The US dollar is consolidating against a basket of major currencies. The US dollar index (#DX) closed the trading session in the negative zone (-0.47%). The US currency is under pressure due to yet another decrease in the 10-year US government bonds yield. The inversion of the US government bond yield curve has strengthened concern over the recession again.

Positive economic data released yesterday supported the US dollar. Thus, the CB consumer confidence index counted to 135.1 in August, although experts expected 129.5.

Investors are still concerned about tense trade relations between the US and China. It should be recalled that Donald Trump said that representatives of China called Washington several times intending to continue trade negotiations. However, the editor of the Global Times, Hu Xijin, said that the calls were just a technical formality and did not carry the significance attached to them by the US President.

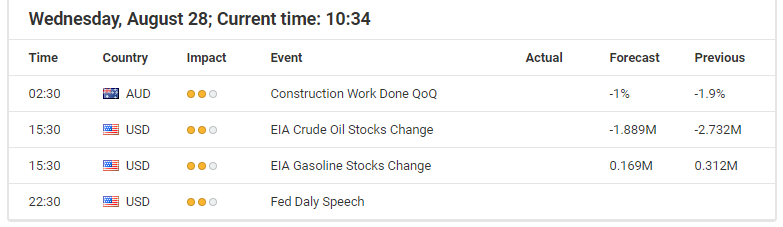

The “black gold” prices are rising. Currently, futures for the WTI crude oil are testing the $55.75 mark per barrel. At 17:30 (GMT+3:00), the US crude oil inventories will be published.

Market Indicators

Yesterday, the bullish sentiment was observed in the US stock markets: #SPY (-0.39%), #DIA (-0.50%), #QQQ (-0.21%).

The 10-year US government bonds yield has updated local lows again. At the moment, the indicator is at the level of 1.47-1.48%.

The News Feed on 2019.08.28:

Today, the publication of important economic news is not expected. Investors expect signals regarding the escalation of the trade war between the US and China.

While the economic calendar is thin today, the latest political developments have us instead looking at Gold, especially in regards to the trade war between the US and China.

In general, the picture in Gold stays clearly bullish after the continued escalation of the trade dispute last Friday. After the retaliation of China which was answered by Trump after markets closed on Friday, announcing new tariffs on Chinese goods and the growing expectation of an outright currency market intervention announced to devalue the US dollar are clearly risk-off-drivers and thus bullish for Gold.

And while Trump tried to take the heat out of the trade dispute at the G7 meeting, saying that China called over the weekend, beginning an attempt to get at a table with the US again which was not confirmed by the Chinese, one thing became nevertheless certain: uncertainty in financial markets remains high.

That said, the long-side in Gold should be favoured and the dip in the precious metal, closing the gap over the weekend around 1,525/530 USD can be considered an interesting region for long engagements in Gold.

In general, the mode stays short-term bullish (Hourly chart) above 1,492 USD, a little longer-term (Daily chart) above 1,380 USD with an overall potential target around 1,650/700 USD in the weeks to come:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between May 29, 2018, to August 27, 2019). Accessed: August 27, 2019, at 10:00pm GMT – Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2014, the value of Gold fell by 1.7%, in 2015, it fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, meaning that after five years, it was up by 6.4%.

Discover the world’s #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter “Analysis”) published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter “Author”) based on the Author’s personal estimations.

To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

Prime Minister Boris Johnson is inflicting unnecessary economic damage on an already vulnerable UK economy, warns the CEO of the world’s largest independent financial advisory organization.

The warning from Nigel Green, chief executive and founder of deVere Group, comes as it is revealed that the government is to ask the Queen to suspend Parliament when lawmakers return to work next week. This means that they are unlikely to have time to stop the Prime Minister taking the UK out of the EU without a deal on October 31.

Mr Green comments: “It could be argued that Boris Johnson’s decision to ask the Queen to suspend parliament, and therefore to prevent democratically elected representatives of the people doing their job, is deeply unconstitutional and has the hallmarks of a tin-pot dictator.

