The work the company has conducted to date at the project and the implications are discussed in a Scarsdale Equities report.

In a Jan. 3 research note, Scarsdale Equities analyst Mike Niehuser reported that “evidence continues to mount for an alkaline gold system” at Lion One Metals Ltd.’s (LIO:TSX.V; LOMLF:OTCQX) Tuvatu project in Fiji. Accordingly, Scarsdale increased its target price on the gold company to CA$2.25 per share and kept it Buy rated. In comparison, Lion One’s current share price is CA$1.64.

The analyst reviewed the indicators that point to Lion One continuing to define a world-class alkaline gold system in Fiji’s Navilawa caldera.

In the recent past, the gold company engaged Dr. Quinton Hennigh as a technical geological advisor, who indicated the Tuvatu gold deposit in the Navilawa caldera could be part of a larger, world-class alkaline gold system, like that of the Vatukoula gold mine.

Hennigh initiated a program of conducting bulk leach extractable gold (BLEG) geochemical surveys to analyze stream sediments in the caldera. These showed the presence of surface gold mineralization throughout it.

The most recent positive sign is the results Lion One reported from the first of its four deep hole drill program at Tuvatu. Hole TUDDH493 intersected gold mineralization about 70 meters below TUDDH-160 (the best drill hole to date under the Tuvatu gold deposit). Results for the second deep drill hole TUDDH494, which tested areas 70 meters below TUDDH493, are pending.

“As alkaline gold systems may extend deeper, we see the Tuvatu gold deposit, coupled with other surface expressions of gold in the BLEG surveys, as having a reasonable likelihood of connecting at depth,” Niehuser explained. “This would suggest that the Navilawa caldera has the potential to host another world-class gold deposit in the South Pacific.”

Further, Lion One acquired a drill company with a deep hole drill capacity of 1,000m. It also developed an assay lab “to expand and accelerate exploration through BLEG sampling and deep drilling,” noted Niehuser.

Currently, the Canadian explorer is carrying out a CSAMT, or controlled-source electromagnetics and audiofrequency magnetotellurics, geophysical survey to delineate deep structures at Tuvatu. “When combined with BLEG surveys, this will be the first comprehensive exploration program assessing the potential of the Navilawa caldera,” Niehuser commented. Also, Lion One is developing a “lower-cost modular production scenario.”

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Lion One Metals. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from Scarsdale Equities, Lion One Metals Ltd., January 3, 2020

Author Certification: R. Michael Niehuser, the author primarily responsible for this report certifies, with respect to each security or issuer in this report, that: (1) all of the views expressed in this report accurately reflect his own personal views about the subject companies and their securities; (2) part of the authors compensation may be, directly or indirectly, related to a portion of the commissions generated by Scarsdale Equities LLC [SE] in transactions in this or other securities designated for the authors credit; (3) the author does not receive compensation based on investment banking or advisory services SE might provide to this or any other issuer.

Scarsdale Equities LLC, at the time of publication, does not make a market in any security. The author does not have a financial interest Lion One Metals Limited (LIO.V) covered in this report. Part of the authors compensation may consist of a portion of the commissions generated by transactions in this issuer’s securities placed at Scarsdale Equities LLC for the credit of the author. Scarsdale Equities LLC expects to receive advisory or investment banking compensation from the issuer in the next ninety days.

Shares of Applied Genetic Technologies skyrocketed to a new 52-week high price after the company reported positive six-month data from its ongoing Phase 1/2 clinical study for treatment in X-Linked Retinitis Pigmentosa. The firm stated that the trial data suggests durable and meaningful improvements in central visual sensitivity and advised that it plans to initiate a pivotal trial by year-end 2020.

Clinical-stage biotechnology firm Applied Genetic Technologies Corp. (AGTC:NASDAQ), which is engaged in exploring gene therapies for the treatment of rare and inherited diseases, today announced positive interim six-month data from its ongoing Phase 1/2 clinical program in X-linked retinitis pigmentosa (XLRP). The company reported that “the results show that patients treated centrally with its product candidate demonstrated durable improvement in visual function six months after dosing.”

The firm claimed that the additional data reinforces previously reported efficacy and safety results and that the updated data will be used in the design and implementation of the company’s XLRP pivotal trial that is anticipated to commence by the end of 2020. AGTC stated that it plans to review the data from the XLRP and achromatopsia Phase 1/2 clinical programs at an R&D Day in New York City on January 28, 2020.

The company’s President and CEO Sue Washer commented, “These promising results further demonstrate that our XLRP candidate has tremendous potential to provide meaningful benefit to XLRP patients who today have no treatment options…The positive results observed to date give us confidence that the data as a whole will support advancement of our XLRP clinical program to a pivotal trial in 2020.”

Dr. Paul Yang, MD, PhD, assistant professor of ophthalmology at the Casey Eye Institute, Oregon Health & Science University in Portland, stated, “The sustained improvement in visual sensitivity in centrally dosed patients are compelling and, if confirmed in a pivotal trial, would be highly meaningful to patients…This is the first investigational therapy for XLRP to report on encouraging improvements in visual acuity. The combination of improved visual function across two endpoints in centrally treated patients and the previously reported stabilization of visual function in peripherally dosed patients, suggest that this gene-based therapy has the potential to be an important new approach to treating XLRP.”

The company explained that X-linked Retinitis Pigmentosa (XLRP) “is an inherited condition that causes progressive vision loss in boys and young men. Characteristics of the disease include night blindness in early childhood and progressive constriction of the visual field. In general, XLRP patients experience a gradual decline in visual acuity over the disease course, which results in legal blindness around the 4th decade of life.”

Applied Genetic Technologies is a is a clinical-stage biotechnology company headquartered just north of Gainesville in Alachua, Fla., that employs a proprietary gene therapy platform to develop transformational genetic therapies for patients suffering from rare inherited conditions and debilitating diseases. The firm indicates that its initial focus is in the field of ophthalmology and that its most advanced therapy programs are designed to restore visual function and meet the needs of patients with rare blinding conditions. The company has active clinical trials in X-linked retinitis pigmentosa and achromatopsia. AGTC additionally has preclinical programs in optogenetics and other ophthalmology indications and other central nervous system diseases including adrenoleukodystrophy (ALD).

Applied Genetics started off the day with a market capitalization of about $75.8 million with approximately 18.22 million shares outstanding. AGTC shares opened nearly 60% higher today at $6.65 (+$2.49, +59.86%) over yesterday’s $4.16 closing price. The stock set a new 52-week high price of $8.80/share in morning trading and has traded today between $5.90 and $8.80 per share on extremely high relative volume. The firm’s shares are currently trading at $8.77 (+$4.61, +110.73%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Rare disease biopharmaceutical company Ultragenyx Pharmaceutical’s shares traded 30% higher after the firm reported positive topline results from Cohorts 2 and 3 in its Phase 1/2 study of DTX301 gene therapy in Ornithine Transcarbamylase Deficiency.

After U.S. markets closed yesterday afternoon, Ultragenyx Pharmaceutical Inc. (RARE:NASDAQ), a biopharmaceutical company engaged in the development of novel products for rare and ultra-rare diseases, announced “positive topline safety and efficacy data from Cohort 3 and longer-term data from Cohort 2 of the ongoing Phase 1/2 study of DTX301, an investigational adeno-associated virus (AAV) gene therapy for the treatment of ornithine transcarbamylase (OTC) deficiency.”

