By www.CentralBankNews.info Armenia’s central bank raised its benchmark refinancing rate by 50 basis points to 8.50 percent, saying it expects inflation to slowly decline in coming months amid slower economic growth, which will allow the central bank to loosen monetary conditions.

The Central Bank of Armenia (CBA), which has held rates steady since September 2011, said headline inflation rose by 0.4 percent in July for an annual rate of 8.5 percent, up from 6.5 percent in June.

“The council agreed that inflation will gradually return to target levels and will remain in the permissible variation range,” the CBA said.

The Armenian central bank targets inflation of 4.0 percent within a 1.5 percentage point band.

Apple, To Be Followed In The Next Period

Article by Investazor.com

Apple is back on the game, or better said… it always lead the mobile phone industry? At least on the American market, Apple is indeed the one with the greatest influence. According to a research made by Nielsen, 40% of American smartphone users own an iOS mobile device while 24.7% use mobiles with android operated by Samsung.

Another surprise is to come in less than a month. On 10th of September, a new iPhone will be launched, iPhone 5S which is expected to bright by its brand new operating system iOS 7. Investors already started to buy Apple shares, given the momentum that is expected next month.

The third quarter’s result for Apple disappointed. Comparing with last year-quarter ($8.8 billion net profit), this quarter reported only $6.9 billion. The CEO Tim Cook was proud to announce increased sales on mobile phones and strong growth in revenue from iTunes, Software and Services. Increasing the divided on share at more than $3, in its latest earnings report Apple declared itself satisfied by returning $18.8 billion in cash to shareholders through dividends and share repurchases. Next month will cause trepidations and investors will find out if Apple is indeed going in the right direction after losing its founder, Steve Jobs. Lately, Apple announce that will launch several products which will be cheaper, news that could affect the quality product picture that represents the company.

The post Apple, To Be Followed In The Next Period appeared first on investazor.com.

The Beginner’s Guide in Forex Trading

Article by Investazor.com

What is Forex?

First of all let us get to know what Forex actually is. The name Forex comes from foreign exchange and it is specific to currencies market. After the accord from Breton Woods, that took place in 1971, the currencies were allowed to change freely against one another so their value started to vary. The commercial and investment banks took the opportunity and offered the process of exchange to their clients creating this way a speculative environment for trading on currency against another. The foreign exchange market started to be better known with the help of the internet and the online brokers.

The stock exchange is a regulated market in which you know the traded volume, the traders and why the stock is traded. Forex is a OTC (Over the Counter) market because, simply said, it incorporates every currency exchange done anywhere at any time, so it is pretty hard to regulate something that doesn’t have a headquarters and the trades cannot be registered.

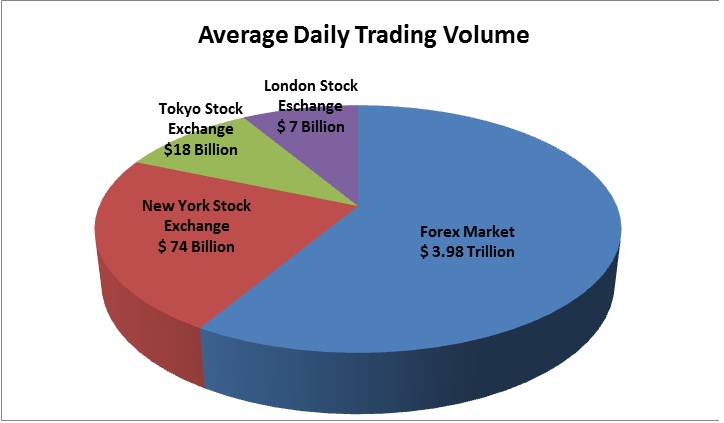

Practically if you want to change dollars for euros you go to the bank and change them, but you can also get some euros for your dollars from a European friend. Both ways you take part in the Forex market, but it doesn’t mean that you can move the Euro – Dollar pair exchanging 100$, 1.000$ or even 1.000.000$. Forex has the biggest amount of money involved every day. As you can see in the chart, an estimate daily volume is about 3.98 trillion dollars, more than on any other regulated exchange.

