Weekend Update

December 20, 2013

— VIX made a new high, challenging its weekly mid-Cycle resistance at 16.74. It closed back down in the cluster of supports between 13.42 and 14.23. It is now poised to challenge its Head & Shoulders neckline at 21.00.

SPX closes at a Broadening Top.

— SPX closed at a new high, but does so within the context of an Orthodox Broadening Top, which began forming one month ago. The Orthodox Broadening Top is formed by three successively higher tops and two bottoms, the second of which must be lower. This forms a “Megaphone” pattern . The Broadening Top is considered complete when the decline from the third peak falls below the level of the second bottom.

(ZeroHedge) Earlier today, the Bureau of Economic Analysis surprised everyone by announcing a final Q3 GDP growth of 4.1% compared to 3.6% in the first revision (and 2.8% originally), driven almost entirely by the bounce in Personal Consumption which rose 2.0% compared to estimates of 1.4%. As a result many are wondering just where this “revised” consumption came from. The answer is below: of the $15 billion revised increase in annualized spending, 60% was for healthcare, and another 27% was due to purchases of gasoline.

NDX also makes a new high.

— The NDX made a high that only retraced 68% of its decline from the 2000 peak. It may now be complete since it is at the upper trendline of its Broadening Wedge & Ending Diagonal formations. Elliott Wave analysis appears complete and NDX may now due for a major correction.

(ZeroHedge) Jim Grant tells Germany’s Finanz und Wirtschaft that he “fears that this journey will not end well.” The sharply thinking Wall Street veteran doesn’t trust the theoretical models of the central banks and warns of irrational exuberance in the financial markets adding that “the stock market is increasingly full of stocks that are borne aloft by hope rather than demonstrated performance.”

The Euro completes a very strong retracement.

.

— After retracing most of its decline from the October 24 high, the Euro reversed down this week. Because it could not overcome its previous high, it is now vulnerable to a panic sell-off. If so, the next bottom may occur in early January.

(EuroNews) Greek statistics now suggest 34.6 percent of the population lives in or close to poverty, nearly 10 percent above the EU average. This is because their jobs have gone and there is no sign of them returning any time soon. Worse could be to come; 14.1 percent of the population lives in a household at risk of unemployment. “These are ordinary people. People who have lost their jobs and had their lives turned upside down. It is estimated that more and more Greeks facing severe economic difficulties are leaning towards the help provided by the church through its NGO Mission. Thousands of people will celebrate the Christmas holidays with special meals that are being delivered over the coming days,” said euronews reporter Theodora Iliadi in Athens.

The Yen is now testing its Head & Shoulders neckline.

–The Yen probed at the Head & Shoulders neckline at 96.00 this week. The Yen appears to be breaking down beneath the neckline in a Primary Wave [5] in a very strong Primary Cycle decline through that may last into the New Year.

(Bloomberg) The Bank of Japan maintained its record easing, after a U.S. Federal Reserve decision to taper policy helped weaken the yen to a five-year low against the dollar.

Governor Haruhiko Kuroda’s board kept its pledge to expand the monetary base by an annual 60 trillion to 70 trillion yen ($670 billion) today after a two-day meeting in Tokyo, in line with forecasts of all 35 economists surveyed by Bloomberg News.

The US Dollar tested its mid-Cycle resistance.

— USD made quite a comeback testing its weekly mid-Cycle resistance at 80.89. Wednesday’s wide-ranging move completed the correction and launched the dollar on a new rally. The bear trap for dollar shorts has now been sprung.

(Reuters) – Currency speculators decreased bets in favor of the U.S. dollar for the third week in a row in the latest week, according to data from the Commodity Futures Trading Commission released on Friday.

The value of the dollar’s net long position fell to $18.32 billion in the week ended Dec. 17, from $19.10 billion the previous week. To be short a currency is to bet it will decline in value, while being long is a view its value will rise.

