The US dollar continues to strengthen against most currencies. The US dollar index (#DX) closed in the positive zone (+0.18%). Participants in financial markets are awaiting meetings of Central Banks to be held in the next two weeks. On Thursday, a meeting of the European Central Bank is expected. After that, the Bank of Japan will decide on monetary policy, and next week the Fed’s meeting will take place.

Yesterday, members of the Conservative Party of Great Britain voted for the new party leader, who will take the post of Prime Minister. The name of the new 77th Prime Minister of Great Britain will be known today at 15:00 (GMT+3:00). Two candidates fought for the post: former Foreign Secretary, Boris Johnson, and the current head of the same department, Jeremy Hunt. The most likely winner is Johnson.

The single currency fell against the US currency due to investors’ confidence that at the next meeting of the ECB, the head of Mario Draghi will point to a decrease in the interest rate in September. The likely rate reduction is connected with the tension in international trade relations.

In addition, participants of financial markets continue to monitor the development of trade relations between the United States and China. It became known that the US delegation, led by US Trade Representative Robert Lighthizer and US Treasury Secretary Steven Mnuchin, will go to Beijing next week to resume talks with China.

The “black gold” prices show a positive trend amid tensions in the Middle East. At the moment, futures for the WTI crude oil are testing the mark of $56.35 per barrel. At 23:30 (GMT+3:00) the API Weekly Crude Oil Stock report will be published.

Market Indicators

Yesterday, the bullish sentiment was observed in the US stock markets: #SPY (+0.25%), #DIA (+0.07%), #QQQ (+0.80%).

The yield on 10-year US government bonds is at 2.04-2.05%.

The news feed for 2019.07.23:

– Existing home sales in the USA at 17:00 (GMT+3:00).

The National Association of Realtors will be releasing the US existing home sales report today.

Forecasts show that existing home sales will rise by 5.35 million or about 1.2% on the month ending June 2019.

This follows May’s increase of 2.5%, where existing home sales rose by 5.34 million. But on a year over year basis, existing home sales are down 1.1%.

The gains in May were the first in two months. Therefore, if the data for June matches or beats estimates, it would mark a second consecutive month. The data could also help improve the year over year levels as well.

U.S. Existing Home Sales, May 2019

The existing home sales report measures completed transactions across single-family homes, townhomes, and condominiums. The report also only covers sales of already constructed (existing) homes or units.

The uptick in the existing home sales is seen as a reflection of the favorable conditions on the ground. This comes amid falling mortgage rates and with inflation staying low. The outlier remains the wages, of course.

The US labor market went through a downtrend in the months leading up to May. But there was a rebound in June. However, we will have to wait to see the data for July if this rebound is sustainable.

As long as wages outstrip inflation and mortgage rates (dictated by the Fed funds rate) are low or falling, there is a possibility for home sales to rise.

Falling Fed Funds Rate Could See Housing Affordability Rising

In May and June, there was a lot of chatter about the Fed funds rate. It was more evident during these periods that the Fed will cut rates. This, of course, has an impact on the borrowing costs for home purchases.

With the Fed due to cut rates in July and maintaining a dovish outlook, mortgage rates are likely to fall further if the dovish outlook continues.

But the ground reality shows that the housing markets are yet to respond. In a recently released report, US homebuilding activity fell for a second consecutive month in June. Meanwhile, housing permits fell to a two-year low.

The data indicates that housing markets are yet to respond to falling mortgage rates. However, the uptick in existing home sales could start to bring some optimism.

While the housing construction activity is often seen as a leading indicator of recession, data has been mixed. With the Fed pledging to cut rates, this marks a proactive move from the central bank.

Mortgage rates in the US are currently averaging around 3.75%, compared to November last year when mortgage rates rose to 4.94% for a 30-year fixed mortgage.

We could expect to see the housing market data staying mixed in the near term. There could be a lag of up to three months in order for the various indicators to tick higher. But, having said that, the cost of raw materials for construction could dampen the outlook.

There are already higher costs of imports for steel and aluminum raw materials, one of the key elements in housing construction. With the US-led tariff wars, the cost of other materials has also suffered the impact.

