Colombia’s central bank cut its rate for the second time this year to continue what it described as a “countercyclical drive of monetary policy” and said it would increase the amount of currency hedging by conducting new sales of U.S. dollars through forward operations for up to US$1 billion. The Central Bank of Colombia (CBC) cut its benchmark interest rate by another 50 basis points to 3.25 percent and has now cut it by 100 points this year following a similar cut in March. The rate cut was expected by analysts who expect the rate to be cut further to 3.0 percent by mid-year. In April 2014 CBC embarked on a tightening cycle, raising its rate 14 times by 450 basis points to 7.75 percent in July 2016. But in December 2016 it reversed course, lowering the rate 12 times until it paused in April 2018. The rate cut in March this year was the first cut since then. In today’s statement, CBC said it would also continue to hold foreign exchange swaps for up to US$400 million. Earlier this month the International Monetary Fund (IMF) forecast Colombia’s economy, which remained resilient last year with growth of 3.3 percent, would contract 2.4 percent this year due to the disruptions from the Covid-19 pandemic and lower oil prices. This would be Colombia’s first economic recession since 1999. Growth in 2021 is expected to rebound and remain around 3.5 percent over the medium term, supported by domestic demand. Colombia’s peso fell sharply at the start of March but has stabilized since then and was trading around 3,958 to the U.S. dollar today, down 17 percent this year.

SmileDirectClub shares traded 20% higher after the company reported it has been awarded a U.S. patent for its SmileShop retail concept and treatment process and that it plans to reopen stores on a rolling basis starting in May.

SmileDirectClub Inc. (SDC:NASDAQ) today announced “it has been issued a patent for its SmileShop intellectual property from the U.S. Patent & Trademark Office which further strengthens the telehealth dentistry pioneer’s efforts to bring affordable, accessible oral care to more people through its unique and innovative teledentistry platform and direct-to-consumer business model.” The firm claimed that the patent will prevent other clear aligner competitors from duplicating its business model for the next 18 years.

The company’s CEO David Katzman commented, “This patent designation is a significant validation of our unique customer-oriented care model, and expands our category ownership, including the manufacturing and retail experience…As the industry pioneer and inventor of the SmileShop concept, this patent is recognition that SmileDirectClub offers an innovative way for consumers to access oral care that is safe, doctor-directed and convenient. We look forward to welcoming customers back to our SmileShops at the earliest and safest possible time.”

“We are focused on the entire teeth straightening and care process, and we now own the manufacturing process of our clear aligner products, the customer experience via our teledentistry platform, as well as the retail experience for clear aligner therapy. This patent is another step in our process as we continue to grow and protect our business,” Katzman added.

The firm advised that “the patent encompasses the unique SmileShop concept and process” which includes appointment scheduling, conducting an intraoral scan, generating an approved treatment plan by a licensed dentist or orthodontist and then creating and shipping the aligners to the customer. The company noted that so far more than one million customers have used its clear aligner therapy platform.

The company stated that it is planning to slowly reopen its SmileShops in the U.S. and other markets starting in May as local governments begin to lift business restrictions. The firm indicated that it will be supplying all of its SmileShop team members with face shields and other PPE and will institute staggered appointment times, temperature scans and other social distancing and sanitary measures to provide a safe experience for all staff and customers.

SmileDirectClub is an oral care company headquartered in Nashville, Tenn. The firm stated that it is the creator of the first direct-to-consumer medtech platform for teeth straightening. The company has since expanded its business and now offers its products directly through dentist and orthodontists’ offices. Some of the products offered by the company include aligners, impression kits, retainers and whitening gel. In addition to the U.S., the company also operates in Australia, Canada, Germany, Hong Kong, Ireland, New Zealand and the U.K.

SmileDirectClub began the day with a market capitalization of around $2.1 billion with approximately 385 million shares outstanding and a short interest of about 10.4%. SDC shares opened more than 26% higher today at $6.76 (+$1.37, +26.42%) over yesterday’s $5.39 closing price. The stock has traded today between $6.13 to $6.80 per share and is currently trading at $6.64 (+$1.25, +23.14%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

Shares of Chimerix Inc. traded higher after the company reported it has received U.S. FDA clearance to initiate a Phase 2/3 Study of dociparstat sodium in acute lung injury for patients afflicted with severe COVID-19.