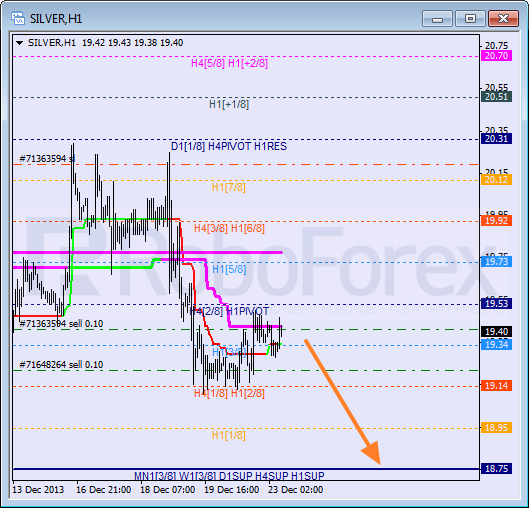

Gold closes beneath its Cup with Handle formation.

— Gold closed beneath its Cycle Bottom support and the the Lip of its Cup with Handle formation at 1205.00. There are often multiple formations that may either agree with the others or give additional targets or information. Gold has two legitimate targets for its decline. These targets may not be exclusive of the other, since Head & Shoulders patterns present probable Wave 3 lows, while Cup with Handle formations often complete the impulse.

(ZeroHedge) As persistent trackers of the CME’s daily depository statistics update are well aware, over the past week, JPM has been accumulating an impressive amount of gold, and what is more curious, it has been precisely in increments of 64,300 ounces of eligible gold on a daily basis. Putting this scramble in context, two months ago JPM had only 181K ounces of eliglble gold. And yet, just today, the Comex announced that JPM’s eliglble vault gold rose by almost that amount, increasing by 125K to a reputable 1.2 million eligible ounces.

Treasuries inching beneath the Broadening Wedge.

— USB appears to be probing beneath the trendline of its massive Broadening Wedge formation. This pattern suggests a probable 20% loss beneath this support level. In addition, the Cycles Model anticipates further decline through most of January before the next support may be reached. Two recent articles in this regard are here and here.

Crude breaks above a Head & Shoulders neckline.

— Crude rallied above the neckline of an inverted Head & Shoulders formation at 99.00. This implies further bullish moves in WTIC. There is yet some resistance at the weekly Long-term resistance at 100.42, where a consolidation may occur. The rally has the capability of stretching through late January, giving it the time it needs to develop more fully.

(Bloomberg) The price gap between the world’s two biggest oil benchmarks probably will narrow next year as U.S. exports of refined fuels reach a record and crude supply from the Middle East and North Africa expands. While the U.S. is pumping the most crude oil in a quarter century, laws prohibit most exports, driving down costs for domestic refiners and spurring record shipments of everything from diesel to gasoline that will diminish stockpiles. The forecasters expect Brent prices to weaken as regional supply recovers, led by Iran and Libya.

China stocks take a plunge.

–The Shanghai Index plunged beneath all supports in a very bearish left-translated cycle. SSEC may continue its decline through mid-January in what appears to be a liquidity crunch. In the process, it has a high probability of making some new lows. This decline may not be finished until mid-March..

(ZeroHedge) Overnight we warned that short-to-medium-term money market rates had spiked to record highs (1-Year rate-swaps over 5.06%) and that the PBOC was bravely standing firm on its (lack of) liquidity injections… that didn’t last long. Despite the PBOC’s veiled ongoing attempts to ‘taper’ its own liquidity provisions, as MNI noted, echoes of the June liquidity crunch were heard again in the Chinese money market Thursday and authorities moved to extend trading amid a surge in rates which quiet injections of funding by the People’s Bank of China failed to stem.

The India Nifty retraces half of last week’s loss.

— The India Nifty made a 54% retracement of its initial decline from its Cycle Top and the top trendline of ita Orthodox Broadening Top formation. This suggests the current Cycle may resume its decline into early January. The decline may be deflationary to an extreme. The potential for a panic decline to the weekly Cycle bottom (4737.34) is very high.

The Bank Index retraces 49% of its 2007-2009 decline.