Thus, there is a delicate balancing act in the housing markets as it weathers various conditions, ranging from lower mortgage rates, but offset by a higher cost of building materials.

Existing Home Sales Could Improve

In the past, central bank officials reacted to the downturn in the economy. Thus, we could expect to see home buying and construction likely to pick up in the months ahead.

While there is scope for housing activity to decline, for the moment, the prospect of an impending recession is still far off. Thus, the impact of the lower interest rates could help revive home buying sentiment among US consumers.

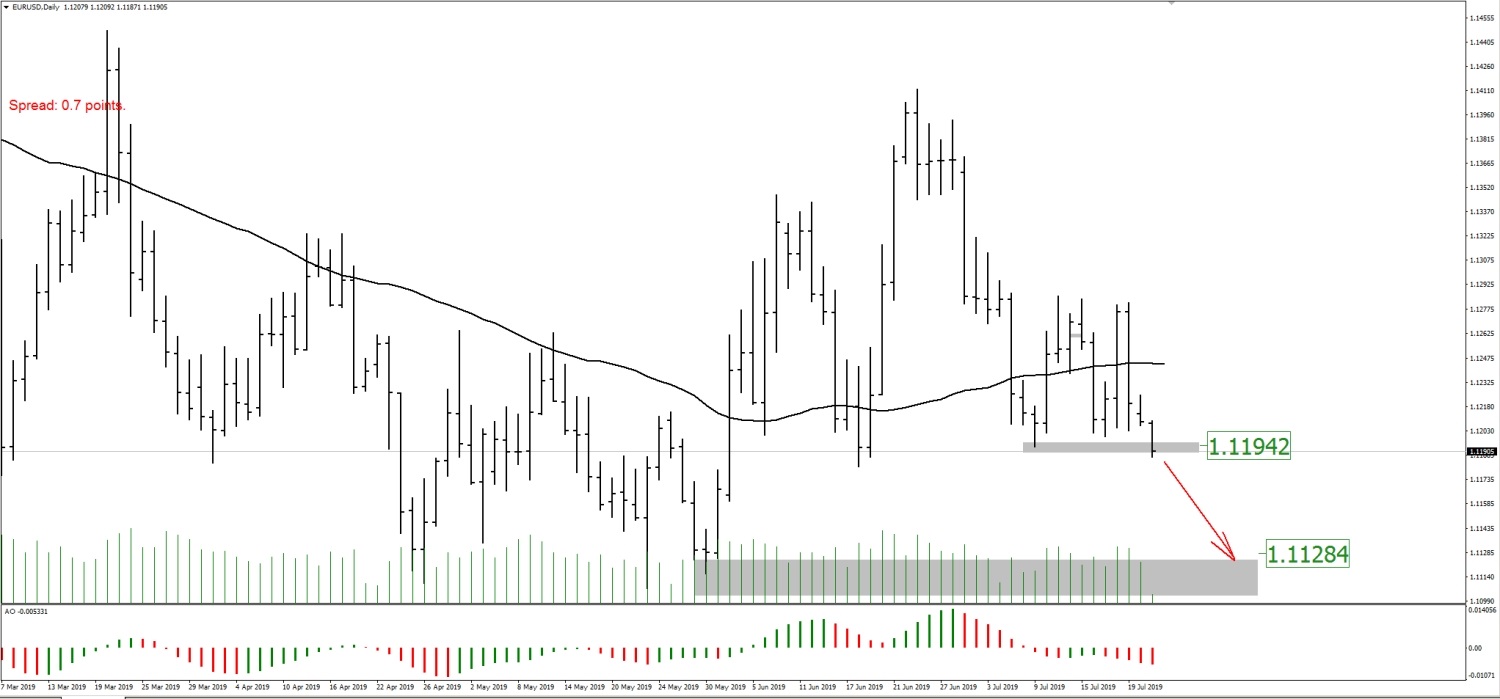

On Monday the 22nd of July, trading on the euro against the dollar took place within a corridor of 1.1225 to 1.1206 across all sessions, closing around the 1.1208 mark. Such a narrow trading range was down to a lack of any significant news or macroeconomic data. In today’s Asian session during RBA Deputy Governor Kent’s speech, we got a breakout of a crucial zone between 1.1194 and 1.1189, which gives us reason to believe that the market is set to decline.