Biopharmaceutical company Chimerix Inc. (CMRX:NASDAQ), which focuses on developing medicines to treat cancer and other serious diseases, today announced that it will initiate a Phase 2/3 study of dociparstat sodium (DSTAT) in COVID-19 patients suffering from acute lung injury (ALI).

The firm explained that “DSTAT is a glycosaminoglycan derivative of heparin with robust anti-inflammatory properties, including the potential to address underlying causes of coagulation disorders with substantially reduced risk of bleeding complications compared to commercially available forms of heparin.“

Joseph Lasky, M.D., Professor of Medicine, Pulmonary and Critical Care Section Chief, John W. Deming, M.D. Endowed Chair in Internal Medicine at Tulane University Medical School commented, “Given the severity of the COVID-19 pandemic, we have evaluated many potential targets to address the clinical manifestations associated with severe COVID-19…Based on the literature, we believe DSTAT has the potential to reduce the excessive inflammation, immune cell infiltration and hypercoagulation associated with poor outcomes in patients with severe COVID-19 infection.”

The company’s CEO Mike Sherman remarked, ” DSTAT is well-suited to unlock the anti-inflammatory properties of heparin as it may be dosed at much higher levels than any available form of heparin without triggering bleeding complications…We had planned to evaluate DSTAT in several indications of high unmet need, including ALI from different causes. The pandemic intensified our focus on ALI associated with COVID-19. Our team has worked closely with critical care physicians treating COVID-19 patients and with the U.S. Food and Drug Administration (FDA) to develop a Phase 2/3 protocol to determine if DSTAT can reduce the need for mechanical ventilation and improve the rate of survival in patients with severe COVID-19 infection.”

The company outlined its plans for the study indicating that it will be a randomized, double-blind Phase 2/3 trial to determine the safety and efficacy of DSTAT in adults with severe COVID-19 who are at a high risk of respiratory failure. The study subjects will be confirmed COVID-19 patients who require hospitalization and supplemental oxygen therapy. The primary endpoint established in the study is the percentage of subjects who survive and do not require mechanical ventilation through 28 days. Several secondary endpoints listed include time needed for showing improvement, time to hospital discharge, time to resolution of fever, number of ventilator-free days, all-cause mortality and changes in several key biomarkers.

The study will begin by enrolling 24 subjects in Phase 2 to first establish dosage levels and then expand to 74 total patients. The firm advised that if Phase 2 results are positive, it would enroll approximately 450 subjects in the Phase 3 portion of the study.

The company reported that “the clinical manifestations of COVID-19 range from mild, self-limited respiratory tract illness to severe alveolar damage and progressive respiratory failure, multiple organ failure, and death. Mortality in COVID-19 is associated with severe pulmonary disease and coagulation disorders such as disseminated intravascular coagulation.” The firm indicated that the mechanisms of action of DSTAT may address overactive inflammatory response including underlying causes of blood coagulation disorders associated with COVID-19.

Chimerix is a development-stage biopharmaceutical company based in Durham, N.C. which is engaged in advancing medicines in the areas of cancer and other serious diseases. The company listed that it presently has two active clinical-stage development programs. The first is dociparstat sodium (DSTAT) which is a glycosaminoglycan compound derived from porcine heparin that has low anticoagulant activity. The second pipeline candidate is brincidofovir (BCV) which is an antiviral drug being developed as a medical countermeasure for smallpox.

Chimerix began the day with a market capitalization of around $93.2 million with approximately 61.74 million shares outstanding. CMRX shares opened 30% higher today at $1.97 (+$0.46, +30.46%) over yesterday’s $1.51 closing price. The stock has traded today between $1.82 to $2.62 per share and is currently trading at $2.27 (+$0.76, +50.33%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. 6) This article does not constitute medical advice. Officers, employees and contributors to Streetwise Reports are not licensed medical professionals. Readers should always contact their healthcare professionals for medical advice.

