By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM, ForexTime

Investors keeping their fingers crossed as hope builds following gradual steps from world governments to slowly loosen lockdown restrictions will eventually lead to a return of demand for the global economy has kept risk appetite kicking so far into the new trading week. South Africa, Nigeria, New Zealand and the United Arab Emirates represent just a few of the countries that have loosened some restrictions in recent days, and the test of time on whether more countries are set to follow these footsteps will determine whether the modest rally in stocks can continue.

I have my own doubts on how much more fire can be added to the flame to push markets higher and a trend that investors can keep an eye on is whether any signals creep through that positions could be closed as April concludes. Upcoming central bank decisions from the likes of the U.S. Federal Reserve, European Central Bank as well as earnings announcements from corporations such as HSBC, Facebook, Samsung, Tesla and Amazon will also be viewed as event risks.

Can lightning strike twice for oil?

Investors will be unable to dismiss an element of recent history repeating itself with tanking oil prices and whether lightning could be set to strike twice. WTI has already dropped more than 12% so far during on Tuesday below $11 while Brent Crude is 5% down below $20. It looks like fear is kicking into investor sentiment following the insane shock just one week ago that eventually led to negative U.S oil prices and nobody wants to see the next contract expiry date follow the path of the May contract. As a result it appears that upcoming contracts are becoming very liquid, and investors can expect to see continued volatility.

No signs of lockdown exit strategy to risk sell in May trend for Pound?

The first speech from UK Prime Minister Boris Johnson on his return to work following his battle with the coronavirus indicated to investors that life in the United Kingdom as it stands will be very much stay at home throughout May. It was expected that we would have a cautious speech from the UK Prime Minister and any guidance from officials on a potential timeline for when some measures can be lifted will be viewed as a potential opportunity for a pop higher in UK assets.

Eased lockdown measures to threaten the Dollar’s throne?

One trend in the currency markets that can be watched closely is what impact signs of loosened government restrictions has on demand for the USD. The Greenback has shown signs of getting out of the wrong side of the bed so far this week with initial declines against a mixture of its counterparts, and more signs of eased lockdowns across several countries can be digested as a test ahead for King Dollar. As well as with emerging markets, some of the other currencies that can cheer potential weakness in the USD include the Euro, Australian Dollar and British Pound.

Prospects for South African assets improving, but Rand not completely out of the woods just yet

South African assets, including its currency and stock market are aiming to strengthen as investors continue to reflect positively that the economy is set to begin a partial reopening. Improved global sentiment based on other economies providing indications that they are also gradually loosening the leash on their own lockdown restrictions would also benefit South African assets on risk appetite.

Prospects are looking stronger for Rand, although there is a cautious undertone that the Rand and wider South African assets are not completely out of the woods yet. However, the majority of the tornado intensity that has seen the Rand weaken more than 30% during 2020 so far has hopefully passed.

The economic calendar of scheduled releases from South Africa for this week are mostly void of major tier-one data, although the trade balance for March is set to be announced this Thursday and it should provide insight on what impact the early stages of world lockdowns had on South African trade.

There isn’t a genie in a lamp that can be rubbed to take the last month away from memory, so there is a need for deep breathes as economic data releases globally point towards the direction that the fight against the coronavirus pandemic has threatened the worst recession in close to a century.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

– Crude Oil continues to be a big mover as the supply glut has really pushed global capacity to its limits. Dozens of full tanker ships are anchored off the California and Singapore coastlines waiting for demand to pick up. As long as the Virus shutdown persists globally, the supply gut will continue to wreak havoc on oil price levels into Summer. As of early Monday morning, Crude Oil is lower by -17% to $14.10 as I type.

What most readers of our articles here don’t fully grasp is just how accurate our long-term predictions truly are and its why we link to past research posts that clearly prove our analysis can be deadly accurate.

You may remember our incredible research post from July 2019 which suggested Crude Oil would collapse in early 2020 calling out a potential $14 price target.

You may also like to review our warning from January 2019 related to Oil and Energy. We also predicted the gold bullion breakout and bull market to happen last year in April, May, or June, which is it, and we called that six months prior. Eric Sprott talked about our gold prediction and how much he liked out analysis on his podcast back then.

Our Adaptive Fibonacci price modeling system is suggesting a support zone near $9 to $18 may become a new sideways trading zone for Crude Oil. We believe the downside risk to price levels is still excessive, but we also believe that true price valuation levels will keep Oil above $4 ppb as global demand will eventually recover. Thus, we believe Oil will likely settle into a sideways price range between $9 and $18 as this virus event continues. It may attempt brief moves outside these ranges but eventually, settle back into this range until true demand begins to accelerate higher.

Before we continue, be sure to opt-in to our free market trend signals before closing this page, so you don’t miss our next special report!

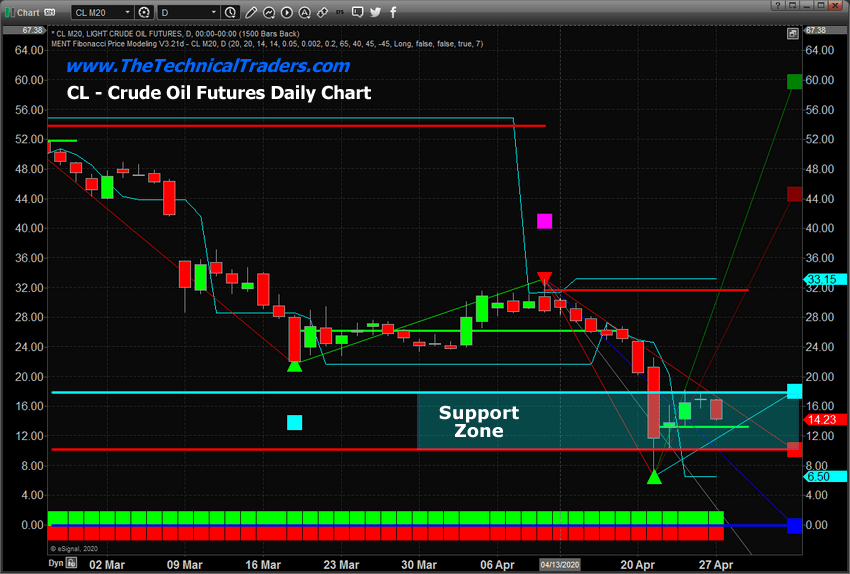

This Daily Crude Oil Chart highlights our Adaptive Fibonacci Price Modeling system’s results and clearly shows the Support Zone. We believe this Zone will become a new sideways price channel for Crude oil.