The company advised that the objective of the Phase 1/2 study of DTX301 is to “evaluate the change in the rate of ureagenesis, ammonia levels, neurocognitive assessment, biomarkers, and safety of DTX301 in patients with OTC deficiency.” The firm explained that OTC deficiency is the most common urea cycle disorder that affects more than 10,000 individuals worldwide caused by a genetic defect in a liver enzyme responsible for detoxification of ammonia. The company indicated that to date there have been no infusion-related adverse events and no treatment-related serious adverse events reported in the study.

Ultragenyx indicated that DTX301 has been granted Orphan Drug Designation in the U.S. and Europe and is “an investigational AAV type 8 gene therapy designed to deliver stable expression and activity of OTC following a single intravenous infusion, which has been shown in preclinical studies to normalize levels of urinary orotic acid, a marker of ammonia metabolism.”

Eric Crombez, M.D., chief medical officer of the Ultragenyx Gene Therapy development unit, commented, “We are encouraged to see a more uniform response at the higher doses including three female responders. To date, three patients in the study have discontinued alternate pathway medication and liberalized their diets while remaining clinically and metabolically stable…We are moving to prophylactic steroid use in the next cohort as we believe this could further enhance the level and consistency of expression that we have demonstrated so far.”.

Ultragenyx is headquartered in Novato, Calif., and is a biopharmaceutical company specializing in developing novel products for the treatment of serious rare and ultra-rare genetic diseases. The company aims at addressing diseases with high unmet medical need with clear biology for treatment for which there are no presently approved therapies for treating the underlying disease.

Ultragenyx Pharmaceutical started the day with a market capitalization of approximately $2.5 billion with about 57.77 million outstanding shares and a short interest of around 10.6%. RARE shares opened nearly 12% higher today at $48.91 (+$5.18, +11.85%) over yesterday’s $43.73 closing price. The stock has traded today between $44.84 and $58.54 per share and is currently trading at $58.44 (+$14.71, +33.64%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up we’ll hear an eye-opening interview with Craig Hemke of the TF Metals Report. Hear from the man who accurately predicted a year ago that 2019 would be the best year for gold and silver since 2010. And we’ll hear his new call for 2020. Craig also takes serious issue with some of the gold naysayers and perma-bears and calls them out for being blinded by their agendas. So, don’t miss my conversation with Craig Hemke, coming up after this week’s market update.

A wild week for markets as the U.S. and Iran come to the brink of war before both sides apparently decided it would be wiser to pull back.

After Iranian missiles hit a U.S. military base Tuesday night, gold prices surged above $1,600 an ounce. As gold headed toward a 7-year high, even the mainstream media had to take note. Jim Cramer and his fellow stock market pumpers on CNBC took time to lament the fear-driven buying of gold.

CNBC Anchor: All right. Jim, what’s caught your attention this morning beyond Citi in terms of the key to this market? Obviously, we see, broadly speaking, a down market.

Jim Cramer: It’s gold, gold, gold, gold. When I see this endless buying of gold, it makes me think, for the first time, maybe people are just saying, “I am really fearful.” It’s not just Treasures. The gold buying has been endlessly, over and over and over. There are only a few growth gold companies. The main one is Agnico Eagle. People want to buy, that’s the one to buy. But it’s relentless and it feels like gold wants to go to $1,700, $1,800. That would be very negative for the market.

CNBC Anchor: Uh, yeah.

Fear buying of gold and other safe havens ended up being short lived. After U.S. officials reported there had been no casualties and Iran stood down, fears of World War III suddenly turned into hopes for a quick end to hostilities. Wall Street celebrated as metals markets sharply reversed mid-week.

As of this Friday recording, gold is now relatively flat overall for the week to trade at $1,560 per ounce. The silver market shows a slight weekly gain of 0.2% to bring spot prices to $18.16 an ounce. Platinum is off 0.4% last Friday’s close to come in at $982.

And finally, palladium pushed through the $2,000 level for the first time ever. It currently trades at $2,129 on the heels of a 6.5% advance this week.

Well, while we can all take comfort in the tamping down of tensions between the U.S. and Iran, it would be naïve to believe that the threat of further conflict in the region is over.

It appears that Iran was in fact responsible for shooting down a Ukrainian passenger jet. If it instead had been an American Airlines jet loaded with U.S. citizens, we’d likely be seeing much more of a reaction from President Donald Trump and perhaps our military forces as well.

Iran or Iranian-backed terrorists could be planning other forms of retaliation as I speak. The assassination of Iran’s top general has stoked extreme new levels of anti-American resentment. It won’t abate anytime soon, especially as the Trump administration is vowing to impose tougher economic sanctions to punish Iran.

America is also struggling to keep Iraq from forging closer relations with Iran. Iraqis increasingly want U.S. forces out of their country.

Democracy in the Middle East never quite works out the way the foreign policy central planners in Washington envision. After so many years since 9/11, after so many trillions of dollars invested and ultimately wasted in Iraq and Afghanistan, President Trump at this point is looking for an honorable way to cut our losses.

But his neo-conservative advisors still cling to grand notions of re-making the region in our own image. And the pull of the Israeli lobby and military-industrial complex is perhaps the most powerful force in Washington. D.C. — as all Presidents come to learn.

Of course, precious metals markets will need more than occasional geopolitical flare ups to drive a long-term bull market advance. The fundamentals are turning in favor of higher gold and silver prices. From fiscally reckless trillion-dollar deficits in Washington, to a Federal Reserve obsessed with generating higher rates of inflation, to mining supplies of gold and silver looking tight, the ingredients for a big bull market are in place.

However, safe haven demand from investors has yet to pick up in a big way. We saw some of it this week, but it will likely be fleeting until the general public sees good reason to pull assets out of the stock market.

As stocks hit record highs last year, gold and silver coin sales at the U.S. Mint plunged to multi-decade lows.

The U.S. Mint sold just 152,000 ounces worth of gold American Eagles in 2019. That marks the lowest total on record going back to 1986. Meanwhile, sales of silver American Eagle coins came in at their lowest level since 2007. Now granted, a robust secondary market as a result of hordes of retail investor selling supplied the market with a cheaper alternative to the newly minted coins, and that explains part of those low numbers for 2019 U.S. minted product.

Australia’s Perth Mint, however, saw an increase in coin demand from its more internationally based buyers. Many sought physical bullion as a refuge from negative interest rates in their home countries.

As U.S. investors realize that they too face the prospect of negative real interest rates on savings and bubble valuations in equity markets, they too will increasingly find a compelling value proposition in gold and silver.

Well now, for some predictions on what 2020 will look like for the metals and the other markets, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome in Craig Hemke of the TF Metals Report. Craig is a well-known name in the metals industry and runs one of the most highly respected websites in our space and provides some of the best analysis you will find anywhere on banking schemes, global macroeconomics, and evidence of manipulation in the gold and silver markets.

Happy New Year to you, Craig. Thanks for coming on and welcome, how are you?

Craig Hemke: Mike, it’s always a pleasure. New Year’s started off with a bang, man. I hope it’s not indicative of how crazy this entire year is going to be. We’ll see.

Mike Gleason: Yeah, certainly this week sparking action itself. Lots going on both geopolitically and in the markets, and we’ll get to a lot of that. Well, Craig, here we are entering another new year. The conflict with Iran and the potential for an escalation there spurred some safe haven buying in recent days, but the rally in metals started last month. I’d like to open by getting your thoughts on what you believe will be driving metals prices this year. Yes, we expect the forces of evil to continue doing their best to manage prices, and we’ll get to that topic of price manipulation in a moment, but talk about what you’re seeing in the metals here recently and discuss some of the themes you anticipate people will be talking about this year when it comes to the metals.

