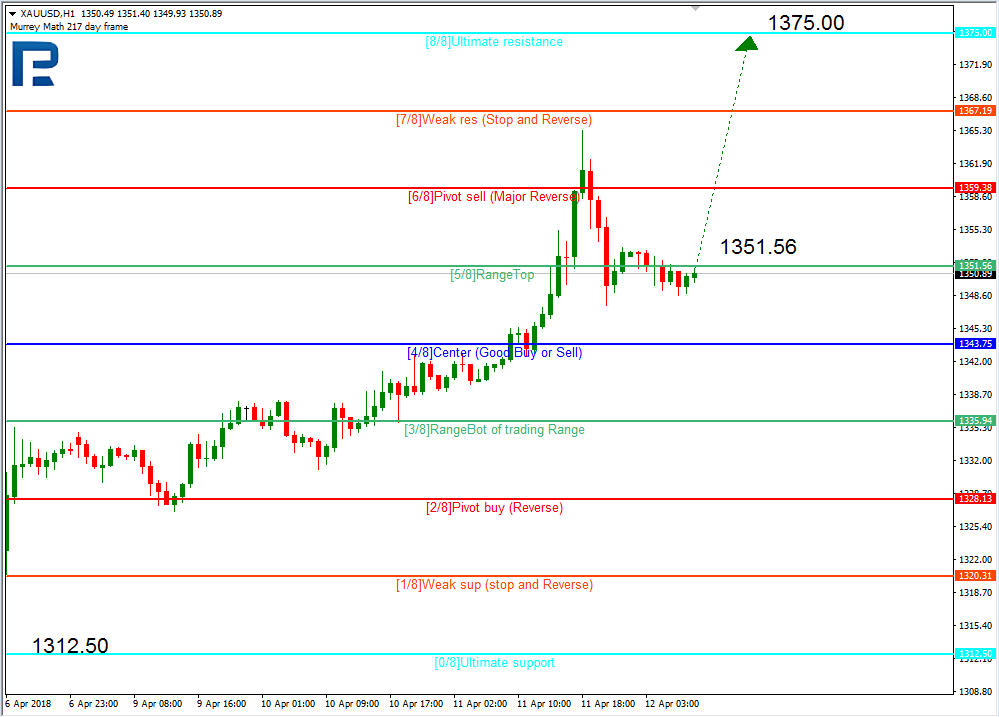

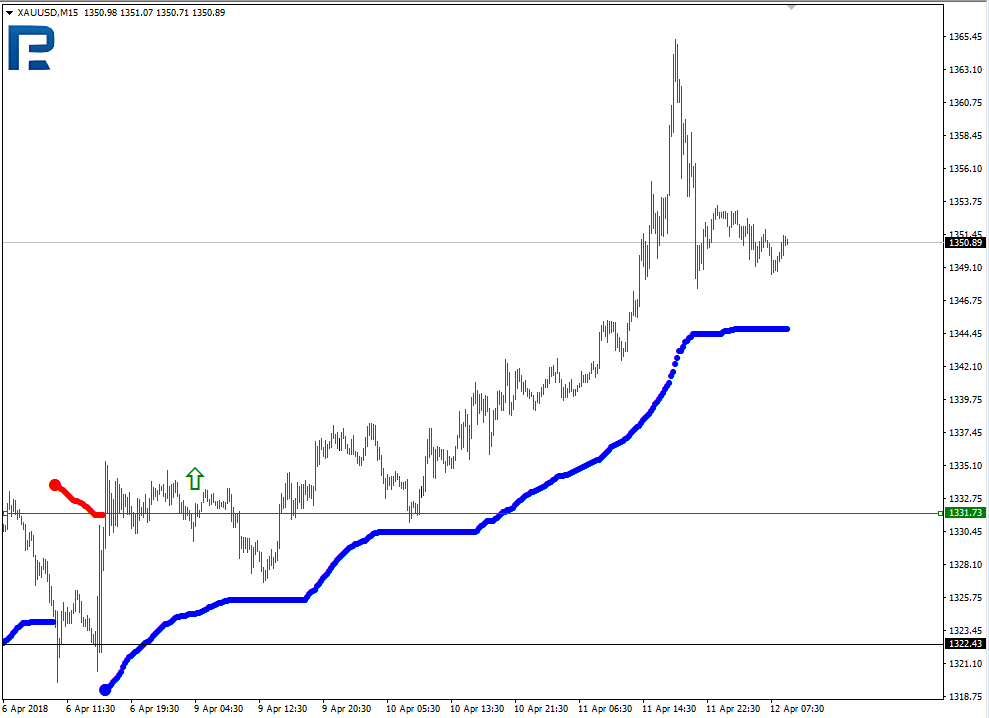

New massive breakout patterns have been setting up in the markets for months and our research team at the Wealth Building Newsletter has been quietly watching these setups – waiting for the right time to alert our followers of these exceptional opportunities. Today, we are announcing our research and triggers to all of our followers so you can attempt for profit from our hard work and see just how critical our “Adaptive Learning Tools” are for success.

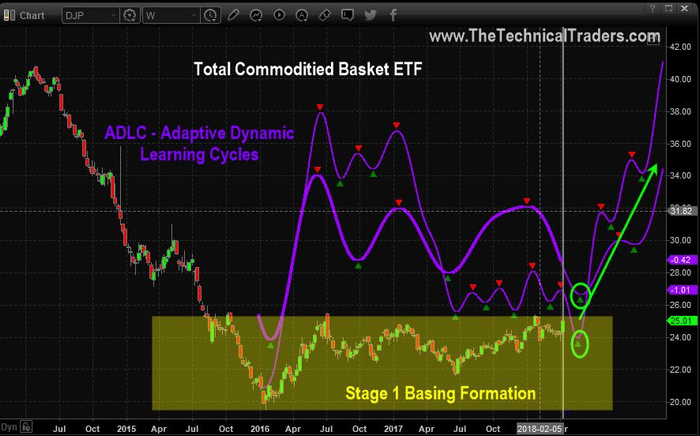

We believe the following charts clearly show just how important these breakout patterns are for traders. This first chart shows the Stage 1 Basing formation that we’ve been following for quite a while with our Adaptive Dynamic Learning Cycles. These cycle projections help us to determine the future potential of any markets as well as help us to understand historical and current price cycle rotations.