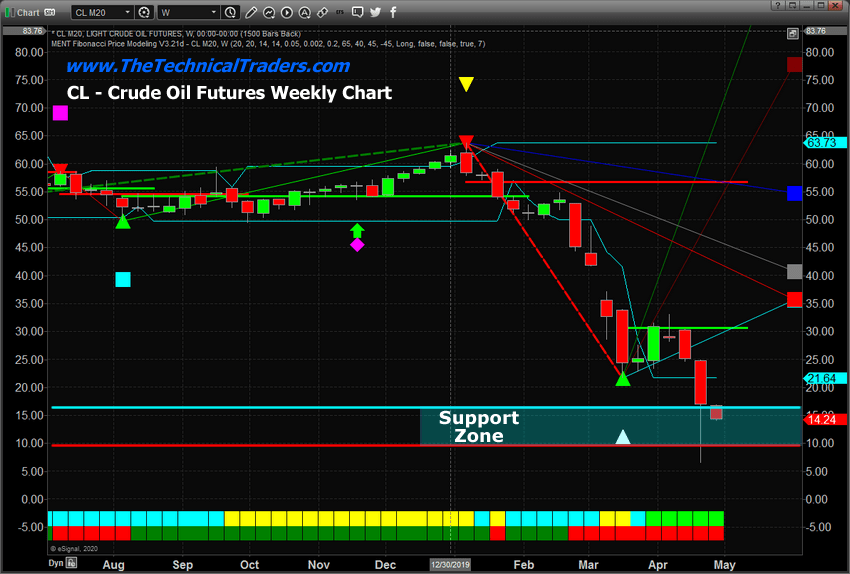

Weekly Crude Oil Price Chart – Support Zone

This Weekly Crude Oil Price chart also highlights the Support Zone. The potential for Crude prices to retest the $7 to $8 price range based on this massive supply glut is not out of the question. We believe Crude Oil will settle into the Support Zone while attempting to establish a price bottom near $7 or $8 over the next 90+ days. It may become an extended sideways bottom/flag formation as the bottom forms.

Our suggestion is to expect a more sideways bottom formation in Crude Oil over the next 60 to 90+ days. The supply-side glut is really pushing price levels down to extreme levels. Nothing will change that aspect of the market dynamic until we exit this Virus shut-down and demand starts to skyrocket higher. That may come in August or later in the year.

We do believe Oil will attempt to find support above $7 to $8 ppb as we believe the supply glut will push oil prices to a “core value level” where global buyers will attempt to say “we can’t sell oil at anything less than $x.xx”. We believe that level is $7 to $8 ppb overall.

As a technical analyst and trader since 1997, I have been through a few bull/bear market cycles in stocks and commodities. I believe I have a good pulse on the market and timing key turning points for investing and short-term swing traders. 2020 is an incredible year for traders and investors. Don’t miss all the incredible trends and trade setups.

We all have trading accounts, and while our trading accounts are important, what is even more important are our long-term investment and retirement accounts. Why? Because they are, in most cases, our largest store of wealth other than our homes, and if they are not protected during a time like this, you could lose 25-50% or more of your entire net worth. The good news is we can preserve and even grow our long term capital when things get ugly like they are now and ill show you how and one of the best trades is one your financial advisor will never let you do because they do not make money from the trade/position.

If you have any type of retirement account and are looking for signals when to own equities, bonds, or cash, be sure to become a member of my Long-Term Investing Signals which we issued a new signal for subscribers.

Subscribers of my ETF trading newsletter had our trading accounts close at a new high watermark. We not only exited the equities market as it started to roll over in February, but we profited from the sell-off in a very controlled way with TLT bonds for a 20% gain. This week we closed out SPY ETF trade taking advantage of this bounce and entered a new trade with our account is at another all-time high value.

Ride my coattails as I navigate these financial markets and build wealth while others watch most of their retirement funds drop 35-65% during the next financial crisis.

Building up with the gradual closures of major sports leagues around the world, online betting platforms were always expected to take a hit on the London Stock Exchange. One of the biggest in the UK, Flutter Entertainment PLC, was certainly among those to be impacted by the lockdown on sports.

The company, which is comprised of the online gambling platforms Paddy Power, Betfair, and brands incorporated under The Stars Group, is one of many which sees much of its revenue come via sports betting. While share prices dropped somewhat, they have recovered rather well since the drop. A major reason behind this is the omnichannel nature of the company’s leading brand, Paddy Power.

Flutter Entertainment, as rebranded in 2019 from Paddy Power Betfair, saw its share price take a significant drop from 11 March to 12 March, falling from 7,924.00 GBX to 6,700.00 GBX. The drop coincided with the continued closures of elite-level football leagues across Europe and the impetus on the Premier League and English Football League to follow suit. On 13 March, the Premier League, FA, EFL, and WSL postponed professional football.

The value continued to tumble, hitting a year-low, by quite some margin, of 5,512.00 GBX on 18 March. This was the point at which the UK as a whole was going into lockdown. As Flutter totes several shops across the UK, further drops were inevitable, with the prime minister, Boris Johnson, further emphasising a stay-at-home order of seven days to two weeks.

As those orders were extended a great deal, one would assume that the company deriving much of its profits from betting would see its share price continue to decrease. However, in the weeks since the 18 March low, Flutter has risen a tremendous amount.

One of the key aspects which have allowed Paddy Power to become such an influential figure in British iGaming is that they provide a wide-ranging gambling platform. While sports betting is, of course, big business, the Paddy Power platform also prominently displays its expansive games section. Known for their advertising campaigns, the Flutter company now appears to be benefitting from bringing in the likes of Jose Mourinho and Rhodri Giggs as comedic advert stars over the past couple years.

Just by looking at the page’s betting games online, it’s clear to see that people are making the most of the offering. The progressive jackpots – Monster Jackpot, Daily Jackpot, Jackpot King, and Cash Boost Jackpot – were all increasing at a rapid pace, at the time of writing, meaning that many players must be playing the associated titles. Then, of course, there are the unseen levels of gaming across the other slots, instant wins, roulette, and blackjack games.

On 16 March, Flutter Entertainment announced that the closures of sports around the world could cost the company significantly; yet despite this, share prices have been getting stronger. On 24 April, the Flutter Entertainment PLC price climbed to 9,044.00 BX, ticking up slightly on its more normalised pricing of 9,018.00 GBX from 17 April.

Without any sport on the cards, it’s inevitable that most of the UK’s premier iGaming companies will feel the loss. However, at least in regards to share price, Paddy Power’s long-lasting embrace of its games offering appears to have allowed them to remain relevant with punters, which may have influenced their share price to recover quickly.

The silver futures price is near $15.50 per ounce but good luck buying the white metal anywhere near that price (with one notable exception discussed later).

The inventory of low-premium retail coins, rounds, and bars mostly disappeared in a matter of days when fears over COVID-19 pricked the bubble in global equity markets back in March.

Buying demand increased 5-fold and sellers all but vanished. Mints and refiners producing new products were unable to bridge the widening gap between supply and demand, and premiums exploded higher.

Today the lowest premium product available for delivery – the 10 oz silver bar – is sold at approximately $3.50/oz over the paper futures market price. The higher premiums on some coins – especially the Silver Eagle – are giving investors pause.

The question is whether or not to buy now or wait for better pricing.

Before we examine that question, we should point out that investors who don’t need physical possession of their metal don’t have to make this difficult choice.

However, anyone who wants delivery of silver now does have to make a choice. The key consideration is when supply will once again be plentiful relative to demand.

