After initially rallying on geopolitical tensions during the early parts of January, WTI Crude and Brent have both taken a painful beating over the past few weeks. Rising concerns over Asian economic growth and oil demand weakening from the coronavirus outbreak in China sent oil prices tumbling to levels not seen since November 2019 below $55 on Thursday. WTI Crude has depreciated more than 5% this week and almost 10% since the start of the year!

The path of least resistance for oil prices will most likely point south for the time being due to a host of factors. China is the world’s largest energy consumer, so essentially a drop in demand due to slowing economic growth should negatively impact oil markets. Another theme weakening oil is the mighty Dollar. General uncertainty and unease could force investors to maintain some distance from riskier assets with safe-haven destinations like the Dollar, Japanese Yen and Gold becoming attractive hotspots.

If uncertainty over US-China trade ends up making an unwelcome return, this could be the knockout blow that sends oil prices crashing towards $50.

From a technical standpoint, WTI Crude is under intense selling pressure on the daily timeframe with prices trading around $55.32 as of writing. A breakdown below $54.80 should encourage selloff towards $53.70. Should $54.80 prove to be reliable support, Oil prices could rebound towards $57.60.

ECB meeting another snoozer

In other news, the European Central Bank left monetary policy unchanged as widely expected.

The Euro fell to a seven-week low below 1.1040 at after European Central Bank President Christine Lagarde struck a slightly more dovish tone than some expected during the press conference. Moving forward, the EURUSD is likely to bounce within a wide 150 pip range until a fresh directional catalyst is bought into the picture.

Technical traders will continue to closely observe how the EURUSD trades around 1.1050. A decline towards 1.1000 could open a path towards 1.0879 in the medium to longer term.

Commodity spotlight – Gold

Gold held gains on Thursday, finding comfort around $1565 after the European Central Bank left monetary policy unchanged.

Appetite towards the precious metal should remain supported by growing fears over the coronavirus outbreak in China. The general uncertainty is likely to accelerate the flight to safety with Gold seen testing $1580 in the short term. Should $1555 prove to be an unreliable support level, prices could slip back towards $1545.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

– With initial production at its Argentina project expected in 2022, Peter Epstein of Epstein Research believes the company could be an “excellent” bet when lithium prices rebound.