The interesting quandary is over 17 million warrants at $0.14, well in the money. They are two-year warrants but have a potential acceleration clause if the share price closes over $0.25 for over ten days. It’s been above $0.25 just recently so that is not an out of the question alternative.

While the liquidity of the shares has gotten a lot better over the last ninety days, if 17 million shares were dumped on the market over a thirty day period to exercise the warrants, the stock would head right back down to $0.14 a share. Then everyone would hate the company. Including me.

I talked to management recently about their plans for the 2020 work season after they put out a press release a month ago. Their prime focus naturally is on the high-grade million ounce plus deposit at Fondaway Canyon. The intention is to put all of their data together to totally reevaluate the resource and future plans including a PEA. There was about 2,500 meters of drilling from the 2017 program that were not included in the 2017 43-101 resource.

I asked about the $0.14 warrants because there are so many of them. And some are being exercised now reducing the overhang but almost all are in really strong hands. Management is fine for cash for now. The warrants would bring in an additional $2.38 million so there is almost a zero chance of a financing any time soon.

I got the impression that the company can go to a few of the strong hands holding the warrants and ask for cash any time they need it. I don’t see them needing that kind of money any time soon but it is there for the asking when they will want it. So I really doubt investors have to worry about the company dumping warrants onto the price.

Given the 1.06 million ounce 43-101 resource at over 6 grams and a theoretical exercise of all 28 million warrants the company would have about $6 million in cash and just over 85 million shares outstanding. With a share price today of $0.19 CAD that gives a market cap of about $17 million CAD or $12 million in US pesos. Again, using US pesos because after all we are talking Nevada, the rock in the ground is over $330 a ton. Someone is going to want to mine that one day soon.

I don’t know many companies with US projects are selling at a price of under $12 an ounce of high grade gold in USD. That is not going to last for long, warrants or not.

Getchell did a great deal with perfect timing. The idiots in the Fed have guaranteed that resources are going to be the last game in town. Investors have no idea of what a zero brainer investing in gold and silver will prove to be. When I saw oil down to a negative $37 one day last week, all I could think about was the $650 trillion in derivatives blowing sky high and neither Wall Street nor Washington see it coming.

One day, not next week or even perhaps next month, you will see gold up $100 in a day. Fasten your seat belts; there is no bull market like a gold bull market.

I owned shares in Getchell before they did this deal in Nevada. I participated in the latest PP and the company is an advertiser. Naturally that makes me biased. Do your own due diligence. It is will worth your time to go through their excellent presentation. They have four other gold, silver and copper projects in Nevada.

Robert J Moriarty President: 321gold Archives 321gold

Bob Moriarty founded 321gold.com, with his late wife, Barbara Moriarty, more than 16 years ago. They later added 321energy.com to cover oil, natural gas, gasoline, coal, solar, wind and nuclear energy. Both sites feature articles, editorial opinions, pricing figures and updates on current events affecting both sectors. Previously, Moriarty was a Marine F-4B and O-1 pilot with more than 832 missions in Vietnam. He holds 14 international aviation records.

Disclosure: 1) Bob Moriarty: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Getchell Gold. My company has a financial relationship with the following companies mentioned in this article: Getchell is an advertiser on 321 Gold. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Getchell Gold, a company mentioned in this article.

April marks a second month of truly extraordinary developments in markets – from negatively priced crude oil futures to a record spike in unemployment claims to a lockdown-defying rally in stocks.

The financial media is touting the S&P 500’s surge of more than 13% in April – the biggest one-month gain for the index since 1974.

While stock market investors have made up a big chunk of their 2020 losses, the major averages and nearly all sectors within them are still down significantly for the year.

One exception is the mining sector. The GDX Gold Miners ETF (NYSE:GDX) exploded 42% higher in April to make fresh new 7-year highs.

For the first time in a very long time, mining stocks are showing leadership. That has profound implications for precious metals markets.

