US stock market plunge renewed on Friday as Senate considered a second bailout package that could exceed $1 trillion while President Trump announced interest on student loans would be waived temporarily following postponement of the US tax filing in the US to July 15. The S&P 500 fell 4.3% to 2304.92, almost doubling the weekly loss to 15%. Dow Jones industrial dropped 4.6% to 19173.98. The Nasdaq ended 3.8% lower at 6879.52. The dollar strengthening halted as the Federal Reserve’s bond and other debt security purchases to provide liquidity reached at least $300 billion for the week. The live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.5% to 102.37 and is lower currently. Futures point to lower market openings today.

CAC 40 leads European indexes’ rebound

European stocks rebounded on Friday. Both EUR/USD and GBP/USD reversed their sliding on Friday with both pairs higher currently. The Stoxx Europe 600 Index added 1.4% led by travel and leisure shares. The DAX 30 advanced 3.7% to 8928.95 Friday. France’s CAC 40 jumped 5% and UK’s FTSE 100 edged up 0.8% to 5190.78.

Asian indexes fall while Nikkei rebounds

Asian stock indices are mostly lower today after Senate voted against the nearly $2 trillion economic rescue package on weekend as Democrats claimed the bill was tilted too much toward aiding corporations and would not do enough to help individuals and healthcare providers. Senate will be voting again on the revised bill today. Nikkei however managed to gain 2% to 16887.78 after reports the International Olympic Committee might postpone, rather than scrap, the Tokyo Games. Yen continued its climbing against the dollar. China’s markets are falling: the Shanghai Composite Index is down 3% while Hong Kong’s Hang Seng Index is 5.2% lower. Australia’s All Ordinaries Index plummeted 5.6% despite government announcement of $38.5 billion stimulus package on Sunday and resumed sliding of Australian dollar against the greenback.

Brent futures prices are in retreat following 20.3% plunge last week. Prices fell on Friday after news that Russian President Vladimir Putin refuses to submit to what Russia’s government sees as oil blackmail from Saudi Arabia. Brent for May settlement lost 5.3% to $26.98 a barrel Friday.

Gold rebounds as Dollar weakens

Gold prices are extending gains today. Prices fell on Friday as dollar strengthening reversed. Gold for April delivery gained 0.4% to $1484.60 on Friday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Shares of Bellerophon Therapeutics reached a new 52-week high price after the firm reported that the FDA granted emergency expanded access for its INOpulse® nitric oxide delivery system device for use in treatment of COVID-19 virus.

Bellerophon Therapeutics Inc. (BLPH:NASDAQ), which focuses on developing innovative therapies in the treatment of cardiopulmonary diseases, today announced that “the U.S. Food and Drug Administration has granted emergency expanded access allowing its proprietary inhaled nitric oxide (iNO) delivery system, INOpulse®, to immediately be used for the treatment of COVID-19.”

The company explained that “nitric oxide (NO) is a naturally produced molecule that is critical to the immune response against pathogens and infections and that in vitro studies have shown that NO inhibits the replication of severe acute respiratory syndrome-related coronavirus (SARS-CoV) and improves survival for cells infected with SARS-CoV.”

The firm noted that “in a clinical study of patients infected with SARS-CoV, iNO demonstrated improvements in arterial oxygenation, a reduction in the need for ventilation support and an improvement in lung infiltrates observed on chest radiography.” The company stated that due to the genetic similarities between the two coronaviruses, the SARS-CoV data supports the potential for iNO to provide real benefit for patients infected with COVID-19.

The company reported that “the clinical spectrum of the COVID-19 infection ranges from mild signs of upper respiratory tract infection to severe pneumonia and death and added that preventing disease progression in patients with mild or moderate disease would improve morbidity/mortality and significantly reduce the impact on limited healthcare resources.”

The company’s CEO Fabian Tenenbaum commented, “Based on currently available data and its significant role in the immune response, we believe INOpulse has the potential to be a safe and effective treatment for COVID-19…INOpulse technology utilizes targeted pulsatile delivery of inhaled nitric oxide, providing important antiviral potential, as well as improved arterial oxygenation. Importantly, INOpulse is designed to treat patients in the outpatient setting, which may be critical in helping combat the further spread of the virus and significantly alleviate the mounting impact on hospitals and intensive care units. We look forward to supporting patients and physicians in order to help address the current COVID-19 global health pandemic.”

Bellerophon Therapeutics is a clinical-stage therapeutics company headquartered in Warren, N.J. The company concentrates on developing products that address medical needs in the treatment of cardiopulmonary diseases. The firm’s primary focus is on developing its nitric oxide therapy for patients with pulmonary hypertension using its INOpulse delivery system. The firm’s INOpulse device delivers brief, targeted pulses of nitric oxide timed to occur at the beginning of a breath for delivery to the alveoli of the lungs which minimizes the amount of drug required for treatment.

Bellerophon Therapeutics began the day with a market capitalization of around $15.5 million with approximately 4.58 million shares outstanding and a short interest of about 2.1%. BLPH shares opened greatly higher today at $25.62 (+$22.23, +655.75%) over yesterday’s $3.39 closing price and reached a new 52-week high price this morning of $26.00. The stock has traded today between $15.28 and 26.00 per share and is currently trading at $18.67 (+$14.28, +443.39%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Simple, non-invasive hospital-style wrist band and SaaS technology could spell explosive growth for company as the world combats the coronavirus.

A Vancouver-based tech company has recently acquired an effective quarantine monitoring technology, now being used in Hong Kong, to combat the spread of COVID-19. The adaptation of its Bluetooth enabled bracelet and software technology gives Blockchain Holdings Ltd. (BCX:CSE) the potential for explosive growth in the coming months.

The Hong Kong government alone is rapidly expanding its use of the system, coined TRACEsafe, to manage its quarantine program for foreign visitors at all of its points of entry.

Based on the success of the program in Hong Kong, BCX expects to roll out TRACEsafe in multiple countries in the coming weeks and months, with early adapters including the larger Asian countries. Built on a software as a service (SaaS) platform, and utilizing a simple, hospital-style bracelet produced by an outsourced manufacturer, BCX is poised to scale significantly to meet a truly global demand as COVID 19 continues to gain momentum in the coming months.

Earlier today, BCX announced that it has entered into an agreement to acquire 100% of the TRACEsafe assets from California-based WiSilica Inc. As described in its news release, “TRACEsafe is a global health product directed at governmental and corporate organizations as they fight a global pandemic and try to keep global commerce flowing.” BCX will pay TRACEsafe a total consideration of US$1,574,189, composed of 6,000,000 common shares of BCX at a deemed price of CA$0.305 per share and the remaining US$250,000 in cash payments. To fund the acquisition, BCX is raising CA$1,000,000, of which CA$250,000 will go towards the cash component of the acquisition and the rest will go to establishing partnerships in new markets. In their favor, return on equity and the payback period is fast, once the system is in place.

The TRACEsafe System

TRACEsafe is a ground-breaking suite of patent-protected medical products including the flagship identification bracelet and software system used to enforce quarantine guidelines set out by governments for travelers.

The first to implement the technology was the Hong Kong Supply Chain and Multi-tech R&D center, which started monitoring foreigners entering Hong Kong over the bridge from Macau. Understandably Hong Kong was an early adapter as it was hit hard by the SARS outbreak in 2003.

To enforce compliance upon re-entering the country, Hong Kong had citizens install a What’s App or WeChat on the users’ phones using the locationing features of these applications. This was easily circumvented as a user could simply leave their phone at home with someone else.

The TRACEsafe pairs itself to the hospital-style wristband itself with Bluetooth, so once the connection is broken by distance, or if the bracelet is removed the Hong Kong government levies a steep fine of HK$25,000 and six months in jail. Upon entry to Hong Kong, each bracelet has its own unique QR code which is scanned by a customs agent, the app is downloaded onto the phone, then paired to the bracelet. After required quarantine period the bracelet is simply disposed of.

