Large metals speculators increased their bullish net positions in the Silver futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Silver futures, traded by large speculators and hedge funds, totaled a net position of 17,453 contracts in the data reported through Tuesday May 29th. This was a weekly advance of 2,228 contracts from the previous week which had a total of 15,225 net contracts.

Speculative positions have now risen for four straight weeks and have been in positive territory for three straight weeks. Over the past few months, silver bets had seen their first declines into bearish positioning since 2003 but have now bounced back to the highest bullish level since January 30th.

Silver Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -35,297 contracts on the week. This was a weekly decline of -3,874 contracts from the total net of -31,423 contracts reported the previous week.

SLV ETF:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the SLV ishares ETF, which tracks the price of silver, closed at approximately $15.44 which was a decrease of $-0.14 from the previous close of $15.58, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators). Find CFTC criteria here: (http://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm).

Large precious metals speculators decreased their bullish net positions in the Copper futures markets this week, according to the latest Commitment of Traders (COT) data released by the Commodity Futures Trading Commission (CFTC) on Friday.

The non-commercial futures contracts of Copper futures, traded by large speculators and hedge funds, totaled a net position of 37,600 contracts in the data reported through Tuesday May 29th. This was a weekly decline of -1,412 contracts from the previous week which had a total of 39,012 net contracts.

Speculative bets had risen in the previous two weeks before this week’s slight turnaround. The overall net position remains above the +30,000 contract level for a seventh consecutive week.

Copper Commercial Positions:

The commercial traders position, hedgers or traders engaged in buying and selling for business purposes, totaled a net position of -41,235 contracts on the week. This was a weekly gain of 2,514 contracts from the total net of -43,749 contracts reported the previous week.

Copper Futures:

Over the same weekly reporting time-frame, from Tuesday to Tuesday, the Copper Futures (Front Month) closed at approximately $306.25 which was a decrease of $-6.95 from the previous close of $313.2, according to unofficial market data.

*COT Report: The COT data, released weekly to the public each Friday, is updated through the most recent Tuesday (data is 3 days old) and shows a quick view of how large speculators or non-commercials (for-profit traders) as well as the commercial traders (hedgers & traders for business purposes) were positioned in the futures markets. The CFTC categorizes trader positions according to commercial hedgers (traders who use futures contracts for hedging as part of the business), non-commercials (large traders who speculate to realize trading profits) and nonreportable traders (usually small traders/speculators). Find CFTC criteria here: (http://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm).

Welcome to this week’s Market Wrap Podcast, I’m Mike Gleason.

Coming up Axel Merk joins me to break down the situation in the Eurozone, the likelihood of more nations following the UK in exiting the EU and how all this might affect the dollar, Fed policy and precious metals. Don’t miss an enlightening interview with Axel Merk of Merk Investments, coming up after this week’s market update.

A political crisis in Italy roiled markets earlier this week, sparking a flight to U.S. Treasuries and a spike in the Dollar Index. That spike was short lived, however. The dollar quickly came right back to where it started the week, a possible indication that an upside exhaustion point has been reached in this spring’s dollar rally.

Precious metals markets are also seemingly on the verge of a major turning point. Nothing decisive happened this week, though, as gold continues to trade close to the $1,300 level and silver still finds itself stuck in a tight trading range.

Silver prices currently check in at $16.48 per ounce, down 0.3% since last Friday’s close. Spot gold is down 0.4% for the week to trade at $1,296 an ounce. Meanwhile, platinum is unchanged at $911 and palladium is off by 0.7% this week at $988 per ounce as of this Friday morning recording.

Precious metals prices have hung tough during the dollar rally of the past few weeks. The latest boost to the dollar came as anti-establishment political parties in Italy moved to begin breaking the country’s ties to the European Union. Without Italy, the entire EU could collapse. Italy is the euro zone’s third biggest economy. More importantly for global financial markets, Italy has a massive sovereign debt obligation of about $2.5 trillion in U.S. dollar terms.

The long-term future of the euro as a viable currency is in doubt, but it probably won’t go away anytime soon. The same could be said of the U.S. dollar if for different reasons. Investors who jump from one troubled fiat currency to another in hopes of landing on a safe haven are being short sighted. In the long run, all national currencies stand to lose value and some may even go into hyperinflation like the Venezuelan bolivar.

Venezuela’s annual inflation rate is now approaching 14,000%. The socialist-run country has left its people suffering under constant shortages of bare essentials such as food and medicine.

In a country now so economically destitute that many Venezuelans have been reduced to eating rats, insects, and other unconventional foods just to survive, those who do have any savings to speak of have also been forced to take unconventional steps to protect their wealth. As the Venezuelan bolivar becomes increasingly worthless, people are turning to the black market. They’re turning to U.S. dollars. They’re turning to cryptocurrencies. They’re turning to scrap gold, to silver coins, and even to aluminum cans.

We may never find ourselves in the chaos of a true hyperinflation. But even modest inflation can exert a devastating impact on the value of savings and investments after a number of years. Physical precious metals are among the premier inflation-fighting assets. If hyperinflation ever does break out and parts of the economy revert to barter, then you may actually need to use your bullion as money.

It’s been said that gold is the money of kings while silver is the money of the masses. During an economic crisis, copper may become the money of the expanding peasant class. For this reason and for another way to protect themselves against inflation, metals investors may wish to consider adding some physical copper to their stash. Copper fills an important gap, being suitable for smaller transactions where gold and even silver may not be practical options.

Even if you never need to use copper in barter or trade, you may still be glad you have some exposure to the industrial metal for its upside potential. Copper prices haven’t done much in 2018, but they are still up big since Donald Trump’s election in 2016. President Trump’s pro-manufacturing, pro-infrastructure policies should put additional bullish pressure on the copper market. Copper is essential in the modern economy. Electronics, automobiles, and utilities among other things can’t function without it.

Copper rounds are an appealing way for any metals investor to add to their stack. They are pure copper in a barter-ready size – clearly marked with weight and purity.

A less aesthetically pleasing but more cost effective way to own copper is through circulated pre-1983 copper pennies. Don’t bother hoarding any of the newer pennies – they contain only a thin layer of copper and the metals they contain are worth well less than one cent.

But a stash of old, solid 95% copper pennies could come in handy in the event you need metals to barter and trade. Money Metals has pre-1983 95% copper pennies sold by weight in 34 pound bags, and the copper in each of these pennies is worth about two cents at current market prices. We currently have them at less than two percent above melt value of the copper, making these older pennies a highly efficient way to get exposure to copper prices.

Just like gold, silver, and other precious metals, you can order any of our copper coins, rounds, and bars securely at the MoneyMetals.com website — or by calling 1-800-800-1865.