For one thing, it suggests that gold and silver are back in favor as alternative, non-cyclical, safe-haven asset classes. Oftentimes during a major rally in the broad equities market, precious metals and mining shares get left behind – or even sold off.

Not during these times. Gold itself rallied to a multi-year high of $1,775/oz mid-month before taking a breather. A break from its current consolidation pattern to the upside would likely entail a run toward gold’s former all-time high above $1,900.

Relative strength in the GDX compared to gold has persisted throughout the month, which suggests mining stock investors are anticipating further upside in gold.

There is plenty of technical and fundamental evidence to support the thesis that gold is in a major bull market versus all fiat currencies and that it will soon trade up to new record highs in U.S. dollar terms.

The monetary backdrop has never looked worse for holders of U.S. dollars.

Interest rates have been pushed down toward zero at the same time as the Federal Reserve has embarked on an infinite asset-buying campaign.

At this week’s policy meeting, the Federal Open Market Committee pledged to maintain interest rates near zero for as long as necessary.

Policymakers also vowed to keep using any and all available tools to support the economy, which is currently contracting at a double-digit rate amidst nationwide COVID-19 lockdowns.

Fed Chairman Jerome Powell said the central bank is prepared to use its powers to push even more stimulus into the economy and “will do it to the absolute limit of those powers.”

The ultimate consequences for inflation are difficult to predict and won’t become clear until after the economy is allowed to begin functioning again.

The potential exists for a lot of pent-up demand to be unleashed and a lot of newly created Federal Reserve notes to push consumer and commodity prices sharply higher.

So far this year, gold has gained less on inflation fears and more on fears that everything else is at risk of collapsing. That showed up quite clearly in the gold:silver ratio spiking to over 125:1 in March – a mountainous peak never previously reached in modern recorded history.

The ratio didn’t come down as much in April as might have been expected given the rapid unwinding of the fear trade in the stock market and the upside breakout in high-risk mining equities. The gold:silver ratio closed Wednesday at 112:1 – still an extraordinarily wide spread between the two money metals.

A narrowing in favor of silver seems inevitable over time (years ahead). But as long as we remain in a crisis environment with an intentionally stunted economy, the gold:silver ratio can remain stubbornly elevated.

A major component of silver demand comes from industry, and much of the world’s industrial productive capacity has been taken offline.

At the same time, nearly half of the world’s silver mines have been shuttered during this crisis.

Even though the industry is contracting, investors are apparently optimistic that it can also become more profitable. Lower energy costs plus higher metal prices could certainly do the trick.

The mining sector as a whole has been forced to drastically decrease its production volumes instead of stupidly selling as much as it can at ridiculously low prices. In other words, it has been forced to adopt sound business practices in spite of its own apparent natural inclination to do otherwise!

Better profit margins and diminished output should bode well for both mining equities and the metals themselves.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Governments are being asked to do the near impossible: to deliver on both health and the economy. In many circumstances doing both at the same time would be completely impossible. But fortunately in Australia we have separate instruments we can use to target separate goals.

The health objective is to minimise the number of lives lost and keep the spread of the virus low enough to not overwhelm the health care system. Until there is a vaccine we will need to keep in place many of the current restrictions, including bans on large gatherings and international travel.

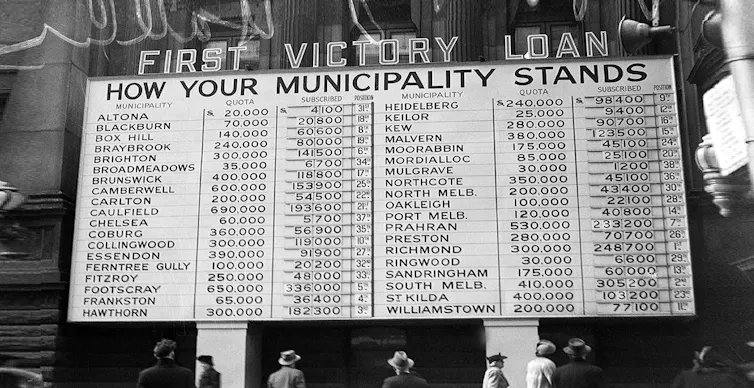

Tally boards publicising the contributions of different suburbs during the second world war. Australian War Memorial

The economic objective can be assisted by relaxing other restrictions, such as those on the maximum number of people who can gather in one place, alongside careful monitoring and a readiness to reimpose them where needed. But any relaxing of restrictions won’t be anywhere near enough to restore the economy to its full health.