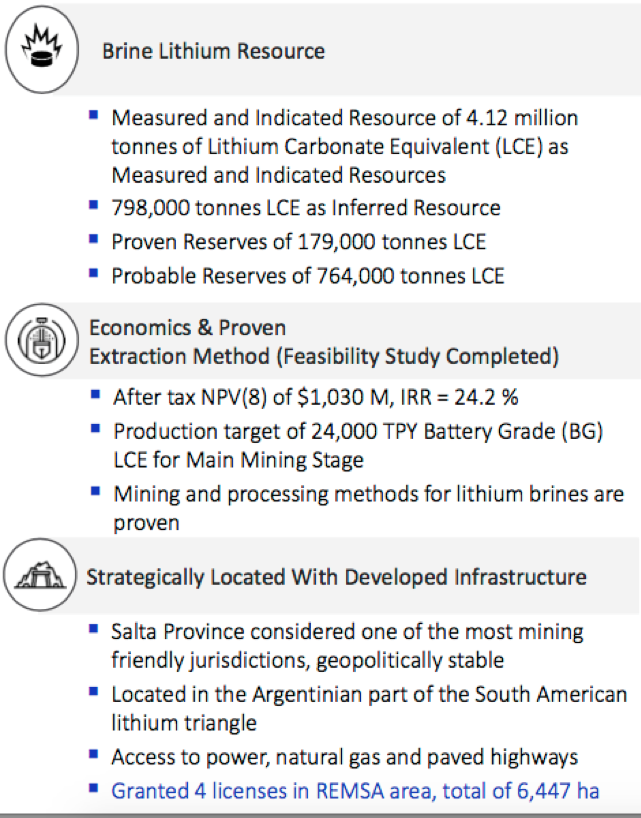

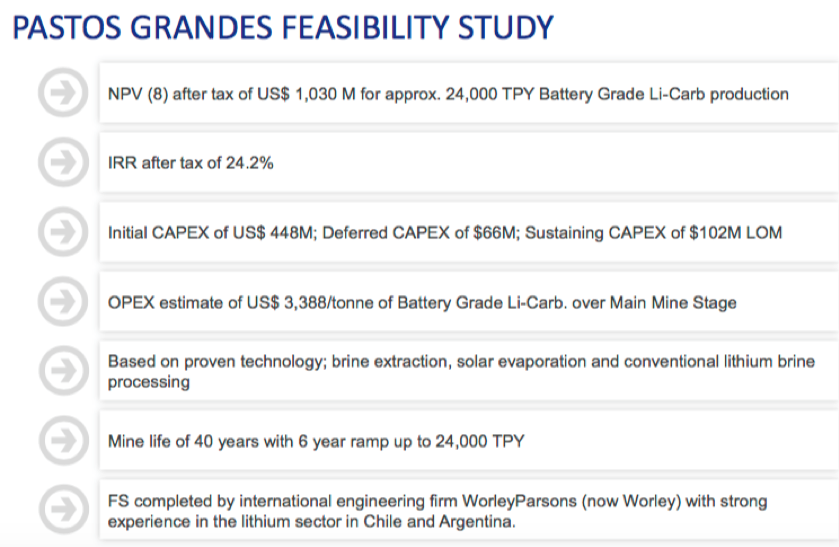

Earlier this month, the mining court of Salta, Argentina, granted Millennial Lithium Corp.’s (ML:TSX.V; MLNLF:OTCMKTS) Argentine subsidiary four mining licenses on its 100%-owned Pastos Grandes project in Salta province. Readers may recall that Millennial recently delivered a bank feasibility study (BFS) and expects to reach initial production in 2022 (subject to funding and permits), ramping up to nameplate capacity of 24,000 tonnes lithium carbonate equivalent (LCE)/year by mid-decade.

Farhad Abasov, president & CEO, commented: “Millennial is pleased to have received four mining licenses which comprise ~97% of the property area at Pastos Grandes. Millennial expects the final license to be granted in the near future. The company continues to actively advance its three-tonne-per-month lithium carbonate plant and pilot evaporation ponds. Millennial is moving forward with financing, off-take and other key strategic initiatives with large industry players.”

This news comes on the heels of the October announcement that the national mining secretary of Argentina granted a federal fiscal stability certificate (FFSC) for Pastos Grandes. The certificate outlines the tax regime, plus additional benefits bestowed on the project, and officially confirms a reduction in the corporate income tax rate from 30% to 25%.

CEO Abasov commented, “The granting of the FFSC assures the tax and additional benefit terms under which we can operate a lithium carbonate production operation. Receipt of the FFSC confirms our confidence that mining projects in Salta have the support of all levels of government.”

This means that, like Australia-listed Galaxy Lithium’s (GXY:ASX) Sal de Vida and Lithium Americas Corp. (LAC:TSX; LAC:NYSE)/Jiangxi Ganfeng Lithium Co. Ltd.’s (002460:CH) 50/50 joint venture (JV) (Cauchari-Olaroz) brine projects in Argentina, Millennial’s Pastos Grandes has both a BFS and fiscal stability package. At a time when many lithium brine projects in Chile and Argentina are moving very slowlyor are stalledit’s clear that Millennial’s management team is working closely with all stakeholders to successfully advance Pastos Grandes.

Unlike most peers, Millennial has been blessed with ample cash liquidity. Even today it’s sitting on ~$23 million, enough to last well into 2021 if necessary.

Exciting times ahead

Next is the lining up of strategic/financial partners, signing offtake agreements, raising construction capital, construction of ponds and plant, and first productionexpected in 2022. That’s about 1218 months behind Lithium Americas’ JV project. Importantly, Millennial will greatly benefit from valuable lessons learned from Lithium Americas’ and Galaxy’s development progress, as well as expansions underway at Livent Corp. (LTHM:NYSE) and Orocobre Ltd. (ORL:TSX; ORE:ASX).

Chile’s Albemarle Corp. (ALB:NYSE) and SQM (SQM:NYSE), and Argentina’s Livent, Orocobre, Galaxy and Lithium Americas are public companies. Problems with ponds or processing facilities at those companies will become known to Millennial’s technical team. Therefore, there’s a decent chance that mishaps at other projects can be avoided. Sometimes there are benefits to not being a first mover.

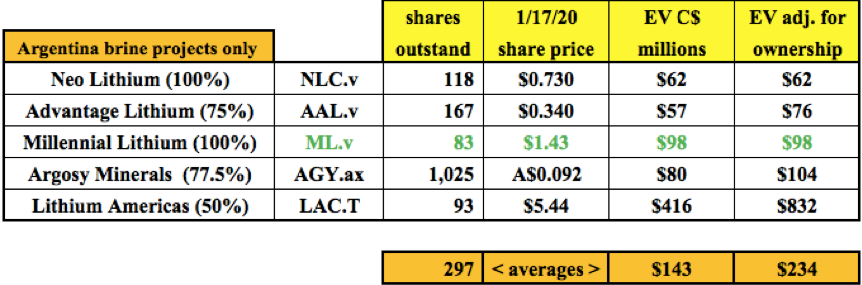

In addition to benefiting from the learning curve others are ascending, Millennial will enjoy regional infrastructure that is being built and/or expanded: roads, rail, power lines, natural gas pipelines, etc. Mining equipment and service providers are setting up offices to serve companies including Lithium Americas/Ganfeng, Livent, Orocobre, Galaxy, POSCO (PKX:NYSE), Neo Lithium Corp. (NLC:TSX.V), Argosy Minerals Ltd. (AGY:ASX), Advantage Lithium Corp. (AAL:TSX.V; AVLIF:OTCQX) and Millennial.