Well, now without further delay, let’s get right to this week’s exclusive interview.

Mike Gleason: It is my privilege now to welcome back Axel Merk, President and Chief Investment Officer of Merk Investments and author of the book Sustainable Wealth. Axel is a highly sought after guest at financial conferences and on news outlets throughout the world and it’s great to have him back on with us.

Axel, it’s a pleasure to have you join us again today and thanks very much for coming on.

Axel Merk: Great to be with you. What a week.

Mike Gleason: Exactly. Well, Axel when we spoke to you in February the equity markets were in the midst of a sell off and some significant volatility, which had been extraordinarily low, came roaring back to life. Since then, the stocks have recovered some. The S&P regained about half of what it lost by the end of February and has been trading in a range since then.

Our thoughts are that precious metals are trading inversely correlated to equities markets, at least for now. Unless we get a pullback in stocks or more appetite for safe-haven assets it will be hard for metals to get much going to the upside. But what are your thoughts on the relationship between gold prices and stock markets, Axel? And what factors do you expect to be driving stocks between now and say the end of the year?

Axel Merk: Sure, and for context I think we should just mention we are talking before the Non-Farm Payroll Reports (are out), so who knows what’s happened to markets since we have talked? One of the things I don’t recall if I mentioned in February is, ever since last December, and I still believe in that, the markets have been a bit like a washing machine. That correlations have been breaking down. And, if you go back to, kind of, all the way to the financial crisis, that’s the 2008 one, not the one from a week ago, that means that whenever there was a crisis the Fed bought treasuries. And so whenever “risk” falls off, when equities are plunging, bonds were rising. And that kind of ingrained this perception about certain types of correlations and so, similarly, the price of gold was actually reasonably highly correlated to that of treasuries. And so we got this thing that gold and the stocks are sometimes moving in tandem, sometimes they move in opposite directions.

Since January 1970, if you look at monthly correlations, the correlations between stocks and bonds is 0.00. So, there is no correlation. Yet, we get caught up in this thing that, for months at a time, sometimes there’s a correlation that is significant. I think the most noteworthy thing of late is that yields have been, until a good week ago, have been matching higher and the price of gold was falling up. And then, conversely, when bond yields were falling, gold didn’t rise.

And so, gold has kind of marched on its own in some ways and I happen to believe that a lot of the buyers of gold these days are doing it because they are concerned about the equity markets because of volatility spiking. And the reason why volatility and the price of gold are related is because gold doesn’t have cashflow. And that means the future cashflows don’t get discounted more, whereas, if you have a quote unquote risk asset, like equities, and volatility increases, those future cashflows get discounted more and the prices of equities, all else equal, tends to fall. So, that’s why in “normal” circumstances the price of gold should rise when equities tumble. Obviously, that doesn’t always happen.

Mike Gleason: You pay more attention than most people to events in Europe and the European markets. Lately, troubles in the PIGS nations have crept back into the news. Populace in Italy and Spain are making hay by opposing EU imposed austerity and it’s a reminder that deep fundamental issues remain and the union may not survive. Let’s start by getting your take, if we can, on the overall status of the EU. Will there be any high-profile exits, perhaps by Italy or Spain? Is Great Britain going to complete its exit? Or are you expecting the EU to weather the storm here, Axel?

Axel Merk: The UK is almost certainly going to exit and nobody else, probably, any time soon. Now, I say that, I might have egg on my face in a few years down the road on that. But let me, maybe before we get too far carried away, make a general statement because I think we’ve seen this movie before. What we’ve had is a classic case, classic as in classic for financial crisis type of case, where investors were piling in into an asset that they perceive to be risk free, only to wake up that it is risky after all. And what I’m referring to, of course, is Italian bonds, right?

Who wouldn’t want to grab for some yield? And if you don’t grab for some yield, especially if we’ve had someone like the head of the ECB doing quote unquote whatever it takes, all but guaranteeing the debt. So, why would you get a negative yield, or very low yield on German bonds when you can get Italian treasuries for a much juicier return? So, we’ve had yield chasers in there.

Now, the noteworthy thing is, and, again, this is the same picture we’ve had throughout the financial crisis, the folks holding these are not risk-friendly investors. Those are folks who thought that stuff was risk-free. So, sure enough, there is some event happening and people is “Oh, my God! Italian bonds are risky! How could I have possibly known?” So, they run for the exit.

Now, that doesn’t mean there’s nobody there to buy them. Whenever somebody sells something, somebody has to buy it. The folks buying are risk-friendly investors. And so, for example, on Wednesday, there was a treasury option and it was very well received and obviously they’re not the same guys that sold the day before, but now you have risk-friendly investors come in. And you needed to have that kind of a shake-out and have other investors go in.

Now, none of that means whether Italy is going to survive or not, but the relevant part here is that the system cracks when you build up this pressure cooker, when you have an unsustainable situation, and to me, it is unsustainable that folks, like Italians, pay a very, very small premium over – kind of a borrowing cost – than in Germany, for example.

And when this pressure builds up, well, at some point, some steam has to be let gone and, depending on how much pressure has built up, the fallout can be greater. And so, for now, people woke up and now they can deal with this crisis as a risk event, whereas, before, it was something that was kind of a black swan event, and it blew up in some people’s faces.

Mike Gleason: Let’s talk a little bit more about the implications for gold and silver markets. In recent weeks, the euro has weakened and that has been a big driver in the rally of the dollar indexes. This prompted some selling in gold and silver. On the one hand, we could see a continued euro weakness and dollar strength weighing on gold and silver prices; on the other hand, metals could get a bid if concerns over serious trouble in the EU drives some safe-haven demand. What is your best guess about which dynamic might win out there?

Axel Merk: Curiously, during much of the Eurozone debt crisis, I’m referring to several years ago, the price of the euro and gold were quite highly correlated, but anybody liking gold wouldn’t touch the euro with a broomstick. So, I’m just pointing out, as you pointed out, it’s because if the dollar strengthens that, of course, this yellow metal doesn’t change. And so, as the price of the dollar appreciates, the price of gold might go down. Now, that said, again, as volatility flares up, I do think gold is worthy of the consideration as a diversifier.

Also, the reason why I went into detail here about the yield chasers, the market didn’t trade as if the Eurozone were to break apart. By all means, bank stocks sold off, by all means, volatility surged, all kinds of things happened. But this was, here, momentum traders, yield chasers, being wrong-footed. And we had a violent unwinding of that. And that is one of the reasons why the price of gold didn’t surge in this context, because this was not a trade that said “Oh, my God, the Eurozone is going to fall apart”. Now, if that were to happen, then we going to see a very, very different picture.