The biggest players in the Forex market are usually the Commercial Banks followed by investment funds, hedge funds, corporations and brokerage houses. The highest liquidity it is found at the biggest players so if an exchange is needed it can be done with banks with a huge spread (bid/ask difference) if the sum of money is small and with a very small spread if the sum of money is considerable.

Why Forex?

Foreign exchange came first as a necessity. If an US investor would like to invest in another country he would have to use that countries money so he would have to change the US dollars in the other currency. If a company would like to make a purchase of another company from another country it will have to change between currencies and the examples can go on.

Because of the fluctuating value of one currency an investment would suffer from the currency devaluation so the need to hedge came next. From here it was only one step to speculation. Nowadays speculation is one of the most important features of the Forex market and it is done starting with the biggest players all the way to a retailer.

Banks traded huge amounts of money with low costs. If a retails would like to do the same exchange with a lower volume he will get big costs that eventually will not pay for the bother. For this the financial system invented derivatives like futures and CFDs which gives you the benefit of leverage. Using the leverage with a brokerage house will give the retail not only the possibility to win more, but also lower costs for the trade. Keep always in mind that higher leverage brings bigger wins but also bigger losses.

To conclude if you have a big amount of money to invest the forex market will give you an opportunity to make some profits, but it can do the same for a trader with a smaller account thanks to leverage and brokerage houses which offers this services.

4 myths in Forex trading

It is well known that less than 20% from the forex traders are winners, around 15% are keeping themselves on the breakeven and about 65% are been thrown out of this environment.

1. Leverage is one reason to blame for the losses. It is not true, at least not entirely. The leverage increases the possibility of win and loss but as a trader you will always be in charge of your trading volume. The trader can adjust his investment to respect a certain money management. A trader can always cut his losses using tools like Stop Loss and leave his profit pile up if the market runs in his favor. If a trader losses money trading with leverage than he will certain lose money trading without leverage.

2. News Feed and information are considered to be another factor that sends traders to losing money. Again nothing could be less true. Banks, investment funds and other type of investors have access to the same news and economic data as any other trader or investors. The only difference is the services that are used to get the news. A paid service will give you a head start while a free service will give you the news with a lag. A trader can always adjust his strategy to combat this issue so that it will not be a problem in his day to day trading.

3. The money invested will always make a difference between traders. It is well known that there is a higher probability to erase the deposit if the amount is a small one, especially if it comes to a novice trader. When it comes to a professional trader the amount of money invested will not be a problem because he will always know to portion his every trade so that he will put and earn more money on the high probability trades. Each investment fund, bank or private investor has its own money management strategy suited for the investment.

4. Volatility is a factor that should be taken into consideration while trading. Forex market is known for its high liquidity and volatility and sometimes traders blame them for their losses. In fact volatility is the one that helps the professional traders to make more money. They adjust their system to the market; they modify their strategy and the money management so that the volatility will bring them an important income. Options are usually used in volatile markets.

A trader that has lost money will easily blame the leverage, the lack of information, the market volatility or the fact that he did not have enough money in his trading account. But the main reasons for the loss sit in his lack of knowledge and discipline, not having a strategy that includes a good money management and probably the most important he is driven by his emotions.(we will talk about them in our next articles).

Our recommendation

Even though it seems a very simple and accessible domain in which anyone can invest from as little as 10 bucks to millions of dollars, you should always bear in mind that it involves risks of losing money. Starting your trading experience in Forex could result in empting your account, but the good part is that you can start with a smaller balance than in stock or futures trading.

As a beginner you should better start with an amount of money that you can lose and consider it your education fee. The experience of trading on real account it does not resemble with the experience of trading on a demo account. The majority of mistakes done by traders are caused by emotions like fear and greed which appear while trading with real money.

The post The Beginner’s Guide in Forex Trading appeared first on investazor.com.

