By CentralBankNews.info Kyrgyzstan’s central bank raised its key rate, the discount rate, by 75 basis points to 5.0 percent, saying higher food prices are continuing to exert upward pressure on inflation in the medium term. It is the first change in rates by National Bank of the Kyrgyz Republic (NBKR) since May 2019 when paused in its easing cycle after 7 rate cuts starting in March 2016. Between March 2016 and May 2019 NBKR cut its by a total of 575 basis points but since then inflation has accelerated. In January consumer price in the Kyrgyz Republic rose for the 10th consecutive month to 3.2 percent and the central bank expects inflation to approach the lower boundary of its target of 5.0 to 7.0 percent in the second quarter. By December this year, the central bank expects inflation to be about 5.0 percent and to average 4.6 percent in 2020.

By Dan Steinbock – In addition to the Chinese mainland, the struggle against the new cases and outbreak clusters of the COVID-19 is shifting to countries outside China – not just Asia, but Europe, North America, the Middle East and Africa.

In China, the number of confirmed coronavirus cases is about to exceed 80,000, but the momentum of new outbreaks is now shifting to countries outside China, where the number of confirmed cases soared to almost 1,800 with 17 deaths.

This is only a prelude to what’s yet to come, however.

New virus risks outside China

While these numbers will continue to climb, the low starting-point suggests China’s draconian measures may have saved many lives within and outside China. The same cannot be said about preemption measures outside China’s borders.

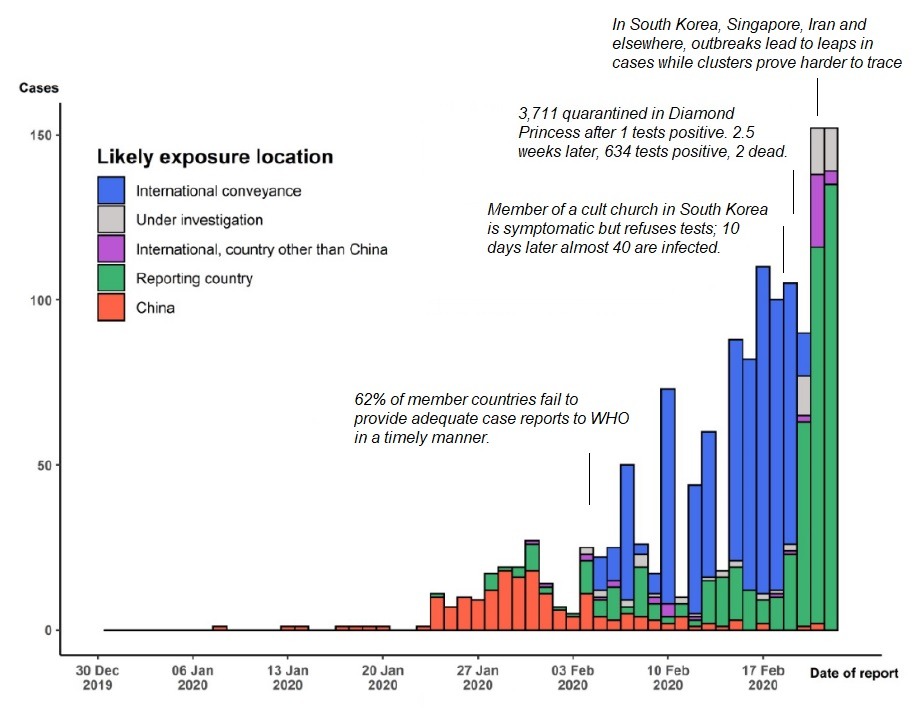

Risk of international complacency (WHO member states). On February 4, the WHO’s chief Dr. Tedros said that, after almost a month of international crisis and global alert, three of five WHO member countries outside China had failed to provide adequate information in a timely manner. As the timeline suggests, the number of cases outside China soared after February 4 and the missed opportunities of greater international cooperation (Figure).

FigureCOVID-19 international risks have soared since early February

Source: WHO; DifferenceGroup.

Risk of botched quarantines (Diamond Princess Cruise). On February 3, more than 3,700 passengers and crew were quarantined by the Japanese Ministry of Health after one passenger on the ship tested positive for COVID-19. Just two and half weeks later, some 635 passengers tested positive for the virus, while two passengers had died after contracting the virus.

Risk of “super-spreaders” (South Korean cult church). From the start, potential super-spreaders who could endanger others have been a great concern. On February 10, a 61-year old woman, who worships at the Daegu cult church, developed fever but twice refused to be tested for the virus claiming she had not recently travelled abroad. After she had attended at least four services before the diagnosis, 40 other members of the church were infected.

Risks of potential evacuation failures (State Department vs CDC). As countries seek to rescue citizens from infected territories, failed evacuations can pose new risks. Last week, the US Centers for Disease Control urged to keep 14 infected US citizens in Japan, yet the State Department put the infected on a plane with healthy people claiming that a plastic-aligned enclosure would mitigate infection risks.

Risks of poorly-monitored self-quarantines (several countries). On February 21, California health officials said that 7,600 people who had returned to the state after visiting China during the virus outbreak had been asked to quarantine themselves at home this month. Laxness in self-quarantine could endanger far more lives. However, the CDC is not tracking how many people from each US state who have returned from China have been asked to isolate themselves. Further, local health departments have discretion in how to carry out the quarantines.

Unknown risks

In addition to the threats that we know, there are potential, more challenging risks which we understood poorly or don’t even know about.

Risks of untraceable virus clusters (several countries). In South Korea, Singapore and Iran, virus clusters have led to rapid leaps in cases. As it is becoming harder to trace where the clusters started, the virus may be spreading too broadly for traditional public-health steps to contain it. That highlights the importance of Chinese standard-setting measures that several countries are now emulating in part or fully.

Risk of real incubation period (faster, longer than presumed). Initially, clinical evidence suggested that the incubation period was 2-14 days, which then became the standard for quarantine measures. In the past weeks, Chinese authorities have extended these periods because new evidence suggests that, with possible outliers, the incubation period could be 0-27 days.

Risks of weaker healthcare systems (poorer developing countries). In late January, the WHO declared the ongoing virus outbreak a “public health emergency of international concern” (PHEIC). The goal was to boost international coordination against the expected internationalization of the outbreaks. As WHO officials have repeatedly noted, the PHEIC was motivated by the possible effects of the virus, if it would spread to countries with weaker healthcare systems.

In addition to proximate Asia, virus clusters have emerged in emerging Asia, big European economies, North America, Middle East, and Russia. Even though Italy has been the only European country to have barred flights to and from China, Hong Kong, Macau and Taiwan, it has seen a dramatic increase of cases, centered in the regional towns of Lombardi, near Milan – the country’s business hub.

The world’s most vulnerable

The big question is how forcefully the virus will arrive in the rest of Americas and particularly Africa.

Risks of local transmission. On Feb 21, when the virus had spread to 25 countries, local cycles of transmission had already occurred in 12 countries after case importation. In Africa, Egypt has so far confirmed one case. As such cases are expected to proliferate, the probability of such risks will climb accordingly.

In modeling simulations based on air travel, new research indicates that the highest importation risk involves a set of countries – including Egypt, Algeria, and South Africa – that have moderate to high capacity to respond to outbreaks. In turn, countries at moderate risk – including Nigeria, Ethiopia, Sudan, Angola, Tanzania, Ghana, and Kenya – have variable capacity and high vulnerability.

Several African countries are already struggling to contain another Ebola virus outbreak, while others are fighting the worst locust in decades. Having already decimated crops throughout Ethiopia, Kenya and Somalia, Eritrea and Djibouti, locust swarms threaten South Sudan, Uganda and Tanzania, while breeding along the both sides of the Red Sea in Egypt, Sudan, Eritrea and Saudi Arabia.

Old risks could resurface along with the new

As new risks are evolving, old risks are not yet fully contained and can still pose lingering threats in China and particularly in countries outside China.

Risk of “closed spaces” (prison systems, nursing homes). On February 21, Chinese prisons reported some 500 new cases of infections among inmates and guards. It was followed by news of infections in nursing homes. Both cases highlight the high transmissibility of the virus in spaces of confinement.