“However, it could also be argued that it is Mr Johnson fulfilling, one way or another, the will of the British people who voted to leave the EU in the 2016 referendum.

“It is likely to be a tactic to spook negotiators into making concessions to the Withdrawal Agreement. Whether it will work remains to be seen. It will almost certainly be challenged in the courts.”

He continues: “What we do know for sure though is that this step will inflict further unnecessary economic damage on an already extremely vulnerable UK economy.

“Depressingly, a recession is looming for Britain and Johnson’s highly controversial tactics seriously increase the uncertainty which will further drag on investment and trade.

“In addition, it will further batter the beleaguered pound, which reduces people’s purchasing power. Weaker sterling means imports are more expensive, with rising prices typically being passed on to consumers.”

Mr Green goes on to add: “The situation in the UK is deteriorating. As such individuals and businesses will, inevitably and quite sensibly, be looking to grow and safeguard their wealth by moving assets out of the UK through various established international financial solutions.

“Brexit has plunged Britain into an existential crisis that will last for generations.

“It has also already cost billions upon billions of pounds. Indeed, it has cost the UK economy a staggering £66bn in just under three years, according to S&P Global Ratings.

“But perhaps even worse is the haemorrhaging of opportunity and confidence in the UK that will continue far beyond the Halloween deadline.”

The deVere CEO concludes: “Boris Johnson’s decision to suspend parliament will have far-reaching economic effects, many of which will not be known for years to come.

“Domestic and international investors in UK assets need to watch the situation carefully and ensure that their portfolios are best-positioned to deal with the growing uncertainties.”

About:

deVere Group is one of the world’s largest independent advisors of specialist global financial solutions to international, local mass affluent, and high-net-worth clients. It has a network of more than 70 offices across the world, over 80,000 clients and $12bn under advisement.

The Pound fell by over one percent before paring losses, with GBPUSD sinking to sub-1.22 levels while EURGBP rising above 0.91, following news that the UK government is seeking to suspend Parliament from the week of September 9 until mid-October, which would be alarmingly close to the October 31 Brexit deadline. Such an event would curtail attempts to block a no-deal Brexit within the UK parliament, which is set to reconvene next week.

The pace of Sterling’s drop demonstrates yet again the currency’s susceptibility to Brexit fears, and that there’s little conviction to ensure that the Pound remains elevated. The jovialities at the G7 summit have given way to the harsh realities of the UK political arena, as markets are reminded yet again that the threat of a no-deal Brexit remains alive and well. With just over two months to go before the Brexit deadline, noting UK Prime Minister Boris Johnson’s willingness to leave the European Union without a deal should it come to that, the Pound is expected to remain highly sensitive to Brexit fears in the interim, while maintaining an easier path to the downside.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

On Tuesday the 27th of August, trading on the euro closed slightly down. Initial growth was snuffed out by the trend line at 1.1116. In the US session, the EURUSD pair slid to the 67th degree at 1.1085.

The single currency came under pressure via the EURGBP pair, which dropped from 0.9095 to 0.9016 on the back of a rising pound. Leader of the UK’s opposition Labour Party Jeremy Corbyn has said the he will do everything he can to prevent the UK leaving the EU without a deal. The opposition parties have made a pact to use any legal means necessary to prevent a no-deal Brexit on the 31st of October.

The pound was the only major to make gains against the dollar. Most currencies have lost ground against the dollar amid a retreat towards the safe havens by investors, who are skeptical of Donald Trump’s optimistic suggestion that a trade deal could be reached by September. Trump said on Monday that he received a call from China asking him to return to the negotiating table. China’s foreign ministry has denied making any such calls.

At the time of writing, the euro is trading at 1.1089. As predicted yesterday, the pair reached the 67th degree, but the ensuing rebound was weak due to the EURGBP pair putting pressure on the bulls. All the majors are trading down against the greenback in today’s Asian session. The euro has lost the least ground at -0.01%. Despite the drop on the majors, it seems likely that the euro will rise against the dollar today.