Icahn claims large stake in ‘undervalued’ Apple

Icahn claims large stake in ‘undervalued’ Apple (via AFP)

Icahn claims large stake in ‘undervalued’ Apple (via AFP)Corporate raider Carl Icahn said Tuesday he has taken a “large position” in Apple, calling the US tech giant “extremely undervalued.” Icahn, who is in the midst of a fierce battle over computer maker Dell and has a history of taking stakes in firms…

US July retail sales rise 0.2 percent

US July retail sales rise 0.2 percent (via AFP)

US July retail sales rise 0.2 percent (via AFP)US retail sales rose by 0.2 percent in July, shy of forecasts, government data showed Tuesday, but some analysts pointed to overall strength in non-automobile purchases. The July rise in overall retail and food service sales compared with a revised…

Electric Transportation Could Jump-Start Rare Earth Markets: Patrick Wong

Source: JT Long of The Metals Report (8/13/13)

Remember when CD players cost hundreds of dollars? The same volume-based price slide is starting to take place with electric vehicles, according to Patrick Wong, CEO and director of Innovation Metals Corp. Wong believes that hybrid and electrical cars are on the cusp of overtaking standard automobiles as the vehicles of choice. And when they do, the rare earth markets that supply the materials needed in every electric car battery and drive motor will take off. In this interview with The Metals Report, Wong encourages investors to get into the market before they get left behind.

The Metals Report: You’ve said that the ratio of natural gas to oil prices [see price charts below] represents the largest arbitrage opportunity in history. What does that mean for the future of transportation and rare earth element (REE) consumption?

Patrick Wong: This trillion-dollar arbitrage will bring a lot of momentum into the electrification of transportation. You need REEs to make the permanent magnets that go into the electric drive motors, so they have a key role. In 10 years, we’ll look back and recognize that this is the beginning of the end of a world dependent upon petrol-based transportation.

Above: Henry Hub prices are in decline, while West Texas Intermediate prices rise.

TMR: With gas stations on every corner, where will the desire and the money come from to support this massive shift to electric vehicles?

PW: The economic divide between cheaply produced electricity versus expensive oil is all the support the hybrid market needs in order to grow quickly. The economics will drive everything. We have one of the most advanced power grids in the world, with more plugs than gas stations. Any new technology—plasmas, LCD TVs, Blu-Ray—starts off at higher prices because the research and development costs have to be amortized. As volume picks up, the prices decline, and they eventually push the old technology out. Right now, hybrid electric cars can be as much as 20% more expensive than regular cars, but in a short period of time, this price differential will drop to less than 10%. Soon it will be like choosing an automatic or a manual.

TMR: You’ve said that finding REE deposits isn’t an issue—they’re actually not rare—and that being economic can be a misplaced concept.

PW: Being uneconomic doesn’t mean it’s necessarily a bad investment, especially when the underlying commodity has huge price volatility. I had some of my best days as a hedge fund manager investing in high-cost gold mines that were uneconomic at $350 per ounce ($350/oz) gold. Everyone hated them, but when it went to $1,000/oz, these companies had a ton of leverage. Solid investing is about making the right risk-adjusted bets over and over. When an analyst says a project is uneconomic, you should consider the price that would make a given mine become economic.

TMR: Are partnerships with end users the holy grail, or are they a pitfall?

PW: I don’t see why it’s such a big deal when a company announces that it has a partnership or offtake. Investors assume there is an end market, so why is it such a surprise when a customer is announced? What’s more of an issue is that most of these companies intend to produce a mixed concentrate, but I don’t know any end user that can use a mixed bag like that. Most customers use only two or three elements. This is where a refinery comes in to produce the material end users need at the specifications they require.

TMR: Are you saying that a centralized refinery would make it possible for more companies to compete, considering most juniors would not have to bear the cost of building their own processing facilities?

PW: Absolutely. Mines are good at mining. The refinery is a chemical-processing plant. My company, Innovation Metals, is currently raising capital for a facility that should help address the rare earth processing bottleneck.

TMR: What are your projections for REE prices?

PW: Prices are bottoming out. We keep track of customer inventories, and they are running low. The demand for magnet-based REEs remains strong and is growing, but dysprosium and the terbium, europium and yttrium for phosphors might stay flat until we see a larger adoption of energy-efficient lighting. A lot depends on whether or not the United States weans itself off incandescent lighting.

