By CentralBankNews.info

Fiji’s central bank maintained its current accommodative policy stance by keeping its Overnight Policy Rate (OPR) steady at 0.5 percent and said domestic demand continues to be buoyant so the economy in 2014 should surpass the pre-budget forecast of 3.0 percent growth.

The Reserve Bank of Fiji, which has maintained rates since December 2011, also said economic activity in 2013 was broadly positive and the economy should achieve the forecast 3.6 percent growth.

In October the central bank revised upwards its 2013 growth forecast to 3.6 percent and its 2014 growth forecast to 3.0 percent.

Domestic demand in Fiji is being supported by improving labour market conditions, an expansionary government budget, record low commercial bank lending rates and a favorable business environment.

Barry Whiteside, governor of the central bank, said in a statement that partial indicators for investment showed that the pace of investment strengthened last year and will remain above 25 percent of Gross Domestic Product this year, adding that this was reflected in rising domestic credit growth, which had accelerated to 14.3 percent in December.

The central bank’s policy objectives also remained intact, Whiteside said, with Fiji’s foreign reserves at US$ 1.77 billion as of Jan. 29, enough for 4.7 months of imports, and inflation is expected to trend toward 3.0 percent by year-end.

In November Fiji’s inflation rate rose marginally to 3.4 percent from 3.3 percent in October, mainly due to higher prices of food and non-alcoholic beverages.

USDCAD Elliott Wave Analysis: Wave 3 Near Top

USDCAD is moving sharply to the upside for the last couple of weeks since pair managed to move above 1.0660 resistance zone, back from 2011. Sharp and big move in short period of time like this one on USDCAD usually occurs in the middle of wave three of an impulsive price action. As such we adjusted the wave count and around now tracking an incomplete five wave recovery, either in wave (C) or (3). In both cases we expect higher levels, up to 1.1600/1.1700 as long as 1.0600 level holds.

USDCAD Weekly Elliott Wave Analysis

USDCAD Daily

USDCAD seems to be trading in the middle of an impulsive red wave 3) from a weekly chart that needs to be made by five subwaves. That’s still not the case from 1.0177 swing region so we expect to see even higher prices in 2014. At the moment we are tracking a subwave 3 that may stop around 1.1200 figure.

USDCAD Daily Elliott Wave Analysis

Written by www.ew-forecast.com

14 days trial just for €1 >> www.ew-forecast.com/register

Crude Oil Prices Climbs on Stockpiles Report

Crude oil prices advanced following the report released by the EIA, which showed that inventories climbed higher than expected last week. West Texas Intermediate (WTI) rose , trimming the biggest monthly fall for January since 2010 as market participants focus on the release of the US GDP later in the day.

Meanwhile following the Federal Reserve’s two day policy meeting, fed officials decided to reduce its bond buying program by an additional $10 billion.

WTI crude oil for March delivery added 0.56% higher, trading at $97.91 per barrel on the New York Mercantile Exchange as of 9:59a, GMT. At the same time Brent for March settlement rose 0.35%, standing at $108.23 per barrel on the ICE Futures Europe exchange. The European benchmark crude was at a premium of $10.25 to WTI on the ICE exchange.

US Crude Inventories

Data from the Energy Information Administration (EIA) showed that crude inventories climbed by 6.4 million barrels in the week ended January 24. The figures surpassed analysts forecast of a rise by 2.15 million barrels.

The same data also revealed that the demand for distillates; which includes heating oil, climbed to the highest level in nearly six years. Meanwhile, Cushing crude stockpiles reported a 237,000 rise, compared with the 722,000 rise seen in the previous week.

The American Petroleum Institute (API) report reveled oil inventories added 4.7 million barrels in the week ending January 24, compared to analysts forecast of an additional 2.3 million barrels.

US GDP in Spotlight

Market participants are expecting to see an upbeat gross domestic product (GDP) report which is forecasted to show a 3.2% annualized rise. The upbeat reading is based on approximately 45% of the whole quarter data.

On Wednesday, The Federal Open Market Committee (FOMC) concluded its two-day meeting by deciding to reduce the central bank’s monthly purchases of treasuries and mortgage-backed securities (MBS) by an additional $5 billion each.

“Growth in economic activity picked up in recent quarters,” The statement from the Federal Reserve stated. “Household spending and business fixed investment advanced more quickly in recent months.”

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today.

The post Crude Oil Prices Climbs on Stockpiles Report appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Australian Dollar Drops From Previous Gains

The Australian dollar rebounded from its recent gains on Thursday. The Australian currency was dragged lower by the Federal Reserve’s (Fed) decision to reduce its monthly bond purchases and China’s weak Purchasing Managers’ Index (PMI).

Following the Federal Reserve’s two day policy meeting, Fed policymakers concluded the meeting by deciding to reduce the central bank’s stimulus further by $10 billion to $65 billion, showing signs that the world’s largest economy is expanding despite the recent disappointing non-farm payrolls data for the previous month.

The Federal Reserve’s decision to trim its monthly asset purchases further slightly strengthened the greenback.

The Australian dollar weakened by 30 pips to $0.8730 following the Fed’s decision, while the downbeat Chinese PMI dragged the aussie 20 pips lower to $0.8709.

China Purchasing Managers’ Index (PMI)

The final PMI for January weakened, standing at 49.5, dropping from the previous reading of 49.6 seen last week. Any reading above 50 indicated the rise in manufacturing activity, while any reading below 50 points a contraction.

