The government and central bank response to pandemic fears has ignited retail demand for precious metals like never before, and this special issue tells you all about what’s been happening.

Under these extraordinary circumstances, I’m proud of – and deeply grateful to – our dedicated Money Metals employees who have been able to keep key items in stock and ship orders faster than ALL our industry peers.

Meanwhile, I’m pleased to announce the launch of our Vault Gold and Vault Silver storage offerings – absolutely the best way to get low-cost gold and silver ounces in the current period of high premiums and shortages. You can read all about it on page 7 of your free Money Metals Insider newsletter.

Also, a quick reminder, not only does Money Metals offer super competitive pricing when you want to BUY, but we are also – without a doubt – the #1 place in the country to SELL, STORE, or even GIVE YOU A CASH LOAN AGAINST your precious metals.

Here are the highlights from your free Money Metals Insider newsletter:

So download the PDF of this fantastic free newsletter right now – and pass it around to your friends! It’s another free benefit for those who have signed up for the Money Metals email list.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Money manager Adrian Day discusses a general approach to the market, as well as recent developments at several companies on his list, including some buy recommendations, despite being overall cautious.

Most markets have enjoyed a meaningful rally off their lows of three to four weeks ago. The S&P is up nearly 30%, with the Business Development Companies up 50% and more, while global markets have also rallied, though typically less; the XAU index of gold stocks has risen over 40%. It is not unusual to see an initial strong bounce after sharp market declines, but what often follows is a retreat to the lowsperhaps new lowswith a more selective and more delayed recovery after that. When stocks hit their lows again, we should avoid the temptation to immediately load up indiscriminately expecting another sharp rally.

Looks for sales in you added last month

Because of these rallies, we would be buying very little right now, waiting for a pullback to start buying again. (See “Top Buys” near the end of this letter.) Indeed, we would look for possible sells, but so much depends on individual circumstances. If, for example, you managed to buy more Ares Capital Corp. (ARCC:NASDAQ) at a good price, maybe under $9, you could sell some of that additional purchase for a better-than 30% gain. I am most definitely not suggesting you sell all your Ares; I am just looking at possibilities depending on individual circumstances.

This general advice applies to gold stocks as well. If you doubled your position in, say, Wheaton Precious Metals Corp. (WPM:TSX; WPM:NYSE) under say, $26you had seven trading days last month to do soyou could cut back over $34. Remember, be alert to tax-loss consequences. Since any sales of add-on positions at last month’s lows will not be outside the 30-day wash-sale rule, decide whether you want to sell shares in which you have a gain and preserve any tax losses for later sales; or avoid paying tax now but give up the tax loss. (You can designate which shares you are selling; talk with your accountant if it’s a meaningful amount.)

Evrim’s royalty gets more valuable

Evrim Resources Corp. (EVM:TSX.V, 0.28) announced that First Majestic had upgraded the resource at the Ermitano Project, which Evrim discovered and subsequently sold to First Majestic in exchange for a 2% royalty. The operator announced a 345% increase in the silver-equivalent ounces, and a 15% increase in grade, for an indicated resource of 311,000 ounces of gold and 4,730,000 ounces of silver. A pre-feasibility study is expected by year-end. Production, and revenues to Evrim, are estimated to commence in early 2021.

Separately, Evrim has regained 100% of the Cerro Cascaron project after Harvest Gold completed two seasons of exploration including drilling with promising results. Much of the project remains unexplored, and Evrim will seek another partner.

Although the stock price has recently moved up, at 28 cents, the market cap is C$24 million, about the same as the cash and value of the its Ermitano royalty, so it remains undervalued. If you do not own it, Evrim is a strong buy.

Fortuna’s mines all closed down, but stock cheap

Fortuna Silver Mines Inc. (FSM:NYSE; FVI:TSX; FVI:BVL; F4S:FSE, US$2.36), like other mining companies, withdrew its production guidance for this year, following the closing of both of its operating mines, and the suspension of construction activities at its Lindero project, nearing completion in Argentina, all the result of the Covid virus. As a result, the commencement of operations and production has been pushed back again, with no new date announced.

The company is in a strong position, with $123 million cash, which includes $40 million just drawn on its credit facilities. As part of its response, the company said that senior executive compensation was being reduced.

At its current price, Fortuna is trading at only 6 times last year’s cash flow, 14 p/e, and 60% of book value. These are very low numbers for a mining company. Although clearly the impact of the shut downs in three countries on at least this quarter’s revenues will be significant, once the mines reopen and Lindero starts production, revenue will move up sharply. Fortuna is a very strong buy at this level. It traded as low as $1.80 last month, so if you already own a meaningful allocation, you might wait for an additional pullback to add to positions.

Royal well positioned to withstand closures

Royal Gold Inc. (RGLD:NASDAQ; RGL:TSX, US$107.81) said its gold and silver sales in the first quarter were in line with previous guidance, though it ended the quarter with lower inventory. Several of the mines at which Royal earns its royalties and streams have temporarily closed because of the virus, including its principal earner Mt. Milligan.

The company drew another $200 million on its credit facility, bringing to just over $300 million the amount outstanding on its $1 billion credit facility, The drawdown was a “prudent precautionary measure,” the company said. Separately, CEO William Heissenbuttel said he has complete confidence in the revised mining plan for Mt Milligan put out by owner Centerra. We are holding.

Reopening, purchase and dividend continues

Osisko Gold Royalties Ltd. (OR:TSX; OR:NYSE, CA$8.31) received good news when the Quebec government announced mines were “essential,” and many mines, including Malartic (Osisko’s largest royalty earner) and Eleonore announced plans to resume operations, the latter on a “phased” schedule. Hold.

Reservoir Capital Corp. (REO:TSX.V, 0.04) has completed the previously announced acquisition of Olocorp Nigeria, which holds shares in an operating Nigerian hydro company. The final 40% of Olocorp was purchased for Reservoir shares. Hold.

Gladstone Investment Corp. (GAIN:NASDAQ, 9.96) said it was proactively engaged with its portfolio companies, providing assistance and support as necessary. These companies have been affected by Covid and the shutdowns to various degrees, depending on sector and location. It announced the monthly dividend would remain the same as last quarter, with a special extra 9 cents per share payment in June. If these payments continue, it would equate to a 12% in the year ahead. Hold.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: Ares Capital, Evrim Resources, Gladstone Investments, Royal Gold, Osisko Gold Royalties and Altius Minerals. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: All. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Evrim Resources, Royal Gold, Osisko Gold Resources and Altius Minerals, companies mentioned in this article.

By CentralBankNews.info Iceland’s central bank joined the growing number of central banks that are engaged in asset purchases, also known as quantitative easing, saying it will begin buying Treasury bonds in the secondary market starting in May to ensure its easy monetary policy stance is transmitted to households and businesses. The Central Bank of Iceland (CBI), which has cut its key interest rates three times this year by a total of 125 basis points and eight times since May 2019 by a total of 2.75 percentage points, said it may purchase up to 150 billion krona of Treasury bonds, with the amount it intends to buy each quarter to be announced in advance. The total amount to be purchased in the second quarter may range up to 20 billion krona with the purchases focused on all nominal benchmark Icelandic krona bonds maturing in 2021, 2022, 2025 and 2031, and any new benchmark bonds that will be issued. Today’s announcement follows a decision by CBI’s monetary policy committee on March 23 – only a week after CBI last cut its rate at an unscheduled monetary policy meeting – that it would begin direct purchases of Treasury bonds in the secondary market and “will do what is needed” so its accommodative policy stance is transmitted to the economy. At that time, it said details of its decision would be announced later. Governments worldwide, including Iceland’s are sharply boosting spending and thus the issuance of government debt, to cushion the economic damage from measures to contain the coronavirus. This will tend to reduce liquidity and push Treasury yields higher, disrupting the normal transmission of easier monetary policy at a time when the central bank’s actions are amid at easing the financial conditions faced by households and businesses, CBI said in March 23.

The Central Bank of Iceland issued the following press release:

“At the beginning of May 2020, the Central Bank of Iceland will begin buying Treasury bonds in the secondary market, in accordance with the 23 March 2020 statement by the Monetary Policy Committee. The objective of the purchases is to ensure monetary policy transmission across the yield curve, so that the more accommodative monetary stance is transmitted normally to households and businesses. In this context, particular consideration is given to the market effects that the foreseeable increase in Treasury bond supply will have on monetary policy transmission.

The aim will be to keep the scale of the purchases consistent with normal market functioning. The Central Bank reserves full right to adjust amounts, frequency, and execution of the purchases so as to ensure the efficacy of the measures.