Craig Hemke: Well, I think it’s critical that people try to have a longer memory than 48 hours. As we record this today, I’m seeing all kinds of garbage. I saw garbage from some group that is always a perma-bear, always talking about how gold has topped out and going down, has a clear agenda, just like some of the short sellers that are always anonymously pound the mining stocks with fake research reports and stuff like that. And I’m seeing these things today about how, “Oh yeah, gold, look at that. Look how terrible that candle looks on the daily chart, and how come hold’s not going up when all this war stuff,” and it’s like, do you not understand? I mean, gold went up prior to the war starting. Beginning last Thursday, gold closed on the Comex, last Thursday, January the 1st at about $15.30. So, the whole move from $1,530 to $1,580 was war premium, if you will, really short-term war premium. Then the spike to $1,610 was when we seemed to be on the verge of what could even have been a nuclear war in the Middle East.

The fact that it’s pulled back to $1,550 shouldn’t surprise anybody. I mean, we hadn’t even worked out all the war premium yet. Despite what is some pretty cheery economic news this week, service sector PMIs, the ADP jobs report, that kind of thing, so jeez-Louise, I sure hope people keep their perspective. You are correct in pointing out, Mike, that the metals rallied strongly into the year and it had nothing to do with war. That wasn’t on anybody’s mind prior to about six o’clock in the evening on January the 2nd. Gold rallied 3% from December the 20th through that date. Silver rallied 8.5% from December 9th at $16.60 up to $18.40 on January the 2nd. The HUI, the gold bugs index … which everybody’s freaking out because the shares went down yesterday. The HUI is up 15% still since the middle of October. For a while it was up 20, and why is this happening? Because the Fed, whether they want to call it QE or not, began this direct monetization of the debt program in October.

Everything’s going up. Stock market, you name it, and that is going to continue this year. It’s only going to get worse. A lot of people missed last Friday, the 3rd, the minutes for the December Fed meeting were released. First of all, everybody was on vacation still on Friday, January the 3rd, and second of all, those are always released on a Wednesday, three weeks after the Fed meeting. So, no one’s looking for them on a Friday afternoon at two o’clock, but here they came. And buried within the minutes, anybody can pull these up, is admission that what’s very likely to happen in the months ahead is the Fed will start monetizing not just T-bills, but notes, longer term duration notes, two years, three years, five years, seven years, ten years. There’s no other option. They cannot afford the stock market to go down. They cannot afford the money supply to contract, and thus they will constantly be printing all through this year more and more dollars, and everything is going to go up for the reasons that were driving them last year. Please don’t get caught up in what happened and how the chart looks based on these extraordinarily rare events that we saw back on Tuesday.

Mike Gleason: There’s been a bit of a pattern in recent years where the metals start perking up in December and perform well in the first half of the year. Any thoughts about what’s behind that and are you looking for that pattern to repeat this year, Craig?

Craig Hemke: Yeah. We were talking about it on my site all the way through December. It was logical to expect, first in November, you expected the metals to trade lower because the December contract is always the most heavily traded all year long. And the December contracts, both gold and silver, had massive open interest and they were both going off the board at the end of November, which meant all the speculators that were long were going to have to sell, and if they don’t completely roll over their positions into February, then that effect is a selling pressure. The price went down.

I told people all through November, I thought, $1,440, that’d about do it. We’re already so extremely oversold. I couldn’t see a waterfall down. I think we saw $1,445. I thought we’d rally into the end of the year because as you said, Mike, that’s typically been the pattern, especially since the bear market lows were put in back in 2015. The shares performed well, especially in the back half of December, because they’re subject to so much tax loss selling, particularly in Canada, and that usually concludes around 18th, 20th. People want to get that done before they go on Christmas holiday. And so once again, we got that behind us and up with the metals. Let me just point this out to you, Mike, because this is a lot like last year. You remember last year, the stock market crashed. Remember that in December of 2018?

Mike Gleason: Sure. Worst December in decades.

Craig Hemke: Yeah, it was crashing, and basically the stock market was catching down to the contraction of the money supply that the Fed was doing by trying to “normalize”, whatever that means, their balance sheet, and the stock market finally caught on to that disappearance of liquidity. And so, what happened? On Christmas Eve, (Treasury Secretary Steven) Mnuchin… and anybody can look it up, I’m not making this stuff up… Mnuchin called a meeting of what’s called the Plunge Protection Team, the President’s Working Group on Financial Markets. They came up with a strategy to float it back higher. The day after Christmas, after the holiday, the Dow went up a thousand points and never looked back. Now, this was when gold first started to move higher, was in December last year, because interest rates had peaked in November, and this is what all caused me to issue a forecasting saying ’19 was going to be the best year for the metal since 2010. Well, why? Because the Fed was going to be reversing course and they were going to be printing cash because they don’t have any choice but to liquefy and continue to liquefy all these markets.

They can’t have deflation. They can’t have crashing stock markets. They can’t have higher interest rates, none of that stuff. So, in December of 2018, gold starts to rally, and everywhere everybody’s like, “Well, this is just a safe haven deal. Gold’s going to $1,100 in 2019,” and all this crap, Harry Dent stuff. Anyway, that’s not what happened. It wasn’t what was going to happen. It’s not what did happen, and so now here we are, gold rallying again, anticipating what’s going to be happening this year and it’s the same thing. “Well, the only reason gold went up is because of the safe haven stuff,” as if gold rallying in December and the shares railings since October had something to do with the idea that the U.S. was going to whack this Soleimani character on January the 2nd. It didn’t have anything you do with that. Gold is simply looking ahead, looking over the horizon as it always does, sees all this liquidity coming from the central banks around the world because it can’t afford to do anything else and it’s moving higher, and people need to understand that and they need to plan for that as they make their investment allocations for 2020.

Mike Gleason: Now let’s talk about price manipulation. Nobody does a better job than you when it comes to covering what the crooked bankers are up to in the paper markets for gold and silver. They sold a boatload of futures contracts last year in both metals. You observed that open interest in gold was up a whopping 70%. Said another way, the supply of paper gold rose by 70%. Yet the amount of gold in the vaults backing that paper barely budged. It’s quite the racket. So, while gold itself is actually scarce and hard to produce, futures contracts are exactly the opposite. The supply is essentially unlimited. Last year, 33 million new ounces of paper gold were dumped into the market. Despite that, gold prices still managed to rise by 18% or so. So, what do you make of that?

Craig Hemke: Yeah, I mean, how the world, and I guess, I don’t know, too many people get their beaks dipped in this or just simply don’t care, but how the world allows, how the mining companies allow their product to be priced, not off of the exchange of the actual commodity, but off the exchange of these derivative contracts that have nothing to do with anything. It’s like I look at you and I say, “Mike, here. We’ll call this contract between you and I gold, and I promise at some point that I got the gold behind it and if you want it, I’ll deliver it to you,” and then you promise that you’re actually interested in it and you go borrow a bunch of money from your broker-dealer to buy it on margin, and then we just pretend that that contract is actually … there’s going to be some physical exchange between us at some point, but that never happens, and at the end of the day you just say, “Well, I liked my exposure,” and I sell my contract. You sell your contract and I, taking the other side of it, buy it back, and there was never any gold exchange at all. There was just some weird promise that there was a backing to it and it’s a trading of those things that is allowed to determine prices. It’s just ridiculous.