Readers should not take for granted the fact that Millennial owns 100% of its project. By contrast, Advantage Lithium owns 75% of its flagship project, Argosy Minerals owns 77.5%, Lithium Americas owns 50%, and Orocobre owns 66.5% of their respective projects.

Owning 100% of Pastos Grandes, with a BFS and fiscal stability pact in place, greatly enhances management’s ability to fund construction. Selling a meaningful portion of the project could raise a substantial amount of capital. That, combined with debt financing and (possible) advance payments from offtake agreements, would minimize the need for excessive equity capital.

Important derisking events to continue in H1 2020 In speaking with CEO Farhad Abasov, he and his board believe that news on one or more parts of a funding package could come within three to six months. Management is speaking with global industrial companies, some of which have already done substantial due diligence.

A few interested parties would like to see a staged ramp-up to minimize capex, so instead of moving to 24,000 tonnes LCE/year by 202526, [the company would get] to 10,000 tonnes and remain at that level, only expanding if/when market conditions warrant. In that scenario, capex could be reduced from US$448.2 million to under US$300 million. Then, operating cash flow could be deployed to partially fund an expansion from 10,000 to 24,000 tonnes at a later date.

Also, a few prospective partners have lithium extraction/processing technologies, or access to technologies, that (if they work at commercial scale) could further optimize Millennial’s operating flow sheet, potentially enhancing project economics. In some cases, the need for evaporation ponds would be eliminated.

Giant auto and battery manufacturers can very comfortably afford to fund projects like Millennial’s, with capex requirements of around half a billion US dollars. Although we haven’t seen much of that yet, it’s coming. Look no further than Benchmark Mineral Intelligence’s running tally of lithium-ion battery mega-factories. Benchmark Mineral Intelligence has been tracking the number of global mega-factories for years. The number has soared, currently standing at 115.

Ranked by size, the top 10 global automakersVolkswagen, Daimler, Toyota, Ford, BMW, GM, Hyundai, Tesla, Honda and Ferrarihave an average enterprise value (EV) of about US$135 billion. Any of these companies could fund even the largest lithium projects in the world. Yet, I estimate that fewer than ten new projects, brine, hard rock or clay-hosted, (>20,000 tonnes LCE/year) are likely coming online by 2025.

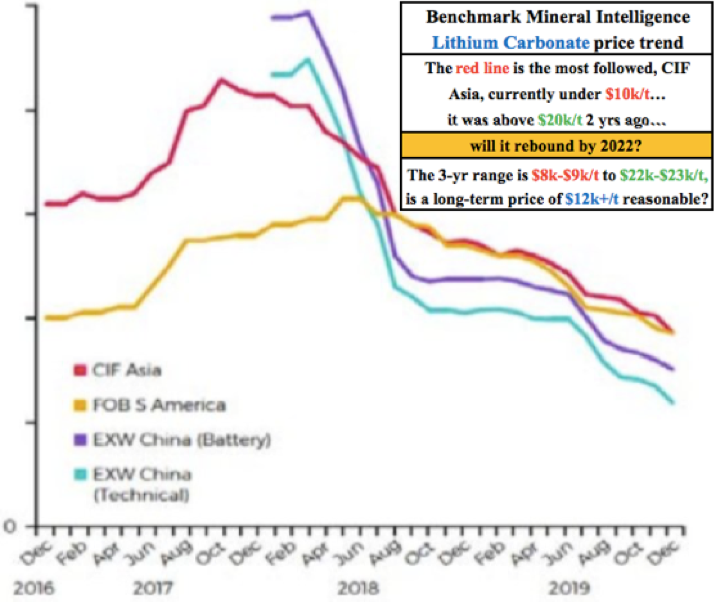

Lithium prices below US$10,000/tonne unlikely to last One of the main reasons for such negative sentiment in the lithium junior space has been the decline in lithium prices from unsustainably high levels above US$20,000/tonne. However, now below US$10,000/tonne, prices may have overshot to the downside. Many analysts and pundits believe that 2020 or 2021 will mark a bottom in the three-year slide in prices.

