US stocks may rise thanks to the Fed’s decision to buy short-term corporate debt directly from companies. Thus, it intends to reduce credit risks and stabilize financial markets that are under pressure due to the COVID-19 coronavirus pandemic. For the first time, such a mechanism of the redemption of corporate bonds by the Fed was tested at the peak of the global economic crisis of 2008 and proved to be quite effective. Then the stock indices actively bounced up. In turn, gold is declining amid appreciable demand for dollars. As a rule, quotes of the American currency and precious metals are moving out of phase. In addition, a small liquidity shortage may now be a negative factor for gold. It arose due to the fact that many companies suspended their work against the background of quarantine in a number of countries and are not receiving proceeds.

By Dan Steinbock – Despite China’s success in containment, the novel coronavirus is exploding outside China, due to complacency and inadequate preparedness. The impending contraction will compound human risks and economic damage.

Although the epicenter of the outbreak is now Europe, only a few major economies have launched effective battles against the virus. Hence, the rising levels of imported cases in the borders of China and the rest of Asia.

Since complacency and inadequate preparedness prevailed outside China until recently, the consequent global pandemic casts a dark shadow over the global economy. It, too, shall pass, but only with effective global cooperation.

Extended economic impact outside China

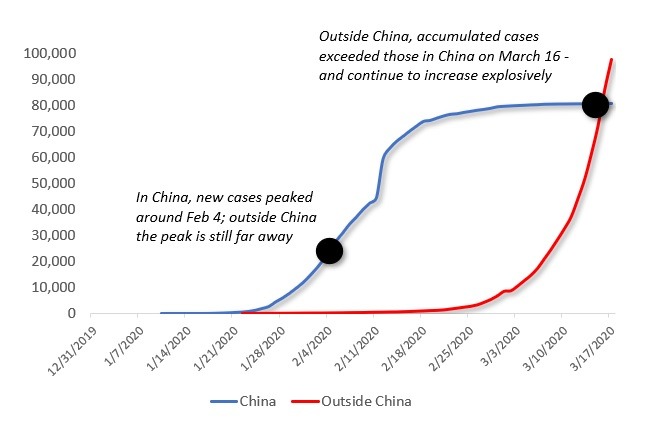

With the novel coronavirus (Covid-19), the number of accumulated confirmed cases worldwide is exceeding 200,000 people. But in the absence of adequate testing, even these official figures are just the tip of the iceberg.

In China, the turnaround came a month after the first novel coronavirus cases were diagnosed, thanks to strong containment measures. But outside China, the first cases were reported after mid-January and they continue to accelerate and now exceed those in China (Figure).

Figure Accumulated confirmed cases in and outside China (until March 16)

Source: WHO, China National Health Commission, Difference Group

In China, the impact of the coronavirus could ease in April. But outside China, epidemiologists currently anticipate a peak around June. If that’s the case, economic damage in China would be largely limited to the first quarter, but international economic damage would endure well into the second quarter.

Assuming the rise in new imported cases in China and elsewhere can be kept down, even this relatively benign scenario would mean adverse repercussions on the world economy.

After mid-January, I projected three probable virus impact scenarios, which can now be reassessed. In the “SARS-like impact” scenario, a sharp quarterly effect, accounting for much of the damage, would be followed by a rebound. The broader impact would be relatively low and regional. That is no longer in the cards, however.

In the “extended impact” scenario, the adverse impact would last two quarters. The broader impact would be more severe and have an effect on global prospects. That’s where the world economy is now heading to.

In the “accelerated impact” scenario, adverse damage would be steeper and even broader with serious consequences on the global economy. If the containment measures continue to fail outside China, this scenario would ensue.

In early March, the International Monetary Fund (IMF) projected global growth to fall 0.1 percentage points from the expected 3.3%. The estimate was too optimistic. Global growth could drop to 2.4 percent in 2020 – or worse, if infection rates continue to rise.

Contraction, stagnation, debt in advanced economies

Before the virus, quarterly growth in the Eurozone was 0.1 percent; the weakest in seven years. Now things will get worse. German GDP will continue to stall, France and Italy will remain in contraction. In the UK, annualized growth is likely to fall from 1 percent by another 0.2 percent and more. In Spain, soaring coronavirus cases will reverse the growth pickup. With debt at 135 percent of its GDP, Italy will be particularly vulnerable in 2020.

If the virus cases continue to increase in the Eurozone, regional growth could halve to 0.5 percent or worse.

In North America, local transmissions are on rapid rise, yet local testing is badly lagging. Despite greater awareness of the coronavirus and weeks of time to prepare, politization replaced mobilization, coupled with a series of missteps, including faulty and belated local testing, failures in evacuations and quarantines, lax enforcement and monitoring of self-quarantines.

Recently, the IMF projected US growth to suffer a slowdown from 2.0 to 1.6 percent. But the estimate is too optimistic. After the White House’s delays of outbreak management, the Fed cut interest rates close to zero, coupled with a new round of $700 billion for quantitative easing.

In the short-term, the move is understandable. But in the long-term, it compounds new risks. As the US national debt now exceeds $23.5 trillion (107.3% of GDP), Washington’s debt burden is at par with Italy just before its 2010 European Union (EU) sovereign debt crisis.

Moreover, the Fed’s rate cut is likely to be coupled with fiscal stimulus, which may still not suffice. Yet central banks in Europe, the UK and Japan will follow the US footprints into more monetary and fiscal accommodation. But that is likely to fail to quell virus fears, if infection rates continue to soar.

Prior to the coronavirus, Japanese growth contracted 0.7 percent in the 4th quarter of 2019. After last fall’s consumption tax and the consequent economic turmoil, contraction prevailed in January, while great uncertainty overshadows the 2020 Olympics. And Japan’s sovereign debt is already 2.4 times bigger than its economy.

In addition to Japan and South Korea, the rest of Asia’s advanced economies are in or almost in recession, including Australia and the regional financial hubs Singapore and Hong Kong. Since these countries are significant investors in Southeast Asia, their challenges will reverberate across emerging Asia.

Early damage limited in emerging economies, risks rising

In Southeast Asia, the expected 5 percent growth is now history. Even countries that have strong structural growth potential, including Indonesia, Vietnam and the Philippines, are not immune to indirect short-term hits as their trade, investment, migration and remittance flows depend on international environment.

The same goes for South Asia, particularly India, Pakistan and Bangladesh. In India, the growth rate in the past two years has decelerated from 7.7 percent to 4.7 percent in January. The impact of the global pandemic will compound such threats.

Before the crisis, Chinese economy was still benefiting from a mild recovery. Recently, the IMF anticipated China’s growth below 5.6 percent. US analysts anticipate baseline growth of less than 5%, with significant downside risk. However, if China can limit the adverse impact mainly to the first quarter of this year, a variation of the rebound story is still possible.

The real risk in China and other large emerging economies is the potential negative feedback effect from the world economy in the second quarter. While virus cases have so far been low in Russia, it will be penalized by oil prices, just as Brazil’s growth has been harmed by the fall of commodities.

In the Middle East, too, virus cases are climbing, from the Gulf to Egypt and Northern Africa’s Maghreb economies. In Iran, US withdrawal from the nuclear deal and incessant efforts at destabilization have been accompanied by a severe outbreak of the novel coronavirus, which will cause further economic erosion.

Sub-Saharan Africa is already struggling with a lingering Ebola crisis in the West and locust plagues in the East. Official virus cases are still low (South Africa, Nigeria, Senegal), but tests have only begun. In simulations, the highest importation risk involves countries (South Africa) that have moderate to high capacity to respond to outbreaks, whereas countries at moderate risk (Nigeria, Ethiopia, Sudan, Angola, Tanzania, Ghana, and Kenya) have variable capacity and high vulnerability.

Seizing opportunities and avoiding risks

If the current downside scenarios were to materialize, the net effect could mean a $2 trillion shortfall in global income. That would penalize developing economies (excl. China) by some $220 billion or more.

In such scenarios, oil exporters would be hit the worst. In the past two months, crude oil prices have halved to less than $30; $10 below the 2008 crisis plunge. While commodity exporters could lose over 1 percentage point of growth, along with those with trade exposure to the most affected economies. The misguided and badly timed oil price war will further compound the erosion.

In developing economies with weaker health systems, endemic poverty and social instability could result in a secondary epidemic with potential global impact. In this crisis, the world economy is only as strong as its most fragile links.

What is really needed is multipolar cooperation among major economies and across political differences. In this quest, China, where containment measures have been successful, can show the way, along with major advanced and large emerging powers.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world and the founder of Difference Group. He has served at the India, China and America Institute (USA), Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net

A version of the commentary was released by China Daily on March 18, 2020

The UK government’s economic strategy to combat the impact of Covid-19 might need a rethink, warns the CEO of one of the world’s largest independent financial advisory organizations.