Right now, these cycle predictions are warning that a massive cycle bottom is likely to happen within the next 2 to 3 weeks followed by a massive upside price rotation in commodity prices. We don’t believe this future bottom cycle will be very deep – therefore we believe now is an excellent time to consider a positional trade expecting higher commodity prices in the future.

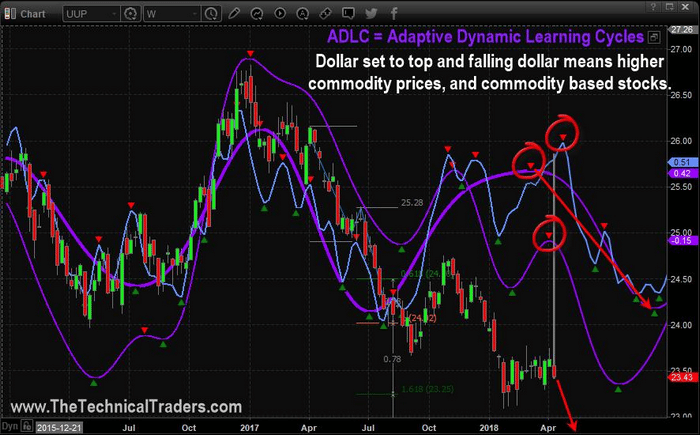

Conversely, our Adaptive Dynamic Learning Cycles are showing future weakness in the US Dollar. Combine these two cycle patterns, weakening US Dollar and potentially stronger general commodity prices, and we have an almost perfect setup for traders and investors. If the US Dollar weakens while external market factors (like foreign geopolitical tensions and trade issues) continue to drive the news cycle, we may be setting up for a very explosive upside move in commodities.

On Wednesday, April 11th, we issued a buy signal in a specific asset which we believe will post the largest gains of all for our subscribers and this can be trades both as an active swing trade, or as a long-term investing position.

We are providing you with this general analysis currently because we believe unique opportunities will continue to present themselves over the next 2 to 5 weeks as this movement continues to play out. We believe active traders will want to take advantage of these setups to execute successful trades as this move extends.

If you want to learn how to profit from these setups and others, please visit www.TheTechnicalTraders.com to learn more about how we help our members take advantage of these setups. Our research team is dedicated to helping you stay ahead of the markets while identifying these types of trading opportunities. You will be amazed how just how stress-free trading and investing can be when you know with a high probability where the markets are headed in the days and months ahead so Join Now!

53 years experience in researching and trading makes analyzing the complex and ever-changing financial markets a natural process. We have a simple and highly effective way to provide our customers with the most convenient, accurate, and timely market forecasts available today. Our stock and ETF trading alerts are readily available through our exclusive membership service via email and SMS text. Our newsletter, Technical Trading Mastery book, and 3 Hour Trading Video Course are designed for both traders and investors. Also, some of our strategies have been fully automated for the ultimate trading experience.

For a year, President Trump has promoted global division and trade friction, while China has defended global trade and cooperation. It is time to defend the open, global economy.

If President Xi Jinping’s speech was highly anticipated in the Boao Forum, it was even more eagerly waited in Washington and Wall Street, as trade tensions have begun to penalize US markets.

In his keynote speech, Xi urged countries to “stay committed to openness, connectivity and mutual benefits, build an open global economy, and reinforce cooperation within the G-20, APEC and other multilateral frameworks.” The ultimate goal is to make economic globalization “more open, inclusive, balanced and beneficial to all.”

Xi presented plans to further open up the Chinese economy, including lower import tariffs for autos and other products, enforcement of the legal intellectual property of foreign firms, and improving the investment environment for international companies.

It was a balancing act that highlighted China’s goal to safeguard open global economy, even amid Trump’s trade wars.

Trump’s trade war

In early March, President Trump introduced a global tariff of 24 percent on steel imports, while launching a 10 percent duty on all aluminum entering the US.

On March 22, Trump directed his administration to make a case against Chinese technology licensing in the WTO, launched a slate of tariffs at $50 billion on Chinese products and proposed to step up restrictions on Chinese investment in key US technologies. That’s when China, in response to US steel and aluminum tariffs, imposed tariffs on $3 billion worth of US goods.

On April 2, China imposed tariffs of up to 25 percent on 128 US products, in response to steel and aluminum tariffs. The next day, the US proposed tariffs on $50 billion worth of Chinese electronics. Afterwards, China launched $50 billion in tariffs on more US products, including soybeans, cars and chemicals. And on April 5, Trump said he was considering an additional $100 billion in tariffs against China.

With substantial geopolitical leeway, Trump is also playing targeted countries against each other. That’s why he has granted “initial exemptions” to US NAFTA partners, Mexico and Canada, and “temporary exemptions” to the EU, South Korea and others on steel and aluminum tariffs.

Over a year ago at Davos, President Xi Jinping stressed the need for global cooperation to sustain global recovery. In a trade war, he said, “no one will emerge as a winner.”

In the White House, that wisdom got lost in translation. Now the only question is how costly that policy mistake will prove.

Costly consequences

President Trump may be in for a cruel awakening. For now, the economic impact on Chinese companies and banks is still limited. The US accounts for only 15 percent of China’s goods exports, and China’s domestic activity – not net exports anymore – now fuels its economic growth. US economy will carry a substantial burden, however.

Second, Trump’s unilateral tariffs will soon begin to hit hard the constituencies that were vital for his triumph in 2016 and who remain critical to Republicans in the fall mid-term elections. These farmers and blue-collar voters gave Trump a mandate to negotiate better terms with US trade partners, but not a carte blanche, and certainly not a license for a trade war.

China is the largest customer for America’s farm surplus at over $20 billion per year. Since US farm groups have greatly benefited from the reduction of trade barriers over time, there is an unease across the US heartland that Trump’s tariffs could upend decades of progress. Even worse, if trade friction worsens with NAFTA and EU partners, US farmers would take hits from all directions.

Third, as US sovereign debt now exceeds $20.7 trillion (107% of GDP) and Trump’s infrastructure initiative is fueled by record-high leverage, trade war is undermining America’s critical revenue sources.

Fourth, Trump’s trade war is escalating at a time when even rising interest rates can no longer ensure a strong dollar, and petroyuan is on the ascend. Moreover, with $1.2 trillion of US debt, China remains the largest foreign holder of US Treasuries. And it also has $3.1 trillion of foreign exchange reserves.