These are the challenges to bringing more supply of retail coins, rounds, and bars to market:

Mints and refiners need to ramp up production. That means hiring people and getting machinery up and running.

All other considerations aside, it takes months to expand production capacity. Given these firms are emerging from several years of poor demand, they may be reluctant to make large investments right away.

COVID-19 is disrupting supply and that may continue. Major Swiss refineries, the Royal Canadian Mint and the U.S. Mint have all dealt with temporary closures over the past 6 weeks. Going forward, these firms are likely to deal with any virus outbreaks by pausing operations once again.

There are very few people selling bullion right now. We’ll need some combination of higher prices and lower fear before more metal can be pried loose from those who hold it.

Now let’s take a look at demand:

Investor sentiment remains supportive of bullion buying. The bullion market went from being a sleepy backwater to a hot ticket.

The recent rally in stock prices doesn’t seem to have changed that much. Lots of people recognize the rise in equities is 100% fueled by Fed stimulus and not by any improvement in fundamentals.

There should be very few people left who view current monetary and fiscal policy as temporary. The Fed will continue suppressing interest rates and buying up bonds. Officials aren’t even talking about these measures being temporary anymore; that would be an obvious lie.

One round of stimulus after another coupled with lower tax receipts will mean multi-trillion dollar deficits as far as the eye can see. We have entered the end-game for the U.S. dollar as the world reserve currency.

The case for falling demand in precious metals hinges on some sort of return to “normalcy”. COVID-19 will need to turn out to be less deadly and economically disruptive than people thought. And it’ll also take people fairly quickly going back to work and resuming their regular activities.

A return to normalcy is, in our view, a real long shot. The 25 million people who have already lost jobs won’t all have a job to go back to.

Many businesses will not weather this storm, and fear of the virus is going to permanently change consumer habits.

When we consider both supply and demand, the odds favor premiums remaining high for months (at a minimum). The wait for lower premiums could be a long one.

If you are contemplating an investment in physical metal as a safe haven, you need to consider whether or not you have the luxury of time. The less metal you currently hold, the more urgent it is to bite the bullet and start stacking.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

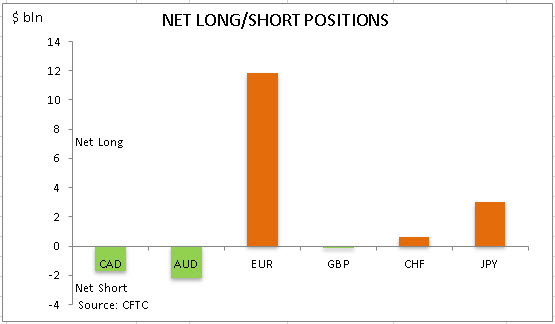

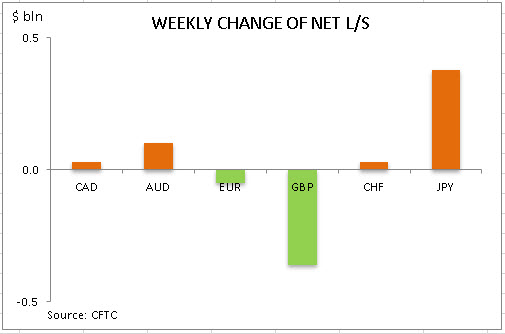

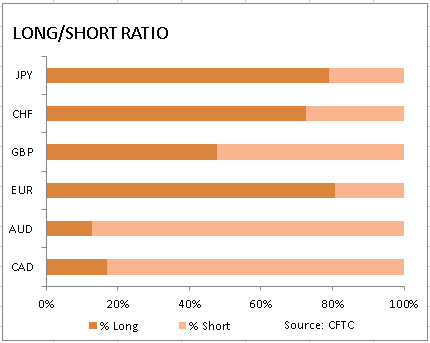

US dollar net short bets increase continued to $11.51 billion from $11.34 billion against the major currencies during the one week period, according to the report of the Commodity Futures Trading Commission (CFTC) covering data up to April 21 and released on Friday April 24. The change in overall dollar position was due to increase in bullish bets on yen and Swiss franc, while bearish bets on Canadian and Australian dollars were cut further as they maintained net short positions against the dollar. British Pound bets turned bearish joining Canadian and Australian dollars. Bearish dollar bets rose as the Commerce Department reported a bigger than expected 8.7% drop in retail sales in March, and the Federal Reserve reported US capacities utilization declined to lower than expected 72.7% in March from 77%, while the industrial production fell 5.4% – the largest drop since 1946.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Agora Financial’s Byron King and John-Mark Staude of Riverside Resources offer their viewpoints on markets during the COVID-19 pandemic in this conversation with Maurice Jackson of Proven and Probable.

Maurice Jackson: Today, we will seek to discover the true price of gold and silver and prospect generators. Joining us for a conversation is Byron King of Agora Financial, along with Dr. John-Mark Staude of Riverside Resources Inc. (RRI:TSX.V; RVSDF:OTCQB). Gentlemen, I hope you both doing well.

Mr. King, I’d like to begin with you, sir. Bloomberg issued a press release recently that Bank of America expects gold to reach $3,000/ounce, which is a 50% increase from its record. In your opinion, is this a realistic number, or was Bank of America being far too generous or conservative?

Byron King: I think Bank of America is on track. I don’t think there’s any question gold will see $3,000. As with all things in life, it’s just a question of how long it will take.

But when you say that gold will be $3,000, that means that the U.S. dollar will be dropping in value relative to gold by quite a bit, about 50% from almost where it is now. So if it’s at $1,700 now, it has to move that extra $1,300 up to get to $3,000, which implies a decrease in value of the dollar relative to gold, because gold is the inverse of the value of the dollar.

Maurice Jackson: John-Mark, what are your thoughts regarding Bank of America’s gold price expectations?

John-Mark Staude: I agree with Byron. It’s always about time, but I’ve never seen so much creation of new money. COVID-19 has given an opportunity to pop bubbles that maybe already existed.

And now, I’m getting checks in the mail as a U.S. person for just breathing, and it’s pretty amazing. If I get free money, I don’t get free gold. So I see gold is a hard real asset that I think is worth a lot more money, and also it is very difficult to get it out of the ground and find it. So I think companies that have it or companies that can develop it are of great value.

Maurice Jackson: That’s a great perspective. They’re not getting free gold. I like that one. Byron, can you provide us with some insight as to what is going on in the precious metal space as a whole?

Byron King: In the precious metal space as a whole, plenty is going on. Demand is going up because you can view gold really as a barometer of people’s trust in government. And so when people distrust government, when they distrust the fundamental currency of their government, gold tends to go up.

In the gold space globally, in pretty much every currency of the world, gold has already set records. It’s setting record prices in euros, in Russian rubles, in Chinese yuan, British pounds, Japanese yen. The only currency that it hasn’t really broken through previous highs, and [set] a new record, is the U.S. dollar. And that has to do with the dollar’s role as the world’s reserve currency.