Australia’s Housing Prices

Australia Housing Industry Association posted a rise of 14.4% in home sales last year, indicating an expansion for the first time since 2008. Month-on-month sales declined 0.4% in December, dropping from the previous rise of 7.5% seen in the previous month.

Fed-Tapering Decision

The Federal Open Market Committee (FOMC) concluded its two-day meeting by deciding to reduce the central bank’s monthly purchases of treasuries and mortgage-backed securities (MBS) by an additional $5 billion.

“Growth in economic activity picked up in recent quarters,” The statement from the Federal Reserve stated. “Household spending and business fixed investment advanced more quickly in recent months.”

Fed members concluded to reduce the monthly asset purchases despite the weak employment report which came in below analyst forecast. The unemployment rate dropped to 6.7% in December, the lowest since October 2008.

Visit www.hymarkets.com to find out more about our products and start trading today with only $50 using the latest trading technology today.

The post Australian Dollar Drops From Previous Gains appeared first on | HY Markets Official blog.

Article provided by HY Markets Forex Blog

Gold Crybabies Are Born to Lose, Says Lawrence Roulston

Source: Peter Byrne of The Gold Report (1/29/14)

http://www.theaureport.com/pub/na/gold-crybabies-are-born-to-lose-says-lawrence-roulston

Geologist, engineer, Midas-touch investor and financial newsletter publisher Lawrence Roulston has little patience for investors without the nerves to hold onto a good thing during tough times. Gold has been the main embodiment of value for thousands of years, Roulston points out, so why should tomorrow be different? In this interview with The Gold Report, Roulston has some tips on how to double down on gold investments and wipe away the tears.

The Gold Report: Let us be brutally frank, Lawrence. Is investing in gold dead as a reasonable investment strategy?

Lawrence Roulston: No, not at all. Gold is headed higher in the medium term and the long term. There will still be a lot of volatility at play during the short term, but gold will continue its uptrend of the last 13 years. It is highly speculative to bank on near-term appreciation in value. That approach can be incredibly frustrating when the price is volatile. But the long-term perspective is a different matter. Gold is always going to have an intrinsic value.

Think about the big selloff in paper gold last year. People were lining up to buy physical gold as investors were dumping exchange-traded funds and paper gold on the market. But central banks are still net buyers of gold. China is emerging as the biggest buyer at both the consumer and the central bank level. Gold has been the mainstay of financial systems for more than 5,000 years!

TGR: What is the current relationship between physical gold and paper gold?

LR: At one level, the pricing is identical because paper gold matches the physical gold pricing. But, these two forms of yellow metal ownership are held by very different groups of people. Paper gold, especially over the last few years, has been primarily held by North American short-term speculators. Physical gold is more of a long-term holding. Europeans who are concerned about the long-term viability of euro-denominated assets are holding on to physical gold as a store of wealth, as protection. China is now vying with India as the largest market for physical gold.

TGR: Can you quantitatively model long- and short-term gold cycles?

LR: Predicting the gold cycles is challenging because so many interrelated factors influence the movement of gold prices. To a very large extent, the short-term price moves are emotional—driven by news, by headlines, by rumors and gossip. But even when one takes a medium- or a longer-term perspective, there are still huge numbers of variables. It is very difficult to model gold. I consider taking ownership of bullion or the paper equivalent of bullion as more of a speculation than a surefire investment—unless one considers gold to be a long-term store of wealth.

Every time the gold price runs up and then falls off, people say, “It’s over for gold. This is no longer a viable commodity. It’s a relic of the past.” Then gold takes off again. Gold prices will always run in short- and long-term cycles. And the long-term trend points upward.

TGR: Is gold a true hedge against inflation?

LR: The short-term downswing in the gold market is largely driven by the emergence of a low inflation environment in the near term. And the outlook for inflation remains low to modest. There is no hint of runaway inflation in America or Europe. In Japan, interestingly, the rate of inflation is notching up at the low end, but that is where the Japanese bankers actually want to see a bit of corrective inflation.

Of course, in two, three or four years, the global status quo for gold prices could change quite dramatically. But hedging against inflation is not the only reason for owning gold as a store of value. It is also appropriate to protect wealth against nonfinancial or non-currency related factors. For example, a large part of the boom in gold ownership in China is tied to investors searching for hard assets as they exit the overheated real estate market.

TGR: You recently made a presentation at the Mines and Money conference in London. What was your message?

LR: The take-home message is that the resource market is notoriously cyclical. It’s a no-brainer to buy at the bottom of the cycle and sell at the top of the cycle. While we may not be exactly at the bottom, we are close enough that now is a good time to buy gold and gold equities. I noted that there are a significant number of buyers in the market who at this stage are quietly accumulating.

The higher-quality junior companies in the sector are starting to see a strong level of support at their current prices and many of them are notching higher. The professionals who are most familiar with the resource markets understand the cyclical nature of these markets and, more important, they know how to differentiate among the 2,000 publicly traded junior companies.

The risk is in failing to get into the market before it is too late to win big. If an investor waits for a clear signal that the market has bottomed, the good quality companies will already have moved up substantially. At that point, wannabe investors will be forced to pay high prices for the quality companies or, worse, to buy second-tier companies thinking they are getting a bargain.

TGR: How do you decide which junior precious metal firms to buy or hold or sell in the current environment?

LR: The most important thing is that a company has a quality asset. In this market, a junior needs to have a deposit, ideally an advanced-stage deposit. Investors are more risk averse now than normal. They want to see something tangible and real that they can put a hard value on. I am focused on companies that are drilling a reasonably large deposit with a good grade that can generate a decent return in the current metal price environment. Grade is very important; it will be some time before the huge low-grade deposits that were once all the rage will come back into vogue.