We also had, for example, bonds rally, right? But there was a very, very substantial short-position bond and so a lot of these guys took profits or said “Oh, I didn’t expect it that a trade could go against me” and then when something is too good to be true, if too many people are piling the same trades, things go bad.

Now, as far as the context of how this is going to evolve, we have no idea even by the time your broadcast is, what’s going to happen next. Are they going to form a new government, are they going to have called new elections, who knows? Anything is going to happen. We have a populace resentment for all the right reasons and the European Union is incapable of communicating with the people and saying “Hey, we’re the good guys. We actually mean well for you.” People are fed up.

Now, that said, the majority of Italians do appreciate the euro and so that means they want to find a way. Also, we tend to forget that it is extremely expensive to leave the EU. It’s one thing for the Brits to leave the European Union; they don’t share the same currency. If you shared a currency, your banking system is going to be sucked empty. Your economy is going to implode if you leave. And that is something that is not really a very attractive proposition. And so, when push comes to shove, most of these countries decide, “Hey, we might want to stay.”

Now at the other end of the spectrum, though, if you have a populist rising, usually the more extreme opinions prevail. And so they are not ruling out that some bad things can happen. When I buy something in Europe, I buy the German stuff, the Northern European stuff. And ultimately, if it were to break apart while I still have that Northern European stuff, right? And that doesn’t mean buying Italian securities is necessarily a bad thing, but you better be aware of the risks that come with it and tying it back to the price of gold, the question is “Is there contagion? Is the Federal Reserve going to change course?” and so forth. In the short term, I don’t think the Fed it rattled by this. Access to credit continues to be easy. I think the Fed is going to continue to march higher.

Now, all that said, I do also think inflationary pressures in the euro’s going to move higher because I don’t think the U.S. economy is about to implode. And so, because of that, I do think people are going to continue to look at gold as a diversifier and at some point that cycle’s going to turn. I don’t know whether it’s in six months or in a year or down the road. We’re looking at these indicators, I don’t think we’re at the top of the cycle at this stage. I think it’s going to continue for another six months, maybe twelve months, and maybe even eighteen months. I can only give us like a six to ten months outlook on this.

But, for the time being, inflationary pressures are rising and the Fed is going to slowly but surely march higher.

Mike Gleason: George Soros made news this week, and I’m talking about much more than what Roseanne Barr said about him during her Ambien-induced Twitter rampage. Soros warned that Europe and even the world financial markets face an “Existential threat saying everything that could go wrong has gone wrong.”

He’s apparently quite upset at the unraveling of the Iran nuclear deal, anti-EU populism, and new calls for fiscal austerity. At the same time, he launched a campaign this week to try to reverse the Brexit decision. Is this just sour grapes by Soros or do you think the world financial markets are truly on the precipice?

Axel Merk: To understand Soros, I think the only thing one has to understand that he is Hungarian at heart. He grew up in Hungary and he loves Hungary. He would love everybody in the world, especially the European Union, to write blank checks to the Hungarians so that that country’s standard of living moves higher. And so they want the Germans to write checks, they want the French to write checks, they want everybody to write checks so that the Europeans are happy. It has nothing to do with the Eurozone being sustainable or not. I have no idea why people are listening to Mr. Soros. Sure, he had a great trade on the Bank of England, but for him, it is all about trying to support Eastern Europe. That’s very well intended. Godspeed for him, let him help these folks and he has some initiatives and foundations that does it. Great for him. But, to conclude from any word he says, whether the Eurozone is stable or not, I wouldn’t listen for two seconds to his opinion.

Now, that doesn’t mean there aren’t any issues in the Eurozone, by all means. But, a lot of people are biased when they hold a trading position, well, George Soros’s trading position is that he wants Eastern Europe to thrive. And if the West can write a check to do that, then he likes that. Anything, any tough austerity measures, anything that against that, Mr. Soros says “Don’t do it”.

And so, it’s very different answer, probably than you might have expected, or you get from other folks, but, if you look at George Soros as a person who has an agenda to help Eastern Europe, then you understand everything and anything that he says.

Mike Gleason: Getting back to the Fed here, briefly. They have been tightening, which is contributing to some of the dollar’s strength, but they almost certainly don’t want a collapse in the euro, and there is, we think, a limit to how much of a rally they’re going to put up with in the dollar. What are your thoughts there? Expand on that a bit. It seems like the markets have priced in a couple more rate hikes this year. Sounds like you think we’ll probably get those?

Axel Merk: Well, let’s think about it. We got a new Fed chair, right? Jay Powell. And he’s a lawyer. He does not have a magic framework. Bernanke had this Great Depression framework, Yellen was a labor economist, well Powell is a lawyer. And he’s a smart lawyer. And he has good intentions. So, what do lawyers do? Well, they call a committee to decide on things. So, one thing you can be sure of with Powell, in my view, is that he’s not going to be very fast. He’s going to call the best and the brightest, to give him their opinion, and then he’s going to make a judgment based on that. And that might be a very boring answer, but, that’s what it is. And the one thing that a Powell Fed will look at is A, is the economy going to continue to move ahead, is the “slack” exhausted, and are financial conditions all right?

One of the things Yellen always said is that “Hey, our quantitative tightening is like watching paint dry on a wall and it’s really nothing.” Well, that’s a bunch of BS because the whole point of raising rates is to tighten financial conditions. But, at the same time, it hasn’t happened. The financial conditions have been easing. In early 2016, the Fed panicked because the fracking market didn’t do well. This time around, stock marks has had a hiccup or so, but access to credit hasn’t been any tighter. So, as long as access to credit is not tightening, the Fed is going to continue to march.

And what we have is, the typical thing at this time of the cycle is that banks are actually easing lending standards. Because the economy is doing all right, they want to write more credit. And that’s why the Fed is going to continue to tighten. Now, as that happens, of course, at some point they’ll overdo it and push the economy into a recession and maybe they’re geniuses and do a soft landing, but that’s usually more luck than anything else.

And so, at the same time, they’re not in a rush. Last year was the first year in many, many years where the Fed tightened more than was priced in the beginning of the year. This year, I would think the same thing can happen again and what has happened over the last week to ten days is that rate hikes expectations has come down quite significantly, obviously, partially because of what happened in Italy.

Now, that said, 85% of the U.S. economy is domestic, 15% is international. And so, unless Europe blows up the next day, I don’t think the Fed, in the near term, can change course. Also, keep in mind, by the way, just a word back on Italy. Italy has had about one government a year. And so even if they have a new election, even if they elect a more populist government, odds are that their new government is not going to survive very long. There’s a European parliament election next year and the two populist parties, if the two are going to buddy up, and that’s still an if, they might get into an argument because, ideologically, they’re not exactly aligned.