Risks of new potential mutations and infection scenarios. The plausible current assumption is that, like seasonal influenza, the COVID-19 is causing mild and self-limiting disease in most people who are infected, with severe disease more likely among older people or those with comorbidities (e.g., diabetes, pulmonary disease).

But if the scenario changes towards wider community transmission with multiple international foci (or toward new kind of mutations), current mitigation procedures will prove inadequate and countries will be more likely to emulate Chinese measures.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

Based on Dr. Steinbock’s briefing of Feb 23, 2020, on COVID-19 human and economic impact.

By TheTechnicalTraders – Over the past 5+ days, a very clear change in market direction has taken place in the US and global markets. Prior to this, the US markets were reacting to Q4 earnings data and minimizing the potential global pandemic of the Coronavirus. The continued “rally to the peak” process was taking place and was very impressive from a purely euphoric trader standpoint. Our researchers found it amazing that the markets continued to rally many weeks after the news of economic contraction and quarantines setup in China/Asia.

Make sure to opt-in to our free market trend signals newsletter before you continue reading this or you may miss our next special report!

We believe a number of critical factors may have pushed global investors away from their comfortable, happy, bullish attitude over the past 5+ days – most importantly the reality that the virus pandemic was very real and would continue to result in a more severe global economic contraction process and the outcome of the Caucus voting where Bernie Sanders appears to be leading almost every early voting event. There are now two major concerns hanging over the global markets and the future of the US 2020 Presidential elections. These two major issues may be enough to change investor sentiment and present a very real volatility event.

Uncertainty breeds fear and can cause traders to move away from risk. We discussed these topics in research posts many months ago.

Our researchers believe the underlying concerns that are becoming more evident to global traders are the very real facts that the global economy may continue to contract because of the spreading Corona Virus and risks of a global pandemic event and the fact that the US 2020 Presidential election process appears to be setting up to become a real battle between Donald Trump and Bernie Sanders. Our researchers believe the combination of these two unknowns is creating an environment where global traders are fearful of the future growth opportunities within the US and global markets.

Bernie Sanders has been dominating the Caucus events in the US as a Socialist/Progressive candidate. For many Americans, this is a frightening concept. Even early into the Caucus voting cycle, it appears Mr. Sanders has taken a very clear leadership role headed into the 2020 Presidential election event. Business and global investors are not going to like the concept of a Socialist/Progressive US Presidential candidate. This is going to cause investors and business owners to avoid engaging in projects and opportunities until after the November 2020 elections.

Add into this fear contagion the fact that the Coronavirus event may continue to add to the global fear component of the US and global economy. How much more risk is involved because of the spread of this virus over the next 12+ months and how will this concern complicate the concerns related to the US Presidential electing event?

Daily Dow Jones Industrial Chart

This Daily Dow Jones Industrial chart highlights the huge Gap lower that took place early on Monday, February 24, 2020. This huge move resulted from an extended fear of a growing potential for a global pandemic event and a renewed fear that global economic activity may be greatly reduced over the next 12+ months. We believe the extended fear of a potential Socialist/Progressive Democrat candidate may be adding to this massive decline in the global markets.

Transportation Index Daily Chart

The Transportation Index is an excellent measure of future economic activity expectations and investors belief that the global economy will recover from this potential contagion event. On Monday, February 24, 2020, the Transportation Index collapsed below 10,600 on a Gap Down move as the markets collapsed. This is a real sign that global investors suddenly believe the global markets will contract over the next 3 to 6+ months and are moving away from risky instruments in the US and global markets.

Weekly Transportation Index

This Weekly Transportation index chart illustrates just how far the TRAN could move while still saying within the range of price activity from 2018 to 2019. The TRAN could fall all the way to levels near 8,800 before reaching the lows of December 2018. Thus, from current levels near 10,500, we could see a continued price decline in the global markets of at least 15% to 20% before we near the 2018 lows.

As our research team has been predicting, it appears a Waterfall event is beginning to take place. This Gapping downside move may become the catalyst top in the global markets that presents a broader market rotation/decline. As we’ve been warning, be prepared for broad sector market rotation and for precious metals to skyrocket as greater fear sets up in the global markets. We hope you were paying attention to our research over the past 5+ months. We’ve been all over this setup and have issued multiple warnings for all our friends and followers.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for both short-term swing trading and long-term investment capital. The opportunities are massive/life-changing if handled properly.

I urge you visit my ETF Wealth Building Newsletter and if you like what I offer, join me with the 1-year subscription to lock in the lowest rate possible and ride my coattails as I navigate these financial market and build wealth while others lose nearly everything they own during the next financial crisis. Join Now and Get a Free 1oz Silver Bar!

Shares of Baudax Bio traded more than 20% higher and set a new 52-week high price after reporting that the FDA approved the company’s non-opioid ANJESO drug for management of moderate to severe pain.

Specialty pharmaceutical company Baudax Bio Inc. (BXRX:NASDAQ), which is engaged in the development of therapeutics for acute care settings, yesterday announced that “the U.S. Food and Drug Administration (FDA) has approved the New Drug Application (NDA) for ANJESO (meloxicam injection), which is indicated for the management of moderate to severe pain, alone or in combination with other non-NSAID analgesics.”

Gerri Henwood, President and CEO of Baudax Bio commented, “The approval of ANJESO marks a major advancement in the treatment landscape for managing moderate to severe pain…With our nation currently in the midst of a national opioid epidemic, we are thrilled to be able to offer a novel, non-opioid therapeutic option with the potential to meaningfully impact the acute pain treatment paradigm. We expect to make ANJESO available to physicians and patients in late April or early May 2020.”

The company’s Chief Medical Officer Stewart McCallum, M.D. remarked, “The safety and efficacy of ANJESO have been well-established through several mid- and late-stage clinical studies…Moreover, data from our Phase III safety trial demonstrated that ANJESO is well tolerated and impacted opioid consumption compared to placebo, further highlighting its value to patients, providers and health systems.”

Dr. Keith Candiotti chair of the Department of Anesthesiology, Perioperative Medicine and Pain Management at the University of Miami added, “The approval of ANJESO marks an important achievement for the medical community given the unmet need for non-opioid options in the pain treatment landscape…ANJESO has the potential to serve as a meaningfully differentiated analgesic alternative.”

The company advised that ANJESO is indicated for use in adults for the management of moderate-to-severe pain, alone or in combination with non-NSAID analgesics. The firm explained that “ANJESO (meloxicam) injection is a proprietary, long-acting, preferential COX-2 inhibitor that possesses analgesic, anti-inflammatory and antipyretic activities, which are believed to be related to the inhibition of cyclooxygenase type 2 pathway (COX-2) and subsequent reduction in prostaglandin biosynthesis.”

Baudax expects that ANJESO will be available in the U.S. in late April or early May 2020. The firm noted that ANJESO has already been studied in several comprehensive Phase 3 clinical trials studying the safety and efficacy of use following Bunionectomy and Abdominoplasty surgeries and as well as other major surgical procedures including total hip and knee replacements, spinal, GI, hernia repair, and gynecologic surgeries.

Baudax Bio is based in Malvern, PA and is a specialty pharmaceutical company that focuses on developing therapeutics for acute care settings. The firms indicates that its lead drug ANJESO (IV meloxicam) is a non-opioid which has the potential to overcome many of the issues associated with commonly prescribed opioid therapeutics without having addictive qualities while maintaining meaningful analgesic effects for relief of pain.

Baudax Bio has a market capitalization of around $75.5 million with approximately 9.436 million shares outstanding and a short interest of about 9.0%. BXRX shares opened greater than 23% higher today at $9.85 (+$1.851, +23.14%) over yesterday’s $7.999 closing price and reached a new intraday 52-week high price this morning of $10.14. The stock has traded today between $8.66 and $10.14 per share and is currently trading at $8.965 (+$0.966, +12.08%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Premier Health Group announced that it changed its name to CloudMD Software & Services Inc., and trading under the symbol DOC will begin Feb. 24.

In a news release, Vancouver, B.C.-based Premier Health Group Inc. (PHGI:CSE; PHGRF:OTCQB; 6PH:FSE), which is engaged in “delivering quality healthcare through the combination of connected primary care clinics, telemedicine and artificial intelligence (AI),” advised that “pursuant to a directors’ resolution, it has changed its name to CloudMD Software & Services Inc.”