TGR: What about firms that have really good management and a lot of potential, but do not control a quality asset yet?

LR: We are in a hunter’s market. Companies with good management and cash in hand are going to be making some very value accretive acquisitions in the very near term. Everybody wants to control at least one deposit. The focus now is on companies that are adding shareholder value aside from moves in the metal prices.

TGR: Can you give us some ideas?

LR: True Gold Mining Inc. (TGM:TSX.V) is a tremendous example of what’s happening in the market. The company has a great asset with near-term production potential and a very strong management team that raises money. Its stock is trading at a very low value relative to what this kind of quality asset was trading at before the last couple of years. True Gold is precisely the kind of company that will be sought after by people in the know. On the other hand, True Gold is determined to build a mine on its own and it certainly has the capability of doing that. Management has scaled back its development plan to a level that a junior can self-finance.

TGR: They are not crybabies?

LR: A lot of companies are claiming that it is difficult or impossible to raise money in the junior resource market. Not true at all. In fact, there is an enormous amount of money sitting on the sidelines evaluating companies and looking to make a move. That money almost to a penny is aimed at producing or near-term producing situations. A large part of it is private equity looking for near-term or current cash flow. True Gold will find financing because it has a quality management team and a good asset with production in sight.

TGR: What other companies are you following?

LR: Pretium Resources Inc. (PVG:TSX; PVG:NYSE) has a large, high-grade deposit in a favorable jurisdiction. The company’s challenge is that the gold distribution within the deposit is very erratic. It has found spectacularly high-grade intercepts in the drilling, and the bulk sample confirmed the grade is there. Pretium needs to convincingly average its high-grade points across a larger bulk of material that can be mined. The challenge is for the engineering firms involved to agree on an approach that allows Pretium to project drilled samples across the larger volume of material. The results of the bulk sample were better than predicted, but the challenge is getting to a suitable level of confidence by averaging across the entire volume.

TGR: Is there any reason to buy Pretium right now?

LR: Pretium’s price recovered fairly strongly after it announced results for the first part of the bulk sample. The engineers are now working with those numbers. There is a lot of upside potential here. Nobody doubts that there is a lot of gold in the ground. But it is necessary to be able to predict the distribution of gold within the deposit in order to develop a reliable mine plan. That will be done; it’s just a matter of how long it will take to finish.

TGR: Do you have any picks in the platinum space?

LR: Within the precious metal realm, platinum has very favorable economics, even better than gold. Platinum is primarily an industrial metal and its fundamentals are very positive. There are not a lot of platinum companies to choose from. I particularly like Wellgreen Platinum Ltd. (WG:TSX.V; WGPLF:OTCPK;). The company’s new management team has re-evaluated what was previously seen as a large, low-grade nickel-copper deposit. Now, that type of deposit often has platinum associated to it. Wellgreen re-thought its geological approach and re-assayed a lot of the old drill core. Then, it drilled new holes and confirmed its new geological interpretation: It is now looking at one of the most attractive, undeveloped platinum deposits on the planet.

TGR: What is going on for precious metal juniors in Asia?

LR: There is a great company in Fiji called Lion One Metals Ltd. (LIO:TSX.V; LOMLF:OTCQX; LY1:FSE). It recently bought a deposit that had been evaluated about a decade ago by a company that was operating a nearby mine. The previous company had planned to develop the deposit as a satellite. But the main mine went bankrupt and the situation was tied up for years until the Lion One group bought the deposit. Lion One has re-evaluated the old drill core and by re-assaying it found significant intervals of gold that had not been picked up in the previous round. It has drilled quite a number of new holes and confirmed the presence of a very substantial area with a high-grade gold occurrence. It is moving toward permitting and developing a new mine.

TGR: What about Mexico?

LR: Our Resource Opportunities newsletter has had huge success covering the early days of First Majestic Silver Corp. (FR:TSX; AG:NYSE; FMV:FSE) andEndeavour Silver Corp. (EDR:TSX; EXK:NYSE; EJD:FSE). We are now looking for companies following a similar path. Santacruz Silver Mining Ltd. (SCZ:TSX.V; 1SZ:FSE) fits that trajectory. Remember, First Majestic and Endeavour achieved fantastic success by developing past-producing silver mines and then bringing subsequent mines on with a strong operating team. Santacruz has four silver deposits with past production. The company has now brought the first mine into production. It has started development on the second deposit and the other two are in the pipeline.

I really like the model of looking at past-producing mines with a data set in place. For example, Cayden Resources Inc. (CYD:TSX.V; CDKNF:NASDAQ) has optioned a Mexican property from a major that was not quite able to put all the pieces together for a district-scale play. Cayden is coming up with very good results that support the idea that there are a number of significant gold deposits along what could become a very substantial trend.

Another firm looking at past producers for redevelopment is Western Pacific Resources Corp. (WRP:TSX.V) in Utah. The company has the Deer Trail mine with a production history spanning more than 100 years. There is already a mill in place. Western Resources just announced a financing package intended to bring that property back into production. In fact, I recently worked with a U.S. private equity group to put the Western Resources package together. There is a really interesting twist to it: base metal streaming.

TGR: Please explain the nature of this streaming.

LR: Most investors in the precious metals sector are familiar with Silver Wheaton Corp. (SLW:TSX; SLW:NYSE) and its silver streaming strategy. Streaming is fronting the cash to buy the right to the output of a particular metal over the life of a mine. Silver Wheaton has put up billions of dollars to assist a large number of companies to bring their mines into production or to expand existing operations.