TMR: Funding is a challenge for all juniors in this market. How are rare earth companies, which sell on a less transparent market, finding the money to move their projects forward?

PW: Traditional bank financing won’t be there because there is no way for banks to hedge out financial risk. The banks will lend off these forward contracts, but a substantial amount will need to come from traditional equity financing.

TMR: Gareth Hatch, who works with you, said in an interview last November that the vast majority of companies in the space would not go into production soon. How many are still out there, and how many can be successful?

PW: Just a handful will make it in the short term. In the long term, if the demand is there, prices will go to a point where marginal supply will meet marginal demand, and those projects will become economic. Anything could still pull a rabbit out of the hat, but investors shouldn’t depend on being lucky.

TMR: When you say a handful, how many are we talking about?

PW: Five or six.

TMR: Are there still opportunities for juniors in the light rare earth elements (LREEs), or do Molycorp Inc. (MCP:NYSE) and Lynas Corp. (LYC:ASX) have that market cornered?

PW: Just because a few large companies dominate by volume doesn’t mean a smaller player can’t compete. There are always opportunities. In the end, it will come down to cost and capital expenditures (capex). With the high cost of capital these days, companies with a low capex have an advantage over large projects and can afford to sell cheaper. More volume will encourage more transparency. Eventually, an efficient market will form and the company with the lowest cost base will set the stage, regardless of its size.

TMR: What are some examples of companies with low capex that could be successful?

PW: On the heavy rare earth element (HREE) side, Matamec Explorations Inc. (MAT:TSX.V; MRHEF:OTCQX) and Tasman Metals Ltd. (TSM:TSX.V; TAS:NYSE.MKT; TASXF:OTCPK; T61:FSE). A bit further down the road is Namibia Rare Earths Inc. (NRE:TSX, NMREF:OTCQX). Having access to a refinery is key, especially for HREE projects.

TMR: Matamec has an agreement with Toyota Tsusho Corp. (TYHOF:OTC; 8015:JP) and a feasibility study coming out. Do those give it an edge?

PW: It’s one of the more advanced projects. We’re looking forward to reading the feasibility study. What makes me a little bit nervous is that, as far as I know, a third party will be pricing out the concentrate prices that Matamec will receive. Toyota doesn’t have an HREE separation plant, so I don’t know where it is going to ship this material.

TMR: Does being the first to market give Matamec an advantage?

PW: The whole first-to-market issue has been overglorified. It’s nice to be first, but ultimately, the end users will buy from anybody with the lowest price as long as their specs and quality control are consistent. So whether you’re first, second or third, there is still a large end-user market that needs the product. When you’re first, you might get access to better pricing. That is a bit of an advantage.

TMR: You mentioned Tasman, which is in Europe. Does location make a difference?

PW: Definitely. When you have infrastructure available, it lowers capex and reduces the volatility of the assumption behind it because things are better defined. Tasman has a suite of HREEs, for which demand should come from not only Asia but Europe as well, for use in things like phosphors and magnets.

TMR: What are some other companies that have a shot at being in the top six?

PW: Ucore Rare Metals Inc. (UCU:TSX.V; UURAF:OTCQX), Great Western Minerals Group Ltd. (GWG:TSX.V; GWMGF:OTCQX) and Geomega Resources Inc. (GMA:TSX.V; GOMRF:USX), even though it’s more of an LREE project. I like the management teams that are resizing their projects. They’re looking to bootstrap their mines―to start off smaller and get to cash flow quicker. Companies likeGreenland Minerals & Energy Ltd. (GGG:ASX) in Greenland and Arafura Resources Ltd. (ARU:ASX) in Australia have looked at the market environment and realized that the billion-dollar project isn’t feasible, so they’re looking at smaller projects that can fund future growth. Peak Resources Ltd. (PEK:ASX; PKRLY:OTCQX), in Australia, has low capex.

TMR: Great Western Minerals has been working with the Department of Defense (DOD) on finding yttrium. Is that partnership as valuable as working with an automobile maker?