A lot of people across the world owe immense levels of debt, and the only way to pay that debt is to denominate it in dollars. They need to get dollars. So they’re selling stuff to move to dollars, so they can pay their debt. That’s one aspect of it. That’s the monetary aspect of it.

On the practical side of things, there’s immense demand for everything, from little one-ounce coins and what have you, that are practically sold out. The U.S. mint is charging $400, $500 premiums over spot for gold coins, all the way up to the big bullion bars that people traded internationally. Those have all sorts of shortage issues over the breakdown in global commerce. The fact that there’s very little airline trafficking to move gold from London to New York or from New York to Switzerland, or wherever, people are chartering airplanes, just to put a bunch of gold bars on the airplanes instead of people.

And then another angle you have to look at is that across the world, many, many minesgold mines specifically, but gold-silver, gold-silver-copper, copper-lead-zinc that has a gold offtake from itthose mines have throttled back. I think something like 30% of the world’s copper mining right now is either shut in completely or dramatically scaled back. And that is also reflected in gold mining, just because of mines that have issues with the virus problem, sick workers or they can’t get the fuel or the explosives or the chemicals, whatever they need, from the port up to the mine, just because of the roads are closed. You can’t travel.

Maurice Jackson: I think a lot of people are not considering the supply-chain constraints, when you’re discussing what’s going on in the space. And Mr. King, you’ve seen the up and down in the markets in the past. Is this one different in terms of the government devaluing the currency?

Byron King: I hate to say this time it’s different, but yeah, this time it is different. I’ve been around for a while, according to my driver’s license, and I’ve seen governments do really stupid things, monetarily, politically, economically, militarily, over the years. I’ve seen some really stupid things happen.

But right now, they’ve just basically opened the valves on the dam of stupid monetary and economic ideas. And it’s all being done out of true desperation. When we say, “Oh, the government’s sending checks out to everybody,” yeah, and they should, because we have 26 million people in the United States who are freshly unemployed, and we have to do something. The only idea that they can implement quickly is to send everybody a check and the heck with the monetary aspects.

I hope at some point things start to clear up and clarify and we can resolve and start to fix what’s broken. But man, oh man, this is a stupidity squared in terms of what governments ought to do versus what they are doing.

Maurice Jackson: We’ve discussed the price of bullion. What is your outlook on mineral exploration with an increase in gold and silver prices? And how do you see the summer and the latter part of 2020 going?

Byron King: Oh man, that’s about four or five questions here. How do I see the summer? First of all, in the company space, I see a lot of great companies, ranging from really big guysthe BHPs of the world and the Rio Tintosall the way down to small juniors, such as Riverside and many others; a lot of these companies from the small to the big, were smart enough and nimble enough to capitalize up in the last six or eight months in the lead-up to before the current calamity. So a lot of these companies have some money. But not just money, they’ve got people with ideas. And so, they have a drilling program, they have an exploration program, they have development programs.

So the companies that are well positioned to move forward will move forward to the extent that they can. It’s very much dependent on the jurisdiction. In Canada, for example, if you go to the Yukon, which is a very large mineral exploration area, it’s a 14-day quarantine. You don’t just fly up to Whitehorse, go visit a site, jump on the plane the next day or two and come back in. No, no, no. You go to Whitehorse, you’re going to spend 14 days in a hotel with them sliding pizzas under the door for you before you get to go to work.

And other places in the world have similar aspects. The thing is that once you’re there, once you’re on the ground, and you’ve got your teams and your crews, and if you can keep the bug out of your mining camp, you can explore, you can drill, you can map, you can do geophysics, you can do a lot of things.

You’ve got issues in terms of moving. Let’s say you drill some core, you crush it, you bag it and you send it to the lab. You’ve got just logistical issues in sending it to the lab, and the lab [in] turning it around. Maybe the lab is slow.

But I think there are a lot of exploration things that are happening and going to happen in the near term. In terms of who’s doing well: If you have an operating project, and you have the virus issues under control, you are making money hand over fist, and if you’re not, there’s something wrong.

If you have an operating gold mine that can either pour out the gold ore bars or come up with a concentrate or something, there’s a market for that as long as you can, again, logistically get it from where you are to where it needs to be. And that, again, has issues that have to do with aircraft availability, truck and driver availability. Oil is cheap, fuel is cheapif you can get it. If you’re in the wrong place and they can’t deliver the fuel from the terminal to the gas station and the fueling station, that makes a problem.

But that’s maybe a more detailed answer than you’re looking for that. That’s how I’m looking at the gold space. I have a very positive view of it, for the right companies with money and good management teams. And again, working in the right spots.

Maurice Jackson: John-Mark, Riverside Resources exemplifies many of the virtues that Mr. King just alluded to. How has Riverside prepared for the situation?

John-Mark Staude: We were lucky. We were already working virtually in terms of teams working offsite, and not a big office setting. Secondly, we have guys on the ground.

What Byron is saying is correct, that you have the 14-day quarantines. Well, we already have the team in place. In fact, right now some of those guys are still able to work in their local communities, and where they live and work is the project sites.

And a third thing is that we have big partners. Having a partner like BHP Billiton Ltd. (BHP:NYSE; BHPLF:OTCPK), as Byron said. . .[we are] in the field doing field work and doing programs and we’re delighted. We have regular meetings with them, all virtually, and we’re able to help the guys on the ground to do the programs.

Maurice Jackson: Byron, with a rising gold price, are more generalist investors basically taking notice and flowing into the mining space? And if yes, where is a good starting point for them to consider when looking for good value propositions and exploration?

Byron King: Well, the answer is yes. A lot of people were very badly burned with their traditional market investments up until late February, early March. And then, by mid-March, when the big crashes came, a lot of people watched their IRAs and their 401Ks just absolutely fall off of a cliff. And some people did the wrong thing; they sold at the bottom, just out of panic. There’s been some recovery, but a very significant recovery has happened in the gold and the gold-mining space.

If you’re new to the business, unless you really are a fast study, you want to be careful about getting into the junior mining space, if you don’t know what you’re doing. And I say that, with my dear friend John-Mark Staude here, who runs the junior mining company.

I don’t want to put words in your mouth, John-Mark, but I think you’d agree with me. If an investor out there doesn’t understand what this is all about, be very, very careful. It doesn’t mean don’t go into gold. Physical gold, if you don’t have some, get some. We’re just talking about $3,000 gold and it’s at $1,700. So in the sense that you can go to certain physical dealers and buy a coin or buy a small ingot, start to build your stash. That’s probably not a bad idea to preserve some wealth.

In terms of other things, there are mutual funds that focus on the gold mining space, some better than others. But a lot of those gold-mining-focused mutual funds have done very, very well. There’s oneI’ll just give you a symbol, it’s OGMIXit’s up 50% since March 18. It had a nasty crash to get there, but it’s recovered nicely.