And so, a lot of things can happen, and the Fed is not going to pay attention to that because they going to say “Hey, if something does blow up in our face, we can still reverse course”. And so, it’s very different from the Yellen Fed in early 2016, when it was spooked about equity markets going down. And the reason they were spooked about it is because access to credit in the fracking industry was at risk of spilling over to the rest of the economy. At this stage, we see no signs that access to credit is tighter, so they’ll continue to march ahead.

Now, what does it mean for metals? It doesn’t necessarily mean it’s bad, because the pace at which they’re moving is very slow and, by the way, we are already at extremely low unemployment. The labor participation rate is slowly inching higher. I happen to think that in about six months we’ll have exhausted that so-called slack, which means inflationary pressures are going to accelerate. And that’s exactly when the Fed is going to be at a point where it’s going to slow down the economy. And so, we going to have this inflationary push at the end of this economic cycle where the Fed is, in my view, not going to be fast enough to do something about it. And then, because of the higher rates causing more volatility in the markets, in my view, all of that are reasons why precious metals historically, do reasonably well at the end of an economic cycle, which we’re going to see presumably a year from now, or whenever it’s going to be.

Mike Gleason: Yeah. Very well put. There’s a lot of things circling about, and I think you summarized that all very well. As we begin to close here, any other news stories that you’re going to be watching closely as we progress throughout the year, Axel?

Axel Merk: Well, we’ve got a European Central Bank meeting in June 14th. So, in the short term, that’s probably the most interesting event. Whether anything is going to happen, the one thing that Mr. Draghi is not going to do is he’s not going to take options off the table, which means he’s not going to announce the end of QE. There might have been an early chance for him to do it, but, with what’s happening in Italy, he’s not going to do it.

The one thing to keep an eye on there is, what I think may happen in the Eurozone is that they have indicated they’ll stop QE before they’ll start tightening. I wouldn’t be surprised if they’ll get more flexible in that. Meaning that they’ll start hiking rates. At the same time, at some point, if the crisis were to escalate, Mr. “Whatever-It-Takes” Draghi is going to say “Hey, but, we’re not going to allow Italian bonds to trade at too much of a premium” and so to interfere in the markets that way. But they have to, in my view at least, get off that negative interest rates because it’s creating havoc in the rest of the Eurozone that’s actually doing quite well. So, he might, again, pull up some ace up his sleeve where he’s going to say “Yep, rates are going to move higher, but only for Germany and the Northern European countries, whereas, for Italy and others, we’ll guarantee that rates are not going to move higher”.

And before you dream too far ahead, just keep in mind, Draghi’s job is coming to an end at the end of next year, so, as we go towards the end of this year, people are going to speculate who’s going to succeed him. But that’s a story for another day.

Mike Gleason: Yeah, we seem to be focusing a lot of our interest on Europe, once again here. It seems like we’ve been down this road before.

Well, good stuff as always, Axel. It’s great to get your perspective on these matters and we look forward to catching up with you again later this year. Now, before we let you go, please tell listeners a little bit more your firm and your services and then also how they can follow you more.

Axel Merk: Sure. The firm is, my name, Merk Investments. Look us up. Sign up for our newsletter on our website. Follow me on Twitter, that’s really the best way to be in tune of what is happening there. We have several funds, including a gold fund. And we provide some services to institutions and other folks. But come to MerkInvestments.com and browse around.

Mike Gleason: Excellent stuff. Thanks again, Axel. Appreciate your time and hope you enjoy your summer and thanks for joining us again. Take care.

Axel Merk: Yep. My pleasure. Take care.

Mike Gleason: Well, that’ll do it for this week. Thanks, again, to Axel Merk, President and Chief Investment Officer of Merk Investments, Manager of the Merk Funds. For more information, be sure to check out MerkInvestments.com and follow him on Twitter. His handle is @AxelMerk.

Check back here next Friday for our next weekly Weekly Market Wrap Podcast. Until then, this has been Mike Gleason with Money Metals Exchange, thanks for listening and have a great weekend everybody.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

Market expectations of a probable US interest rate hike in June were reinforced by today’s blockbuster U.S jobs report which illustrated steady growth in the US labour market.

The US economy created 223,000k jobs in May while the unemployment rate unexpectedly dropped to its lowest level in 18 years to 3.8% from 3.9% in April. With average hourly earnings exceeding estimates by rising 2.7% YoY, speculation may heighten over the Fed adopting a more aggressive approach towards monetary policy normalization this year. Interestingly, Dollar bulls were unimpressed by today’s solid US jobs report with the Dollar Index trading around 94.15 as of writing.

Focusing on the technical picture, the Dollar Index remains bullish on the daily charts as there have been consistently higher highs and higher lows. An intraday breakout above 94.35 could encourage an inline higher towards 94.50 and 95.00, respectively. Alternatively, a failure for prices to keep above 94.00 could result in a decline towards 93.40.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

A Vancouver-based miner diversifies by adding a Brazilian portfolio to its Mexican project.

Leagold Mining Corp. (LMC:TSX.V; LMCNF:OTCQX) announced on May 24 that it has closed its acquisition of Brio Gold. This is a major milestone in the company’s goal to become a mid-tier gold producer with a focus on Latin America.

The Brio acquisition brings three operating mines, a near-term gold mine restart project and two development projects, all located in Brazil.

Neil Woodyer, Leagold CEO, stated: “We are very excited about Leagold’s new position as a mid-tier gold producer with the growth of our production rate to over 400,000 ounces per year. Our business and market profiles are strengthened by our diversification in both Mexico and Brazil and across four operating mines. Leagold’s measured and indicated resources have increased to 16.4 million ounces and proven and probable reserves have increased to 5.6 million ounces.”

The company’s original project is Los Filos, where it is operating two open-pit mines, Los Filos and Bermejal, and one underground mine. Leagold acquired Los Filos from Goldcorp in 2017.

Leagold is continuing exploration activities at the Los Filos Underground Mine and earlier this month announced high-grade drill results of 24.2 grams per tonne (g/t) over 4.10 metres, 23.6 g/t over 6.95 metres, and 9.1 g/t over 8.69 metres. The company has stated that the goal of the drill program is to “identify additional resources to replace reserves and extend the overall mine life. The program is on track with over 12,000 metres of step-out drilling completed to date and the majority of the exploration drilling to take place in the second half of this year.”

The company plans to incorporate the drill results into a final resource estimate by the end of the year.

Peter Marrone, CEO of Yamana Gold, has accepted a position on Leagold’s board. Yamana holds a 20.5% stake in the company.