PW: It’s not any better or worse; the DOD has the same needs as any end user. For REE products, there’s a high threshold to meet in terms of consistency and quality, whether it’s for the DOD or another end user.

TMR: Great Western’s stock price has ticked up recently. What’s behind that?

PW: Some REE stocks seem to be stabilizing. Maybe some of the speculators are looking to bottom feed and pick a trough. Great Western has a good shot at production; it was beaten down along with the rest of the sector and probably poses a better risk-reward opportunity than other stocks.

TMR: Geomega has both graphite and REEs. Is that a benefit?

PW: I don’t think it has any synergistic benefits. It’s nice to have an end user that might use both, but you need to value both deposits separately.

TMR: Geomega is in Quebec, as is Quest Rare Minerals Ltd. (QRM:TSX; QRM:NYSE.MKT). What geological benefits does Quebec offer?

PW: Each mine has a different geology and will have a different metallurgical process. Quebec does boast a lot of resources. Gareth has said it has the highest concentration of REE resources in a given location, which is one reason we’re putting our REE refinery in Quebec. There are other advantages to Quebec—it also has access to cheap power and a good labor force.

TMR: REEs often come along with uranium or thorium. How do you deal with the issue of radioactivity?

PW: Mining companies must have the ability to take out and store any radioactive material at the site, because it can’t be shipped. The feedstock the refinery takes is free of radioactive material and already concentrated to a point that it’s mostly REEs.

TMR: Is the ability to deal with radioactivity one of the things that you look for in the feasibility studies? Do some companies have fewer issues with that than others?

PW: Some deposits have less radioactive material than others, but any amount needs to be dealt with. You need to have a permit and a plan for how you’re going to deal with it. In a feasibility study, I look more for its business approach. Is it going to sell a mixed REE concentrate, or does it have the ability to produce a product end users need?

TMR: What end products are most in demand?

PW: Out of the LREEs, neodymium and praseodymium are most in demand for their use in magnets. For the HREEs, dysprosium is definitely the most in demand. The markets for europium, terbium and yttrium can quickly turn around and be very strong.

TMR: Some investors in the REE space have been suffering for a while. Do you have any words of comfort?

PW: Continue to look for low-capex projects. They are less risky and have a better chance of making it to market. Look for a pragmatic management team that understands the market it’s in and can change its business strategy to suit it. The refinery space is another way to invest in the future of rare earth elements. I have found that institutional investors are interested in the space for all the reasons mentioned above. In 10 years from now, you will look back and see this was the transition point from a world dependent on petrol-based transportation to one using much cleaner, more efficient electrical or hybrid cars.

TMR: Thank you so much for your time.

PW: It was my pleasure.

Patrick Wong, chief executive officer and director of Innovation Metals Corp., is a seasoned hedge fund manager with over 15 years of experience in various trading strategies, including capital structure arbitrage. He was co-founder and chief investment officer of Dacha Strategic Metals Inc., a unique investment vehicle that invests in physical rare earths. Prior to Dacha, Wong was president of a natural gas trading company that created models to trade physical gas. More recently, he has traded rare earths and metals.

Want to read more Metals Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Metals Report <href=”#interviews” target=”_blank”>homepage.

DISCLOSURE:

1) JT Long conducted this interview for The Metals Report and provides services to The Metals Report as an employee. She or her family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Metals Report: Matamec Explorations Inc., Tasman Metals Ltd. and Namibia Rare Earths Inc. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Patrick Wong: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Innovation Metals is in talks with juniors about using a central refining plant. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2013 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

Many Currency Pairs Have Range Trading Due to Low Liquidity

EURUSD – The EURUSD Remains in Narrow Range

The EURUSD was lowly decreasing towards the 30th figure first, then – to the level of 1.3015. Afterwards, it started increasing to the resistance at 1.3070 and dropped back to 1.3033 during the Asian session. The first day of the new trading week turned out to be like this, and there happened nothing new to the EURUSD pair. It remains in a narrow range, which will surely be broken, but hardly anyone knows the time period and the direction as well. It is indisputable that if the euro passes the support at around 1.3000, the rate will decrease towards the 29th figure. If the bulls make their way above 1.3070-1.3100, their chances to test the 1.3200 level will be dramatically increased.