This private equity group is doing it from a different perspective: It looks to stream only the byproduct—the base metals production—of a precious metal company. The company gets access to capital and is able to keep control of its precious metal production. The public companies in this space get a higher multiple on income from precious metals than they do on income from base metals. Streaming is basically a value creating mechanism.

TGR: Who else does this?

LR: A number of private equity groups are looking at doing it. But we have not seen any other transactions of the type that we did with Western Pacific Resources—streaming a byproduct from a precious metal-dominant mine. Sandstorm Metals & Energy Ltd. (SND:TSX.V) streams, but its deals access the dominant base metal stream.

TGR: Any final thoughts about gold today?

LR: The message for the non-crybabies is that the resource market is notoriously cyclical and it makes a whole lot of sense to come in at the bottom of the cycle. Evidence is mounting that we are close enough to the bottom of the gold cycle and the resource market cycle that this is a good time to acquire shares in the best quality junior companies.

TGR: Have a good day, Lawrence.

LR: Thank you.

Lawrence Roulston is an expert in the identification and evaluation of exploration and development companies in the mining industry. He is a geologist, with engineering and business training, and more than 30 years of experience in the resource industry. He has generated an impressive track record forResource Opportunities, a subscriber-supported investment newsletter. Roulston has launched an investment fund, the Metallica Development Fund, to take advantage of severely oversold positions in high-quality resource companies. The focus of the fund is on companies with production and/or advanced-stage exploration and development projects—companies with potential for near-term recovery in value that also have potential for longer-term growth.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Peter Byrne conducted this interview for The Gold Reportand provides services to The Gold Reportas an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: True Gold Mining Inc., Pretium Resources Inc., Wellgreen Platinum Ltd., Santacruz Silver Mining Ltd., Lion One Metals Ltd. and Cayden Resources Inc. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Lawrence Roulston: I or my family own shares of the following companies mentioned in this interview: Western Pacific Resources Corp., Santacruz Silver Mining Ltd., Lion One Metals Ltd. and True Gold Mining Inc. I have been nominated to become a director of Western Pacific Resources Corp. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

Streetwise – The Gold Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported.

Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734.

Participating companies provide the logos used in The Gold Report. These logos are trademarks and are the property of the individual companies.

101 Second St., Suite 110

Petaluma, CA 94952

Tel.: (707) 981-8999

Fax: (707) 981-8998

Email: [email protected]

China’s Secret “Doomsday” Weapon Has America Defenseless

When it comes to the burgeoning Internet of Things (IoT) – whereby companies are equipping everyday objects with internet connectivity – security is an afterthought.

Or as Trend Micro’s (TMICY) Christopher Budd says, “Lurking behind some of the most exciting products being showcased this year are serious privacy and security concerns.”

That’s downright frightening news for consumers. I mean, China could already be assembling a cyber weapon of mass destruction to exploit these vulnerabilities.

Yet, at the same time, it’s unbelievably positive news for investors.

Here’s why…

Another Avenue for Attack

Almost every expert agrees that cyber threats aren’t going away anytime soon.

What’s more, a brand-new frontier of devices is opening up for cyber criminals to target.

Literally billions upon billions of new devices are about to come online – with the ability to send and receive data, no less. And some teenager in Hungary will be able to turn these devices against us, forcing them to bombard the internet with insane amounts of data traffic – grinding vital global websites to a halt.

Or worse. Our sworn enemies could literally kill us by hacking into our medical implants.

Don’t believe me? Then you obviously didn’t see the 60 Minutes piece with former vice president, Dick Cheney, where he revealed that his doctor insisted on disabling the wireless functionality of his heart implant. He feared that terrorists might hack it in an assassination attempt.

And you must have definitely missed my article last week, when I revealed how an unsuspecting refrigerator was commandeered to participate in a 750,000-message spam attack.

Obviously, we can’t stand around defenseless. Our daily lives, our economic security – even our national security – are on the line.

So the investment implication for us is obvious…

Go “long” leading cyber-security companies. Because demand for their services can only go one way from here – up!

In fact, the uptick is already underway.

Cyber-security firms are reporting double-digit quarterly sales growth – almost without exception.

But here’s the $64,000 question: What cyber-security stocks hold the most upside potential?

As promised last week, I’m going to answer that question for you today. I’m a man of my word, after all.

Let’s Make a Deal

Understandably, we’ve witnessed a spate of mergers and acquisitions in the cyber-security space, as big players like Cisco (CSCO) jockey for position.

In the last year alone, the number of cyber-security deals in the United States doubled, according to Dealogic.

So if we want to maximize our profit potential, we’d be wise to identify not only a leading cyber-security firm, but also one that’s a prime takeover target. That means focusing on small-cap players. After all, they’re the most affordable in dollar terms.

With that in mind, the recent deal between FireEye, Inc. (FEYE) and privately held Mandiant proves most instructive.

On January 2, FireEye paid $1.05 billion in a cash-and-stock deal for Mandiant, which works out to roughly 10 times revenue.

Rest assured, the valuation isn’t an outlier. Not when we consider that Cisco paid 12 times revenue for Sourcefire back in July 2013.

If we apply the same multiple for the Mandiant purchase to the remaining independent cyber-security firms, an obvious investment choice emerges for us: The KEYW Holding Corporation (KEYW).

It’s important to note that the company boasts similarly impressive growth rates as its peers. So the fact that it’s trading at a discount to the industry on a price-to-sales basis isn’t based on inferior fundamentals.

Could the upside potential really be that significant, though? Yes, indeed! And don’t just take my word for it.