The breakout of 1.1194 gives us a sell signal on the EURUSD pair, with a rough target of 1.1108. In the long term, despite expectations that the dollar is set to rise against the euro, it’s perfectly feasible that things will work out differently. Given the escalation of currency conflicts between the ECB, the Fed, and the banks of Japan and China, along with forthcoming rate slashes, it’s impossible to say conclusively that the dollar is set to rise.

The British Pound is shaky this morning as anticipation mounts ahead of the announcement of the next Tory leader and Prime Minister.

Although expectations remain heated over Boris Johnson becoming the new Prime Minister, the reality has the potential to weaken the Pound significantly.

Focusing on the technical picture, prices are trading towards the 1.2400 level. A breakdown below this point should open a path towards 1.2350.

GBPJPY hovers near 6 month low

GBPJPY could jump back into the drivers seat this week if fears of a no-deal Brexit reduce appetite for the British Pound.

This currency pair is firmly bearish on the daily charts and is likely to sink lower once a daily close under 134.00 is secured. With attraction towards Sterling fading by the day amid Brexit uncertainty, the GBPJPY could test 132.00 in the short to medium term.

EURGBP eyes 0.9000

A weaker Pound could send the EURGBP shooting back past 0.9000 today. A daily close above this point should open the doors towards 0.9060 this week.

GBPAUD trades around 1.7700

Renewed fears of a no-deal Brexit could send the GBPAUD below 1.7700 this week. Sustained weakness below this point should open the doors towards 1.7600 and 1.7500.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

By CentralBankNews.info Paraguay’s central bank lowered its policy rate for the third time this year, saying there is a space to give the economy a monetary boost as inflation is still expected to converge toward the bank’s 4.0 percent target. The Central Bank of Paraguay (BCP) cut its key rate by another 25 basis points to 4.50 percent and has now lowered it by a total of 75 points this year following earlier cuts in February and March. In April, May and June the rate was kept steady and BCP said the next monetary policy decision would depend on the evolution of both domestic and external macroeconomic data. “The economy remains weak, both on the activity and demand side,” the central bank said, adding some progress around reforms has been seen on the regional level, which has also helped strengthen the exchange rates of those countries. However, there is a still uncertainty on the international level from the trade conflict between the U.S. and China although the economies of the main advanced economics and emerging economies are still growing at moderate rates, helped by more lax monetary policy. Inflation in Paraguay has remained below the target for several months and inflationary pressures remain limited, which could affect the convergence of inflation to the target, BCP said. Paraguay’s inflation rate eased to 2.8 percent in June from 3.8 percent in May, below 2018’s average rate of 3.6 percent and the 4.0 percent target, while the economy shrank 0.9 percent in the first quarter of 2019 from the fourth quarter of 2018 for an annual drop of 2.0 percent. In May the International Monetary Fund forecast growth this year of 3.5 percent, down from 3.7 percent in 2018, with risks tilted to the downside, mainly from weaker-than-expected growth in Argentina and Brazil, weather-related shocks and delays in public investment.

US stock market resumed advancing on Monday led by technology shares. The S&P 500 gained 0.3% to 2985.03. Dow Jones industrial added 0.1% to 27171.9. The Nasdaq composite rose 0.7% to 8204.14. The dollar strengthening decelerated: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, added 0.2% to 97.28 and is higher currently. Stock index futures point to higher market openings today

CAC 40 outperforms European indexes

European stocks ended little changed on Monday as companies reported mixed quarterly results. Both GBP/USD and EUR/USD continued their slides and are down currently as European Union trade official said EU sought to work with Washington to reform the World Trade Organization and cooperate on common challenges to global trade, but will retaliate if Washington makes good on its threat to raise car tariffs. The Stoxx Europe 600 index ended flat. The DAX 30 added 0.2% to 12289.40. France’s CAC 40 rose 0.3% and UK’s FTSE 100 edged up 0.1% to 7514.93.