According to the above-mentioned Monetary Policy Committee decision, the Bank may purchase Treasury bonds for up to 150 b.kr. The Bank will announce in advance the maximum amount it intends to buy each quarter. The total amount to be purchased by the Bank in Q2/2020 may range up to 20 b.kr. market value.*

The purchases will focus on all nominal benchmark issues denominated in Icelandic krónur and maturing in 2021, 2022, 2025, 2028, and 2031, and any new nominal benchmark issues that may be added.

The Central Bank will purchase the bonds either by submitting bids to the Nasdaq Iceland trading system or by auction. The purchases will begin with submittal of bids to the Nasdaq Iceland trading system.

Any auctions that are held will be announced with one day’s advance notice. The announcement will specify the series and the estimated maximum amount to be purchased. Information on the general terms and conditions for auctions that may be held in connection with the Central Bank’s purchase of Treasury bonds in the secondary market can be found here.”

China may reduce raw material exports amid falling GDP

China’s GDP fell in the 1st quarter of 2020 by 6.8% in annual terms. This was the first time since 1994. Compared to the 4th quarter of 2019, the decrease was 9.8%. Chinese industrial production slid down by 8.4% in March. This is noticeably better than the forecasts (-10%) and the February figures (-13.5%). China is the main buyer of Australian coal, iron ore and non-ferrous metals. The share of Australia’s exports to the PRC is about 30%. An additional negative factor for the Australian dollar was the April meeting proceedings of the Reserve Bank of Australia, which noted the possibility of further easing of monetary policy in order to maintain the national economy and the labor market.

By CentralBankNews.info Turkey’s central bank cut its policy rate for the fourth time this year and for the 8th time since July 2019, saying the outlook for inflation is to the downside from weak domestic demand, inflationary expectations and producer prices stemming from the efforts to contain the spread of the coronavirus. The Central Bank of the Republic of Turkey (CBRT) cut its one-week deposit rate by another 100 basis points to 8.75 percent and has now cut it by 325 basis points this year and by 15.25 percentage points since July last year when it began its easing cycle after a new governor was installed. As other central banks worldwide, CBRT has been using a wide range of its monetary tools to ease its policy stance and has injected liquidity into financial markets to ensure they continue to function smoothly so they can supply credit to businesses and the economy. CBRT has also been purchasing government debt, including from the country’s unemployment insurance fund, and on April 17 it doubled its limit on its asset purchases to 10 percent of its total assets from 5 percent. Turkey’s headline inflation rate eased to 11.86 percent in March from 12.37 percent in February and while core inflation rose to 11.65 percent, CBRT said inflation expectations, demand conditions and producer prices were contributing to a “mild trend” in core inflation indicators. Despite a depreciation of the Turkish lira due to global developments, a continued sharp fall in commodity prices, especially crude oil and metals prices, were having a favorable effect on the outlook for inflation. “Keeping the disinflation process in track with the targeted path requires the continuation of a cautious monetary stance,” CBRT said, adding maintaining a sustained disinflation process remains key to lowering the sovereign risk, lowering long-term interest rates and a stronger economic recovery. Turkey’s lira, which has been falling for the last decade, has depreciated sharply this year and fell further in response to today’s rate cut to trade at 6.99 to the U.S. dollar, down almost 15 percent this year.

The Central Bank of the Republic of Turkey issued the following press release:

“Participating Committee Members

Murat Uysal (Governor), Murat Çetinkaya, Ömer Duman, Uğur Namık Küçük, Oğuzhan Özbaş, Emrah Şener, Abdullah Yavaş.

The Monetary Policy Committee (the Committee) has decided to reduce the policy rate (one-week repo auction rate) from 9.75 percent to 8.75 percent.

As developments regarding the spread of the coronavirus substantially weaken global growth outlook, central banks in advanced and emerging economies continue to take expansionary measures. The pandemic disease is closely monitored for its evolving global impact on capital flows, financial conditions, international trade and commodity prices.

Having displayed a strong upward trend in January and February, thanks to the improvement in financial conditions, economic activity has started to weaken in mid-March due to the effects of the coronavirus pandemic on external trade, tourism and domestic demand. In order to contain negative effects of the pandemic on the Turkish economy, it is of crucial importance to ensure the healthy functioning of financial markets, the credit channel and firms’ cash flows. In this respect, recent monetary and fiscal measures will contribute to financial stability and post-pandemic recovery by supporting the potential output of the economy. Current account balance, which recently recorded significant improvement, is expected to follow a moderate course throughout the year due to the restraining effects of commodity prices and imports.

Developments in inflation expectations, domestic demand conditions and producer prices have contributed to a mild trend in core inflation indicators. Despite the recent depreciation in the Turkish lira due to global developments, continued sharp decline in international commodity prices, especially crude oil and metal prices, affects inflation outlook favorably. While the rise in unit costs resulting from declining production and sales is closely monitored, the disinflationary effects of aggregate demand conditions are estimated to have increased. In this respect, it is considered that risks on the year-end inflation projection are on the downside. Accordingly, the Committee decided to make a 100 basis point cut in the policy rate.

The Committee assesses that maintaining a sustained disinflation process is a key factor for achieving lower sovereign risk, lower long-term interest rates, and stronger economic recovery. Keeping the disinflation process in track with the targeted path requires the continuation of a cautious monetary stance. In this respect, monetary stance will be determined by considering the indicators of the underlying inflation trend to ensure the continuation of the disinflation process. The Central Bank will continue to use all available instruments in pursuit of the price stability and financial stability objectives.

It should be emphasized that any new data or information may lead the Committee to revise its stance.

The summary of the Monetary Policy Committee Meeting will be released within five working days.”

Gold was back in fashion on Wednesday, rising over 1% as Dollar weakness and lingering concerns over the global economy supported the flight to safety.

The precious metal seems to be finding support from the market mayhem and could extend gains as investors adopt a guarded approach towards riskier assets like stocks and emerging market currencies.

Looking at the technical picture, a move towards $1735 could be on the cards if a solid daily close above $1700 is achieved. Given how sensitive global sentiment remains to the historic oil meltdown and global recession fears, the rally in Gold could happen sooner than later.

Brent Crude whacked by oversupply fears

Brent Crude fell below $16 a barrel for the first time since 1999 on Tuesday evening as markets struggled with oversupply caused by the coronavirus lockdown.

This development comes after US oil prices turned negative for the first time as Oil producers paid consumers to take the commodity off their hands over fears that storage capacity could run out in May.

Brent Crude has depreciated over 70% since the start of the year and could extend losses in the short to medium term. Looking at the charts, sustained weakness below $25 could open the doors back towards $19.

GBPJPY breakout in the making

Over the past five weeks, the GBPJPY has traded within a wide 350+ pip range with support at 132.00 and resistance at 135.70.

Sustained weakness below 134.00 could encourage a decline towards 132.00 and 130.00. Alternatively, a breakout above 134.00 may open a path towards 135.70 which will then clear the road for 137.00.

USDCAD waits for the next catalyst

It is no surprise that the Canadian Dollar has weakened against almost every single G10 currency year-to-date.

The Canadian Dollar shares a posotive correlation with Oil prices, so when the commodity tumbles – the CAD also weakens. Looking at the technicals of the USDCAD, prices are trading within a wide range. If 1.4050 proves to be reliable support, the currency pair could retest 1.4250. Alternatively, a breakdown below 1.4050 should signal a move towards 1.3850.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Today’s data on changes in the US oil reserves for the week may affect the dynamics of the markets. The main reason for the decrease in world oil prices is that world production is still 90 million barrels per day, while global demand is only 75 million. Due to the quarantine and the reduction of passenger traffic, the world’s demand for motor fuel has fallen against the backdrop of coronavirus. The surplus so far goes to oil storages of different countries. The decline in oil prices has a negative impact on stock markets, as it is a sign of a global economic downturn.

Forex news

Currency Pair

Change

EUR USD

+0.1%

GBP USD

+0.39%

AUD USD

+0.18%

Yesterday’s collapse in world oil prices weakened the currencies of commodity countries, causing the US dollar index to rise. It updated the 2-week maximum. Today, the US currency is correcting downwards. No significant economic information is expected in the USA, but weekly oil reserves data will come out soon. The Australian dollar rose today thanks to preliminary data showing an 8.2% increase in retail sales in Australia in March. This is the maximum monthly growth in more than 20 years. However, it may turn out to be a one-time event, as it is caused by mass purchases of the population before quarantine. Reserve Bank of Australia forecasts a 10% drop in GDP for the first half of this year. The British pound has strengthened slightly today due to lower inflation in Britain in March to 1.5% year-on-year from 1.7% in February. The euro is being traded narrowly in anticipation of the outcome of the virtual EU finance ministers’ meeting on Thursday. They will discuss measures to support the European economy affected by the coronavirus epidemic and the amount of funds required.