Yeah. Let’s backtrack to that open interest thing that you said, because here’s a great way to look at it. Everybody knows, or at least should know, that 2018 was the largest year of global central bank gold purchases since 1969, the year after the London Gold Pool, 651 metric tons. Projections are, run rates, I haven’t seen the actual final numbers yet, but the projections are the 2019 was even greater, probably about 670 metric tons. So, there is what, 25% of global mine output actually demanded, I guess, as far as we can tell, physically delivered to the central bank – 670 metric tons of physical demand, offset by, as you said, the creation of over 1,000 metric tons of digital pretend paper, gold contracts. It’s like a two headed monster. I mean you’ve got the actual physical product, which as you said, is scarce, being priced by the trading of derivatives, which can be created infinitely because no one ever calls any of these people to the carpet. So it’s ridiculous. It’s outlandish.

Yes, gold managed to rise 18% last year, even while the supply of derivative contracts increased by 73%. Imagine if there was some forced linkage between the ability to create contracts and the amount of actual gold on deposit in the vaults, and you couldn’t have increased it by 73%. What if the supply only increased by 10%? Well then all that money around the planet looking for gold exposure would have had to find it through acquisition of existing contracts. This is how the stock market that allegedly works, but that’s not how it works in the pricing of precious metals. The banks just create more contracts, taking the opposite side, taking the short side, and figuring they can out last the speculators, eventually maybe forced them out and cover their shorts. It’s disgusting, and again, at the end of the day, what’s really astonishing are these dopey rock breaking geologist CEOs of the mining companies that think it’s a valid pricing structure and they fall for it. That’s what’s really mind blowing.

Mike Gleason: I want to ask you about the possibility of whether or not the bullion banks will lose control of prices anytime soon. That 70% jump in open interest is extraordinary. The department of justice is prosecuting several people and they have secured some guilty pleas. It’s interesting that they are using RICO laws. Perhaps they actually see the bank activity for what it truly is, organized crime. Officials in London are asking some pointed questions about the fraudulent use of EFPs, exchange for physical. An optimist would say that some of these developments will lead to reforms, but I think we’ve all learned that you should never overestimate bureaucrats’ ability or willingness to do the right thing. We may have to wait for the market to solve the problem, which will happen right after confidence in the futures markets, the banks, and/or the dollar collapses. What are your thoughts about how much longer this crooked price discovery system will persist, Craig?

Craig Hemke: Well, Mike, you’ve said a mouthful there. Let me pick off a couple of things. You mentioned the regulatory agencies. You got the Rico investigations here in the U.S. It’s pervasive. The fraud is pervasive. The former head of JP Morgan’s precious metals desk, who is also on the board of the London bullion marketing association, the LBMA – why would he be on both? Why would he be a JPM trader and on the board at the LBMA? But anyway, he’s now been indicted. The RICO statutes allow you to not just go after the goon, but allow you to go after the Don. So, we’ll see how far it reaches, however, it does reach across the pond. My friend Andy McGuire has been telling me this now for over a year, that the FCA, which is the English/British equivalent of the SEC, I guess, or Department of Justice, whatever, has been looking into the risks that are being taken by the English banks, and what that might pose the system.

Andy has told me about a meeting he had with a couple of Members of Parliament, and this guy, Andrew Bailey, who at the time was the head of the FCA. This was back in maybe August, and this Bailey had no idea, because the LBMA’s so opaque. I mean, you don’t get these stats every day, all the unallocated gold and all this stuff, and the risk that the bullion banks are taking there. So Andy laid it out for him and he said, this guy’s jaw dropped, and he’s like, “Look, we can’t afford a second financial crisis off of this. I mean the people … we already shafted them once. They’ll never let us get away with it again. We have to put a stop to this somehow,” and Andy told him about the EFPs, and we’ll get to how that continues in a second.

So anyway, this guy Bailey, who according to Andy said we got to somehow put a stop to this, this guy Bailey was just nominated and confirmed to be the head of the bank of England by Boris Johnson. So what’s he going to do? Does the buck stop when he leaves there, leaves the FCA and now he’s got to be a servant to the bank of England and stop paying attention? Or maybe he’s going to call the banks on the carpet. I know what direction I think any cynical or non-cynical person would think that that’s going to go, but I digress. These EFPs that I’ve been writing about for a couple of years, this is an arcane process that’s a part of every futures market, but I just can’t even describe the degrees to which it is abused … I guess that’s the right word … within golden silver.

I’ve kept track of … I don’t even know what it is… over the last two years, something like 14,000 metric tons of gold contracts. Each Comex gold contract is a hundred ounces, allegedly, of gold. Well, enough contracts that are the equivalent of 14,000 metric tons had been moved off the Comex and exchanged for physical (EFP) through London. Andy says they have this process where they swing them into these 13 day little contracts that are off the books and just keep rolling them over and over and over trying to kind of hide it and pretend that it’s not there, but this process continues. Mike, let me lay this on you. It’s just that we’ve had, as we speak, five trading days in the year 2020. In those five trading days, there have already been 67,713 Comex contracts shifted off of the exchange and exchanged for physical, as they say again, in London. 67,000. Mike, again every contract is a hundred ounces. That’s 6.7 million ounces. That’s 210 metric tons of gold.

The whole Comex vaults only holds 8 million ounces and they shifted 210 metric tons, 6.7 billion ounces off exchange in just five days? This is the scam of the greatest order, and like I said, again, the amazing thing is that it still exists… that people in 2020, when the world is all interconnected and everybody knows everything and I can watch missiles take off in Iran five minutes after they’re shot just by following Twitter. It’s amazing that this continues. It’s just mind boggling that this is allowed to continue.

Mike Gleason: Yeah. Well put, you beat your head against the wall trying to figure out when it’s going to finally end and why there’s not more talk about it. Well, Craig, before we wrap up, I’d like to get any final thoughts. I know you’ve got a lot to say here early in the year. If you could give metals investors an idea of what it is that you’re going to be watching most closely, what they should be watching most closely over these first few months of the year, and then maybe a sign that perhaps the powers that be are losing control, or any other comments you want to make here as we wrap up?

Craig Hemke: Yeah, I don’t know, Mike. Since I’ve been doing this, and I have to admit kind of fallen forward a little bit and getting excited about it myself back in 2009 and ’10, that kind of thing. This hyperbole of, “The Comex is going to fail.” Come on. That’ll all happen in a blink of an eye someday or overnight, but to sit there and … these people that say it’s going to fail above $22 silver. I mean, come on. We’ll see. The banks are going to keep it going as long as they possibly can and I don’t think anybody can come up with a time table for it. The only thing it that will end is a run on the banks for physical metal, and this kind of thing gains momentum and it snowballs and finally that realization of what a scam at all is sinks in and people panic to get their hands on actual mental while they can. Again, I can’t stress this enough, ignore the perma-bears with an agenda.

They’re trying to talk down the market. They’re trying to talk down the shares, or trying to talk down the individual shares because they have some massive short position. The Fed is going to continue with the repo crisis. It’s not going away. The U.S. is going to have at least a $1.2 trillion deficit every year this decade. That’s what the Congressional Budget Office says. That money’s got to come from somewhere. The central banks cannot afford a deflationary collapse. They will be printing and printing and printing. Even absent that argument about what that does to the dollar and all this other stuff, that cash goes someplace, and it goes everywhere. Again, it’s not a mistake that the HUI… was up 20% since October 15th… is now up 15%. What happened on October 15th? That’s when this whole new not-QE debt monetization program kicked in.