Nikkei leads Asian indexes rebound

Asian stock indices are recovering today after reports U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin would travel to Beijing next week to resume trade negotiations with China. Nikkei closed 1% higher at 21620.88 as yen slide accelerated against the dollar. Markets in China are rising buoyed also by news President Donald Trump had agreed to make “timely” licensing decisions for U.S. tech companies seeking to renew sales with Huawei: the Shanghai Composite Index is up 0.4% while Hong Kong’s Hang Seng Index is 0.2% higher. Australia’s All Ordinaries Index rebounded 0.5% as Australian dollar continued its slide against the greenback.

Brent futures prices are edging higher today as traders watch for developments in the Strait of Hormuz after Iran seized a British tanker last week. Prices rose yesterday: September Brent crude gained 1.3% to $63.26 a barrel on Monday.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

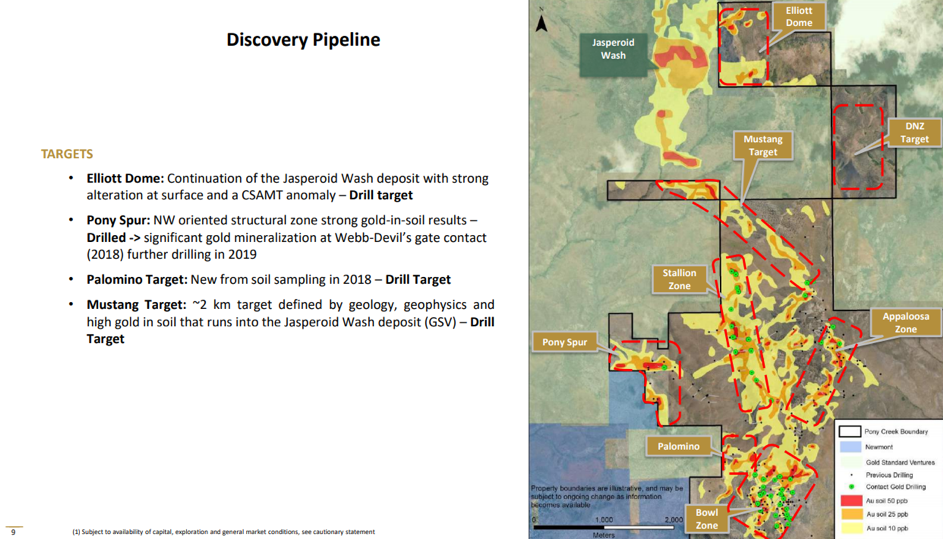

For this Nevada miner, 2019 should be a busy and interesting year of exploration, says Thibaut Lepouttre of the Caesars Report.