— BKX made a near-50% retracement of its decline from 2007 to 2009. The rally is getting old and worn out, as indicated by the momentum oscillators. This kind of rally won’t end well. The resumption of the secular bear market may be most evident in BKX.

(ABCNews) European Union leaders gave an enthusiastic thumbs-up Thursday to a new mechanism agreed on to handle ailing banks, but analysts likened it to a band aid that falls short of what is needed to stabilize the bloc’s financial system.

French President Francois Hollande said the new centralized institution for saving or shutting down troubled banks across the 17-nation Eurozone will help preventing new financial crises and spare governments from having to save failing banks.

(ZeroHedge) Late last night (Wednesday), European Union finance ministers agreed on a new system to centralize control of failing euro-zone lenders – a so-called “bank resolution mechanism” – in the hope that it will stop expensive banking crises from ruining the finances of entire countries. As WSJ reports, “”Taxpayers will no longer foot the bill when banks make mistakes and face crises, ending the era of massive bailouts,” according to Michel Barnier, the EU’s internal market commissioner.” Sadly, Mr. Barnier is incorrect, for two main reasons.

(USNews) When the long-awaited Volcker Rule finally emerged last week, the outside world took out its magnifying glass. The advance buzz had said it would be “tougher than expected.” But soon enough, critics were poring over the text, spotting weaknesses, comparing notes, and even, in a few cases, calling it things like “Washington’s latest bonanza for lawyers and lobbyists” or the “one of the great pieces of Swiss cheese in regulatory history.“

The grounds for concern are real. This was a committee product, shaped by 22 principal negotiators representing five agencies, dogged every step of the way by powerful and determined Wall Street lobbyists. At the same time, it is worth a cheer that the rule got done at all, thanks to the vigilance of advocates and recent prodding by Treasury Secretary Jacob Lew, among other things. Too often, rules opposed by industry can languish indefinitely, sometimes even for decades. We should also be grateful that those 22 principals included supporters of a strong rule who were able to insist on important improvements as the process came down to the wire.

(ZeroHedge) After having followed a zero interest rate policy strategy and facing a further deteriorating economy in an environment of falling prices (deflation), the Bank of Japan (BoJ) announced the introduction of QE on 19 March 2001 and kept it in place until 9 March 2006. The BoJ chose for a very orderly and gradual unwinding of its government securities portfolio, by continuing its regular purchases of these securities (i.e a taper and not sale). The market rejoiced at the normalization for a week or 2… before dropping 24% in the following 2 months. Of course, that was a “policy mistake”; the Fed knows this time is different.

Is this progress???

Regards,

Tony

Anthony M. Cherniawski

The Practical Investor, LLC

P.O. Box 129, Holt, MI 48842

www.thepracticalinvestor.com

Office: (517) 699.1554

Fax: (517) 699.1558

Disclaimer: Nothing in this email should be construed as a personal recommendation to buy, hold or sell short any security. The Practical Investor, LLC (TPI) may provide a status report of certain indexes or their proxies using a proprietary model. At no time shall a reader be justified in inferring that personal investment advice is intended. Investing carries certain risks of losses and leveraged products and futures may be especially volatile. Information provided by TPI is expressed in good faith, but is not guaranteed. A perfect market service does not exist. Long-term success in the market demands recognition that error and uncertainty are a part of any effort to assess the probable outcome of any given investment. Please consult your financial advisor to explain all risks before making any investment decision. It is not possible to invest in any index.

The use of web-linked articles is meant to be informational in nature. It is not intended as an endorsement of their content and does not necessarily reflect the opinion of Anthony M. Cherniawski or The Practical Investor, LLC.

P.O. Box 129  Holt, MI 48842 (517) 699-1554 Fax: (517) 699-1558

Holt, MI 48842 (517) 699-1554 Fax: (517) 699-1558

Email: [email protected] www.thepracticalinvestor.com

Micro-cap stocks, which my MicroCap Tech Trader subscribers know all too well, performed best, rising an average of nearly 40%.

Micro-cap stocks, which my MicroCap Tech Trader subscribers know all too well, performed best, rising an average of nearly 40%.