Asian equities are mixed as markets await the next event that will sway risk sentiment. The Dollar is stronger against all of its G10 peers, while Asian currencies are experiencing contrasting fortunes against the Greenback.

The relative lull in the markets now belies investors’ anxiousness who are fretting over global downside risks. The gains in safe haven assets only speak to the rising fears in the markets which have prompted a clear pivot towards risk aversion. Investors cannot rule out another spike in US-China trade tensions coming out of the blue in the near-term, which ensures that markets will remain trepidatious for the time being.

Pound moderates as markets remain cognisant of potential political landmines in Brexit’s path

The Pound briefly breached 1.23 against the US Dollar before moderating, amid flickering hopes that a no-deal Brexit can be averted, given news that the Labour Party is making an attempt to stop a no-deal Brexit. Markets are well aware of the political hurdles that could manifest as early as next week when Parliament reconvenes, which is limiting the immediate upside for Sterling.

With the current Brexit deadline just some two months away, the clock is ticking on the UK and the EU to avert this worst-case scenario, provided there’s enough political will to do so. Despite the jovialities on display at the recent G7 summit, UK Prime Minister Boris Johnson may still stick to his hardline stance and trigger the much-dreaded no-deal Brexit by October 31. Such an event risk ensures that potential gains for the Pound remain capped, until the path forward for Brexit gets some much-needed clarity.

Dollar traders await US Q2 GDP for near-term moves

The Dollar index didn’t need long to make its way back above the psychologically-important 98 level. Investors are once again paring back expectations over the number of Fed rate cuts for the rest of 2019. Fed funds futures now point to back-to-back 25-basis points cuts over the next two meetings, with the FOMC expected to stand pat in December.

The second reading of the US Q2 GDP due Thursday could prompt gyrations in the Greenback, depending on how far the figures deviate from the 2.1 percent print that markets currently expect. A better-than-expected GDP print could hearten Dollar bulls, as they take comfort in the resilience of the US economy. Should investors get the sense that the Fed will have to incur larger “insurance” rate cuts, perhaps due to a steeper slowdown in the US economy or rising downside risks, that should translate into another soft patch for the Dollar.

Disclaimer: The content in this article comprises personal opinions and should not be construed as containing personal and/or other investment advice and/or an offer of and/or solicitation for any transactions in financial instruments and/or a guarantee and/or prediction of future performance. ForexTime (FXTM), its affiliates, agents, directors, officers or employees do not guarantee the accuracy, validity, timeliness or completeness, of any information or data made available and assume no liability as to any loss arising from any investment based on the same.

Following a rather volatile start to the week, the US dollar traded flat on Tuesday. Economic data remains sparse. The US Richmond manufacturing index rose to 1 from -12 previously. This was slightly better than the forecasts.

However, the regional manufacturing index signals a larger slowdown in the sector. Meanwhile, the Conference Board’s consumer confidence report showed that the index fell slightly to 135.1 from 135.8 previously.

ECB VP Says Policy Not Market Dependent

ECB Vice President Guindos said on Tuesday that the monetary policy of the ECB will be focusing on the economy and not the markets. His comments come ahead of the September 12 ECB meeting. The central bank has all but signaled its intentions to relaunch its QE program including possible rate cuts as well. The euro was however muted to comments while maintaining a downside bias.

EURUSD Retests the Descending Wedge Breakout Level

The common currency quickly erased the gains made over the past few days. Price action is back, hovering near the descending wedge breakout level of 1.1098. If the EURUSD loses this handle, we expect to see further declines along the way. The next downside target is in the 1.1030 region.

Pound Maintains Bullish Bias

The British pound maintained the bullish bias on Tuesday. This comes amid EU President Jean-Claude Juncker’s comments. Juncker said that the no-deal Brexit scenario was entirely up to the UK. The negotiations on Brexit continue to remain in a deadline as the October 31st deadline looms closer.