Why we’ll need more stimulus

That’s where Australia’s two separate tools come in. Restrictions are (for now) the primary means of maintaining health.

Huge government spending is the primary means of fending off massive unemployment and a recession worse than any since the Great Depression.

Treasury Secretary Stephen Kennedy acknowledged the scale of what we are facing on Tuesday, telling a Senate committee Australia had “never seen an economic shock of this speed, magnitude and shape.”

Even if we lifted all of its restrictions right now, demand for our exports would remain at global recession levels, pushing our economy backwards.

Adding to the case for enormous extra spending is the additional reality that business cycles are almost always asymmetric: the output lost in a recession isn’t regained in the recovery.

To allow a big recession is to permanently alter our standard of living, and possibly our future growth path; all the more so in downturns caused by pandemics which have been linked to a long-lasting increase in precautionary saving.

Fortunately, fiscal stimulus has been shown to be at its most effective when the economy is massively under-utilising its resources, as it is now.

JobKeeper is a placeholder

The bridging measures undertaken by the government, including JobKeeper, will be critical for mitigating the severity of the recession and maintaining a platform for recovery.

But they will only mitigate the severity of the recession. They won’t avoid it. In common language, they are not “stimulus” measures, but measures that will merely maintain (some of) the status quo.

Even with them, it is entirely reasonable to expect the unemployment rate to climb into double digits as 15-20% of the workforce lose their jobs.

Australia is in the fortunate position of being able to spend big in part because of its prudent policy during the good times and in part because of its comparatively good trade prospects once the global recession is over.

And Australia is able to borrow at historically low levels. The Commonwealth government can issue 10 year bonds or longer at an annual interest rate well below 1%.

This means that even A$1 trillion of extra spending (more than one half of Australia’s annual gross domestic product) would carry a price tag of $10 billion a year or about $400 per person.

As the economy grows, partly as a result of this extra spending, net debt will shrink as a proportion of gross domestic product, just as it did after the second world war.

Crucially, it won’t need budget surpluses to do this, just as net debt withered after the war, even though the budget remained in deficit.

Our government went into this crisis with ample capacity to conduct large scale fiscal stimulus, having one of the lowest net debt to GDP ratios in the developed world – just short of 20%.

Err on the high side

But the scale of the stimulus that will be needed is gargantuan, and it will be better to err on the high side – at least 15-20% of GDP per year, for two to three years.

Anything less runs the risk of a debt-default deflationary spiral of the kind seen in the Great Depression, when the ability of households and businesses to pay their debts decreased with deflation and the resulting defaults led to further deflation.

If stimulus is big enough to be successful, financial markets will understand that debt issued by the Commonwealth will ultimately be backed by a higher GDP.

It will be important to signal in advance that the stimulus measures will be in place by the time JobKeeper ends (currently September). The forward guidance should emphasise that the measures will remain well into the recovery and not end at the first sight of it.

The early measures should focus on boosting the capacity of the economy to make it better able to withstand future pandemics.

Examples include

improving the national broadband network, with a focus on reducing outages and building infrastructure that will allow homes to act as offices, especially in higher density areas

improving the ability of Australian Post to deliver physical items to households, and the ability of ports and road transport to get things to where they are needed

building and encouraging the use of the robust technologies that will be needed to ensure keeping the spread of this virus and others low

labour intensive programs that boost improve local environments, everything from tree planting and waterway cleanups to cycle path construction and dune repair

online delivery for universities, including investment in materials for overseas students who will be given a commitment to be allowed to travel to Australian campuses once restrictions are removed

making Australia a world leader in the remote delivery of arts in a way that makes Australian culture available worldwide, and also a world leader in the local delivery of art via labour-intensive public art works

The general point, more important than the specific examples, is that there is a lot of infrastructure that can be created even the under current circumstances.