Going back to the Bowl Zone yields the desired results

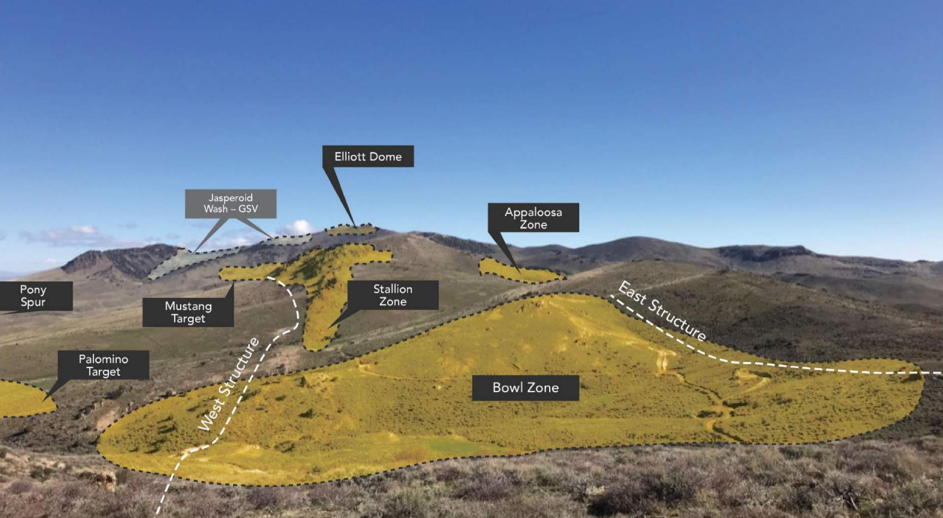

After a successful exploration campaign in 2018, wherein Contact Gold Corp. (C:TSX.V) confirmed the widespread presence of gold mineralization on its greater Pony Creek area (with very thick intervals such as 93 meters at 0.33 g/t gold), the company decided to go back to the main Bowl Zone, which hosts the majority of the historic resource estimate (1.4 million ounces at 1.5 g/t gold). We aren’t sure that historical estimate is very reliable, so perhaps it’s safer to assume there’s around 0.7-1 million ounces at the Bowl Zone.

Nevertheless, this zone could be the kick starter for all future exploration and development programs at Pony Creek. While we totally understand the company’s desire to go out there and kick the rocks to figure out what Mother Nature has hidden on the property, it could make more sense to have some sort of “main” zone that could be developed, where the cash flows from mining that zone could then be used to go hunt for more discoveries. After all, you can run a mine with 93 meters at 0.33 g/t (especially with Contact Gold’s excellent metallurgical test results) but you can’t build a mine with those grades.

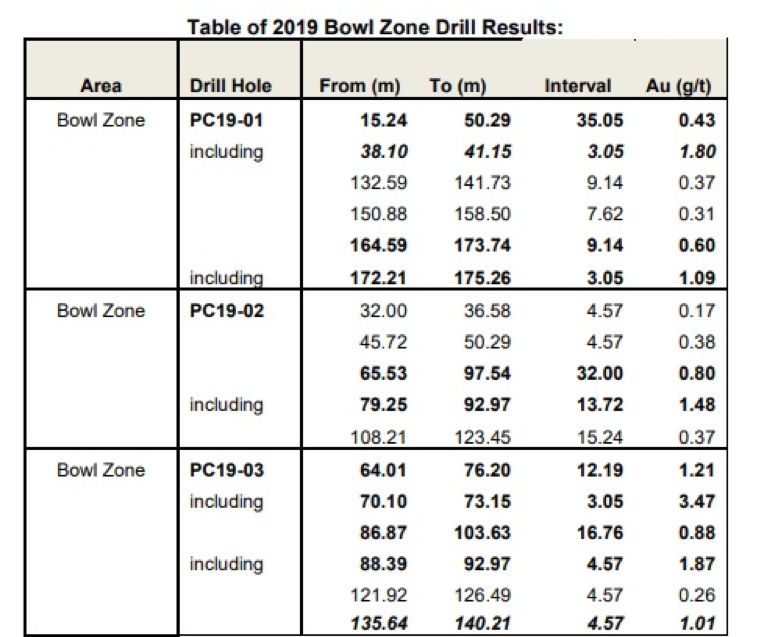

Now that Contact Gold’s bank account has been cashed up with the proceeds of a CA$4 million (CA$4M) public offering (and the CA$2.85M private placement that closed in March), the company went back to the Bowl Zone, and the initial results are very pleasing.

Only three holes have been reported so far, but with 35 meters containing 0.43 g/t gold almost starting at surface (the interval stated just 15 meters downhole), 32 meters at 0.8 g/t, and 12 meters at 1.21 g/t gold, immediately followed by almost 17 meters containing 0.88 g/t gold starting just 10 meters below the previous interval, Contact Gold has confirmed the higher grade gold mineralization at the Bowl Zone. Some of the reported intervals are relatively deep, but that’s not necessarily an issue, as you’d obviously design the open pit so that you can excavate the tonnes that are the closest to the surface first.

Surprisingly, the market didn’t seem to care at all about these intervalssurprising, considering even the near-surface 0.43 g/t gold over 35 meters would result in healthy operating margins. Applying Contact Gold’s average recovery rate of 8590% (as published in May 2018), the recoverable gold value would be around 0.37 g/t for a rock value of $16.6 per tonne using a gold price of $1,400/ounce.