The warning from Nigel Green, the chief executive and founder of deVere Group, comes as government bonds appear in crisis mode and as the British pound dropped below $1.20 to hit multi-decade lows in a rush into cash.

Mr Green says: “The UK government’s response of a £330bn ‘war chest’ package sounds impressive and has generated positive headlines.

“However, the economic strategy to combat the impact of Covid-19 might need a rethink for two main reasons.

“First, there are concerns that the fiscal stimulus they have offered might not be enough. This is evidenced by spooked stock markets sinking as investors fear the measures are not adequate.

“There are serious questions. Can they get it into the hands of individuals and companies quick enough? Is the system too political to get these measures to the people that matter most and fast enough?

“Second, the government is raising this enormous headline-hitting injection through issuing bonds. But the bond market has responded with fear: the 10-year gilt yield is up from 0.5 per cent yesterday morning to 0.75 per cent.

“An oversupply risk is also exacerbating a wider and deeper lack of confidence, as we have seen on stock markets. The UK’s leading stock index, the FTSE100, was down 4.8 per cent this morning.”

He continues: There are some concerns about the mechanics of markets. The Volcker Rule post-2008 prevents banks warehousing risk, so if everyone sells and there is no-one to buy, then what happens? Previously, banks’ proprietary trading desks would take risks, but they are not allowed to now, meaning central banks will have to step in.

“If the markets don’t function as they should, this could hit the credit markets – a major issue as corporate America has borrowed more than ever before.”

Mr Green concludes: “I’m confident that ultimately the current volatility will highlight that we live in a time of great capabilities, opportunities and great promise.

“But with this volatility, people should revise and perhaps rebalance their financial strategies and portfolios to create, build and protect their wealth as the economic landscape evolves.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

On Tuesday, US stocks quotations rose. The Fed launched the Commercial Paper Funding Facility, CPFF program and began to buy directly short-term corporate bonds in order to help companies affected by the coronavirus pandemic. The same measures were taken during the 2008 crisis and were quite effective. Let us remind that on Sunday the Fed lowered the rate to 0.25%. An additional positive factor for the stock market was the decision of the Administration of the US President Donald Trump to allocate $ 1.2 trillion as economic assistance to business and American citizens. The S&P 500 (+6%), Nasdaq (+6,23%) and Dow Jones Industrial Average (+5,2%) indexes rose. The S&P 500 is still 25% below its historic maximum, which was recorded on February 19, 2020. On Monday, it collapsed by 12%, which was the 3rd highest drop in its history. The first powerfull drop of the S&P 500 was in 1929, during the Great Depression, and the second in 1987, during the crisis. Yesterday, the following sectors of the S&P 500 turned out to be growth leaders: utilities (+ 13%), consumer commodities (+ 8.4%) and high technologies (+ 6.8%). We can also note good demand for the shares of individual pharmaceutical companies that announced the development of drugs from Covid-19: Pfizer Inc (+6,6%), Regeneron Pharmaceuticals Inc (+11,5%). Yesterday, the turnover of US exchanges amounted to 16.9 billion shares, which is 20% more than the 20-day average (14 billion). Today data on the residential real estate market for February will come out in the US. The ICE dollar index rose yesterday, and over the past 2 weeks has risen by almost 5%. There is a strong demand for US dollars in the world, as investors buy them when they get rid of the weak currencies of those countries that depend on exports: Canadian, Australian, New Zealand dollars, euros, the Russian ruble and others.

European stock indices fall today again after sluggish growth on Tuesday

European stocks rose yesterday along with American ones. Another positive factor was the statement by the Spanish government on the allocation of 200 billion euros to help the Spanish economy, which suffered from the coronavirus pandemic. Top gainers were the sectors of utilities and telecommunications. Top losers were paper airlines, tourism and entertainment sectors. Shares in the UK-based Cineworld Group cinema chain fell by 43% yesterday and the SSP Group restaurant chain 33% after news on quarantine in Britain. The British FTSE 100index crashed this morning by almost 5%. The shares of aircraft manufacturers fell significantly: Airbus (-12.8%), MTU Aero Engines (-15%) and Rolls Royce (-18%). Investment Bank JP Morgan predicts that recovery of air travel in Europe will take several years. According to it, in 2020 air traffic will be 20-30% lower than last year. Today, the EU trade balance for January and inflation for February in the 2nd reading will be released. EUR/USD quotes slightly decreased today. Investors expect that, following the example of Spain, other European countries will also announce economic stimulus measures.

Nikkei resumes decline after yesterday’s growth

All Asian indices fell today, except for the Thai SET (+ 1.2%). Nikkei grew yesterday thanks to a statement from Bank of Japan. The Japanese Central Bank intends to spend 12 trillion yen ($ 113 billion) by the end of the year on the purchase of securities of Exchanged Traded Funds (ETFs) – owners of shares in Japanese companies in order to support the Japanese stock market and dilute the portfolio of shares already existing on its balance sheet. The head of Bank of Japan Haruhiko Kuroda said that at current stock prices, the hidden losses of his department could amount to 2-3 trillion yen. Today, Nikkei resumed falling and updated its minimum over 3 and a half years. Fujifilm Holdings Corp quotes soared by 15% thanks to reports from the Chinese authorities that its Avigan medication is helping treat coronavirus. Hang Seng fell 4.2% today and updated a 3-year low.

Brent Brent drops below its psychological level of $ 30 per barrel

Futures quotes for U.S. crude collapsed to a 17-year low. Goldman Sachs Investment Bank expects Brent quotes to drop down to $ 20 per barrel in the 2nd quarter of this year. According to its forecasts, global demand will fall in March this year by 8 million barrels per day (BPD), and for the whole of 2020 – by 1.1 million BPD. Rystad Energy Agency expects a decrease in global oil demand by 2.8 million bpd this year. Moreover, in April it predicts a drop in global demand by 11 million bpd compared to April 2019. The main reason for this may be the quarantine, introduced immediately in almost all countries. For example, Japan reduced oil imports by 9% in February. Australia has canceled all international departure flights for its citizens. Australian prime minister, Scott Morrison, said it could last six months.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Iceland’s central bank cut its key interest rate for the second time in a week and slashed the Countercyclical Capital Buffer for banks to zero, saying the spread of the coronavirus is having a “profound impact on communities, dampening economic activity and eroding financial conditions worldwide” and while it is uncertain how strong this impact will be and how long it will last, “is is clear that the economic outlook for Iceland has deteriorated sharply, at least for the short term.”

The Central Bank of Iceland (CBI) cut its benchmark seven-day deposit rate by another 50 basis points to 1.75 percent and has now cut it three times this year by a total of 125 points.

It is CBI’s second unscheduled rate cut following a first emergency cut on March 11, when it also cut the reserve requirement on banks to 0 percent from 1.0 percent to ease their liquidity positions.

Since May 2019, when the outlook for the North Atlantic island began to deteriorate, CBI has cut the rate eight times and by a total of 2.75 percentage points.

CBI’s Financial Stability Committee cut the countercyclical capital buffer on financial institutions by 200 basis points to 0.0 percent and said it would not raise the buffer in the next 12 months, which means it will remain unchanged for at least 2 years until the first quarter of 2022.

The committee said the capital position of Iceland’s banks is strong, well above current requirements and the banking system is well equipped to respond to shocks.

However, it is important to ease the negative impact of increased payment arrears and removing the buffer will make it easier for banks to support households and businesses by increasing the flexibility for new lending in amounts up to 350 billion krona, or 12.5 percent of their loan portfolio.

The Central Bank of Iceland released the following statements:

“The Monetary Policy Committee (MPC) of the Central Bank of Iceland has decided to lower the Bank’s interest rates by 0.50 percentage points. The Bank’s key interest rate – the rate on seven-day term deposits – will therefore be 1.75%. This action eases the monetary stance still further, in view of the continued deterioration in the economic outlook following the accelerated spread of COVID-19 and the broad-based actions taken by Iceland and other countries in an attempt to slow the spread of the virus. The MPC will continue to monitor economic developments and will use the tools at its disposal to support the domestic economy.”