Leagold has gained the attention of industry analysts. CIBC just initiated coverage of Leagold with an Outperformer rating and a 12- to 18-month target price of $5 per share. Leagold’s shares are currently trading at around $2.87.

Analyst David Haughton of CIBC wrote on May 29 that “an experienced operating and development team backed by a solid balance sheet should offer investors greater assurance that Leagold can achieve the full potential of the Brio assets and Los Filos.” He sees the company having a strong platform for growth, noting that the firm expects Leagold to “produce ~365koz in 2018 and potentially over 700koz by 2020E. The near-term focus is to improve each operation, to redevelop Santa Luz, and to complete the Bermejal underground at Los Filos. Upside of the possible Los Filos CIL development could offset any changes in outlook for the higher-risk Santa Luz project.”

“Leagold provides an attractive combination of a better-than-average growth profile and value amongst mid-tier gold producers. The P/NPV of just 0.5x at spot reflects the legacy issues at Brio that Leagold has the opportunity to improve,” Haughton concluded.

Jamie Spratt, an analyst with Clarus Securities, noted on May 4 that Leagold “currently trades at a ~50% discount to peers on a P/NAV basis and in our view, this provides a deep value re-rating opportunity with continued management execution and a successful integration of the Brio assets.”

Clarus has a target price of $6.24 and gives Leagold a Buy rating.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure: 1) Patrice Fusillo compiled this article for Streetwise Reports LLC and provides services to Streetwise reports as an employee. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Leagold Mining Corp. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

Disclosures from CIBC, Leagold Mining Corp., May 29, 2018

Analyst Certification: Each CIBC World Markets Corp./Inc. research analyst named on the front page of this research report, or at the beginning of any subsection hereof, hereby certifies that (i) the recommendations and opinions expressed herein accurately reflect such research analyst’s personal views about the company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analyst’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Analysts employed outside the U.S. are not registered as research analysts with FINRA. These analysts may not be associated persons of CIBC World Markets Corp. and therefore may not be subject to FINRA Rule 2241 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

Potential Conflicts of Interest: Equity research analysts employed by CIBC World Markets Corp./Inc. are compensated from revenues generated by various CIBC World Markets Corp./Inc. businesses, including the CIBC World Markets Investment Banking Department. Research analysts do not receive compensation based upon revenues from specific investment banking transactions. CIBC World Markets Corp./Inc. generally prohibits any research analyst and any member of his or her household from executing trades in the securities of a company that such research analyst covers.Additionally, CIBC World Markets Corp./Inc. generally prohibits any research analyst from serving as an officer, director or advisory board member of a company that such analyst covers.

In addition to 1% ownership positions in covered companies that are required to be specifically disclosed in this report, CIBC World Markets Corp./Inc. may have a long position of less than 1% or a short position or deal as principal in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon.

Recipients of this report are advised that any or all of the foregoing arrangements, as well as more specific disclosures set forth below, may at times give rise to potential conflicts of interest.

Important Disclosure Footnotes for Leagold Mining

· CIBC World Markets Inc. expects to receive or intends to seek compensation for investment banking services from Leagold Mining Corporation in the next 3 months.

Disclosures from Clarus Securities, Leagold Mining Corp., May 4, 2018 The analyst has visited the Company’s mining operations in Mexico. Partial payment or reimbursement was received from the issuer for the associated travel costs.

The research analyst and/or associates who prepared this report are compensated based upon (among other factors) the overall profitability of Clarus Securities and its affiliate, which includes the overall profitability of investment banking and related services. In the normal course of its business, Clarus Securities or its affiliate may provide financial advisory and/or investment banking services for the issuers mentioned in this report in return for remuneration and might seek to become engaged for such services from any of such issuers in this report within the next three months. Clarus Securities or its affiliate may buy from or sell to customers the securities of issuers mentioned in this report on a principal basis. Clarus Securities, its affiliate, and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities discussed herein, or in related securities or in options, futures or other derivative instruments based thereon.

Each Clarus Securities research analyst whose name appears on the front page of this research report hereby certifies that (i) the recommendations and opinions expressed in the research report accurately reflect the research analysts personal views about the Company and securities that are the subject of this report and all other companies and securities mentioned in this report that are covered by such research analyst and (ii) no part of the research analysts compensation was, is, or will be directly or indirectly, related to the specific recommendations or views expressed by such research analyst in this report.

Brian Szeto, an analyst with PI Financial, relayed this gold explorer/developer’s first pass at assessing its lead asset.

In a May 29 research note, PI Financial analyst Brian Szeto reported that Revival Gold Inc. (RVG:TSX.V) announced an NI-43-101 compliant, maiden resource estimate for its flagship Beartrack gold project in Idaho; the resource estimate far exceeded PI Financial’s forecast.

The initial resource, based on 458 holes comprising 71,000 meters of drilling, was 2 million ounces (2 Moz) gold at an average grade of 1.22 grams per ton (1.22 g/t). About 61% of the resource is in the Indicated category, and roughly 17% is made up of oxide material. Further, the deposit remains open at depth and to the south.

The base case, Szeto pointed out, assumes a US$1,300 per ounce gold price and a cutoff grade of 0.6 g/t. With a higher cutoff grade of 0.8 g/t, “there are still 1.3 Moz within the resource block model.”

The analyst noted that PI Financial views this reported 2 Moz gold resource size as “very positive.” He added, “We had been expecting an initial resource of approximately 1 Moz, so the resource announced today is significantly above our expectations.” Also impressive, he wrote, is how quickly Revival advanced Beartrack to this stage, in about seven months post acquisition.

Because Revival aims for a 3 Moz resource at Beartrack and Arnett Creek, “this resource means it is well on its way to achieving that goal,” Szeto indicated. PI Financial is confident the company will grow the project’s resource sufficiently to restart mining operations there.

Szeto reiterated that historically, Beartrack produced 609,000 ounces of gold at 1.34 g/t between 1995 and 2002, when mining was stopped due to low gold prices. Over the period the mine was running, PI Financial determined, the cash cost averaged US$200250 per ounce but was down to US$140/ounce in the latter days of operation.

For Buy-rated Revival, PI Financial derived a net asset value of CA$3.05 per share and a target price of CA$1.70 per share. Today, the company’s stock is trading at around CA$0.85 per share.

Want to read more Gold Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent articles and interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure: 1) Doresa Banning compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. She or members of her household own securities of the following companies mentioned in the article: None. She or members of her household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: Revival Gold. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article. As of the date of this article, officers and/or employees of Streetwise Reports LLC (including members of their household) own securities of Revival Gold, a company mentioned in this article.

