rate spiked to 10%. Several readers have sent me very interesting information and youtube videos on the subject matter. I thought it was a good time to sift through all the information and present my analysis on what the hell I believe is going on.

First and foremost, while there are many reasons given for why the Fed Repo rate spiked, forcing the Fed to provide hundreds of billions of dollars of short-term liquidity in the market, these are “ALL SUPERFICIAL” reasons. The major factors causing wide-spread havoc throughout the financial system are the Falling EROI- Energy Returned On Investment of oil and the Thermodynamics of oil depletion. While these are two different energy analyses, they come to the same conclusion. The financial analyst community and market are still ignoring these key energy factors.

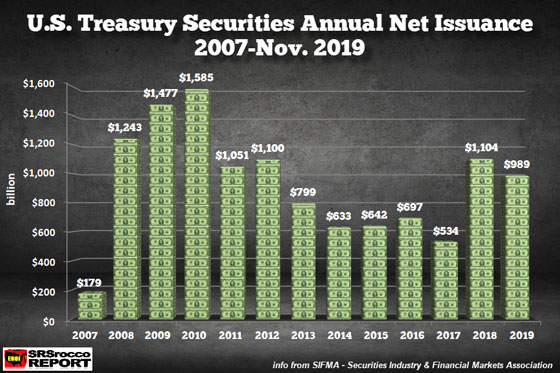

Second, the main “SUPERFICIAL” reason that caused the Fed Repo rate to spike is that there weren’t enough buyers for the increasing amount of U.S. Treasury issuance.

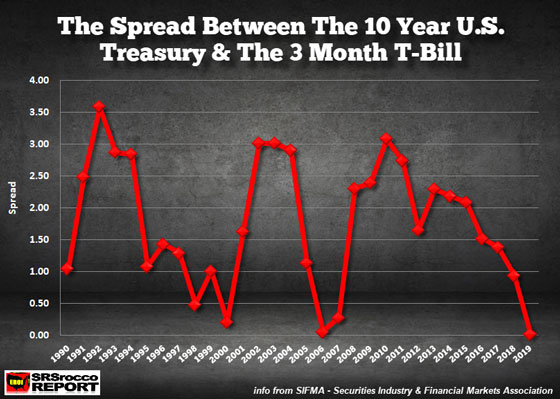

After the 2008-2009 financial crisis, U.S. Government deficits ballooned, forcing the “Net Issuance” of more U.S. Treasuries. In the chart above, the net issuance of U.S. Treasuries spiked to $1,585 billion ($1.58 trillion) in 2010. However, after the economy started to recover, the net issuance of U.S. Treasuries continued to decline to only $534 billion in 2017. But, the very next year, in 2018, something changed as the U.S. Treasury net issuance surged to $1,104 billion. This was bad news… but why?

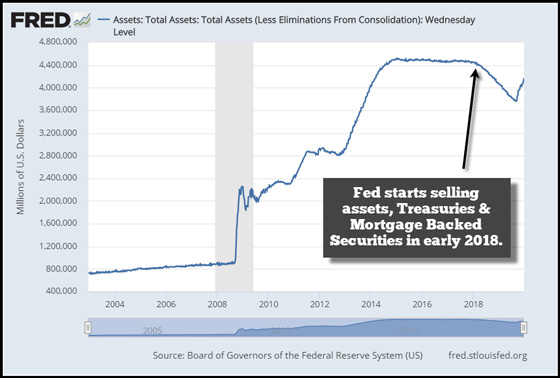

We have to remember that the Fed started reducing its balance sheet by selling U.S. Treasuries and Mortgage-Backed Securities into the market in early 2018:

So, get this… the Fed was a net seller of U.S. Treasuries and Mortgage-Backed Securities in 2018 right at the very same time, the U.S. Government’s net issuance of U.S. Treasuries doubled from $534 billion in 2017 to $1,104 billion in 2018. This had a profound impact on the U.S. Treasury rates, especially the 10 Year/3 Month Spread.

Now, to make this easy to understand, the 10-Year/3 Month Treasury rate spread shows how much more demand there is for either the shorter-term Treasuries or the longer-dated ones. If the 10-Year/3 Month spread falls, then there is more demand for the 10 year Treasury, which suggests investors are worried about an upcoming recession. The 10-Year/3 Month U.S. Treasury spread has been steadily falling since 2010 and is now only 0.02 compared to 3.08 in 2010:

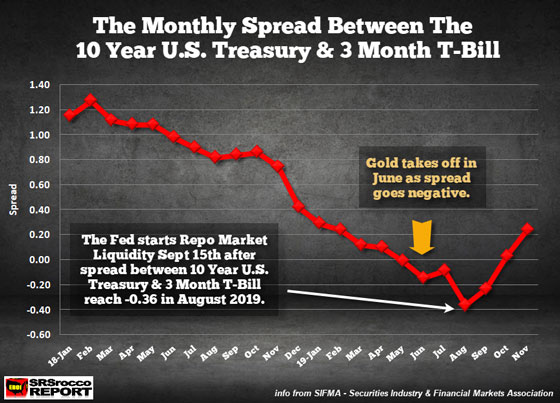

According to SIMFA, the Securities Industry & Financial Markets Association, the average rate for the 10 Year U.S. Treasury (Jan-Nov) was 2.17 versus 2.15 for the 3 Month Treasury Bill. Thus, there is a positive 0.02 Spread. However, there were some real problems starting in June when the 10-Year/3 Month Treasury spread went NEGATIVE:

There is no coincidence that the Gold Price began to take off in June 2019 when the 10-Year/3 Month Treasury spread went negative… for the first time since the 2007 financial crisis began. As the 10-Year/3 Month, Treasury spread went further negative until August, the gold price continued higher to reach a peak of $1,560 at the end of the month. Then what happened in September and October?? You got it, the Fed came in and started the Repo Operations in mid-September and then announced the $60 billion a month in U.S. Treasury purchases in mid-October:

The GREEN arrow shows where the 10-Year/3 Month Treasury spread started to go negative, and over the next three months, as the spread reached a low of -0.36 in August, the gold price increased $300. The RED arrows show that when the Fed came in to save the day in September with its Repo Market operations, providing short-term liquidity, and then again in October to buy $60 billion a month, the 10-Year/3 Month spread moved higher.

If we look at the U.S. Treasury Net Issuance chart again, we can see that the U.S. Government is in trouble as it has to finance a lot more of its annual deficits:

With the global economy stalling and some regions heading into a recession, there are fewer surpluses available to be able to buy the increasing amount of U.S. Treasuries, not including the amount that is continuously rolled over.

Even though there may be a BIG PROBLEMS with individual banks that caused the Fed Repo rate to spike on September 17th, the main issue is that the U.S. Government is issuing more Treasuries than the market can absorb. Thus, the Fed had to start buying U.S. Treasuries, which helped push the 10-Year/3 Month spread back into positive territory. However, the problem isn’t over as the market mistaken assumes… IT’S JUST BEGINNING.

I believe the September 17th Fedo Repo rate spike to 10% was the CRISIS and will only get worse as time goes by.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Shares of specialty cardiovascular medical device company Neovasc Inc. opened more than 100% higher after the firm reported that it submitted a Premarket Approval application to the FDA for its Neovasc Reducer device for use in the treatment of refractory angina.

This morning Vancouver, Canada-based specialty medical device company Neovasc Inc. (NVCN:NASDAQ), which develops, manufactures and markets products for the cardiovascular marketplace, announced that “it has submitted a Premarket Approval application (PMA) to the U.S. Food and Drug Administration (FDA) for its Neovasc Reducer (“Reducer”) medical device for the treatment of refractory angina.” The firm noted that that the submission also included a request for an Advisory Panel meeting.

The company’s President and CEO Fred Colen commented, “This submission marks an important milestone in our effort to bring Reducer to the U.S. market, where it is estimated that there are up to 1.8 million patients with refractory angina…These patients have traditionally had no options they are either unsuitable for revascularization or continue to suffer with angina following revascularization procedures. The Reducer provides potential relief of angina symptoms by altering blood flow within the myocardium of the heart and increasing the perfusion of oxygenated blood to ischemic areas of the heart muscle.”

The company advised that “the PMA for Reducer includes clinical data from the COSIRA 104 patient randomized, double-blind, sham-controlled trial, the ongoing REDUCER-I European Post-Market study, with over 200 patients currently enrolled with up to 5 years of follow-up, and supportive clinical evidence from multiple peer reviewed publications on Reducer.”

The firm explained that refractory angina is a painful and debilitating condition that affects millions of patients worldwide. The condition occurs when the coronary arteries deliver an inadequate supply of blood to the heart muscle despite treatment with standard revascularization or cardiac drug therapies. The company claims that “the Reducer provides relief of angina symptoms by altering blood flow within the myocardium of the heart and increasing the perfusion of oxygenated blood to ischemic areas of the heart muscle and that placement of the Reducer is performed using a minimally invasive transvenous procedure.”

Neovasc is headquartered in Vancouver, British Columbia, and describes itself as “a leader in the development of minimally invasive transcatheter mitral valve replacement technologies and in the development of minimally invasive devices for the treatment of refractory angina.” The firm’s products include the Tiara technology in development for the transcatheter treatment of mitral valve disease and the Neovasc Reducer for the treatment of refractory angina, and tissue products. The Tiara transcatheter device is designed to treat mitral regurgitation as a result of mitral heart valve disease, an often severe condition that can lead to heart failure and death. The Neovasc Reducer is a percutaneous treatment for refractory angina, a condition which affects millions worldwide. Though not yet commercially approved in the U.S., the company received Breakthrough Device designation for the Neovasc Reducer in October 2018 from the FDA.

Neovasc has a market capitalization of about $30 million with approximately 7.65 million shares outstanding. NVCN shares opened greater than 100% higher today at $7.99 (+$4.06, +103.31%) over yesterday’s closing price of $3.93. The stock has traded today between $6.11 and $8.65 per share and is currently trading at $7.09 (+$3.16, +80.41%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.