Fifth, if Trump proceeds in the trade war path, he would undermine US ties with its NAFTA partners, alienate EU allies while undercutting US alliances with the rest of its trade and security partners in Asia. Over time, that would undermine not just trade, but investment and finance with America’s biggest economic partners in North America, Western Europe and East Asia.

Sixth, global growth prospects are not immune to the trade war. Before Trump’s tariffs, global investment flows remained well behind their peak a decade ago. World export volumes reached a plateau already in early 2015. In finance, global cross-border capital flows have declined by a 65 percent since 2007.

Prohibitive lessons

For now, the damage of the Trump tariffs is still reparable and reversible. However, the net effect of further escalation would result in critical erosion in global investment, trade, and finance. That has potential to derail the fragile global economic recovery and disrupt international supply chains.

In that case, four decades of bilateral confidence-building could be undermined in four weeks and mistrust would soon spread to US relations with its partners in Americas, Western Europe and East Asia.

In that path, there is a historical precedent. After the US economy drifted into the Great Depression in the 1930s, Washington enacted the Smoot-Hawley Tariff Act, which led the way to tit-for-tat retaliation, and ultimately paved the way to much worse.

Trump’s unilateral tariff war is on the wrong side of history.

About the Author:

Dr Dan Steinbock is an internationally recognized strategist of the multipolar world.and the founder of Difference Group. He has served at the India, China and America Institute (USA) , the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see http://www.differencegroup.net/

The original, slightly shorter version was published by China Daily on April 10, 2018

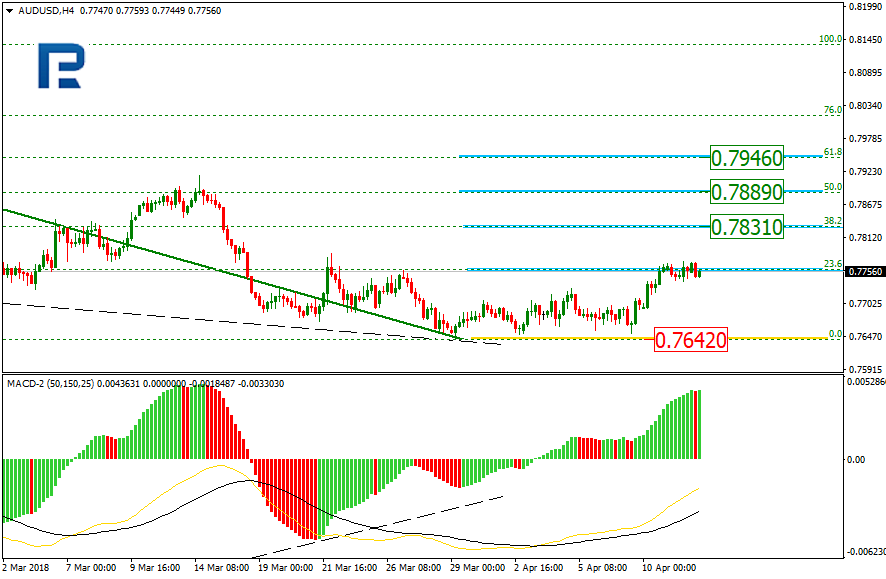

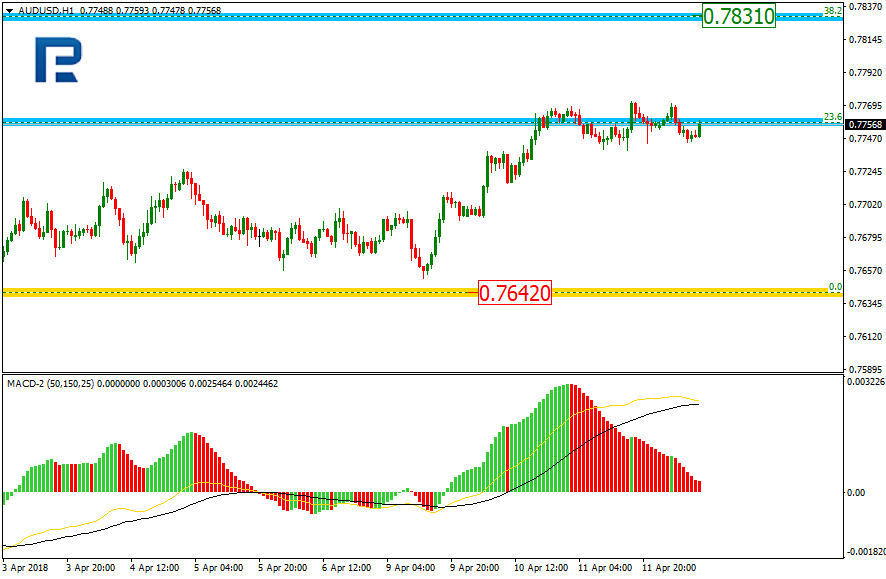

In the H4 chart, the convergence made AUDUSD finish the downtrend, reverse, and start a new rising correction, which has already reached the retracement of 23.6%. The next upside targets may be the retracements of 38.2%, 50.0%, and 61.8% at 0.7831, 0.7889, and 0.7946 respectively. The support level is the short-term low at 0.7642.

As we can see in the H1 chart, the pair is trading sideways near the retracement of 23.6%. The closest upside target may be at 0.7831.

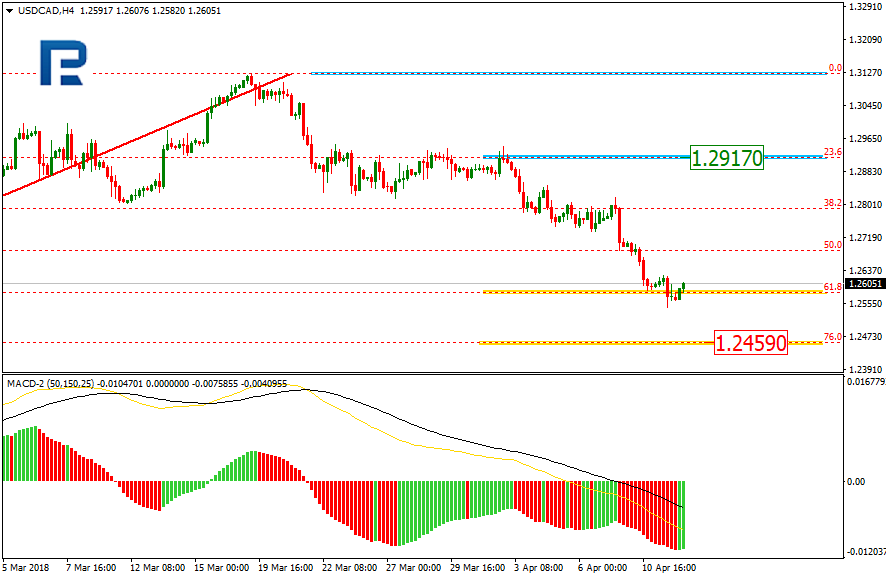

USDCAD, “US Dollar vs Canadian Dollar”

As we can see in the H4 chart, the downtrend has reached the retracement of 61.8%. The next downside target may be the retracement of 76.0% at 1.2459. The short-term resistance is at 1.2917.