GBPUSD – The GBPUSD Trading Below Figure 53

The GBPUSD managed to consolidate above 1.5200 and increase to 1.5297 due to the EURGBP decrease. As long as the pair is trading below 1.5300, its increase does not change anything — that is, the downwards risks remain. This has been evidenced by the Parabolic SAR, which is located above the price chard on the 4-hour chart and is coloured in red. However, if the pound can form the bottom above the 52nd figure, the upward correction may be continued.

USDCHF – The USDCHF Scores About 55 Points

The USDCHF dynamics was no less boring — the par has passed for about 55 points in the upward direction. After it reached the level of 0.9370, it rebounded to 0.9340. The increase was due to the low activity and low volumes as well, thus you can draw a parallel with the non-alcoholic beer: the stomach is not only full of it, but there is no use of it at all. The key stage for the pair at the moment is the 93rd and the 94th figures, whose passing will set the future direction of the movement in the USDCHF.

USDJPY – The USDJPY Retreats from Figure 100 Again

Another hike to the 100.00 level for the USDJPY bulls was not successful again, and they were forced to retreat to 98.58. But is not necessary to talk about the bulls’ backdown, of course, at least as long as the pair has comfortably consolodated above 98.53-98.00. But in case of the pair’s decrease below the latter level, the bears will manage to test the support at 97.20 – it will be able to weaken the bulls’ strength and power as well. However, the 100th figure clearly attracts the dollar buyers and the Japanese yen sellers as well, thus another testing of this level looks very likely.

Central Bank News Link List – Aug 13, 2013: Mozambique central bank cuts rate 25 bps

By www.CentralBankNews.info Here’s today’s Central Bank News’ link list, click through if you missed the previous link list. The list comprises news about central banks that is not covered by Central Bank News. The list is updated during the day with the latest developments so readers don’t miss any important news.

- Mozambique central bank cuts rate 25 bps (Central Bank of Mozambique)

- Russian central bank sees economy slowing, inflation ties hands (Reuters)

- BOJ minutes raise debt concerns (WSJ)

- Indonesia central bank likely to hold BI rate steady (Jakarta Globe)

- China money rates rise after c.bank mops up cash injection (Reuters)

- Capital outflows to weigh on Russian rouble – central bank (Reuters)

- Banks cut 5,500 branches across Europe in 2012 (Reuters)

- Chile analysts see interest rate remaining at 5% in August (WSJ)

- Kenya shilling eases, central bank injects liquidity (Reuters)

- New Zealand central bank spells out house loan limit rules (Reuters)

- How stimulatory are large-scale asset purchases? (San Francisco Fed)

- www.CentralBankNews.info

Theme Park Revenue Riding High

Up, up and away.

That’s where revenue of U.S.-based theme parks has been heading for the past three years.

Indeed, theme park revenue has grown by 3.6% in each of the past two years. And that’s after a 4.5% jump in 2010.

Those numbers may not sound that impressive, but the trend represents something spectacular.

It means that 131.6 million visitors – 4.6 million more than in 2011 – felt comfortable enough financially to fork out the big bucks these parks command.

People don’t do that when money is tight, or when they’re jobless or scared about the state of the economy.

And this year, U.S. theme parks are expected to reach a record $13.4 billion, a 2.8% gain from 2012, according to market research firm, IBISWorld.

So let’s take a look at a few stocks in this arena that could provide entertaining gains.

First Stop: The Happiest Place on Earth

Disney California Adventure, Universal Studios Hollywood and Magic Kingdom at Walt Disney World accounted for 57% of the increase in visits to the top 20 parks in North America in 2012.

Dominant among Disney (DIS) properties is its resort in Orlando, with 48.5 million visitors last year. Magic Kingdom drew 400,000 more fans due, in part, to Disney’s continuous flow of money into improvements and new attractions. Disneyland Resort in Anaheim had 23.7 million visits in 2012, an increase of 1.3 million visits versus 2011.