“The Financial Stability Committee of the Central Bank of Iceland has decided to reduce the countercyclical capital buffer on financial institutions from 2% to 0%. Rules to this effect have been approved and will take effect upon publication in the Law and Ministerial Gazette (Stjórnartíðindi). The Committee will not increase the countercyclical capital buffer in the next twelve months; therefore, according to the applicable rules, it will remain unchanged for at least two years, until Q1/2022. The spread of COVID-19 has had a profound impact on communities, dampening economic activity and eroding financial conditions worldwide. It is uncertain how strong this impact will be and how long it will last, but it is clear that the economic outlook for Iceland has deteriorated markedly, at least for the short term. The Icelandic banks’ capital position is strong, and well above current Central Bank requirements. The banking system is well equipped to respond to shocks. It is important, however, to mitigate the negative impact of increased arrears and impairment on the intermediation of credit. Lifting the countercyclical capital buffer requirement will make it easier for the banking system to support households and businesses by increasing flexibility for new lending in an amount ranging up to 350 b.kr., or 12.5% of the current loan portfolio, all else being equal. The main objectives of the countercyclical capital buffer are to strengthen financial institutions’ resilience to cyclical risk and strengthen credit intermediation during contractionary episodes, thereby mitigating the impact of the financial cycle on the real economy. In recent years, the buffer has been built up in order to mitigate cyclical risk. The Financial Stability Committee urges financial institutions to take into consideration the currently high level of economic uncertainty when they take decisions on dividend payments and stock buybacks in the coming term. The Committee expects the scope created with the reduction in the countercyclical capital buffer to be used to supporthouseholds and businesses. The banking system’s response, the position of households and businesses, and the financial conditions offered to them will be closely monitored in the coming term. The Committee is prepared to use the tools at its disposal to safeguard financial stability in Iceland.” www.CentralBankNews.info

Be prepared for some really ugly earnings data in Q2 and Q3 of this year, then we’ll figure out if our expectations were accurate or not and what we should be doing to plan going forward.

The type of market condition I think we have entered could be here for a long time, and it’s going to be a traders’ market, which means you must have a trading strategy, plan your trades, and trade your plan. It’s amazing how simple a few trading rules that are written down on paper can save you thousands of dollars a week or month from locking in gains or cutting losses.

I have this mini trading strategy mastery course if you want to take control of your trades and override your emotional issues. And also if you want to start making money from home which is the only option going forward the next 3-6 months from the looks of it my trading as a business program is something to think about doing.

– If you hold winners until they turn into losers

– Taking too large of a position and get stuck with a drawdown so large that if you close the position you will lose 10-50% of your trading account

– have masted the art of buying high and selling low repeatedly?

All these things happen to most traders, and they can easily be overcome with a logical game plan I cover in the crash courses, pun intended ?

In short, if you have lost money with your trading account this year giving back years of gains, I think it’s worth joining my trading newsletter so you can stay on top of the markets and if you really want to excel take my mini-courses. I take the loud, emotional, and complex markets and deliver simple common sense commentary and a couple of winning trades each month for you to follow.

My trading is nothing extreme or crazy exciting because I’m not an adrenaline trading junky. I only want to grow my entire portfolio 2-4% a month with a couple of conservative ETF trades. Earning 22% – 48% return on my capital every year without the stress of being caught up in this type of market, and knowing I have a proven bear market trading strategy incase this market continues to fall is a comforting thought.

As a technical analysis and trader since 1997, I have been through a few bull/bear market cycles. I believe I have a good pulse on the market and timing key turning points for short-term swing traders.

Visit my ETF Wealth Building Newsletter and if you like what I offer, and ride my coattails as I navigate these financial markets and build wealth while others lose nearly everything they own during the next financial crisis.

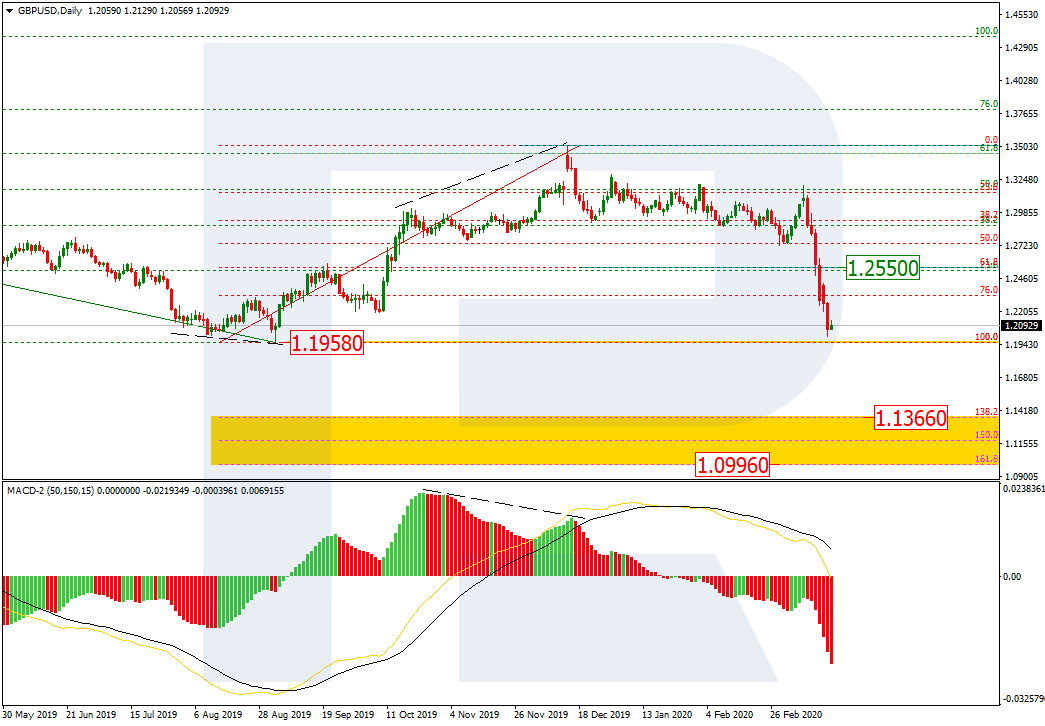

As we can see in the daily chart, a quick descending wave in GBPUSD, which started when the Bank of England decided to cut the benchmark rate, is heading to break the key low at 1.1958. If it happens, the pair may continue falling towards the post-correctional extension area between 138.2% and 161.8% fibo at 1.1366 and 1.0996 respectively. the resistance is 61.8% fibo at 1.2552.

In the H1 chart, the pair is getting closer towards the low at 1.1958. At the same time, there is a convergence on MACD, which may indicate a possible pullback towards the resistance in the nearest future.