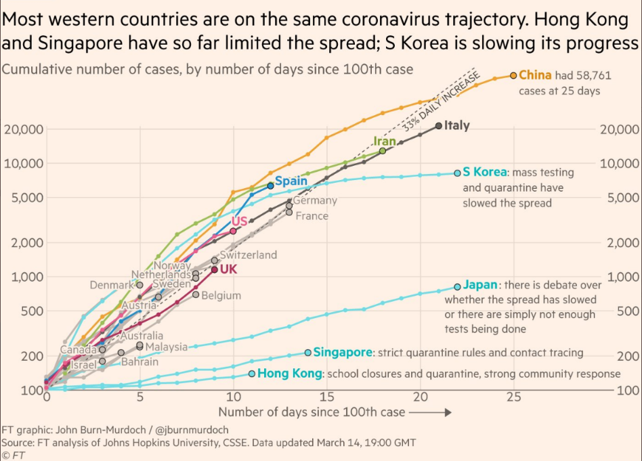

Hong Kong’s overall quarantine measure are now translating to flattening the coronavirus trajectory amongst other world centers. Recent data from John Hopkins show the trajectory of cases throughout the world as of March 14, 2020. Sadly, a heavy-handed approach seems to yield the best results. TRACEsafe CTO Dennis Kwan says, “The system is less invasive than what is being implemented in some countries such as Israel, which has turned to anti-terror technology to counter coronavirus.”

According to Al-Monitor, “Israel’s government approved on March 15 emergency regulations that would enable the Shin Bet to perform mass surveillance of phones belonging to Israelis who contracted COVID-19. These measures are not designed to monitor quarantined people but to retroactively track the movements of those found to be carriers of the novel coronavirus in order to see with whom they interacted in the 14 days before they were diagnosed. Subsequently, people who were in contact with persons diagnosed with COVID-19 will receive SMS messages instructing them to enter home quarantine.”

Alternatively, the TRACEsafe system uses a permission-based system, whereby the user is asked to allow access to their location via their phone’s GPS. Undoubtedly, the use of GPS enabled monitoring systems brings up a many questions around privacy, cost and implementation logistics, but as the virus continues its spreads world-wide, this type of technology may be a good compromise in hot-spot areas such as what Wuhan has become. Governments are getting more and more serious as this disease progresses. Already there is “coronavirus” hotel in Washington’s King County for those can not quarantine at home.

With more preventative measures in store around the globe, TRACEsafe and its parent BCX.C may be one of the few companies that see its valuation rise at the height of this unfortunate crisis.

Knox Henderson is a journalist and capital markets communications consultant. He has advised for a broad range of small cap companies in the resource, life sciences and technology sectors for more than 25 years.

Disclosure: 1) Knox Henderson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: Blockchain Holdings Inc. My company has a financial relationship with the following companies mentioned in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with Blockchain Holdings. Please click here for more information. Within the last six months, an affiliate of Streetwise Reports has disseminated information about the private placement of the following companies mentioned in this article: Blockchain Holdings. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Blockchain Holdings Ltd., a company mentioned in this article.

Rick Rule of Sprott USA and Maurice Jackson of Proven and Probable explore the effects of coronavirus on the precious metals markets and the best ways to invest in a recession.

Maurice Jackson: Today, we will find out if there is a crisis response for your investment portfolio. Joining us for a conversation is legendary investor Rick Rule of Sprott USA.

Rick Rule: Maurice, thank you so much for having me on. These are really interesting times, and it’s fun to address your audience in times like these.

Maurice Jackson: Sir, it is an absolute privilege to have you on our program during these extreme global market conditions. Speculators want to find out what you’re doing as a crisis response and what actions they may take on their portfolio under these current market conditions. From your perspective as one of the most highly regarded credit analysts in the world, was this financial collapse inevitable?

Rick Rule: I believe it was. I think what is more interesting than the pin, the pin being the virus, was the balloon. I really believe that the balloon is a function of various policy decisions and decisions that people, individually and as a society, made. I’m not belittling, by the way, the virus. I think that the rapid spread of the virus and the fact that there is, at present, no cure per se for the virusthat what you do is support the patient until the patient heals themselfmeans that there will be circumstances where the number of patients that require care exceeds society’s current ability to provide that care. So, I’m not belittling the impact of the trigger or the virus.

What I would point out, however, was that the virus was the pin, and debt and the lack of savings, a lack of equity, was, in fact, the balloon. What we’re into in an economic sense right now is a classic liquidity squeeze, a classic circumstance where trust between individuals, trust between individuals and their government, trust between banks has all eroded. Everyone is holding cash. Anything that has a bid is being sold, not necessarily by the investor but, as often as not, by the margin clerk where margin is unwinding.

Among gold investors, the lack of near-term response to go buy gold in the event of a crisis is always bewildering, because everybody buys gold in anticipation of the fact that gold will respond. First of all, gold has done its job. It hasn’t held all of its value, but it’s held a lot of value, and the fact is that gold has been sold to meet margin calls, which means for its owners, gold did the job. It provided the liquidity that enabled investors to hold on to some of their portfolio. That bid was there to hit while other bids weren’t hit, but more importantly for gold investors and gold stock investors, the circumstance that causes the gold price to go up is not the crisis itself, but rather the policy response to the crisis.

In every circumstance, governments around the world are responding to the lack of liquidity, the lack of trust and the economic dislocation caused by the coronavirus to increase liquiditythat is, to pump more currency into the markets. Understand what this is. The currency isn’t backed by anything. What the governments are doing with quantitative easing and liquidity operations, with overnight operations, is really truly counterfeiting.

The second thing that they’re doing, of course, is that they are lowering the interest rate. In the case of the United States, 10-year treasury now to zero. So, if we think about the combined response of increasing the stock of currency unbacked by anything while simultaneously reducing the compensation to savers on borrowing, what we are doing is guaranteeing that people who save for future consumption in conventional instrumentsU.S. 10-year treasuries and things like thatare absolutely guaranteed to enjoy lower purchasing power in the future than they enjoy today. That set of circumstances historically has always favored gold.

So, my suggestion to people is that the near-term performance of gold has been good. The intermediate and longer-term performance of gold should be very good. Notice that I said should be, because predictions often tell you more about the predictor than the future, and while everyone wants certainty, the only certainty that exists is that there is no certainty. We exist in probability. But if you think about gold’s response over time to circumstances where officially sanctioned liquiditythat is, government debt and things like thatare questioned, gold has always done well in those times. I would expect gold to do well in those times today.

My own suspicion is that the gold stocks will continue to suffer relative to gold, but my belief is that ultimately, the gold stocks will do well relative to other stocks, and even relative to gold itself. If one remembers the period of time 20082010that financial crisisyou will see immediately after the crisis that the gold price fell off. Then, the gold price recovered as a consequence of policy response. Then, the price of gold equities really took off as a consequence of the gold price.

In this circumstance, it is my suspicion that past will be prologue, and I think that your subscribers and our clients should look at their portfolios in that same vein. Sorry for the long answer, Maurice, but I’ve been answering this question all weekend so it’s fresher on my mind.

Maurice Jackson: Well, you’re speaking my language, and you’ve covered all the bases of what I actually want to cover, but I’ll ask a couple more questions here, because these are questions that we received, of course, from shared clients and subscribers. What are the Fed’s actions indicating to you? Second, are they enough? Is this finally the collapse that we’ve heard for a number of years? Is this finally going to come to fruition?

Rick Rule: Well, I think it depends on how you define a collapse. I don’t think that we’re going to have a circumstance where faith in the U.S. currency and U.S. institutions goes away. I don’t think we’re going to see the end of the dollar. I don’t think we’ll see the end of the Fed. I don’t think we’re going to see the end of the U.S. economy. It would not surprise me to have a legitimate debt crisis in this country. It would not surprise me to see a circumstance where major equity markets ended up being down by 50%. None of those things would surprise me.

The truth is, and this is hard for people to understand, a bear market doesn’t cause real wealth to disappear. The fact that the price of your home falls from, I don’t know, $700,000 to $500,000, doesn’t make the house less livable. The brick and mortar, the real estate don’t disappear, but sometimes they change hands. While that is unpleasant for the person whose hands the asset slipped from, over time, it’s not unpleasant for the person to whom those assets were accrued.