Low? Absolutely. But the processing costs of a heap leach operation in Nevada are low as well. Fiore Gold Ltd. (F:TSX.V; FIOGF:OTCQB), for instance, has a mining cost of $1.50/t and a processing cost of $1.22/t. Even with a 3:1 strip ratio, the operating expenses would be just $7.5/t, leaving a margin of $9/t on the table. Although we agree the head grade of 0.43 g/t appears to be only marginally better than last year’s 0.33 g/t interval at the Stallion Zone (previously called the West Zone, a few kilometers away from Bowl), the latter has a recoverable value of just $12.6/t, indicating the margins would be approximately 40% lower.

Ten holes have already been drilled to offset the higher grade (and more oxidized) corridor that was encountered in 2018, and we should see more exploration results come in over the next few weeks.

Contact Gold is now fully cashed-up for the season

As of the end of March (the financial statements for the June quarter should be filed in a few weeks), Contact Gold had in excess of CA$2.2M in cash on its balance sheet, thanks to closing a CA$2.85M financing in March. That round was priced at CA$0.29, and rather than attaching a warrant to the share, Contact Gold’s management team came up with a refreshing idea: it would issue “bonus shares” rather than warrants.

The reason behind this was simple: Warrants do create a certain overhang, but on the other hand, the participants in that private placement deserved some sort of kicker, as the hold period was 12 months (which will be reduced to six months once Contact Gold completes the paperwork related to its public offering of shares in May).

Indeed, subsequent to the end of the quarter, Contact Gold completed a larger offering, raising CA$4M by issuing 20 million shares at CA$0.20. This means that we can reasonably expect the company’s cash position to exceed CA$3.5M as of the end of June, and the cash will go a long way to fund the planned exploration activities in 2018.

Interestingly, insides of the company took care of almost half of the March placement at CA$0.29. CEO Matthew Lennox-King acquired almost 259,000 shares (for a total investment of CA$75,000) while CFO John Wenger and director John Dorward invested an additional CA$15,000 and CA$50,000 in that CA$0.29 placement. Other directors also participated in the financing, so it’s clear they continue to keep their interests aligned with the shareholders. CEO Lennox-King basically reinvested (more than) his bonus of fiscal year 2018 back into the company, a gesture we certainly can appreciate.

Conclusion

2019 will be a very interesting exploration year for Contact Gold, as the company is planning a step-out drill program at the Bowl Zone and the Appaloosa Zone, which should result in a first NI-43-101-compliant resource estimate (we would be fine if this maiden resource estimate would just focus on the Bowl Zone if this means Contact Gold would be able to achieve the “critical mass” status at Bowl to advance the zone toward a preliminary economic assessment).

2019 will also be a busy year for Contact Gold, and thanks to the two raises earlier this year, the company’s treasury is fully prepared for this year’s exploration program.

Thibaut Lepouttre is the editor of the Caesars Report, a newsletter and mining portal based in Belgium that covers several junior mining companies with a special focus on precious metals and base metals. Lepouttre has a Bachelor of Law degree and two economics masters degrees that have forged his analytical approach to the mining sector. Considered a number cruncher, Lepouttre focuses on the valuations of companies and is consistently on the lookout for the next undervalued mining company.

Disclosure: 1) Thibaut Lepouttre: I, or members of my immediate household or family, own securities of the following companies mentioned in this article: a long position in Contact Gold and participated in the CA$0.29 placement. My company has a financial relationship with the following companies referred to in this article: Contact Gold. I determined which companies would be included in this article based on my research and understanding of the sector. Additional disclosures are available here. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.

At least the Financial Times now has come clean about its hostility to gold – as well as to free markets and elementary journalism.

Gold Anti-Trust Action Committee (GATA) friend Chris Kniel of Orinda, California, sent to the newspaper’s chief economic columnist, Martin Wolf, the excellent summary of gold and silver market manipulation just written by gold researcher Ronan Manly.

Wolf replied derisively and dismissively: “This is a matter of absolutely no importance whatsoever. Who cares about the prices of useless metals?”