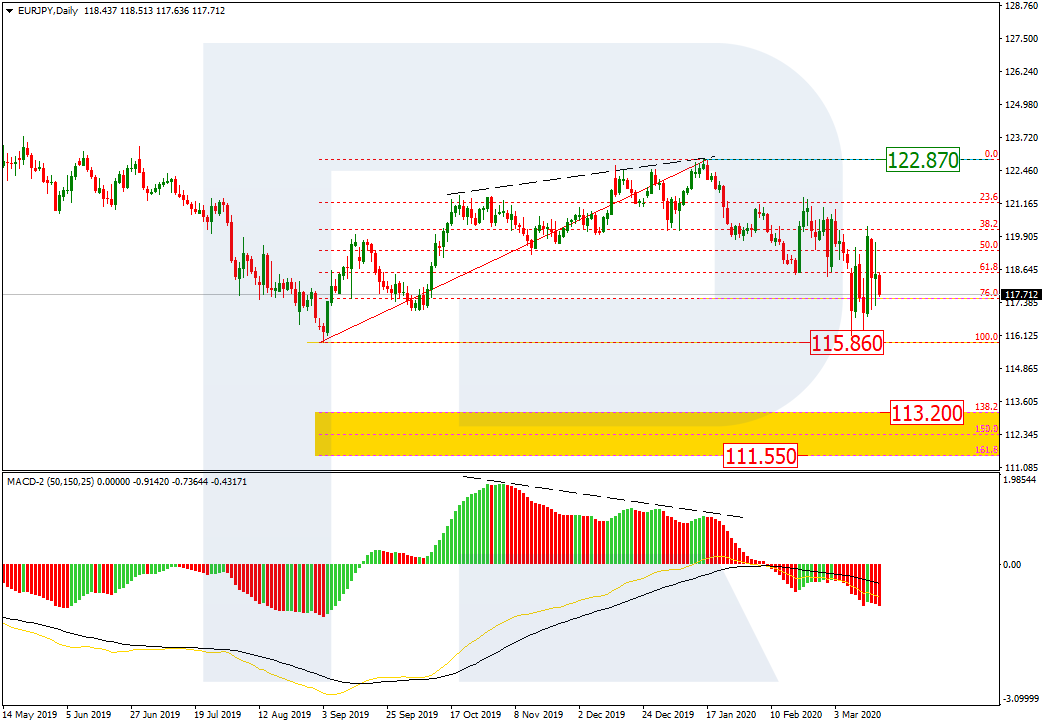

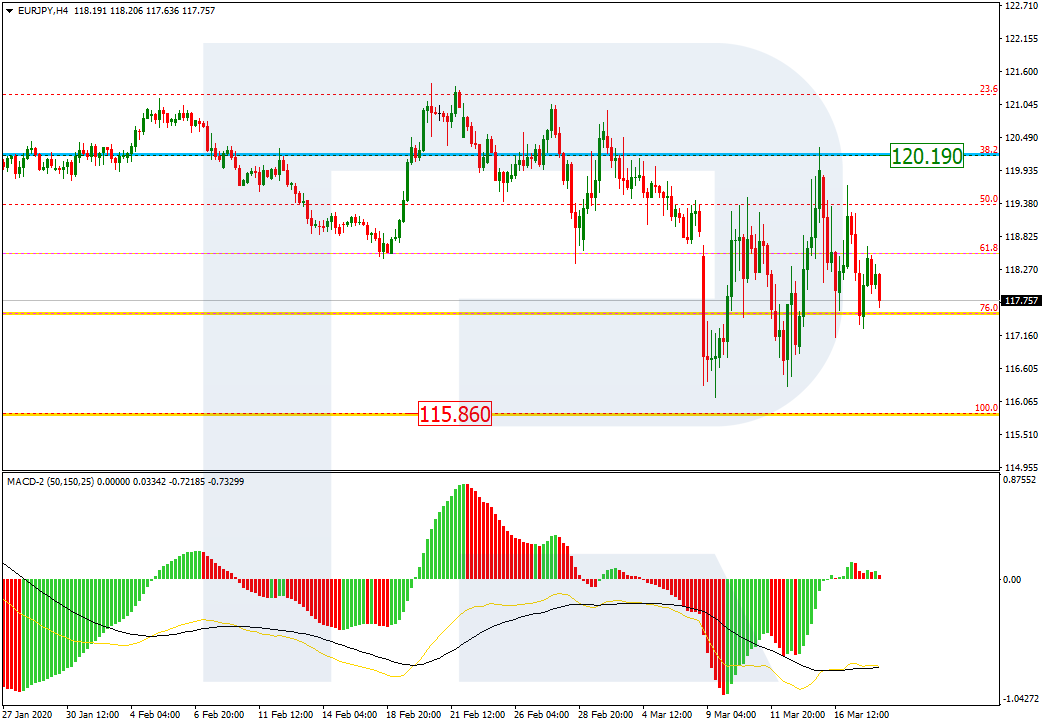

EURJPY, “Euro vs. Japanese Yen”

As we can see in the daily chart, the descending wave attempted to reach and test the long-term low at 115.86. However, after reaching the low, the pair rebounded from it, thus indicating a long correction. If the price breaks the low, the instrument may continue falling towards the post-correctional extension area between 138.2% and 161.8% fibo at 113.20 and 111.55 respectively.

In the H4 chart, the correction is taking the form of a volatile Zigzag. At the moment, EURJPY is moving between the long-term low and 38.2% fibo at 115.86 and 120.19 respectively.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

After forming the second descending impulse at 1.0954, EURUSD is correcting to reach 1.1044. After that, the instrument may resume falling to break 1.1005 and then continue trading downwards with the target at 1.0930.

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD continues falling towards 1.1940. Possibly, the pair may reach this level and then start consolidating near the lows. If later the price breaks this range to the downside, the market may resume trading downwards with the target at 1.1810; if to the upside – start a new correction towards 1.2444.

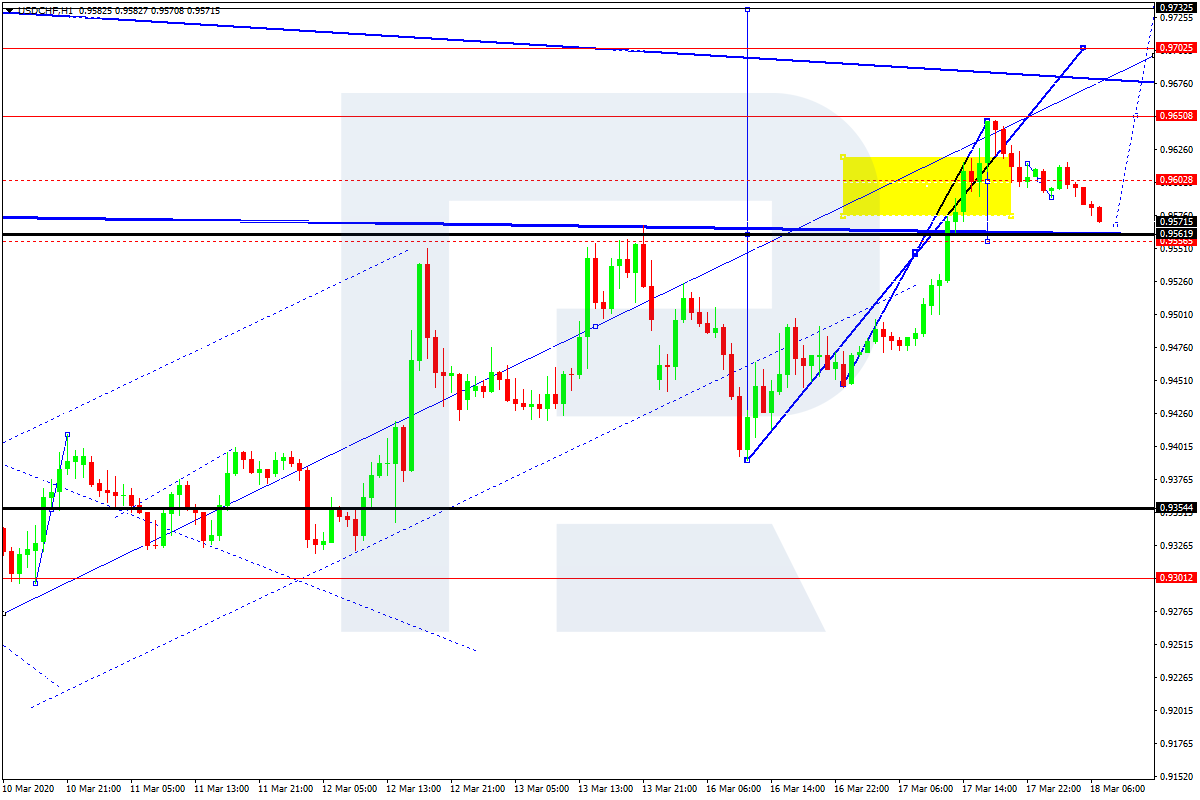

USDCHF, “US Dollar vs Swiss Franc”

USDCHF has completed the ascending structure at 0.9650; right now, it is correcting towards 0.9555. Later, the market may start a new growth with the target at 0.9700.