GBPUSD Likely to Correct to Lower Support

Cable is likely to see some near-term correction. This comes as the support area of 1.2170 remains untested. For further upside gains, the GBPUSD needs to establish support to maintain the bullish bias. The 4-hour chart shows a bearish divergence forming, with the Stochastics forming a lower high, while there is a hidden bearish divergence on the daily chart time frame.

Gold Advances Gains Amid a Quiet Session

Gold prices rose sharply once again on the day on Tuesday. The gains come as China’s Premier said that he was not aware of any calls made to Trump. President Trump claimed that China wanted to get back to negotiating the trade deal. The confusion kept the market sentiment in check.

Is Gold on the Verge of Forming a Top?

The recent gains in the precious metal are showing signs of exhausting momentum. Gold prices have rebounded in the short term. But unless we see a strong breakout, it is unlikely that the precious metal will have further room to run. The Stochastics oscillator is currently signaling a possible easing of the momentum. The initial support at 1508 will be key to the downside.

US stock indexes pulled back on Tuesday as Treasury yield curve inversion deepened with 30-year yields slipping below those on three-month notes. The S&P 500 slid 0.3% to 2869.16. Dow Jones industrial lost 0.5% to 25777.90. The Nasdaq retreated 0.3% to 7826.95. The dollar strengthening halted as the Case-Shiller home price index growth slowed to 2.1% in June from a 2.4% gain the previous month: the live dollar index data show the ICE US Dollar index, a measure of the dollar’s strength against a basket of six rival currencies, lost 0.04% to 98.00 but is higher currently. Stock index futures point to lower market openings today.

CAC 40 leads European indexes gains

European stocks recovery continued on Tuesday as China’s State Council issued 20 directives to boost consumption by providing credit support for purchases of new energy vehicles and smart home appliances. The GBP/USD turned higher yesterday while EUR/USD continued sliding with both pairs lower currently. The Stoxx Europe 600 ended 0.5% higher. The German DAX 30 gained 0.6% to 11730.02 despite final GDP reading confirmed Europe’s largest economy contracted 0.1% in second quarter. France’s CAC 40 rose 0.7% after president Macron said on Monday US and France reached a deal on digital tax. UK’s FTSE 100 slipped 0.1% to 7089.58.

Australia’s All Ordinaries Index leads Asian indexes gains

Asian stock indices are mixed today. Nikkei gained 0.1% to 20479.42 as yen resumed its slide against the dollar. Chinese stocks are retreating: the Shanghai Composite Index is down 0.3% and Hong Kong’s Hang Seng index is 0.1% lower. Australia’s All Ordinaries Index extended gains 0.4% as Australian dollar’s move lower against the greenback continued.

Brent futures prices are steady today. The American Petroleum Institute late Tuesday report indicated US crude inventories fell by 11.1 million barrels last week. Prices rose yesterday: October Brent gained 1.4% to $59.51 a barrel on Tuesday. Today at 16:30 CET the Energy Information Administration will release US Crude Oil Inventories.

Note: This overview has an informative and tutorial character and is published for free. All the data, included in the overview, are received from public sources, recognized as more or less reliable. Moreover, there is no guarantee that the indicated information is full and precise. Overviews are not updated. The whole information in each overview, including opinion, indicators, charts and anything else, is provided only for familiarization purposes and is not financial advice or а recommendation. The whole text and its any part, as well as the charts cannot be considered as an offer to make a deal with any asset. IFC Markets and its employees under any circumstances are not liable for any action taken by someone else during or after reading the overview.

Sector expert and money manager Adrian Day discusses resource firms that he covers, including two major producers, one royalty company and one exploration company.

Newmont Goldcorp Corp. (NEM:NYSE, $39.30) has underperformed this year, largely due to concerns surrounding the acquisition of Goldcorp, which closed in April. Many Newmont shareholders believe the company overpaid for bad assets. Not all Goldcorp’s assets are “bad,” of course, and Newmont’s strong operational history should see some of these underperforming assets turn around. In addition, the recent pact with Barrick Gold Corp. (ABX:TSX; GOLD:NYSE) on the two companys’ Nevada assets should see synergies and lower costs over time.