Stunned by such a counterfactual assertion, Kniel prompted Wolf to elaborate, receiving this from the FT columnist: “I mean to dismiss the whole monetary history of gold. It has no significance in the modern world. It is, as Keynes said, a barbarous relic.”

Actually, Keynes’ “barbarous relic” remark was made not about gold itself but about the gold standard for currencies. Keynes wasn’t denying gold’s use as money. But that is the least of the problems with Wolf’s reply.

Who cares about the prices of useless metals? “No significance in the modern world”?

For starters, governments themselves care.

That’s why central banks, against Wolf’s advice, continue to hold huge inventories of gold and lately have been increasing them.

It’s why central banks classify gold as a Tier 1 asset, equivalent to government-issue bonds and cash.

It’s why central banks constantly trade the metal and its derivatives surreptitiously, directly and through the Bank for International Settlements, usually to restrain the metal’s price, recognizing that gold is a determinant of currency values, interest rates, and government bond prices.

It’s why the International Monetary Fund forbids its members from formally linking their currencies to gold, lest the metal gain precedence over government-issued currencies.

Further, London is the center of the world’s gold trading, the bullion banks are major employers there, and the FT is based in London, so the newspaper itself ordinarily might care.

Of course, Wolf’s dismissing “the whole monetary history of gold” doesn’t make that history disappear. Indeed, today Agence France-Presse distributed a report about gold’s monetary history that is both fascinating and tragic, gold’s history being a big part of human history.

But Manly’s wasn’t only about gold and silver. It was also about largely secret market rigging by government, and the Financial Times says it’s in the business of reporting about markets.

So is market rigging by government of no concern to Wolf as well? Since such market rigging is now so pervasive – for years now there have really been no markets anymore, just central bank interventions – why does any reader need someone of Wolf’s views of journalism?

And if Wolf’s indifference to both history and market rigging really represents the Financial Times (FT), what does anyone need the newspaper for, except possibly disinformation?

For years, GATA has been supplying FT journalists with documentation of surreptitious intervention in the gold market by governments and central banks. At least twice your secretary/treasurer has delivered such documentation to FT staffers face to face in London – in 2011 to the journalist who is now chairman of the newspaper’s editorial board and U.S. editor at large, Gillian Tett, and in 2017 to FT reporter Thomas Hale.

Tett took enough notice to mention GATA in a column in the newspaper without ever pursuing the issue of market manipulation and without ever putting a critical question to a central bank.

Hale listened politely for 45 minutes, asking a few questions, perhaps not realizing that the FT would never permit him to commit journalism with this issue. Maybe Wolf himself told Hale that market rigging by governments doesn’t matter or at least must not be revealed.

But in fairness to the FT, GATA long has been providing the same documentation to many other mainstream financial news organizations around the world with not much more satisfactory results, though a major story might be gained just by asking the U.S. Federal Reserve and Treasury Departments to specify the markets in which they are secretly trading and why, and then reporting their refusals to answer, and then by asking the U.S. Commodity Futures Trading Commission whether it has jurisdiction over secret manipulative trading by the U.S. government or its agents or if such trading is legal.

For more than a year, those agencies have refused to answer thosequestions for a member of Congress.

Also in fairness to the FT, most monetary metals mining companies don’t care, or pretend not to care, about the suppression of the prices of their products.

But then mining companies are terribly vulnerable to governments for their mining permits, royalty requirements, and enforcement of environmental regulations, and to their bankers, most of whom are formally government agents in financial markets.

By contrast news organizations in the West and in some places in the East are free, at least nominally. So what are they afraid of? What is the FT afraid of? What is Wolf afraid of?

Do they fear not getting invited to the Bank of England’s Christmas party? Or is it the revelation that the conventional wisdom on which Wolf bases his pontification is a bit off?

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

It’s bad enough when bait-and-switch “rare” coin dealers stick it to naive customers. But when one of those shady peddlers got involved with politicians in the state of Ohio more than 15 years ago, it was a major statewide scandal. And the fallout continues today…

Last week, state legislators in Ohio voted to repeal the state’s sales tax exemption on precious metals. Now, starting in October, residents there will generally pay at least 5.75% tax when purchasing gold and silver. Precious metal coins, rounds, and bars may be the only investments they hold that are subject to this additional cost.