Stock Market news

Indices

Change

Dow Jones Index

-2.65%

S&P 500

-3.05%

Nasdaq 100

-3.68%

Nikkei Index

-2.79%

US Dollar Index

+0.28%

On Tuesday, global stock indices dropped, as investors believe the collapse of oil prices could mean a global economic downturn. All 11 sectors of the American S&P 500 index fell. According to Refinitiv agency, the total net profit of the energy sector in the 1st quarter will fall by 58.9% compared to the previous year. Because of this, quotes of the S&P 500 energy index have fallen by 46% since the beginning of the year and it became the leader of the fall in S&P 500. Regarding forecasts for the 1st quarter, the total profit of all companies in the S&P 500 stock index is expected to decrease by 13.6%. It should be noted that quotes of this index are now below the figures of the beginning of the year by 14% or about the same amount. Thus, the drop in company profits is included in the S&P 500 value. This morning, futures on US stock indexes are being traded up. Investors responded positively to the US Senate’s decision to allocate $500 billion to help American small businesses. Another positive factor was the increase in profit of the Netflix online cinema in the 1st quarter. The demand for online entertainment and services increases due to quarantine amid Covid-19.

Commodity Market news

Commodities

Change

WTI Crude

-36.86%

Brent Crude Oil

-19.13%

On Tuesday, the U.S. crude oil futures, with repayment in May, in a moment demonstrated an absurd price minus $40 per barrel. This means that the seller must pay the buyer to take the oil. However, by the time the market closed on Tuesday, US oil still rose to $ 11 per barrel. Today, oil is being traded in a narrow range, awaiting the release of the US reserves changes data for the week ended April 17. They are projected to increase by 12.9 million barrels. Recall that on April 10, S&P Global Platts agency estimated the main US oil storage occupancy rate in Cushing at 70%.

Gold Market News

Metals

Change

Gold

-0.52%

On Tuesday, gold was trying to get cheaper against the backdrop of a stronger dollar, but its downward movement was short-term. Today, gold quotes continued to grow, as investors remain fearful of the global economic crisis. Yesterday, palladium prices fell by 15%. This metal is used in the manufacture of automobile catalysts and its price is highly dependent on the state of the global economy.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Swiss trade surplus rose in March: the trade surplus reached 4.02 billion francs from 3.54 in February, when a decline to 3.23 billion was expected. This is bearish for USDCHF.

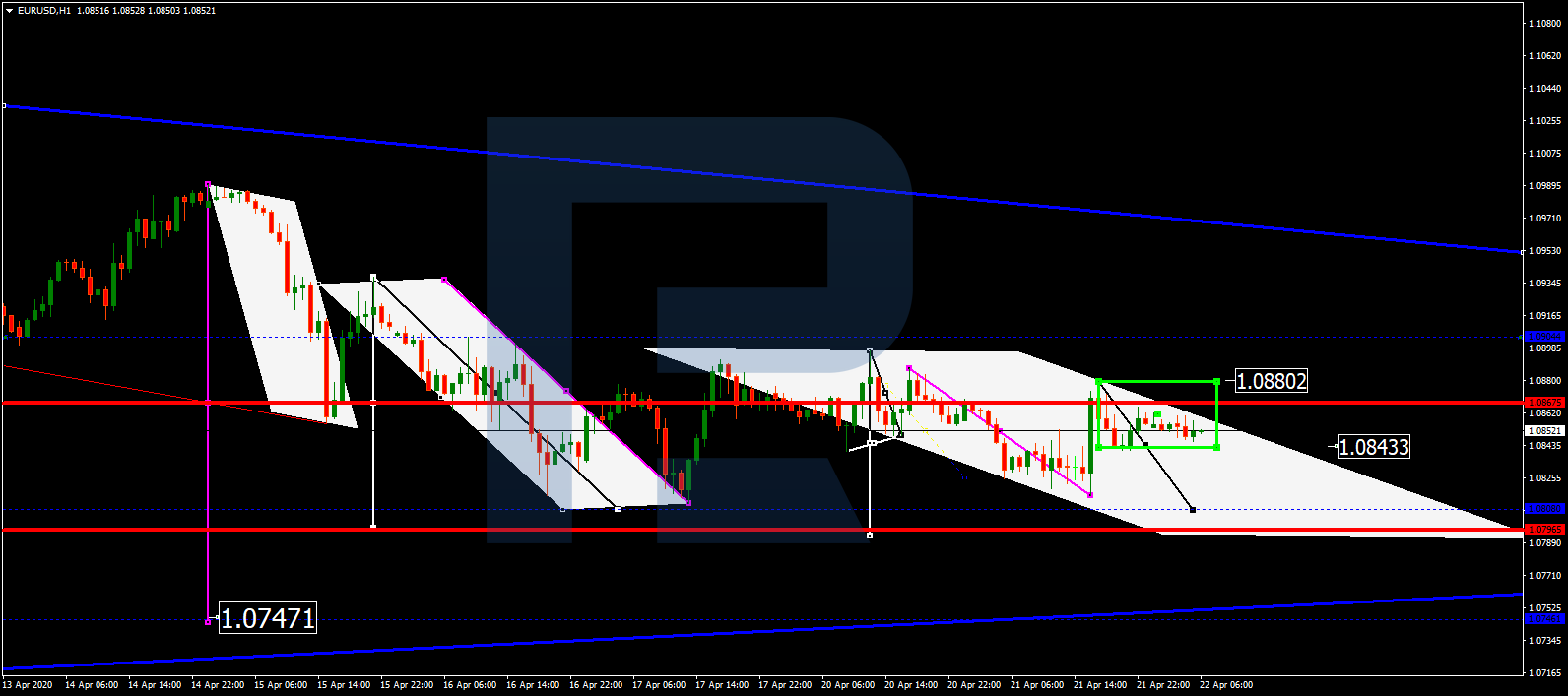

After falling towards 1.0820, EURUSD has completed the ascending structure at 1.0880, thus forming a new consolidation range around 1.0844, which may be considered as a downside continuation pattern. According to the main scenario, the price is expected to start another decline to reach 1.0800 and then resume growing to return to 1.0844. After that, the instrument may form a new descending structure with the target at 1.0750.

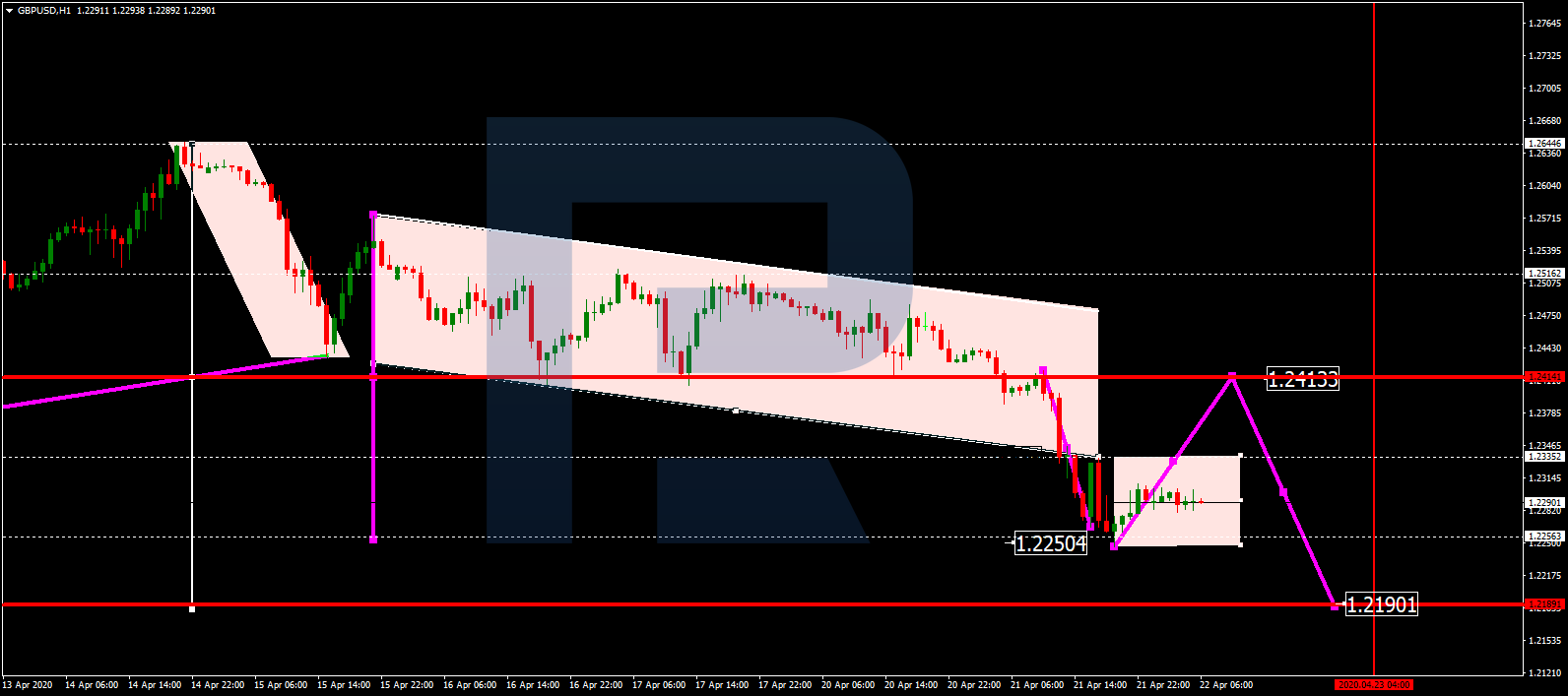

GBPUSD, “Great Britain Pound vs US Dollar”

After reaching the target of the third descending wave at 1.2250, GBPUSD is consolidating below this level. Possibly, the pair may grow towards 1.2333 and then resume moving downwards to reach 1.2190. Later, the market may start a new correction with the target at 1.2415.