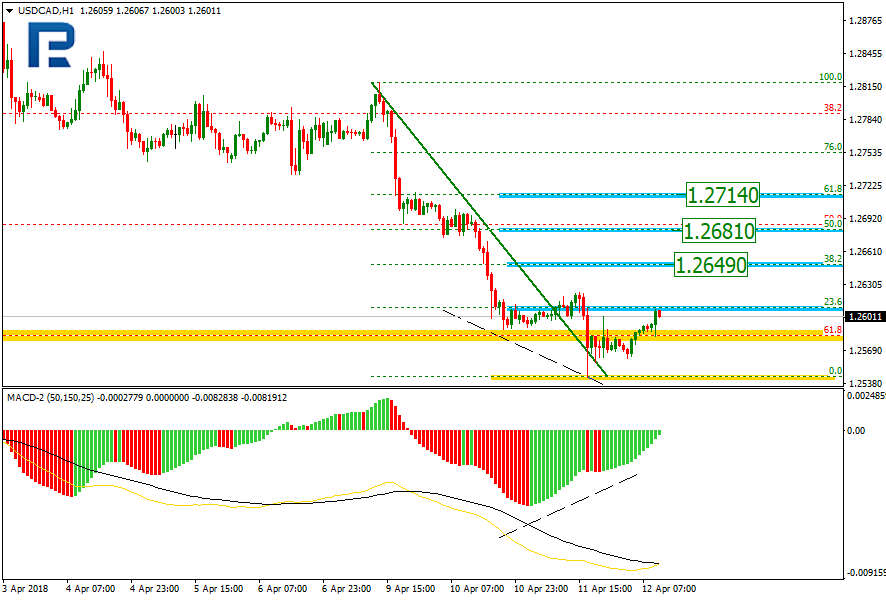

In the H1 chart, the convergence is being formed< which may indicate a possible correctional uptrend. The first ascending impulse has already reached the retracement of 23.6%. The next targets may be the retracements of 38.2%, 50.0%, and 61.8% at 1.2649, 1.2681, and 1.2714 respectively.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

On Wednesday the 11th of April, trading on the EURUSD pair closed slightly up. The pair spent most of its time hovering around the 135th degree at 1.2380. Markets swung in all directions as they braced themselves for a potential strike in Syria by the US, France, or Germany. It’s been 48 hours, but Trump has yet to make the decision to strike. The euro slid against the dollar from 1.2396 to 1.2347 after the FOMC minutes were published.

The minutes of the FOMC’s March meeting show that many committee members expect the economic situation in the country to continue to improve and for inflation to rise. All 9 committee members voted in favour of the 25-base-point rate hike. This was the 6th rate hike since December 2015. Senior members of the Fed expect a further two rate hikes this year. The regulator also expressed concerns over the influence the White House’s trade and fiscal policies are having on markets.

My predictions for yesterday came off in full. The 135th degree held back the bulls’ advancement. After the FOMC minutes were published, the rate met the LB balance line at 1.2347.

For Thursday, the 1.2338 – 1.2345 range is a strong support. Since most of the euro crosses are trading up and the stochastic oscillator is in the buy zone, I expect prices to recover to 1.2367 in Europe. From here, an upwards breakout of the downwards channel looks unlikely. If the hourly candlestick closes above the channel, the prospect of a drop will disappear.

At 14:30 (GMT+3), the ECB will release a report on its latest meeting on monetary policy. This could cause the euro to decline up until trading opens in the US. For now, I can’t see quotes falling any lower than the 67th degree at 1.2313. If the pair returns to this level ahead of time, i.e. before 15:00 (GMT+3), I’ll revise my target.

For years, drugs and corruption thrived in the Philippines as policymakers engaged in external adventures ignoring domestic investment. The Duterte government is fostering a historical investment drive, while seeking to defuse the threat of drugs and corruption. So why is it penalized in the West?

Recently, President Duterte said that people should look to the Central Intelligence Agency (CIA) in case anything happens to him, referring to the US criticism against the war on drugs in the Philippines. “If my airplane explodes or a roadside bomb goes off, you can ask the CIA,” he said.

Timing matters. After former US Ambassador Philip Goldberg left Philippines in the aftermath of the 2016 election, he allegedly wrote a “blueprint to undermine Duterte within 18 months” – we are amid the deadline period.