This is a period of time where you have to manage your emotions and you have to manage your balance sheet. We’ve discussed many times, Maurice, in these interviews that a different phrase for bear market is sale. These are sales. It doesn’t mean that the prices can’t go lower. It doesn’t mean that you go all in in this circumstance. What it means is that you look for circumstances where your estimation of the reward is much greater than your estimation of the risk, and where you personally can afford the risk that you were taking. I’m nibbling in this market now, Maurice, but I intend to be gobbling in the next while.

Maurice Jackson: This reminds me of our last conversation we had. To my disappointmentand I take full responsibilityit’s been nine months, but we last talked about courage and conviction, and how fitting that is for this moment right here, right now.

Rick Rule: Agreed. Absolutely agreed.

Maurice Jackson: I also think back to your recent interview with Albert Lu of Sprott Media. An event that causes panic that is other than permanent is an opportunity. I couldn’t have stated that any more perfectly, and I don’t even know if you can expand on it any further than what you’ve already have, but it just makes so much sense, and it has so much clarity that if someone has been listening to our interviews, they should be prepared for opportunities that are generational here. Literally speaking, generational lifestyle changes are ahead of you.

So, we’ve talked about the natural resource spacein general, gold stocksbut are there any other sectors within the natural resource space that kind of have your attention as a shopping list item that you’re looking at?

Rick Rule: The answer to that is yes, Maurice, and that merits a brief explanation. My own outlook, four or five weeks ago, was that in natural resource commodities other than precious metals, we were in for a long, slow, grinding bear marketthat the price of those metals and materials was dependent on demand, and demand was going to begin to be constrained because we’d been in a 10-year economic recovery. That recovery itself was more driven by low interest rates than anything else.

What I think will happen now is that the economic decline will be much more precipitous rather than the unwinding of a recovery that would normally take place over two or three or four years, a long, slow, grinding retreat. I think we’re going to have a hard recession, and I think the hard recession will do all of the damage to commodities that I expected to happen over three or four years in three or four months.

It would not surprise me; I’m not saying it’s going to happen. This is not a forecast. It would not surprise me to see the copper price go below $2. It would not surprise me to see the oil price go to $20. It would not surprise me to see the uranium price go lower. It would not surprise me to see a whole range of commodity prices that I had expected to decline gradually, decline rapidly. That’s bad news for those who hold the stocks like myself, some of them.

Now, the good news is that I would expect the recovery to begin to occur, not that we will feel it, but I would expect the recovery to occur this year rather than in 2023, 2024. I think the materials tradethat is, I think the time to buy the oil stocks, as an example, the big base metal stocksmay be the fourth quarter of this year or the first quarter of next year. That doesn’t mean that there won’t be individual opportunities in industrial materials that get so oversold this year that people with a long-term perspective shouldn’t buy them. It just means that the buying opportunities that I see today in the better gold equities will likely appear in the raw materials sector Q4/2000 or Q1/2021.

Maurice Jackson: Let’s take this conversation now back to the physical precious metals, if I may. I’m a licensed representative from Miles Franklin Precious Metals Investments, and I can tell you over the last couple of weeks here: huge demand on gold and silver; zeroI mean flatlineon platinum. What does that tell you about the current situation?

Rick Rule: I think a couple things. It probably tells you that people are nervous about any industrial recovery. Platinum is viewed in the United States as an industrial material rather than a precious metal. Were you, Maurice, a retail physical dealer in Japan or Korea or China, you would be feeling substantial demand for platinum investment products, but culturally, that isn’t the way that Americans respond. Americans look at platinum as a component in catalytic conversion. Americans, probably rightly, are expecting lower auto sales this year and next year and, as a consequence, aren’t buying platinum.

Similarly, I think the decoupling of gold and silver tells you that this market, in particular, is a fear-driven market. Gold responds to fear. Silver responds to greed. The people who are buying silverexcept for people who are buying junk silver because they think they might need it for day-to-day liquiditythe people who are buying silver are buying silver because they believe that after gold moves, silver will move, and silver will move further. There is less greed buying, less silver buying in this market, than there is gold buying. What’s driving this market right now is fear, and probably not misplaced fear.

Maurice Jackson: Just for clarification, because you introduced the value proposition to me regarding the platinum and palladium group elements here, as well as rhodium. . .so is platinum on your shopping list, or you’re not a buyer right now?

Rick Rule: Platinum is on my shopping list. I have a reasonable proxy in physical platinum, in the Sprott Physical Platinum and Palladium Trust. I should note parenthetically that at my ageI’m 67it’s simply easier for me to buy physical precious metals on the New York Stock Exchange through the Sprott products. I don’t discourage physical ownership; in fact, I encourage physical ownership. But for me, it’s just easier to buy the stuff and sell the stuff online in an account, and I like the tax advantages of the Sprott product.

Were I younger and more inclined to take physical delivery and store it in a safe deposit box, I would likely be a platinum buyer now. The reason for that is that the utility of platinum is so extraordinary. The amount of platinum that it takes to deliver the air quality that we enjoy today relative to the cost of the vehicle that that platinum enables the sale of is incredible. At today’s platinum prices, it takes about a $100 or $125 worth of platinum in catalytic converter to sell a $40,000 car. Were the price of platinum to double, it wouldn’t impact the price of the vehicle whatsoever.

Also, the disparity in price between platinum and palladium means that people are investing like crazy in fabrication technology that will allow us over timeand by time, I mean two to five yearsto begin to substitute platinum for palladium in many fabrication applications, but particularly in gasoline-powered internal combustion engines. So, I think that the price disparity between platinum and palladium will begin to close. I don’t expect this to happen until the very real fears associated with the economic impact of the coronavirus fade.

In other words, don’t be looking for a six-month response in your platinum trade, but the truth is that almost all of the people who are [reading] today will be spending money five years from now, 10 years from now, and 15 years from now. Their portfolio response over the five-year term, while it doesn’t seem important today, will be very important over the course of their lifetime. In that circumstance, making investments that take into account longer time frames is always critical, and platinum fits very well in that thesis.

Maurice Jackson: Unfortunately or fortunately, I think you’re probably aware of this, there was an explosion recently at the Anglo American platinum plant there in South Africa.

Rick Rule: Correct.

Maurice Jackson: So, that adds to the value proposition. By the way, you referenced the Sprott Physical Platinum Palladium Trust. The symbol for that is SPPP. That is a proxy; what that means, ladies and gentlemen, is you actually have the opportunity, if you had enough of a position in that, you could actually receive physical delivery, which is unique in and of itself because other precious metals exchange-traded funds (ETFs) do not allow you to take possession in kind, meaning physical possession. Rick, if you wanted to expand on that further, please jump in.

Rick Rule: The Sprott products, differently than ETFs, always have physical metal representing the investments that the shareholders have. In the case of our gold and silver products, as an example, that metalthe physical metalis stored at the Royal Canadian Mint. The ETFs, which must respond every day to inflows and outflows of capital, often, for some portion of their portfolio, hold delivery receipts or deposit receipts, which means that for some fraction of the overall portfolios in a real liquidity crisis, rather than having physical metals, you would have physical metals and unsecured credits to financial institutionsthat is, their promises to pay. While it would take a real extraordinary circumstance for that to be a problem, if you are the type of investor that buys gold and silver so that you won’t have problems, that’s something to consider.

Maurice Jackson: All right. In closing, sir, what keeps you up at night that we don’t know about?

Rick Rule: There’s a lot that keeps me up at night, Maurice. When people panic, they ask their government to do something, and I’m terrified that my government will do something. The circumstances that we find ourselves in today cannot be cured by government. They were caused by government. My hope is that all of your [readers] read a wonderful book by Nassim Taleb about being anti-fragile, and understand that the way out of this circumstance is for everyone individually to look after himself and herself and their families and their friends and their communities. Build strength yourself. By strengthening each of ourselves as individuals and families, we strengthen our society organically. The circumstance that we find ourselves in can’t be solved by a policy response. It’s a consequence of policy responses. Don’t be looking to the collective to make you strong. Make yourself strong. Make your family strong, and the collective will take care of itself.