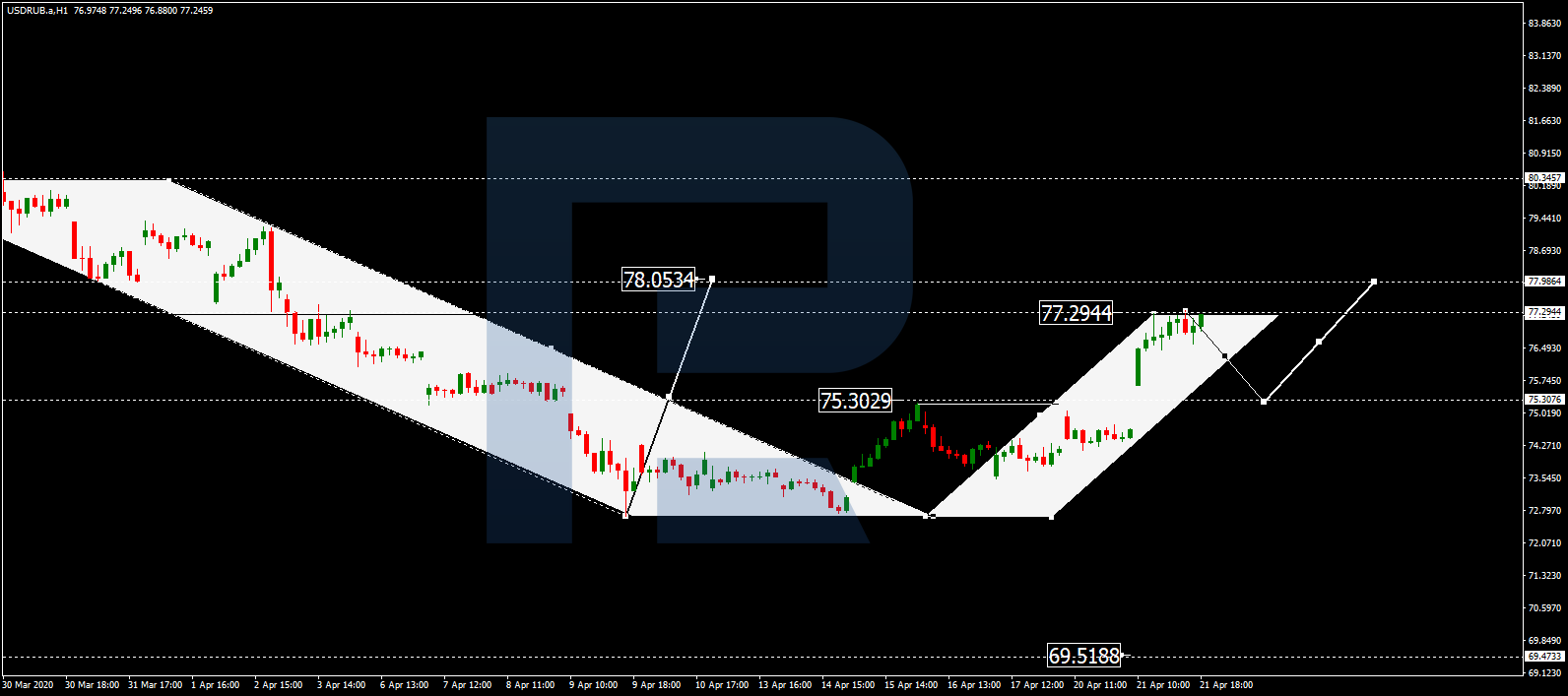

USDRUB, “US Dollar vs Russian Ruble”

After breaking 75.30 to the upside, USDRUB is still growing. Today, the pair may extend this wave to reach 78.05 and then start a new correction to return to 75.30.

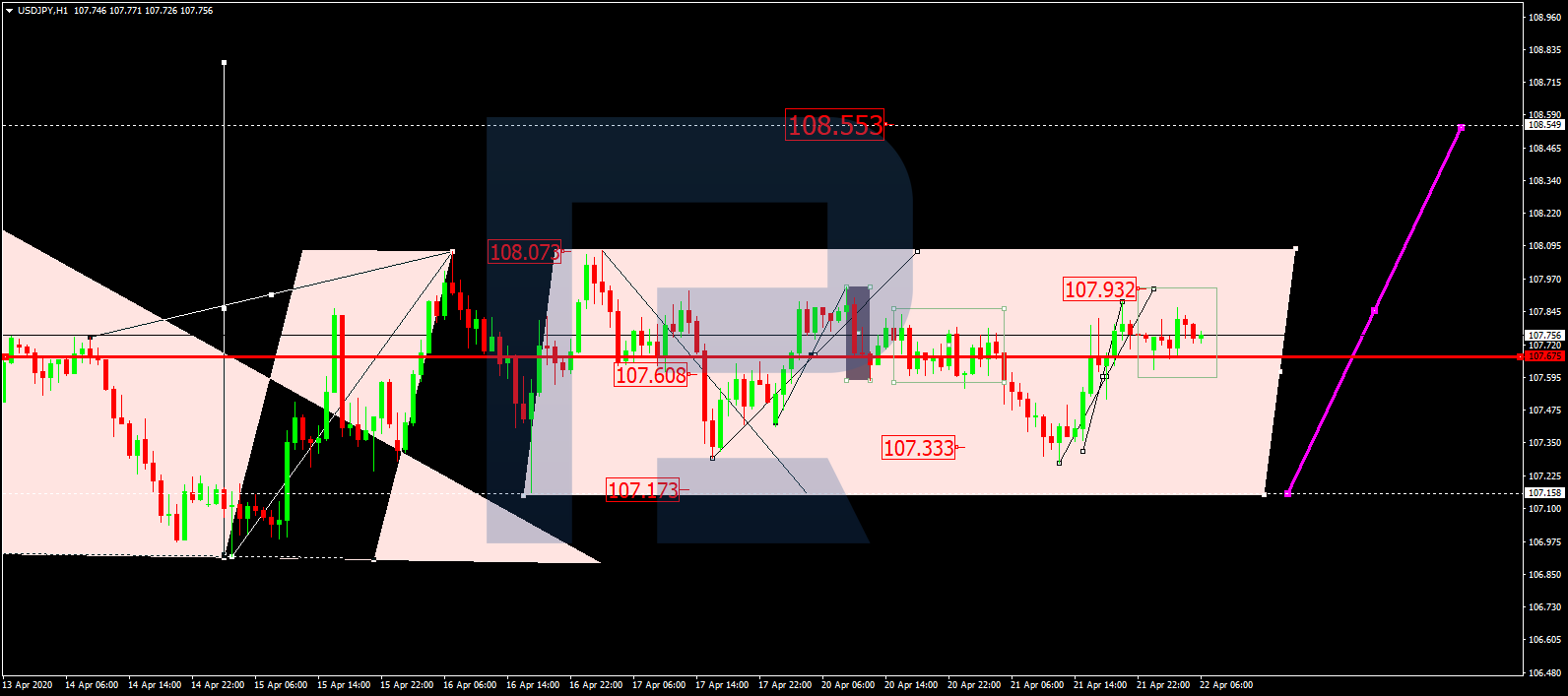

USDJPY, “US Dollar vs Japanese Yen”

USDJPY is forming a wide consolidation range around 107.60. Possibly, today the pair may expand the range up to 107.90 and then return to 107.60. After that, the instrument may expand the range again up to 108.07. However, if the price breaks 107.60 to the downside, the market may start another decline to expand the range down to 107.20.