There are many others though, some of the ETFs [exchange-traded funds] are pretty good. Anything with the name Sprott in front of itthe Sprott gold miners, Sprott junior gold miners[are] probably good way to get in there. There are the big minersBarrick Gold Corp. (ABX:TSX; GOLD:NYSE), Newmont Goldcorp Corp. (NEM:NYSE), those big names, if you want to pick stocks[are] companies that are probably going to do very, very well in the next few months, especially in rising gold prices. Or some of the royalty companies, and they range in size from really, really big guys, like Franco-Nevada Corp. (FNV:TSX; FNV:NYSE), to smaller guys, very well run, like Metalla Royalty & Streaming Ltd. (MTA:TSX.V; EXCFF:OTCQB), but [they are] terrific royalty companies.

Then you start to get into the intermediates, and then you get into the juniors. And if you’re not familiar with that space, that’s a very dangerous space to walk into because while there’s really a lot of upside on some of these risky plays, there’s a whole lot of downside too. When one says: “Oh look, it’s a $0.10 stock, how low can it go?” It can go to zero. It can go to $0.01. But at the same time, some of those $0.10 cent stocks are going to be $5 stocks too.

Maurice Jackson: Byron, you and I visited John-Mark in Mexico and reviewed some of Riverside’s property bank, and I’d like to find out from you, what do you recall from that experience?

Byron King: Oh, several things. First of all, visiting Mexico with John-Mark is worth the trip, just to spend time with John-Mark. I say this while he’s sitting here; I’m going to embarrass him. But he’s just a wealth of knowledge. He’s been studying Mexico. He’s been studying the Western U.S. for years and years and years. He doesn’t look nearly old enough to have done this, but it’s true. He did. So first of all, if you go on a field trip with John-Mark, you come back with a master’s degree in John-Markdom. And you are geologically much smarter than you used to be. That’s one of the things I remember.

Other things I rememberand we were talking about this before Riverside made their deal with BHP to become the exploration partner in Mexico for BHPJohn-Mark has this list of things, of names of places that are all worthwhile exploration opportunities or development opportunities.

I remember one particular one, just south of the U.S. border with Arizona. I’m in love with Cecilia, a beautiful place, gorgeous geologically situated. Other places, we were driving along this one area, going to this one exploration site. . .I’ll let John Mark tell the whole story. When you look out the window of the truck, as you’re driving along and bouncing around on this gravel road, the gravel is green, and you look down and you say, gee, why is the gravel green? He says, “Well, it’s because it’s made out of malachite, but not pure malachite. You’re driving over perfectly good ore to get to the exploration zone.” So right away I’m thinking, oh man, there’s something here.

So those are some of the things that I remember, it’s just John-Mark personally, John-Mark, professionally, some of these fabulous locales that he’s been able to stake out and claim for the company over the years. And now he’s partnered up with BHP, which has nice deep pockets to write big checks for good projects, of which there are many.

Maurice Jackson: John-Mark, what is the advantage that prospect generators, and in particular, Riverside Resources, have in the current climate of mineral exploration, and especially as it relates to COVID-19?

John-Mark Staude: Well, I think first thing is the prospect generators have a portfolio, so it’s not betting on one project. So, as COVID-19 and these other things were causing problems, they’re not necessarily homogeneous everywhere. And so, there’s opportunities.

I think the second thing for the prospect generator is, they’re usually partnered. As we’ve mentioned, we’re partnered with other companies, so we’re not going off their balance sheet.

The third thing is, they have quality projects, or projects that other people are funding and working on, so they must have something of interest to allow those people to wish them good. And so, they’ve done their due diligence.

But for us, we’ve been project generators working with Antofagasta Plc (ANTO:LSE), Cliffs Natural Resources Inc. (CLF:NYSE), Kinross Gold Corp. (K:TSX; KGC:NYSE), Hothschild, and now with BHP. So we have good projects and I think the opportunity is that, build a group that has good projects in this market, you have a really good chance for success.

Maurice Jackson: John-Mark, what are a couple of the key mineral exploration objectives Riverside is progressing during the COVID-19 social distancing?

John-Mark Staude: I think one of the key things is our spin out of Capitan Mining, which is going well. We actually had the AGM [annual general meeting], and now we’ve had the approval through the BC [British Columbia] courts. Now we’re working for the TSX listing and the financing. But gold price going up is really great, because that’s what Capitan is. It’s an open-pit gold project that Riverside owns. So that’s one of the big things we’ve been doing.

The other thing is working with BHP. On that, we’ve been able to move ahead with programs.

And the third is we’re working on some new deals. I think people at home has been great. You’re able to call them and do lots of business. Usually, it’s hard to catch people. They’re on planes or running around the meetings. We are able to have lots of meetings and go over data. Now, we’re able to do a number of term sheets. So we look forward to having more deals announced in the coming month.

Maurice Jackson: All right. In closing, Mr. King, what keeps you up at night that we don’t know about?

Byron King: Well, there’s a lot of doubt about where the economy is going. The virus is a medical issue. It’s an epidemiological issue. If you’ve paid the slightest bit of attention to it, you’ve probably gotten a lot smarter about biology and medicine and epidemiology than you were a month ago. I want to say that matter will resolve. I mean this is a bug. It is a virus. It’s not the world-killing plague that’s going to wipe out humanity or anything.

But it has accelerated a lot of trends that were sort of in motion that may have occurred, but now they’re all jamming us right in the faceeverything you can think of, from the idea that your local school is now online, colleges are online, the kids are home from school. It completely changed education. We’ve completely changed the idea that millions, tens of millions of people are working from home. That’s going to change the real estate business.

The idea that so much change is happening so quicklythere are so many unknowns and just pieces of fallout that are going to occur. And so, I think about where is all this going. Now, considering what I do with much of my timewhich is I spend my time doing geology, worrying about the minerals and mining businessI’m thinking about what does this mean in terms of mines and minerals? Does the world still need copper, gold, silver, lead, zinc, rare earth minerals, all these sort of things? Well, the answer is yes, it does.

And so the question is, how will the area that I am knowledgeable about. . .adapt? In terms of thinking about the future, I think these mining companiescompanies like Riverside, people like John-Mark, there are other companies out thereI want these companies to be successful. I want these gentlemen to succeed, and these gentleladies. There’s some women in the business too. I want these people to succeed. I want them to do well.

And the question is that, in the economy that has evolved, with millions of unemployed and the government just spending money like it’s the Niagara Falls of dollar bills or somethingwhat is all that going to do to the whole financial and economic underpinnings of what. . .what we do out there in the field, which is real science, real geology? This has to work, because a lot of the trends that were coming beforenot enough copper, not enough rare earth, not enough battery metals, technology metalsall those things are going to be there on the other side of this virus issue.

So in terms of myself, in terms of what I think about and worry about, I worry about that a lot. I do stay up late or wake up in the middle of the night, thinking about what’s the next idea here.

Maurice Jackson: John-Mark, what keeps you up at night that we don’t know about?

John-Mark Staude: What keeps me up at night is people are forgetting that we actually need to mine, and it’s a vital thing. I’m disappointed at certain jurisdictions for not allowing the mining to go forward because it is vital. And I think that’s something that we can do to produce resources for the planet that’ll make the planet stronger. And we definitely all need those to grow the economic rebound that we’re up for.