What keeps me awake at night is the specter of increased government interference in private affairs. The fact that people have been trained that there is a Fed put, that Big Brother will take care of them rather than Big Brother will victimize them, that’s what keeps me awake at night.

Maurice Jackson: Last question. What did I forget to ask?

Rick Rule: I don’t think much. One thing that I would say is that people who think like you think and I think, Mauricepeople who are nervous about the ongoing purchasing power of the U.S. dollar[may] decide as a consequence of that not to have any dollars. Big mistake in the short term. Maintain liquidity, including U.S. dollar liquidity. The fact that your purchasing power will decline by 3% or 4% annually compounded does not mean that you can afford not to have dollars. Having liquidity gives you the cash and the courage to take advantage of hard times rather than to be taken advantage of by hard times.

Repeat: Despite the fact that you are losing purchasing power holding dollars, hold some dollars. You will need liquidity to get through this next patch comfortably. Gold and silver are liquidity, but they’re not the only form of liquidity. They are volatile liquidity. In addition to holding physical precious metals, hold U.S. dollar liquidity.

Maurice Jackson: Rick, I was dumb enough to listen to those words of instruction you provided about 10 years ago on one of your many interviews, and it has positioned me right here, right now to take advantage of opportunities that are presenting themselves. So, thank you for those words of wisdom. Rick, in the past, you’ve been extremely generous to us. May I ask, does Sprott USA still provide a free portfolio ranking?

Rick Rule: Yeah. There’s no better time to avail yourself of this service either. I personally will review every precious metal portfolio submitted to me. This will not be investment advice because I don’t know the person reading this interview. I don’t know what will work for them. What I will do is review every company that I am familiar with. I will rank them on a scale of one to 10, one being best; 10 being worst. I will provide comments on the companies where that is appropriate.

All that the subscriber need do is e-mail me their portfolio, both names and symbols in text. Right now, our IT people won’t let me open attachments for fear of viruses and my own technological incompetence. So, names and symbols in text. As an added bonus, I will include in my response a chart of the Barron’s Gold Mining Index, which will show you just how cheap gold mining companies are in the historical context, and also a hundred-year commodity chart.

So, email those portfolios to me, names and symbols in text to [email protected]. By the way, we’re being buried in requests, so please be patient. It could take us a 10 days or two weeks to get these responses back to readers.

Maurice Jackson: For our readers, please make sure that you put in the subject line, Proven and Probable. Sir, for someone listening that wants to get more information on Sprott USA, please share the contact details.

Rick Rule: I think the best way to do it is to go to our website, www.sprottglobal.com. I would also urge anybody who is interested in our general point of view to go to Sprott Media, www.sprottusmedia.com, or look up our playlist on YouTube. All useful additions to your Proven and Probable subscription.

Maurice Jackson: They certainly are, and that’s Albert Lu spearheading their Sprott Media. Before you make your next bullion purchase, make sure you call me. I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio from physical delivery, offshore depositories, precious metal IRAs and private blockchain distributed ledger technology. Call me directly at (855) 505-1900, or you may e-mail [email protected].

Finally, please subscribe to www.provenandprobable.com, where we provide mining insights and bullion sales. Subscription is free. Rick Rule of Sprott USA, thank you for joining us today on Proven and Probable.

Rick Rule: Always a pleasure, Maurice. Thank you.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Statements and opinions expressed are the opinions of Maurice Jackson and not of Streetwise Reports or its officers. Maurice Jackson is wholly responsible for the validity of the statements. Streetwise Reports was not involved in any aspect of the article preparation. Maurice Jackson was not paid by Streetwise Reports LLC for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. 2) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 3) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

The leverage Methanex Corp. could use to still pay its dividend in a low price environment is discussed in a BMO Capital Markets report.

In a March 17 research note, BMO Capital Markets analyst Joel Jackson reported that Methanex Corp. (MEOH:NASDAQ; MX:TSX; METHANEX:SSE) is an attractive investment opportunity given that methanol is resilient and the company could defer completion of its G3 plant.

Jackson noted that Methanex is expected to make an announcement before or at its annual meeting in late April about a potential G3 delay. That move would ease balance sheet pressure more than a partial divestment of its Egypt stake, a logistics asset sale and leaseback, and/or a receivables sale would.

A G3 deferral for two years would result in roughly $1.2 billion left to spend after 2019, Jackson indicated. This assumes a minimal, incremental G3 capex spend as of Q2/10, about $25 million in 2021 for care and maintenance along with $125 million per year in companywide maintenance capex.

Yet, were Vancouver-based Methanex not to defer G3 but, instead, keep Titan idle until 2021 and Chile IV idle until Q4/20, Jackson indicated, the company still would have enough free cash flow to cover the 12% dividend, even in scenarios in which methanol prices recovered slowly.

Jackson provided two such low price scenarios in which Methanex could still pay its $110115 million dividend. It could do so at a methanol price of $250 per ton over the next few quarters and increasing to $285 per ton in 2021. That would result in free cash flow of about $200 million and leverage by year-end 2021 of about 3.5x.

The company could even pay the dividend if the methanol price stayed constant at $250 per ton. In that case, the free cash flow yield would be $100130 million, but 2020 leverage would be higher, at about 55.5x.

Jackson also highlighted that the methanol price is resilient and historically bounced back rapidly from lows. He cited the period following Q1/ to Q3/16 in which the price quickly rebounded to about $400 per ton from about $230 per ton.

The analyst concluded that Methanex’s “share price seems too punitive as G3 deferral is a lever the company can pull to calm leverage concerns.”

BMO maintained its Outperform rating on Methanex but reduced its target price on the company to $20 per share from $60. The current share price is about $10.47.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from BMO Capital Markets, Methanex, March 17, 2020

IMPORTANT DISCLOSURES

Analyst’s Certification I, Joel Jackson, hereby certify that the views expressed in this report accurately reflect my personal views about the subject securities or issuers. I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this report.

Analysts who prepared this report are compensated based upon (among other factors) the overall profitability of BMO Capital Markets and their affiliates, which includes the overall profitability of investment banking services. Compensation for research is based on effectiveness in generating new ideas and in communication of ideas to clients, performance of recommendations, accuracy of earnings estimates, and service to clients.

Analysts employed by BMO Nesbitt Burns Inc. and/or BMO Capital Markets Limited are not registered as research analysts with FINRA. These analysts may not be associated persons of BMO Capital Markets Corp. and therefore may not be subject to the FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Company Specific Disclosures

Disclosure 1: BMO Capital Markets has undertaken an underwriting liability with respect to Methanex within the past 12 months.

Disclosure 2: BMO Capital Markets has provided investment banking services with respect to Methanex within the past 12 months.

Disclosure 3: BMO Capital Markets has managed or co-managed a public offering of securities with respect to Methanex within the past 12 months.

Disclosure 4: BMO Capital Markets or an affiliate has received compensation for investment banking services from Methanex within the past 12 months.

Disclosure 5: BMO Capital Markets or an affiliate received compensation for products or services other than investment banking services within the past 12 months from Methanex.

Disclosure 6A: Methanex is a client (or was a client) of BMO Nesbitt Burns Inc., BMO Capital Markets Corp., BMO Capital Markets Limited or an affiliate within the past 12 months: A) Investment Banking Services

Disclosure 6C: Methanex is a client (or was a client) of BMO Nesbitt Burns Inc., BMO Capital Markets Corp., BMO Capital Markets Limited or an affiliate within the past 12 months: C) Non-Securities Related Services.

Disclosure 9B: BMO Capital Markets makes a market in Methanex in United States.

For Important Disclosures on the stocks discussed in this report, please click here.

As for Q4/19, Fortuna Silver’s adjusted earnings per share (EPS) and cash flow per share (CFPS) were a beat, Chiu relayed. EPS was $0.07 and CFPS was $0.17, higher than consensus’ $0.06 and $0.11 projections, respectively, and CIBC’s estimates.