Everything’s going up. Okay? So everything’s going to continue to go up. The banks are going to throw up roadblocks. We’ve already got 800,000 contracts of open interest Comex gold. So, I don’t know how far gold will go. $1,650? Maybe if it kind of gets rolling, it can go to $1,750 this year. That’d be a pretty good year from where we are. Where I think the real interest should be, for people that want to either have some fun, make some trading fiat currency that then they can buy more physical metal, that kind of thing … I mean start looking into whether or not you have exposure to the mining shares, not just the big companies, but the medium juniors and the explorers, that kind of stuff, because as global asset managers, who have all this cash, and they’re always looking for a place to go. Once the GDX, the DDXJ, the HUI begin to make new highs versus 2016, the floodgates are going to open and money’s going to come pouring into the sector and it all has to pass through a little tiny funnel because there’s only so many places it can go.

It’s just simple economics. You get twice the cash chasing the same handful of stocks, and they’re going to go up in price. So, I think it’s going to be a very good year again for the metal, just like last year was, and I was right when I predicted it last year. But I think the real outsize gains will probably be in the shares more than in the physical metal. I wrote that up. I kind of make an annual forecast every January. I posted it to my site. It’s a free link. Maybe I’ll send it to you, Mike. You can put it on this page. I always try to come up with a catchy name, so this year’s title is 2020 Foresight, instead of 2020 hindsight. Kind of clever, huh?

Anyway, 2020 Foresight is what it’s called. You can go to my site, or like I said, click the link, if you can put it on this page, and it will just explain to you the basis for why I think it’s going to be a good year. If you’ve got time, I think it’s worth a read.

Mike Gleason: Yeah, it would be time well spent for sure. I always say, we spend a lot of time looking at your site here in this office. It’s money well spent for anybody that wants to get on board there with TF Metals Report. And before we let you go here, Craig, tell people a little bit more about your site, how they can get signed up, and maybe some other tidbits they should know.

Craig Hemke: Well really the best thing about my site, I mean I do analysis every day and we try to keep people locked into the big picture, not the tick by tick stuff, but the site is… I mean the people that populate it are from all around the world, all different political views, but we realize we’re all in the same boat, and so instead of bickering at each other and name calling and all that kind of stuff, rule number seven in the community guidelines is treat others the way you want to be treated. Come on, your mother taught you that. Why do you think just because it’s an anonymous website, you can be rude and mean like Twitter, things like that. So anyway, the community itself is what’s worth it.

It’s only 12 bucks a month. So it’s not like I’m getting rich off of it. 40 cents a day to give you access, really keep you on top and grounded of where we’re headed. And again, I just can’t emphasize enough. I mean Mike, the old line is a rising tide lifts all boats, right? Think of the rising tide being all of the cash. It has to be created from nothing. You must understand, this is direct monetization of the debt by the Fed. Primary dealers, they get the Treasury bills, soon to be Treasury notes from the Treasury. The primary dealers are the ones responsible for making that market and getting them filled. They buy them themselves, and anybody can, ZeroHedge has been great about writing this. The Fed then buys these directly from the primary dealers about 72 hours later. Okay, so there’s an intermediary in between, but basically the Fed is buying the Treasury bills, soon to be notes, directly from the Treasury.

How that isn’t direct monetization of that? I don’t know. Just because there’s a step in between? So, this is happening, Modern Monetary Theory, all that stuff that the politicians daydream about, that’s coming, and whether you are going to want to talk about gold standard and system reset and all that kind of stuff, whatever. Yeah, sure. But all of that cash is going to be sloshing around. Stock market’s going to go up, everything. So, gold and silver are going to go up and the shares are going to be particularly advantageous to own in the next few months. And so, again, I just want to keep everybody grounded and not be thinking about the events of Tuesday, and I mean that was a real, you want to talk about one off, that was a one off. That was hopefully something that you’ll never see again in your lifetime. This on the brink of maybe nuclear war in the Middle East. Ignore the reaction to it, the run up to it and look at the bigger picture and I think you’ll see that physical gold and silver and maybe some mining shares must be a part of a portfolio in 2020 going forward.

Mike Gleason: Yeah, well put. It’s going to be a great time to kind of focus more in on this if you’re not already doing that, and it’s going to be an interesting maybe, tumultuous year. Ignore the blips or don’t pay as much attention to them. We do have a trend in place here and Craig and TF Metals Report is a great way to follow that, hopefully right here on this podcast as well.

Well, very good. Thanks again Craig. Have a great weekend. I wish you a happy and prosperous New year and we look forward to catching up with you again soon. Keep up the good work, my friend.

Craig Hemke: All the best, Mike. Go Chiefs!

Mike Gleason: Yeah, good luck to your Chiefs this weekend. Well, that will do it for this week, thanks again to Craig Hemke. The site is TFMetalsReport.com, definitely a fantastic source for all things precious metals and a whole lot more. We urge everyone to check that out if you haven’t already done so for some of the very best commentary and analysis on the metals markets that you will find anywhere.

And be sure to check back here next Friday for our next Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange. Thanks for listening and have a great weekend, everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

This is a trick question because it depends on who you ask.

To someone who has a good strategy and risk management scheme, Forex trading is definitely worth it. They do it consistently, and in many cases, live off of it.

If you ask someone who has tried to get rich quick through Forex trading and migrated from broker to broker because each of them is playing some kind of scam, they’ll probably say it’s not worth it.

The fact of the matter is, banks, hedge funds, and even multinational corporations engage in some form of Forex trading. And they wouldn’t be doing it, if it wasn’t worth it.

What If I’m Not a Multinational Corporation?

The real question for the (potential) retail FX trader is whether Forex trading is worth it for them. And that’s a bit like asking whether being a lawyer or a plumber is worth it.

If you can learn how to do it, and it’s something you enjoy, then Forex, like any other form of making money, is definitely worth it.

You might see warnings on reputable FX broker sites that show high percentages of people losing money. That’s usually because people get into Forex trading without doing their homework, and spending enough time on a demo account to get enough experience.

The fact you are reading this shows you are doing at least some research, so you’re on the right track.

The key is to think of Forex trading as a consistent, long-term investment activity, and not as a one-off, get-rich-quick scheme. The latter is where all the people who think Forex isn’t worth it come from.

How Much Can I Make?

In order to evaluate whether something is worth the effort, you have to have a realistic grasp of what the gain is.

How much gain you get depends on several personal factors, such as the FX strategy used, the type of trading, how often you trade, what kind of trade psychology you have, your discipline and your ability to manage risk… among others.

See? Forex isn’t something you can just jump into.

That being said, it is possible to make relatively large returns on your investment (compared to, for example, a standard safe investment such as indexed mutual funds). However, the higher the return, the less likely it is that you will be able to achieve it.

What to Expect

For reference, the median return on investment (that is, half of FX traders make more than this, half make less than this) is around 10% per month.

That means that if you have $15,000 in your account, as a median successful you’d make around $1,500 per month. Of course, that’s just a rough estimate, and how much you could make depends on your decisions. And almost all of those Forex traders took at least a couple of years to get enough experience to get to that level.

Like all things, Forex requires practice to get good at it; and can be very rewarding for those who like it.

The near-term events expected to trigger movement of the biotech’s share price are outlined in a ROTH Capital Partners report.

In a Jan. 2 research note, ROTH Capital Partners analyst Jonathan Aschoff reported that he is assuming coverage on VBL Therapeutics (VBLT:NASDAQ) and changing its target price to $5 per share. The stock is now trading at around $1.26 per share.