The company’s stock trading symbol will be changed to DOC and it is expected that the common shares will commence trading under the new name CloudMD Software & Services Inc. on or about Monday, February 24, 2020.

“We are excited to be announcing our name change to reflect the Company’s strategic focus on increasing our digital health and telemedicine based revenue,” said Essam Hamza, M.D., CEO of Premier Health.

“With the recent launch of our direct to consumer telemedicine app, CloudMD, we are focused on getting the over 5 million patients in BC access to the care they need, when they need it. Leveraging the latest developments in technologies like 5G, the days of waiting weeks for a doctor’s appointment or rushing to an emergency room during a viral outbreak like the coronavirus are quickly disappearing,” added Dr. Hamza.

The company stated that it currently has a combined ecosystem of 315 clinics with over 3,000 licensed practitioners and almost 3 million registered patients and is endeavoring to digitize the delivery of healthcare by providing patients access to all points of their care from their phone, tablet or desktop computer.

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Premier Health Group Inc. Please click here for more information. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Premier Health Group Inc., a company mentioned in this article. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Keeping up appearances is about to get a lot harder for the central planners trying to manage perceptions of the U.S. (and global) economy. The coronavirus is going to have a meaningful impact on global supply chains, even if stock market cheerleaders haven’t fully realized it yet.

This might be because the corporate media and ruling elites are burning a lot of what is left of their fading credibility trying to ignore or downplay the problem.

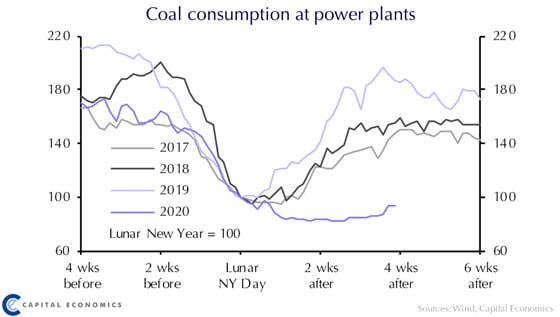

Some things can’t be ignored, however. Capital Economics published some telling charts last week showing conditions on the ground in China. Below are two which detail the Chinese economy all but grinding to a halt.

Bloomberg reported a 92% drop in Chinese car sales during the first half of February.

And Maersk, the world’s largest container shipping company, warned that the coronavirus will have a big impact on earnings. The company reported Chinese factories are operating at 50-60% of capacity.

That is very bad news to pile on top of the company’s already dismal performance. Maersk reported a loss in the 4th quarter, before the impact of the virus.

CNBC pundits can talk all they want, but what is happening in China will soon be felt around the world. Americans will find out what is real when many of the shelves in the local Walmart start looking a little bare.

If the virus is not contained quickly and factories remain closed, the supply chain could completely break down for merchants selling Chinese goods.

Managing perceptions may get harder, but that doesn’t mean the Federal Reserve won’t try. Christopher Irons of Quoth the Raven Research summed it up nicely on Twitter:

“The year is 2023…

The coronavirus has wiped out humankind…

A lone server in the basement of the NY Fed building continues to bid the Dow Jones to new all-time highs.”

Shares of Walmart are up about 1.5% since the World Health Organization declared the coronavirus to be a “public health emergency of international concern” on January 30th. The broader S&P 500 index enjoyed a similar bump following the news, until today that is.

Could it be that investors think central banks will look at the coronavirus news as an excuse to ramp up stimulus?

They may be right, but no amount of printed money is can put merchandise on store shelves.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Such dynamics means a rise in price of silver and weakening of the Mexican peso. On February 13, the Bank of Mexico lowered the rate to 7% from 7.25%. Against this background, last week the peso showed its maximum decline in 9 months. Market participants do not rule out further rate cuts amid relatively low Mexican inflation of 3.18% in the second half of January, in annual terms. Mexico will release many important macroeconomic data next week: inflation for the 1st half of February (Monday), final GDP and current account balance for the 4th quarter (Tuesday), retail sales for December (Wednesday), unemployment for January ( Thursday) and the trade balance for January (Friday). These figures indicators can affect the dynamics of the Mexican peso. On the other hand, silver rises in price along with other precious metals amid the risks of the coronavirus epidemic expansion. Note that the volume of silver trading on the COMEX exchange in January 2020 increased by 32% compared with January 2019 and amounted to 313 thousand tons.

Israel’s central bank left its key interest rate steady at 0.25 percent and confirmed its recent guidance that it expects to maintain this rate for a prolonged period or to reduce it to ensure inflation stabilizes around the midpoint of its target range and the economy continues to grow strongly.

The Bank of Israel (BOI), which has kept its rate steady since raising it in November 2018 for the first time since 2012, also reiterated it was taking additional steps to make monetary policy more accommodative, a reference to its intervention in foreign exchange markets to curb the strong shekel.

While the outbreak of the coronavirus in China is “casting uncertainty regarding future economic activity globally and in Israel,” BOI said its baseline scenario is that the spread of the virus will be halted in coming months and the overall impact on the global economy will be limited.

“The Bank of Israel’s assessment in this scenario is that no significant macroeconomic impact is expected in Israel,” it said.

However, if the crises were to spill over into additional countries and preventative measures are required in Israel, it is expected to have a more significant economic impact.

“In such as scenario, the Monetary Committee has a range of tools to make monetary policy more accommodative,” BOI said.

Israel’s inflation rate has been below the lower bound of BOI’s 1.0 – 3.0 percent target range since June last year and fell to 0.3 percent in January from 0.6 percent in December.

“The moderation of inflation is largely influenced by the appreciation of the shekel,” BOI said, adding it is possible the inflation rate may be negative in coming months before moving back toward the lower bound of the target range in the second half of the year.

The shekel has been rising since early 2019 and BOI has a history of intervening to curb it.

In November and December last year BOI purchased $3.6 billion in one of its biggest bouts of intervention in nearly a decade, and at the end of January BOI’s foreign exchange reserves rose $3.9 billion from end-December to $129.97, mainly due to foreign exchange purchases totaling $2.95 billion.

In its January press conference, BOI Governor Amir Yaron affirmed the banks’ readiness to prevent “excessive appreciation of the shekel, by purchasing foreign exchange whenever necessary” as it sees the rise due to short-term financial factors.

But BOI’s foreign exchange intervention has not dented the shekel much and today it was trading around 3.43 to the U.S. dollar today, up 0.9 percent this year and close to historic lows seen during the global financial disruptions in January 2018, July 2014 and June 2011.

Since the start of 2019 the shekel has risen almost 10 percent against the U.S. dollar.

Against the euro, the shekel has been hitting record highs since mid-2019 and was trading around 3.72 to the euro today, up 4.3 percent this year and up 16 percent since the start of 2019.

Israel’s economy has been growing around its long-term rate in recent months and gross domestic product grew 3.8 percent in the fourth quarter of last year, up from 3.5 percent in the third quarter.

BOI said data from January point to continued growth but the interim budget is expected to have a “markedly contractionary effect” in the first half of 2020.

The Bank of Israel released the following press release:

“The inflation environment continues to be low. The January CPI was lower than expected, and inflation over the past 12 months remains 0.3 percent. Inflation excluding energy and fruits and vegetables also remains low. The moderation of inflation is largely influenced by the appreciation of the shekel. It is possible that in the coming months, the year over year inflation rate will be negative, but it is expected to move back toward the lower bound of the target range in the second half of the year.

Since the previous interest rate decision, the shekel has strengthened by approximately 3 percent in terms of the nominal effective exchange rate, a development that continues to weigh on the return of inflation to the target range.

The economy continues to grow at around its long-term growth rate. According to the Research Department’s assessment, the growth rate in the fourth quarter, net of the volatility in vehicle imports, was about 3.5 percent, and the growth encompassed virtually all sectors. Indicators of economic activity in January point to continued growth, and the labor market remains tight. The interim budget is expected to have a markedly contractionary effect in the first half of 2020, and there is continuing uncertainty regarding budgetary policy after the elections.