Lastly, Newmont can now be flexible in disposing of some non-core assets, as it promised during the takeover of Goldcorp. The asset review process is still underway. Proceeds will reduce debt taken on to buy Goldcorp, as well as sharpen the company’s focus and improve synergies. We are holding.

Is this time for real?

Yamana Gold Inc. (YRI:TSX; AUY:NYSE; YAU:LSE, US$3.62) continues to struggle with a weak balance sheet. Earlier this year, it sold one of best assets, Chapada, to help pay down debt. The company has negative working capital, negative returns and profitability. Despite its high debt load, it increased its dividend and announced a stock buyback, actions intended as a sign that the company’s financial issues were behind it, but most investors would have rather seen further reductions in debt. Operationally it is moving in the right direction, and the new Aqua Rica could add to NAV (net asset value) and to cash flow.

But Yamana has disappointed so many times in the past. Right now, its cash flow goes completely on G&A (general and administrative expenses) and debt service. We think the second half could see improved revenues and a high stock price if gold remains strong. Given the stock is at its highest since January 2018 and has not been much higher for three years, we are holding.

Positioned for changed market

Altius Minerals Corp. (ALS:TSX.V, CA$11.17) has had to contend with weak copper and other base metals prices. Even potash, which had offset the general weakness in the resource sector, now looks set for weaker prices as Chinese demand is affected by U.S. tariffs. The stock is close to the low for the year, and the company has renewed its stock buyback program given the strong balance sheet, with nearly $24 million cash, net debt of $94 million, plus a portfolio of junior equities valued at almost $54 million as of the end of June, and undoubtedly more today.

Some $7.7 million was raised during the quarter from portfolio sales, which went to cutting debt. Now, a stock buyback seems justified. There is $85 million available on a line of credit. There may be no immediate catalyst, but Altius, with strong, contrarian management, is a buy at these levels.

The good and the bad, no ugly

Evrim Resources Corp. (EVM:TSX.V, CA$0.35) continues to move projects and get work commitments. Earlier this week, drilling commenced at its Ball Creek gold-copper porphyry targets in British Columbia, funded by a new junior partner. Although previous partner Antofagasta Plc (ANTO:LSE) spent over $2 million over the past two years in exploration on Ball Creek and another property, this will be the first drilling on the property since 2012. Evrim has also extended an agreement with another junior on the Cerro Cascaron property, despite somewhat uninspiring results from the first round of drilling.

Offsetting these positive developments, Coeur Mining Inc. (CDE:NYSE) decided to relinquish its option on the Sarape project, after a fairly modest maiden drill program testing for blind mineralization. It would have been somewhat against the odds to find anything attractive in such initial drilling, and the property needs much more drill testing before killing it. But Coeur has its own financial issues at present. Sarape, near Ermitaño, a property discovered by Evrim and later sold to First Majestic Silver Corp. (FR:TSX; AG:NYSE; FMV:FSE), is on track for first production at the end of next year to produce feed for First Majestic’s Santa Elena mine, which is running out of ore. Another company will likely want a shot at Salape.

In other developments, the company’s vice president of exploration, Charles Funk, stepped down, and was replaced by seasoned geologist Dave Groves. Charles was energetic and well respected in the time he had been with the company, but has other fish to fry. Groves brings 35 years of experience, including at Newmont and Centerra Gold Inc. (CG:TSX; CADGF:OTCPK), and has most recently been a consultant for Evrim, so can hit the ground running.

Solid company, very cheap

With a market cap slightly under CA$30 million, Evrim is trading for less than the value of its cash on hand and the royalty it retains on Ermitaño. The rest of the company is free, including several option agreements, regional alliances and 100%-owned projects. The excitement and subsequent disappointment over its Cuale property last year is the main reason the stock is languishing. It is a great buy here, all the more so since it has top management and a rock-solid balance sheet. It is one of the great buys in the sector right now that doesn’t depend on higher gold prices.