Also, Aschoff highlighted that 2020 for VBL Therapeutics will be “catalyst rich” with respect to its lead drug candidate, VB-111, which it is developing for three initial oncology indications: recurrent, platinum-resistant ovarian cancer, glioblastoma multiforme and colon cancer.

Specifically, two interim data readouts are expected in Q1/20 and Q4/20 from VBL’s Phase 3 ovarian cancer trial. The analyses of those data “will evaluate efficacy and futility, as well as serve as an indication that the trial is progressing like the successful prior 21-patient Phase 1/2 ovarian cancer trial that was presented at the annual meeting of the American Society of Clinical Oncology in 2019,” Aschoff explained.

In addition, the analyst pointed out, two further studies involving VB-111 are expected to be launched in Q1/20. One is a randomized, controlled investigator-sponsored trial in recurrent glioblastoma multiforme, for which complete results are anticipated in Q1/21.

The other is a National Cancer Institute-sponsored, colon cancer trial in which VB-111 will be evaluated in combination with the checkpoint inhibitor Opdivo. An initial data readout for that study is anticipated in Q4/20. “The NCI trial is of particular interest because it may show synergy between VB-111 and widely used immunotherapy,” Aschoff indicated.

Two further catalysts expected in late 2020 are investigational new drug application filings by VBL Therapeutics for two of its monoclonal antibodies (mAb) in development: its traditional anti-inflammatory mAb VB-601 and its bispecific anticancer mAb VB-611. These mAbs target MOSPD2, a protein the biopharma has characterized comprehensively. “We believe there is genuine potential outside interest in drugs having this mechanism of action,” commented Aschoff.

He concluded that ROTH’s $5 per share, 12-month price target on VBL Therapeutics is wholly based on the company’s commercial success in the U.S. of VB-111 in ovarian cancer, primarily the recurrent, platinum resistant kind, and in recurrent glioblastoma multiforme. ROTH has a Buy rating on the biopharma.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Disclosures from ROTH Capital Partners, VBL Therapeutics, Company Note, January 2, 2020

Regulation Analyst Certification (“Reg AC”): The research analyst primarily responsible for the content of this report certifies the following under Reg AC: I hereby certify that all views expressed in this report accurately reflect my personal views about the subject company or companies and its or their securities. I also certify that no part of my compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

ROTH makes a market in shares of VBL Therapeutics and as such, buys and sells from customers on a principal basis.

Shares of VBL Therapeutics may be subject to the Securities and Exchange Commission’s Penny Stock Rules, which may set forth sales practice requirements for certain low-priced securities.

Within the last twelve months, ROTH has received compensation for non-investment banking securities-related services from VBL Therapeutics.

ROTH Capital Partners, LLC expects to receive or intends to seek compensation for investment banking or other business relationships with the covered companies mentioned in this report in the next three months.

Dollar bears triggered a knee-jerk reaction in sending the Dollar index (DXY) lower by 0.16 percent to break below 97.1 in the minutes following the latest US non-farm payrolls report. However, that decline counted for naught as DXY was then quickly restored above the 97.2 mark.

In December, the US economy added 145,000 new jobs, which is lower than the 160,000 figure that markets had expected. Average hourly earnings also underwhelmed at 2.9 percent, which is its slowest growth since July 2018. The unemployment rate however held steady at 3.5 percent, which is the lowest in about five decades.

Although the US jobs market appears to have lost momentum at the tail-end of 2019, the Federal Reserve is unlikely to adjust its benchmark interest rates in 2020, with Fed officials often insisting that the US economy is in a good place. Still, if US consumers begin to show surer signs of faltering and cannot keep the US economy chugging along, then policymakers may have to conduct more policy easing in order to support the world’s largest economy. Should the prospects of a US rate cut grow, then a softer Dollar is expected to follow in tow.

Gold bulls struggling as Dollar bears falter

Having meandered along the $1550 line since January 9, Gold climbed some 0.6 percent to pass $1556 in an immediate reaction to the underwhelming December US non-farm payrolls, only to find such gains fleeting as the Dollar quickly rebounded. Bullion bulls are struggling to find cause for a sustained liftoff back to $1600, after the US and Iran appeared to walk away from the brink of an all-out conflict earlier this week. The abruptness of the heightened US-Iran conflict over the past week however shows that investors cannot fully rule out heightened geopolitical risks, and such a sense of caution should keep Bullion relatively elevated above its 50- and 100-day moving averages which currently reside in the high $1400s.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

This is what the bears don’t get about oil stocks: These are no longer the reckless, wasteful, binge years of the shale boom. The smart companies have adapted to a new reality.

Now, it’s about dramatic new offshore discoveries that are being brought online in record speed.

It’s about brilliant new well-completion designs that enhance productivity.

It’s about integrated giants who win, either way.

It’s about extremely ambitious small-caps that slip into new venues and scoop up massive basins when no one’s looking.

It’s about ingenuity on multiple levels that translates into something for every investor appetite.

Here are 6 stocks to watch in 2020, and between them they cover every sort of risk-vs-reward level out there:

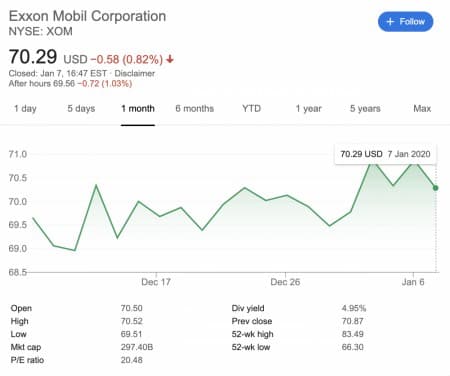

If dividends are what you’re after, look no further on the oilfield. Even the volatility of the oil and gas market over the past years have failed to disrupt Exxon’s dividend payouts.

First, the supergiant’s Q3 earnings report last week was better than expected, with earnings of 75 cents per share–compared to analyst estimates of 67 cents. Sales, at $65.05 billion, also beat estimates. And it’s planning to double its cash flow through 2025.

One of the most exciting things is the new oil that will come online from the superstar Guyana-Suriname Basin and Exxon’s 14 finds that just put Guyana on the oil map.

It’s also got new production and infrastructure coming online in the Permian basin, not to mention a major LNG project in Mozambique.

Our assessment is that Exxon is recovering nicely, and 2020 should see much better performance, particularly following the divestment of its North Sea assets for a cool $3.5 billion.

But overall, the great thing about Exxon is that no matter how oil prices fluctuate, this integrated giant is covered. Lower oil prices help its upstream assets, while higher prices boost the downstream.

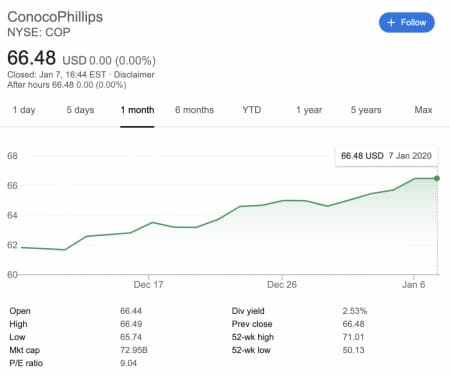

Few oil stocks shared in as much glory as COP when it comes to Q3 earnings. Not only did COP report a net income increase to $2.74 share, or $3.056 billion, but it also managed adjusted earnings of $914 million, or $0.82 per share.