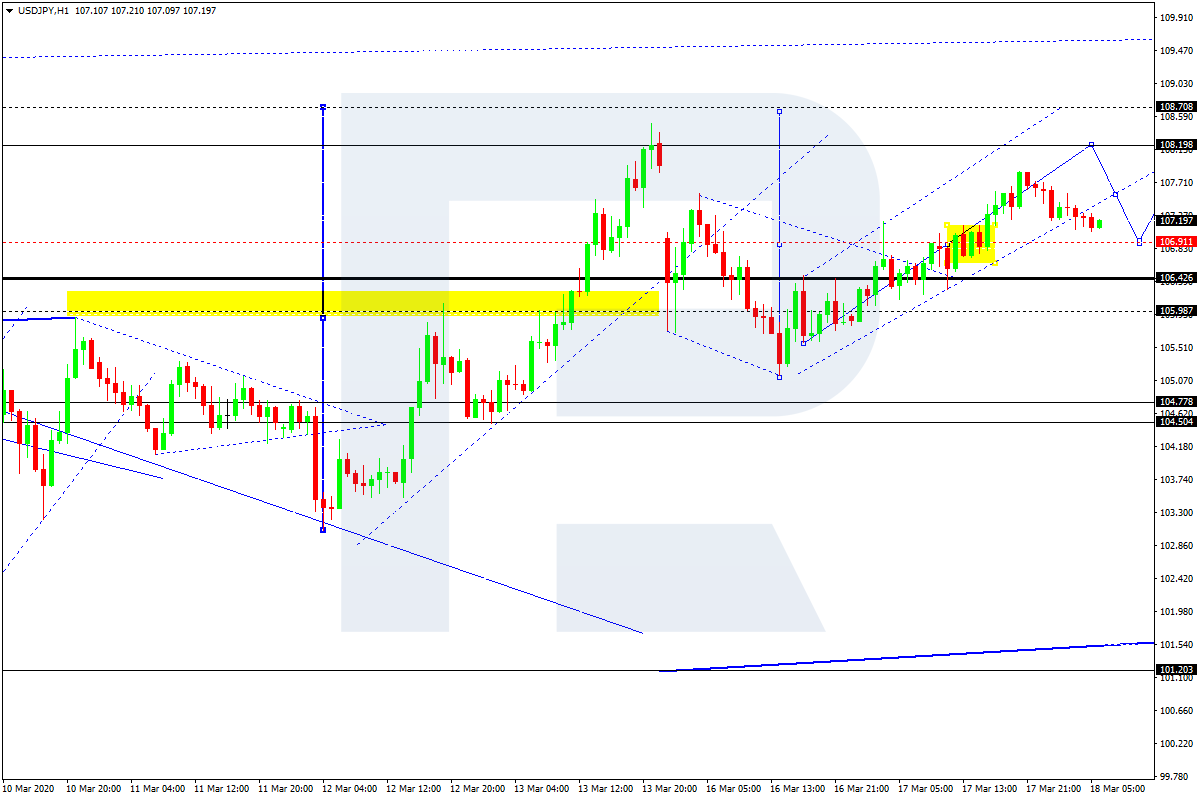

USDJPY, “US Dollar vs Japanese Yen”

After finishing the ascending structure to 107.77, USDJPY is correcting towards 106.44. After that, the instrument may resume trading upwards with the short-term target at 108.20.

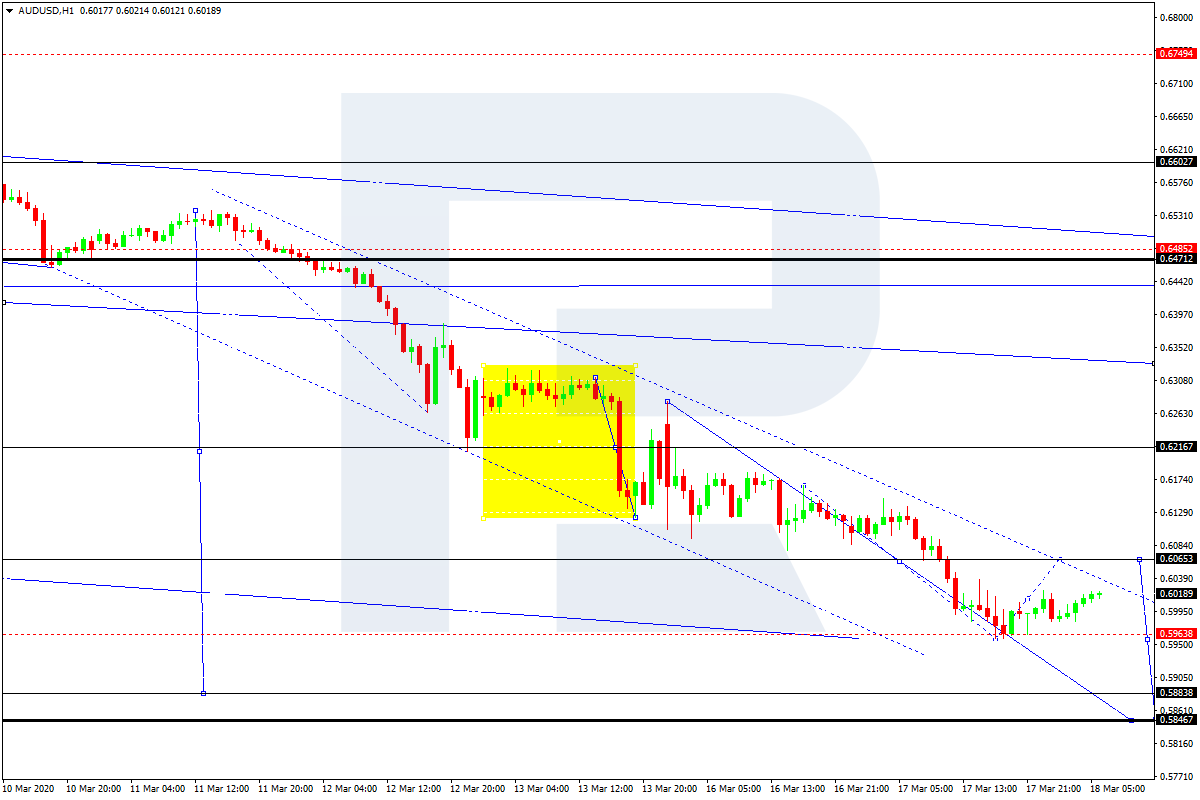

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD has finished the descending structure at 0.5964; right now. it is correcting to reach 0.6065. After that, the instrument may start a new decline with the target at 0.5888.

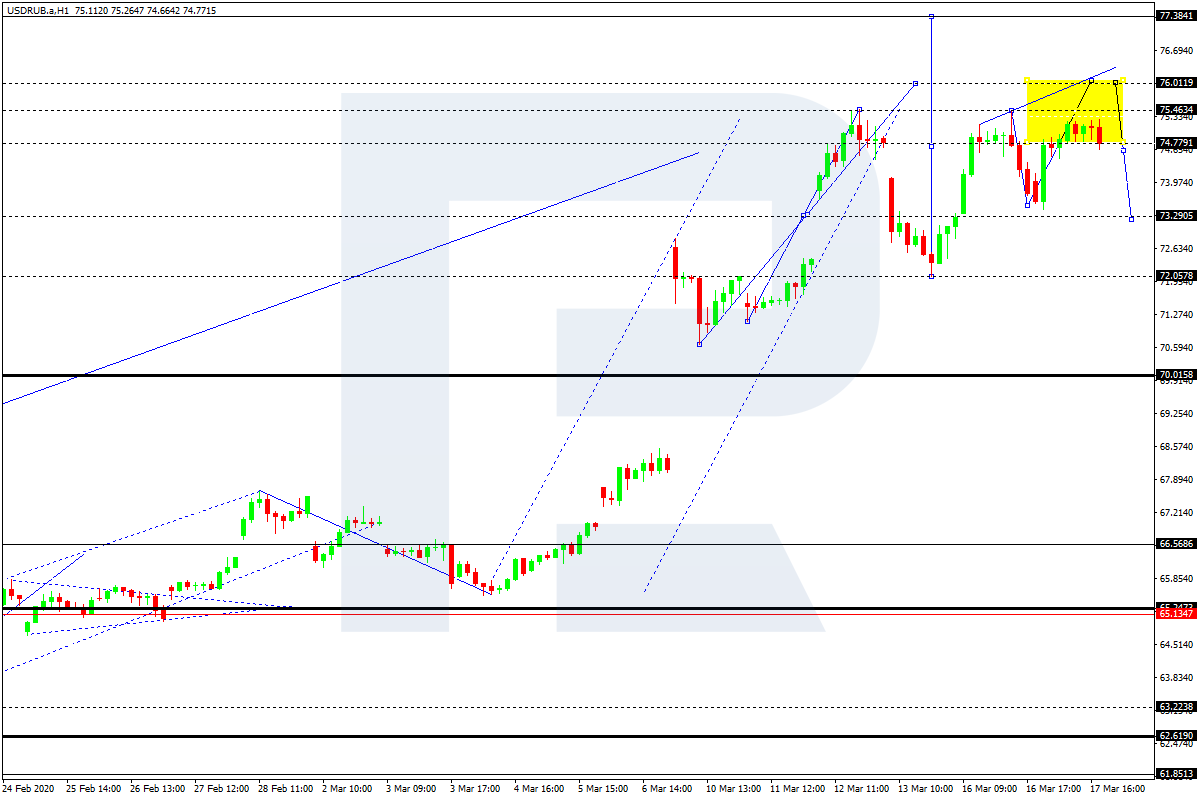

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is consolidating around 74.47. Possibly, today the pair may expand the range up to 76.00. Later, the market may resume trading downwards to reach 73.30 and then start another growth with the target at 77.38.