Chiu highlighted that the Canadian company’s Q4/19 production from its San Jose mine in Mexico and its Caylloma mine in Peru was steady and cash flow generating. It amounted to 2,250,000 ounces (2.25 Moz) at a cash cost of $8.27 per ounce and an all-in sustaining cost of $12.58 per ounce. Both costs were 10% and 5% better, respectively, than in Q3/19.

Fortuna’s 2020 production guidance remains unchanged at 7.58.3 Moz of silver and 101,000125,000 ounces of gold (101125 Koz), with 6080 Koz coming from Lindero.

Chiu noted that after the recent announcement that the first pour at Lindero would be delayed to sometime in Q2/20, Fortuna increased total capex for Lindero to about $320 million from $298 million and raised preproduction working capital needs to $40 million from $25 million. “Fortuna should be able to meet the remaining capital requirements at Lindero until commercial production is announced, expected in Q3/20,” Chiu commented.

CIBC kept its Neutral rating but decreased its target price on Fortuna Silver to CA$4.75 per share from CA$5.75. The stock is currently trading at around CA$3.46 per share.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

Disclosures from CIBC, Fortuna Silver Mines Inc., Earnings Update, March 15, 2020

Analyst Certification: Each CIBC World Markets Corp./Inc. research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein accurately reflect such research analyst’s personal views about the company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets Corp./Inc. are compensated from revenues generated by various CIBC World Markets Corp./Inc. businesses, including the CIBC World Markets Investment Banking Department. Research analysts do not receive compensation based upon revenues from specific investment banking transactions. CIBC World Markets Corp./Inc. generally prohibits any research analyst and any member of his or her household from executing trades in the securities of a company that such research analyst covers. Additionally, CIBC World Markets Corp./Inc. generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report, CIBC World Markets Corp./Inc. may have a long position of less than 1% or a short position or deal as principal in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Fortuna Silver Mines Inc. (FVI.TO)

2a These companies are clients for which a CIBC World Markets company has performed investment banking services in the past 12 months: Fortuna Silver Mines Inc. 2c CIBC World Markets Inc. has managed or co-managed a public offering of securities for these companies in the past 12 months: Fortuna Silver Mines Inc. 2e CIBC World Markets Inc. has received compensation for investment banking services from these companies in the past 12 months: Fortuna Silver Mines Inc. 2g CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services from these companies in the next 3 months: Fortuna Silver Mines Inc.

For important disclosure footnotes for companies mentioned in this report that are covered by CIBC World Markets Inc., click here: Disclaimers & Disclosures.

Delighted to have you back to provide us with a number of updates regarding the value proposition of Calibre Mining, which is focused on execution, opportunity and discovery. Before we begin, Mr. King, please introduce Calibre Mining and the opportunity the company presents to the market.

Ryan King: Calibre Mining is a multi-asset gold producer focused on execution and building sustainable value for our shareholders, communities we operate in, and all stakeholders. This past year Calibre has gone through a very significant transaction with B2Gold Corp. (BTG:NYSE; BTO:TSX; B2G:NSX). Prior to this transaction we were, and still are, an exploration company, but we were predominantly an exploration company focused on some assets in Nicaragua called the Borosi Triangle, or Golden Triangle, up in the northeast section of Nicaragua. We went through a transaction where we acquired two producing gold mines and one development-stage project in Nicaragua with B2Gold. We raised a little over $100 million dollars to complete that transaction. Our team is the ex-Newmarket gold team, which successfully discovered very high-grade gold mineralization at the Fosterville Mine in Australia, and then went on to merge Newmarket Gold with Kirkland Lake Gold Inc. (KL:TSX; KL:NYSE).

We see another excellent geological opportunity here in Nicaragua. Our focus is, as you said, on execution, opportunity, and discovery. Calibre believes that we’ve got the right ingredients to execute our value proposition successfully in Nicaragua. We’re very excited to be a gold producer and doing a lot of exploration work around those assets.

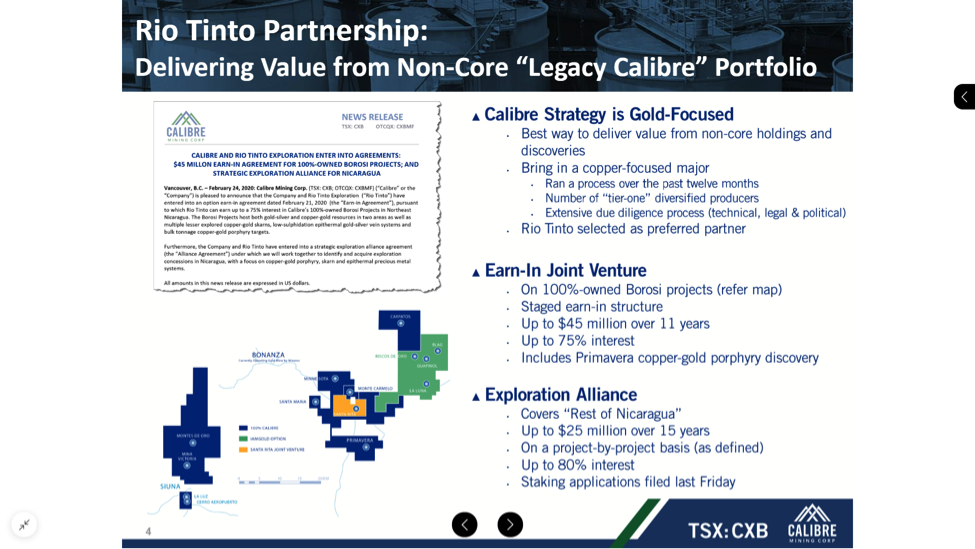

Maurice Jackson: We last spoke in December of 2018. Calibre Mining has exceeded all of those benchmarks for success from that interview. We’re going to delve into those shortly. But before we get into that, let’s discuss the press release that has shareholders giving a standing ovation to management. That is the strategic alliance with Calibre Mining and Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK), entering into a $45 million earning agreement (press release). Sir, please provide us with the details of this transaction.

Ryan King: Prior to announcing this deal with Rio Tinto, they had not been in the country before. This is what required an NCE, a new country entry, for Rio Tinto. This spawned back to 2018 actually, when we first started to have discussions with them about the geological potential at some of the assets that we have in those Borosi exploration projects up in the northeast corner, which were the initial assets that brought us to Nicaragua.

It was way back in 2013 when we discovered a copper gold porphyry system. At the time it didn’t get big enough to be a deposit or a mine, but we continued to do work on it. We continued to advance it. We weren’t able to do drilling. We did geochemical work. We did some geophysical work and identified a number of additional targets. What happened was that when we started to introduce the opportunity to Rio Tinto, they brought some people down to look at it and felt that it was a good geological opportunity. Keep mind, Rio Tinto only seeks to be aligned with significant size deposits.

In the northeast portion, or the northern half of the country of Nicaragua, it has the type of rocksthe age of rocks, older rocksthat could have these large, porphyry type deposits. After 18 months of due diligence, not only technically but on the infrastructure in the country, political situation in the country, the geological potential in the country, Rio Tinto was given the green light to be able to proceed and go into the country and be able to do an earn-in deal with us and along with a strategic alliance with us. This is very exciting that the second largest mining company in the world has validated Nicaragua as a country that they’d like to enter into and do business in.

The deal is that on our 100%-owned Borosi concessions, which amass to about 665 square kilometers, Rio Tinto can earn up to 70% in those concessions. . .sorry, 75% of those concessions by spending US$45 million. It’s an incredible deal for our shareholders. Because keep in mind, we acquired the producing assets down in the south part of Nicaragua, La Libertad and El Limon. Our team is focused on extending mine life and drilling all around those operations. The Borosi concessions up in the north weren’t going to see a huge amount of investment this year by Calibre. This allows some additional optionality for our shareholders and new shareholders. If Rio and Calibre decide to really spend some money there and do some drilling, I don’t know what the plans are going to be yet. Technical sessions are underway with both companies to decide on a plan.