Earlier in October, it also announced a 38% increase in its quarterly dividend, along with plans to repurchase $3 billion of shares next year.

COP has had lots of ups and downs this year, but this is what we like: It’s refocusing more narrowly on US shale, and on the Permian in particular. It’s spent the last year cutting costs and getting slimmer and trimmer, including a deal to sell its Australian assets for $1.4 billion. It’s likely that US shale expansion plans are in the works here, so this is a bet on that.

Recon Africa has just received an exploration license for a huge area for a tiny company with a market cap of only around $28 million and shares selling for under $0.50. Yet, it’s got 90% of the exploration rights to a shale basin of 25,000 square kilometers, that’s the same size as the Eagle Ford. It acquired the oil and gas rights for the entire 6.3-million-acre Kavango Basin in Namibia— with Africa’s oil production friendly government.

It’s pretty unique for a company this small to have a basin this big, so when it happens, we take note. We’ve also taken note of the CEO, Jay Park QC, who is the former director of Caracal Energy, which was acquired by giant Glencore in 2014 for $1.3 billion. That puts RECO squarely on our radar. So does anything that goes through Bill Cathey, well known geoscientist. We’ve heard that Cathey examined the Kavango Basin magnetic data and said it’s comprised of a 30,000-foot sedimentary basin. That’s when RECO licensed rights to the rest of the massive basin.

They have a 90% interest in a 4-year exploration license leading to a 25-year production license on commercial discovery, and the first test wells are slated to be drilled in Q2 2020–just a few months away.

The Kavango Basin is part of the Karoo Supergroup of geology, and it’s also been shown to have the same depositional environment as Shell’s Whitehill Permian shale play, part of the Karoo Supergroup in South Africa.

Sproule – a tier 1 resource assessment company – estimated that Kavango has a potential 12 billion barrels of oil or 119 trillion cubic feet of natural gas. That’s just for the shale. It doesn’t include any conventional potential.

Namibia is one of the up-and-coming oil venues in the frontier of Africa. Ask Shell or Exxon, both of whom are acquiring a lot of assets here, making Recon a natural acquisition target if a commercial discovery is made.

Not only is HESS sharing in the future wealth of the outsized oil discoveries with Exxon in Guyana at the Stabroek Block, but it will also be getting a boost from the block’s ahead-of-schedule first production in December.

Right now, HESS is doing well enough as it is on its position in US shale, in the Bakken, and when it adds its Guyana production to its portfolio by the end of this year, that will outshine the Bakken. So, what’s good becomes even better.

This stock is looking great going into 2020, and it exceeded its Q3 output guidance based on the Bakken alone. In fact, Hess’ Bakken production got a 38% boost year-on-year–way past expectations–and thanks in part to a new well-completion design to enhance productivity. That’s really what we like to see.

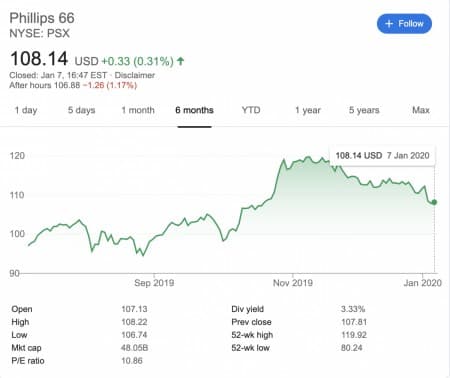

PSX soared more than 15% in October. It’s loving the low oil prices for its refineries, and now it’s busy building up pipelines, too, to carry all that Permian largesse to the refiners.

It’s targeted over $4 billion in pipelines. The next big pipeline in the … pipeline is one that leads from the Permian Basin to the Gulf Coast–meeting a major demand and allowing Phillips 66 to rake in more cash on more cheap North American oil.

This company is a bet on low oil prices–bottom line.

Fairly confident in the knowledge that nothing short of WWIII will result in a surge in oil prices at this point, this is Phillips 66’s playground through the rest of this year and presumably into 2020.

That’s refining + roaring midstream businesses that are doing much more than thriving in this atmosphere.

Halliburton is one of the largest oilfield services companies in the world. The company has secured its place as a giant in the oil and gas industry. But it didn’t happen overnight.

Over the past month, Halliburton has jumped by 12% on a string of positive news.

The oilfield services sector is highly competitive and ripe with innovation. In order to stay ahead, companies must be on the absolute cutting edge of technology. And that’s exactly what Halliburton has done.

And recently, Halliburton increased the heat for its competition. Partnering with Microsoft, Halliburton has become one of the most exciting “tech” plays in the industry.

This partnership is significant. Microsoft, a leader in the tech world, is looking to bring machine learning, augmented reality, and the Industrial Internet of Things to the oil and gas industry, and Halliburton is welcoming the new take on the resource realm with open arms.

In addition to its forward looking approach with regards to technology, Halliburton is also wheeling and dealing in the traditional oil world.

In its efforts to expand outside of the U.S. shale boom, the oilfield services behemoth has secured major deals in the Middle East, including a $597 million contract with Kuwait Oil Company to help develop its offshore program.

**IMPORTANT! BY READING OUR CONTENT YOU EXPLICITLY AGREE TO THE FOLLOWING. PLEASE READ CAREFULLY**

Forward-Looking Statements. Statements contained in this document that are not historical facts are forward-looking statements that involve various risks and uncertainty affecting the business of Recon. All estimates and statements with respect to Recon’s operations, its plans and projections, oil prices, recoverable oil, production targets, production and other operating costs and likelihood of oil recoverability are forward-looking statements under applicable securities laws and necessarily involve risks and uncertainties including, without limitation: risks associated with oil and gas exploration, development, exploitation and production, geological risks, marketing and transportation, availability of adequate funding, volatility of commodity prices, imprecision of reserve and resource estimates, environmental risks, competition from other producers, government regulation, dates of commencement of production and changes in the regulatory and taxation environment. Actual results may vary materially from the information provided in this document, and there is no representation that the actual results realized in the future will be the same in whole or in part as those presented herein. Other factors that could cause actual results to differ from those contained in the forward-looking statements are also set forth in filings that Recon and its technical analysts have made, We undertake no obligation, except as otherwise required by law, to update these forward-looking statements except as required by law.

Exploration for hydrocarbons is a speculative venture necessarily involving substantial risk. Recon’s future success will depend on its ability to develop its current properties and on its ability to discover resources that are capable of commercial production. However, there is no assurance that Recon’s future exploration and development efforts will result in the discovery or development of commercial accumulations of oil and natural gas. In addition, even if hydrocarbons are discovered, the costs of extracting and delivering the hydrocarbons to market and variations in the market price may render uneconomic any discovered deposit. Geological conditions are variable and unpredictable. Even if production is commenced from a well, the quantity of hydrocarbons produced inevitably will decline over time, and production may be adversely affected or may have to be terminated altogether if Recon encounters unforeseen geological conditions. Adverse climatic conditions at such properties may also hinder Recon’s ability to carry on exploration or production activities continuously throughout any given year.

DISCLAIMERS

ADVERTISEMENT. This communication is not a recommendation to buy or sell securities. Oilprice.com, Advanced Media Solutions Ltd, and their owners, managers, employees, and assigns (collectively “the Company”) may in the future be paid by Recon to disseminate future communications if this communication proves effective. In this case the Company has not been paid for this article. But the potential for future compensation is a major conflict with our ability to be unbiased, more specifically:

This communication is for entertainment purposes only. Never invest purely based on our communication. We have not been compensated but may in the future be compensated to conduct investor awareness advertising and marketing for TSXV:RECO. Therefore, this communication should be viewed as a commercial advertisement only. We have not investigated the background of the company. Frequently companies profiled in our alerts experience a large increase in volume and share price during the course of investor awareness marketing, which often end as soon as the investor awareness marketing ceases. The information in our communications and on our website has not been independently verified and is not guaranteed to be correct.