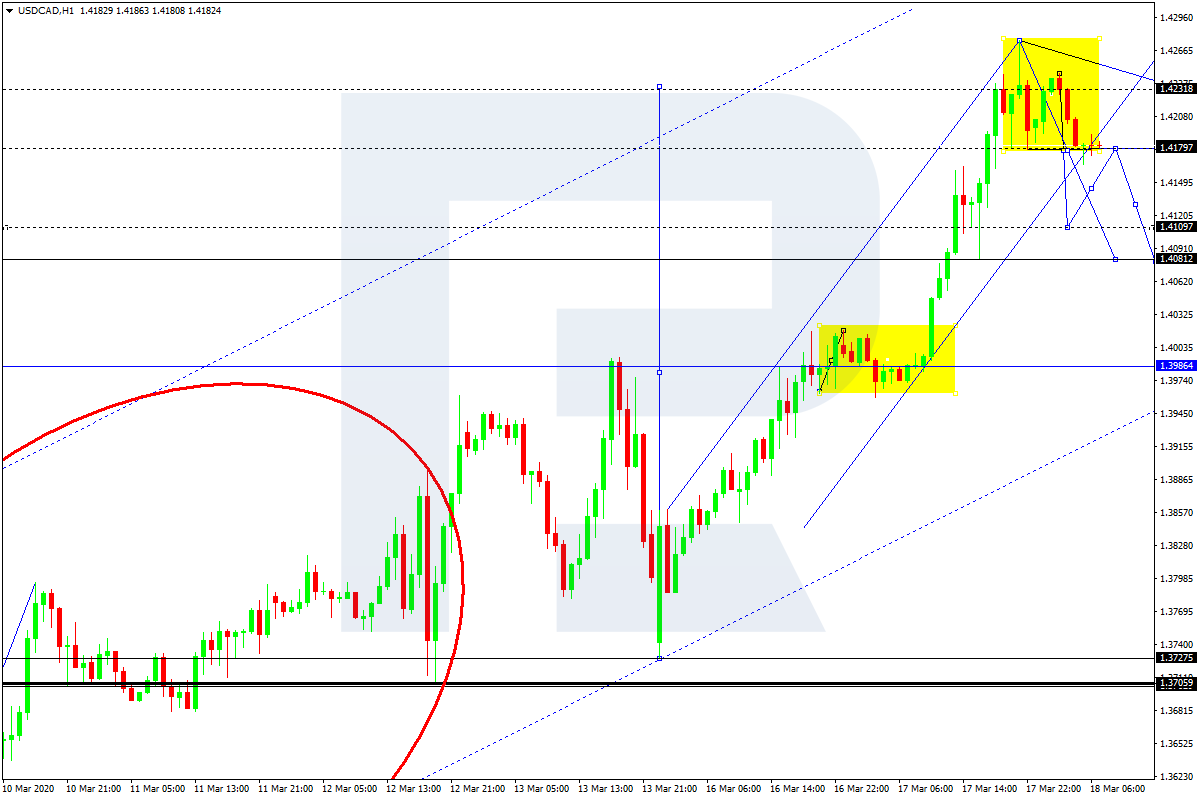

USDCAD, “US Dollar vs Canadian Dollar”

After completing the ascending wave at 1.4275, USDCAD is consolidating above 1.4180. Today, the pair may break this level to the downside and start a new correction with the target at 1.4082.

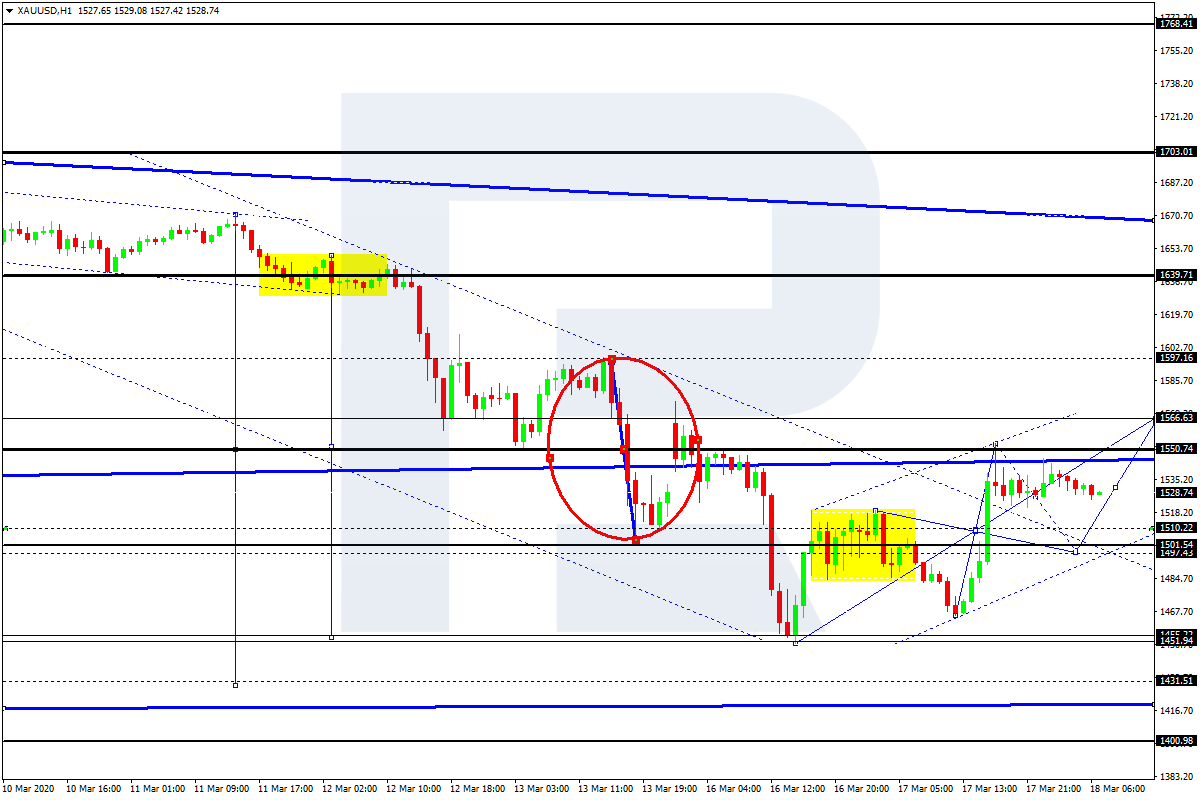

XAUUSD, “Gold vs US Dollar”

Gold has completed the second ascending impulse at 1550.70. Possibly, today the pair may fall to reach 1501.55 and then resume trading upwards with the target at 1566.60. Later, the market may form a new descending structure towards 1440.00.

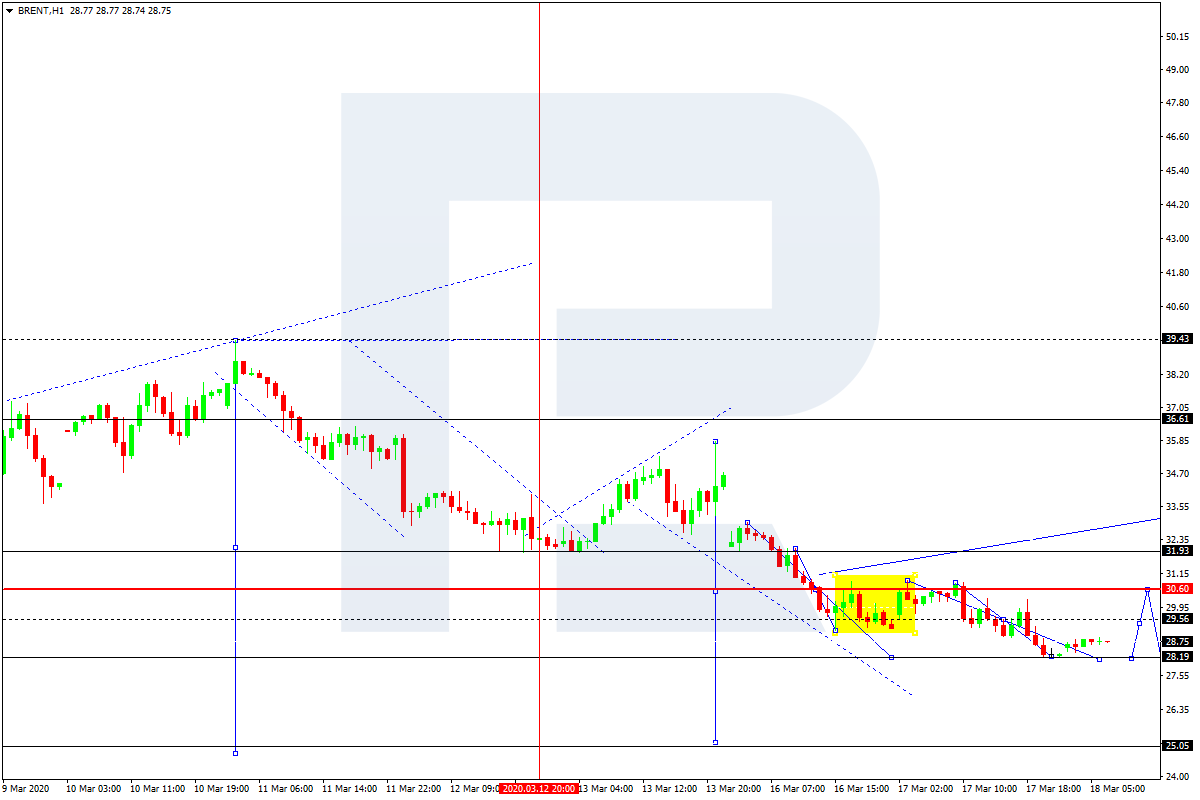

BRENT

Brent continues falling with the target at 27.90. According to the main scenario, the price may reach this level and then start another correction to test 32.00 from below. Later, the market may resume trading downwards with the target at 25.05.