Maurice Jackson: Last question, Dr. Staude, what did I forget to ask?

John-Mark Staude: Oh, you’ve asked a lot. This is great. But I think one thing is, from Riverside’s standpoint is, we really look forward to talking to current and prospective shareholders. We invite you to visit our website, www.rivres.com.

Maurice Jackson: Mr. King, what did I forget to ask?

Byron King: Well, you know, [in a] very mercenary sort of way, you forgot to ask me what newsletter I write. And the answer to that is, I write a newsletter called Whiskey and Gunpowder. I work with a group called Agora Financial. And so you want to go to www.agorafinancial.com. It’s actually a free e-letter, so it doesn’t even cost you anything.

And then, on a more serious note, the one thing that we did not discussyou’ve got to keep an eye on the energy industry. Right now, there is a price war going on. Saudi Arabia has decided to flood the world with oil, where 200 million barrels [are] just floating around on tankers out there. Not long ago, we saw the price of oil go negative for West Texas Intermediate. The U.S. and Canadian energy industries are being completely, totally, utterly wrecked by this price war. And the longer it lasts, the more the carnage.

And what you want to be really careful about, and worry about to some extent, is what the global energy industry [is] going to look like on the other side of this current economic situation. Are we all going to go back to the good old days of relying on the Middle East for our oil?

And then, the other angle to this is the petrodollarthe U.S. dollar as the world’s reserve currencyis under extreme threat with the breakdown of international oil markets. Breaking down international oil is another way of breaking down the petrodollar. And when the petrodollar fails as a monetary instrument in the worldnotice I said when it fails because I’m not sure how you can fix it from herewe are in for a really wild ride.

If you think this wild ride is wild, the next wild ride can be worse, and that is why, to bring it all back, that’s why you need to have some gold. The gold is what is going to preserve your wealth through whatever rough seas lie ahead. And I’m pretty sure that there are some rough seas, and I’m pretty sure that they’re coming our way.

Maurice Jackson: And speaking of gold, before you make your next bullion purchase, contact me at (855) 505-1900 or email [email protected]. I’m a licensed representative for Miles Franklin Precious Metals Investments, where we provide a number of options to expand your precious metals portfolio from physical delivery to offshore depositories and precious metal IRAs. Finally, we invite you to subscribe to www.ProvenandProbable.com, where we provide mining insights and bullion sales.

Gentlemen, I’d like to thank you both for your time, and I look forward to speaking with you in the near future.

Maurice Jackson is the founder of Proven and Probable, a site that aims to enrich its subscribers through education in precious metals and junior mining companies that will enrich the world.

Disclosure: 1) Maurice Jackson: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Riverside Resources. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: Riverside Resources is a sponsor of Proven and Probable. Proven and Probable disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own shares of Riverside Resources, Franco-Nevada, Newmont Goldcorp and Metalla Royalty, companies mentioned in this article.

Disclosures for Proven and Probable: Proven and Probable LLC receives financial compensation from its sponsors. The compensation is used is to fund both sponsor-specific activities and general report activities, website, and general and administrative costs. Sponsor-specific activities may include aggregating content and publishing that content on the Proven and Probable website, creating and maintaining company landing pages, interviewing key management, posting a banner/billboard, and/or issuing press releases. The fees also cover the costs for Proven and Probable to publish sector-specific information on our site, and also to create content by interviewing experts in the sector. Monthly sponsorship fees range from $1,000 to $4,000 per month. Proven and Probable LLC does accept stock for payment of sponsorship fees. Sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

The Information presented in Proven and Probable is provided for educational and informational purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. The Information contained in or provided from or through this forum is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. The Information on this forum and provided from or through this forum is general in nature and is not specific to you the User or anyone else. You should not make any decision, financial, investments, trading or otherwise, based on any of the information presented on this forum without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available on or through this forum at your own risk.

During difficult times, we hope that everyone will pull together, keep calm, and work as a unit to ensure that society continues to run smoothly. Unfortunately, this is not always the case – as is particularly evident right now.

Toilet paper has reached incredible prices on eBay. Videos of supermarket brawls populate the internet. One man in Tennessee bought 17,000 bottles of hand sanitiser, hoping to sell them for a fat profit. In the UK, where I’m currently under lockdown, we are increasingly seeing bare shelves in store and huge online queues to order groceries by delivery.

But we are also seeing acts of kindness and benevolence – hospital doctors working long shifts to help treat ill patients, and social media campaigns to allow elderly, vulnerable individuals to have a dedicated hour to shop in supermarkets before they open. How can we explain these two approaches to crisis situations?

The decision of whether to buy supplies in a socially responsible manner, or to hoard them, is related to game theory. This approach is based around the understanding that our pay-off in some situations is based not only on what we do, but what on others do too. For example, getting the food we want from a supermarket is dependent on us and all (or most) other shoppers acting sensibly. If we decide to be socially responsible, that is of little effect if others decide to panic buy.

Social psychology research suggests that there are two main motives for “selfish” behaviour – greed and fear. When greedy, individuals are simply unconcerned with others and take what they want to benefit themselves. Fear is more complicated. In this case, individuals may wish to act in a socially-responsible fashion, but are concerned that others will not. If they shop sparingly and others hoard, they will be left with the worst outcome – the so-called “sucker’s payoff”. The belief that others are acting selfishly can often exacerbate those tendencies in others.

How to stop hoarding

So how can self-interest be reduced? Research suggests several ways in which socially-responsible behaviour – and the reduction of hoarding – might be encouraged.

One method may be to emphasise the feelings of kinship between shoppers. Perceiving others as similar to ourselves usually increases cooperation. Another is to play down the idea that everyone is panic-buying. Fewer newspaper articles highlighting bare shelves should lower concerns about getting the “sucker’s payoff”. And although acts of hoarding can lead to more hoarding, the opposite is also true. Acts of generosity can increase others socially minded tendencies and promote cooperation.

The extended nature of the situation should also be emphasised. When people believe they are in for the long haul, and may encounter the same people in the same situation again, they tend to be more socially responsible.

People tend to be more cooperative in small groups, especially with strangers. So, allowing small numbers of people into a place at once may help to reduce selfishness. Luckily, this is happening already thanks to social distancing rules. Promoting discussion and conversation often improves relationships amongst people in game theory-type situations. Although this may not be a very practical solution, perhaps the Blitz spirit of singing songs together could help with this – supermarket karaoke anyone?

Finally – and perhaps more drastically – we could introduce punishment for acting selfishly. Social sanctions – such as naming and shaming or ostracising those who hoard – can often be effective, but relies on the person caring about being shamed. Direct punishment – such as fines – can work, but only if it is strong enough to be a deterrent to others. Too weak a punishment can actually increase selfishness if individuals realise the cost/benefit analysis will work in their favour. It remains to be seen whether the regulations recently put in place in the UK banning groups of more than two people gathering in a public place will be strict enough to work as intended.

Unfortunately, it is the case that some people just don’t trust others or actually prefer to make sure that others get less than them. Little can be one about these ingrained personality traits. But, they are in the minority and over the coming weeks (or months) we will hopefully see that the human spirit is far stronger than a dangerous virus, even in the face of toilet paper shortages.