And consider war bonds

In normal times it might make sense to develop this infrastructure privately or through public-private partnerships, but in the present crisis it can only be done publicly on the scale that is needed. The Australian government has the capacity to do it.

The best way to make that clear would be a set of separate accounts for the emergency, offset by the issuing of long-term “COVID bonds” at low interest rates, much like the war bonds Australia issued during the second world war.

The bonds would allow visibility into the extent to which the Commonwealth government remained prudent in other spending and would use a precedent already established in making a distinction between spending for investment and spending for consumption.

A broad take-up could also engender the political support needed to extend JobKeeper to more than one million casual workers, and temporary visa holders and students.

Denying people who could contribute to Australia’s economic recovery the opportunity to do it risks denying Australia the resources it will need when the crisis is over.

Announcing these programs as soon as possible and providing guidance on the scale and duration of the planned spending will help prevent further declines in economic activity right now.

The government is delivering an economic statement in a fortnight, on May 12. It would be the right day to start.

USDJPY falls on better than forecast Japanese data

Japan’s industrial output fell less than forecast in March: industrial production fell 3.7% in March following 0.3% decline in February when a 5% drop was expected. This is bearish for USDJPY.

As the coronavirus pandemic has accelerated the move to telemedicine, two investment professionals are following CloudMD, a small cap rapidly expanding in Canada.

As people are avoiding going to doctor’s offices and hospitals during the coronavirus pandemic, telemedicine has taken off. Two investment professionals, Bruce Campbell and Keith Schaefer, have called CloudMD Software & Services Inc. (DOC:CSE; DOCRF:OTCQB; 6PH:FSE), a small-cap Canadian telemedicine firm, a top pick.

Bruce Campbell, founder and portfolio manager of Stonecastle Investment Management, spoke about CloudMD on April 27 on BNN:

“The first top pick is CloudMD Software, a technological medical play. We’ve tried to look at opportunities that are really going to be able to take advantage of Covid and this is one of the ones that we think is; what they do is telemedicine.

“The jumping off point for TeleHealth is here and I think CloudMD is the best pure-play TeleHealth stock right now.” – Keith Schaefer

If you look back at a year ago, where everyone had to go to the doctor, and now all of the different provinces have opened up billing codes, so that now we don’t have to go into a doctor’s office. We can do a virtual doctor’s visit and the doctor gets paid just like they do with an in-house appointment. Obviously with everything that has happened with this crisis, people really don’t want to go into a doctor’s office and they need a prescription renewal or something like that.

If you look at CloudMD’s peers in the U.S., there is a company called Teladoc, which is a big U.S. company that does the same thing. Obviously, the size of the market is different, but the multiple it trades at is multiple times higher than where CloudMD is.

CloudMD is just starting to gain adoption. They started off here in BC, they have moved to Ontario, and they are going to be rolling out really across the country, so tons of opportunity for a company like this. They will probably change the way that we view our doctor and our healthcare visits going forward.”

Keith Schaefer, editor and publisher of Oil & Gas Investments Bulletin, is also following CloudMD, and wrote:

“An entirely newand highly profitableindustry is being borne out in 2020TeleHealth. CloudMD Software & Services Inc. (DOC:CSE; DOCRF:OTCQB; 6PH:FSE) is my favorite way to play TeleHealth. It’s growing quickly with over 100,000 patients registered on its app and over 3000 doctors in 8 provinces in its Electronic Medical RecordsEMRsystem. It has MULTIPLE revenue streams and it just moved into Canada’s largest marketOntariosetting up an even faster growth rate.

The recent spread of coronavirus is only accelerating this. Covid-19 has forever changed how we all will think about visiting a hospital or seeing our doctor. We really don’t want to do that at all, if possible. It will have a very positive and long lasting impact on TeleHealth.