In 1955, admission to the Anaheim park cost $1 per person, making it affordable for just about anyone. Today, that same ticket goes for $95 after a recent 9.6% hike in price.

The average amount of money spent by a Disney visitor rose 10% in the first calendar quarter of 2013. After tumbling 6% in 2009, average spending per Disney visitor rose 3% in 2010, 8% in 2011 and 7% in 2012.

The company hasn’t resorted to any special pricing for the slower months, either.

During the second quarter 2013, Disney’s theme park and resort unit generated revenue of $3.3 billion, up 14% compared to last year. Those higher prices also helped push operating income up 73% that same quarter.

Although DIS currently trades just shy of its all-time high of $67.89, many analysts see continued growth in the range of $73 to $75 for the year.

What makes Disney a great company is that it never rests on its laurels, pumping some $10 billion into expansion from 2009 to 2015. As long as people can spend, they will – and wait in football-field length lines for the experience.

That makes Mickey and company very happy.

Because the Disney theme parks contribute only about 20% to the entire company’s bottom line, here are a few pure-plays to consider…

Six Flags: Smooth Sailing or Rough Ride?

Six Flags Entertainment Corp. (SIX) owns and operates 18 amusement parks – 16 in the United States, one in Mexico and one in Canada.

The company reported a 34% drop in net income for the three-month period ending June 30.

However, that drop may sound worse than it actually is. Apparently, Mother Nature is to blame for some of the loss, soaking its Midwest and East Coast parks for extended periods and making mud out of previously rising admission figures.

On a quarter-to-quarter basis, Six Flags may not have fared well, but revenue had consistently improved over the past three years, and earnings went from a small loss to a large gain between 2011 and 2012. Six Flags is trading at nine times earnings and yields a 5% dividend.

So there’s reason to believe Six Flags can rebound. It certainly wouldn’t be the first time the company overcame financial adversity, either.

Overbearing debt and poor management drove the company into bankruptcy during the 2008 to 2009 recession. It was subsequently bought out of Chapter 11 protection by investment firms and taken public in May 2010.

This one should deliver either way, be it through equity growth or hefty yields.

Will SeaWorld Keep its Head Above Water?

Another company to keep an eye on is SeaWorld Entertainment Inc. (SEAS). These are the folks who bring us 11 theme parks, including SeaWorld, Shamu, Busch Gardens, Adventure Island and Sesame Place.

It went public in April in one of the largest IPOs this year, after Blackstone bought the company from Anheuser-Busch InBev (BUD). It opened at $27 per share. Today it’s trading at $35.31 with a market cap of nearly $3.6 billion. For the full year 2013, SeaWorld expects to deliver around $1.46 billion to $1.49 billion in revenue.

SeaWorld releases earnings today from its first full quarter since going public. We’ll see if the company has kept its head above water, or has fallen below. Stay tuned on this one.

Ahead of the tape,

Karen Canella

The post Theme Park Revenue Riding High appeared first on | Wall Street Daily.

Article By WallStreetDaily.com

Original Article: Theme Park Revenue Riding High

Ukraine cuts rate 150 bps, improved inflation expectations

By www.CentralBankNews.info Ukraine’s central bank cut its benchmark discount rate by 150 basis points to 6.50 percent to “promote sustained economic growth” amid improved expectations for inflation.

The National Bank of Ukraine, which also cut its rate in June, said a survey in the second quarter showed that inflationary expectations reached an all-time low since 2006 and banks’ resource base had expanded.

Ukraine’s headline inflation rate was zero in July, up from a fall in inflation of 0.4 percent in June. Ukraine has been suffering from deflation for the last 14 months

The central bank has now cut rates by a total of 200 basis points this year following the 50 basis point reduction in June.

The bank said funding in the national currency was the main contributor to growth in deposits and in the first seven months of the year deposits had expanded by 17.8 percent compared with a 0.6 percent decline in foreign currency deposits.

It also said interest rates on loans had been on a gradual downward trend with the average weighted interest rate on loans down to 15.7 percent in July from 17.6 percent in December 2012.

In the first quarter, Ukraine’s economy expanded by 0.6 percent from the previous quarter for annual contraction of 1.1 percent.