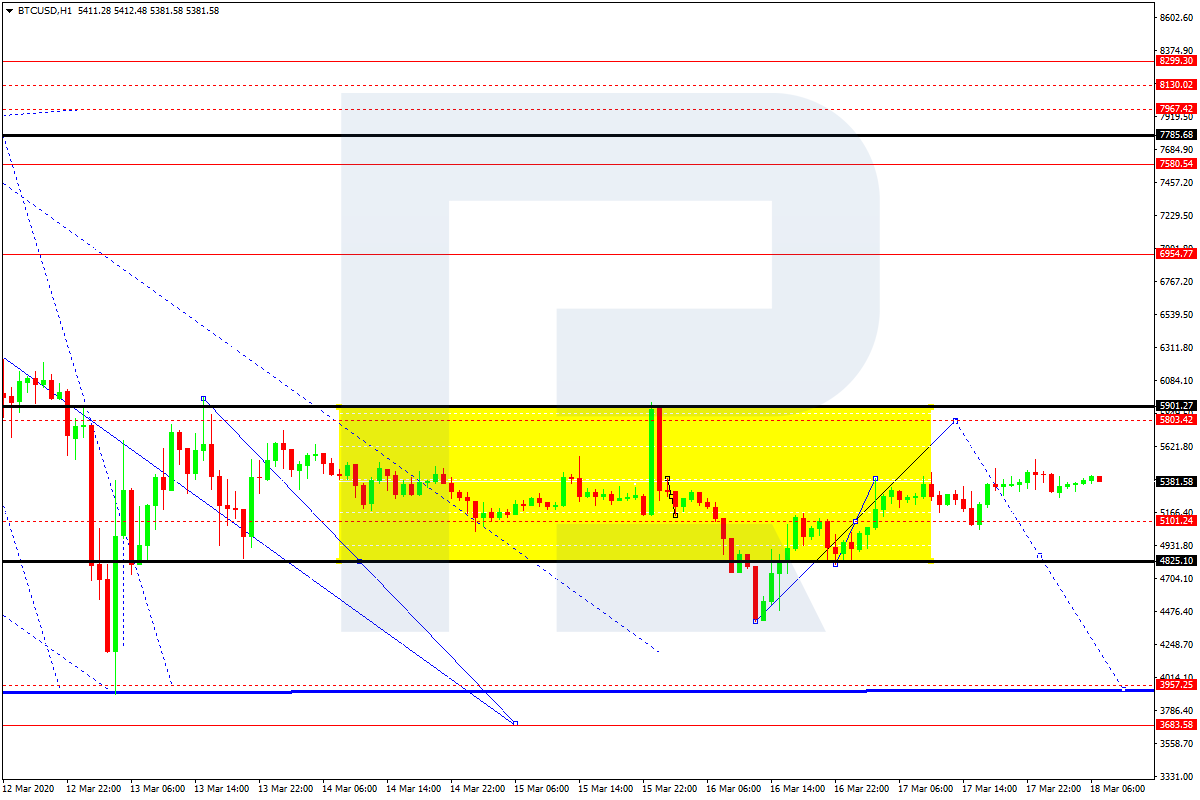

BTCUSD, “Bitcoin vs US Dollar”

BTCUSD is consolidating around 5100.00. Possibly, today the pair may expand the range up to 5800.00 and then form a new descending structure to break 4800.00. After that, the instrument may continue falling with the target at 3900.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

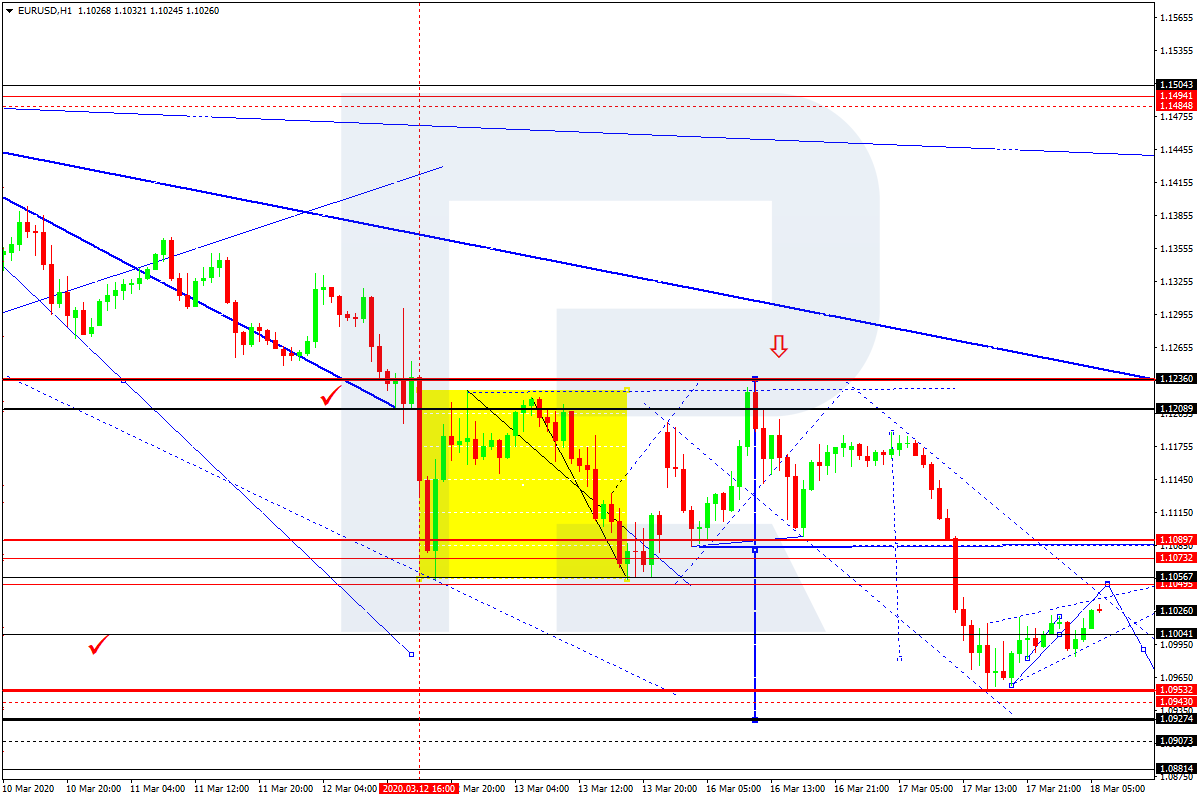

The EUR/USD currency pair has moved down. Yesterday the drop in quotes exceeded 170 points. The trading instrument has set new local lows. The demand for USD grew after Donald Trump’s statements. The US president promised to provide emergency financial aid to the population, to postpone tax payments and to provide new credit incentives. Currently, EUR/USD quotes are consolidating in the range 1.09550-1.10600. The can decline further. Open positions from key levels.

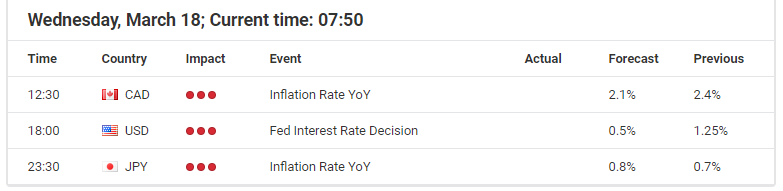

The Economic News Feed for 18.03.2020:

– Inflation Report (EU) – 12:00 (GMT+2:00);

– Real Estate Market Report (USA) – 14:30 (GMT+2:00);

The indicators signal the sellers’ power: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone, indicating a bearish sentiment.

The Stochastic Oscillator is in the neutral zone, the %K line is below the %D line, which gives a sell signal for EUR/USD.