The most recent data published regarding global economic activity indicate low growth in Europe and negative growth in Japan, while the US continues to exhibit positive growth. Global growth forecasts for 2020 were revised slightly downward, and the slowdown in world trade continues.

The outbreak of the coronavirus in China is casting uncertainty regarding future economic activity globally and in Israel, and regarding the impact on inflation and on the financial markets. The baseline scenario guiding the assessments of most international financial institutions is that the spread of the virus will be halted in the coming months, and the overall impact on the global economy is expected to be limited. The Bank of Israel’s assessment in this scenario is that no significant macroeconomic impact is expected in Israel. If the crisis persists and spills over into additional countries, and particularly if strict preventative measures are required in Israel, it is expected to have a more significant impact. In such a scenario, the Monetary Committee has a range of tools to make monetary policy more accommodative.

The Monetary Committee’s assessment is that in view of the inflation environment in Israel, the monetary policies of major central banks, developments in the global economy and the risks to the domestic economy, and the development of the exchange rate, it will be necessary to leave the interest rate at its current level for a prolonged period or to reduce it in order to support a process at the end of which inflation will stabilize around the midpoint of the target range, and so that the economy will continue to grow strongly. Furthermore, the Committee is taking additional steps to make monetary policy more accommodative. The Bank of Israel continues to monitor developments in inflation, the real economy, fiscal policy, the financial markets, and the global economy, and will act to attain the monetary policy targets in accordance with such developments.

For the file of figures accompanying this notice, clickhere.

The inflation environment continues to be low. The CPI reading for January declined by 0.4 percent, a greater decline than expected, and year over year inflation remained below the target range. In the past 12 months, the inflation rate was 0.3 percent (Figure 1 in the attached file of figures), and inflation excluding energy and fruit and vegetables stabilized at a low level, which indicates a low basic inflation rate (Figure 2). The moderation of inflation does not reflect weakness in demand, and is largely influenced by the appreciation of the shekel. Inflation of nontradable goods prices remained moderate, and inflation in the prices of tradable goods remained negative. Inflation is expected to remain low in the coming months, and may even become negative, but it is expected to move back toward the lower bound of the target range in the second half of the year. Most one-year forecasts and expectations remain around the lower bound of the target range or slightly below it (Figure 4). Medium-and long-term forward inflation expectations derived from the capital market continue to be largely stable since the previous interest rate decision (Figure 5). An analysis of the risk premium in 5–10-year expectations shows that excluding the premium, inflation is expected to be above 2 percent in this range. Since the previous interest rate decision, the shekel has strengthened by about 3 percent in terms of the nominal effective exchange rate (Figure 6), a development that continues to make it difficult to return inflation to the target range.

The economy continued to grow at a stable pace around the long-term growth rate. According to the first estimate of National Accounts data for the fourth quarter, GDP grew by 4.8 percent (Figure 11), while according to an assessment by the Bank of Israel’s Research Department, the growth rate net of volatility in vehicle imports was about 3.5 percent. The growth encompassed virtually all sectors. Exports (excluding diamonds and startups) grew by 5 percent, driven by services exports, but the prolonged weakness in goods exports continues. Investment grew by 5.9 percent, while investment in residential construction again contracted (Figure 12). The Business Tendency Survey (Figure 13) and the Composite State of the Economy Index (Figure 14) for January point to continued solid growth at the beginning of 2020. The labor market remains tight: The unemployment rate remained low, while the employment and participation rates increased (Figure 17). Wage increases continue, but their rate of growth slowed somewhat (Figure 19). The interim budget is expected to have a markedly contractionary effect in the first half of 2020, and uncertainty remains regarding budgetary policy following the elections and its implications for economic activity and inflation.

For most of the period since the previous interest rate decision, equity markets in Israel were relatively stable, but in recent days, there have been sharp price declines. Long-term government bond yields declined since the previous interest rate decision, similar to declines in yields in Europe and the US, and the declines have grown stronger in recent days (Figure 7).

Home prices increased in the past year by about 3 percent. The number of home purchases grew, led by first-home purchasers and buyers upgrading their housing situation. Mortgage volume continued to expand, with some increase in leverage levels, and mortgage interest rates continued to decline.

The most recent data published regarding global economic activity indicate low growth in Europe and negative growth in Japan, while the US economy continues to exhibit positive growth. Investment houses’ global growth forecast for 2020 were revised slightly downward, while the revision for growth in China is more significant (Figure 20). The slowdown in world trade continues (Figure 21), but the political risks have moderated in view of the signing of the first stage of the trade agreement between the US and China, and the decline in uncertainty surrounding the progress of the Brexit process. Headline inflation in the major economies increased, but inflation continues to be lower than the central banks’ guiding targets (Figure 23). The US economy grew by 2.1 percent in the fourth quarter of 2019. The Federal Reserve kept the federal funds rate unchanged, and signaled that the rate is expected to remain at its current level unless there is a significant change in the state of the economy. In Europe, growth remains low, with contraction in France and Italy, and near-zero growth in Germany, and the manufacturing sector continues to weigh on activity. The ECB left its interest rate unchanged, and signaled that it expects to leave its policy in place for a considerable time. In Japan, there was significantly negative growth in the fourth quarter following a number of one-off effects, and there are signs that the slowdown will continue. Data on 2019 activity in China were positive, but the long-term trend of moderation continues, and the outbreak of the coronavirus is expected to weigh on growth in Asia at least in the short term. Prices of oil and commodities used in manufacturing declined in view of an expectation of a significant decline in demand from China (Figure 24).

The outbreak of the coronavirus in China is casting uncertainty over a range of areas—future economic activity globally and in Israel, and the impacts on inflation and on the financial markets. The baseline scenario guiding the assessments of most international financial institutions is that the spread of the virus will be halted in the coming months, and the damage to the Chinese economy will be restricted mainly to the first quarter of 2020. In this scenario, the growth rate in later quarters is expected to compensate, so that the overall effect on the global economy will be limited. According to the Bank of Israel’s assessment, beyond the impact on specific companies, this scenario is not expected to have a significant macroeconomic effect in Israel, even though China is a significant trading partner in a range of industries. If the crisis persists and flows over into other countries, and particularly if strict preventive measures will be required in Israel, it is expected to have a more significant impact, the scope of which is difficult to assess at this stage. The decline in global demand for various goods is expected to slow the rate of inflation, but on the supply side, the shortage of goods and raw materials imported from China may serve to increase inflation somewhat. Until recently, the reaction in the financial markets was moderate, but in recent days, the uncertainty has increased and there have been sharp declines in equity markets.

The minutes of the monetary discussions prior to this interest rate decision will be published on March 9, 2020. The next decision regarding the interest rate will be published at 16:00 on Monday, April 6, 2020, followed by a press briefing by the Governor.”

As we can see in the daily chart, XAUUSD is totally dominated by bulls. After finishing the correction, the pair has broken its previous high and right now is trading to reach 76.0% fibo at 1708.10. At the same time, there is a divergence on MACD, which may indicate a possible pullback after the instrument reaches the target. The support is 50.0% at 1482.50.

In the H4 chart, the pair has broken the post-correctional extension area between 138.2% and 161.8% fibo and right now is moving towards 76.0% fibo at 1708.10.