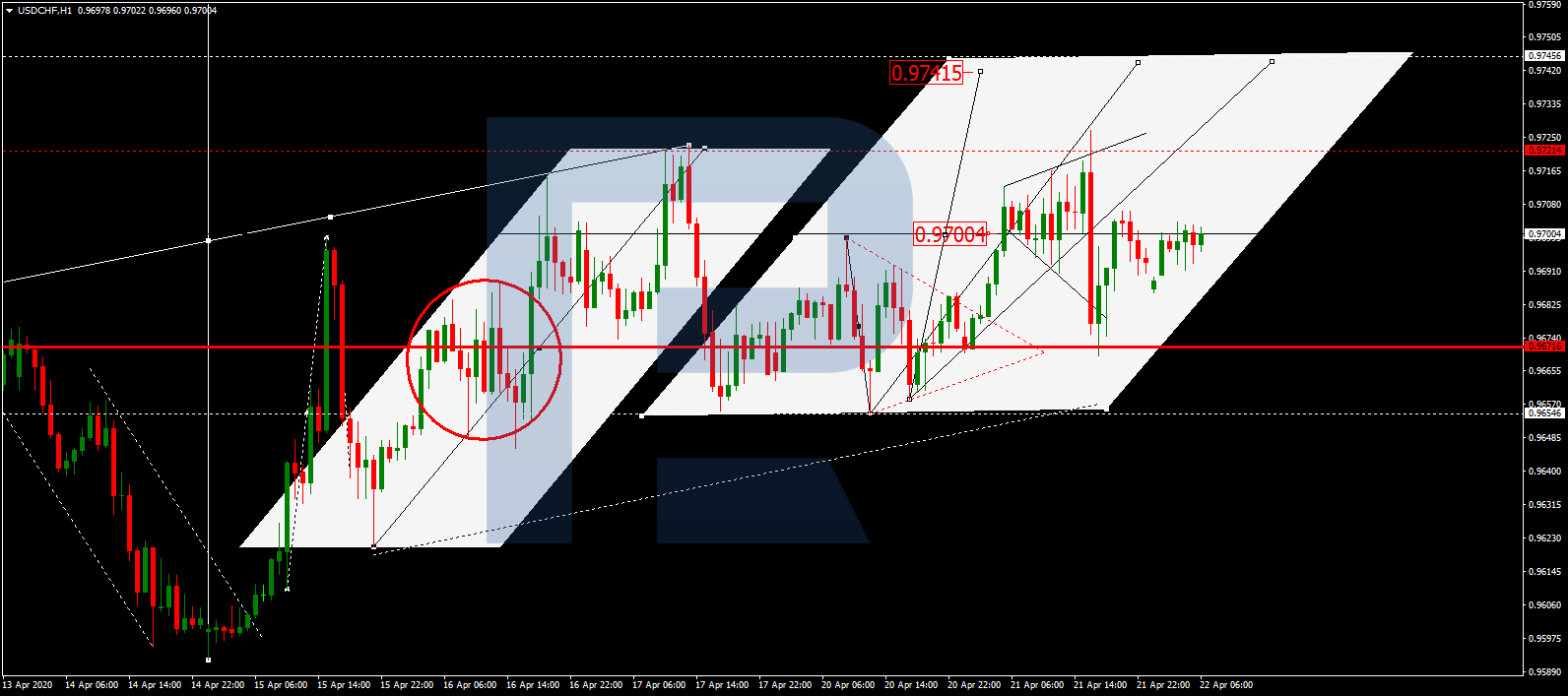

USDCHF, “US Dollar vs Swiss Franc”

After expanding the consolidation range up to 0.9726 and then down to 0.9675, USDCHF is moving not far from 0.9700, right in the middle of the range, which may be considered as an upside continuation pattern. The main scenario implies that the price may break the upside border and reach the first target at 0.9740. However, if the pair breaks the downside border, the market may correct towards 0.9650 and then resume trading upwards to reach the above-mentioned target.

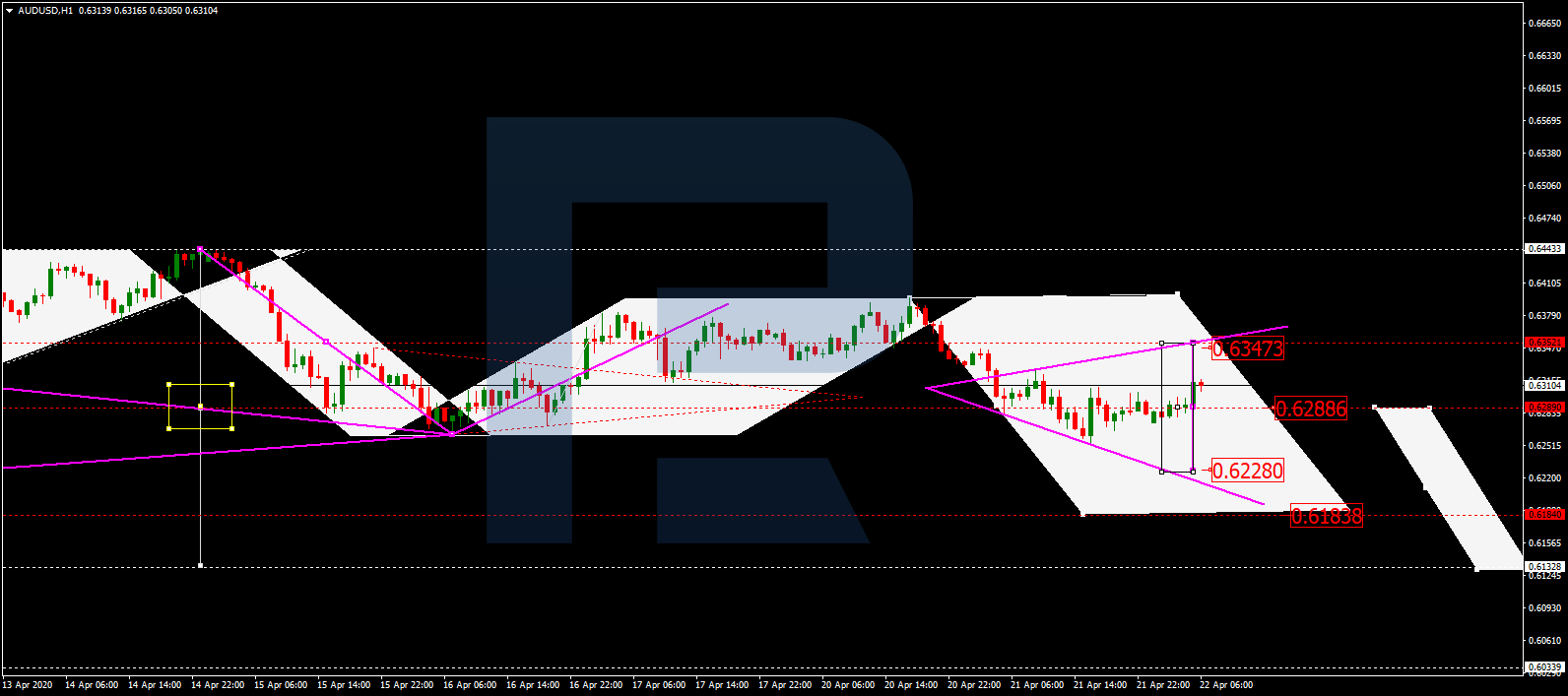

AUDUSD, “Australian Dollar vs US Dollar”

After finishing the descending structure towards 0.6235 and then completing the correction at 0.6352, AUDUSD is expected to continue falling and reach 0.6228. Possibly, the pair may form a downside continuation pattern. After that, the instrument may grow to reach 0.6288 and then resume trading inside the downtrend with the short-term target at 0.6183.