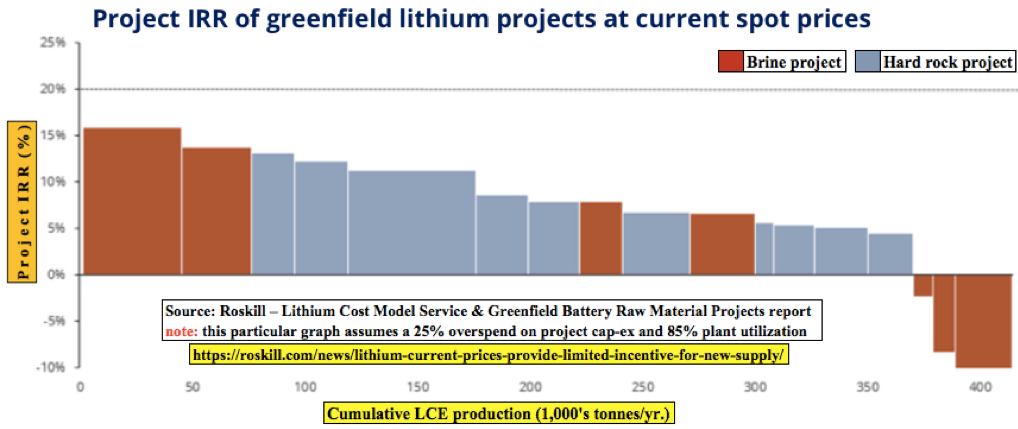

In the chart below, Roskill demonstrates why prices are likely to improve. At current spot levels, all advanced-stage hard rock and brine projects in the pipeline come in at under a 16% internal rate of return (IRR). Some projects have negative IRRs; the average is closer to 5% than 10%.

Millennial is poised for a great decade, and the 2030s could be even better. Management expects Pastos Grandes to be next in line in Argentina after Lithium Americas/Ganfeng. Any project, anywhere in the world, that comes to market and ramps up over the next five years should enjoy strong demand for its lithium offerings.

A major global supply source (about 1/3 of the market) is experiencing unexpected bottlenecks, uncertainty and delays. In Chile’s Atacama salar, both Albemarle and SQM had planned massive expansions to lithium carbonate production, upward of a tripling, from 2018 to 2021. Two years into these expansions, annual production has hardly budged.

More uncertainty and caution is expected as local communities have convinced a Chilean environmental court to uphold claims of excessive water use by SQM and Albemarle, seriously threatening their expansion plans. Therefore, this news should be supportive of lithium prices in the mid-to-longer term.

Conclusion Millennial Lithium has an excellent asset, more advanced (BFS-stage) than all but two or three global brine projects, with relatively low upfront capex compared to other mining and metals projects, producing a metal with expected annual demand growth of 15% (or more) over the next 10 years. Millennial has over $20 million in cash on its balance sheet.

Not many significant projects could possibly commence production by 2022not many at all, besides Lithium Americas and Galaxy. No new operations are coming in Chile in the next three to five years, and only a small handful in North America (Bacanora Minerals Ltd., Standard Lithium Ltd. [SLL:TSX.V; STLHF:OTCQX]). If lithium demand really takes off, few companies on the planet are better positioned to capture that need than Millennial Lithium.

Adjusted for ownership interests in their respective flagship projects, all but Lithium Americas trade at similar valuations. Any of these companies that successfully advance toward production (secure cornerstone investor[s], offtake agreement[s], commencement of construction, etc.) offer the potential for significant share price gains. Notice that Lithium Americas’ valuation is about four times that of the others.

Millennial is trading at just one-fourth the valuation, but could be only 1218 months behind Lithium Americas. Is this 75% discount warranted? Lithium Americas is fully funded on its 50% JV project and construction is well underway. Millennial owns 100% of its project, has ample cash liquidity, no debt, a BFS, four of five mining licenses have been granted, and has secured a signed federal fiscal stability certificate.

If one believes, like I do, that lithium prices will rebound, Millennial Lithium could be an excellent way to benefit from the rebound.

Peter Epstein is the founder of Epstein Research. His background is in company and financial analysis. He holds an MBA degree in financial analysis from New York University’s Stern School of Business.

Streetwise Reports Disclosure: 1) Peter Epstein’s disclosures are listed below. 2) The following companies mentioned in the article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy.

4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Author’s Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Millennial Lithium., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Millennial Lithium are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

AX1 Capital Corp. retained Epstein Research for a six-month advertising campaign. AX1 Capital is closely affiliated with Millennial Lithium. It is 100%-owned by a single individual who has a contract for services with Millennial Lithium. This individual owns 150,000 restricted share units and a similarly modest number of warrants in the company. Therefore, readers should consider Epstein Research [ER] to be biased in favor of Millennial Lithium. Peter Epstein of [ER] does not own any shares, warrants, options or restricted share units of Millennial Lithium.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Unlike most countries, New Zealand publishes its inflation data only once per quarter. This means there are a lot more expectations ahead of the release.

Many analysts are saying this is a key point that will set the trend for monetary policy for the next three months. And, by extension, this would affect how the NZD will trade for that period.

The current outlook suggests that the RBNZ is less likely than before to continue easing, and inflation is seen to finally have turned the corner. Until recently, optimism of Chinese growth following signing the Phase 1 trade deal with the US helped the outlook for New Zealand.

However, now with the outbreak of the coronavirus, there are increasing concerns that the Kiwis could be affected by a drop in travel, and slowing consumption in the Asian giant.

What We Are Looking For

Expectations are for the quarterly CPI change rate to slow this time around to just 0.1% compared to 0.7% in the prior quarter. But, and this appears to be the more relevant fact, it doesn’t stop the annualized inflation rate from moving up to 2.2% compared to 1.5% prior.