TeleHealth companies in Canada are getting paid more money for services than bricks-and-mortar clinics, and have a fraction of the costs. Doctors want more of it, patients want more of it, government wants more of itand the Market REALLY wants more of it. Everybody wins here; there is no downside.

The rapid scale-up and profitability is key for investors.

CloudMD is established, growing quickly and trading at a fraction of its peers. The average multiple of competitors in the sector trade at 5-7x revenue, and CloudMD is trading way below that at 2.5x per revenue. But realize that the Canadian use of telemedicine is still just a fraction of where it is in the U.Sso the quick, early upside is even bigger.

The market desperately wants to own TeleHealth right now. I see CloudMD as the best way to do that in the junior sector (where the leverage is!).

For this stock to have a major run all that needs to happen is for institutional investors to wake-up to the fact that the company exists. That’s happening now with the company entering the province of Ontariowhich has 14.5 million peopleover one-third of Canada’s population.

CloudMD is a fully integrated health care companykind of like a hospital-in-the-sky. They do have five bricks-and-mortar clinics, but they also own their own EMRElectronic Medical Recordssystem that operates in eight provinces and is used by over 3,000 doctors and is supported by an in-house 25 person development team. They have their own CloudMD appwhich has over 100,000 registered patients already.

The EMR gives CloudMD a recurring monthly revenue stream, which The Street loves. The app gives them high-margin fees from doctors, specialists and groups like massage therapists & counselors. These people are revenue, not costs. As I said, full hospital-in-the-sky. Multiple revenue sources with lower costs.

To schedule a virtual doctor’s appointment all that a patient has to do is download the free CloudMD app and then arrange an appointment with one of the doctors. There is zero charge for the patient and they can see a doctor very quickly.

CloudMD can scale up the number of patients VERY quicklyand they are. Every aspect of healthcare that’s very fractured and disjointed will now be in the one CloudMD ecosystem. Everyone wins with this system. Patients, doctors, the medical system, society, even investors. Everyone.

Doctors who have signed up with CloudMD work remotely from home or wherever they are (like their winter home down south). The rapid scale-up potential excites me. CloudMD can add in unlimited number of doctors and patientsso it has a virtually unlimited ability to scale quickly with little incremental cost.

Profit margins are wide and there is no cap on the number of customers that can be handled.

After a patient has an appointment, CloudMD bills the government directly just like every bricks-and-mortar clinic in Canada does. CloudMD records 100% of the revenue and gets to keep 30% of the billing for every patient that is seen through telemedicine, which is actually 10% more than what a bricks-and-mortar clinic receives. That is because the governments are trying to push TeleHealth. The doctor gets the other 70% and doesn’t have to deal with any headaches of commuting or running a business.

Without the overhead of a bricks-and-mortar clinic, AND more revenue, CloudMD will be much more profitable than traditional healthcare stocks. Faster scale, more cash flow. And they just entered Canada’s largest market. This is the right stock in the right market at the right time. That’s the great thing about this business model. It’s very scalable, very easy, and it grows very quickly.

CloudMD has been growing its recurring SAAS (Software-as-a-Service) revenue by 30% YoY with its EMR system. But this year the company is expecting that doctor growth to be much much higherwith a new full time sales team and the coronavirus pandemic. SaaS revenue is highly lucrative!

The jumping off point for TeleHealth is here and I think CloudMD is the best pure-play TeleHealth stock right now.”

Disclosure: 1) Keith Schaefer: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: CloudMD. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: CloudMD. My company has a financial relationship with the following companies mentioned in this article: None. Additional disclosures are listed below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. As of the date of this article, an affiliate of Streetwise Reports has a consulting relationship with CloudMD. Please click here for more information. An affiliate of Streetwise Reports is conducting a digital media marketing campaign for this article on behalf of CloudMD. Please click here for more information. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of CloudMD, a company mentioned in this article.

Additional Disclosures

Keith Schaefer Disclosures: CloudMD has reviewed and sponsored this article. The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom. Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter.

Keith Schaefer is not registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. He is also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.

Bruce Campbell, Stonecastle Investment Management: A guest firm/affiliate holds a position in CloudMD. There is no guest position held, members of his household do not hold positions and CloudMD is not an investment banking client.