EURUSD rising despite drop in Ifo business sentiment index

Business sentiment in Germany deteriorated more than expected in April: the IFo business climate index dropped to 74.3 in April, after declining to 85.9 in March, when a drop to 79.8 was forecast. This is bearish for EURUSD but the technical setup is bullish for the pair.

The mighty Dollar was not so mighty on Monday as investors turned more positive amid plans to ease lockdown restrictions across the world.

The Greenback weakened against every single G10 currency, with the Dollar Index (DXY) slipping to a fresh one week look below 100.00 thanks to the renewed appetite for risk. Given how the DXY is coming under increasing pressure on the daily charts, a solid daily close below 100.00 could open the doors towards 98.90.

Alternatively, a technical rebound from 100.00 could inspire a move back towards 101.00 and 103.0.

Aussie explodes higher towards 0.6500

Appetite towards the Australian Dollar has jumped following positive news regarding the coronavirus developments in Australia.

The AUDUSD soared more than 1.5%, making the Australian Dollar the best-performing currency among its major counterparts today.

Looking at the technical picture, prices are bullish on the daily charts. A solid breakout above 0.6500 should trigger a move towards 0.6680. If prices are unable to break above the 0.6500 resistance, the next stop is south around 0.6270.

Same old story with British Pound

The fundamental drivers haunting investor attraction towards the British Pound remain intact.

Concerns remain elevated over the UK plunging into a coronavirus induced economic recession while there are many unanswered questions over Brexit. The British Pound is running on empty and running on fumes and running on borrowed time.

Looking at the technical perspective, the GBPUSD may approach 1.2500 in the short term as markets cheer Boris Johnson’s return to No 10 Downing Street. Should this level act as a stubborn resistance, prices could sink back towards 1.2200.

GBPJPY: Did somebody say breakout?

Over the past few weeks, the GBPJPY has traded within a wide 350 pip range with support at 132.00 and resistance at 135.50.

It looks like bears are winning the current tug of war with prices trading around the 133.00 level. Sustained weakness below this point should encourage decline towards 132.00. If this stubborn support level gives in, prices could tumble towards 130.20.

Commodity spotlight – Gold

It is no surprise that Gold has slipped amid the positive market mood. The metal has shed almost 1% today sinking towards $1715 and could extend losses if risk-on becomes the name of the game.

Looking at the technical, prices still remain bullish on the daily timeframe as long as $1675 proves to be reliable support. A technical rebound from the psychological $1700 level could spark a move back towards $1735 and $1750.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Facing what it said was “an increasingly severe situation” from the spread of the coronavirus, Japan’s central bank enhanced its monetary easing by boosting its purchases of commercial paper, corporate bonds, exchange-traded funds and real estate trusts, and will buy an unlimited amount of government bonds to ensure their yield remains around zero percent. The Bank of Japan (BOJ) slashed its outlook for economic growth and inflation, and now sees the economy shrinking between 0.4 percent and 0.1 percent in the current 2019 fiscal year, which began on April 1, and then shrinking a further 5.0 percent to 3.0 percent in fiscal 2020. “Japan’s economy is likely to remain in a severe situation for the time being due to the impact of the spread of the novel coronavirus (COVID-19) at home and abroad,” BOJ said. In January BOJ forecast growth of 0.8-0.9 percent in fiscal 2019 and then 0.8-1.1 percent in fiscal 2020. For fiscal 2021 BOJ sees growth of 2.8-3.9 percent and then 0.8-1.6 percent in 2022. In the fourth quarter of 2019 Japan’s economy contracted 0.7 percent year-on-year. BOJ added it “will not hesitate to take additional easing measures if necessary, and also it expects short- and long-term interest rates to remain at their present levels or lower levels.” While BOJ will continue with its current monetary policy framework of “quantitative and qualitative monetary easing (QQE) with yield cure control to boost inflation to its 2.0 percent target, there is still no prospect of meeting this target for the time being. Consumer price inflation in the current fiscal year is now seen averaging 0.6 percent, slightly below its January forecast of 0.6-0.7 percent, but in fiscal 2020 consumer prices are seen falling by 0.7-0.3 percent before rising to between 0.0-0.7 percent in fiscal 2021. In January BOJ forecast inflation of 1.0-1.1 percent in fiscal 2020 and 1.2-1.6 percent in fiscal 2021. For fiscal 2022 BOJ sees inflation of 0.4-1.0 percent. In March and February Japan’s inflation rate was steady at 0.4 percent. BOJ has used a combination of negative interest rates and “yield curve control” since September 2016 and will continue to apply a minus 0.10 percent interest rate on banks’ excess reserves. But its asset purchases, also known as quantitative easing, will expand greatly, and as far as Japanese government bonds, known as JGBs, it will be buying “a necessary amount of JGB’s without setting an upper limits so that 10-year JBB yields will remain at around zero percent.” It also decided to boost its purchases of commercial paper and corporate bonds to 7.5 trillion for each asset class from an earlier limit of 1 trillion, with the upper limit on outstanding holdings of 20 trillion. The additional purchases will continue until the end of September 2020. The amount of exchange traded funds (ETFs) and Japanese real estate trusts (J-REITs) to be purchased will rise to an upper limit of 12 trillion and 180 billion yen, respectively, from an earlier limit of 6 trillion and 90 billion yen. BOJ will also expand a special coronavirus fund set up in March aimed at facilitating corporate financing. The range of collateral will now include private debt, including household debt, of up to 23 trillion yen from an earlier 8 trillion, boost the number of eligible counterparties and a positive interest rate of 0.1 percent will be applied to the outstanding balances of the current accounts of financial institutions that equal their outstanding loans under this operation.

The Bank of Japan issued the following statement about “Enhancement of Monetary Easing” and a statement pertaining to its purchases of corporate bonds:

Japan’s economy has been in an increasingly severe situation due to the impact of the spread of the novel coronavirus (COVID-19) at home and abroad. Although policy responses taken by the government and the Bank of Japan have been exerting some positive effects, financial conditions have been less accommodative in terms of corporate financing, as seen in deterioration in firms’ financial positions.

Given these developments, the Bank judged it appropriate to further enhance monetary easing through (1) an increase in purchases of CP and corporate bonds, (2) strengthening of the Special Funds-Supplying Operations to Facilitate Financing in Response to the Novel Coronavirus (COVID-19), and (3) further active purchases of Japanese government bonds (JGBs) and treasury discount bills (T-Bills). The Bank will take these measures with a view to doing its utmost to ensure smooth financing, such as of financial institutions and firms, and maintaining stability in financial markets.

To this end, at the Monetary Policy Meeting (MPM) held today, the Policy Board of the Bank decided upon the following. (1) Increase in purchases of CP and corporate bonds The Bank decided, by a unanimous vote, to significantly increase the maximum amount of additional purchases of CP and corporate bonds and conduct purchases with the upper limit of the amount outstanding of about 20 trillion yen in total. 1 In addition, the maximum amounts outstanding of a single issuer’s CP and corporate bonds to be purchased will be raised substantially, and the maximum remaining maturity of corporate bonds to be purchased will be extended to 5 years (see Attachment).