If expectations are met, it would put the inflation rate over the RBNZ’s target. It would, therefore, justify not cutting rates at least for the next three months. It would also be the highest rate since early 2017, long before the latest easing cycle.

The Partners Matter, Too

Another more recent factor that contributes to reducing expectations of action on the part of the central bank is the better than expected jobs data from Australia yesterday.

Analysts adjusted expectations for when the RBA would cut rates, pushing the balance of expectations firmly into the second quarter.

In the shorter term, though, the NZD isn’t likely to get much of an upside from global conditions. The virus outbreak has put markets off taking risks and delving into commodity currencies.

The next update from the WHO on the situation isn’t until Tuesday. And China starts its Lunar New Year holiday today, which means less guidance from New Zealand’s largest customer.

Market Moves

It should be noted that while the consensus is for the inflation rate to come in near, if not at the RBNZ’s target, there is still quite a range among views.

New Zealand-based economists, chief among those from Westpac, are more inclined towards sluggishness in the inflation rate. A result below 1,8% annual, for example, might be seen as insufficient by many traders. And it could lead to increased speculation that the RBNZ could take action soon.

On the other hand, the top of the range is as high as 2.3%, mostly from foreign analysts. However, as an object of carry trading and speculation, a lot of NZD moves are related to relative strength in other currencies.

So, a result above 2.0% might be more in line with what the market is expecting. As a result, it might not offer as much upside.

Expectations of US output increase bearish for BRENT

On the daily timeframe #C-BRENT: D1 has breached below the 200-day moving average MA(200), which is declining. This is bearish.

We believe the bearish momentum will continue after the price breaches below the lower boundary of Donchian channel at 61.46. A level below this can be used as an entry point for placing a pending order to sell. The stop loss can be placed above 62.46. After placing the order, the stop loss is to be moved every day to the next fractal high, following Parabolic signals. Thus, we are changing the expected profit/loss ratio to the breakeven point. If the price meets the stop loss level (62.46) without reaching the order (61.46), we recommend cancelling the order: the market has undergone internal changes which were not taken into account.

EIA forecasts US domestic crude oil output increase. Will the BRENT decline?

The Energy Information Administration forecast a monthly rise in US shale oil production of 22,000 barrels a day to 9.2 million barrels a day in February in the latest monthly report issued Tuesday. This followed another bearish sign for oil – Baker Hughes reported last Friday that the number of active US oil rigs rose by 14 to 673 this week. That is the first increase in four weeks. In the previous monthly report the Energy Information Administration forecast an oversupply of global petroleum relative to consumption. And trade group the American Petroleum Institute late Wednesday report indicated US crude supplies rose by 1.6 million barrels last week when a decline was expected. A spike in geopolitical tensions in Middle East is an upside risk for oil while output is seen rising in US.

Its been a rather muted week for the yellow metal. Following moves in both directions, gold is trading roughly flat on the week as of writing.

In the absence of any key US data, there has been limited movement in the USD, which is typically a big source of direction for gold prices. However, on the back of a slew of better data last week, the greenback has been broadly supported over the week, capping upside moves in gold.

The signing of the US/China trade deal has also taken some of the upward pressure out of gold. With the US and China now legally agreed on the terms of the phase-one trade deal, the market is confident that talks will soon progress onto the second phase of the deal, boosting expectations that the trade war will soon be brought to a proper end. This improved level of optimism around negotiations has again weakened safe-haven demand for gold.

However, the metal has found some support this week on lingering risk factors.

The outbreak of coronavirus in China, which has spread through parts of Asia and also reached the US, has fuelled some risk-off trading which has seen demand for hold. There is also some uncertainty around the ongoing Trump impeachment trial.

While the Republican-controlled Senate is unlikely to convict the President, the damage to his reputation and public-perception could negatively impact his chances for re-election later this year.