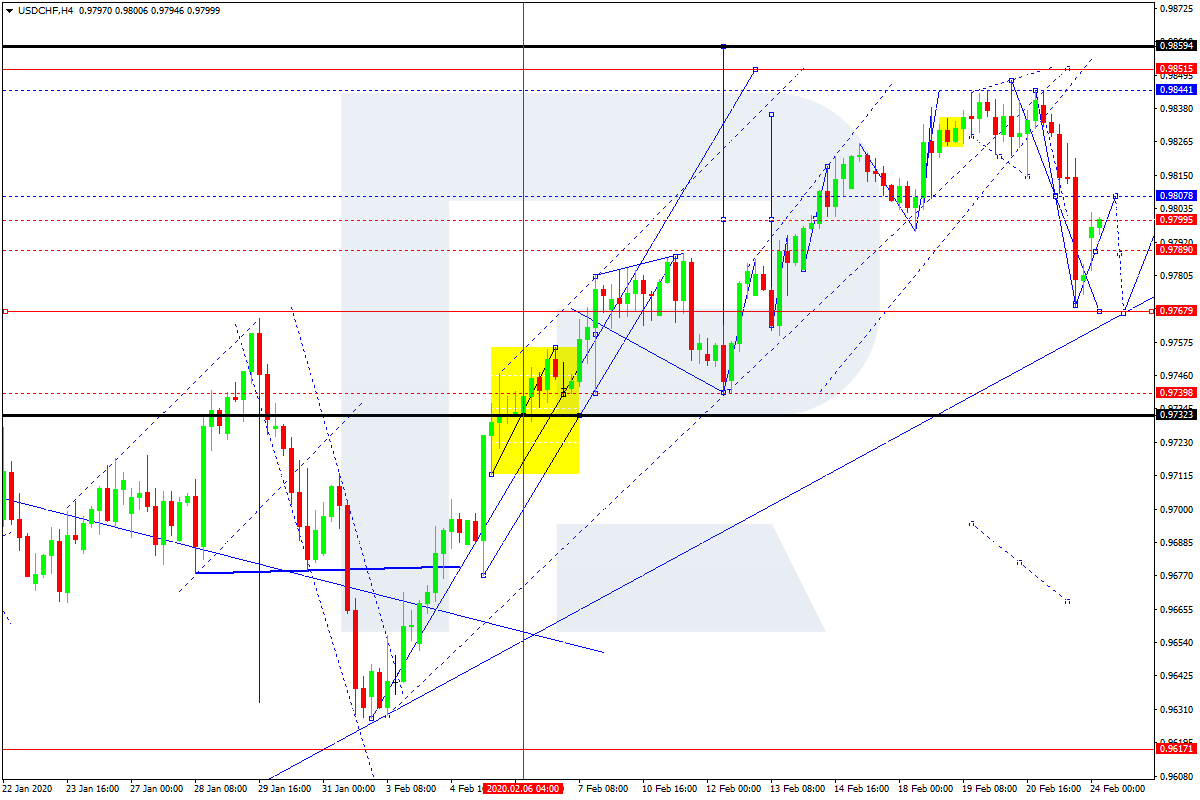

USDCHF, “US Dollar vs Swiss Franc”

As we can see in the H4 chart, the divergence on MACD made the pair reverse after reaching 50.0% and start a new descending movement, which has already tested the support at 38.2% fibo (0.9769). If the price breaks this level and fixes below it, the instrument may continue falling to reach the low at 0.9613.

The H1 chart shows more detailed structure of the current downtrend. The pair has already reached 23.6% fibo and may continue falling towards 38.2% and 50.0% fibo at 0.9764 and 0.9738 respectively. The resistance is local high at 0.9848.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

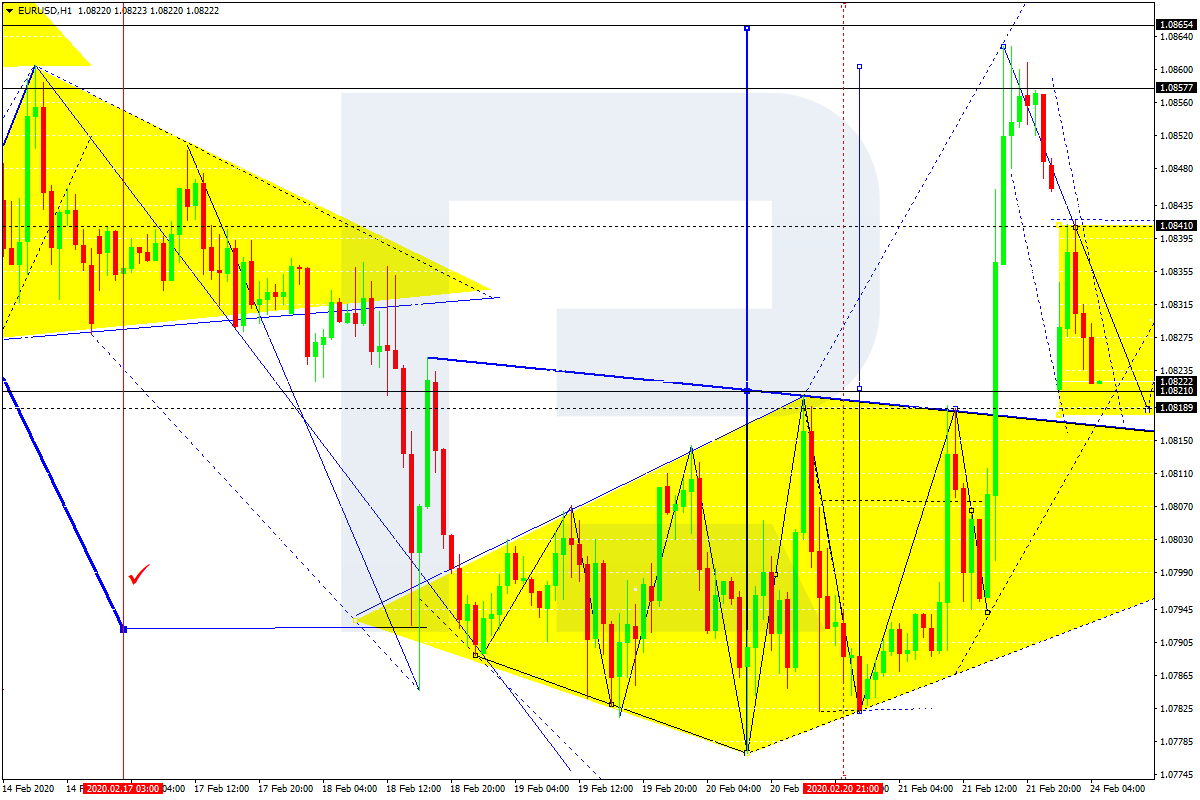

After breaking the consolidation range upwards and reaching the short-term target at 1.0857, EURUSD is moving downwards. Possibly, today the pair may test 1.0818 from above and then form one more ascending structure to reach 1.0865. After that, the instrument may start a new correction to return to 1.0818.

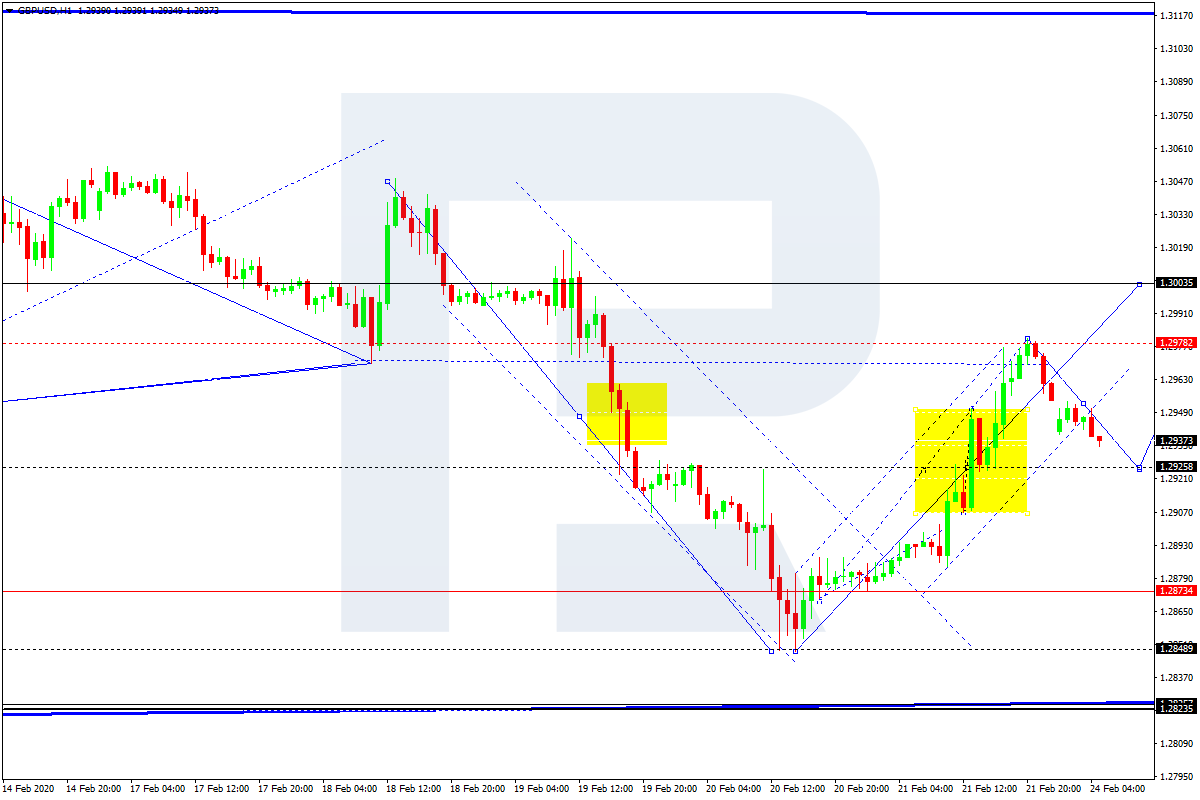

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD has reached the short-term upside target at 1.2978; right now, it is falling towards 1.2925. Later, the market may start a new growth to reach 1.3003.