Fewer Ohioans, likely, will buy physical bullion. Those who do must pay the state of Ohio for the privilege of investing in something other than conventional securities and real estate – the preferred assets of banks, brokers, and now, Ohio politicians.

Jp Cortez, Director of Policy for the Sound Money Defense League, fought on the front lines to defend the sales tax exemption for metals. He offered these comments:

“Under the dark cloud left by a rare coin shyster who stole tens of millions in Ohio taxpayer dollars a decade ago, the legislature revoked the sales tax exemption for gold and silver. We’re disappointed in this setback at the hands of tax-hungry politicians. But any tax revenues Ohio may gain will almost certainly be offset by revenues lost, as some business and coin conventions could flee the state. We hope to persuade Ohio’s legislature to fix this policy error in the future.”

The “dark cloud” Cortez referenced is a scandal dubbed “Coingate.” The memory of that debacle unfortunately still remains fresh in Ohio legislators’ minds.

The state had awarded a contract to Tom Noe, a rare coin dealer, to invest $50 million on behalf of the Ohio’s Workers’ Compensation fund starting in 1998.

Noe, and his associates, spent a few years misappropriating funds and making dubious investments in “nickels, dimes and pennies.” Several years later the scheme began to unravel. Noe ultimately pled guilty to “theft, money laundering, forgery, and corrupt activity” in 2006.

It’s worth noting that some of this shady activity is familiar, given the number of reports we’ve had from clients who have been victimized by other “rare” coin dealers over the years, particularly, the boiler-room operations that advertise with their celebrity spokesmen on TV.

The Wikipedia article on Coingate references two coins purchased for $185,000 in 2003. The first coin was a $3 gold piece dated 1855 and the second was a $10 gold coin with an 1845 date. The highest priced example we could find for the first coin was sold in 2009 for a little over $40,000. The second coin appears to have a much lower value.

Evidently state funds were used to purchase rare coins for at least three times what they were worth. Gross overpricing is the most common tactic in the rare coin business, especially when it comes to the high-pressure phone sales operations.

However, that probably isn’t the only cheat involved. The values mentioned above are for coins with an established grade at the highest end of the spectrum. The actual grade of the coins purchased with Ohio money may not even be known. Some coins were sent for grading and apparently went missing in the mail before arriving back.

What we do know is that no one who knows what they are doing would pay record prices for numismatic coins without a grade from one of the trusted grading services. And misrepresenting the grade of a coin is perhaps the second most common scam in the trade.

Ohio politicians made a big mistake when they got tangled up with a rare coin dealer. Unfortunately, that wasn’t the end of the story.

Current legislators do not understand the mistake wasn’t investing in precious metals, per se. It was allowing that investment to be diverted into dubious “collectible” items.

The dark cloud generated by that fraud now obscures the fact that physical gold and silver was an excellent investment in 1998.

Had officials steered clear of collectible coins and instead purchased bullion, the returns for Ohio would have been great. Metals have vastly outperformed stocks since that time period, for example.

Instead, Ohio taxpayers lost most of that $50 million invested nearly two decades ago, and last week they lost the ability to buy gold and silver without paying sales tax.

The Money Metals News Service provides market news and crisp commentary for investors following the precious metals markets.

This week – July 22 through July 27 – central banks from 14 countries or jurisdictions are scheduled to decide on monetary policy: Paraguay, Hungary, Nigeria, Georgia, Kenya, Fiji, Turkey, Tajikistan, euro area, Russia, Azerbaijan, Angola, Colombia and the Eastern Caribbean.

The central banks of Ghana and Uzbekistan had been scheduled to release their policy decisions today, July 22, but announced the decisions to maintain rates last week.

Following table includes the name of the country, the date of the next policy decision, the current policy rate, the result of the last policy decision, the change in the policy rate year to date, and the rate one year ago.

The table is updated when the latest decisions are announced and can always accessed by clicking on This Week.