Technical Perspective

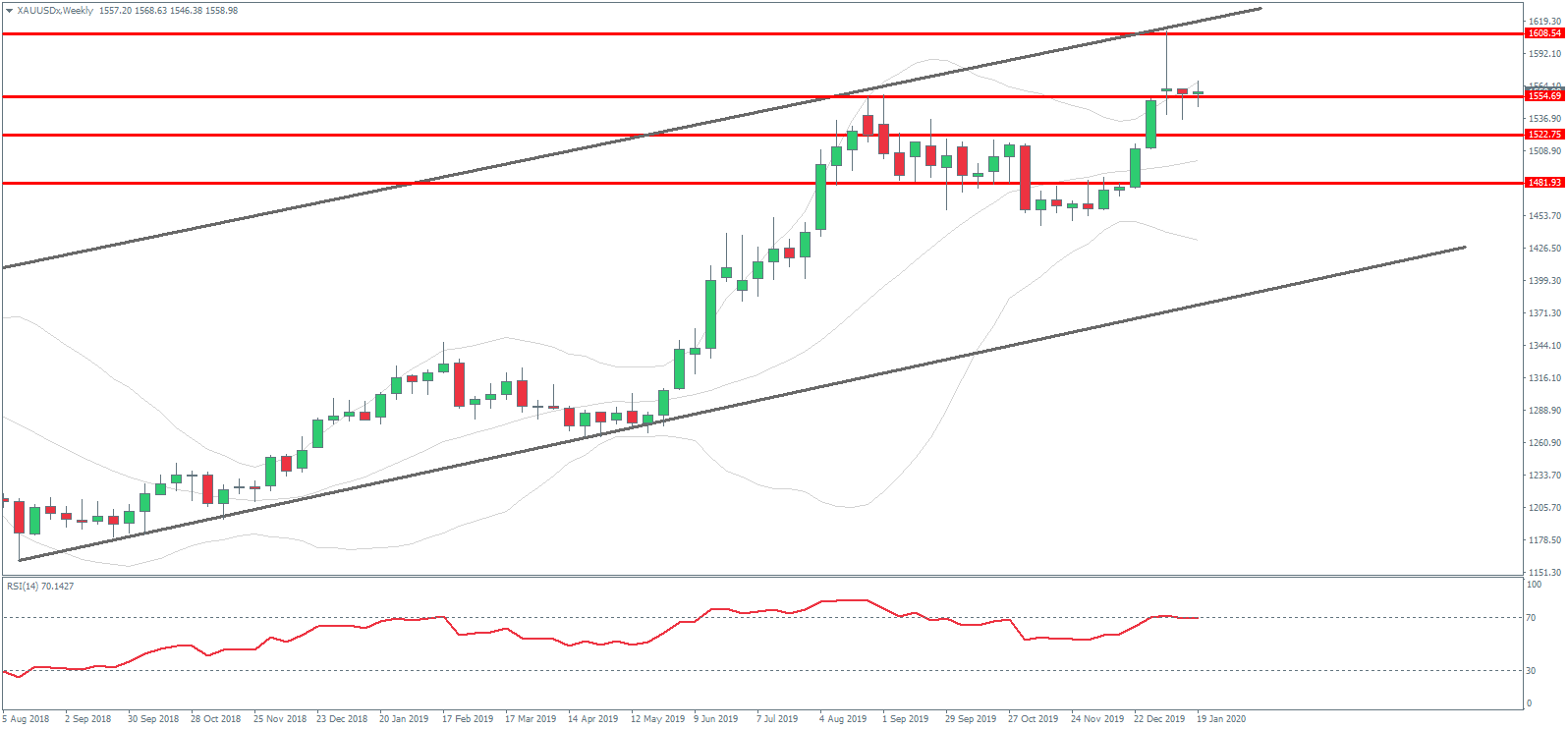

Gold prices continue to consolidate just above the broken 2019 highs around the 1554.69 level. The recent rejection from the 1608.54 level has failed to follow through.

While price holds above the 1554.69 level, a further push higher within the bullish channel looks likely. To the downside, a break of the 2019 lows would bring the 1522.75 level back into focus.

Silver

Silver prices have been a little worse off than gold this week.

Price is trading broadly lower over the week’s session. For the most part, the moves have tracked those of gold, though it seems volatility has been a little higher in silver this week, taking price lower.

As with gold, the main drivers continued to be expectations for the path of the US dollar, largely linked to incoming data and Fed signals, as well as risk-flows around the US/China trade talks.

Despite the positive steps being made in that space, the second round of talks presents far more risk of difficulty given the more complex nature of the issues to be addressed. As such, risk assets still face downside risks in the near term if talks are seen struggling.

Technical Perspective

Silver prices continue to range between the 17.3408 – 18.6397 level, caught between the two bearish trend lines. While price is still holding above the 17.3408 level, a further test of the 18.6397 level is still viable. To the downside, a break of 17.3408 would pave the way for a test of the 16.52 level next.

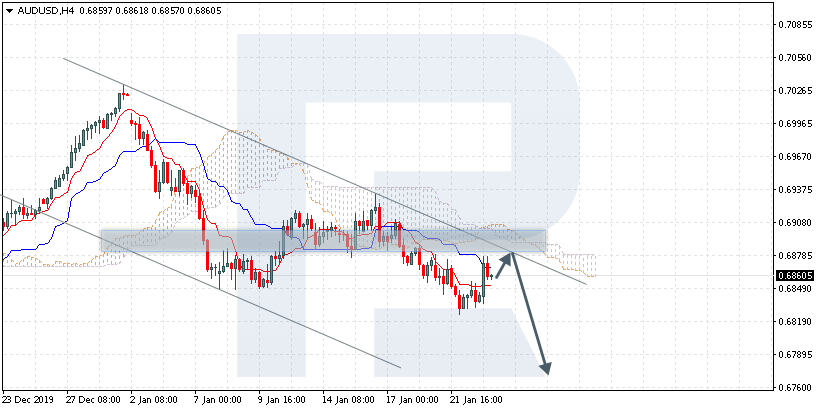

AUDUSD is trading at 0.6860; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 0.6875 and then resume moving downwards to reach 0.6765. Another signal to confirm further descending movement is the price’s rebounding from the descending channel’s upside border. However, the scenario that implies further decline may be canceled if the price breaks the cloud’s upside border and fixes above 0.6925. In this case, the pair may continue growing towards 0.7005.