USDCHF, “US Dollar vs Swiss Franc”

After finishing the descending wave at 0.9777, USDCHF has completed one more ascending structure towards 0.9808. The main scenario implies that the pair may fall to reach 0.9766 and then grow with the target at 0.9851.

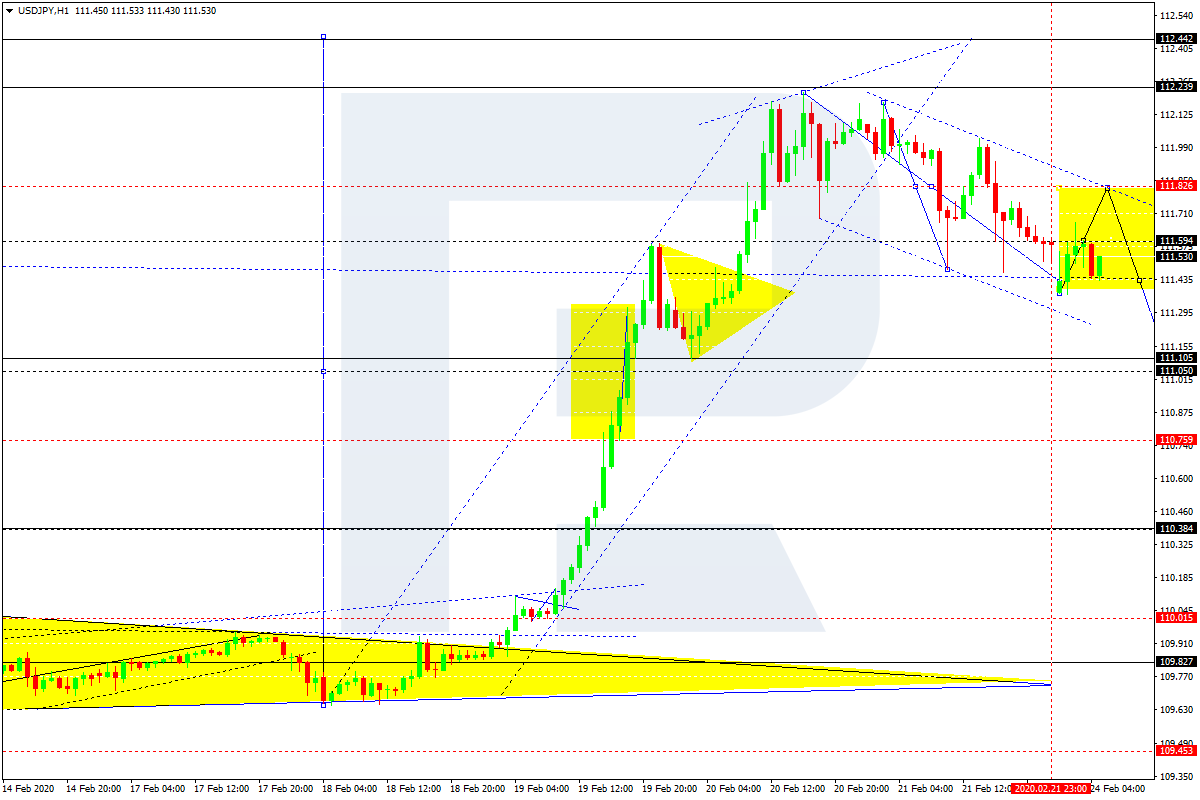

USDJPY, “US Dollar vs Japanese Yen”

USDJPY has completed the descending wave towards 111.40. Today, the pair may correct towards 111.82 and then start another decline with the target at 111.11.

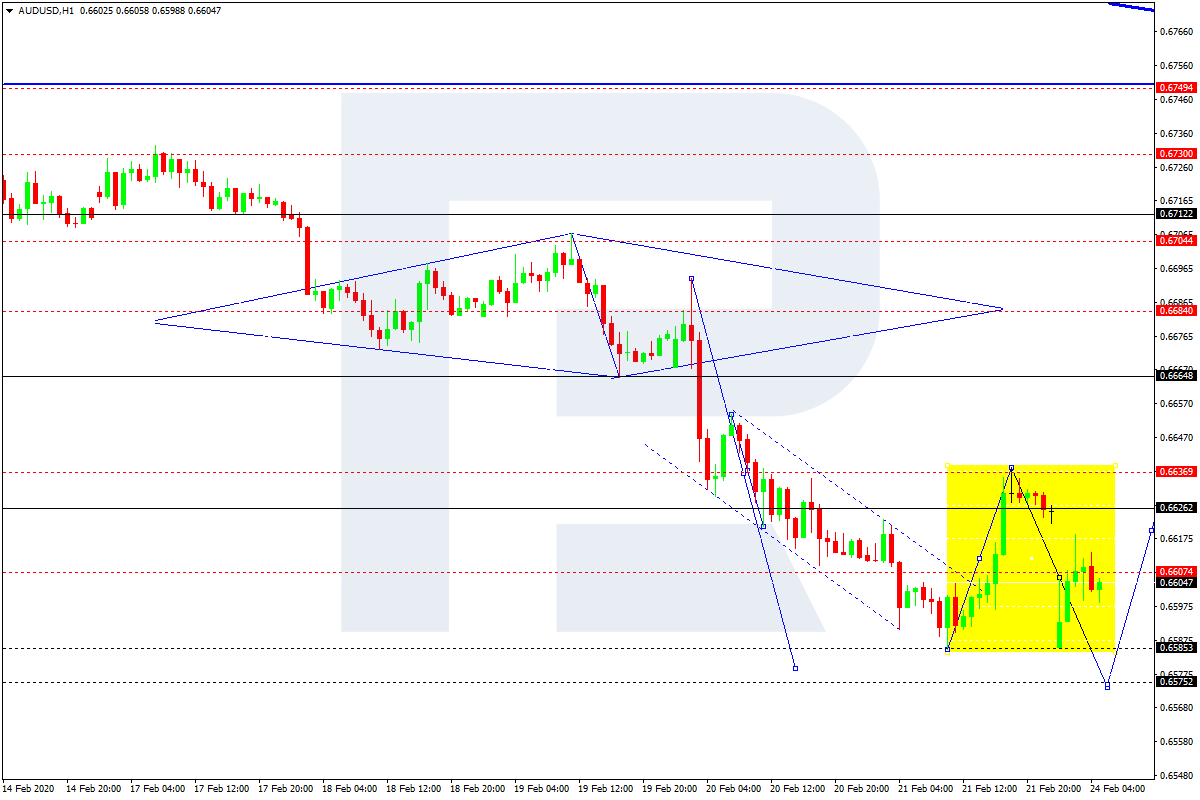

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD has completed the correction at 0.6638; right now, it is falling towards 0.6575. Possibly, today the pair may reach this level and then start another continue the correction with the target at 0.6660.