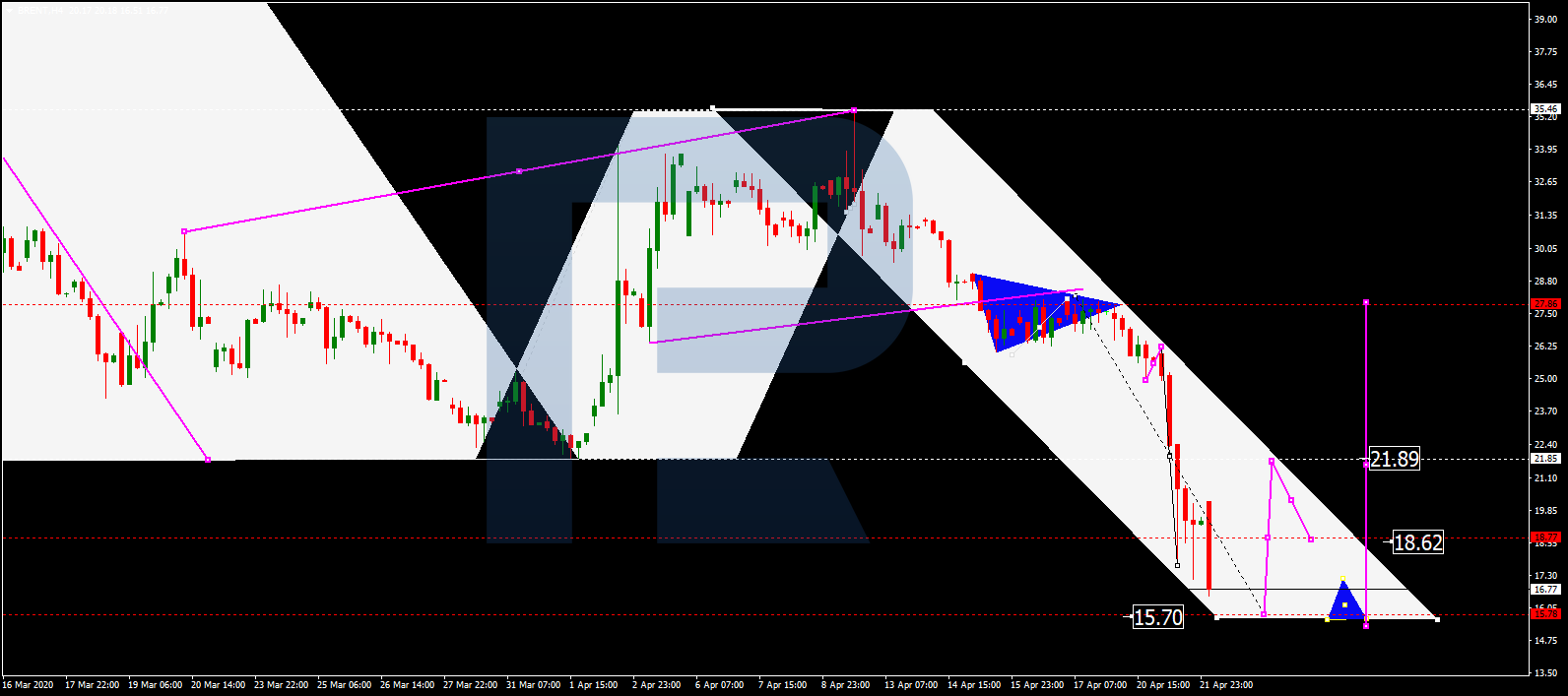

BRENT

Brent is moving downwards. Possibly, the pair may reach 15.70 and then resume growing towards 18.60, thus forming a new consolidation range between these two levels. If later the price breaks 25.00 to the upside, the market may form one more ascending structure with the target at 21.90.

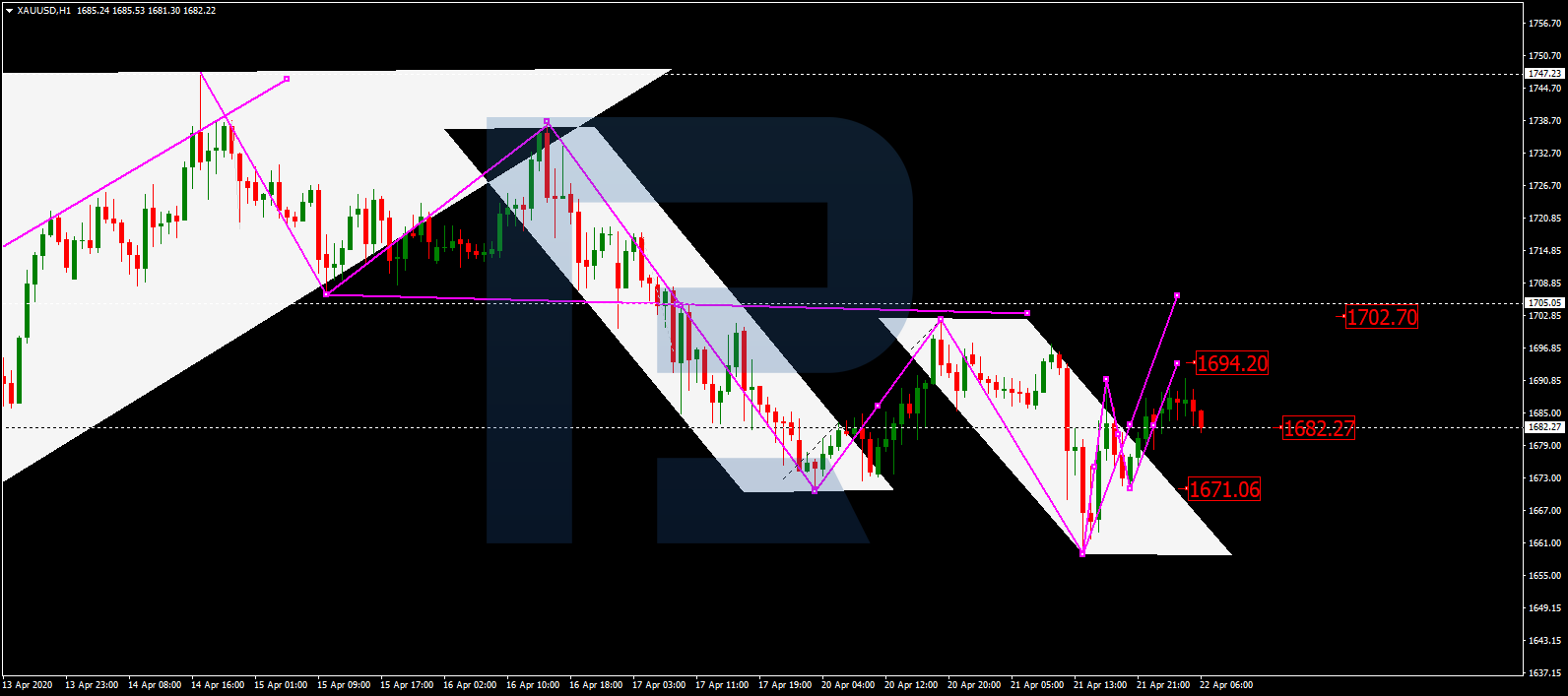

XAUUSD, “Gold vs US Dollar”

After completing the descending wave at 1660.00, Gold is trading upwards with the short-term target at 1694.20. After that, the instrument may correct towards 1682.22 and then form one more ascending structure to reach 1702.70.