NZDUSD, “New Zealand Dollar vs US Dollar”

NZDUSD is trading at 0.6588; the instrument is moving below Ichimoku Cloud, thus indicating a descending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 0.6615 and then resume moving downwards to reach 0.6485. Another signal to confirm further descending movement is the price’s rebounding from the resistance level. However, the scenario that implies further decline may be canceled if the price breaks the cloud’s upside border and fixes above 0.6645. In this case, the pair may continue growing towards 0.6735.

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is trading at 1.3167; the instrument is moving above Ichimoku Cloud, thus indicating an ascending tendency. The markets could indicate that the price may test Tenkan-Sen and Kijun-Sen at 1.3115 and then resume moving upwards to reach 1.3245. Another signal to confirm further ascending movement is the price’s rebounding from the support level. However, the scenario that implies further growth may be canceled if the price breaks the cloud’s downside border and fixes below 1.3010. In this case, the pair may continue falling towards 1.2935.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Investors look to today’s ECB’s monetary policy meeting knowing full well that the central bank will maintain the status quo. At best, the ECB will only review the impact of its monetary policy so far.

In terms of any surprises, the chances are minimal.

From a monetary policy perspective, the central bank will maintain interest rates at 0%. The marginal lending rate is likely to remain at 0.25% and the deposit facility rate at -0.50%. The central bank will also keep the asset purchases at the current 20 billion euro a month.

The decision to leave rates and asset purchases unchanged comes as the governing council prefers to assess the impact. The ECB last made changes to its monetary policy in September 2019.

This was done in response to sluggish inflation and slowing growth. This came at a time when the German economy was particularly hit hard. Being the growth engine for Europe, the decision came out as a timely response to stoke growth.

Regarding the larger scope of the monetary policy path, investors are also well aware that new ECB Chief Christine Lagarde, will be sticking to the tried and tested familiar path set by her predecessor, Mario Draghi.

Assessment of the Eurozone Economy

Since the September monetary policy changes, growth looks to have returned to the eurozone. However, this is something that is yet to show. Investors will be waiting for the Q4 GDP performance.

The preliminary GDP report for the eurozone is due on January 31st. However, early indicators such as the PMIs suggest that growth has stabilized. This was evident in the minutes of the December meeting.

The ECB released the December ECB meeting minutes last week. The report indicated that members of the ECB’s governing council were optimistic about growth. Although GDP is unlikely to turn the corner, preliminary data suggests that growth is stabilizing in the region.

Despite the slight optimism, the governing council members remain wary of the downside risks and a bit skeptical of the industrial output in the region.

Consumer price data last week confirmed that headline inflation grew at a pace of 1.3% on the year ending December 2019. While this is still far away from the target inflation rate of 2.0%, there were some positives to take away.

For example, at one point, inflation in the eurozone dropped below 1%, indicating that consumer prices could further deviate from the ECB’s target.

Given the overall preliminary data, the ECB is likely to give a cautious but optimistic review in its assessment of the eurozone economy.

Focus on ECB’s Strategic Review

Last week, news outlets reported that the ECB was preparing for a strategic review. This comes after the fact that the ECB Chief told policymakers to remain tight-lipped on the review.

The ECB strategic review will take place at today’s meeting after the members received the documents last week. Given the confidentiality of the strategic review, speculation has risen on what constitutes the strategic review.

Some of the speculations include the ECB’s approach towards a symmetrical inflation target, as noted by Francois Villeroy, a member of the ECB governing council and President of the Bank of France.

But opposition remains in the form of German Bundesbank Chief Weidmann who said that there was no need to tinker with the inflation target.

The strategic review might not see any big impact on the forex markets today. At best, if we do see any big changes, they can only be felt over the course of time. EURUSD and EURGBP will be the main currency pairs that will exhibit some form of volatility heading into today’s meeting.

The US dollar has been fairly stagnant over the last 24 hours. The lack of any key US data this week has created an absence of directional drivers which has seen the USD index remain in consolidation mode just below the recent 97.42 resistance level.

Some weakness in equities over the week as a result of concerns over the outbreak of the coronavirus has helped keep USD underpinned at recent levels.

Euro Lower Ahead of ECB

EURUSD has been a little weaker today. The residual strength in USD over the week has weighed on EUR. The ECB meets today and while no change in policy is expected, traders will be keen to hear the details of the bank’s strategy review. Special attention will be paid to the details around the inflation target. EURUSD trades 1.1089 last.

GBP Pauses At Highs

GBPUSD has been a little softer today, pausing just below the recent 1.3152 highs. GBP has been much stronger over the week though upside has stalled over the last 24 hours.