Wall Street Analyst Goes Rogue

On the heels of FireEye’s deal for Mandiant, SunTrust Robinson Humphrey analyst, Tobey Sommer, wrote in a note to investors that KEYW would be worth over $80 per share in a buyout.

At the time, shares were only trading hands for about $15. So his estimate implies an upside of more than 400%, too.

Never in my career have I witnessed such a bold call from a mainstream Wall Street analyst. It’s not in their nature. They’re herd animals.

Accordingly, I admire Sommer’s willingness to break rank. And, of course, I wholeheartedly agree with his analysis.

Bottom line: With cyber attacks on the rise, don’t be foolish and leave your portfolio vulnerable, too. Load up on shares of KEYW before one of the titans of the industry – like Cisco, IBM (IBM), Juniper (JNPR), Symantec (SYMC), or EMC (EMC) – goes on a buying spree and beats you to it.

Full disclosure: We originally recommended KEYW to WSD Insider subscribers when it was trading for $11.26 per share. And now they’re sitting on an unrealized gain of 48% (and counting).

If you want early access to similar market-beating intelligence, all you have to do is sign up for a risk-free trial here.

Ahead of the tape,

Louis Basenese

The post China’s Secret “Doomsday” Weapon Has America Defenseless appeared first on Wall Street Daily.

Article By WallStreetDaily.com

Original Article: China’s Secret “Doomsday” Weapon Has America Defenseless

Murray Math Lines 30.01.2014 (AUD/USD, CAD/JPY, SILVER)

Article By RoboForex.com

Analysis for January 30th, 2014

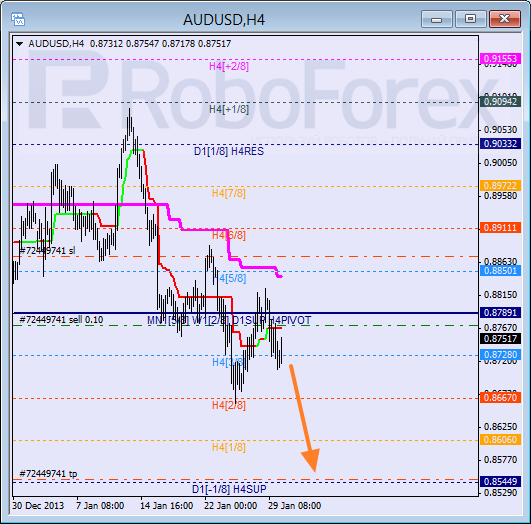

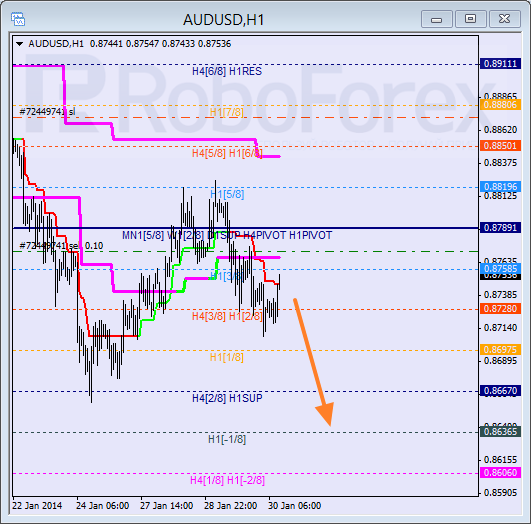

AUD/USD

Australian Dollar rebounded from the 4/8 level and right now is moving below H4 Super Trend again. If pair is able to stay below the 3/8 level, bears will return to the market and continue pushing price towards their target at the 0/8 level.

At H1 chart, Super Trends formed “bearish cross”. Possibly, price may break the 0/8 level and enter “oversold zone” in the nearest future. In this case, later pair is expected to reach and break the -2/8 level.

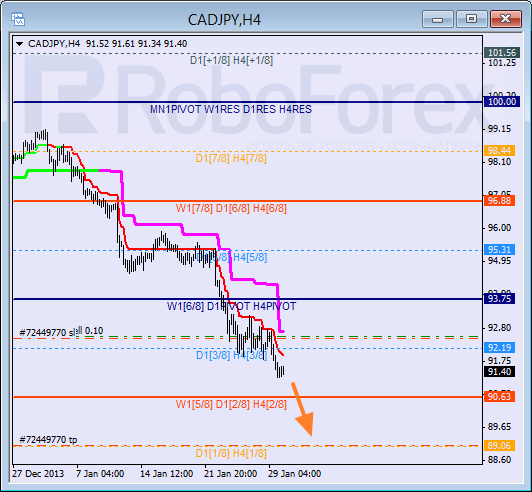

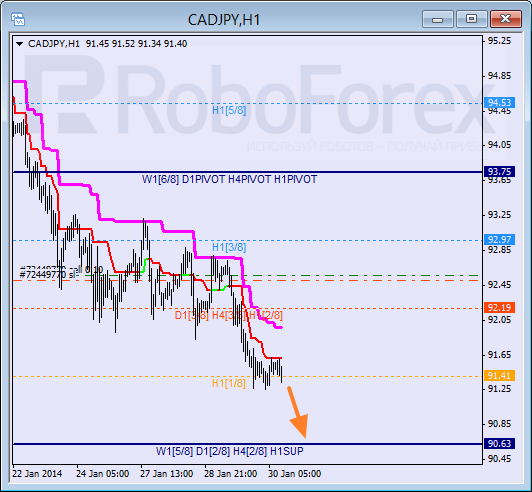

CAD/JPY

After rebounding from H4 Super Trend several times, pair continued falling down. Probably, pair may rebound from the 2/8 level as well, because this level has been tested on major timeframes. Main target for bears is at the 1/8 level.