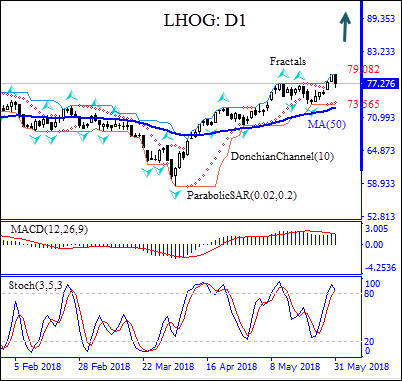

Rising US pork exports indicate strong pork demand. Will the LHOG continue rising?

US pork export demand is strong: exports hit historic record in 2017 exceeding $1 billion in total value. Recent trade agreements also point to increasing export trend this year too: the new export agreement with South Korea provides for essentially duty free export of US pork into that country, with latest data showing an increase in volume of about 33% for February. US pork demand is up in Central and South America too, and trade agreements support higher export into that area. At the same time seasonally high domestic demand is expected as the Memorial Day weekend marked the unofficial beginning of the summer grilling season. Higher demand is bullish for pork prices.

On the daily timeframe the LHOG: D1 has been rising after hitting 7-month low in the beginning of April. It is above the 50-day moving average MA(50) which is rising too.

The Parabolic indicator has formed a buy signal.

The Donchian channel indicates no trend yet: it is flat.

The MACD indicator gives a bullish signal: it is above the signal line and the gap is widening.

We expect the bullish momentum will resume after the price breaches above the upper Donchian bound at 79.082. A price above that level can be used as an entry point for a pending order to buy. The stop loss can be placed below the lower Donchian bound at 73.565. After placing the pending order, the stop loss is to be moved to the next fractal low, following Parabolic signals. By doing so, we are changing the probable profit/loss ratio to the breakeven point. If the price meets the stop loss level (73.565) without reaching the order, we recommend canceling the order: the market sustains internal changes which were not taken into account.

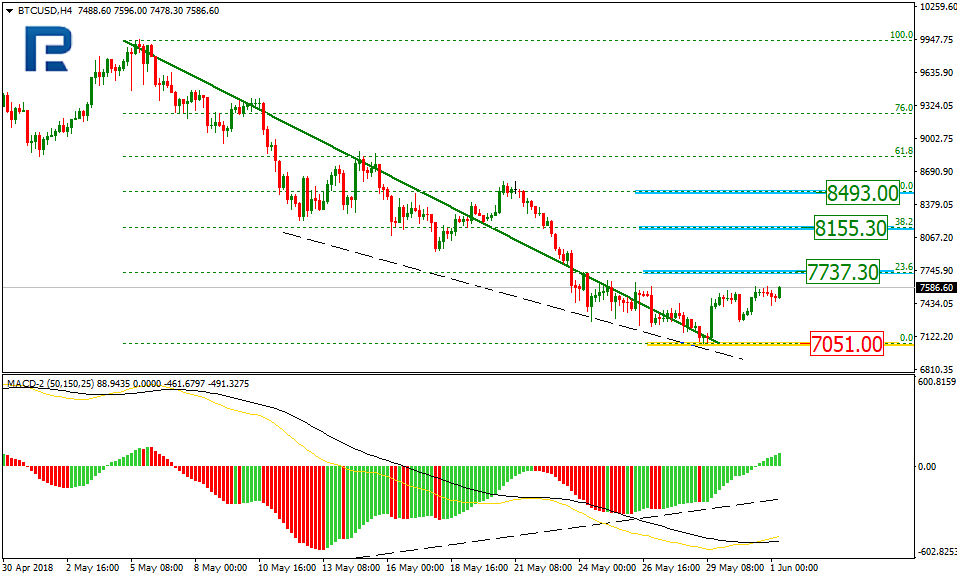

As we can see in the H4 chart, the downtrend continues; at the same time, the convergence is being formed, which may indicate a possible pullback to the upside. The targets of this pullback may be the retracement of 23.6%, 38.2%, and 50.0% at 7737.30, 8155.30, and 8493.00 respectively. The support level is the low at 7051.00.

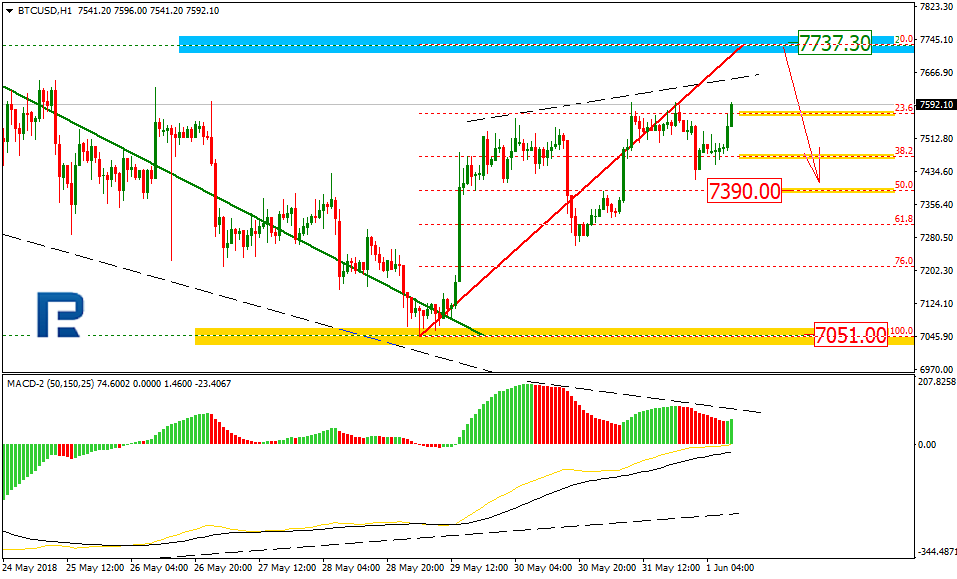

As we can see in the H1 chart, BTCUSD is growing towards 7737.30. At the same time, one can see the divergence being formed, which may indicate a new correction downside. The target may be the retracements of 50.0% at 7390.00.

ETHUSD, “Ethereum vs. US Dollar”

As we can see in the H4 chart, the convergence made ETHUSD finish the downtrend and start a new correction, which has already reached the retracement of 23.6% and right now is trading towards the one of 38.2% at 596.00. The next upside targets may be the retracement of 50.0% and 61.8% at 623.40 and 651.00. The support level is at 504.50.

The H1 chart shows more detailed structure of the current movement.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Precious metals expert Michael Ballanger dissects his volatility trades.