That’s just additional optionality for our shareholders. It’s very exciting that they’ve identified this opportunity. But in addition to that, we signed this strategic alliance with Rio [for mineral concessions on a] total amount is 1.4 or 1.5 million hectares of the northern portion of Nicaragua. I think it’s close to 15% of the land mass of Nicaragua. They’re very excited. We’re very excited about this. Then, during this strategic alliance, Rio Tinto would be funding and doing generative-type work. If a project is identified in the next couple of years, they could pluck that project out of the strategic alliance and enter into another earn-in joint venture for up to $25 million and get 80% of that project.

There’s a lot of opportunity here, a lot of optionality in the portfolio, that we, as Calibre, would not have maybe focused on so much in the near term because we’re so focused on the operating assets that we have down in the southern Nicaragua. It’s a very exciting opportunity for us. I think as I mentioned, it really does validate the geological potential and it validates the country as a great place to operate.

Maurice Jackson: Truly impressive, sir. Ryan, this reminds me of our conversation back in December. You were foot stomping about the commercial and the technical expertise that the management team has. This is a great example here. But the business acumen and the geological acumenit goes further than this transaction. Let’s look back now at 2019 and discuss some additional impressive feats that Calibre Mining accomplished in the last 15 months.

Mr. King, back in July of 2019, Calibre made an accretive move joining forces would B2Gold (press release). You acquired two producing mines from El Limon and the La Libertad. Introduce us to these mines, and why is this the right move for shareholders?

Ryan King: In our first interview, when we first discussed Calibre as mentioned, we were just an exploration company with resources in the ground and partners in the country. IAMGOLD is one of our partners. Now Rio Tinto is one of our partners up in the north. As the market was back and forth with exploration companies, our team that had bought producing gold mines in a previous lifein Newmarket Gold and through cash flow, through operating cash flow, [where] we were able to fund exploration, expand mine life and make new discoverieswe felt that that was going to be the best move for Calibre shareholdersbuilding another operating, cash-flowing business.

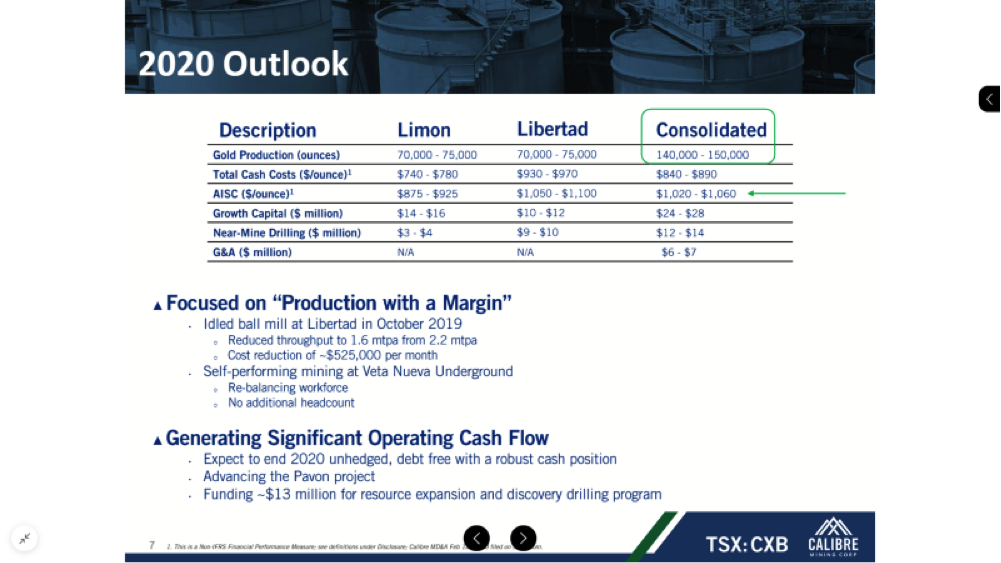

In doing so through relationships, our founders, Doug Forester, Doug Hurst, Blaine Johnson and Russell Ball, felt that the best move would be to buy, if we could, operating assets. We were able to strike a deal, a win-win deal, with B2Gold in the sense that B2Gold were focused so heavily on their Otjikoto mine, their Masbate mine and Fekola, that we were able to bring in the right team with the experience in-country. We were able to raise enough capital that we could really invest in these operations. Yet, at the same time B2 retains almost 34% equity ownership in Calibre. As you mentioned, we have joined forces with B2 on this. We think this is a fantastic opportunity for Calibre shareholders and that this year, in 2020, we will produce between 140,000 and 150,000 ounces of gold and right around $1,000 all-in-sustaining cost (AISC). It’s a great opportunity for our shareholders.

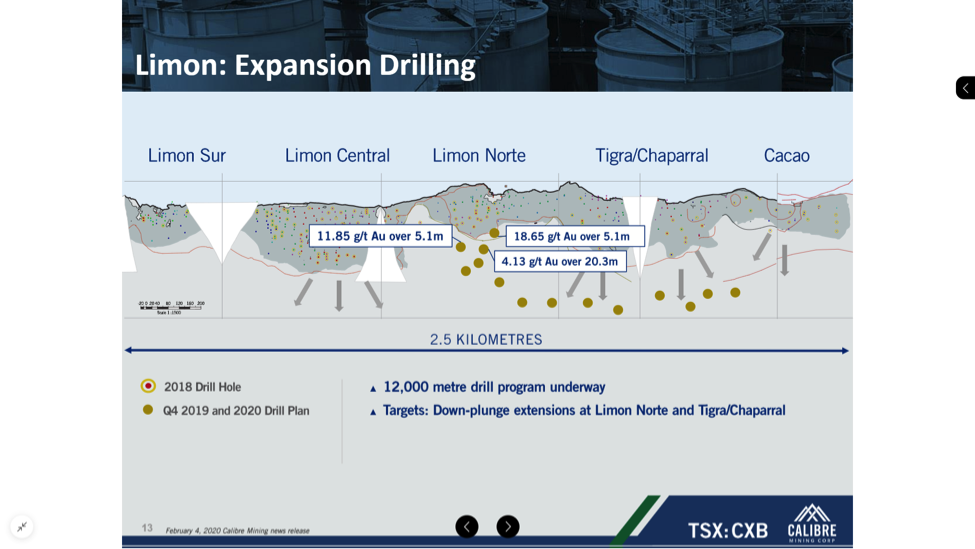

What’s equally, or even more exciting, for Calibre shareholders is the amount of drilling we plan on doing in 2020. We’ve earmarked almost 50,000 meters for drilling. That has been going very well. We started that in the fourth quarter of 2019. That’s been going very well. We’ve already had success with a new area at the La Libertad mine called Amalia in a very large concession that had never been drilled. Also at the El Limon mine, we were drilling down-plunge of current resources. And it looks like we’ll expand resources at the El Limon central and Norte deposit.

Really exciting time for Caliber. Really exciting time, I think, for the operations, as we’re seeing lots of new investment. We’ve been really welcomed into the country. We’ve met the minister of Mines and Energy. We’ve met the president. They’re very encouraged about the new investment that we’re making into these operations. Also, they really wanted to know that B2 was still involved. We have a board member at Calibre that’s from B2Gold. We have an advisory group that’s partly made up of B2Gold employees and executives. . .with their significant 34% equity ownership of the company, they are very, very much involved with us in these assets.

It’s exciting for all people involved. I think it’s a really good opportunity for all looking at the gold space. Now we’re at $1,650 gold. When we announced this deal, we were back at $1,300 gold. It’s been nice to be a part of a rising gold market environment for Calibre.