Why the drug trade was ignored

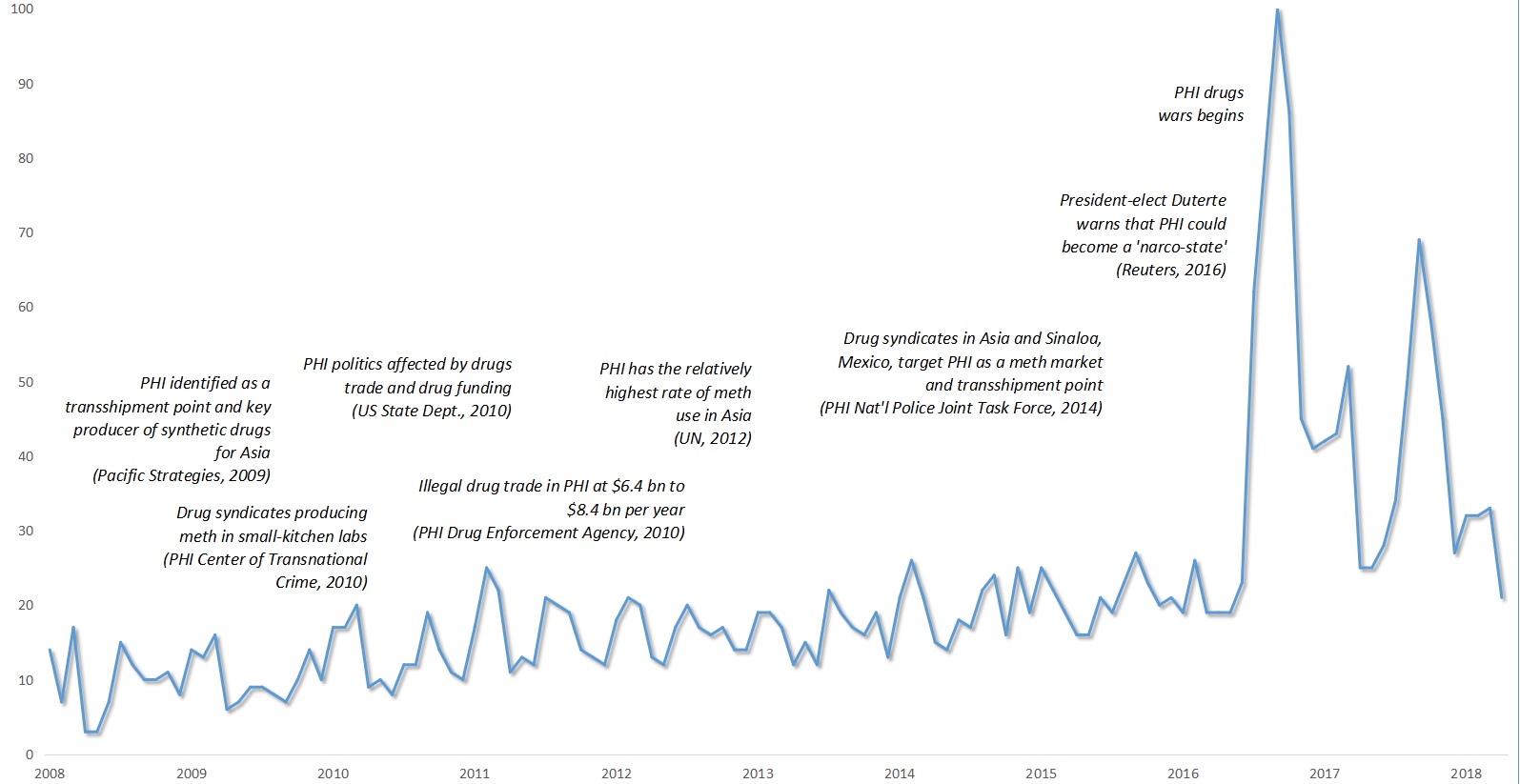

Ironically, Duterte has taken the drug problem seriously, as most Filipinos whose neighborhoods have been invaded by drugs for more than a decade, particularly in the President Aquino III era. During the period, the drug problem was downplayed by the mainstream media and largely ignored by international media. As a Google Trend search demonstrates, it was only when Duterte began the war against the drugs that critics awoke, as evidenced by soaring story mentions about the Philippines and drugs in international media, mainly in the US and Europe (Figure).

Figure The Long silence about PHI drugs invasion until the Duterte Era

Sources: Google Trends; various Philippines, international, US and UN Sources

Under the watch of President Aquino and his Liberal Party (LP), drug syndicates began to produce meth in kitchen labs, which caused illegal drug trade to soar to $8 billion. US State Department warned drug trade and funding affected Philippines politics, as corruption undermined the rule of law. Yet, drug syndicates in Asia and Sinaloa, Mexico, saw the Philippines transshipment potential. The Discovery Channel showed drug trade and gang leaders’ luxurious life in the New Bilibid Prisons, with the involvement of former Justice Secretary Leila de Lima who allegedly received millions of pesos in payola money from drug lords.

Then the plans were derailed. In the 2016 election, Mar Roxas was Aquino’s designated successor – former interior minister and ex-investment banker in Wall Street – but failed to deliver a victory. Instead, Duterte triumphed.

Only days in the office, Duterte named five ‘narco-generals’ believed to be protecting drug lords that allowed shabu (meth) sales to flourish during the Aquino era. Some of them had been linked with Roxas who denied all ties with “Roxas generals,” even though some – including Deputy Director General Marcelo Garbo whom Duterte called a “protector of drug syndicates” – were among the police generals seen in closed-door meeting with Roxas’ staff at Novotel Hotel in Manila.

During his campaign Duterte warned the Philippines was on the way of becoming a “narco-state,” but LP leaders accused him of inflating the problem. Yet, the number of addicts had soared to 4 million people. Between July 2016 and November 2017, 4,000 drug suspects have been killed in 80,700 police operations with the arrest of 119,000 drug personalities, and at the cost of the lives of 86 police officers and soldiers and another 226 wounded.

LP meltdown and politicized rights debacles

As most Filipinos support Duterte and the drug war, the rights accusations have been offshored by politicizing human rights, amid the cataclysmic meltdown of the Liberal Party, as evidenced by the high-profile abuses of public office by President Aquino, Interior Secretary Roxas, Supreme Court Justice Maria Lourdes Sereno, Comelec Chair Andy Bautista, Secretary of Justice Leila De Lima, the ‘narco-generals,’ a slate of high-level government officials and dozens of senior executives.

The Aquino debacles alone – Manila hostage crisis, Typhoon Haiyan, Mamasapano massacre, and the Dengue vaccine scandal – are stupefying. Yet, the flawed story about Duterte as a threat surfaced in February, when he was seen as an impediment to democracy in the US intelligence community’s Worldwide Threat Assessment. In this misrepresentation, the dots can be linked with Goldberg, and the marginalized LP rights politicizers.

A key role in the Duterte misrepresentation belongs to Senator Leila de Lima, Aquino’s former Secretary of Justice, who has been glorified by CNN and BBC and as one of the “leading 100 global thinkers” by the Democratic Foreign Policy.In the Philippines, De Lima’s awards seem perversions of justice, including her 7-year affair with her lucratively-rewarded driver Ronnie Dayan who served as her money collector for drug protection and campaign financing. Despite imprisonment, her international accolades have escalated – from the EU and Inter-Parliamentary Union (IPU) parliamentarians to human rights NGOs – many of which are increasingly funded by private capital and represent Western interests.