One week ago today, I made the following commentary:

“Finally, I am officially revisiting the “volatility trade” (VIX: CBOE Volatililty Index) but unlike February where I used the UVXY (ProShares Trust Ultra VIX Short) as my proxy for the increase in volatility, I am using the TVIX (VelocityShares Daily 2X VIX ST ETN) because it is a double leverage ETF for the VIX but has better leverage than the UVXY. UVXY used to be a triple-leverage play on volatility but the slippage due to its dependence on futures became too difficult to navigate and they cut the leverage from 3:1 to 2:1. I had a 250% gain on this in February but gave back 9.84% in April. I am long 50% of the TVIX position from yesterday at $4.95 and am using the opening this morning to add another 25% in the $5.25 range. I will again use a 10% stop-loss but since the 52-week low is $4.60, that will be the exit level. Upside target will be $8.00 remembering of course that the 52-week high was $26.56.

The month of May is rapidly coming to a close, which starts what is historically the worst six months of the year. With the situations in Turkey and Italy worsening, with the North Korean summit in question, central banks engaged in “quantitative tightening,” rising oil prices, and the possibility that the China-U.S. trade talks go south, markets are going to be in peril as summer illiquidity arrives. For this reason, gold “should” be the go-to asset, but I am banking on volatility rather than gold as the preferred method of riding the correction.”

In the Monday overnight session, the words “panic,” “contagion,” and “implosion” were being bandied about while the S&P futures were off sharply when I arrived at the gym yesterday at 7:00 a.m. Sure enough, gold and silver did not respond to the developing crisis in Europe because U.S. dollar strength is significantly more important to gold demand than Italy and Spain vaporizing in front of our very eyes.

Monetary panic doesn’t throw the slightest of bids into the precious metals any more because they can simply buy the VIX as a hedge because gambling on a piece of financially engineered paper like the VIX ETFs is infinitely more sensible than owning a monetary metal with 5,000 years of well-earned legacy as a preserver of wealth. The huge sell-off in gold initially in response to the currency swing was reversed in the Tuesday afternoon session and what was a $12.30 loss became a slight positive by 2:00 p.m. The chart below of the VIX index shows a gap on January 29, which precluded the moonshot to $49.21 a week later. Since I have been accumulating the TVIX under $5.00 all last week and on Monday, Tuesday’s 38.2% move in the VIX Index was accompanied by a 25.5% move in the TVIX. While our $8.00 target seems a tad conservative given the move in February to $26.56, I have grown to appreciate base hits and doubles over home runs lately, which might be a function of my age or pondering last year’s capital gains/losses report completed last month.

Wednesday’s 38-point rebound in the S&P 500 caused the VIX to give back 13.69% and the TVIX to give back 9.1%, but I continue to gather in “VOL” on dips because those two gaps in January and againTuesday day may be indicative of a violent return of the type of action that allows for a 250% return in eight days as we experienced back in very early February. Furthermore, to have a 32-point decline followed the very next day with a 35-point rebound followed by today’s 18-point drop is classic volatility, and that is not the type of stock market behavior that instills investor confidence.

/p>

The next big story and one which is being underplayed by the financial media is the current debacle called Deutsche Bank (DB:US), which this morning took out the lows of September 2016 and is now resembling a company in severe duress. I did a quick scan of headlines for DB over the past five years and notwithstanding that DB holds the largest derivatives book on the globe, this bank has been infested with numerous problems over the last few years. Mortgage fraud, gold manipulation, Libor fraud and now massive layoffs would imply that all is not well with this behemoth that truly is the ultimate in “Too Big to Fail” financial institutions. The leverage they carry representing sovereign debt positions would create a counterparty contagion the likes of which would make the 20072008 subprime crisis look like May Day picnic. The fact that they are the one bullion bank most responsible for the overt and unsanctioned shenanigans in gold and silver makes their current woes doubly satisfying for metals buffs like us, but you must realize that having Deutsche Bank implode would send shock waves through all of our markets triggering gargantuan liquidity squeezes, which means that long positions in everything would be thrown overboard in order to reduce the leverage that is keeping these markets afloat. This is again why I see the volatility trade as the best method of protecting one’s wealth given the vacuous moves by the Trump administration to impose tariffs on Mexico, Canada and the Eurozone.

Interestingly, the only way to judge the collective risk appetite of the junior resource sector is to glance (if you can stomach it) at a chart of the TSX Venture Exchange (CDNX) which, after reclaiming the 800-level back in April, has once again succumbed to seasonal weakness and is threatening to take out the April low around 754. Every year, I always make a vow to reduce my exposure to zero by the end of March with a view to buying back my favorite TSX.V juniors between mid-August and Labor Day and every June I wind up kicking myself in my own backside for failing to listen in earnest to my own wise counsel. There are isolated pockets of strength out there but they are invariably found in “story stocks” and usually related to something other than gold or silver or exploration issues. It is truly incredible to look back at a chart of the TSX.V from 2001 to 2007 and to recall the moves we enjoyed in the Senior Golds (GDX) and even greater gains in the Junior Golds (GDXJ). Even after the Financial Crisis and meltdown in 20072008, the rebound in the TSX.V from the Crash lows of late 2008 at 666 saw a number of exploration issues perform exceedingly well even though the TSX.V could only rally to two-thirds of its 2007 peak.

TSX Venture 2001-2008

TSX Venture today

So why do I feel it necessary to remind us all of just how LOUSY the juniors have acted since 2011? It is because of charts like this one shown below, which is that of Novo Resources Corp. (NVO.V) whose Karratha gold project in the western part of Australia has been compared to the mighty Witwatersrand region of South Africa. A few months back in October I made this remark regarding NVO: “I sincerely hope that the all of this pseudo-scientific analysis surrounding these so called “Witwatersrand characteristics” have not replaced actual drilling or (better still) bulk sample results as justification for owning the stock.”

The stock peaked in October 2017 at around $8.50, and after I had finished reading all of the reports on the exploration merits of the Pilbara region, I concluded that it was about as close to a perfect “story” as could ever be written. In fact, it was such a good story that it brought to mind the words of a famous mining promoter from the 1970s who coined the phrase “Why ruin a great property by drilling it?” Falling squarely into the category of “You just can’t make this sh1t up!,” to compare this as yet untested region to the Witwatersrand is analogous to comparing Mark’s Work Warehouse to Amazon. The Witwatersrand has produced over 1.7 billion ounces of gold since the initial discovery in 1886. At today’s gold price, that is $2,292,160,000,000 (U.S.) worth of metal so it is quite easy to see how NVO.V could command a speculative market cap of over $1.3 billion with that kind of upside potential being used as a financial divining rod.