Adrian Day, London-born and a graduate of the London School of Economics, heads the money management firm Adrian Day Asset Management, where he manages discretionary accounts in both global and resource areas. Day is also sub-adviser to the EuroPacific Gold Fund (EPGFX). His latest book is “Investing in Resources: How to Profit from the Outsized Potential and Avoid the Risks.”

Disclosure: 1) Adrian Day: I, or members of my immediate household or family, own shares of the following companies mentioned in this article: Altius and Evrim. I personally am, or members of my immediate household or family are, paid by the following companies mentioned in this article: None. My company has a financial relationship with the following companies mentioned in this article: None. Funds controlled by Adrian Day Asset Management hold shares of the following companies mentioned in this article: Newmont Goldcorp, Yamana, Altius and Evrim. I determined which companies would be included in this article based on my research and understanding of the sector. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 3) Statements and opinions expressed are the opinions of the author and not of Streetwise Reports or its officers. The author is wholly responsible for the validity of the statements. The author was not paid by Streetwise Reports for this article. Streetwise Reports was not paid by the author to publish or syndicate this article. Streetwise Reports requires contributing authors to disclose any shareholdings in, or economic relationships with, companies that they write about. Streetwise Reports relies upon the authors to accurately provide this information and Streetwise Reports has no means of verifying its accuracy. 4) This article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases. As of the date of this article, officers and/or employees of Streetwise Reports (including members of their household) own securities of Newmont Goldcorp, Altius and Evrim, companies mentioned in this article.

This morning PDC Energy announced that it will acquire SRC Energy in an all-stock deal valued at $1.7 billion. Shares of both companies are trading higher today on the merger news.

Early this morning before the market open PDC Energy Inc. (PDCE:NASDAQ) and SRC Energy Inc. (SRCI:NYSE.American)announced that they have entered into a definitive merger agreement under which PDC will acquire SRC in an all-stock transaction valued at approximately $1.7 billion, including SRC’s net debt of approximately $685 million as of June 30, 2019. Under the terms of the agreement, SRC shareholders will receive a fixed exchange ratio of 0.158 PDC shares for each share of SRC common stock, representing an implied value of $3.99 per share based on the PDC August 23, 2019, closing price.

Upon closing of the transaction, PDC shareholders will own approximately 62% of the combined company with SRC shareholders owning approximately 38% on a fully diluted basis. The transaction has been unanimously approved by each company’s board of directors and is expected to close in Q4/19 subject to customary closing conditions and the satisfaction of certain regulatory approvals, including the approval of PDC and SRC shareholders.

The report further advised that upon closing the combined company will be led by PDC’s executive management team and will remain headquartered in Denver, Colo. PDCs’ board of directors will be expanded to nine directors including two members from SRC’s board of directors.

The release states that the transaction is expected to be immediately accretive to key 2020 metrics, including: free cash flow per share, cash return on capital invested, net asset value, general & administrative (G&A) costs per barrel of oil equivalent (boe), lease operation expenses per boe, leverage ratio and inventory life.

The company indicated that the merger materially increases PDC’s scale with a consolidated, contiguous Core Wattenberg leasehold position of approximately 182,000 net acres located entirely in Weld County and pro forma Q2/19 total production of nearly 200,000 barrels of oil equivalent (boe) per day (166,000 boe per day in the Wattenberg). On a pro forma basis, the combined company will be the second largest producer in the DJ basin. Coupled with its approximate 36,000 net acre Delaware Basin position, the company will have core assets in two of the premier U.S. onshore basins

PDC also advised that the deal materially enhances free cash flow profile and enhances ability to return additional capital to shareholders. Pro forma free cash flow is estimated to be approximately $800 million from Q3/19 through year-end 2021, assuming $55 per barrel NYMEX. The company has increased and extended its existing share repurchase program from $200 million to $525 million, with a target completion date of year-end 2021.