None of these organizations intervened when drugs took over the Philippines, along with corruption and human rights violations.

Another role in the misrepresentation belongs to the Commission of Human Rights (CHR), which has been led by Chito Gascon since 2015. In mid-2017, Duterte and the House of Representatives sought to exhaust CHR budget as the politicized Commission had lost its credibility. Besides a human-rights lawyer, Gascon is a veteran LP leader. As he no longer could garner consequential rights support at home, he began feeding part of local media, which is in foreign ownership, and international media. What followed was a series of manufactured “events.”

In May 2017, Vice President Leni Robredo, another LP leader, sent a controversial video message on Philippines extrajudicial killings to the UN Commission on Narcotics Drugs, which featured Gascon. It was well timed by David Borden, head of the UN-accredited Drug Reform Coordination Network, also known as StoptheDrugWar.org which has been supported by Soros foundations.

In another case, when Duterte government invited UN Special Rapporteur Agnes Callamard to a public debate about the Philippines war on drugs, Callamard sneaked into Manila for an “academic” lecture, at the request of Gascon. Callamard has served at Columbia University’s Global Freedom of Expression Project whose major supporters include Soros foundations. Reportedly, Soros played a role in her appointment as UN special rapporteur.

Instead of democratic institutions in the Philippines, the rights leaders have relied on transnational NGOs funded by private capital – and guided by Western interests – to do the job. Amnesty International and Human Rights Watch are some of them.

International privatization of rights movements

Amnesty International (AI) sees the Philippines as the site of “thousands of unlawful killings by police and other armed individuals,” and portrays de Lima as a rights martyr. The tone has grown harsh since 2017 when James Gomez became AI’s director for Southeast Asia. While claiming professional neutrality, he considers the charges against de Lima “pure fiction” and Duterte’s policies “bloody and lawless.”

While AI claims to have millions of paying members around the world, it has changed drastically since its founding in the early 1960s by Peter Benenson. In 1966, Benenson himself stated that AI was infiltrated by British intelligence and resigned. Recently, AI has been criticized for excessive management pay, selection and ideological bias. While it claims to refuse donations from governments, it has received grants from the UK, European Commission, Rockefeller Foundation, US State Department and other governments – and Soros foundations.

In Human Rights Watch (HRW), the link has been the head of HRW’s Asia Division Phelim Kine, who has attacked most ASEAN leaders and made Philippines a prime target. In January, Foreign Affairs Secretary Alan Peter Cayetano denounced HRW for its “strategy of deception” in reporting on the government’s anti-drugs campaign.

Like Amnesty, HRW has been criticized for Western bias. It was created as a private US NGO in 1978, as a Cold War instrument to monitor Soviet Union’s compliance with the Helsinki Accords. In early ‘80s, Soros foundations gained leverage in the HRW; and in 2010 Soros cemented ties with a 10-year $100 million HRW donation. Since then, HRW’s record has been tarnished by allegations of partisanship, bias and an 2014 open letter by Nobel Peace Laureates criticizing HRW for intimate ties with the US government.

————

Amnesty, HRW and other well-meaning NGOs were initially founded by idealists who wanted to make a world a better place. Initially, the key question was whether a leader or a regime was making things better or worse for ordinary people. Now, it is more about abstract universals, which allows these NGOs to determine whether a particular leader or regime violates Western-conceived standards of human rights.

Financed largely by the US and Western Europe, these organizations focus on human rights violations in emerging and developing countries in which Western governments and private capital have substantial economic, political and strategic interests. That’s not about universal human rights and economic development, but about new human rights imperialism and old geopolitics.

Like the old tale about the boy who cried wolf, these NGOs raise alarm when it is warranted, but also when it is not. As the distinction between real and fake alarms grows blurry and politicization undermines their credibility , they are digging a grave to their noble cause.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world.and the founder of Difference Group. He has served as at the India, China and America Institute (USA) , the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

The original commentary was released by The Manila Times on April 9, 2018.

EURUSD is moving upwards. Possibly, today the price may reach 1.2390 and then fall towards 1.2300. Later, the market may form another consolidation range between these two levels.

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD is also moving upwards. Possibly, the price may form another ascending structure towards 1.4229 and then fall to reach the target is at 1.4100.

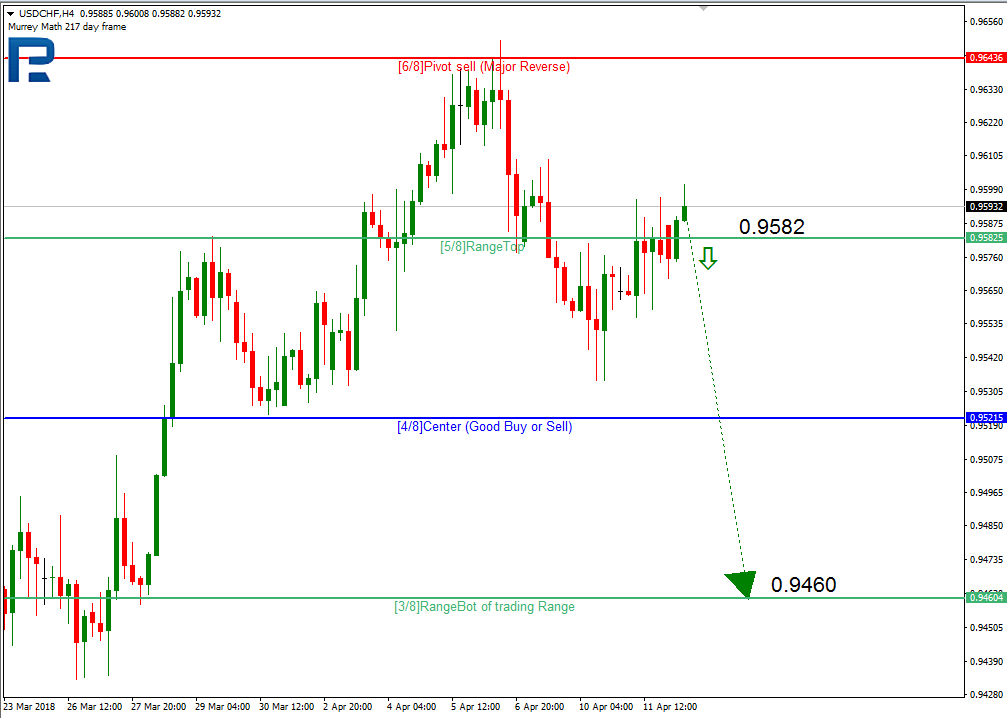

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is trading around 0.9582. Today, the price may fall to reach 0.9522 and then grow towards 0.9622.