Now, I am not casting any negative dispersion on the Pilbara play or any of the people behind it. I am simply pointing out that when the little green monster called “Baron von Greed” arrives at your door, you better be careful because when the Bre-X fraud was revealed in April 1997, it took five years and billions of dollars of lost value to heal things up. For the sake of the junior mining market, I have been rooting for the Pilbara play NOT because I am a shareholder in NVO; I am actually praying for it because I am a shareholder in the same sector. If investors wind up on the scrap heap of failed dreams because the bulk sample results showed distinctly un-Witwatersrandian characteristics, it hurts all of us as if we had owned it at $8.50.

Today’s drop in the Pilbara stocks included Pacton Gold (PAC.V), which was $0.05 last November and which traded up to $1.02 on Monday and which sits at $0.49 today, down 42% on the day and less than half of the 52-week high. I mention this as a living example of how being associated with a “story stock” can be a double-edged sword with lethal consequences once the speculative bloom is off the proverbial rose.

What is actually needed this summer is a major new exploration discovery in a friendly jurisdiction (like Nevada) where assay results reveal a wide intercept of high-grade rock in a previously untested area that gives rise to a massive land rush with massive dollars moving to acquire ground. It happened in northwest Ontario in 1981 (Hemlo); it happened in Canada’s Northwest Territories in 1991 (Dia Met/Ekati); and it happened more recently (2009) in the Yukon after Underworld announced a discovery at Golden Saddle and was eventually acquired by Kinross. What gave those areas plays credibility was the arrival of the majors by way of investments in the junior discovery names. Lac Minerals moved in early at Hemlo; BHP Billiton and RTZ arrived very early in the NWT and Dia Met; and as mentioned, Kinross lit things up by taking out Underworld. So, when you look at the Pilbara play, there is no presence (that I am aware of) of any majors other than the investment made by Kirkland Lake Gold through private placement in NVO and while Kirkland Lake Gold is a fine company, it is no BHP.

As a final note, all Pilbara investors should remember that in 1994, there was a severe correction in the Canadian diamond explorers (including Dia Met and Aber) when Kennecott revealed that a bulk sample taken from one of the kimberlite pipes had proved barren after the junior JV partner, DHK Diamonds, had reported significantly higher grades. After the massive sell-off in all of the exploration juniors nearly crippled the area play, it eventually turned out to be a false alarm because BHP bought out Dia Met and fortunes were eventually made in Dia Met, Aber and Mountain Province. Perhaps today’s panic attack in NVO and its brethren will prove to be a similar false alarm.

I wrap up with today’s missive with two charts representing the two hottest sectors of the Canadian markets as measured by speculative interest. I showed you all back in December how the introduction of Bitcoin futures on the CME was the lasso used by the bankers to reel in BTC. Within literally days of that event, BTC topped out and now resides at a mere 38% of its December 2017 peak. Cannabis stocks are led by Canopy Growth, which was the first shot out of the decriminalization cannon and is the poster child for the Canadian medical marijuana industry, hence the stock symbol W-E-E-D. The mania in the Canadian crypto-deals fell off a cliff here in 2018 with massive losses turning up everywhere on the Street. I have the distinct feeling that based upon the number of marijuana stories out there and based upon WEED’s $7 billion market cap, Canadian marijuana deals might be ripe for a crypto-crack-up any time now.

One way or another, whether it is Tesla or Bitcoin or Novo or WEED, these “story stocks” are elevated in a cloud of hopium and greed, and since they represent the heart of the speculative market mindset, owning a smidgeon of “volatility” through the TVIX does not appear to be an imprudent move.

Originally trained during the inflationary 1970s, Michael Ballanger is a graduate of Saint Louis University where he earned a Bachelor of Science in finance and a Bachelor of Art in marketing before completing post-graduate work at the Wharton School of Finance. With more than 30 years of experience as a junior mining and exploration specialist, as well as a solid background in corporate finance, Ballanger’s adherence to the concept of “Hard Assets” allows him to focus the practice on selecting opportunities in the global resource sector with emphasis on the precious metals exploration and development sector. Ballanger takes great pleasure in visiting mineral properties around the globe in the never-ending hunt for early-stage opportunities.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Disclosure: 1) Michael J. Ballanger: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: None. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies referred to in this article: None. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are below. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article, until one week after the publication of the interview or article.

All charts and images courtesy of Michael Ballanger.

Michael Ballanger Disclaimer: This letter makes no guarantee or warranty on the accuracy or completeness of the data provided. Nothing contained herein is intended or shall be deemed to be investment advice, implied or otherwise. This letter represents my views and replicates trades that I am making but nothing more than that. Always consult your registered advisor to assist you with your investments. I accept no liability for any loss arising from the use of the data contained on this letter. Options and junior mining stocks contain a high level of risk that may result in the loss of part or all invested capital and therefore are suitable for experienced and professional investors and traders only. One should be familiar with the risks involved in junior mining and options trading and we recommend consulting a financial adviser if you feel you do not understand the risks involved.

EURUSD has finished the ascending structure and is about to start form a new descending wave towards 1.1616. Possibly, today the price may reach this level and then grow towards 1.1671, thus forming another consolidation range. If later the pair breaks this range to the upside, the market may continue the correction to reach 1.1818; if to the downside – resume falling inside the downtrend with the target at 1.1400.

GBPUSD, “Great Britain Pound vs US Dollar”

GBPUSD has rebounded from 1.3350 downwards. Possibly, the price may start another decline to reach 1.3190 and then grow towards 1.3290. Later, the market may continue trading to the downside with the target at 1.3075.

USDCHF, “US Dollar vs Swiss Franc”

USDCHF is trading to rebound from 0.9835. The target is at 0.9895. Later, the market may form a new descending structure towards 0.9815 and then grow to reach 0.9960. After breaking this level upwards, the instrument may continue trading to the upside and reach 1.0100.

USDJPY, “US Dollar vs Japanese Yen”

USDJPY is being corrected towards 109.64. After that, the instrument may start another decline with the first target at 107.87.

AUDUSD, “Australian Dollar vs US Dollar”

AUDUSD is consolidating around 0.7561. According to the main scenario, the price may break this range upwards and grow to reach the short-term target at 0.7645.

USDRUB, “US Dollar vs Russian Ruble”

USDRUB is still consolidating and forming a downside continuation pattern. Today, the price may fall to reach 60.08 and then start another growth towards 61.62.

XAUUSD, “Gold vs US Dollar”

Gold has rebounded from 1306.99 once again. Possibly, the price may form a new descending structure to reach 1288.00, break it, and then continue trading to the downside with the target at 1240.00.

BRENT

Brent has completed the ascending impulse and right now is being corrected towards 76.15. Later, the market may grow to reach 80.00 and then start another decline towards 78.50. After that, the instrument may form a new ascending wave with the target at 82.11.

Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.