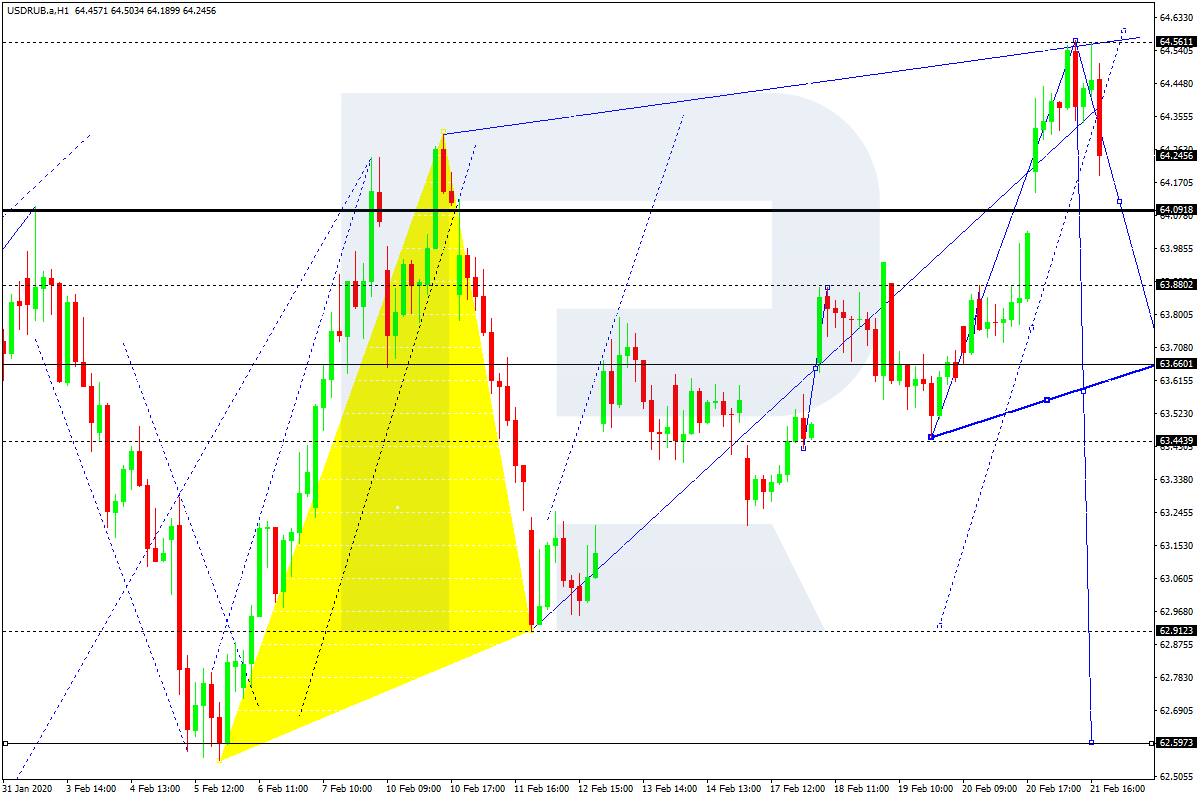

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is moving downwards to reach 64.10. After that, the instrument may grow towards 64.40, thus forming a new consolidation range between these two levels. Later, the market may expand the range up to 64.50 and then resume trading inside the downtrend with the first target at 63.60.

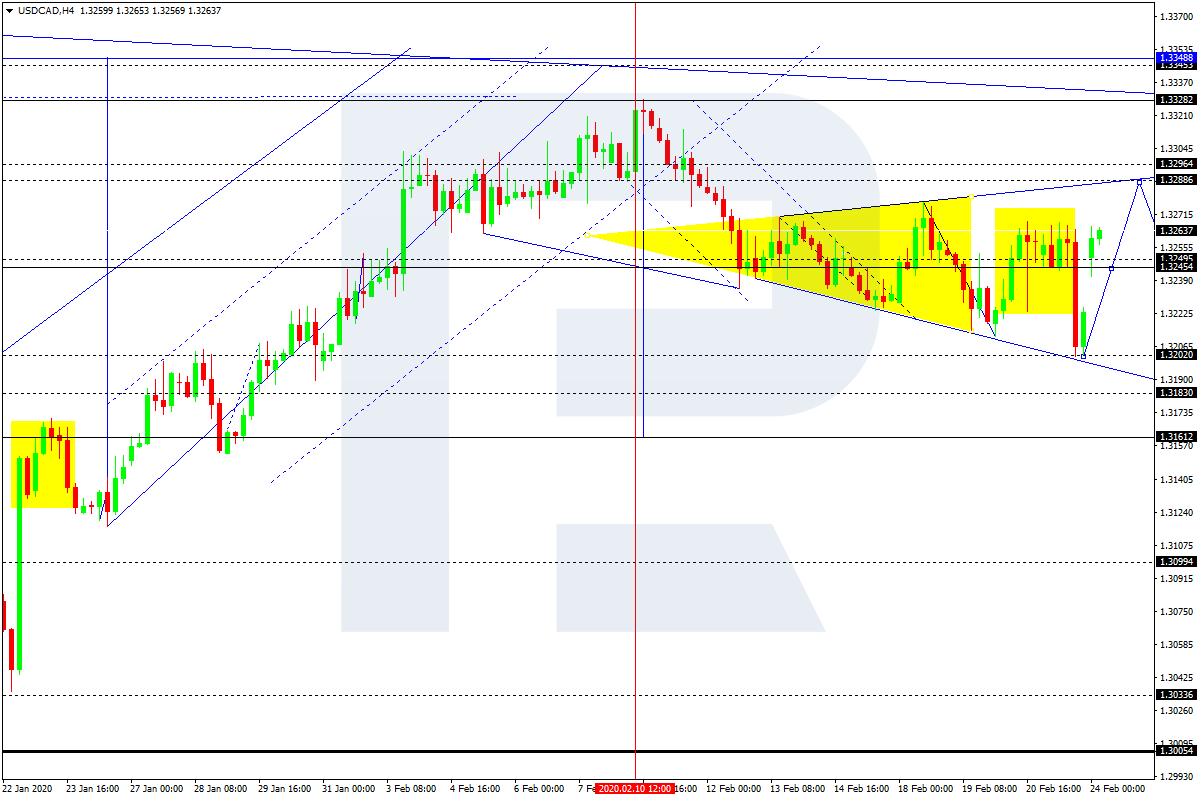

USDCAD, “US Dollar vs Canadian Dollar”

USDCAD is still consolidating around 1.3245. Possibly, today the pair may grow towards 1.3288 and then form a new descending structure to reach 1.3162.