Tomorrow the market will receive the latest manufacturing and services PMIs for the UK which have the potential to create volatility late in the week.

Risk Appetite Softening

Risk assets have been a little softer in recent trading. The outbreak of the Wuhan virus in China is prompting fears of a wide outbreak, as with the SARS virus, which is weighing on risk appetite.

With the Chinese lunar new year travel period coming up there are fears that the contagion will worsen. One case has already been reported in the US. SPX500 trades 3320.83 last.

JPY Sees Strong Rally, Gold Weaker

Safe havens have had a mixed start to early European trading with gold down against USD while JPY has been higher. Residual strength in USD has kept upside capped in gold this week while broader uncertainty around the Wuhan virus is fuelling strong safe-haven demand for JPY.

XAUUSD is currently challenging the 1554.69 level from above. USDJPY trades 109.57 last, having broken back below the 109.71 level.

Crude Crumbles on Bearish API

Oil prices have been lower today, extending decline across the week, as the spread of the Wuhan virus is causing concerns for the global oil demand outlook.

The API yesterday reported a 1.5 million barrel surplus in US crude inventories. The EIA will report its figures today, with the release delayed due to MLK day. Crude trades 55.89 last.

Loonie Higher Following Dovish BOC

USDCAD has been higher today following the sell-off in CAD seen in response to yesterday’s BOC meeting. The BOC kept rates on hold though fuelled expectations of a forthcoming rate cut with a more dovish statement and outlook on the economy.

The bank no longer refers to current policy levels as appropriate and traders now judge a rate cut likely in the near future. USDCAD trades 1.3162 last.

Aussie Jumps On Labour Data

AUDUSD has been firmer today with price rallying back above the .6850 level which was briefly pierced yesterday. Overnight, Aussie unemployment rate was seen moving lower to 5.1% from the prior and expected 5.2%. However, the outlook remains bearish with traders still expecting an RBA rate cut in February.

The Bank of Canada held its monetary policy meeting on Wednesday. As widely forecast, the BoC left the key interest rate steady at 1.75%.

Ahead of the BoC meeting, Canada’s inflation data came out. Consumer prices were seen to be fairly stable for December. The BoC, in its statement, gave a cautious assessment of the economy as it stays alert to persisting slower growth and geopolitical risks.

US Existing Home Sales Rise More than Forecast

Existing home sales report for December beat expectations strongly. Data from the National Association of Realtors showed that existing home sales rose by 5.54 million in December, representing about a 3.6% increase on the month. This came after a drop of nearly 1.7% just the month before.

EURUSD Settles into a Range

The common currency is clearly seen moving into a sideways range between the 1.1100 and 1.1072 region. We expect this sideways movement to continue into today’s ECB meeting.

A breakout from either of these levels will potentially signal a near term momentum and direction. At the moment, the bias is mixed, but there is a possibility that the EURUSD could break to the downside.

UK Public Sector Borrowing Rises in 2019

The monthly report on the government public sector borrowing saw a modest decline in December. But compared over the year, borrowing was higher.

For December, the UK government borrowed about 0.2 billion GBP less compared to the same period in 2018. On a yearly basis, public sector borrowing was 4 billion GBP higher.

GBPUSD Breaks Past 1.3100 Resistance

The currency pair breached the resistance level of 1.3100 on Wednesday right after it broke the falling trend line. A brief retest saw price accelerating to the upside. If the pound sterling can stay above the 1.3100 level, we expect further gains. The next main target is at 1.32260.

Crude Oil Trades Weaker Despite Oil Shortage

Crude oil prices were down over 2% during the intraday on Wednesday. The declines came despite disruptions to oil supply lines in Libya. Earlier in the week, the EIA forecast that prices of Brent crude oil could be slightly lower by the middle of the year. Investors await today’s weekly inventory report.

WTI Crude Oil Could Slip to $56 a Barrel

The current declines in crude oil prices could push the price lower down to the $56.00 level. The bearish momentum could push oil prices lower over the near term. The Stochastics oscillator remains oversold, but the price action from the daily chart dictates that further downside is likely.

In the H4 chart, USDCHF has rebounded from 3/8. In this case, the price is expected to resume falling to reach the support at 0/8. However, this scenario may no longer be valid if the price breaks 3/8 to the upside. After that, the instrument may continue growing towards the resistance at 5/8.

As we can see in the M15 chart, the pair has broken the downside line of the VoltyChannel indicator and, as a result, may continue trading downwards to reach 0/8 from the H4 chart.

XAUUSD, “Gold vs US Dollar”

As we can see in the H4 chart, XAUUSD is still moving below 3/8. In this case, the price is expected to continue trading downwards to reach the support at 0/8. However, this scenario may no longer be valid if the price breaks 2/8 to the upside. After that, the instrument may continue growing towards the resistance at 3/8.

In the M15 chart, the pair may break the downside line of the VoltyChannel indicator and, as a result, continue the descending tendency.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.