At the H1 chart we can see, that pair is very close to the 0/8 level; bears are supported by Super Trend. Most likely, price will break the 0/8 level and continue moving downwards inside “oversold zone”.

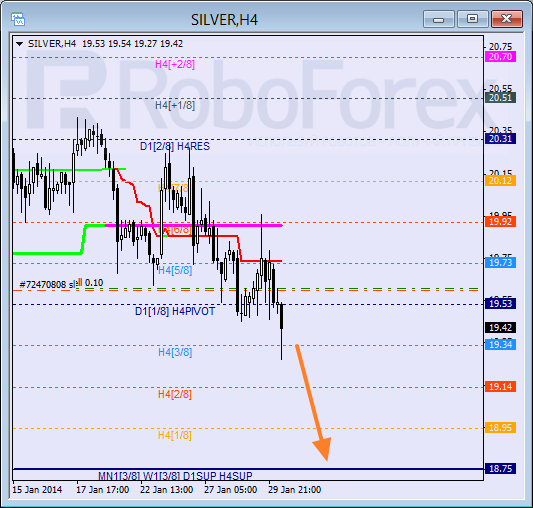

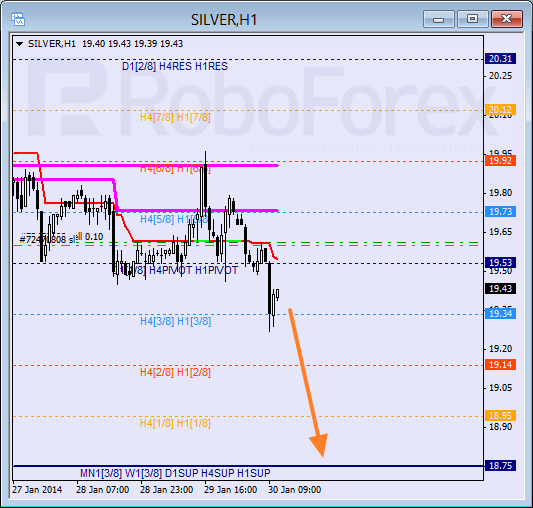

SILVER

Yesterday Silver rebounded from daily Super Trend and then reached new minimum. Taking into account the fact that the market is volatile, I’ve moved stop on my order into the black. Main target is at the 0/8 level.

The lines at the H4 and H1 charts are completely the same. If bears are able to keep price below the 3/8 level, instrument will continue falling down. Closest target for bears is at the 0/8 level, which may later become starting point of new correction.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

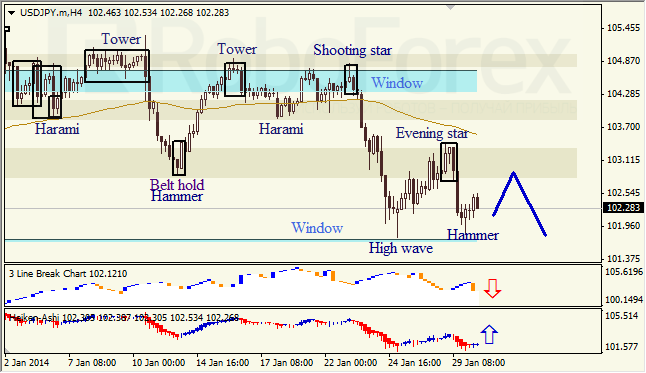

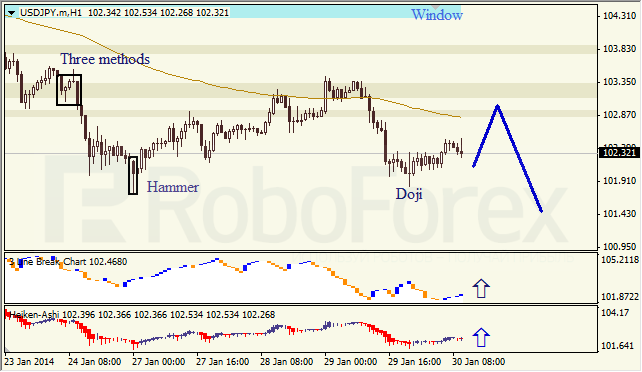

Japanese Candlesticks Analysis 30.01.2014 (EUR/USD, USD/JPY)

Article By RoboForex.com

Analysis for January 30th, 2014

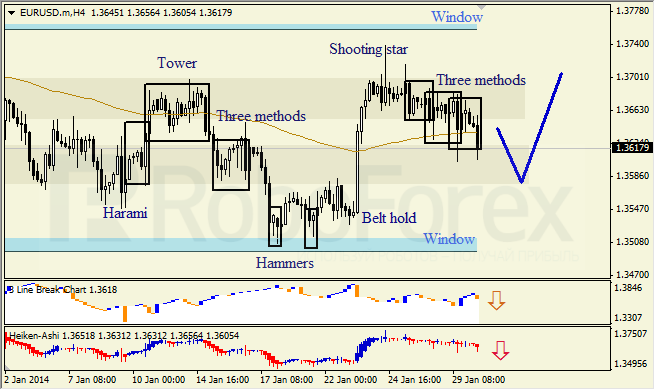

EUR/USD

H4 chart of EUR/USD shows correction, which is indicated by Shooting Star pattern. Bearish Three Methods pattern, Three Line Break chart, and Heiken Ashi candlesticks confirm descending movement.