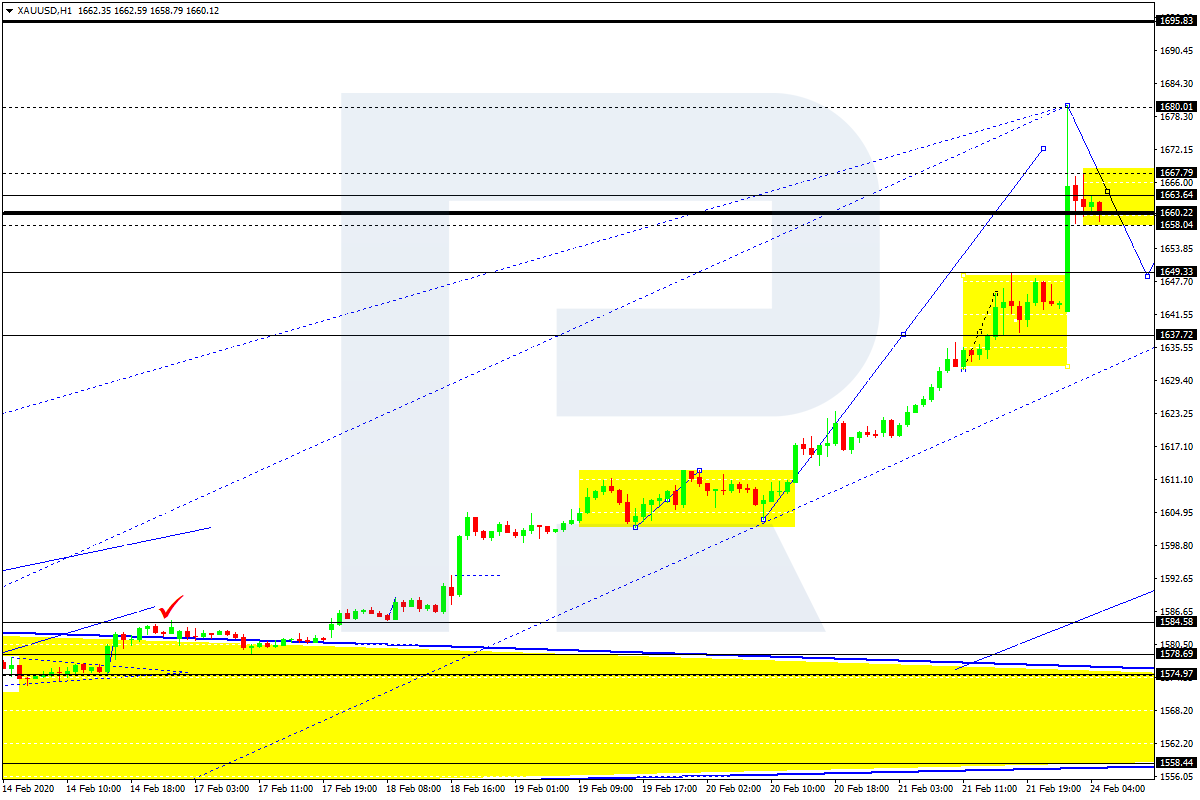

XAUUSD, “Gold vs US Dollar”

Gold has reached 1680.00; right now, it is moving downwards with the target at 1649.33. Later, the market may form one more ascending structure towards 1663.63.

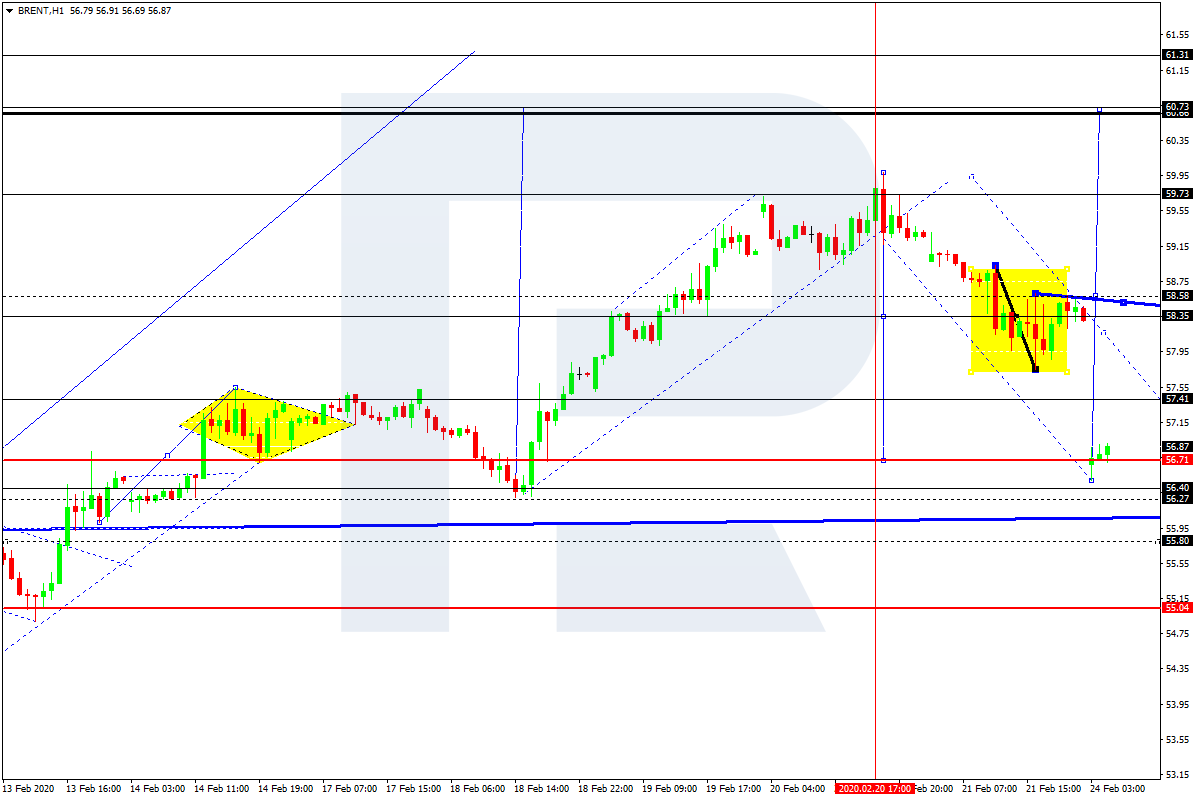

BRENT

After forming the consolidation range around 58.35 and breaking it to the downside, Brent has reached 56.70. Possibly, the pair may form one more ascending structure to return to 58.35 and then resume trading downwards with the target at 57.40.

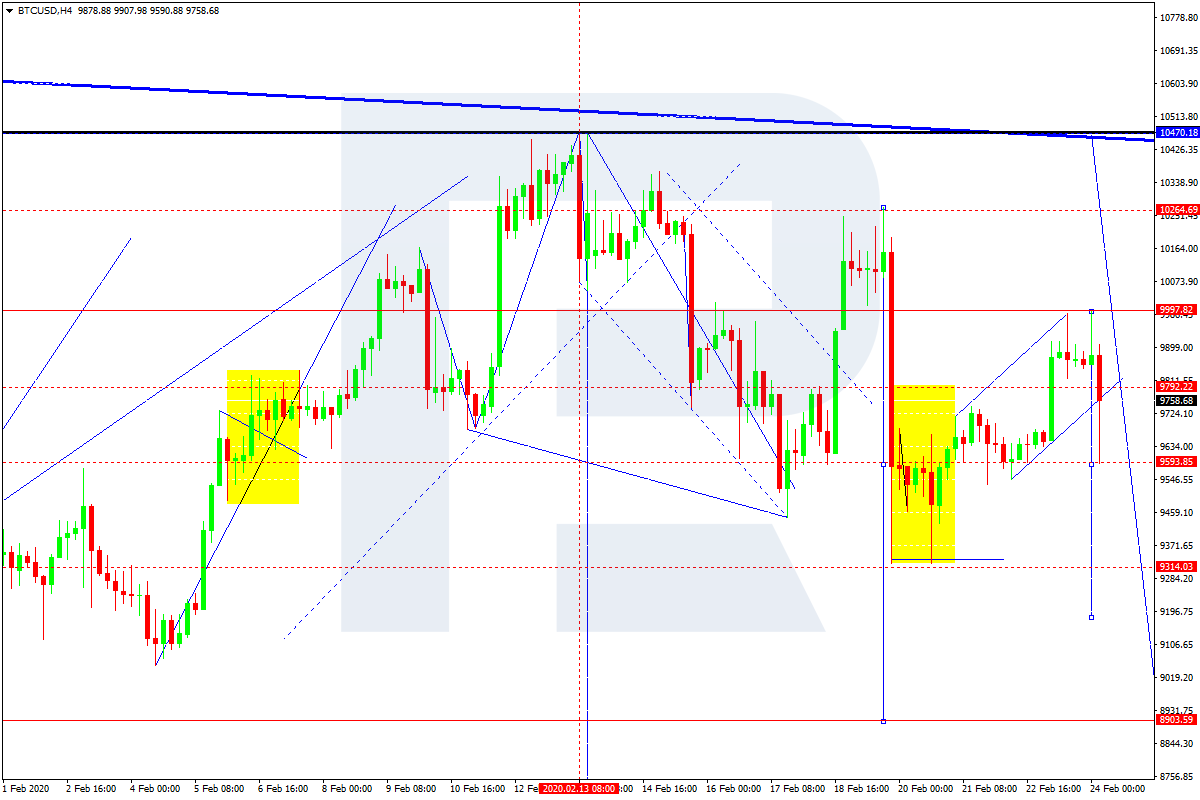

BTCUSD, “Bitcoin vs US Dollar”

After completing the correction towards 9990.00, BTCUSD has finished the descending structure at 9600.00, thus forming a new consolidation range between these two levels. Possibly, today the pair may break the range to the downside and then continue trading downwards with the short-term target at 8900.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.