The firm claims that the deal creates a low-cost mid-cap producer with anticipated peer-leading G&A of approximately $2.00 per boe in 2020 and that the company expects to realize approximately $40 million of G&A savings in 2020 with an additional $10 million of G&A synergies in 2021, after the completion of its integration plan.

President and CEO of PDC Energy Bart Brookman commented, “SRC’s complementary, high-quality assets in the Core Wattenberg, coupled with our existing inventory and track record of operational excellence will create a best-in-class operator with the size, scale and financial positioning to thrive in today’s market…We remain committed to our core Delaware Basin acreage position and are confident the combined company with its multi-basin focus will be well-positioned to deliver superior shareholder returns. With an even more competitive cost structure, including peer-leading G&A and LOE per Boe, the combined company will have the financial flexibility and sustainable free cash flow to return significant capital to shareholders and capitalize on additional growth opportunities…We look forward to working with SRC to integrate these two companies and achieve our shared objectives.”

Lynn A. Peterson, CEO and chairman of SRC Energy added, “I am proud of the SRC team and the high-quality acreage and low-cost operations we have built together. We believe that this transaction will establish the combined company as a leader in the Colorado energy industry. The transaction also provides SRC shareholders with the opportunity to participate in the significant upside potential created by a larger-scale DJ Basin producer with complementary assets in the prolific Delaware Basin”.

PDC also advised that in 2020 it plans to invest between $1.2 and $1.4 billion to operate three Wattenberg and two Delaware Basin drilling rigs. The plan is expected to generate approximately $275 million in free cash flow assuming $55 per barrel and $2.70 per Mcf NYMEX oil and gas prices, respectively, with full-year production averaging between 200,000 and 220,000 boe per day.

PDC Energy has a market cap of approximately $1.6 billion and lists its business as a domestic independent exploration and production company that acquires, produces, develops and explores for crude oil, natural gas and NGLs with operations in the Wattenberg Field in Colorado and the Delaware Basin in West Texas. Its operations are focused on the liquid-rich horizontal Niobrara and Codell plays in the Wattenberg Field and the liquid-rich Wolfcamp zones in the Delaware Basin.

SRC Energy has around a $1 billion market cap and identifies its business as a Denver-based oil and natural gas exploration and production company. SRC’s core area of operations is in the Greater Wattenberg Field of the Denver-Julesburg Basin of Colorado.

PDCE shares opened higher today at $26.70 (+$1.45, +5.74%) over Friday’s close of $25.25 and have traded higher this morning between $26.70 and $30.93/share. At present, the firm’s shares are trading at $28.97 (+$3.72, +14.73%).

SRCI shares opened only slightly higher today at $4.22 (+$0.07, +1.69%). Throughout the morning shares have traded higher though, between $4.19 and $4.89/share and currently are trading at $4.57 (+$0.42, +10.12%).

Disclosure: 1) Stephen Hytha compiled this article for Streetwise Reports LLC and provides services to Streetwise Reports as an independent contractor. He or members of his household own securities of the following companies mentioned in the article: None. He or members of his household are paid by the following companies mentioned in this article: None. 2) The following companies mentioned in this article are billboard sponsors of Streetwise Reports: None. Click here for important disclosures about sponsor fees. 3) Comments and opinions expressed are those of the specific experts and not of Streetwise Reports or its officers. The information provided above is for informational purposes only and is not a recommendation to buy or sell any security. 4) The article does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer. This article is not a solicitation for investment. Streetwise Reports does not render general or specific investment advice and the information on Streetwise Reports should not be considered a recommendation to buy or sell any security. Streetwise Reports does not endorse or recommend the business, products, services or securities of any company mentioned on Streetwise Reports. 5) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their immediate families are prohibited from making purchases and/or sales of those securities in the open market or otherwise from the time of the interview or the decision to write an article until three business days after the publication of the interview or article. The foregoing prohibition does not apply to articles that in substance only restate previously published company releases.