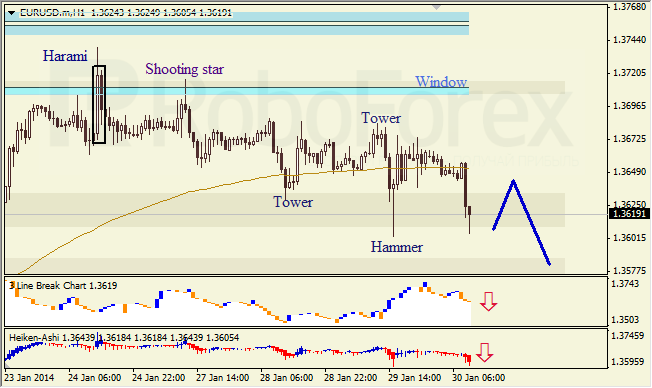

H1 chart of EUR/USD also shows correction. Closest Window is resistance level. Three Line Break chart and Heiken Ashi candlesticks confirm descending movement.

USD/JPY

H4 chart of USD/JPY shows descending trend, which is indicated by Evening Star pattern. Lower Window is support level again. Three Line Break chart indicates current trend; Hammer pattern and Heiken Ashi candlesticks confirm bullish pullback.

H1 chart of USD/JPY shows sideways correction within descending trend. Doji pattern, Three Line Break chart, and Heiken Ashi candlesticks confirm ascending movement.

RoboForex Analytical Department

Article By RoboForex.com

Attention!

Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex LP bears no responsibility for trading results based on trading recommendations described in these analytical reviews.

Are Stocks Primed to Bounce Back?

Bounceback or dead cat bounce?

We’re sure you know what we’re referring to.

It’s got nothing to do with animal cruelty.

A dead cat bounce is a way to describe a market when stock prices bounce after a big fall.

They call it a dead cat bounce because sometimes it’s only a brief bounce before the stock price falls again — much in the same way as a cat would (we assume) ‘bounce’ off the pavement if dropped from a great height…but then fail to get up again.

So, after the Australian share market’s 65 point fall on Tuesday and 54 point gain yesterday, are stocks bouncing back from the low with further gains to come, or is it merely a short-term jump before stocks resume their downward trend?

The overnight numbers from Wall Street provide some clue. The Dow Jones Industrial Average fell 1.2%.

There’s no doubt there are a bunch of problems with the world economy.

We won’t cover them all again here because you’re probably sick of hearing about it. To be honest, we’re sick of writing about it. We’ve felt that way for the past three years.

We were sick of so-called experts pointing out all the problems but never coming up with ways to profit from what was happening; ‘don’t tell us what’s wrong, tell us how to make money.’

It won’t surprise you to know we heard that message loud and clear from readers like you.

What’s Better Than Stocks?

One thing we want to make clear is that we’re not a stock market cheerleader. We don’t always believe that stocks are the best place to put your money.

That’s why we only recommend that you put a maximum of half your investable assets into stocks. Stocks can be risky. You need to choose carefully when to buy them and when to buy other assets, such as gold…or even to stay in cash.

But right now, despite the volatility, we say that buying stocks makes the most sense for investors. There just isn’t any other type of investment that you can easily buy and sell which can give you the same type of returns.

Although it’s fair to say that not everyone shares our view. There are others who think that the recent bout of volatility involving emerging markets is big warning sign.

One of those with that view is Satyajit Das. Das is a well-known finance professional and author. He was the star performer at the first Port Phillip Publishing conference in 2012. He’s back to present at our next conference in March — World War D: Money, War & Survival in the Digital Age.

In a recent interview with the ABC, Das said:

‘In the short run, what will happen is the actual flow of liquidity out of emerging markets will expose the fact that these markets are heavily dependent on, number one, foreign capital, and much of what was called the “boom” in emerging markets may be just the effect of short-term capital flows and particularly the effect of lower interest rates.’

Das says this flow of capital out of emerging markets could lead to problems with local banking systems and even defaults, both by private institutions and even governments.

If such a situation plays out, holding stocks would be a risky investment choice.

So, does that mean you should sell now?

Don’t be Fooled, the Fed is Still Printing

If things play out as Das expects then the answer would be yes.

But we’re not prepared to give that advice.

While many analysts and commentators focus on the prospects of another stock market crash, similar to that seen in 2008, our view is that the market dynamics are very different to what they were then.

That’s not to say things are better. You only have to look at the amount of money printing that has happened since 2008 to understand that things aren’t better.

But what has changed is that today there’s no question about the willingness of central banks and governments to intervene in the market.

It’s not a question of if they’ll do so, it’s a question of when and how much. That’s why you see the market volatility today.

And that’s why you see the market ‘misbehave’ after the US Federal Reserve decided to cut back on its bond-buying program.

But, as we’ve noted previously in Money Morning, even if the Fed tapers its bond-buying program to zero by October this year, it will still have printed nearly half-a-trillion dollars in money in order to buy US government bonds.

That’s more than the amount the US government spent on the infamous TARP bailout package back in 2008 and 2009.

We won’t pretend to know exactly how things will play out in the markets over the next few days. Events have a funny habit of doing the unexpected.

But just as we told you to keep investing while most others ran for cover when Japanese interest rates climbed last year, when China’s economy appeared to slow, and when all the talk was of the US Fed stopping the printing presses…we’ll tell you to keep investing now.

Hold on to those good dividend paying stocks. Keep your money in those speculative small-cap stocks. And buy into beaten down markets when the opportunity presents.

We say buy emerging markets, and we also say to buy the other major victim of the current panic — mining stocks.