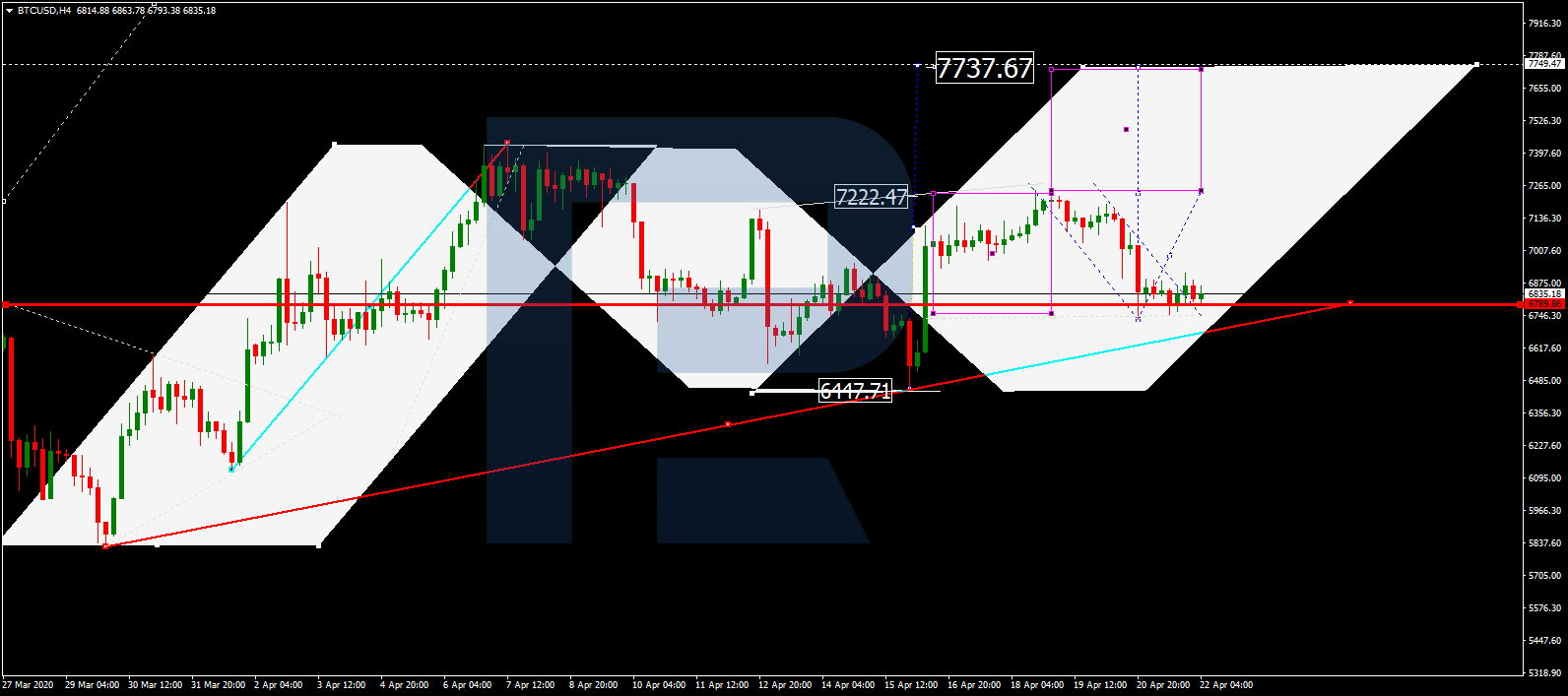

BTCUSD, “Bitcoin vs US Dollar”

BTCUSD is consolidating above 6800.00. According to the main scenario, the price is expected to grow to break 7000.00 and then continue trading upwards with the target at 7700.00. Later, the market may start a new correction to reach 6800.00.

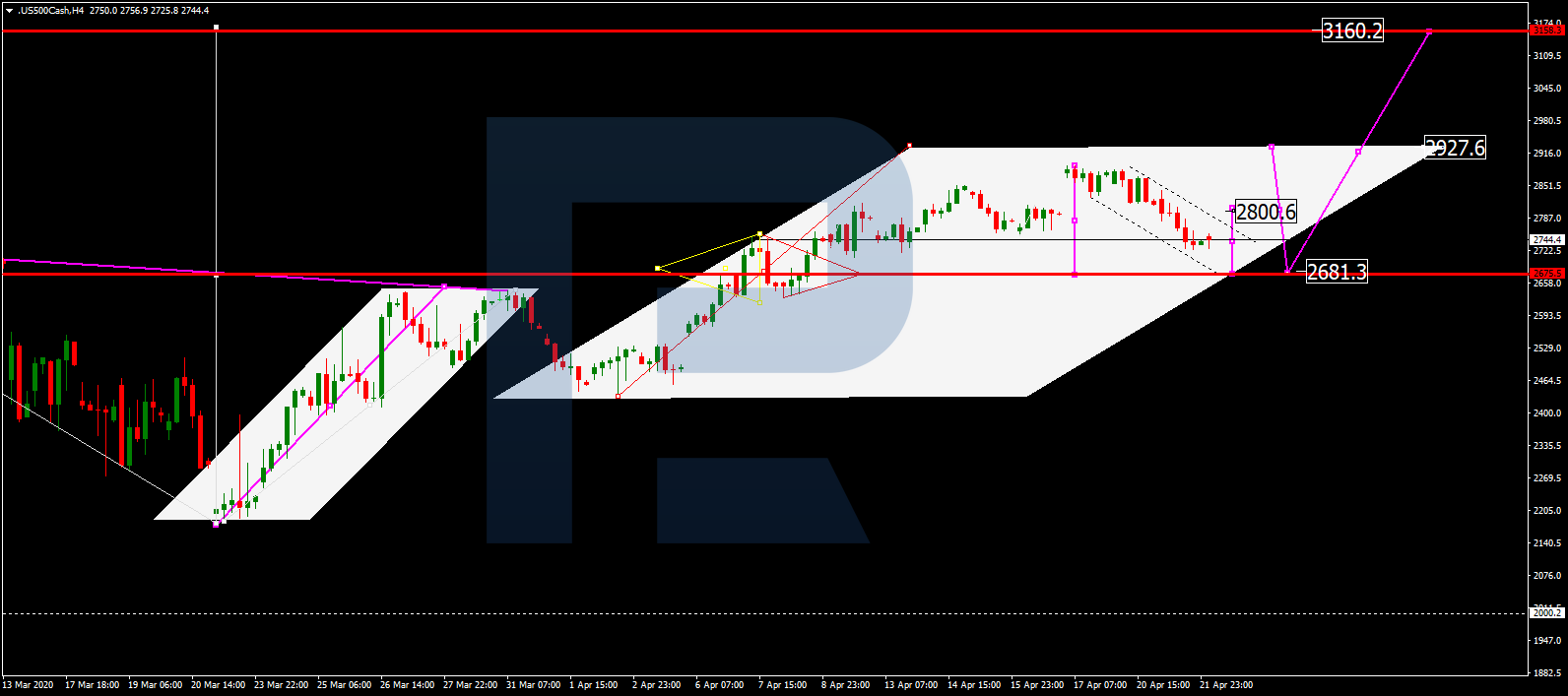

S&P 500

S&P 500 is still correcting. Possibly, the price may form a new descending structure towards 2681.3 and then start another growth to break 2800.5. After that, the instrument may resume trading inside the uptrend with the short-term target at 2927.6.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