USDJPY, “US Dollar vs Japanese Yen”

USDJPY has completed another ascending impulse and right now is being corrected. Possibly, the price may reach 106.87. After that, the instrument may start another growth with the first target at 107.74.

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is extending the ascending structure. Possibly, the price may test 0.7777 from below and then resume falling to reach 0.7567.

USDRUB, “US Dollar vs Russian Ruble”

USDRUB has finished the descending impulse towards 62.00 along with the correction. After breaking the low, the market may fall to reach 61.00 and then start another growth with the target at 66.33.

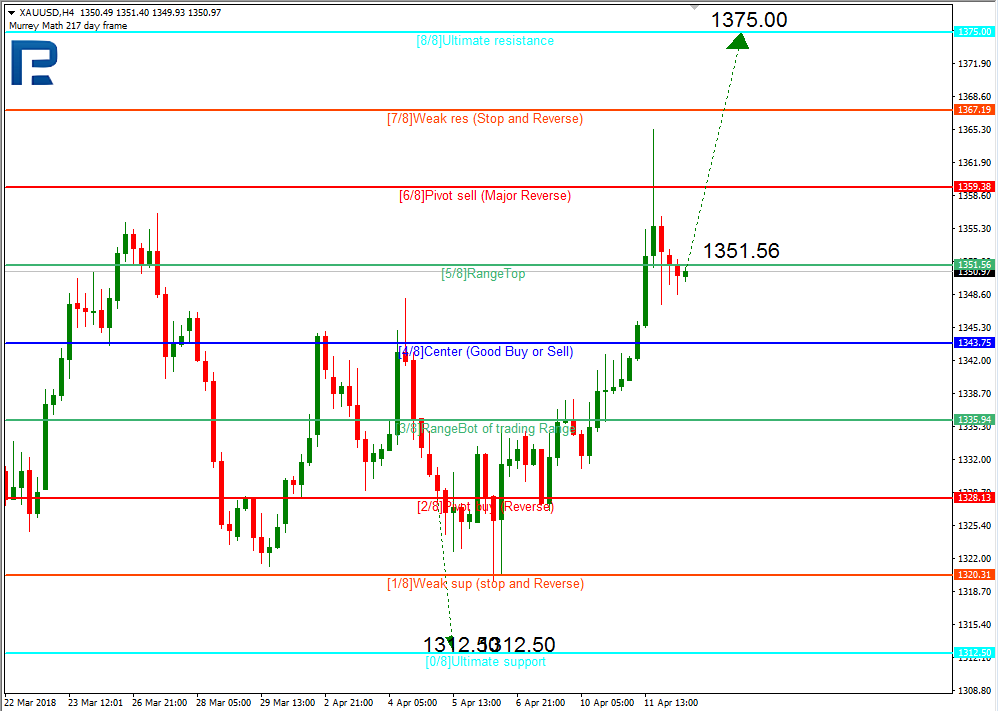

XAUUSD, “Gold vs US Dollar”

Gold continues moving upwards. Possibly, the price may to reach 1344.00. After that, the instrument may start another correction with the target at 1338.00.

BRENT

Brent is trading upwards. Today, the price may reach the short-term target at 72.22. Later, the market may be corrected towards 68.00 and then form another ascending structure to reach 74.00.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

As we can see in the H4 chart, after breaking the support level one more time, USDCAD has formed several Doji and Hammer reversal patterns and right now is being corrected again. At the moment, it may be assumed that the price may complete the pullback very soon and resume falling.

AUDUSD, “Australian Dollar vs US Dollar”

As we can see in the H4 chart, AUDUSD has reached the resistance level and formed several Shooting Star and Engulfing reversal patterns there. At the moment, it may be assumed that after finishing the correction the instrument may break the level and continue its growth.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

On Tuesday the 10th of April, trading on the euro closed up. There was a surge in market volatility as Nowotny, a member of the ECB’s governing council, gave a speech. He said in an interview that the ECB will end its bond-buying program this year and that the regulator could increase the deposit rate from -0.4% to -0.2% before making any changes to the key rate. The euro jumped in response to this to reach 1.2378.

The ECB, however, distanced itself from Nowotny’s comments, with a spokesman saying that “Governor Nowotny’s views are his own. They do not represent the view of the Governing Council”. On this development, the euro retreated to 1.2325.

The EURUSD pair closed the day at 1.2355 on the back of an increased appetite for risk as well as a largely weakened dollar. Comments from Chinese president Xi Jinping eased investor fears over US-Chinese trade relations.

Xi struck a conciliatory tone as he sought not to throw fuel on the trade dispute fire. He said that import tariffs may be reduced and that he would open China’s economy further to foreign investors.

Day’s news (GMT+3):

11:30 UK: industrial production (Feb), manufacturing production (Feb), trade balance (Feb).

14:00 UK: NIESR GDP estimate (Mar).

15:30 USA: CPI (Mar).

17:30 USA: EIA crude oil stocks change (6 Apr).

21:00 USA: FOMC minutes.

Fig 1. EURUSD hourly chart. Source: TradingView

I was wrong in my prediction yesterday that the euro would drop to 1.2275. The bullish trend started on the 6th of April was given a boost by Nowotny. The rate then returned to 1.2325 before recovering to 1.2361 on the back of a broadly weakened dollar.

Buyers were rebuffed at around the 135th degree. Taking the bearish divergence into account, as well as the fact that the FOMC is publishing its minutes this evening, I expect to see a rebound from the LB balance line. Given that the euro crosses are trading up, the bulls look set to reach a new high and form a double bearish divergence.

At 14:00 (EET), Mario Draghi is set to speak. Given Nowotny’s comments yesterday, we might see him expand on the subject of QE.

There’s another thing giving me cause for concern. The US is planning another strike in Syria under false pretenses. During a UN Security Council meeting, Russian permanent representative Vassily Nebenzia called on the West to avoid “hawkish rhetoric” and stop these reckless efforts that put global security at risk. There are Russian servicemen in the area in question and any forceful actions there could have serious consequences. As the US often gets everyone else involved in its escapades, it’s not clear how financial markets are going to react to this. Perhaps we should keep one eye on the dynamics of oil prices and safe haven assets.