By Jameel Ahmad, Global Head of Currency Strategy and Market Research at FXTM, ForexTime

The final trading day of April is seeing investors take profit from stock market positions that have suprisingly noted advances in major indexes throughout the month. One of the trends that the risk-off mood is bringing to trader sentiment, is a weaker Euro senitment and this is something that has not been helped from another horrifying economic release today. Data showed that the Eurozone economy shrank at the sharpest pace on record during the first quarter with an estimate between January-March showing a contraction in economic activity of 3.8%.

ECB President Largade has also made depressing headlines while the European Central Bank left policy unchanged with a warning that the EU economy could shrink by as much as 12% this year.

As a result of the weak Euro sentiment, we have seen some drops today in both the EURGBP and EURUSD.

(EURGBP Daily Chart FXTM MT4)

Should the sentiment for the Euro remain weak while the GBP maintains a more stable footing, further declines in EURGBP can be possible. Should the pair decline below 0.8669, potential areas of interest can become the 5 March low at 0.8620 and even potentially the 2 March low at 0.8593.

The EURUSD is also showing some indications of a move lower ahead, although the current indifferent sentiment that traders are showing towards the USD might prevent volatility in the EURUSD. The pair is trading around 1.0862 at the moment, and I would prefer to see a move below 1.0832 and even the April 29 low at 1.0817 to open up the possibility that the Eurodollar can potentially decline even further than 1.08 as May begins. However and with the USD remaining fragile, one can not dismiss the prospects of an unexpected move higher in the EURUSD closer to 1.09.

(EURUSD Daily Chart FXTM MT4)

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Rwanda’s central bank cut its Central Bank Rate (CBR) by 50 basis points to 4.50 percent to “mitigate the shock on the Rwandan economy” by further loosening monetary policy, ease liquidity conditions in the banking sector and support a recovery of the economy. It is the first rate cut by the National Bank of Rwanda (NBR) this year and only the second since December 2017 following a similar-sized rate cut cut in May 2019. “Considering that inflation is projected to decelerate in the second half of 2020, owed to a drop in aggregate demand, the MPC (monetary policy committee) decided to cut the Central Bank Rate (CBR) from 5.0 percent to 4.5 percent,” NBR said. It added the expected decline in inflation points “out the need for policy measures to support aggregate demand in the economy.” Last month took several initiatives to help mitigate the economic impact from Covid-19, including NBR injecting 23.4 billion Rwandan franc into the banking system by lowering the reserve requirement ratio by 100 basis points to 4.0 percent, setting up a lending facility of 50 billion francs and easing prudential requirements to temporarily allow banks to restructure outstanding loans by borrowers that are facing cash flow challenges. As of April 10, banks had restructured 7,952 loans, worth 255 billion francs, NBR said. “The global economic. disruptions caused by the COVID-19 pandemic are weighing on Rwanda’s economy,” the central bank said, adding the outbreak of the virus had led to a significant slowdown in the services and industry sectors after a strong performance in the first two months of the year. Demand for loans has also fallen, with new authorized loans down by 10.6 percent in the first quarter. The trade deficit has also worsened by 18.8 percent in the first quarter due to higher imports compared with exports. However, NBR said the government’s policy measures to help raised demand for credit after the virus subsides, contributing to a reduction in the trade deficit and a stable foreign exchange. Inflation in the first quarter of 220 was 8.2 percent, mainly due to higher food and energy prices, but inflation in now expected to decelerate to an average of 6.0 percent for the year and 1.0 percent in 2021, respectively. Earlier this month the International Monetary Fund approved the disbursement of $109.4 million to help meet Rwanda’s balance of payment needs as the pandemic has ground the economy to a halt. “A temporary widening of the budget deficit is appropriate to mitigate the health and economic impact of the pandemic,” the IMF said, adding once the crises abates, the fiscal adjustment path should be adjusted to preserve debt sustainability in the medium term. It added that monetary policy should be data driven and NBR should stand ready to provide additional liquidity support if needed.