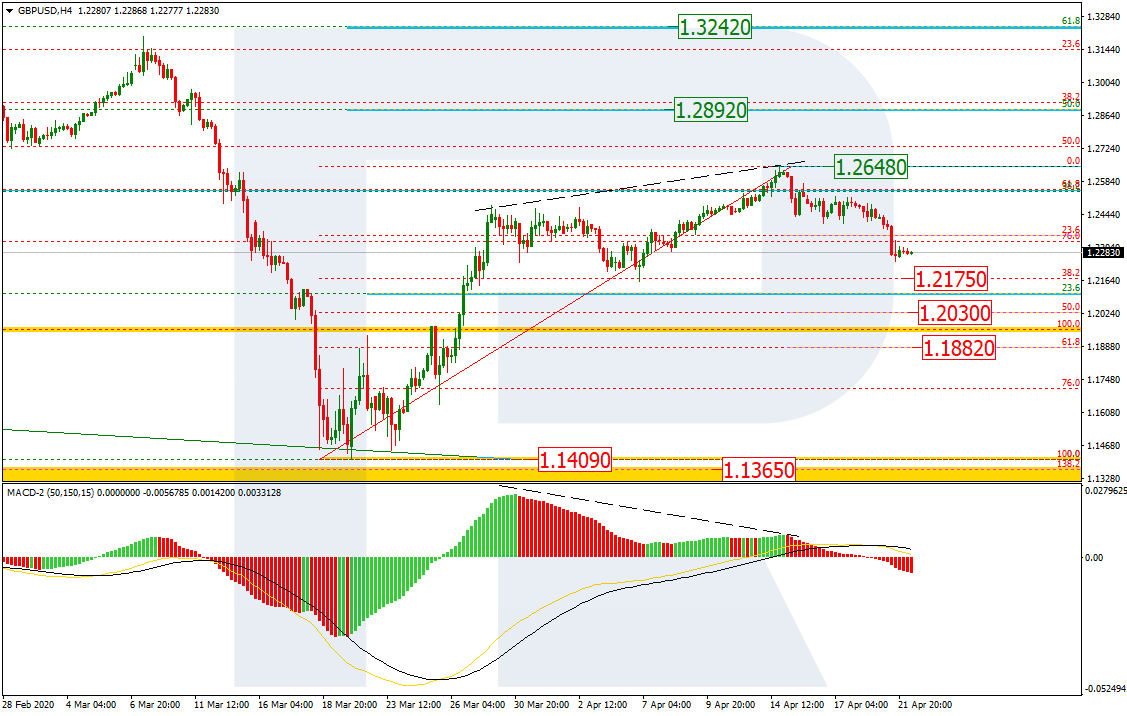

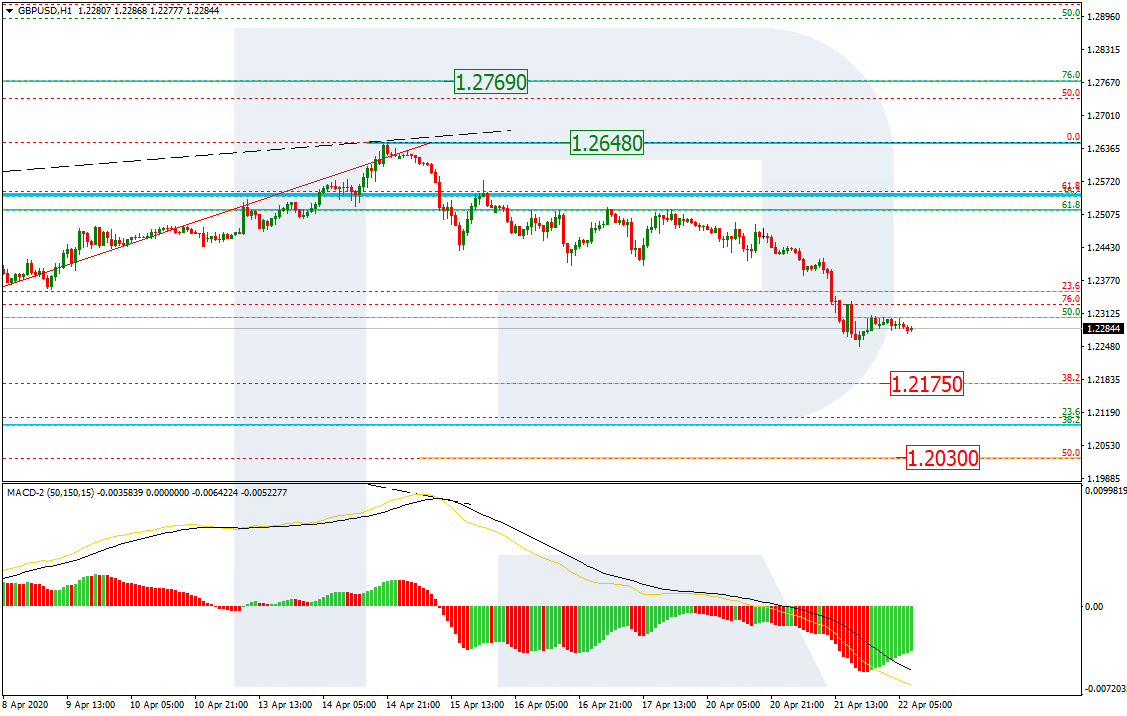

As we can see in the H4 chart, the divergence made the pair start a new decline, which may be considered as a descending correction. At the same time, one should realize that only a decline towards the low at 1.1409 and a breakout of this level may really force a trend reversal. If the price breaks the low at 1.1409, the instrument may continue falling towards the post-correctional extension area between 138.2% and 161.8% fibo at 1.1365 and 1.0996 respectively. After finishing the correctional downtrend, the price may resume trading upwards to reach the local high at 1.2648 and then 50.0% and 61.8% fibo at 1.2892 and 1.3242 respectively.

The H1 chart shows a more detailed structure of the current correction. The pair is approaching 38.2% fibo at 1.2175 and may later reach 50.05% fibo at 1.2030. The resistance is the high at 1.2648. MACD lines are directed downwards, thus indicating further decline.

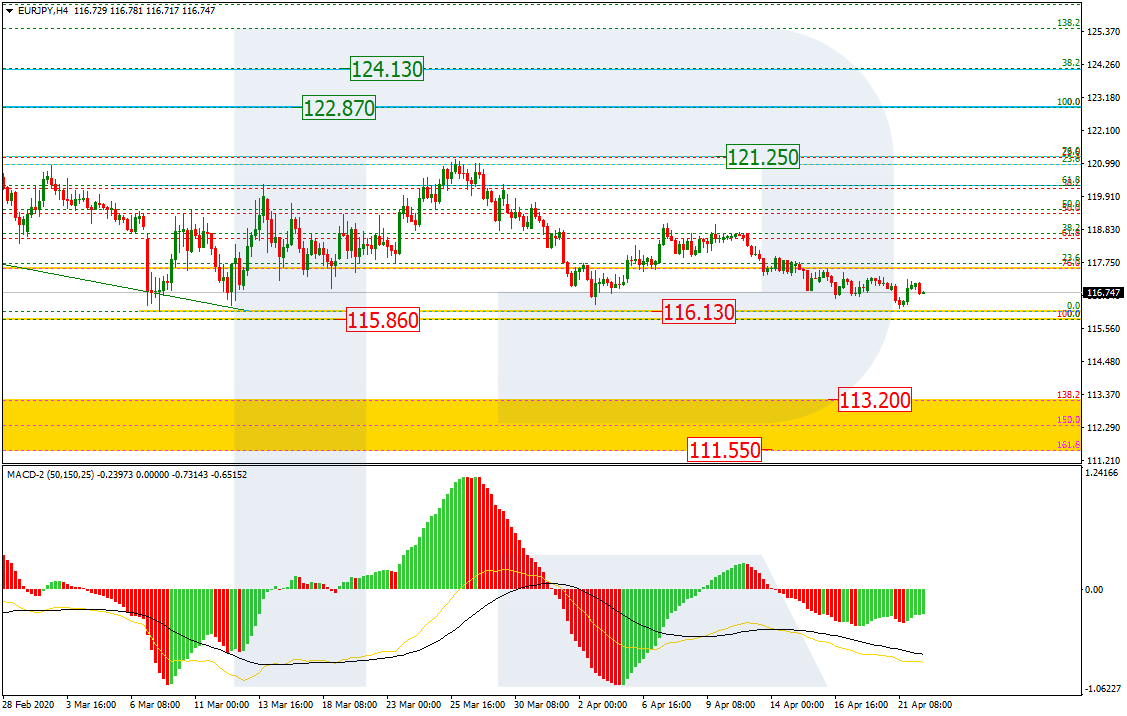

EURJPY, “Euro vs. Japanese Yen”

As we can see in the H4 chart, EURJPY is slowing and steadily falling towards its key lows at 116.13 and 115.85. If these levels are broken, the instrument may continue trading towards the post-correctional extension area between 138.2% and 161.8% fibo at 113.20 and 111.55 respectively. The price may yet try to reach 76.0% fibo at 121.25, but this scenario is rather unlikely.

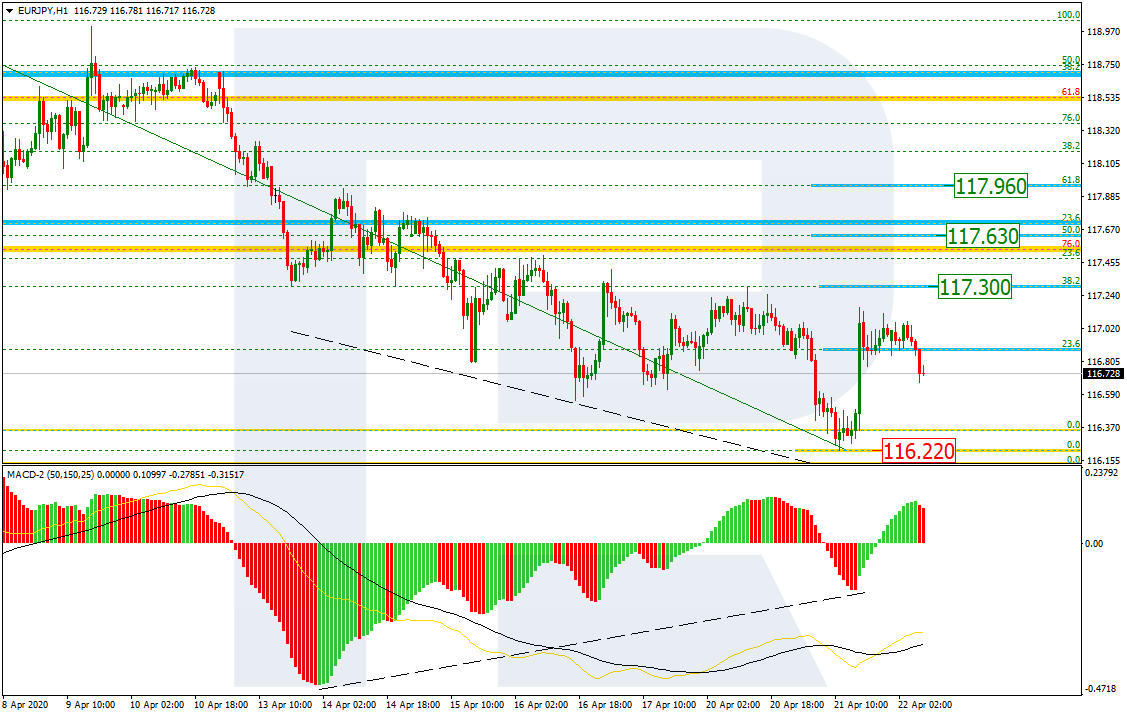

In the H1 chart, the local convergence made the pair start a new correctional uptrend, which has already reached 23.6% fibo. The next upside targets may be 38.2%, 50.0%, and 61.8% fibo at 117.30, 117.63, and 117.96 respectively. The support is the low at 116.22.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.