As oil can now be traded with RMB-denominated contracts, the rise of the petroyuan will accelerate the internationalization of the Chinese currency as investors begin to increase their allocations into Chinese financial assets.

In late March, as international media focused on Trump’s tariffs and the prospects of a trade war, renminbi-denominated oil contracts began trading in the Shanghai International Energy Exchange (INE), for the first time. That will foster the rise of petroyuan, which may cause a dramatic shift in global asset allocations as institutional investors begin to diversify into China’s onshore bond markets.

Today, the status quo is still very different. The US dollar (USD) and the euro (EUR) still dominate more than 85 percent of international payments, followed by the English pound, Japanese yen, the Swiss franc, Canadian dollar and Chinese yuan (1%) (Figure 1).

Figure 1. Major International Payments Currencies

Source: SWIFT, Feb 2018

Following its integration into the global economic and trading environment, China is now integrating into the global financial system. It is already the world’s biggest trading country, has the largest foreign-exchange reserves, and the world’s biggest consumer market. As China now also absorbs most of the world’s commodities, dollar-denominated intermediaries are not warranted – if they ever where.

Rise and eclipse of petrodollar

After World War II, US dollar was the predominant world currency and America fueled almost half of the world economy. Today US dollar accounts for barely 40 percent of international payments while the share of the US in the world economy is less than half of what it was in 1945. So why does the US still benefit from this “exorbitant privilege”? That has nore to do with petrodollar.

After the 1945 Yalta Conference, which effectively divided Europe, the ailing President Franklin D. Roosevelt met Saudi Arabia’s King Ibn Saud. Bypassing the Brits, the former “masters of the universe,” FDR and Saud agreed to a secret deal, which required Washington to provide Saudi Arabia military security in exchange for secure access to supplies of oil.

Despite periodic pressures, the pact survived until the 1971 “Nixon Shock.” As the dire US economic prospects led President Nixon to the unilateral cancellation of the direct international convertibility of the US dollar to gold, the postwar Bretton Woods system of international financial exchange was replaced by a regime based on freely floating fiat currencies. US dollar was decoupled from gold.

To deter the marginalization of US dollar, Nixon negotiated another deal, which ensured that Saudi Arabia would denominate all future oil sales in dollars, in exchange for US arms and protection. Led by Saud, other OPEC countries agreed to similar deals and global demand for US petrodollars soared.

The US-Saudi strategic partnership weathered another four decades of multiple regional wars. When the Fed began to pave way for rate hikes in 2014, the value of the dollar started to climb, though slower than expected, and oil prices plunged since oil markets are dollar-denominated. To seal the old alliance, President Trump signed a historical $110 billion arms deal with King Salman.

Yet, US dollar’s coverage is slipping because structural conditions that supported its dominance have been softening since 1971.

How OBOR drives the rise of petroyuan

The internationalization of the Chinese renminbi accelerated significantly in 2016 when RMB joined the IMF international reserve currency basket. Last October, China established a payment-versus-payment system for transactions involving Chinese yuan and Russian ruble. The China Foreign Exchange Trade System (CFETS) hopes to launch similar systems with other currencies based on China’s huge multi-decade, multi-trillion One Belt One Road (OBOR) initiatives.

As the OBOR expands links between major economies in Asia, Africa, Europe and Latin America, member countries are candidates for RMB-denominated payments. Last December, Iran, which has not deployed US dollar in foreign-trade transactions since the early 2010s, announced it would join the Russia-led Eurasian Economic Union (EEU), which will also have a central role in the OBOR, and thus in RMB-denominated payment systems. US geopolitics is escalating these trends. When the White House suspended US aid to Pakistan, Islamabad announced that the Chinese yuan can be used for bilateral trade and investment activities, which will support the Chinese-Pakistan $57 billion economic corridor.

Recently, China has become the largest global oil consumer (Figure 2). With major oil exporters like Russia, Venezuela, Iraq, Iran, and Saudi Arabia, China’s market means leverage, and many of these suppliers have either already agreed to price their sales to China in RMB, or are actively considering it (Figure 3). In turn, major commodity exporters, such as Indonesia, have joined in non-dollar trades.

Figure 2. US & China Crude Oil Imports (1,000 Barrels per Day), 1980-2016

Source: BP Statistical Review of World Energy 2017

Figure 3. China: Oil Suppliers (% of Total Imports), 2016

Source: World Top Exports, March 2018

The future is on China’s side. By 2040, Chinese annual demand is expected to grow more than 30 percent, whereas US is likely to reduce its reliance on oil imports as it hopes to develop domestic shale oil capacity. US economic interests with Saudi Arabia may erode, even if military interests prevail. If Saudi Arabia decides to adopt the yuan for some of its oil exports, that could unleash a broader shift.

Impending shift

As an increasing share of China’s oil imports will be priced in RMB, that will result in large RMB reserves in oil exporting countries, which will be spent on Chinese exports, or recycled into China’s financial markets. As demand for RMB assets will increase, the role of USD for trading purposes will lessen.

In the short-term, the Chinese system is unlikely to change the way oil is traded globally. Even with exchange convertibility, international investors and resource traders must have confidence in Shanghai INE as a trading hub.

In secular terms, the petroyuan will mean a paradigm shift in global asset allocations to China’s financial markets, as long as China will continue to remove or significantly reduce capital controls for RMB-priced oil trading. Between 2014 and 2017, global institutional investors already tripled their China holdings of onshore bonds. In a year or two, when China’s onshore bond markets are likely to be included in global bond benchmark indices, a major reallocation of capital will flow into China’s onshore bond markets.

An important caveat: The progressive shift to petroyuan will speed up disruptively if investors one day lose faith in the US dollar, due to a US debt crisis, or a huge Trump policy blunder, as the shift away from US dollar could accelerate dramatically.

China’s economic rise is already a reality. The coming shift in global asset allocations is its rightful reflection in world finance.

About the Author:

Dr. Dan Steinbock is an internationally recognized strategist of the multipolar world.and the founder of Difference Group. He has served as at the India, China and America Institute (USA) , the Shanghai Institutes for International Studies (China) and the EU Center (Singapore). For more, see https://www.differencegroup.net/

The original commentary was released by China-US Focus on April 9, 2018.