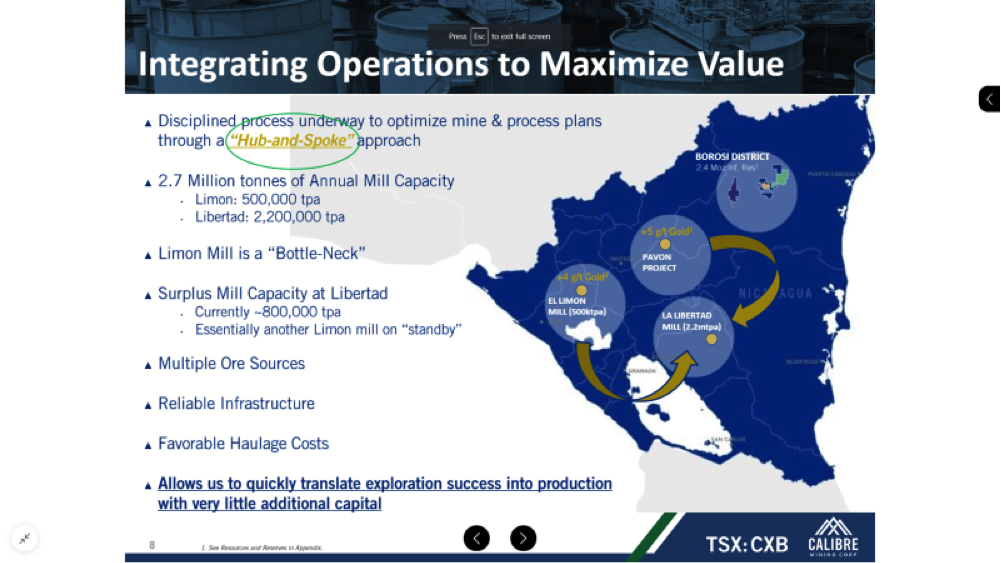

Maurice Jackson: Mr. King, let’s go back on site real quick. I want to ask you one more question before we leave there. Should expansion become successful, can the current mills meet production demand?

Ryan King: It’s a great question because one of the things that we actually did during the fourth quarter when we took over the assets was at the La Libertad operation, we idled down one of the ball mills. We felt that by doing so we could extend mine life, but also our focus is really on margin. Instead of really cranking up production, let’s focus on margin. By idling down one of these ball mills, we’re almost saving $500,000 dollars a month currently of power, reagents and liners in the mill.

The focus turned to margin so that we can accretively reinvest in the operations. One of the opportunities is all of the new targets we’ve identified that level at La Libertad. If we do have success, we could potentially, at the right time, turn that second ball mill back on at La Libertad, which would give us a total of 2.2 million tons of throughput capacity, and could therefore be the right size for the operation. We have excess capacity at La Libertad, which is a great place to be. All the capital has been sunk in the mill. It’s just about finding new opportunities, new mineralization deposits that could be put through the mill.

And, where the bigger opportunity lies is weve started to do some work in the country now. Because of the reliable infrastructure and the favorable cost structure to haul ore around the country, we can see that rather than just looking at the two mills as two standalone mills, which they are, we really look at them as integrated units now. At Libertad, the total capacity is 2.2 million tons of installed milling capacity. We’re only using 1.5 or 1.6 million tons. At El Limon, we’ve got 500,000 tons of installed capacity. What we’re really looking at now is multiple different ore sources, and then where’s the best place to haul the order around. Because we can haul around the country roughly about 200 and 250 kilometers between the two mills.

Based on the analysis we’ve done, it would cost us about a half a gram to three quarters of a gram to haul from, say, Limon to La Libertad or from Pavon, for example, a development-stage project that we’re working through, and permitting would be about a half a gram to three quarters of a gram at today’s gold prices. Quite accretive to look at this as what we call a hub-and-spoke approach.

A long-winded answer to your question is, yeah, it looks like we do have the capacity, barring a great new discovery or some resource expansion that we could really utilize the installed capacity in the country. Down the road, depending on the size of a new discovery, we could see potentially looking at a mill expansion, but we do have excess capacity and capital has been sunk. It’s pretty exciting for us there to hopefully be able to take advantage of the excess capacity in-country.

Maurice Jackson: All right. Let’s just summarize here for reader. We have Rio Tinto with a $45 million earn-in agreement. B2Gold: we have the acquisition of two producing mines. But wait a minute, there’s more. Let’s revisit September (press release). You did an impressive 102 million equity financing to advance some existing projects in the portfolio and you’re embarking on an ambitious 40,000-meter diamond core drill program. Please share on which projects there will be drilling, and can you share with us about the genetic model on the target zones?

Ryan King: You’re absolutely right. We acquired the two mines and then we very quickly identified a number of resource expansion and discovery drilling opportunities around those operations. Part of the reason we raised a little bit excess of what was required to do the deal with B2 was so that we could reinvest in the operations, so that we could see a real significant bump up of drilling and optimization at the operations. These are what’s known as low sulfidation epithermal vein systemsbetween 5 and 20 meters of width, generally coming right to surface based on what we’ve seen, and anywhere from 2 to upwards of 20 grams per ton, [which] we’ve seen in some of the drill results over the years historically and even some new ones.

For example, we started drilling at the high-grade El Limon Central and Norte vein structure that is two and a half kilometers long. We only drilled four holes in the fourth quarter of 2019, but three out of the four holes actually intersected very good widths and gradefor example, almost 12 grams per ton gold over 5 meters. This is just below inferred resources. It looks like resources will be expanding. We drilled 18.7 grams per ton gold over 5 meters. Then 4.2 grams over 20 meters. This was down-plunge of current resources at this new high-grade open pit that we’re currently operating at the El Limon mine. It looks like a really good opportunity to expand resources. We’re drilling again down plunge of the known zones there as well.

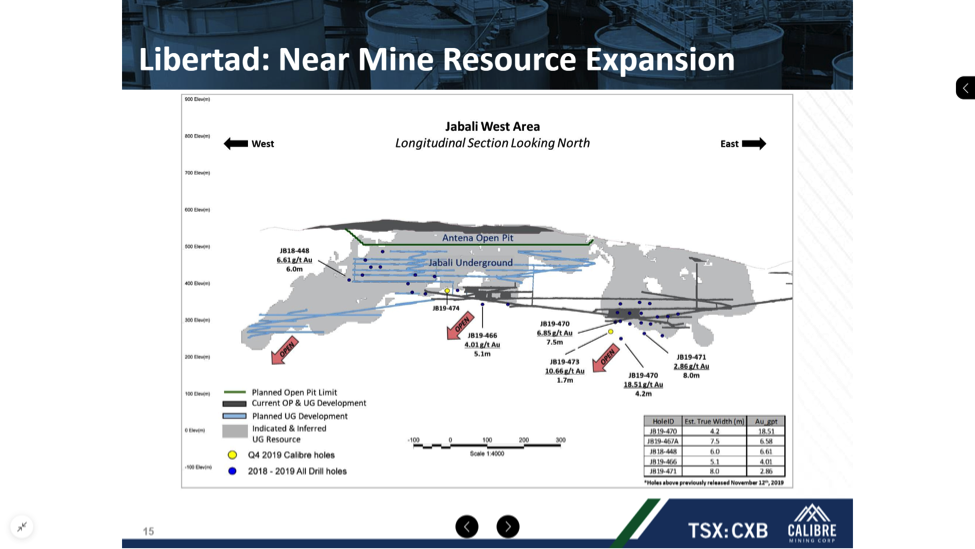

Over at the La Libertad operation, over 1.7 million ounces of gold has been produced in and around the La Libertad proper concession, which is roughly 200 square kilometers. We’ve got three drills turning on a number of targets there, some of which have smaller resources that look like they have expansion potential, and some are in new areas that have great geochemistry anomalies that not been drilled.