SHARE OWNERSHIP. The owner of Oilprice.com owns shares of this featured company and therefore has an additional incentive to see the featured company’s stock perform well. The owner of Oilprice.com will not notify the market when it decides to buy more or sell shares of this issuer in the market. The owner of Oilprice.com will be buying and selling shares of this issuer for its own profit. This is why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

NOT AN INVESTMENT ADVISOR. The Company is not registered or licensed by any governing body in any jurisdiction to give investing advice or provide investment recommendation. ALWAYS DO YOUR OWN RESEARCH and consult with a licensed investment professional before making an investment. This communication should not be used as a basis for making any investment.

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Investing is inherently risky. Don’t trade with money you can’t afford to lose. This is neither a solicitation nor an offer to Buy/Sell securities. No representation is being made that any account will or is likely to achieve profits similar to those discussed.

By CentralBankNews.info Peru’s central bank kept its monetary policy rate steady at 2.25 percent, noting the risks to global growth have eased but the impact of recent geopolitical events on international energy prices is still uncertain. The Central Reserve Bank of Peru (BCRP), which cut its rate twice in 2019, most recently in November, also said the rate had been maintained as inflation is expected to be around 2.0 percent over the forecast horizon but with a moderate downward bias due to the possibility of lower-than-expected increase in domestic demand. Last month the central bank lowered its estimate of 2019 economic growth to 2.3 percent from a previous 2.7 percent but maintained its outlook for this year of 3.8 percent. Today BCRP said expectations of business expectations had remained stable in December from November while indicators of economic activity point to a gradual closing of the output gap. Last year Peru’s economy was hit by a combination of slower global demand for its mining output, political uncertainty and a decline in public investment, with the fiscal deficit shrinking to an estimated 1.7 percent of gross domestic product. This year the fiscal deficit is seen narrowing further to 1.6 percent. Peru’s mining sector accounts for around 15 percent of GDP and 60 percent of exports and Julio Velarde, BCRP governor, said on Dec. 20 higher mining output this year will boost growth. Peru’s inflation rate rose slightly to 1.9 percent in December from 1.87 percent in November and the central bank has forecast 2.0 percent inflation for 2020, in line with its target of 2.0 percent, plus/minus 1 percentage point. Peru’s sol has been relatively stable in the last four years and was trading at 3.32 to the U.S.dollar today, slightly down from 3.31 at the start of this year but up 1.8 percent since the start of 2019. Last month the International Monetary Fund (IMF) called on BCRP to greater exchange rate flexibility to help absorb external shocks and promote financial development as the level of dollarization in the country is declining. BCRP on occasions intervenes in the foreign exchange market, reflecting concern over liability dollarization, but loan dollarization is now at 39 percent for firms and 10 percent for households so greater exchange rate flexibility carries lower risks. “Limiting central bank intervention to cases of disorderly market conditions could help reduce dollarization further, encourage the use of hedging instruments, and strengthen the interest rate channel of monetary policy,” IMF said on Dec. 3.

The Central Reserve Bank of Peru issued the following statement:

“1. The Board of Directors of the Central Reserve Bank of Peru (BCRP) decided to maintain the reference at 2.25 percent, in light of the following developments: i. Year-on-year inflation is expected to be around 2.0 percent over the forecast horizon, with a moderate downside bias due to the possibility of a lower-than-expected increase in domestic demand. ii. Monthly inflation was 0.21 percent in December, consequently, year-on-year inflation remained at 1,9 percent in December 2019. With monthly inflation excluding food and energy at 0.34 percent in December, the year-on-year figure also remained at 2.3 percent. iii. One-year ahead expected inflation as of December remained at 2.2 percent. iv. The weak performance of primary industries and General Government investment in 2019 was attenuated by the activity in non-primary industries. Business conditions expectations as of December remained stable with respect to November, while economic activity indicators point to a gradual closure of the output gap. v. Global growth risks from trade tensions have attenuated, although the impact of the recent geopolitical events on international energy prices is still uncertain.

2. The BCRP Board pays close attention to new information on inflation and its determinants in assessing future changes in the monetary policy stance.

3. The Board also decided to maintain the interest rates on BCRP off-auction credit and deposit operations in domestic currency with financial entities. i. Overnight deposits: 1.00 percent per year. ii. Direct security/currency repo and rediscount operations: i) 2.80 percent per year for financial entities’ first 10 operations over the last 12 months; and ii) the rate fixed by the BCRP Monetary and Foreign Exchange Operations Committee for operations other than financial entities’ first 10 operations over the last 12 months. iii. Dollar swaps: a fee equal to a minimum annual effective cost of 2.80 percent.

4. The BCRP Board’s next monetary policy session will take place on February 13, 2020.”

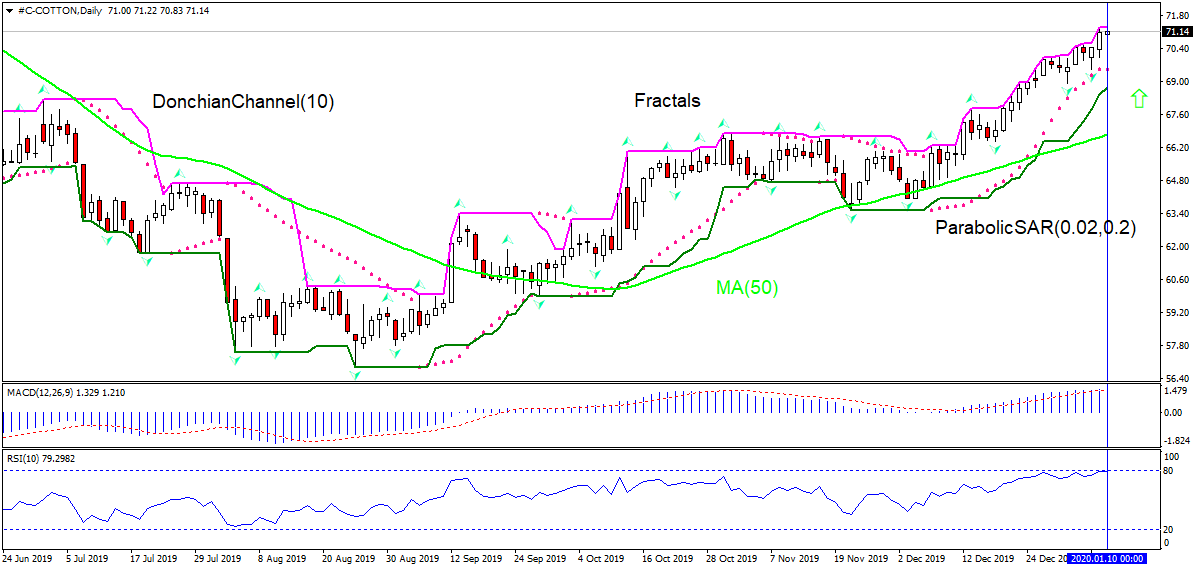

Lower cotton supply forecast bullish for Cotton price

Analysts expect lower US cotton production. Will the Cotton price rise continue?