Fortunes Are Made in Recessions

Although it may seem crazy, it looks to us like the Aussie mining sector is bouncing back. The past two years has been terrible for resource stocks, but if we’re right about the market heading towards a turning point, this is where brave investors can make a lot of money.

A statistic we like to point out is that around half of the Fortune 500 companies came into existence during recessions or depressions. So when folks try to tell us it’s too risky to invest, we tell them that the depths of a bear market are where investors can make a fortune.

For that reason you should keep an eye out for a special research report which will be available online this weekend. In it resource analyst Jason Stevenson makes the case for a major bounce back in a handful of key mining sectors in 2014…including three beaten down Aussie miners that could lead the way.

The fact is, investing is always risky, and right now it’s as risky as heck.

But as any experienced investor will tell you, when the market is this risky, more often than not, that’s exactly the time when you should buy.

Cheers,

Kris+

Special Report: Retirement Security Ladder

Why I’m Thinking of Shorting Apple Stocks

‘Can’t innovate any more, my ass!’

Apple’s head of marketing, Phil Schiller, came across a little defensive in his speech at last year’s Macworld conference. I can see why he might feel that way! For the last decade, Apple set the pace when it comes to consumer electronic gizmos…but now, its competitors are closing in.

In fact, I think Apple’s glory days could be over…

Don’t get me wrong — Apple is a great business. But I have severe misgivings about its longevity, and the way it treats its customers. Last week, I seriously looked at shorting Apple’s stock…but in the end, I thought better of it. After all, Apple’s products are still selling like hotcakes, and it’s making great strides into the emerging markets.

Apple released a trading update on Monday…and boy did I wish I’d put my money down on a short position! It reported record profits, but the stock took an 8% whack.

Apple’s problem isn’t sales. It’s got plenty of those. The problem is growth — or lack thereof. And if Apple is no longer considered a growth stock, then there needs to be a fundamental revaluation of the shares.

Apple is no better than Ryanair

At first sight, Apple’s customer service may look nothing like Ryanair’s. After all, Apple’s loyal fan-base seems to love the products, and I’m pretty sure that Apple doesn’t flagrantly abuse its customers like Ryanair. But there are some similarities.

First, customers are loyal because they’re forced to be. Apple operates what’s known as a ‘walled garden’. Apple controls its products’ operating software and also decides what applications and services you’re allowed to use.

Like Ryanair, once you’re on its plane, you’re limited to what it wants to offer you. Three quid for a bottle of water anyone?

But it’s not just customer services that Apple controls with its iron fist. It’s the actual hardware too. One of the big reasons I’m against Apple’s mobile gadgetry (which is the most important aspect of Apple’s business) is because of how limiting the stuff is.

Take the latest iPhone. It’ll cost you 50 quid more for a higher spec unit if you want to increase the memory from a measly 8Gb to 16Gb. Other customers can just add a memory card to their phone. I just upgraded my phone’s memory by 32Gb for less than £15.

Of course, this means Apple makes very decent margins. In fact, Apple’s gross margin comes in at just under 40% — that’s at least double what any other hardware maker might expect.

Apple is clearly profitable. But is this sustainable? I propose not. There are now cheaper and better alternatives.

The fall of a giant

Apple just can’t keep up. Market share is falling — from about 18% last year, I see it falling to 15% by the end of this year. Though that may not sound like a lot, but in reality it’s a massive drop.

As market share falls, the business will find it increasingly difficult to keep up with Google’s Android offering.

Regular readers will know that I’m a fan of Google, and the way it’s using cloud technology to integrate the user experience. I’m working on documents on my laptop, phone and tablet, seamlessly in the ‘cloud’. I know that Apple offers something similar — but it’s just not as joined up as Google.

Apple’s Research and Development budget has doubled in the last two years. But still market share dwindles. The fact is, Google doesn’t need to spend gazillions on trying to keep up. Much of the R&D function is effectively done by outsiders. They don’t need to control the whole process. Not only is this approach cheaper, but it produces better results.

As I survey the market for Android devices, I see products that could suit just about anyone’s requirements. Literally thousands of devices. With Apple on the other hand, you have to pick from a very limited range indeed.

Of course, Apple has been able to get away with all of this in the past. After all, it was the innovator. It seemed to know what the punter wanted before the punter knew it himself.

But now, it looks like the game could be up. Manufacturers across the globe are innovating like mad. Apple can’t keep up. A walled garden approach simply isn’t good enough.

On Tuesday Apple’s biggest hardware rival, Samsung, announced that it is to launch 60 new retail stores across Europe. It’s talking about a ‘powerful new retail concept’ that will include an ‘exciting new customer experience with merges retail and technology innovations’.

I guess what it’s talking about is an experience not unlike Apple’s wonder stores?

Apple is going to get hit from all sides. Watch out as the great innovator gets out-innovated.

Bengt Saelensminde,

Contributing Editor, Money Morning

Ed Note: The above article was originally published in MoneyWeek.

From the Archives…

Just How Secure is a Smart Home Security System?

25-01-14 — Shae Smith

Monkey Derivatives won’t pay you in Retirement, but this could

24-01-2014 — Kris Sayce

An Aggressive Way to Achieve Amazing Growth in the Market

23-01-14 — Tim Dohrmann

Last Year Was Great for Stock Investors, But 2014 Could Be Even Better

22-01-14 — Kris Sayce

Why It’s Too Soon to Burst the Stock Price Bubble

21-01-2014 — Kris Sayce

Why I’d Rather Pick Bubbles Than Stock Market Crashes

20-01-2014 — Kris Sayce