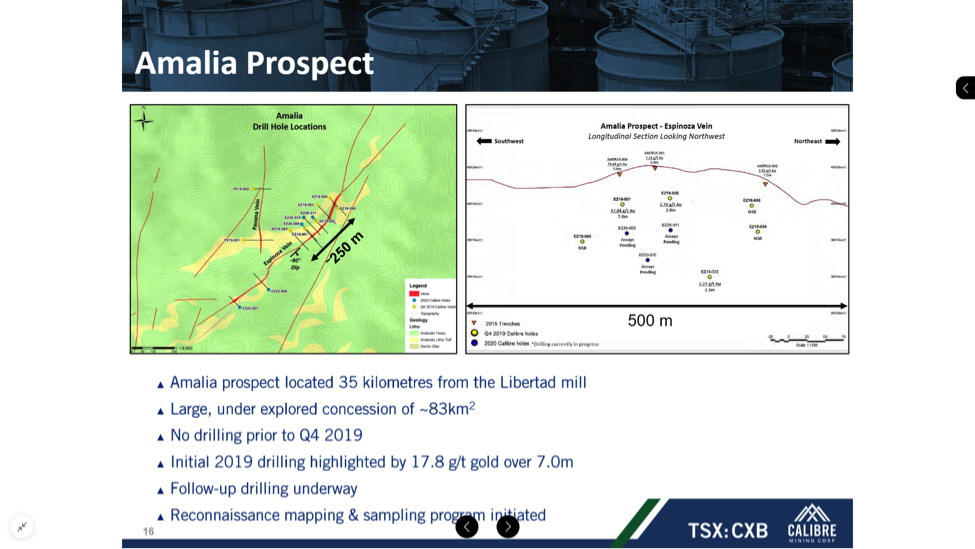

Then [there is] a new area which we call Amalia. Amalia had been identified by B2Gold. Some great trench results; 6.7 meters of 7 grams, 13 meters of 4.7 grams, so about a kilometer-long geochemistry signature. We went in, and in the fourth quarter of 2019 drilled some holes, and we got some excellent results and it looks like we’ve identified a new area. One of the drill intercepts with 17.8 grams over 7 meters, only 45 meters vertical from surface.

Keep in mind, this had never been drilled before. There’s been no mining there. We’re in an area that’s 350 square kilometers in that mineral concession. Very exciting opportunity to maybe we’ve come into a new district or camp of these low-sulfidation veins, like the La Libertad proper. Amalia is only located 30 kilometers north of the current mill, which has as mentioned excess capacity. It’s a pretty exciting opportunity for us. We have a total of four drills operating at La Libertad right now. Stay tuned for future news releases and drill results.

Maurice Jackson: The value proposition for Calibre Mining just seems to continue to get better and better. Multimillion dollar question: When can the market expect to see drill results?

Ryan King: Everyone likes to get to see the drill results as they unfold. Most companies would put out drill results once, maybe twice a year for an operating company that has between 100,000 and 200,000 ounces of annual production. Because of the amount of drilling is so significant this year for Calibre, we will be putting out results every 67 weeks. I expect our next set of drill results will come from the El Limon gold mine, where we’re going to be producing 70,000 to 75,000 ounces this year. El Limon have a number of different zones. [There’s the] Limon Central Norte, 2.5-kilometer, open pit vein structure, which we’re drilling now, as well as an underground mine called Santa Pancha and Panteon, which we’re drilling as well. I suspect the next set of results will come from Santa Pancha and Panteon. That’ll probably be in the next 2-3 weeks.

Then in April, we should have some results from La Libertad, the Amalia district, as well as a couple of zones in around the La Libertad district. Lots on the go, as I’ve mentioned. We’re almost doing 50,000 meters in what we’re now calling a phase-one drill program. This could be a multiphase drill program, obviously predicated on success, but it’s a very exciting time for Calibre and all the news that that will be coming out.

Maurice Jackson: Switching gears, Ryan, what is the next unanswered question for Calibre Mining? When can we expect an answer and what will determine success?

Ryan King: A lot of people have been asking us about mergers and acquisitions, [given] the bench strength that we have in this team. Our chief executive officer [had] over 25 years at Newmont as the chief financial officer there. The founders of Calibre, the founders of Newmarket Gold, which sold for over a billion dollars to Kirkland Lake in a very successful transaction that saw Kirkland Lake go up five- or sixfold from that transaction, or even more. A lot of people [are] asking us about mergers and acquisition in a rising gold market environment. I would say that we’re always looking. We’re always looking at opportunities where we can add value for our shareholders. Where we can add accretive value, not just to get bigger, but accretive value so that we can work towards a higher share price.

But what we see in front of us right now is a really good opportunity to execute on these assets, drill a number of these targets, because the geological potential looks so good. Then look to extend mine life, make new discoveries, expand resources. That’s going to add a lot of value in our opinion for our shareholders and to this new story, this new budding story of Calibre. It’s only six months old now. I think that’s the big question we consistently get.

But the news going forward will be a lot of drill results, quarterly results, financial results. As the year unfolds at these gold prices, we should be adding cash to our balance sheet, reinvesting in the assets. We’ll hear some as the year goes on, we’re advancing this Pavan gold project, which could be another ore source for the La Libertad mill.

There’s a number of things coming out as well in the background. We’ll consistently and continuously look at mergers and acquisitions that could potentially add value. But first and foremost, it’s execution. It’s drilling and building mine life at these operations to be able to see the most amount of value that we can for these assets in the short period of time. A lot’s going on across the board, Maurice.

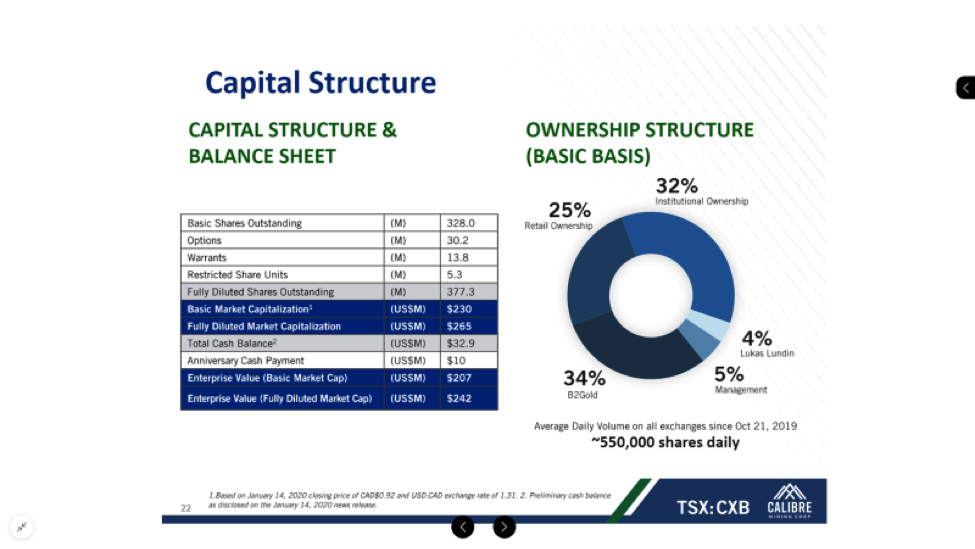

Maurice Jackson: Speaking of the shareholders, can you please provide us with an update on the capital structure of Calibre Mining?

Ryan King: I think today, at about CA$0.80, our market capitalization is around CA$240250 million. We essentially have no debt. We’ve got one remaining payment of $10 million to B2Gold, which is in October of 2020. We trade on average between 500,000 to 750,000 shares a day. We have just a little over or just a little under US$33 million in the bank. Lots of capital to reinvest in these operations.

As mentioned, our guidance for the year is 140,000 to 150,000 ounces at roughly $1,000 all-in sustaining cost, plus, some investment we’re putting in the operations. I think it’s between $20 and $25 million and about $15 million in drilling for the almost 50,000 meters of drilling that we’ll do in this phase one program.

About CA$240 million? What is that about? Just a little under US$200 million market cap for a company of our size I think demonstrates a good value proposition. The management insiders own just a little under 6%. A well-known resource investor, Lukas Lundin, owns a little under 5%. We’ve got about 35% institutionally held. B2Gold, of course, owns the 34% ownership in Calibre. That sort of breaks down the capital structure of the company, and the balance sheet in a sense.

Maurice Jackson: In closing, sir, what keeps you up at night that we don’t know about?

Ryan King: [For] any resource company that is developing operations, first and foremost, the most important thing is your social license around the operations in any place where you operate. We have a very good social license around the mines. We have good relationships with our communities. We do a lot of excellent environmental, social community work. We have a great team in Managua that does all of that.