1 The maximum amounts of additional purchases of CP and corporate bonds will be increased from 1 trillion yen to 7.5 trillion yen for each asset. Other than the additional purchases, the existing amounts outstanding of CP and corporate bonds will be maintained at about 2 trillion yen and about 3 trillion yen, respectively. The additional purchases will continue until the end of September 2020.

(2) Strengthening of the Special Funds-Supplying Operations to Facilitate Financing in Response to the Novel Coronavirus (COVID-19) With regard to the Special Funds-Supplying Operations to Facilitate Corporate Financing regarding the Novel Coronavirus (COVID-19), which was introduced and became effective in March, the Bank decided, by a unanimous vote, to (1) expand the range of eligible collateral to private debt in general, including household debt (from about 8 trillion yen to about 23 trillion yen as of end-March 2020), (2) increase the number of eligible counterparties (to mainly include member financial institutions of central organizations of financial cooperatives), and (3) apply a positive interest rate of 0.1 percent to the outstanding balances of current accounts held by financial institutions at the Bank that correspond to the amounts outstanding of loans provided through this operation. 2 The Bank decided to strengthen this operation with a view to firmly supporting financial institutions to further fulfill the functioning of financial intermediation for a wide range of private sectors, mainly in terms of firms. This operation has been renamed to the Special Funds-Supplying Operations to Facilitate Financing in Response to the Novel Coronavirus (COVID-19). In addition, with the aim of further supporting financing mainly of small and medium-sized firms, the chairman instructed the staff to swiftly consider a new measure to provide funds to financial institutions, taking account, for example, of the government’s programs to support financing such as those in its emergency economic measures, and report back at a later MPM (see Attachment for the outline of the measure).

(3) Further active purchases of JGBs and T-Bills In a situation where the liquidity in the bond market remains low, the increase in the amount of issuance of JGBs and T-Bills in response to the government’s emergency economic measures will have an impact on the market. Taking this into account, the Bank will conduct further active purchases of both JGBs and T-Bills for the time being, with a view to maintaining stability in the bond market and stabilizing the entire yield curve at a low level.

2 A positive interest will be applied from the May 2020 reserve maintenance period (from May 16 to June 15) onward. Twice as much as the amounts outstanding of the loans will continue to be included in the Macro Add-on Balances in current accounts held by financial institutions at the Bank. The Special Funds-Supplying Operations to Facilitate Financing in Response to the Novel Coronavirus (COVID-19) will be conducted until the end of September 2020.

4. The Bank decided to set the following guidelines for market operations as well as for purchases of exchange-traded funds (ETFs) and Japan real estate investment trusts (J-REITs). (1) Yield curve control (an 8-1 majority vote) [Note 1] The short-term policy interest rate: The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank. The long-term interest rate: The Bank will purchase a necessary amount of JGBs without setting an upper limit so that 10-year JGB yields will remain at around zero percent. While doing so, the yields may move upward and downward to some extent mainly depending on developments in economic activity and prices. 3

(2) Purchases of ETFs and J-REITs (a unanimous vote) The Bank will actively purchase ETFs and J-REITs for the time being so that their amounts outstanding will increase at annual paces with the upper limit of about 12 trillion yen and 180 billion yen, respectively. 4

5. The Bank will continue with “Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control,” aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner. It will continue expanding the monetary base until the year-on-year rate of increase in the observed consumer price index (CPI, all items less fresh food) exceeds 2 percent and stays above the target in a stable manner. For the time being, the Bank will closely monitor the impact of COVID-19 and will not hesitate to take additional easing measures if necessary, and also it expects short- and long-term policy interest rates to remain at their present of lower levels. [Note 2]

3 In case of a rapid increase in the yields, the Bank will purchase JGBs promptly and appropriately.

4 As for the guideline for purchases of ETFs and J-REITs, in principle, “the Bank will purchase these assets so that their amounts outstanding will increase at annual paces of about 6 trillion yen and about 90 billion yen, respectively. With a view to lowering risk premia of asset prices in an appropriate manner, the Bank may increase or decrease the amount of purchases depending on market conditions.”

6. The Bank recognizes that its current powerful monetary easing measures, including the ones decided today, will contribute to supporting economic and financial activities, coupled with various measures by the Japanese government as well as those by the government and central bank of each country and region in response to the spread of COVID-19. [Note 1] Voting for the action: Mr. KURODA Haruhiko, Mr. AMAMIYA Masayoshi, Mr. WAKATABE Masazumi, Mr. FUNO Yukitoshi, Mr. SAKURAI Makoto, Ms. MASAI Takako, Mr. SUZUKI Hitoshi, and Mr. ADACHI Seiji. Voting against the action: Mr. KATAOKA Goushi. Mr. Kataoka dissented, considering that it was desirable to further strengthen monetary easing by lowering short- and long-term interest rates, in response to a possible increase in downward pressure on prices and with the aim of alleviating firms’ and households’ interest burden. [Note 2] Mr. Kataoka dissented, considering that, given the severe impact of COVID-19, further coordination of fiscal and monetary policy was necessary and it was appropriate for the Bank to revise the forward guidance for the policy rates to relate it to the price stability target.

“Increase in the Maximum Amounts Outstanding of a Single Issuer’s CP and Corporate Bonds to Be Purchased as well as Outline of a New Fund-Provisioning Measure

Increase in the Maximum Amounts Outstanding of a Single Issuer’s CP and Corporate Bonds to Be Purchased

(1) The Bank will increase the maximum amounts outstanding of a single issuer’s CP and corporate bonds to be purchased from the current 100 billion yen to 500 billion yen and 300 billion yen, respectively.

(2) The Bank will increase the maximum share of the Bank’s holdings of CP and corporate bonds within the total amount outstanding of issuance by a single issuer from the current 25 percent to 50 percent and 30 percent, respectively.

(3) The Bank will extend the remaining maturity of corporate bonds to be purchased from the current 1 year or more and up to 3 years to 1 year or more and up to 5 years.

Outline of a New Fund-Provisioning Measure

(1) Amount of fund-provisioning The amount will be calculated based mainly on lending that eligible financial institutions conduct by making use of the government’s programs to reduce or exempt guarantee fees and interest rates of credit guaranteed loans, which are included in its emergency economic measures. Details including the range of lending will be considered later on.

(2) Method of fund-provisioning Loans will be provided against all pooled collateral.

(3) Loan rate The interest rate on loans will be 0 percent.

(4) Addition to the Macro Add-on Balances Twice as much as the amounts outstanding of the loans will be included in the Macro Add-on Balances in current accounts held by financial institutions at the Bank.

(5) Application of a positive interest rate to current account balances A positive interest rate of 0.1 percent will be applied to the outstanding balances of current accounts held by financial institutions at the Bank that correspond to the amounts outstanding of loans provided through this measure. www.CentralBankNews.info