Trading recommendations

Support levels: 1.09550, 1.09000

Resistance levels: 1.10600, 1.11600, 1.12300

If the price fixes below 1.09550, expect further decline of EUR/USD to the round level 1.09000.

Alternatively, the quotes could recover toward 1.09000.

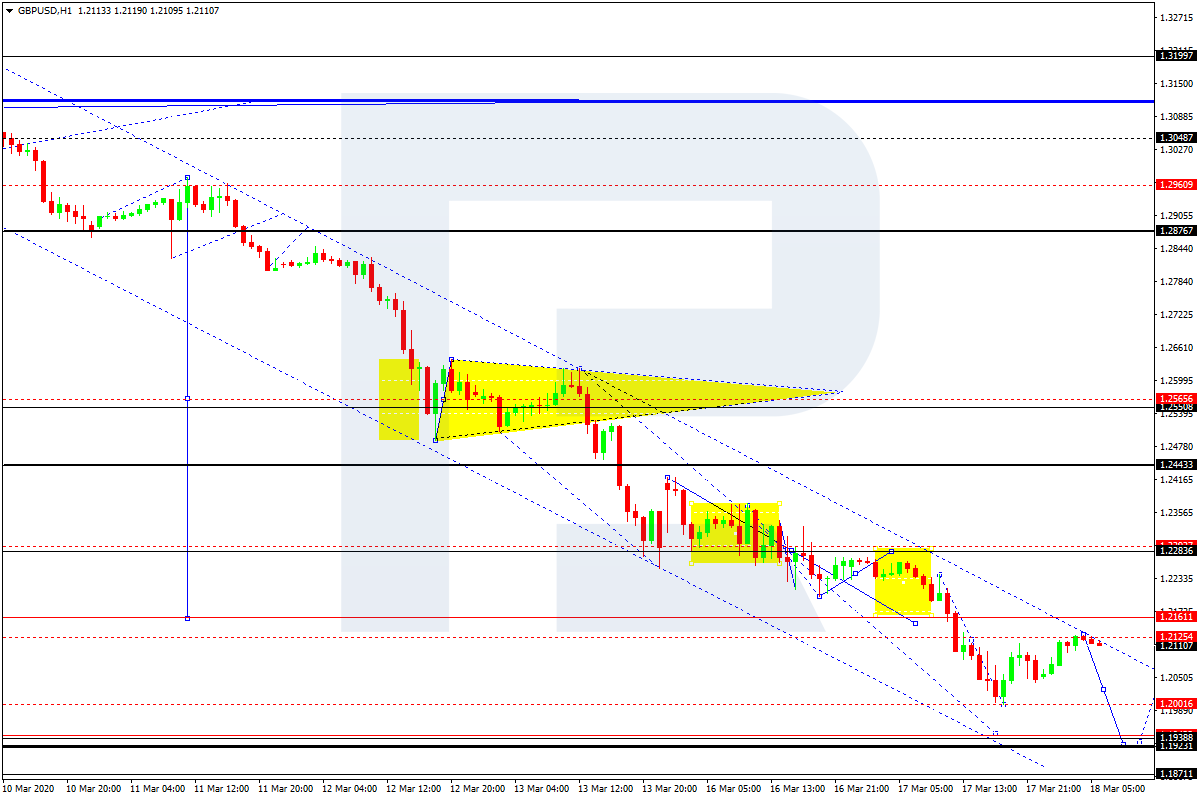

The GBP/USD currency pair

Technical indicators of the currency pair:

Prev Open: 1.22688

Open: 1.20594

% chg. over the last day: -1.23

Day’s range: 1.20200 – 1.21295

52 wk range: 1.1959 – 1.3516

Aggressive sales are still observed on GBP/USD currency pair. Over the past two weeks, the pound lost over 1000 points. GBP reached the level of $1.20. At the moment, the trading instrument is consolidating. Investors continue to monitor the current information about the spread of the virus COVID-19. Technical correction of GBP/USD quotes is not ruled out in the near future. Positions should be opened from key levels.

The Economic News Feed for 18.03.2020 is calm.

The indicators signal the sellers’ power: the price has fixed below 50 MA and 100 MA.

The MACD histogram is in the negative zone, which indicates a bearish sentiment.

The Stochastic Oscillator has reached the oversold zone, the %K line has started to cross the %D line. There are no signals at the moment.

Trading recommendations

Support levels: 1.20000, 1.19000

Resistance levels: 1.21350, 1.22750, 1.24250

If the price fixes below the round level of 1.20000, GBP/USD quotes are expected to fall further toward 1.19500-1.19000.

Alternatively, the quotes could correct toward 1.22500-1.22300.

The USD/CAD currency pair

Technical indicators of the currency pair:

Prev Open: 1.40007

Open: 1.42021

% chg. over the last day: +1.61

Day’s range: 1.41663 – 1.42601

52 wk range: 1.2949 – 1.3566

USD/CAD currency pair continues to show a stable upward trend. The quotes have updated the multi-year highs. The CAD is under pressure from a significant drop in “black gold” prices. At the moment the local support and resistance levels are at 1.41500 and 1.42750, respectively. Nevertheless, technical correction of the trading instrument is not ruled out in the nearest future. We expect important statistics on Canadian economy. Open positions from key levels.

The basic consumer price index in Canada will be published at 14:30 (GMT+2:00).

The indicators signal the power of buyers: the price has fixed above 50 MA and 100 MA.

The MACD histogram is in the positive zone, which indicates a bullish sentiment.

The Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which also gives a signal to buy USD/CAD.

Trading recommendations

Support levels: 1.41500, 1.40150, 1.39500

Resistance levels: 1.42750, 1.43500

If the price fixes above 1.42750, consider buying USD/CAD as the price moves toward 1.40500-1.39500.

Alternatively, the quotes could correct toward 1.40500-1.39500.

The USD/JPY currency pair

Technical indicators of the currency pair:

Prev Open: 105.887

Open: 107.604

% chg. over the last day: +1.44

Day’s range: 106.752 – 107.637

52 wk range: 101.19 – 112.41

The technical picture on USD/JPY currency pair is still ambiguous. The trading instrument is in sideways movement. Participants of financial markets are waiting for additional drivers. Demand for safe haven currencies remains at a high enough level. At the moment local support and resistance levels are at 106.500 and 107.850, respectively. It is recommended to open positions from key levels.

The Economic News Feed for 18.03.2020 is calm.

The indicators signal the power of buyers: the price has fixed above 50 MA and 100 MA.

The MACD histogram is in the positive zone, but below the signal line, which gives a weak signal to buy USD/JPY.

The Stochastic Oscillator is in the neutral zone, the %K line is above the %D line, which indicates a bullish sentiment.

Trading recommendations

Support levels: 106.500, 105.250, 104.500.

Resistance levels: 107.850, 108.500

If the price fixes above 107.850, expect the quotes to rise toward 107.850.

Alternatively, they could descend toward 105.700-105.000.

The state of Gold, given the recent developments around the Coronavirus, collapse in oil prices, and the massive monetary stimulus from the Fed last Sunday, is clearly bullish in the mid- to long-term. A run above 2,000 USD seems only a question of time, so the short-term picture stays way more complex.

On Sunday evening, the US central bank, the Fed, took a massive step: it cut rates to 0.0%-0.25%, launched a massive QE program of USD 700 billion, announced swap lines with global central banks to make sure that enough USD are available, and cut reserve ratios for banks to 0 in anticipation of today’s Fed rate decision. This potentially makes the event a ‘non-event’.

However, these extreme measures failed to lift the market. Equities and Gold dropped. Gold, usually a safe-haven by typically profiting from a dovish Fed and any US yield collapses, failed to gain momentum.

While we could certainly argue that this is a result out of the sharper bounce in US yields after its short-term drop below 0.3% over the last week, this seems only half the truth.

In fact, recent data from the Commitment of Traders Report underlines the point that the drop in Equities resulted in margin calls, which led larger market participants to reduce their Gold Long exposure to meet these.

In addition to this, traders should also recall the drop in Gold during the 2008 financial crisis, where a deflationary shock resulted out of the credit crunch which had a negative impact on the yellow metal with dropping and taking on momentum from 2010 onwards.

This time could be similar, meaning that despite elevated volatility and dropping US yields driven by risk-off tendencies, Gold may fail to profit and see a drop, going hand in hand with a dropping USD and dropping Equity prices.

While the mid- to long-term mode in Gold stays bullish, short-term a drop below 1,440/450 USD would technically darken the picture, activating 1,250/260 USD as a first target:

Source: Admiral Markets MT5 with MT5SE Add-on Gold Daily chart (between December 14, 2018, to March 17, 2020). Accessed: March 17, 2020, at 10:00 PM GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.